New Zeus Motors are in Production and Ready for Use

SAN DIEGO, Nov. 07, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, today announced that its Zeus 1 and Zeus 2 Solid Rocket Motors (SRMs) completed their first successful flight on October 24, 2024, from the NASA Wallops Flight Facility in Virginia. This milestone launch provides the qualifications necessary to transition the Zeus SRMs to test programs supporting the U.S. Department of Defense, Foreign Allies, NASA, and commercial launch sponsors.

Kratos Zeus Solid Rocket Motors Complete Successful First Flight at Wallops

The flight test featured a Kratos two-stage Zeus 1 – Zeus 2 suborbital launch vehicle and provided substantial data to support rocket motor evaluation for use by future customers and sponsors who have baselined the Zeus rocket motors as part of their future test plans. Kratos expects to have production motors ready in the first quarter of 2025.

Kratos developed the Zeus family of SRMs in direct response to the need for affordable commercial launch vehicle stages for hypersonic test, ballistic missile targets, scientific research, sounding rocket and special customer missions. Kratos applied its significant rocket launch experience to establish the Zeus 1 and Zeus 2 motor specifications in close coordination with respective customer and user communities. Kratos internally funded development of the Zeus SRMs which are designed and manufactured to Kratos’ specifications by key merchant supplier and partner, L3Harris Technologies. L3Harris is on contract to begin delivering production motors to Kratos in the first quarter of 2025.

George Rumford, Director of the Department of Defense Test Resource Management Center, said, “Advancements in solid rocket motor development are critical to achieving rapid, affordable hypersonic testing.”

Dave Carter, President of Kratos’ Defense & Rocket Support Services Division, said, “I couldn’t be prouder of our whole team. They met the challenge to deliver these robust motors to market as fast as possible and meet the growing demand for rapid, reliable testing. The motors performed exceptionally well against predictions and are ready for immediate use by the broader test and research community.”

The Zeus 1 and Zeus 2 are high-performance, 32.5-inch diameter SRMs providing substantial performance improvements over similar legacy rockets. They are purposely designed to be fully compatible with existing payloads and launch infrastructure to enable rapid integration of new technologies and advanced payloads, including those currently under development by Kratos. These and other key attributes will provide Kratos and our customers with opportunities to fly more often, faster and farther, using fewer stages, and at a substantially reduced cost.

The Zeus SRM family is designed with versatility and affordability in mind as a complement to Kratos’ other internally funded investments such as the Erinyes hypersonic test “flyer” that debuted in June of this year. Kratos’ investments in the hypersonic and other relevant areas create a versatile family of test and evaluation products that offer complete systems. With the Zeus SRMs, the Erinyes, and other Kratos front end systems, Kratos is one of the only companies boasting both launcher and flyer systems within one organization, providing unmatched innovation, disruptive capabilities, mission responsiveness and affordability to the customer.

Eric DeMarco, President & CEO of Kratos Defense & Security Solutions, Inc., said, “Kratos is laser focused on supporting the Department of Defense, U.S. National Security requirements and working with our government partners to reinvigorate our country’s defense industrial base. Zeus’ successful mission is representative of the value Kratos’ strategy delivers to our stakeholders, with Kratos’ internally funded investments allowing us to rapidly develop and be first to market with affordable relevant systems for our partners and customers.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 31, 2023, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

DENVER, Nov. 07, 2024 (GLOBE NEWSWIRE) — Medicine Man Technologies, Inc., operating as Schwazze, (OTC: SHWZ) (Cboe CA: SHWZ) (“Schwazze” or the “Company”), today announced preliminary financial and operational results for the third quarter ended September 30, 2024.

“We continued to generate momentum from our retail growth and optimization initiatives in Q3, reflected by our ability to outpace two highly competitive markets while generating sequential improvements in profitability and positive cash flow from operations,” said Forrest Hoffmaster, Interim CEO of Schwazze. “Our efforts to sharpen our pricing and promotional strategy, elevate the in-store experience, and improve product quality, assortment and in-stock positions are yielding positive results. I’m proud of our team’s hard work and dedication to drive these improvements in the overall customer experience, which has led to increased store traffic in both Colorado and New Mexico. Over the past year, our focused efforts to optimize our operations have built a solid foundation, setting the stage for sustained growth and enhanced levels of profitability in the year ahead.

“Due to our ongoing re-review process with our new auditor, Baker Tilly, we expect a delay in filing our Form 10-Q for the quarter ended September 30, 2024. Our team, in close collaboration with Baker Tilly, is making every effort to complete this re-review promptly. We expect to release our unaudited third quarter results and host a conference call in the coming weeks to discuss our financial and operational performance in greater detail.”

Q3 2024 Preliminary Financial Results

Based on preliminary and unaudited results, the Company expects to report the following for the third quarter ended September 30, 2024:

Revenue of approximately $42 million

Adjusted EBITDA of approximately $11 million

Cash flow from operations of approximately $0.2 million

At quarter end, the Company held cash and cash equivalents of approximately $11 million with principal amount of debt outstanding of approximately $196 million.

Update on Delayed Filing

As previously announced on April 8, 2024, Schwazze dismissed BF Borgers CPA PC (“BF Borgers”) as its independent registered public accountant and engaged Baker Tilly US, LLP (“Baker Tilly”) as its new independent accountant. Subsequent to the transition, on May 3, 2024, the SEC issued an Order against BF Borgers for systemic failures in meeting PCAOB standards, which impacted over 1,500 SEC filings and affected at least 75 percent of BF Borgers’ 369 clients.

As a result of the SEC Order, Schwazze’s new auditor needs additional time to complete its prior period review, which includes re-auditing the Company’s fiscal year 2023 financial statements and re-reviewing the closing of its 2022 balance sheet prior to filing its 2024 Annual Report. Baker Tilly is actively working to re-audit the Company’s financial statements for the associated periods.

Due to the ongoing re-review process, Schwazze anticipates a delay in filing its Quarterly Report on Form 10-Q for the three- and nine-months ending September 30, 2024. Moreover, the Company expects to simultaneously file its Quarterly Report on Form 10-Q for the three months ending March 31, 2024, and June 30, 2024.

About Schwazze

Schwazze (OTC: SHWZ) (Cboe CA: SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to explore taking its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale.

Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector.

Medicine Man Technologies, Inc. was Schwazze’s former operating trade name. The corporate entity continues to be named Medicine Man Technologies, Inc. Schwazze derives its name from the pruning technique of a cannabis plant to enhance plant structure and promote healthy growth. To learn more about Schwazze, visit https://schwazze.com/.

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements include financial outlooks; any projections of net sales, earnings, or other financial items; any statements of the strategies, plans and objectives of our management team for future operations; expectations in connection with the Company’s previously announced business plans; any statements regarding future economic conditions or performance; and statements regarding the intent, belief or current expectations of our management team. Such statements may be preceded by the words “may,” “will,” “could,” “would,” “should,” “expect,” “intends,” “plans,” “strategy,” “prospects,” “anticipate,” “believe,” “approximately,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing,” or the negative of these terms or other words of similar meaning in connection with a discussion of future events or future operating or financial performance, although the absence of these words does not necessarily mean that a statement is not forward-looking. We have based our forward-looking statements on management’s current expectations and assumptions about future events and trends affecting our business and industry. Although we do not make forward-looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. Therefore, forward-looking statements are not guarantees of future events or performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which are beyond the Company’s control and cannot be predicted or quantified. Consequently, actual events and results may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, without limitation, risks and uncertainties associated with (i) regulatory limitations on our products and services and the uncertainty in the application of federal, state, and local laws to our business, and any changes in such laws; (ii) our ability to manufacture our products and product candidates on a commercial scale on our own or in collaboration with third parties; (iii) our ability to identify, consummate, and integrate anticipated acquisitions; (iv) general industry and economic conditions; (v) our ability to access adequate capital upon terms and conditions that are acceptable to us; (vi) our ability to pay interest and principal on outstanding debt when due; (vii) volatility in credit and market conditions; (viii) the loss of one or more key executives or other key employees; and (ix) other risks and uncertainties related to the cannabis market and our business strategy. More detailed information about the Company and the risk factors that may affect the realization of forward-looking statements is set forth in the Company’s filings with the Securities and Exchange Commission (SEC), including the Company’s Annual Report on Form 10-K and its Quarterly Reports on Form 10-Q. Investors and security holders are urged to read these documents free of charge on the SEC’s website at http://www.sec.gov. The Company assumes no obligation to publicly update or revise its forward-looking statements as a result of new information, future events or otherwise except as required by law.

Investor Relations Contact Sean Mansouri, CFA or Aaron D’Souza Elevate IR (720) 330-2829 ir@schwazze.com

Third Quarter 2024 Revenues of $275.9 Million Compared with Third Quarter 2023 Revenues of $274.6 Million

Third Quarter 2024 Unmanned Systems Revenues of $64.2 Million Compared with Third Quarter 2023 Revenues of $56.7 Million

Third Quarter 2024 Consolidated Book to Bill Ratio of 1.0 to 1 and Last Twelve Months Ended September 29, 2024 Consolidated Book to Bill Ratio of 1.1 to 1

Third Quarter 2024 Consolidated Bookings of $267.2 Million and Last Twelve Months Ended September 29, 2024 Consolidated Bookings of $1.240 Billion

Affirms Full Year 2024 Financial Forecast

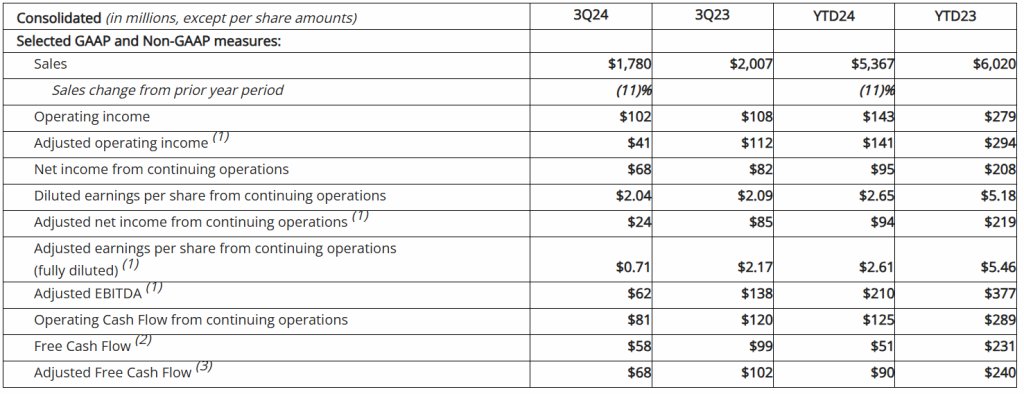

SAN DIEGO, Nov. 07, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq:KTOS), a Technology Company in the Defense, National Security and Global Markets, today reported its third quarter 2024 financial results, including Revenues of $275.9 million, Operating Income of $6.5 million, Net Income of $3.2 million, Adjusted EBITDA of $24.6 million and a consolidated book to bill ratio of 1.0 to 1.0.

Included in third quarter 2024 Net Income and Operating Income is non-cash stock compensation expense of $7.2 million and Company-funded Research and Development (R&D) expense of $9.9 million.

Kratos reported third quarter 2024 GAAP Net Income attributable to Kratos of $3.2 million and Earnings Per Share of $0.02 compared to a GAAP Net Loss attributable to Kratos of $1.6 million and a GAAP Net Loss per share of $0.01 for the third quarter of 2023. Adjusted EPS was $0.11 for the third quarter of 2024 compared to $0.12 for the third quarter of 2023.

Third quarter 2024 Revenues of $275.9 million increased $1.3 million, or 0.5 percent, from third quarter 2023 Revenues of $274.6 million. Including the impact of the Sierra Technical Services, Inc. (STS) acquisition on a pro forma basis as if acquired at the beginning of 2023, Unmanned Systems reported 8.7 percent organic revenue growth. Kratos Turbine Technologies, Microwave Products, C5ISR, Defense Rocket Support and Training Solutions businesses in KGS also all reported organic revenue growth, offset by the previously reported and expected decline of approximately $24.2 million in the Space and Satellite business, primarily resulting from the industry related impact from OEM delays in the manufacture and delivery of software defined satellites.

Third quarter 2024 Cash Flow Generated from Operations was $6.1 million, which includes working capital requirements for increases in prepaid assets, inventory balances, vendor required deposits and reduction in deferred revenue or customer prepayment balances. Free Cash Flow Used in Operations was $9.2 million after funding of $15.3 million of capital expenditures, including the continued manufacture of two production lots of Kratos Valkyrie unmanned tactical jet drone aircraft prior to contract award.

For the third quarter of 2024, Kratos’ Unmanned Systems Segment (KUS) generated Revenues of $64.2 million, compared to $56.7 million in the third quarter of 2023, with organic revenue growth of 8.7 percent, driven primarily by increased target drone production, and reflects the pro forma impact of the STS acquisition as if acquired at the beginning of 2023. KUS’s Operating Income was $0.4 million in the third quarter of 2024 compared to Operating Income of $2.6 million in the third quarter of 2023, primarily reflecting the mix of revenues and resources.

KUS’s Adjusted EBITDA for the third quarter of 2024 was $3.6 million, compared to third quarter 2023 KUS Adjusted EBITDA of $5.4 million, reflecting the mix of revenues and resources.

KUS’s book-to-bill ratio for the third quarter of 2024 was 0.5 to 1.0 and 1.1 to 1.0 for the last twelve months ended September 29, 2024, with bookings of $32.6 million for the three months ended September 29, 2024, and bookings of $295.1 million for the last twelve months ended September 29, 2024. Total backlog for KUS at the end of the third quarter of 2024 was $273.9 million compared to $305.5 million at the end of the second quarter of 2024.

For the third quarter of 2024, Kratos’ Government Solutions Segment (KGS) generated Revenues of $211.7 million compared to $217.9 million in the third quarter of 2023, reflecting aggregate organic revenue increases of $18.0 million generated by the Kratos’ Turbine Technologies, Microwave Products, C5ISR, Defense Rocket Support and Training Solutions businesses in KGS, offset by the previously reported and expected decline of $24.2 million in the Space and Satellite business, as noted above.

KGS reported operating income of $13.5 million in the third quarter of 2024 compared to $15.9 million in the third quarter of 2023, primarily reflecting the revenue volume and mix of revenues and resources. Third quarter 2024 KGS Adjusted EBITDA was $21.0 million, compared to third quarter 2023 KGS Adjusted EBITDA of $22.3 million, reflecting the mix in revenues, revenue volume and resources.

For the third quarter of 2024 and the last twelve months ended September 29, 2024, KGS reported a book-to-bill ratio of 1.1 to 1.0, and bookings of $234.6 million and $945.0 million for the three and last twelve months ended September 29, 2024, respectively. KGS’s total backlog at the end of the third quarter of 2024 was $1.02 billion, as compared to $997.2 million at the end of the second quarter of 2024.

For the third quarter of 2024, Kratos reported consolidated bookings of $267.2 million and a book-to-bill ratio of 1.0 to 1.0, with consolidated bookings of $1.24 billion and a book-to-bill ratio of 1.1 to 1.0 for the last twelve months ended September 29, 2024. Consolidated backlog was $1.294 billion on September 29, 2024 and $1.303 billion on June 30, 2024. Kratos’ bid and proposal pipeline was $12.0 billion at September 29 and June 30, 2024. Backlog at September 29, 2024 was comprised of funded backlog of $1.098 billion and unfunded backlog of $195.4 million.

Eric DeMarco, Kratos’ President and CEO, said, “Kratos’ strategy of making internally funded investments, to be first to market with relevant hardware, software and systems, in coordination with our partners and customers is working, as reflected in our financial results and our $12 billion opportunity pipeline. A recent representative example of this success is the successful flight of Kratos’ Zeus 1 and Zeus 2 system solid rocket motor stack with our customer’s payload, positioning Kratos for potential growth above our current future revenue year over year 10% target beginning in 2026.”

Mr. DeMarco went on, “Consistent with the success of and opportunities from Kratos’ strategy, earlier this year we completed an equity raise to position the Company to ensure successful execution on programs we have received and expect to receive. As an update to the related investments we are making: Kratos is currently manufacturing ~ 165 jet drones a year and we are now positioned to increase to ~400 a year including Valkyrie. Kratos can now produce ~10,000 small jet engines annually for drones and missiles, Kratos Microwave Electronics’ expansion in Israel is on track for a Q2 2025 completion, including an additional new manufacturing facility, an expanded existing manufacturing facility and a space & satellite qualified capability; we have identified the site for our new rocket system production and integration facility including for Zeus, Oriole and Erinyes and plan to break ground by the end of this year; and we have now identified the site for our new turbofan engine facility. Importantly, each of these expansion initiatives have existing programs, customer funded backlog or opportunities, or are in conjunction with a partner.”

Mr. DeMarco continued, “We continue to make progress in Kratos’ tactical drone business, with Kratos’ Apollo drone program now in contract documentation and Kratos’ Athena drone program under contract. Additionally, we have had recent successful Valkyrie flights with the U.S. Marines, Navy and Office of the Secretary of Defense, and Kratos recently has been selected on a new tactical drone opportunity. Importantly, our Ghost Works is on track to fly both a Kratos tactical drone and Kratos target drone in 2025 with Kratos internally funded, developed and manufactured jet engines, which will provide increased performance and electrical power, at reduced cost. Kratos Ghost Works is also expecting to fly the newest version of Kratos Valkyrie in 2025, as we make internally funded investments and continue to expand the Valkyrie families’ capability set and further drive down its operating and overall cost, and our newest 5th Generation drone is also scheduled for first flight in 2025 in conjunction with our customer.”

Mr. DeMarco concluded, “We are in a generational recapitalization of strategic weapon systems, with Kratos being an industry leader in hardware, software and systems for mission critical National Security and Defense applications. Expected growth drivers for Kratos in 2025 include; Kratos Erinyes, Zeus, Dark Fury, Oriole and other relevant rocket systems; Kratos jet engine and propulsion systems for missiles, drones, supersonic and space systems; microwave electronics and C5ISR products for air defense, CUAS, missile and radar systems and jet target drone systems.”

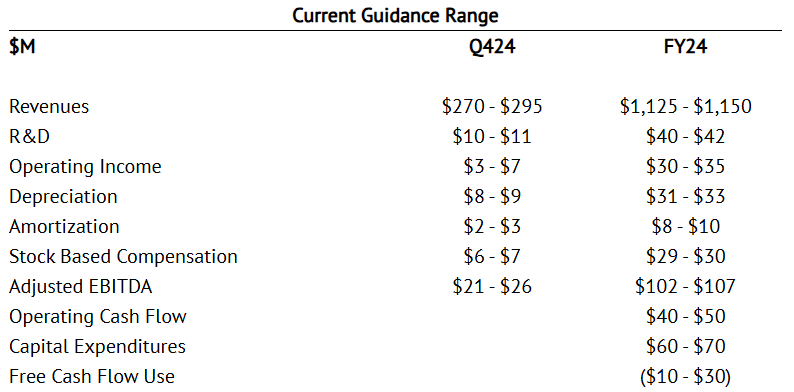

Financial Guidance

We are providing our initial 2024 fourth quarter financial guidance and affirming our full year 2024 guidance today, which ranges include our current forecasted business mix assumptions and expected contract execution and delivery schedules. Our financial guidance also includes our expectations and assumptions for our supply chain’s execution, and for employee sourcing, hiring, retention and related costs. We have also taken into consideration in our affirmed fiscal 2024 guidance the Federal Fiscal Year 2025 Continuing Resolution Authorization (CRA) which began on October 1, 2024, and under such expected CRA, no new program or contract awards, no increases in existing production contract funding, and no transition from program development to production are expected.

Our fourth quarter and full year 2024 guidance ranges are as follows:

For Kratos’ Fiscal year 2025, we are currently forecasting base case Revenue growth of approximately 10%, and Adjusted EBITDA growth. Our industry is currently operating under a Federal Fiscal Year 2025 CRA, which began October 1, 2024 and which is currently expected to continue into Kratos’ Fiscal 2025. There was also an approximate 6-month Federal Fiscal 2024 CRA, which was previously resolved in March 2024, Kratos’ current 2024 fiscal year. Additionally, the recent election will impact the Administration, House and Senate. Accordingly, we will be providing our detailed 2025 Revenue, Adjusted EBITDA, Cash Flow and other financial forecast information and guidance when we report our Fiscal 2024 results, currently expected to be in late February 2025. This will provide Kratos additional time to assess the impacts of these ongoing and recent events, if any, on National Security priorities, our 2025 business mix, contractual and program funding and timing assumptions and potential fiscal year 2025 fiscal quarter to quarter impacts. Kratos’ base case financial forecast does not assume or include any potential tactical drone program production.

Management will discuss the Company’s financial results, on a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

Notice RegardingForward–LookingStatements This news release contains certain forward-looking statements that involve risks and uncertainties, including, without limitation, express or implied statements concerning the Company’s expectations regarding its future financial performance, including the Company’s expectations for its fourth quarter and full year 2024 and fiscal year 2025 revenues, revenue growth, Adjusted EBITDA growth, organic revenue growth rates, R&D, operating income (loss), depreciation, amortization, stock based compensation expense, and Adjusted EBITDA, and full year 2024 operating cash flow, capital expenditures and other investments, and free cash flow, the Company’s future growth trajectory and ability to achieve improved revenue mix and profit in certain of its business segments and the expected timing of such improved revenue mix and profit, including the Company’s ability to achieve sustained year over year increasing revenues, profitability and cash flow, the Company’s expectation of ramp on projects and that investments in its business, including Company funded R&D expenses and ongoing development efforts, will result in an increase in the Company’s market share and total addressable market and position the Company for significant future organic growth, profitability, cash flow and an increase in shareholder value, the Company’s bid and proposal pipeline and backlog, including the Company’s ability to timely execute on its backlog, demand for its products and services, including the Company’s alignment with today’s National Security requirements and the positioning of its C5ISR and other businesses, planned 2024 investments, including in the tactical drone and satellite areas, and the related potential for additional growth in 2025 and beyond, ability to successfully compete and expected new customer awards, including the magnitude and timing of funding and the future opportunity associated with such awards, including in the target and tactical drone and satellite communication areas, performance of key contracts and programs, including the timing of production and demonstration related to certain of the Company’s contracts and control (TT&C) product offerings, the impact of the Company’s restructuring efforts and cost reduction measures, including its ability to improve profitability and cash flow in certain business units as a result of these actions and to achieve financial leverage on fixed administrative costs, the ability of the Company’s advanced purchases of inventory to mitigate supply chain disruptions and the timing of converting these investments to cash through the sales process, benefits to be realized from the Company’s net operating loss carry forwards, the availability and timing of government funding for the Company’s offerings, including the strength of the future funding environment, the short-term delays that may occur as a result of Continuing Resolutions or delays in U.S. Department of Defense (DoD) budget approvals, timing of LRIP and full rate production related to the Company’s unmanned aerial target system offerings, as well as the level of recurring revenues expected to be generated by these programs once they achieve full rate production, market and industry developments, and the current estimated impact of the national election, supply chain disruptions, availability of an experienced skilled workforce, inflation and increased costs, risks related to potential cybersecurity events or disruptions of our information technology systems, and delays in our financial projections, industry, business and operations, including projected growth. Such statements are only predictions, and the Company’s actual results may differ materially from the results expressed or implied by these statements. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Factors that may cause the Company’s results to differ include, but are not limited to: risks to our business and financial results related to the reductions and other spending constraints imposed on the U.S. Government and our other customers, including as a result of sequestration and extended continuing resolutions, the Federal budget deficit and Federal government shut-downs; risks of adverse regulatory action or litigation; risks associated with debt leverage; risks that our cost-cutting initiatives will not provide the anticipated benefits; risks that changes, cutbacks or delays in spending by the DoD may occur, which could cause delays or cancellations of key government contracts; risks of delays to or the cancellation of our projects as a result of protest actions submitted by our competitors; risks that changes may occur in Federal government (or other applicable) procurement laws, regulations, policies and budgets; risks of the availability of government funding for the Company’s products and services due to performance, cost growth, or other factors, changes in government and customer priorities and requirements (including cost-cutting initiatives, the potential deferral of awards, terminations or reduction of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts resulting from Congressional committee recommendations or automatic sequestration under the Budget Control Act of 2011, as amended); risks that the unmanned aerial systems and unmanned ground sensor markets do not experience significant growth; risks that products we have developed or will develop will become programs of record; risks that we cannot expand our customer base or that our products do not achieve broad acceptance which could impact our ability to achieve our anticipated level of growth; risks of increases in the Federal government initiatives related to in-sourcing; risks related to security breaches, including cyber security attacks and threats or other significant disruptions of our information systems, facilities and infrastructures; risks related to our compliance with applicable contracting and procurement laws, regulations and standards; risks related to the new DoD Cybersecurity Maturity Model Certification; risks relating to the ongoing conflict in Ukraine and the Israeli-Palestinian military conflict; risks to our business in Israel; risks related to our international operations; risks related to contract performance; risks related to failure of our products or services; risks associated with our subcontractors’ or suppliers’ failure to perform their contractual obligations, including the appearance of counterfeit or corrupt parts in our products; changes in the competitive environment (including as a result of bid protests); failure to successfully integrate acquired operations and compete in the marketplace, which could reduce revenues and profit margins; risks that potential future goodwill impairments will adversely affect our operating results; risks that anticipated tax benefits will not be realized in accordance with our expectations; risks that a change in ownership of our stock could cause further limitation to the future utilization of our net operating losses; risks that we may be required to record valuation allowances on our net operating losses which could adversely impact our profitability and financial condition; risks that the current economic environment will adversely impact our business, including with respect to our ability to recruit and retain sufficient numbers of qualified personnel to execute on our programs and contracts, as well as expected contract awards and risks related to increasing interest rates and risks related to the interest rate swap contract to hedge Term SOFR associated with the Company’s Term Loan A; and risks related to natural disasters or severe weather. These and other risk factors are more fully discussed in the Company’s Annual Report on Form 10-K for the period ended December 31, 2023, and in our other filings made with the Securities and Exchange Commission.

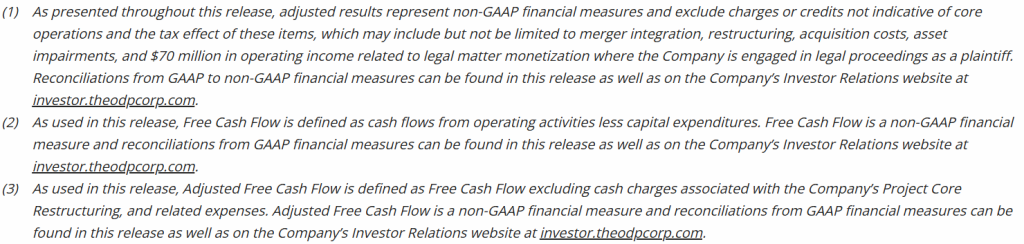

Note Regarding Use of Non-GAAP Financial Measures and Other Performance Metrics This news release contains non-GAAP financial measures, including organic revenue growth rates, Adjusted EPS (computed using income from continuing operations before income taxes, excluding income (loss) from discontinued operations, excluding income (loss) attributable to non-controlling interest, excluding depreciation, amortization of intangible assets, amortization of capitalized contract and development costs, stock-based compensation expense, acquisition and restructuring related items and other, which includes, but is not limited to, legal related items, non-recoverable rates and costs, and foreign transaction gains and losses, less the estimated impact to income taxes) and Adjusted EBITDA (which includes net income (loss) attributable to noncontrolling interest and excludes, among other things, losses and gains from discontinued operations, acquisition and restructuring related items, stock compensation expense, foreign transaction gains and losses, and the associated margin rates). Additional non-GAAP financial measures include Free Cash Flow from Operations computed as Cash Flow from Operations less Capital Expenditures plus proceeds from sale of assets and Adjusted EBITDA related to our KUS and KGS businesses. Kratos believes this information is useful to investors because it provides a basis for measuring the Company’s available capital resources, the actual and forecasted operating performance of the Company’s business and the Company’s cash flow, excluding non-recurring items and non-cash items that would normally be included in the most directly comparable measures calculated and presented in accordance with GAAP. The Company’s management uses these non-GAAP financial measures, along with the most directly comparable GAAP financial measures, in evaluating the Company’s actual and forecasted operating performance, capital resources and cash flow. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP, and investors should carefully evaluate the Company’s financial results calculated in accordance with GAAP and reconciliations to those financial results. In addition, non-GAAP financial measures as reported by the Company may not be comparable to similarly titled amounts reported by other companies. As appropriate, the most directly comparable GAAP financial measures and information reconciling these non-GAAP financial measures to the Company’s financial results prepared in accordance with GAAP are included in this news release.

Another Performance Metric the Company believes is a key performance indicator in our industry is our Book to Bill Ratio as it provides investors with a measure of the amount of bookings or contract awards as compared to the amount of revenues that have been recorded during the period and provides an indicator of how much of the Company’s backlog is being burned or utilized in a certain period. The Book to Bill Ratio is computed as the number of bookings or contract awards in the period divided by the revenues recorded for the same period. The Company believes that the rolling or last twelve months’ Book to Bill Ratio is meaningful since the timing of quarter-to-quarter bookings can vary.

Following the sale of European staffing operations, Q3 revenue down 7.1% year-over-year; nearly flat on an organic basis

Q3 operating earnings of $2.6 million; $11.7 million on an adjusted basis, down 24.5%

Q3 adjusted EBITDA margin increased 20 basis points to 2.5%

Company expects sale of European staffing operations, acquisition of Motion Recruitment Partners, LLC (“MRP”), ongoing transformation actions to contribute to continued year-over-year EBITDA margin expansion in Q4 2024

TROY, Mich., Nov. 07, 2024 (GLOBE NEWSWIRE) — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced results for the third quarter of 2024.

Peter Quigley, president and chief executive officer, announced revenue for the third quarter of 2024 totaled $1.04 billion, a 7.1% decrease compared to the corresponding quarter of 2023 resulting primarily from the sale of the company’s European staffing operations on January 2, 2024, partially offset by the May 2024 acquisition of MRP. Excluding the impact of the sale of the European staffing operations and the recent acquisition of MRP, revenue was down 0.2% on an organic basis, reflecting a stabilization of year-over-year revenues for the second consecutive quarter despite the continued impact of customers’ more guarded approach to hiring, initiating new projects, and backfilling open roles. MRP revenue added 11.2% to reported Q3 year-over-year revenue growth.

Kelly reported operating earnings in the third quarter of 2024 of $2.6 million, compared to earnings of $0.1 million reported in the third quarter of 2023. Adjusted earnings were $11.7 million in the third quarter of 2024. The $9.1 million increase from reported earnings includes costs related to MRP integration and further aligning processes and technology across the Company, as well as charges related to the acquisition of MRP and the sale of our European staffing operations. The acquisition of MRP added $2.0 million of earnings from operations in the third quarter of 2024. Adjusted earnings in the third quarter of 2023 were $15.5 million. The $15.4 million increase from reported earnings included transformation-related charges. The European staffing operations produced $0.8 million of earnings from operations on an adjusted basis in the third quarter of 2023.

Earnings per share in the third quarter of 2024 were $0.02 compared to earnings per share of $0.18 in the third quarter of 2023. Included in earnings per share in the third quarter of 2024 are costs related to MRP integration and further aligning processes and technology across the Company as well as charges related to the acquisition of MRP and the sale of our European staffing operations, net of tax, of $0.18. Included in the earnings per share in the third quarter of 2023 were $0.32 per share of transformation-related restructuring charges, net of tax. On an adjusted basis, earnings per share were $0.21 in the third quarter of 2024 compared to $0.50 per share in the corresponding quarter of 2023.

“In the third quarter, we remained focused on what we can control as uncertain macroeconomic market conditions persisted, and once again delivered stable year-over-year organic revenue that outpaced the market,” said Quigley. “Contributing to this trend is continued double-digit revenue growth in Education, our ongoing expansion into the market for higher-margin outcome-based solutions in SETT and P&I, and sequential stability in MSP and RPO revenue in OCG. We expect to build on our momentum as we close the year, propelled by our growth and efficiency initiatives which are positioning Kelly to capitalize when staffing demand rebounds and continue delivering above-market performance.”

Kelly also reported that on November 5, its board of directors declared a dividend of $0.075 per share. The dividend is payable on December 4, 2024, to stockholders of record as of the close of business on November 20, 2024.

In conjunction with its third-quarter earnings release, Kelly has published a financial presentation on the Investor Relations page of its public website and will host a conference call at 9 a.m. ET on November 7 to review the results and answer questions. The call may be accessed in one of the following ways:

Via the telephone (877) 692-8955 (toll free) or (234) 720-6979 (caller paid) Enter access code 5728672 After the prompt, please enter “#”

A recording of the conference call will be available after 1:30 p.m. ET on November 7, 2024, at (866) 207-1041 (toll-free) and (402) 970-0847 (caller-paid). The access code is 9480328#. The recording will also be available at kellyservices.com during this period.

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements that are not historical facts, including statements about Kelly’s financial expectations, are forward-looking statements. Factors that could cause actual results to differ materially from those contained in this release include, but are not limited to, (i) changing market and economic conditions, (ii) disruption in the labor market and weakened demand for human capital resulting from technological advances, loss of large corporate customers and government contractor requirements, (iii) the impact of laws and regulations (including federal, state and international tax laws), (iv) unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, (v) litigation and other legal liabilities (including tax liabilities) in excess of our estimates, (vi) our ability to achieve our business’s anticipated growth strategies, (vii) our future business development, results of operations and financial condition, (viii) damage to our brands, (ix) dependency on third parties for the execution of critical functions, (x) conducting business in foreign countries, including foreign currency fluctuations, (xi) availability of temporary workers with appropriate skills required by customers, (xii) cyberattacks or other breaches of network or information technology security, and (xiii) other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “target,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. All information provided in this press release is as of the date of this press release and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 500,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2023 was $4.8 billion. Learn more at kellyservices.com.

BOCA RATON, Fla.–(BUSINESS WIRE)–Nov. 7, 2024– The GEO Group, Inc. (NYSE: GEO) (“GEO”), a leading provider of contracted support services for secure facilities, processing centers, and reentry centers, as well as enhanced in-custody rehabilitation, post-release support, and electronic monitoring programs, reported today its financial results for the third quarter and first nine months of 2024.

Third Quarter 2024 Highlights

Total revenues of $603.1 million

Net Income Attributable to GEO of $0.19 per diluted share

Adjusted Net Income of $0.21 per diluted share

Adjusted EBITDA of $118.6 million

For the third quarter 2024, we reported net income attributable to GEO of $26.3 million, or $0.19 per diluted share, compared to net income attributable to GEO of $24.5 million, or $0.16 per diluted share, for the third quarter 2023. Third quarter 2024 results reflect costs associated with the extinguishment of debt of $2.9 million, pre-tax, $0.4 million in transaction fees, pre-tax, and $0.5 million in close-out expenses, pre-tax. Excluding the costs associated with the extinguishment of debt and other unusual and/or nonrecurring items, we reported adjusted net income for the third quarter 2024 of $29.1 million, or $0.21 per diluted share, compared to $23.6 million, or $0.19 per diluted share, for the third quarter 2023.

We reported total revenues for the third quarter 2024 of $603.1 million compared to $602.8 million for the third quarter 2023. We reported third quarter 2024 Adjusted EBITDA of $118.6 million, compared to $118.7 million for the third quarter 2023.

Third quarter 2024 results reflect lower-than-expected revenues in our Electronic Monitoring and Supervision Services segment, primarily due to the decline in participant counts under the federal government’s Intensive Supervision Appearance Program (“ISAP”). Participant counts under ISAP averaged approximately 177,000 individuals during the third quarter 2024, compared to average ISAP participant counts of approximately 184,000 during the second quarter 2024.

George C. Zoley, Executive Chairman of GEO, said, “While our third quarter results were below our expectations due to lower-than-expected revenues in our Electronic Monitoring and Supervision Services segment, we believe we have several potential sources of upside to our current quarterly run rate, with possible future growth opportunities across our diversified services platform. We have 18,000 available beds across contracted and idle secure services facilities, which if fully activated, would provide significant potential upside to our financial performance. We also believe we have the necessary resources to materially scale up the service levels in our ISAP and air and ground transportation contracts.”

“As we evaluate and pursue future growth opportunities, we remain focused on the disciplined allocation of capital to further reduce our debt, deleverage our balance sheet, and position our company to evaluate options to return capital to shareholders in the future,” Zoley added.

First Nine Months 2024 Highlights

Total revenues of $1.82 billion

Net Income Attributable to GEO of $0.11 per diluted share, reflects costs associated with the extinguishment of debt of $85.3 million, pre-tax

Adjusted Net Income of $0.63 per diluted share

Adjusted EBITDA of $355.5 million

For the first nine months of 2024, we reported net income attributable to GEO of $16.5 million, or $0.11 per diluted share, compared to net income attributable to GEO of $82.1 million, or $0.55 per diluted share, for the first nine months of 2023. Results for the first nine months of 2024 reflect costs associated with the extinguishment of debt of $85.3 million, pre-tax.

Excluding the costs associated with the extinguishment of debt and other unusual and/or nonrecurring items, we reported adjusted net income for the first nine months of 2024 of $82.8 million, or $0.63 per diluted share, compared to $79.8 million, or $0.65 per diluted share, for the first nine months of 2023.

We reported total revenues for the first nine months of 2024 of $1.82 billion compared to $1.80 billion for the first nine months of 2023. We reported Adjusted EBITDA for the first nine months of 2024 of $355.5 million, compared to $378.6 million for the first nine months of 2023.

Financial Guidance

Today, we updated our financial guidance for the fourth quarter and full year 2024. While participant counts under ISAP have been increasing subsequent to the end of the third quarter 2024 to approximately 182,500 currently, and while it is possible ISAP participant counts and utilization of ICE processing center beds may further increase this year, we have updated our fourth quarter 2024 guidance to be largely consistent with our third quarter 2024 results. We expect fourth quarter 2024 Net Income Attributable to GEO to be in a range of $0.19 to $0.22 per diluted share on quarterly revenues of $600 million to $610 million. We expect fourth quarter 2024 Adjusted EBITDA to be in a range of $114 million to $124 million.

For the full year 2024, we expect Net Income Attributable to GEO to be in a range of $0.30 to $0.34 per diluted share, which reflects costs associated with the extinguishment of debt of $87 million, pre-tax. Excluding the costs associated with the extinguishment of debt and other unusual and/or nonrecurring items, we expect full year 2024 Adjusted Net Income to be in a range of $0.80 to $0.84 per diluted share, on annual revenues of approximately $2.42 billion and reflecting an effective tax rate of approximately 23 percent, inclusive of known discrete items. We expect our full year 2024 Adjusted EBITDA to be between $470 million and $480 million.

Recent Developments

On October 4, 2024, we announced that U.S. Immigration and Customs Enforcement (“ICE”) exercised the first five-year option period extending the contract for the GEO-owned 1,940-bed Adelanto ICE Processing Center in California (the “Adelanto Center”) through December 19, 2029. ICE and GEO entered into a 15-year contract on December 19, 2019, for the provision of secure residential housing and support care services at the Adelanto Center, consisting of a five-year base period followed by two five-year option periods. The Adelanto Center employs approximately 350 employees.

Balance Sheet

At the end of the third quarter 2024, our net debt totaled approximately $1.69 billion, and our net leverage was approximately 3.5 times Adjusted EBITDA. We ended the third quarter 2024 with approximately $71 million in cash and cash equivalents and approximately $280 million in total available liquidity.

Conference Call Information

We have scheduled a conference call and webcast for today at 11:00 AM (Eastern Time) to discuss our third quarter 2024 financial results as well as our outlook. The call-in number for the U.S. is 1-877-250-1553 and the international call-in number is 1-412-542-4145. In addition, a live audio webcast of the conference call may be accessed on the Webcasts section under the News, Events and Reports tab of GEO’s investor relations webpage at investors.geogroup.com. A replay of the webcast will be available on the website for one year. A telephonic replay of the conference call will be available through November 14, 2024, at 1-877-344-7529 (U.S.) and 1-412-317-0088 (International). The participant passcode for the telephonic replay is 7169822.

About The GEO Group

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 99 facilities totaling approximately 80,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Reconciliation Tables and Supplemental Information

GEO has made available Supplemental Information which contains reconciliation tables of Net Income Attributable to GEO to Adjusted Net Income, and Net Income to EBITDA and Adjusted EBITDA, along with supplemental financial and operational information on GEO’s business and other important operating metrics. The reconciliation tables are also presented herein. Please see the section below titled “Note to Reconciliation Tables and Supplemental Disclosure – Important Information on GEO’s Non-GAAP Financial Measures” for information on how GEO defines these supplemental Non-GAAP financial measures and reconciles them to the most directly comparable GAAP measures. GEO’s Reconciliation Tables can be found herein and in GEO’s Supplemental Information available on GEO’s investor webpage at investors.geogroup.com.

Note to Reconciliation Tables and Supplemental Disclosure – Important Information on GEO’s Non-GAAP Financial Measures

Adjusted Net Income, EBITDA, and Adjusted EBITDA are non-GAAP financial measures that are presented as supplemental disclosures. GEO has presented herein certain forward-looking statements about GEO’s future financial performance that include non-GAAP financial measures, including Net Debt, Net Leverage, and Adjusted EBITDA. The determination of the amounts that are included or excluded from these non-GAAP financial measures is a matter of management judgment and depends upon, among other factors, the nature of the underlying expense or income amounts recognized in a given period.

While we have provided a high level reconciliation for the guidance ranges for full year 2024, we are unable to present a more detailed quantitative reconciliation of the forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because management cannot reliably predict all of the necessary components of such GAAP measures. The quantitative reconciliation of the forward-looking non-GAAP financial measures will be provided for completed annual and quarterly periods, as applicable, calculated in a consistent manner with the quantitative reconciliation of non-GAAP financial measures previously reported for completed annual and quarterly periods.

Net Debt is defined as gross principal debt less cash from restricted subsidiaries. Net Leverage is defined as Net Debt divided by Adjusted EBITDA.

EBITDA is defined as net income adjusted by adding provisions/(benefit) for income tax, interest expense, net of interest income, and depreciation and amortization. Adjusted EBITDA is defined as EBITDA adjusted for (gain)/loss on asset divestitures/impairment, pre-tax, net loss attributable to non-controlling interests, stock-based compensation expenses, pre-tax, start-up expenses, pre-tax, ATM equity program expenses, pre-tax, transaction fees, pre-tax, close-out expenses, pre-tax, other non-cash revenue and expenses, pre-tax, and certain other adjustments as defined from time to time.

Given the nature of our business as a real estate owner and operator, we believe that EBITDA and Adjusted EBITDA are helpful to investors as measures of our operational performance because they provide an indication of our ability to incur and service debt, to satisfy general operating expenses, to make capital expenditures, and to fund other cash needs or reinvest cash into our business.

We believe that by removing the impact of our asset base (primarily depreciation and amortization) and excluding certain non-cash charges, amounts spent on interest and taxes, and certain other charges that are highly variable from year to year, EBITDA and Adjusted EBITDA provide our investors with performance measures that reflect the impact to operations from trends in occupancy rates, per diem rates and operating costs, providing a perspective not immediately apparent from net income.

The adjustments we make to derive the non-GAAP measures of EBITDA and Adjusted EBITDA exclude items which may cause short-term fluctuations in income from continuing operations and which we do not consider to be the fundamental attributes or primary drivers of our business plan and they do not affect our overall long-term operating performance.

EBITDA and Adjusted EBITDA provide disclosure on the same basis as that used by our management and provide consistency in our financial reporting, facilitate internal and external comparisons of our historical operating performance and our business units and provide continuity to investors for comparability purposes.

Adjusted Net Income is defined as net income/(loss) attributable to GEO adjusted for certain items which by their nature are not comparable from period to period or that tend to obscure GEO’s actual operating performance, including for the periods presented (gain)/loss on asset divestitures/impairment, pre-tax, loss on the extinguishment of debt, pre-tax, start-up expenses, pre-tax, transaction fees, pre-tax, ATM equity program expenses, pre-tax, close-out expenses, pre-tax, discrete tax benefit, and tax effect of adjustments to net income attributable to GEO.

Safe-Harbor Statement

This press release contains forward-looking statements regarding future events and future performance of GEO that involve risks and uncertainties that could materially and adversely affect actual results, including statements regarding GEO’s financial guidance for the full year and fourth quarter of 2024, statements regarding GEO’s focus on reducing net debt, deleveraging its balance sheet, positioning itself to explore options to return capital to shareholders in the future, and pursuing a disciplined allocation of capital to enhance long-term value for shareholders, executing on GEO’s strategic priorities, pursuing quality growth opportunities, and the upside this could have on GEO’s quarterly run-rate, and GEO’s ability to scale up the delivery of diversified services to support the future needs of its government agency partners. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” or “continue” or the negative of such words and similar expressions. Risks and uncertainties that could cause actual results to vary from current expectations and forward-looking statements contained in this press release include, but are not limited to: (1) GEO’s ability to meet its financial guidance for 2024 given the various risks to which its business is exposed; (2) GEO’s ability to deleverage and repay, refinance or otherwise address its debt maturities in an amount and on terms commercially acceptable to GEO, and on the timeline it expects or at all; (3) GEO’s ability to identify and successfully complete any potential sales of company-owned assets and businesses or potential acquisitions of assets or businesses on commercially advantageous terms on a timely basis, or at all; (4) changes in federal and state government policy, orders, directives, legislation and regulations that affect public-private partnerships with respect to secure, correctional and detention facilities, processing centers and reentry centers, including the timing and scope of implementation of President Biden’s Executive Order directing the U.S. Attorney General not to renew the U.S. Department of Justice contracts with privately operated criminal detention facilities; (5) changes in federal immigration policy; (6) public and political opposition to the use of public-private partnerships with respect to secure correctional and detention facilities, processing centers and reentry centers; (7) any continuing impact of the COVID-19 global pandemic on GEO and GEO’s ability to mitigate the risks associated with COVID-19; (8) GEO’s ability to sustain or improve company-wide occupancy rates at its facilities; (9) fluctuations in GEO’s operating results, including as a result of contract terminations, contract renegotiations, changes in occupancy levels and increases in GEO’s operating costs; (10) general economic and market conditions, including changes to governmental budgets and its impact on new contract terms, contract renewals, renegotiations, per diem rates, fixed payment provisions, and occupancy levels; (11) GEO’s ability to address inflationary pressures related to labor related expenses and other operating costs; (12) GEO’s ability to timely open facilities as planned, profitably manage such facilities and successfully integrate such facilities into GEO’s operations without substantial costs; (13) GEO’s ability to win management contracts for which it has submitted proposals and to retain existing management contracts; (14) risks associated with GEO’s ability to control operating costs associated with contract start-ups; (15) GEO’s ability to successfully pursue growth opportunities and continue to create shareholder value; (16) GEO’s ability to obtain financing or access the capital markets in the future on acceptable terms or at all; and (17) other factors contained in GEO’s Securities and Exchange Commission periodic filings, including its Form 10-K, 10-Q and 8-K reports, many of which are difficult to predict and outside of GEO’s control.

Cost Management and Higher Occupancy Continue To Drive Positive Financial Performance Raises Full Year Financial Guidance

BRENTWOOD, Tenn., Nov. 06, 2024 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today its third quarter 2024 financial results.

Financial Highlights – Third Quarter 2024

Total revenue of $491.6 million, an increase of 2%

Net income of $21.1 million, an increase of 52%

Adjusted net income of $22.4 million, an increase of 44%

Diluted earnings per share of $0.19; Adjusted Diluted EPS of $0.20

Normalized FFO per diluted share of $0.43, an increase of 23%

Adjusted EBITDA of $83.3 million, an increase of 11%

Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, commented, “CoreCivic’s financial results for the third quarter of 2024 demonstrate our continued strong operating momentum. We achieved notable improvement in our operating margin compared with the prior year quarter through our continued cost management diligence and the strong demand for our essential services, evidenced by the increase in our compensated occupancy to 75.2% in the current quarter from 72.0% in the prior year. Operating margins are particularly impacted by occupancy considering operating leverage in our business.”

“Beyond our solid quarterly financial results,” Hininger added, “CoreCivic’s balance sheet remains strong, and we are pleased with the continued execution of our capital strategy, ending the quarter with leverage, measured as net debt to Adjusted EBITDA, at 2.2x for the trailing twelve months – placing us below our target leverage range of 2.25x to 2.75x that we established in August 2020. As we look forward to opportunities in 2025 and beyond, CoreCivic is ready to respond quickly and flexibly to our governmental partner’s needs due to our talented and experienced teams, healthy balance sheet and readily available and modern bed capacity.”

Third Quarter 2024 Financial Results Compared With Third Quarter 2023

Net income in the third quarter of 2024 was $21.1 million, or $0.19 per diluted share, compared with net income in the third quarter of 2023 of $13.9 million, or $0.12 per diluted share. When adjusted for special items, Adjusted net income for the third quarter of 2024 improved to $22.4 million, or $0.20 per diluted share (Adjusted Diluted EPS), compared with Adjusted net income in the third quarter of 2023 of $15.6 million, or $0.14 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The increased adjusted earnings per share amounts resulted from modestly higher revenue, driven by higher populations and per diem rates at our facilities serving state and local populations, combined with cost containment efforts, lower interest expense and a decrease in shares of our common stock outstanding as a result of our share repurchase program. These earnings increases were achieved despite being partially offset by the expiration of our lease with the California Department of Corrections and Rehabilitation (CDCR) at our California City Correctional Center on March 31, 2024, which accounted for a $0.05 per share reduction during the third quarter, as well as the previously disclosed early termination of our contract with U.S. Immigration & Customs Enforcement (ICE) at the South Texas Family Residential Center effective August 9, 2024. Third quarter 2024 financial results at the South Texas facility were favorably impacted by the accelerated recognition of the remaining deferred revenue of $5.7 million, and due to the rapid ramp-down in detainee populations in July, resulting in the elimination of most operating expenses, though we continued to generate full fixed contractual revenue through the termination date, resulting in a minimal impact on per share results for the third quarter of 2024 compared with the third quarter of 2023.

Operating leverage stemming from improving facility occupancy combined with cost management initiatives continue to yield positive financial results and operating performance. In particular, expenses related to labor attraction and retention, such as registry nursing and temporary labor resources, including associated travel expenses, overtime and incentives, declined meaningfully from the prior year quarter, as well as sequentially.

Revenue from ICE, our largest government partner, decreased 3.4% compared with the third quarter of 2023 and by 7.5% compared with the second quarter of 2024. This decline in revenue from ICE primarily reflects the termination of our ICE contract at the South Texas Family Residential Facility effective August 9, 2024. Excluding the South Texas facility, our revenue with ICE increased 10.9% compared with the third quarter of the prior year and increased 4.6% compared with the prior quarter. During the third quarter of 2024, revenue from ICE was $139.7 million compared to $144.6 million during the third quarter of 2023 and $151.0 million during the second quarter of 2024.

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $81.4 million in the third quarter of 2024, compared with $72.8 million in the third quarter of 2023. Adjusted EBITDA, which excludes special items, was $83.3 million in the third quarter of 2024, compared with $75.2 million in the third quarter of 2023. The increase in Adjusted EBITDA was attributable to an increase in occupancy, combined with a general reduction in temporary staffing incentives and related labor costs, partially offset by the expiration of the lease with the CDCR at the California City facility.

Funds From Operations (FFO) for the third quarter of 2024 was $47.1 million, compared with $38.5 million in the third quarter of 2023. Normalized FFO, which excludes special items, increased to $47.6 million, or $0.43 per diluted share, in the third quarter of 2024, compared with $40.5 million, or $0.35 per diluted share, in the third quarter of 2023, representing an increase in Normalized FFO per share of 23%. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA, further improved by a reduction in interest expense resulting from our debt reduction strategy that is not reflected in Adjusted EBITDA, as well as a 3% reduction in weighted average shares outstanding compared with the prior year quarter. Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Capital Strategy

Share Repurchases. Our Board of Directors has approved a share repurchase program authorizing the Company to repurchase up to $350.0 million of our common stock, including an additional $125.0 million approved on May 16, 2024. During 2024, we have repurchased 4.0 million shares of common stock under the share repurchase program at an aggregate purchase price of $59.5 million, although we did not repurchase any shares during the third quarter of 2024. Since the share repurchase program was authorized in May 2022, through September 30, 2024, we have repurchased a total of 14.1 million shares at an aggregate price of $172.1 million, or $12.20 per share, excluding fees, commissions and other costs related to the repurchases.

As of September 30, 2024, we had $177.9 million remaining under the share repurchase program. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the Board of Directors from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our Board of Directors in its discretion at any time. As a result of ICE’s discontinued use of the South Texas Family Residential Center and the impact such discontinuation will have on our leverage ratios, we intend to prioritize the use of our free cash flow to further reduce our debt, although we may exercise discretion in repurchasing additional shares of our common stock in accordance with the repurchase program.

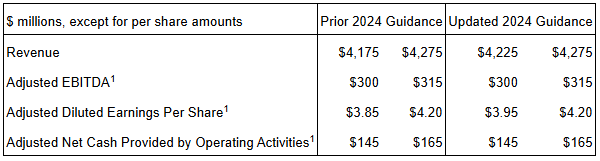

2024 Financial Guidance

Based on current business conditions, we are providing the following updates to our financial guidance for the full year 2024:

New Guidance Full Year 2024

Prior Guidance Full Year 2024

Net income

$55.5 million to $61.5 million

$42.0 million to $50.4 million

Adjusted Net Income

$78.0 million to $84.0 million

$65.6 million to $73.6 million

Diluted EPS

$0.49 to $0.55

$0.37 to $0.45

Adjusted Diluted EPS

$0.69 to $0.75

$0.58 to $0.66

FFO per diluted share

$1.39 to $1.45

$1.28 to $1.36

Normalized FFO per diluted share

$1.59 to $1.65

$1.48 to $1.56

EBITDA

$284.3 million to $288.3 million

$268.0 million to $274.6 million

Adjusted EBITDA

$317.0 million to $321.0 million

$302.4 million to $308.4 million

During 2024, we expect to invest $70.0 million to $76.0 million in capital expenditures, consisting of $30.0 million to $31.0 million in maintenance capital expenditures on real estate assets, $32.0 million to $35.0 million for maintenance capital expenditures on other assets and information technology, and $8.0 million to $10.0 million for other capital investments, including costs to prepare an idle facility for activation in the possible event an opportunity presents. These amounts are unchanged from our prior guidance.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the third quarter of 2024. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the fourth quarter of 2024. Written materials used in the investor presentations will also be available on our website beginning on or about November 26, 2024. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 8:30 a.m. central time (9:30 a.m. eastern time) on Thursday, November 7, 2024, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. To participate via telephone and join the call live, please register in advance here https://registrations.events/direct/NTM123920992. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for over 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements