Image: Gary Gensler on Bloomberg TV, July 27, 2023

SEC Chairman Pushes for More Crypto Cops on the Beat

Gary Gensler, the SEC chair, was asked on Bloomberg TV whether the efforts to protect the consumer related to cryptocurrency are complicated by non-compliance and lack of growth in the agency’s staff. Gensler discussed the need for more enforcement of current laws and lively debate with Congress to create new rules, “the capital markets really wouldn’t work without cops on the beat and rules of the road,” replied the SEC chair.

During his discussion on July 27, the head of the SEC demonstrated the Commission is still taking aim at the crypto markets despite what is seen as legal setbacks related to its authority. Gensler said that the cryptocurrency sector remains underhanded and unregulated. “The securities laws are there to protect you, and this is a field rife with fraud, rife with hucksters. There are good-faith actors as well, but there are far too many that aren’t.”

The overall theme of the conversation is that the crypto asset class lacks adequate protections for investors.

Gensler calmly appealed to investors not to assume that they are getting full protection despite the securities laws applied to many tokens in the crypto space. “A lot of investors should be aware that it’s not only a highly speculative asset class, it’s also one that they currently should not assume they are getting the protections of the securities law,” he said. He alleged that some crypto platforms were “co-mingling and trading against” investors.

As it relates to crypto exchanges and how they operate, the SEC chair said crypto violates laws that other exchanges abide by. “You as investors are not getting the full, fair, and truthful disclosure, and the platforms and intermediaries are doing things that we would never in a day allow or think the New York Stock Exchange or NASDAQ would do,” declared Gensler.

Earlier this month, a U.S. judge ruled that Ripple did not break securities law by selling its XRP token on public exchanges. The decision sent positive ripples through the entire crypto market and sent the value of XRP soaring. If tokens can not be deemed securities, transactions within the asset class may not fall under the SEC at all. This leaves open the question of who will regulate and oversee crypto and its exchanges.

Take Away

SEC chair Gary Gensler warned investors in late July about the lack of regulation for cryptocurrencies. He told Bloomberg TV the sector was rife with “fraud” and “hucksters,” leaving investors at risk. Gensler made listeners aware that some crypto platforms were “co-mingling and trading against” investors.

It is likely that there will ultimately be regulation handed down from Congress and enforced by an agency, which may include self-regulation, but after the Ripple decision, the oversight will not automatically be from the SEC. It appears Gary Gensler has taken to the interview circuit in order to sway opinion in favor of the SEC.

Fragile X Syndrome Often Results from Improperly Processed Genetic Material – Correctly Cutting RNA Offers a Potential Treatment

Fragile X syndrome is a genetic disorder caused by a mutation in a gene that lies at the tip of the X chromosome. It is linked to autism spectrum disorders. People with fragile X experience a range of symptoms that include cognitive impairment, developmental and speech delays and hyperactivity. They may also have some physical features such as large ears and foreheads, flabby muscles and poor coordination.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Joel Richter, Professor of Neuroscience, UMass Chan Medical School and Sneha Shah, Assistant Professor of Molecular Medicine. UMass Chan Medical School

Along with our colleagues Jonathan Watts and Elizabeth Berry-Kravis, we are a team of scientists with expertise in molecular biology, nucleic acid chemistry and pediatric neurology. We recently discovered that the mutated gene responsible for fragile X syndrome is active in most people with the disorder, not silenced as previously thought. But the affected gene on the X chromosome is still unable to produce the protein it codes for because the genetic material isn’t properly processed. Correcting this processing error suggests that a potential treatment for symptoms of fragile X may one day be available.

Repairing Faulty RNA Splicing

The FMR1 gene encodes a protein that regulates protein synthesis. A lack of this protein leads to overall excessive protein synthesis in the brain that results in many of the symptoms of fragile X.

The mutation that causes fragile X results in extra copies of a DNA sequence called a CGG repeat. Everyone has CGG repeats in their FMR1 gene, but typically fewer than 55 copies. Having 200 or more CGG repeats silences the FMR1 gene and results in fragile X syndrome. However, we found that around 70% of people with fragile X still have an active FMR1 gene their cellular machinery can read. But it is mutated enough that it is unable to direct the cell to produce the protein it encodes.

Genes are transcribed into another form of genetic material called RNA that cells use to make proteins. Normally, genes are processed before transcription in order to make a readable strand of RNA. This involves removing the noncoding sequences that interrupt genes and splicing the genetic material back together. For people with fragile X, the cellular machinery that does this cutting incorrectly splices the genetic material, such that the protein the FMR1 gene codes for is not produced.

Fragile X syndrome is the most common inherited form of intellectual disability.

Using cell cultures in the lab, we found that correcting this missplice can restore proper RNA function and produce the FMR1 gene’s protein. We did this by using short bits of DNA called antisense oligonucleotides, or ASOs. When these bits of genetic material bind to RNA molecules, they change the way the cell can read it. That can have effects on which proteins the cell can successfully produce.

ASOs have been used with spectacular success to treat other childhood disorders, such as spinal muscular atrophy, and are now being used to treat a variety of neurological diseases.

Beyond Mice Models

Notably, fragile X syndrome is most often studied using mouse models. However, because these mice have been genetically engineered to lack a functional FMR1 gene, they are quite different from people with fragile X. In people, it is not a missing gene that causes fragile X but mutations that lead the existing gene to lose function.

Because the mouse model of fragile X lacks the FMR1 gene, the RNA is not made and so cannot be misspliced. Our discovery would not have been possible if we used mice.

With further research, future studies in people may one day include injecting ASOs into the cerebrospinal fluid of fragile X patients, where it will travel to the brain and hopefully restore proper function of the FMR1 gene and improve their cognitive function.

Investors Especially Hate Companies that Say They’re Good Then Behave Badly – Unless the Money is Good

The Big Idea

Stock investors punish companies caught doing something unethical a lot more when these businesses also have a record of portraying themselves as virtuous. This hypocrisy penalty is the main finding of a study we recently published in the Journal of Management.

Companies often espouse their supposed virtue – known as “virtue signaling” – usually with the aim of getting benefits, such as higher sales, positive investor sentiment or better employees. We wanted to know what happens when such companies then do something wrong.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Brian L. Connelly, Professor of Management and Entrepreneurship, Auburn University, Lori Trudell, Assistant Professor of Entrepreneurship, Clemson University.

So we examined corporate communications and media coverage for every company in the Standard & Poor’s 500 to develop a comprehensive database of both virtue signaling and misconduct.

To gauge virtue signaling, we conducted linguistic analysis of each company’s letters to shareholders. This is a form of computer-aided text analysis that identifies and categorizes language to draw inferences. For example, we looked for words and patterns to identify conscientiousness, empathy and integrity and considered how language patterns developed over time. Each company received a score that reflected how much of their corporate communication was devoted to virtue rhetoric.

We then examined over half a million news articles to identify unethical behavior, such as egregious events like a CEO’s being fired for sexual misconduct, but also less severe transgressions, like not treating employees fairly.

Finally, our study considered how shareholders respond. Specifically, we looked at price swings the day after the media initially reported the misbehavior.

We found that share prices fell 1.5% overnight in response to unethical behavior when companies had engaged in lots of virtue signaling, compared with 0.4% for those that did less virtue signaling or none at all. For an average company, that difference amounts to over half a billion dollars in lost value.

Keep in mind, too, that these ethical violations are not uncommon events. About a quarter of companies in our sample engaged in this kind of behavior in any given year. Stated simply, bad things happen, and when they do the stock market will clobber those who do not seem to be walking their talk.

Well, with one critical exception related to a company’s expected future performance. If investors anticipate that a company will perform well in the future, there is no hypocrisy penalty – the consequences of misconduct are the same for those that use virtue signaling and those that do not.

Apparently, shareholders are very concerned about executives who say one thing and do another – unless the company is expected to make lots of money, in which case there is little or no penalty for unethical behavior.

Why it Matters

Many companies, and the CEOs who run them, publicly say they care a lot about their people, the environment and the communities around them, among other virtuous signals.

For example, ice cream maker Ben & Jerry’s proudly declares that it seeks to “advance human rights and dignity, support social and economic justice for historically marginalized communities, and protect and restore the Earth’s natural systems.” At the other end of the political spectrum, restaurant chain Chick-fil-A proclaims that it is “about more than just selling chicken”; its corporate purpose: “To glorify God by being a faithful steward of all that is entrusted to us.”

Whether from the right or the left, this virtue signaling establishes, and implicitly promises adherence to, a set of ethical standards. What happens, though, when behavior does not align with virtuous talk?

Academics have two decidedly different views about how to answer this question. Some contend that virtue signaling buffers companies from the negative ramifications of misconduct. Another perspective suggests that there’s a more severe adverse reaction whenever anyone deviates from expectations. Think, for example, of the special vehemence reserved for the priest who pilfers from the church coffers.

Our study confirms that the latter – a hypocrisy penalty – is more likely what is happening.

What’s Next

We are now exploring different types of shareholders and how they respond to organizational behavior – and misbehavior. For example, social activist funds could be especially put off when companies in which they invest behave badly, whereas the most powerful institutional investors are less likely to be concerned about a mismatch between a company’s words and deeds.

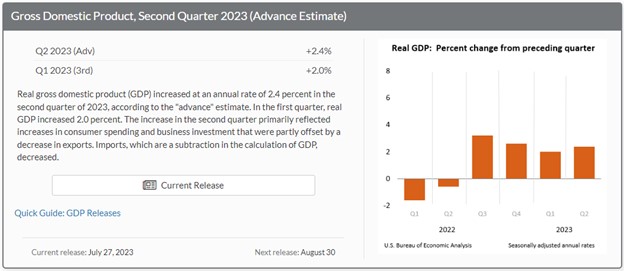

The Surprisingly High Economic Growth Numbers Aren’t Spooking Investors

Gross Domestic Product, or GDP, is one of the best measures of U.S. economic health. The second quarter GDP report as well as the first quarter upward revision, fully support the idea that the economy is growing above expectations and that the Fed’s rate hike in July was justified. This places equity investors in the position they have become very familiar with, wondering if they should be bullish on stocks as the economy rolls on, or should they be bearish as the Fed’s reaction could cause a period of negative growth (recession). Seeing how the Dow is on a winning streak of a dozen days in a row, even as the Fed resumed tightening, it may be that the forward-looking stock market has turned the corner and is now taking good news as good news, and bad news as bad, once again.

Source: Bureau of Economic Analysis (BEA)

GDP was much stronger than expected – economists surveyed by FactSet were expecting a 1.5% gain. This was the first data release since the July FOMC meeting; it will however be followed on Friday by two other key indicators. The U.S. economy grew at a 2.4% annual rate in the second quarter (first estimate of GDP). This is significantly better than economists’ projections and makes abundantly clear that through last quarter, the economy was far from contracting or recessionary.

Contributors to the better-than-expected growth are increases in consumer spending, nonresidential fixed investment, state and local government spending, private inventory investment, and federal government spending, according to the BEA. Non-manufacturing contributors (services) included housing and utilities, health care, financial services and insurance, and transportation services. The contribution to goods spending was led by recreational goods and vehicles as well as gasoline and other energy goods.

Other Market-Moving Releases

The GDP report was the first piece of economic data following the Federal Reserve’s meeting on Tuesday and Wednesday; this concluded with a quarter-point increase in the central bank’s target for the fed-funds rate. That now leaves the Fed’s benchmark rate at a range of 5.25% to 5.5%.

Jobs and the tight employment market, where there are currently more jobs available than workers looking for employment, should still be a big focus of monetary policymakers. On Friday July 28, the employment cost index (ECI) is expected to show that the hourly labor cost to employers in the second quarter grew at a 4.8% annual rate, and by 1.1% quarter to quarter, according to the consensus estimate by FactSet. That’s little changed from the first quarter, when compensation costs for civilian workers increased by 4.8% annually and at a 1.2% rate quarter over quarter, according to the Bureau of Labor Statistics. Labor tightness and wage inflation are both concerning for the Fed and provide evidence that a more restrictive policy is needed.

Investors should look for ECI to provide some insight into how sticky service inflation is right now. This is of high importance because, within the service sector, wages tend to be the highest input cost. If the number comes in higher than expected, that could be a worrisome sign of continued stubborn inflation, which then indicates the need for additional rate hikes.

At the same time the ECI report is released on Friday, the PCE data is released. While the market’s tendency over the months has been to hyperfocus on the “Fed’s favorite inflation measure,” PCE may take a back seat in terms of significance to ECI data.

Take Away

Inflation rates coming down while the economy grows is, if inflation declines enough, a soft economic landing. The stock market, which had been reacting negatively to strong economic news, is beginning to show signs that it expects a soft landing – while this lasts, the markets could continue their winning streak.

“We’re Not Finished Yet” According to the FOMC Post Meeting Statement

The Federal Open Market Committee (FOMC) voted to raise its target rate on overnight interest rates from 5.00% – 5.25% to 5.25%-5.50% after the July 2023 meeting. This 25 bp move follows a pause in rate hikes decided during the June meeting. The Fed still maintains a hawkish stance after raising the Fed Funds rate to its highest level in 22 years and leaving quantitative tightening (QT) targets unchanged.

The implementation note following the meeting spells out QT implementation to reduce the Fed’s balance sheet as:

“Roll over at auction the amount of principal payments from the Federal Reserve’s holdings of Treasury securities maturing in each calendar month that exceeds a cap of $60 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.”

“Reinvest into agency mortgage-backed securities (MBS) the amount of principal payments from the Federal Reserve’s holdings of agency debt and agency MBS received in each calendar month that exceeds a cap of $35 billion per month.”

QT is an important part of the Federal Reserve Bank reducing the stimulus effect of having injected, through quantitative easing (QE), substantial amounts of money into the U.S. economy.

Words in the statement, particularly those changed from the prior meeting, are placed under the spotlight. In June, the FOMC members felt the U.S. economy was “growing” at a “modest” pace. Now it sees “more growth”—at a “moderate” level. This indicates that they may believe they have a higher need to continue tightening credit conditions.

At the previous meeting a Summary of Economic Projections (SEP) for the Fed Funds Rate indicated the Fed expected two additional 25 bp increases. While no SEP is available after the July meeting, the view the economy has become stronger, would suggest that at a minimum, another 25 bp is likely.

The FOMC as the monetary policy arm of the Federal Reserve is, as it says, “data dependent” when determining what tightening or other moves may be appropriate in the future.

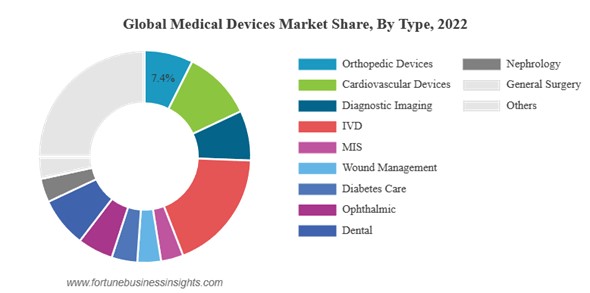

While pharmaceuticals and biotech get much of the attention in the life sciences field, investors in medical device manufacturers got confirmation last week that the high growth projections in sales is on track. Of added interest to those invested in smaller companies in the medtech space, large key players are looking to increase market share through mergers and acquisitions (M&A). This was emphasized in Johnson and Johnson’s (JNJ) Q2 reporting released last week.

Consumer health giant Johnson & Johnson said it has a “pretty voracious” appetite for medical device M&A going forward, as it expects further rebounds in surgery volume, post-pandemic, to continue funneling cash into the company for the rest of the 2023. Projections for the global medical device market size, according to Fortune Business Insights, was valued at $512.29 billion in 2022 & is projected to grow from $536.12 billion in 2023 to $799.67 billion by 2030.

Even after the demand from patients who put off procedures, while labor shortages in hospitals became less of a problem, device sales that are helping fulfill delayed procedures have a much brighter future even after the pandemic-related surge in needs.

Driving demand is an aging and sedentary population, with a growing prevalence of chronic disorders like diabetes, cancer, heart disease, etc. There is also an increased demand for ophthalmic and orthopedic procedures as the population experiences more joint fractures and debilitating vision issues.

Source: Fortune Business Insights

Johnson and Johnson’s admitted during its quarterly reporting that it will continue actively looking for situations to acquire medtech companies. The company’s medtech businesses produced $7.79 billion in global revenue during the second quarter, totaling 14.7% growth compared to the $6.90 billion brought in during the same three-month period in 2022.

Last year JNJ bought a miniature heart pump maker Abiomed, for $16.6 billion. Business from this acquisition accounted for 4.8%, or nearly a third of the Q2 gains, with $331 million in worldwide revenue for the quarter. JNJ’s acquiring Abiomed was one of the largest medtech deals of 2022; as of the end of the second quarter, it has added $655 million to J&J MedTech’s bottom line since the acquisition was closed last December.

Source: JNJ, July 20, 2023

“Everything is moving well and according to plan in Abiomed’s integration, and we are increasingly convinced that this is going to be a key component in our medtech strategy of becoming a leader in heart recovery,” J&J CEO Joaquin Duato said on the company’s investor call.

“When it comes to M&A, we continue to look for opportunities,” Duato said. “And when it comes to medtech … we look forward to growing in areas that are close to where we are today: vision, cardiovascular, surgery, and also high-growth segments in orthopedics.”

Abiomed wasn’t the only contributor in JNJ’s growing medtech businesses. Much of the growth was driven by a 25.9% year-over-year boost in electrophysiology sales, pushing the segment past the billion-dollar mark. The company also saw increases in trauma orthopedics, wound closure kits and biosurgery products, as well as in contact lenses.

Take Away

Medical device companies are helping to fulfill a need as the population ages and new technology, including AI and robotics, are able to provide new solutions to old problems. The announcement by JNJ that they are hungry for medtech companies that fit their criteria ought to cause life sciences investors to pay even more attention to the space.

Late in 2022 Channelchek asked our Med Device & Services analyst to discuss his “shopping list” in the medical device arena, the video is helpful for investors to discover more about this space.

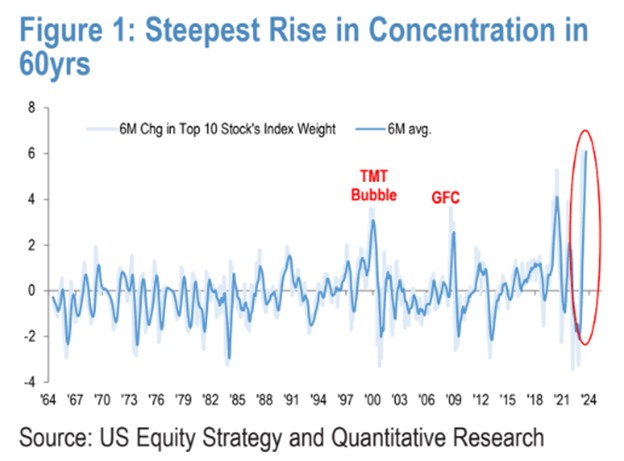

The Warning Signs that the Mega-Cap Era Is Coming to an End are Growing

By Monday of next week, the Nasdaq 100 will be rebalanced to reduce the weighting of its top holdings and add weight to the smaller companies represented. This event can be grouped with the number of experts and outlets waving yellow and red flags warning U.S. stock market investors about the reliance on mega-caps for continued performance. The number of warnings has been increasing. The original purpose of any index is to measure overall market or sector performance. Currently reported performance in the most popular indexes is dependent on five to ten mega-cap names – this trend is not sustainable through time. JP Morgan (JPM) is the most recent firm to warn about an extreme concentration of a few stocks.

JPMorgan Chase & Co.’s equity analysts, led by Chief Global Markets Strategist Marko Kolanovic, warn that overweighting towards very few companies of extremely large-cap stocks could spell trouble ahead. In a research note published on July 24, the firm writes historically, such periods of extreme concentration have often led to negative outcomes. In fact, the current level of concentration is growing at the fastest pace since the 1960s, surpassing even the extremes seen during the infamous dot-com bubble in March 2000.

To illustrate the stark divergence between the largest U.S.-listed companies and the rest of the market, the JPM team compared the six-month change in the index weighting of the ten largest stocks in the S&P 500 with that of the next 40. This analysis revealed that over the past six months, the divergence has widened in favor of the biggest companies, reaching levels comparable to the “Nifty 50” era of the 1960s—a period when large-cap stocks were highly favored by investors.

JPM Chase, July 24, 2023

Crowding in growth stocks represented in the S&P 500 is currently at the 97th percentile historically. This is a level not seen since the dot-com bubble period. While the team provided extensive data and analysis to support their concerns about overconcentration, they were less definitive about the timing or specific implications for the market.

JPM Chase, July 24, 2023

A selloff is expected and appears likely according to JPM; predicting its timing is more challenging. The team pointed out several potential catalysts, such as a deep recession or a sudden resurgence of inflationary pressures, but it remains uncertain when the downturn may begin. Nonetheless, the JPM team believes that the peak in concentration will coincide with waning investor interest in the generative AI/large-language model theme, a trend that has contributed this year to the significant divergence in equity performance.

In light of Monday’s special rebalancing of the Nasdaq-100, the JPMorgan team suggested that this move could potentially mitigate concentration risk by easing the outperformance of mega-cap technology stocks, including Apple Inc., Microsoft Corp., Nvidia Corp., and Alphabet Inc., which have been major beneficiaries of the AI boom. If a larger percentage of dollars entering large-cap funds find their way to the ticker symbols below the giants at the top, the pace at which the markets have become unbalanced may slow or correct without a major problem.

The JPM team pointed out that if correct, speculators may capitalize on this by considering that the S&P 500 equal weight may be in a position to outperform the S&P 500 traditional weight methodology products over the next three to six months.

Interestingly, there are already signs that the overconcentration problem highlighted by JPMorgan are beginning to ease. Over the last month, the S&P 500 equal-weighted index has outperformed its market-cap-weighted counterpart by 2 percentage points, according to FactSet data.

Despite these concerns, the U.S. stock market closed higher on Monday, with the Dow Jones Industrial Average booking its 11th consecutive daily gain, marking its longest winning streak in nearly six years. The performance of the value-heavy Dow, which has been catching up, while the year-to-date rally of mega-cap tech stocks has stalled, highlights the ongoing dynamics in the market.

Take Away

While some market gurus like Michael Burry have been warning of a bubble brought about by index funds, since 2019, the weighting in indexes have only increased. By the last day in July, the Nasdaq 100 will have taken steps to relieve some of the pressure by shrinking the weighting of the top holdings. JP Morgan analysts are still concerned that the trend is strong and can end with a catalyst triggering an unwinding and move away from the larger high P/E names.

Berkshire Hathaway Finds ESG Concerns Are a Plus for Oil and Gas Investments

Warren Buffett’s Berkshire Hathaway is capitalizing on the current commodity price dip to expand its oil and gas sector stake. This year, Berkshire committed $3.3 billion to increase its ownership in a liquefied natural gas export terminal in Maryland. Additionally, it raised its stake in Occidental Petroleum Corp. by 15% and acquired more shares in five Japanese commodity traders. The company is also lobbying for increased financial support for natural gas power plants.

Warren Buffett, the Oracle of Omaha, demonstrated how he earned the “oracle” title during the most uncertain days of the pandemic, by investing heavily in oil and gas. The sector has had impressive returns as it posted record earnings in 2022. The 92-year-old Buffett is not booking the massive gains by selling; instead Buffett is selectively adding to positions.

Are Buffett’s investment moves classic bargain-hunting, with the energy sector possibly undervalued tied to environmental, social, and governance concerns, as well as an anticipation of declining demand for fossil fuels in the future? Based on standard metrics, the energy sector is undervalued. According to data from Bloomberg, energy now trades at the lowest price-to-earnings valuation among all sectors in the S&P 500 Index, at the same time it generates the most cash flow per share. And, as a help to the industry, Berkshire’s energy division is actively lobbying for a bill that would allocate at least $10 billion to natural gas-fired power plants in Texas to support the state’s grid.

His approach in the sector is obviously deliberate and narrowly targeted. Despite Buffett’s interest in energy, his fossil fuel investments aren’t without nuances. For example, Berkshire remains the third-largest shareholder in Chevron Corp., even after it reduced its stake by about 21% in the first quarter. Each investment in companies like Occidental and Cove Point LNG has unique aspects that position them as valuable assets in the global energy landscape, regardless of the path that any U.S. or global energy transition takes.

Buffett believes that shale, a substantial part of U.S. oil production, is different and even preferred over conventional sources of oil in the Middle East and Russia. One difference is taking shale from the ground and into production can be done more quickly and have a shorter production lifespan. This provides flexibility for operators to adapt to changes in oil demand and prices. At Berkshire’s annual meeting in May, Buffett emphasized making rational decisions about energy production and criticized both extremes in the climate debate.

One of Buffett’s nuanced and targeted energy investments is Cove Point LNG. It not only exports liquefied gas but also has the rare capability to import gas, making it more versatile than other facilities along the Gulf Coast. With rising global LNG demand driven by Europe’s shift away from Russian gas and Asia’s use of gas for power generation, Cove Point’s long-term contracts with buyers, including Tokyo Gas Co. and Sumitomo Corp., make it appealing. Berkshire is Sumitomo’s second-largest shareholder after the Japanese government’s pension fund.

Outside of its stock holdings, Berkshire Hathaway Energy, under the leadership of Buffett’s expected successor Greg Abel, has been performing well. Earnings for the division hit a record high of $3.9 billion in 2022, nearly doubling over five years.

Take Away

The world’s appetite for energy, whether from fossil fuels or renewables, seems insatiable; even amid a global penchant to reduce fossil fuel use, oil demand is expected to continue rising throughout the decade. While environmental concerns have caused some investors to shy away from the energy sector, Buffett’s investments demonstrate his belief that ESG considerations are keeping oil and gas stocks attractively priced. Market participants prioritizing ESG, therefore, presents an opportunity for Berkshire to profit further from its strategic investments in the oil and gas sector.

Worldcoin Crypto Project Launched by OpenAI’s Sam Altman

In a revolutionary move, OpenAI CEO Sam Altman began rolling out Worldcoin on July 24. The cryptocurrency project aims to reinvent the way the world identifies living, breathing humans compared to AI bots. The core offering of Worldcoin is its innovative World ID, often described as a “digital passport” that serves as proof of a person’s human identity. But that is just the beginning of the project goals.

To obtain a World ID, users must undergo an in-person iris scan using Worldcoin’s revolutionary ‘orb.’ This silver ball, about the size of a bowling ball, ensures the legitimacy of the individual’s identity, subsequently creating the unique World ID.

The brains behind this revolutionary project are the San Francisco and Berlin-based organization, Tools for Humanity. During its beta phase, the project amassed an impressive 2 million users, and with the official launch on Monday, Worldcoin is rapidly expanding its ‘orbing’ operations to 35 cities across 20 countries.

In select countries, early adopters will be rewarded with Worldcoin’s own cryptocurrency token, WLD. This incentive has already driven WLD’s price to soar after the announcement. On Binance, the world’s largest, WLD reached a peak price of $5.29 and continued to trade at $2.49 (from an initial starting price of $0.15) as of 11:00 AM ET. Notably, the trading volume on Binance has reached a staggering $25.1 million.

The Role of Blockchain

Blockchains play a crucial role in this project, as they securely store World IDs while preserving user privacy and preventing any single entity from controlling or shutting down the system, according to co-founder Alex Blania.

One key application of World IDs is its ability to distinguish between real individuals and AI bots in the age of generative AI chatbots like ChatGPT, which are adept at mimicking human language. By leveraging World IDs, online platforms can effectively combat the infiltration of AI bots into human interactions.

Economic Implications of AI

Altman emphasized the economic implications of AI, stating that people will be profoundly impacted by AI’s capabilities. “People will be supercharged by AI, which will have massive economic implications,” he said.

One interesting example of what Altman believes AI can eventually provide is universal basic income (UBI), a social benefits program aimed at providing financial support to every individual. According to Altman, as AI gradually takes over many human tasks, UBI can play a vital role in mitigating income inequality. Since World IDs are exclusive to genuine human beings, they can act as a safeguard against fraud in UBI distributions.

Though Altman acknowledged that a world with widespread UBI is likely in the distant future and the logistics of such a system are still unclear, he believes that Worldcoin paves the way for experiments and solutions to tackle this societal challenge.

The launch of Worldcoin marks a significant step in the convergence of cryptocurrency and AI technologies, with potential far-reaching effects on how we identify ourselves and interact in the digital age. As the project gains momentum, financial market professionals should closely monitor the developments surrounding Worldcoin and its impact on the future of money.

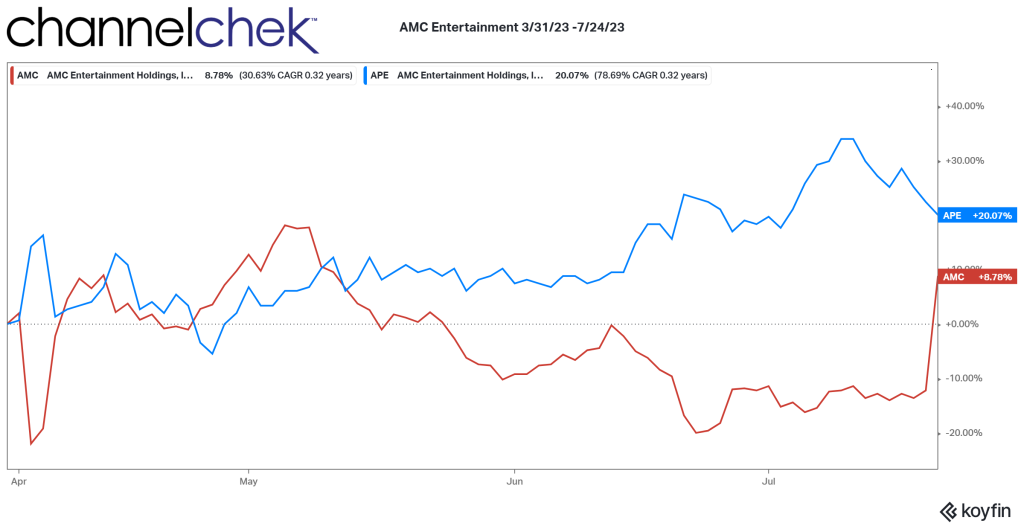

Adam Aron Explains the Reasons Share Conversion and Issuance is Good for APE Shares

Meme stocks are getting attention again as the movie Dumb Money is set for release in late September, GameStop (GME) is implementing a strategy to use its stores as fulfillment centers, and AMC Theatres (AMC) has a court ruling on its APE shares that has added significant volatility, including a 67% upward spike after hours on Friday July 21. The AMC story is involved and likely to cause wide swings until resolved as investors wrestle with guessing what a new ruling means for the company’s financial strength, and whether the judge’s decision could be overturned on appeal or through shareholder approval.

The main source of the ongoing dramatic moves in AMC stems from its proposed APE shares conversion. These preferred shares were provided as a dividend with a 1:1 conversion feature. If/when converted to regular AMC shares, they will dilute the regular shares. When issued, APE shares were considered a brilliant financing mechanism and method to determine if any fraudulent units were used to create a naked short.

In late July a judge blocked the proposed settlement on AMC Entertainment Holdings stock conversion plan that would also allow the company to issue more shares. The stock had been depressed in anticipation of the additional shares that would have been created. With the thought that additional shares won’t be entering the market, common shares (AMC) soared, and preferred shares (plummeted).

The Delaware chief judge Morgan Zurn said in her ruling that she cannot approve the deal, which would provide AMC common stockholders with shares worth an estimated $129 million. The company was sued in February for allegedly rigging a shareholder vote that would allow the entertainment company to convert preferred stock to common stock and issue hundreds of millions of new shares. The investors who sued alleged AMC had enacted the plan to circumvent the will of common stock holders who opposed the company diluting their holdings.

Without the proposed settlement, common stockholders and preferred shareholders would end up owning 34.28% and 65.72% of AMC, respectively. Under the ruling, common stockholders and preferred shareholders would own 37.15% and 62.85%, respectively.

Judge Zurn wrote that while the deal would compensate common stockholders for the dilution, they had no right to settle potential claims by holders of preferred stock in this way. The settlement received more than 2,800 objections from shareholders, a level of interest Zurn called “unprecedented.” She said “AMC’s stockholder base is extraordinary,” adding many “care passionately about their stock ownership and the company.”

But what appears short term to be good for common shares, may actually weaken the financial position of the company over time according to AMC’s chairman. In an open letter, AMC chairman Adam Aron wrote, “What may not be clear to AMC’s shareholders is that if the company is unable to convert APE shares, AMC will be forced to issue significantly more APE shares to cover its upcoming cash requirements.”

Aron explained AMC is burning cash at an unsustainable rate and warned that an inability to raise capital could force the company into bankruptcy. Selling more shares would enable it to pay down some of its $5.1 billion in debt. These financial matters are further complicated by the writers and actors strike which according to Aron could delay the release of movies currently scheduled for 2024 and 2025.

This Trading Week May be Pivotal in the Push and Pull Between Bulls and Bears

The overwhelming focus this week is on the FOMC meeting Tuesday and Wednesday. There is widespread expectation that after skipping a chance to raise rates in June, the Federal Reserve will bump the overnight lending rate up by 25 bp. This would push the target to 5.25%-5.50%. Policymakers have been clear that they don’t believe they are finished in their battle against inflation but have always maintained their actions are data-dependent. Data on inflation over the past month indicate previous moves could be having the desired impact. If the FOMC determines inflation is trending toward its goal of 2% and is expected to stay on the path, it may not find another hike prudent. However, the Fed won’t see a June reading on its preferred inflation indicator, the PCE deflator, until after the FOMC meeting.

Monday 7/24

• 8:30 AM ET, The Chicago Fed National Activity Index in June is expected to have risen to just above neutral at 0.03 (zero equals historical average growth). This would be up from a lower-than-expected minus 0.15 in May.

• 9:45 AM ET, The Purchasing Managers Index Composite flash reading has been above 50 in the last five reports with the consensus for July at 54.0 versus June’s 54.4. A reading above (below) 50 signals rising (falling) output versus the previous month and the closer to 100 (zero) the faster output is growing (contracting).

Tuesday 7/25

• 9:00 AM ET, The Federal Open Market Committee meeting to decide the direction of monetary policy begins.

• 1:00 PM ET, Money Supply is forecast to show that M2 for the month of June rose 0.6% to $20,805.5 billion. The markets resumed focusing on money supply as a way to view the progress and impact of quantitative easing. It helps decipher how the Fed’s actions are filtering through the economy.

Wednesday 7/26

• 10:00 AM ET, New Home Sales are expected to slow after a much higher-than-expected 763,000 annualized rate in May. Junes are expected to have slowed to 727,000.

• 10:30 AM ET, The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the US, whether produced here or abroad. The inventory level impacts prices for petroleum products.

• 2:00 PM ET, The FOMC announcement. After holding steady in June, the Fed is expected to raise its policy rate by 25 basis points to a range of 5.25 to 5.50 percent.

• 2:30 PM ET, The post FOMC Chair Powell press conference helps market participants understand the Fed’s decision(s), if any, during their two-day meeting.

Thursday 7/27

• 8:30 AM ET, Durable Goods Orders are forecast to have risen 0.5 percent in July following June’s 1.8 percent jump. Ex-transportation orders are expected to edge 0.1 percent lower as are core capital goods orders, after also coming in high the previous reporting period.

• 8:30 AM ET, Second-quarter GDP is expected to slow to 1.5 percent annualized growth versus first-quarter growth of 2.0 percent. Personal consumption expenditures, after the first quarter’s burst higher to plus 4.2 percent, are again expected to rise but by only 1.5 percent. Whether or not the US has entered a recession is substantially hinged on whether GDP is negative for a prolonged period (typically two quarters).

• 4:30 AM ET, The Fed’s Balance Sheet is expected to have decreased by $22.371 billion to $8.275 trillion. Market participants and Fed watchers look to this weekly set of numbers to determine, among other things if the Fed is on track with its stated quantitative tightening (QT) plan.

Friday 7/28

• 8:30 AM ET, Jobless Claims Jobless for the week ended July 22 are expected to come in at 235,000 versus 228,000 in the prior week.

• 8:30 AM ET, Wholesale Inventories are expected to increase 0.1 percent (advance report) for June, it was unchanged in May.

• 10:00 AM ET, Consumer Sentiment is expected to end July at 72.6, unchanged from July’s mid-month flash and more than 8 points higher from June. Year-ahead inflation expectations are expected to hold at the mid-month’s 3.4 percent which was one tenth higher than June.

What Else

The week ahead is also set to be the busiest one of earnings season. Thursday will be the most intense day. About 30% of the S&P 500 will give their financial updates during the week, including Alphabet, Microsoft and Meta. Several big pharma companies are getting ready to report and it’s a big week for industrial companies and big oil as well.

Sign up for Channelchek updates on this week’s FOMC meeting as announcements unfold, and to be updated on other critical information.

There will be a number of Roadshows held during the week in South Florida and St. Louis. Learn more about who’s presenting and how to attend by clicking here.

A Social Security Funded Study Demonstrates the Benefit of Including Equities

Should all or part of Social Security be invested in the stock market? A study out this month by the Center of Retirement Research (CRR) at Boston College uses evidence from the U.S. and Canada that shows that investing in equities through government retirement funds is feasible, safe, and effective. In 1984, before he became the Chairman of the Federal Reserve, Alan Greenspan headed a commission on Social Security (S.S.). While he was positive on stocks used for a portion of S.S., it was not part of the commission’s recommendation. Since then, equity returns have averaged about twice that of S.S. investments in U.S. Treasuries.

According to CRR, “evidence from the U.S. and Canada shows that such investing through government retirement funds is feasible, safe, and effective.”

The Center for Retirement Research is a non-profit research institute that studies retirement income security. It was established in 1998 as part of the Retirement Research Consortium and is funded by the U.S. Social Security Administration. The CRR’s mission is to produce first-class research and educational tools and forge a strong link between the academic community and decision-makers in the public and private sectors. The CRR conducts a wide variety of research projects on topics such as Social Security, private pensions, annuities, and retirement savings. It also publishes a variety of research reports, data sets, and educational materials. Policymakers, academics, and the media widely cite the CRR’s research.

Background

The merits of investing a portion of the Social Security trust fund in equities have been discussed for decades. With potentially higher returns compared to safer assets, such as Treasury bonds, equity investments could potentially reduce the need for tax increases or benefit cuts to ensure the long-term solvency of the system. However, this approach also carries risks and raises concerns about government interference in private markets and misleading accounting practices that may give the impression that issuing bonds and buying equities can effortlessly generate wealth for the government.

There are real-world examples that one can point to that demonstrate that governments can engage in equity investments sensibly. Canada, for instance, has a large, actively managed fund that adheres to fiduciary standards and employs conservative return assumptions. In the United States, both the Railroad Retirement System and the Federal Thrift Savings Plan have invested in a diverse range of assets without disrupting private markets. In these cases, the government’s role is primarily passive.

Despite the demonstrated successes, the question remains whether equity investments should be considered as a solution for Social Security. The prerequisite for such an approach is a trust fund with substantial assets available for investment. Currently, the existing trust fund is being depleted, and the likelihood of raising taxes to rebuild it is low. Borrowing to rebuild the trust fund does not guarantee any additional resources for Social Security.

After the Greenspan amendments in 1983, which resolved the problem for a time with taxing S.S., future deficits began to reappear. President Clinton tasked the 1994-1996 Advisory Council on Social Security with considering options for achieving long-term solvency. The council could not reach a consensus on a single plan, and its members put forward three different proposals to close the funding gap, all of which included some form of equity investment. Two proposals involved individual accounts for equity investment, while the third recommended direct equity investment using a portion of the trust fund reserves.

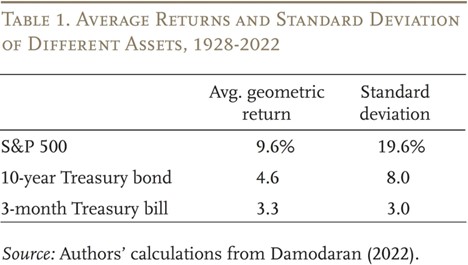

The primary attraction of equity investment lies in its higher expected rate of return compared to safer assets like Treasury bonds or bills. By restoring balance to Social Security, the need for tax increases or benefit cuts could be reduced (see Table 1). Economists also argue that effective risk-sharing across a lifespan requires individuals to bear more financial risk when young and less when old. As young individuals possess limited financial assets, investing the trust fund in equities becomes a means to achieve this goal.

Table showing the average returns and standard deviation of different assets, 1928-2022

Critics expressed concerns that equity investment by Social Security could have adverse effects on the stock market and corporate decision-making while also creating the false perception that trading bonds for stocks yields magical money.

Addressing these concerns involves answering the following questions:

How significant is the equity investment initiative relative to the overall economy? According to a 2016 study, if Social Security had begun investing in the stock market in 1984 or 1997, it would now own approximately 4 percent of the market. For comparison, state and local pension plans currently hold about 5 percent of total equities.

How do government officials select investments? Proponents of equity investment for the trust fund assume that the government would take a passive role. However, the Canada Pension Plan and the Railroad Retirement system, as discussed later, adopt a more active approach.

Do government agencies use expected returns or risk-adjusted returns to evaluate the impact of equities on plan finances? Crediting expected returns quantifies the potential contribution of equities to addressing Social Security’s financing shortfall but may falsely suggest that the government can generate money simply by selling bonds and buying stocks. Adjusting for risk avoids this misperception by acknowledging that returns are not guaranteed, but the risk adjustment would yield no immediate impact from equity investment on the system’s finances. Higher returns are only recognized after they are realized.

Three Federal Government Plans with Equity Investments

The Canada Pension Plan is a major component of Canada’s retirement system, initially established in 1966 as a pay-as-you-go plan with a modest reserve, similar to the U.S. Social Security program. This approach was suitable when the country had a young population and rapidly growing wages. However, factors such as declining birth rates, longer life expectancies, and lower real wage growth led to increased plan costs and the prospect of rising payroll contribution rates.

To address intergenerational fairness and ensure the long-term financial sustainability of the plan, Canada enacted legislation in 1997. The legislation increased payroll contributions to projected long-term rates and introduced equity investments into the fund. Any future changes to the plan must be fully funded.

The investment strategy was implemented through the creation of the CPP Investment Board (CPPIB), a government-owned corporation that operates independently from the CPP itself and is managed at arm’s length from the government. The CPPIB’s mandate is to invest excess CPP revenues in a way that maximizes returns without incurring undue risk, solely for the benefit of CPP contributors and beneficiaries.

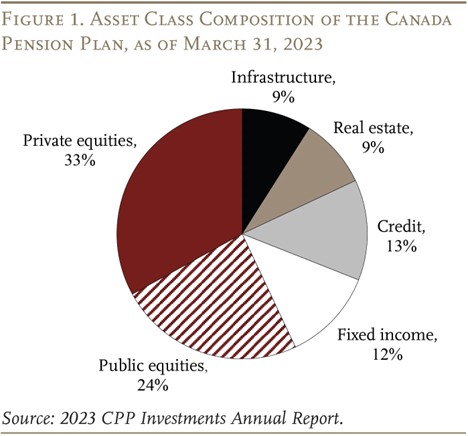

The CPPIB has built a diverse portfolio comprising stocks, bonds, real estate, infrastructure projects, and private equity (see Figure 1). As of 2023, the total assets amount to 570 billion CAD.

Pie chart showing the asset class composition of the Canada Pension Plan, as of March 31, 2023

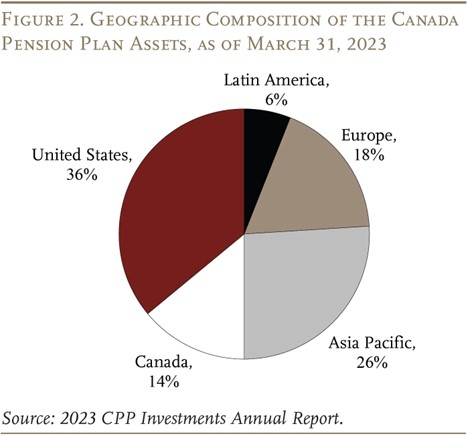

To reduce risks associated with future Canadian economic and demographic conditions, the CPPIB diversifies its investments globally (see Figure 2). Therefore, the fund’s domestic investments are relatively small compared to the country’s GDP (2.8 trillion CAD) and stock market (3.9 trillion CAD).

Pie chart showing the geographic composition of the Canada Pension Plan assets, as of March 31, 2023

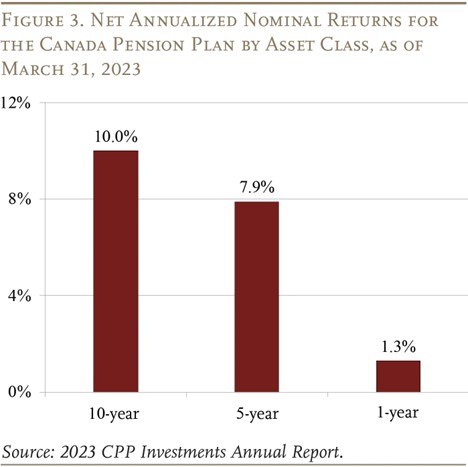

The CPPIB comprises six departments responsible for investing and managing the assets, employing highly compensated in-house managers. Over the past decade, the fund has achieved an annualized net return of 10 percent (see Figure 3).

Bar graph showing the net annualized nominal returns for the Canada Pension Plan by asset class, as of March 31, 2023

The CPPIB also considers economic, social, and governance factors in its investment decisions when managers believe that addressing these issues will generate superior long-term returns. The Board exercises proxy voting at annual meetings and encourages companies to consider climate risks and develop viable transition strategies. Rather than engaging in blanket divestment from high-emitting sectors, the managers believe in using the CPPIB’s influence constructively.

The Board assesses risk using a minimum and a target level. The base CPP’s minimum risk level consists of a portfolio divided equally between Canadian government bonds and global public equities. In 2016, legislation was passed that increased CPP contributions and benefits. The minimum risk levels for the additional component are slightly lower: 60 percent bonds and 40 percent global equities.

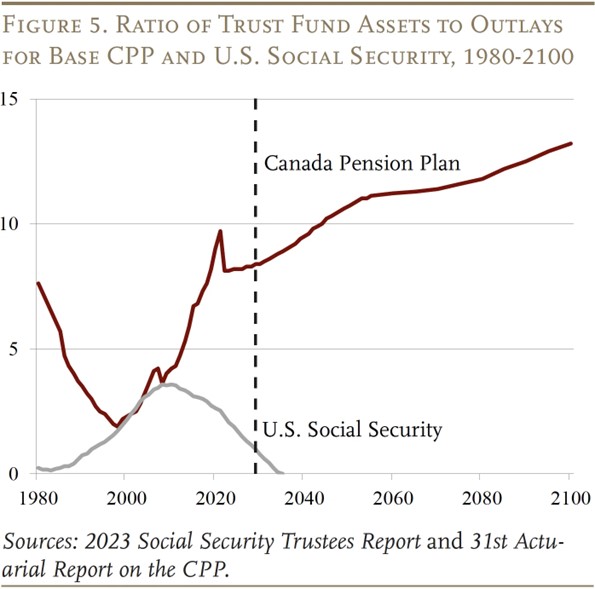

The actuarial reports adopt conservative return assumptions, as the actual investment earnings have consistently exceeded projected earnings. Under these prudent assumptions, both the base CPP and the additional CPP components have been projected to remain sustainable for a 75-year period. If the system’s finances are projected to be imbalanced, an additional safeguard triggers an increase in contribution rates and a freeze in benefit indexation if policymakers fail to address the projected imbalance.

The Canadian investment initiative has proven successful while addressing the concerns raised by critics. Investments represent a small share of the Canadian economy, adhere to strict fiduciary standards, and the assumed investment returns used for evaluating the solvency of the CPP are conservative.

U.S. Railroad Retirement System

The Railroad Retirement system was created by Congress in 1934 to assume responsibility for the rail industry’s ailing pension plan. Initially funded on a pay-as-you-go basis through payroll taxes on workers and employers, the program had a modest trust fund invested solely in government bonds. However, by the 1990s, the trust fund’s assets had grown to four times the annual outlays, reaching historically high levels. There was a belief that further growth could be achieved through equity investments, leading management and labor to negotiate a proposal for such investments. However, given that Railroad Retirement is a government program, the plan required congressional approval.

Congress expressed concerns about potential political influence on investment decisions. To address this, Congress established the National Retirement Investment Trust (NRRIT). The NRRIT comprises six trustees, with three selected by management and three by labor, who then choose a seventh independent trustee. Congress also imposed a private-sector fiduciary mandate on these trustees, requiring them to invest the government’s assets solely in the interest of plan participants. Initially, 65 percent of trust fund assets were allocated to equities. Over time, the NRRIT expanded its portfolio beyond equities to include real estate, private equity, and private debt. As of 2023, the net assets in the trust fund amounted to $27 billion. External managers handle the actual investing.

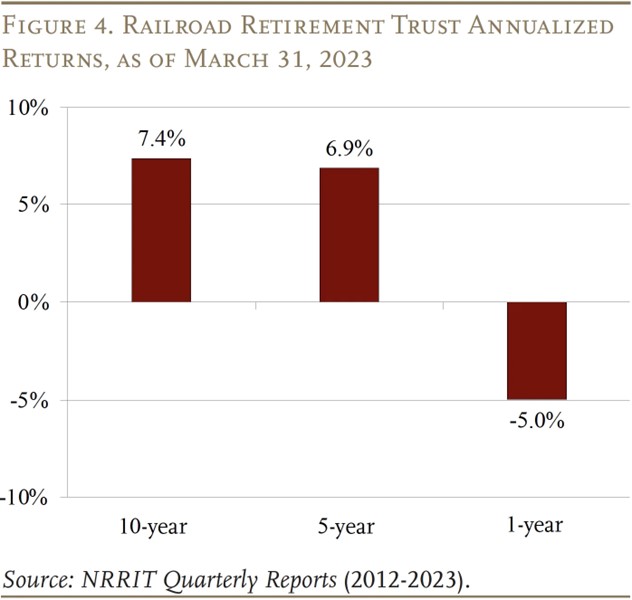

The evaluation of equity use in reform proposals raised a key issue. While the Social Security actuaries credit equities with their expected rate of return, the Office of Management and Budget, in assessing the financial implications of the Railroad Retirement proposal, disregarded the higher expected return and employed a risk-adjusted return—the long-term Treasury rate—to project future trust fund balances. Currently, the Railroad Retirement actuaries assume a 6.5-percent return, striking a balance between actual returns and a risk-adjusted rate.

Bar graph showing the Railroad Retirement Trust annualized returns, as of March 31, 2023

Federal Thrift Savings Plan

Established in 1986, the Federal Thrift Savings Plan (TSP) boasts 6.5 million participants and approximately $800 billion in assets. Concerns among members of Congress regarding potential executive branch pressure on plan fiduciaries to select investment options that align with its policy goals prompted the establishment of stringent safeguards.

The Federal Retirement Thrift Investment Board, responsible for administering the TSP, has limited discretion compared to other plan fiduciaries when setting investment policy. Congress determines the number and types of investment funds that the Board can offer, and any expansion or change requires congressional approval. When choosing benchmark indices for the investment funds, the Board is restricted to those that are widely recognized and reasonably represent the entire market. The Board is also prohibited from removing any stock from the index and categorically barred from using proxy voting power to influence corporate decision-making.

Francis Cavanaugh, the first executive director of the TSP’s Board, reported no difficulties in selecting an index or obtaining competitive bids from large index fund managers. He encountered no instances of government interference in the market. In essence, the TSP provides a model for structuring Social Security’s equity investment, with a passive approach through index funds and no proxy voting.

Does Equity Investments Make Sense in 2023?

In theory, the answer is “yes.” Plans that have adopted equity investments have consistently outperformed bond yields, even in the face of economic downturns such as the dot-com recession and the financial crisis. Concerning critics’ concerns, the experience of the TSP offers guidance on separating government intervention from actual investment decisions. Additionally, evaluating returns on a somewhat risk-adjusted basis, similar to the approach employed by the Railroad Retirement system, prevents the perception of easy money.

However, investing trust fund assets in equities necessitates a substantial trust fund. Unfortunately, the Social Security trust fund that emerged from the 1983 amendments is rapidly diminishing. Rebuilding the trust fund would require a tax increase to cover current program costs and generate an annual surplus to accumulate reserves.

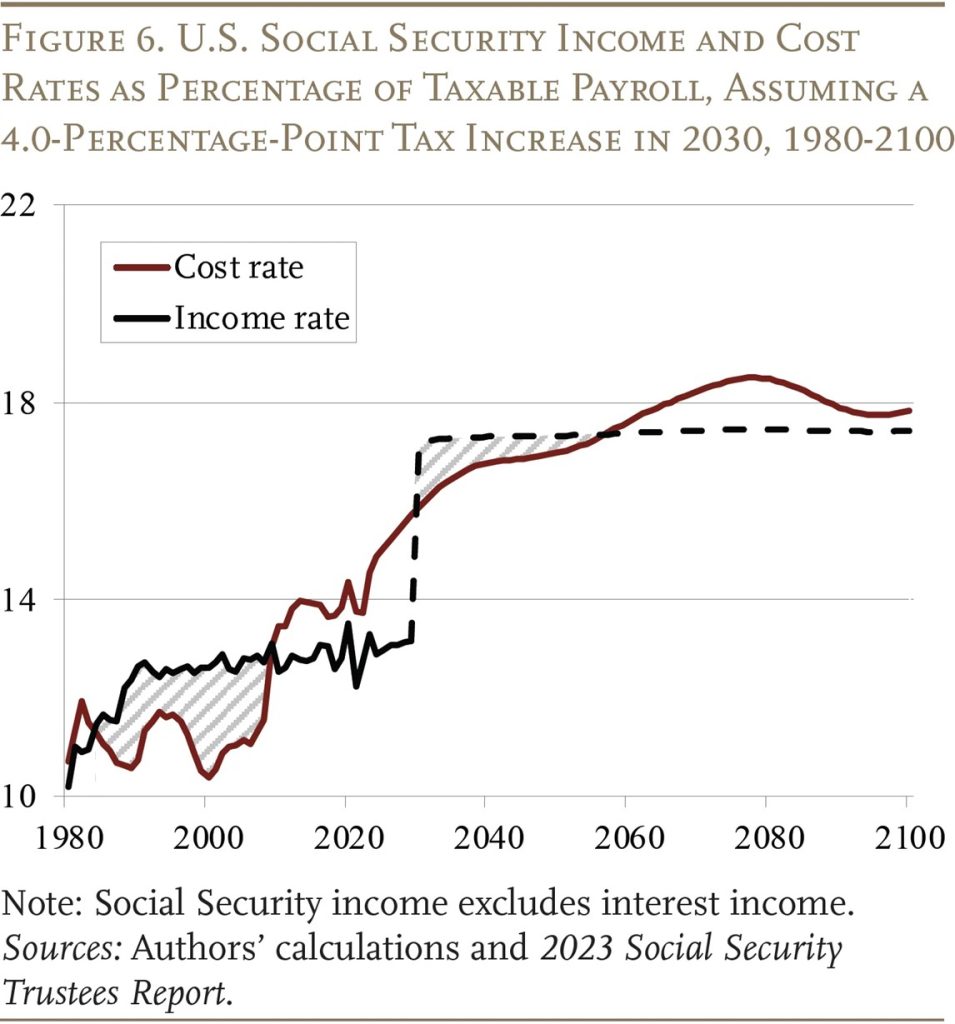

Although such an initiative is not without precedent—the United States and Canada both raised payroll contributions above current program costs and accumulated fund assets—present circumstances differ significantly from those in 1983. The majority of cost increases lie in the past. Even if Congress were to raise the payroll tax rate by 4 percentage points starting in 2030—an amount roughly needed to cover benefits over the next 75 years—it would only result in minor temporary surpluses, followed by future cash-flow deficits. These surpluses would be less than 40 percent of those generated by the 1983 legislation

Line graph showing the U.S. Social Security income and cost rates as a percentage of taxable payroll, assuming a 4.0-percentage-point tax increase in 2030, 1980-2100

Considering the unlikelihood of Congress taking action well before 2030, the combination of current trust fund balances and immediate surpluses resulting from the tax increase would only lead to modest accumulation.

Furthermore, it is questionable whether there is enough political will to implement such measures, and the case for building a large trust fund is not particularly compelling. With costs projected to stabilize, it is challenging to argue that today’s workers should pay more to build a trust fund that will benefit future workers.

If Congress is unwilling to raise taxes sufficiently to create a substantial trust fund, could borrowing be a viable solution? One proposal suggests that the government borrow around $1.5 trillion to invest in stocks, private equity, and other instruments with higher expected returns than government debt interest. In the interim, the government would continue borrowing to cover Social Security’s shortfall. After 75 years, the trust fund proceeds could be used to repay the borrowed funds that financed benefit payments.

This proposal differs fundamentally from Canada’s approach, which involves contributing additional funds to build up a reserve for the future. On the contrary, creating a trust fund with borrowed money that the government must repay with interest means that any proceeds would be limited to returns exceeding the bond rate. Fixing Social Security requires genuine economic changes, such as benefit reductions or increased income. This proposal offers no real solutions except the opportunity to pocket returns exceeding the bond rate.

Critics liken this proposal to advising a middle-aged couple who realize they have insufficient retirement savings to not reduce their spending, plan for reduced expenses after retirement,

Take Away

The US Social Security System investing in equities through retirement program trust funds is a viable concept that has been proven feasible, safe, and effective in both Canada and the United States. So, in theory, this idea could have worked, but can it may be late to attempt now. This is because one critical component is now deficient. SS no longer has a sizable trust fund to invest. And rebuilding the trust fund through additional taxes or borrowing may not be feasible.

While the mechanics are manageable, the window may have passed for raising taxes enough to accumulate a meaningful Social Security trust fund that would make investing in equities worthwhile and prudent according to the CRR.

Image: The author attending a stylish financial industry event in Boca Raton, FL

The Emerging Financial Centers and the Brain Drain from Other Cities are Changing Where Deals Get Done

They used to call it “god’s waiting room,” now they call it home.

If you haven’t guessed, I’m talking about Florida, and more specifically, the big-name financial firms that have either moved their headquarters to “Wall Street South” or have built a much larger presence in West Palm Beach, Miami, Fort Lauderdale, or the Tampa area. I made the move myself some years back after more than 20 years managing large funds for some of the most prestigious firms in NYC – now, some of those very firms are discovering what I have learned, that the weather, costs, and culture make both living and working a lot easier.

Each investment company that chooses South Florida as a region to grow its firm, brings even more sophisticated investors and dealmakers to those already in the state —face-to-face networking is now high caliber and done with ease. Everyone in the industry is benefitting from the closer proximity to each other and being able to meet and make introductions in an environment that, in my opinion, is much more conducive to making acquaintances, building trust, and even having some fun.

Florida is a Disruptor

My old firm, Goldman Sachs, just built out 35,000 feet of office space in the Miami, Brickell area. This is on top of their ongoing presence in Miami and West Palm Beach. They aren’t alone, the absence of a state income tax, coupled with a government that is business-friendly helped prompt hedge fund billionaires and native New Yorkers Paul Singer and Carl Icahn to relocate their firms to Florida.

Other prestigious firms have done the same; Blackstone opened an office in Downtown Miami in 2021. Citadel, relocated its headquarters from Chicago to Miami in 2021. D1 Capital Partners, a hedge fund, announced plans to relocate to South Florida in 2022. Merrill Lynch expanded its presence within Florida a bit sooner, 2020. Hedge fund, Tiger Global Management, announced plans to relocate to South Florida in 2022. In November of 2022, fund manager Ark Invest founded by Cathie Wood moved its headquarters out of NYC to St. Petersburg, FL. And the list goes on, and is growing.

In addition to lower costs of business, the areas these companies are moving to offer an educated base and a financially astute talent pool from which to hire.

And the financially savvy populous is getting deeper as professionals looking to relocate out of colder, high tax states, are moving down and becoming part of the already strong ecosystem. The ever-increasing depth of players include experienced attorneys, accountants, bankers, consultants, insurers, IT experts, and others with which to conduct world-class business dealings.

The other ingredients are here as well. Asset managers require convenient public and private executive airports. Local officials must also be conversant enough in their industry to regulate it intelligently, S. Florida checks both of those boxes too. It takes more than one large asset management firm to generate a demand for services sufficient to build the critical mass necessary to sustain an ecosystem. Florida has passed the tipping point and has already been labeled “Wall Street South.”

Florida Infrastructure

The ecosystem also includes facilities for tradeshows, networking events, and conferences. As an example, this coming December 3-5, Noble Capital Markets, a boutique investment bank located in Boca Raton, FL, will hold its massive, 19th annual investment conference, NobleCon19, at the 52,000 square foot, state-of-the art facility just opened on the Florida Atlantic University campus (FAU), in Boca Raton.

Noble’s 19th Annual Small-cap Investor Conference has been the “must-go” event in the area for 19 years. In 2023 the Noble can now expand this annual event into a facility that boasts the latest technology and conference facilities. This means investors and presenters at NobleCon19 will have an ideal setting to discover new opportunities and more room to welcome and network with the areas new financial executive neighbors, along with other attendees from across the globe.

From Good to Great

There are three defining factors that have helped the S. Florida region grow from an area with many small and mid-size financial firms to a strong and expanding financial center.

In no particular order, these include:

Greater reliance on virtual teams now makes physical proximity to key players less important . Even as many firms reel staff back into the office, companies are far more comfortable reaching team members virtually.

More associated professionals are moving to the emerging centers. When major investors and financial services giants such as Goldman Sachs, Blackstone, Citadel,Ark Invest, and Icahn Enterprises set up shop in a location, expertise follows. This is almost a requirement in sectors such as private equity, where deals are paved by personal relationships, social networks and professional networks.

The major cities in Florida already have existing professional and educational infrastructures. Of course, if the firms leadership is from out of town, it will naturally have a bias in favor of the schools they attended or are familiar with. But it is becoming easier to lose that bias when they learn that, for instance, in Palm County, Florida Atlantic University College of Business’ Executive Education just earned a prestigious global endorsement in the 2023 Financial Times rankings for open enrollment professional education programs – FAU ranked No. 2 in the United States.

Home Life

As one might imagine, with thousands of highly paid professionals looking for homes and “their new favorite restaurants” that real estate values are increasing and entire neighborhoods are becoming wealthier at every level. This growth feeds on itself and the improvements draw more top talent that then call South Florida the place they live and work.

Take Away

South Florida lost its reputation as a large retirement home where Grandma lives, and is now seen as an emerging financial powerhouse where big and small financial firms want to be to do business, grow their network, and live a better life.

With modern infrastructure, lower costs, top professionals, entertainment, and state of the art conference facilities, the trend is likely to continue.