CULVER CITY, Calif., Aug. 13, 2024 (GLOBE NEWSWIRE) — Snail, Inc. (NASDAQ: SNAL) (“Snail” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment, today announced financial results for its second quarter ended June 30, 2024.

Tony Tian, Co-Chief Executive Officer commented, “I’m honored to lead Snail alongside an amazing team as we continue to build upon the company’s incredible legacy of innovation and creativity. Our unwavering passion for delivering exceptional gaming experiences, as showcased by the phenomenal launch of ARK: Survival Ascended, will continue to propel Snail to future successes and victories. Looking ahead, we are excited to expand the reach of our premium mods and introduce new content that will delight our growing community of players worldwide.”

Second Quarter 2024 Highlights:

ARK: Survival Ascended and ARK: Survival Evolved

On October 25, 2023, the Company launched its flagship remake of the ARK franchise leveraging Unreal Engine 5’s stunning graphics and introduced a game-altering cross-platform modding system, ushering in a new era of creativity.

In the three and six months ended June 30, 2024, ARK: Survival Evolved and ARK: Survival Ascended combined for an average total of 218,241 and 213,690 daily active users (“DAUs”) on the Steam and Epic platforms, respectively, as compared to 240,522 and 258,235 in the three and six months ended June 30, 2023, respectively.

Through June 30, 2024, our ARK franchise game has been played for 3.7 billion hours with an average playing time per user of 161 hours and with the top 21.1% of all players spending over 100 hours in the game, according to data from the Steam platform.

Since its launch, ARK: Survival Ascended sold approximately 2.5 million units and has an average of 108,515 daily active users (“DAUs”) with a peak of 307,875 DAUs.

ARK: Survival Evolved averaged a total of approximately 131,927 DAUs and sold approximately 0.5 million units in the second quarter of 2024.

In the second quarter of 2024, the Company successfully launched Bellwright, a medieval survival game, Bob’s Tall Tales DLC for ARK: Survival Ascended and the Power Rangers premium mod for ARK: Survival Ascended . Furthermore, a full-size DLC expansion, Scorched Earth, was made available to all ARK: Survival Ascended owners.

Net revenue for the three months ended June 30, 2024 was $21.6 million compared to $9.9 million in the three months ended June 30, 2023. The increase in net revenue was due to an increase in total Ark sales of $10.0 million, an increase in sales of the Company’s other games of $3.9 million driven by the release of Bellwright, partially offset by a decrease in Ark Mobile sales of $0.3 million and an increase in deferred revenue of $1.9 million related to the Ark franchise.

Net income for the three months ended June 30, 2024 was $2.3 million compared to a net loss of $4.1 million for the three months ended June 30, 2023. The improvement in net income is due to an increase in net revenue of $11.7 million, decreased general and administrative expenses of $1.2 million, and an increase in total other income (expense) of $0.5 million, partially offset by increased research and development expenses of $0.7 million, increased advertising and marketing expenses of $0.5 million, increased costs of revenue of $4.2 million and a decrease in benefit from income taxes of $1.7 million.

Bookings for the three months ended June 30, 2024 was $22.9 million as compared to $9.3 million for the three months ended June 30, 2023, the increase was primarily due to the release of ARK: Survival Ascended in the fourth quarter of 2023, and the release of Bobs Tall Tales and Bellwright along with the ARK: Survival Ascended DLC, Scorched Earth in April 2024. In addition to increased net sales of the aforementioned titles, the Company deferred approximately $7.1 million in revenue during the three months ended June 30, 2024 for the ARK: Survival Ascended DLC’s and parts of Bobs Tall Tales which have not yet released; partially offset by the recognition of $5.6 million for the release of Scorched Earth.

Earnings before interest, taxes, depreciation and amortization (“EBITDA”) for the three months ended June 30, 2024 was $3.1 million compared to a loss of $4.8 million in the prior year period. The increase was due to the improvement in net income of $6.4 million and a decrease in the benefit from income taxes of $1.7 million.

As of June 30, 2024, unrestricted cash was $15.5 million.

Use of Non-GAAP Financial Measures

In addition to the financial results determined in accordance with U.S. generally accepted accounting principles, or GAAP, Snail believes Bookings and EBITDA, as non-GAAP measures, are useful in evaluating its operating performance. Bookings and EBITDA are non-GAAP financial measures that are presented as supplemental disclosures and should not be construed as alternatives to net income (loss) or revenue as indicators of operating performance, nor as alternatives to cash flow provided by operating activities as measures of liquidity, both as determined in accordance with GAAP. Snail supplementally presents Bookings and EBITDA because they are key operating measures used by management to assess financial performance. Bookings adjusts for the impact of deferrals and, Snail believes, provides a useful indicator of sales in a given period. EBITDA adjusts for items that Snail believes do not reflect the ongoing operating performance of its business, such as certain non-cash items, unusual or infrequent items or items that change from period to period without any material relevance to its operating performance. Management believes Bookings and EBITDA are useful to investors and analysts in highlighting trends in Snail’s operating performance, while other measures can differ significantly depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which Snail operates and capital investments.

Bookings is defined as the net amount of products and services sold digitally or physically in the period. Bookings is equal to revenue, excluding the impact from deferrals. Below is a reconciliation of total net revenue to Bookings, the closest GAAP financial measure.

Net sales of $49.2 million; up 25.3% year-over-year driven by volume growth of Lifeway Kefir

19th consecutive quarter of year-over-year growth

MORTON GROVE, Ill., Aug. 13, 2024 /PRNewswire/ — Lifeway Foods, Inc. (Nasdaq: LWAY) (“Lifeway” or “the Company”), a leading U.S. supplier of kefir and fermented probiotic products to support the microbiome, today reported financial results for the second quarter ended June 30, 2024.

“Our incredible momentum continued in the second quarter as we delivered our 19th consecutive quarter of net sales growth and our 5th consecutive quarter breaking the Lifeway record on the topline,” commented Julie Smolyansky, President and Chief Executive Officer of Lifeway Foods. “Our record net sales of $49.2 million were up more than 25% year-over-year, driven by continued volume growth in our flagship Lifeway drinkable kefir. Demand for bioavailable foods like Lifeway Kefir and Farmer Cheese is soaring and our customers further demonstrated their loyalty to our premium, healthy offerings. Notably, we delivered nearly $50 million in net sales, a remarkable milestone that we look forward to surpassing, and we also outperformed our previous quarterly sales record by more than 10%. Our amazing results on the topline demonstrate the effectiveness of our sales and marketing investments at driving trial, capturing new customers and accelerating velocities of our core products. Accompanying the very strong, volume-led topline growth, we continued to enhance our profitability profile with solid gross margins and strong net income growth, a testament to the seamless operational execution of our whole Lifeway team. We are thrilled with our results in the first half of 2024, and will continue to strategically invest behind the Lifeway brand to drive velocities, win new customers and position ourself to deliver more outstanding performances through the second half of this year and beyond.”

Second Quarter 2024 Results

Net sales were $49.2 million for the second quarter ended June 30, 2024, an increase of $10.0 million or 25.3% from the same period in 2023. The net sales increase was primarily driven by higher volumes of our branded drinkable kefir.

Gross profit as a percentage of net sales was 27.0% for the second quarter ended June 30, 2024.

Selling, general and administrative expenses as a percentage of net sales were 15.8% for the second quarter ended June 30, 2024.

The Company reported net income of $3.8 million or $0.26 per basic and $0.25 per diluted common share for the second quarter ended June 30, 2024 compared to net income of $3.2 million or $0.22 per basic and $0.21 per diluted common share during the same period in 2023.

Conference Call and Webcast A pre-recorded conference call and webcast with Julie Smolyansky discussing these results with additional comments and details is available through the “Investor Relations” section of the Company’s website at https://lifewaykefir.com/webinars-reports/ and will also be available for replay.

About Lifeway Foods, Inc. Lifeway Foods, Inc., which has been recognized as one of Forbes’ Best Small Companies, is America’s leading supplier of the probiotic, fermented beverage known as kefir. In addition to its line of drinkable kefir, the company also produces a variety of cheeses and a ProBugs line for kids. Lifeway’s tart and tangy fermented dairy products are now sold across the United States, Mexico, Ireland and France. Learn how Lifeway is good for more than just you at lifewayfoods.com.

Forward-Looking Statements

This release (and oral statements made regarding the subjects of this release) contains “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995 regarding, among other things, future operating and financial performance, product development, market position, business strategy and objectives. These statements use words, and variations of words, such as “continue,” “build,” “future,” “increase,” “drive,” “believe,” “look,” “ahead,” “confident,” “deliver,” “outlook,” “expect,” and “predict.” Other examples of forward-looking statements may include, but are not limited to, (i) statements of Company plans and objectives, including the introduction of new products, or estimates or predictions of actions by customers or suppliers, (ii) statements of future economic performance, and (III) statements of assumptions underlying other statements and statements about Lifeway or its business. You are cautioned not to rely on these forward-looking statements. These statements are based on current expectations of future events and thus are inherently subject to uncertainty. If underlying assumptions prove inaccurate or known or unknown risks or uncertainties materialize, actual results could vary materially from Lifeway’s expectations and projections. These risks, uncertainties, and other factors include: price competition; the decisions of customers or consumers; the actions of competitors; changes in the pricing of commodities; the effects of government regulation; possible delays in the introduction of new products; and customer acceptance of products and services. A further list and description of these risks, uncertainties, and other factors can be found in Lifeway’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023, and the Company’s subsequent filings with the SEC. Copies of these filings are available online at https://www.sec.gov, http://lifewaykefir.com/investor-relations/, or on request from Lifeway. Information in this release is as of the dates and time periods indicated herein, and Lifeway does not undertake to update any of the information contained in these materials, except as required by law. Accordingly, YOU SHOULD NOT RELY ON THE ACCURACY OF ANY OF THE STATEMENTS OR OTHER INFORMATION CONTAINED IN ANY ARCHIVED PRESS RELEASE.

Media: Derek Miller Vice President of Communications, Lifeway Foods Email: derekm@lifeway.net

General inquiries: Lifeway Foods, Inc. Phone: 847-967-1010 Email: info@lifeway.net

NEW YORK, August 12, 2024 /PRNewswire/ — Bit Digital, Inc. (Nasdaq: BTBT) (“Bit Digital” or the “Company”), a sustainable platform for digital assets and artificial intelligence (“AI”) infrastructure headquartered in New York, announced today that it will release its Second Quarter 2024 results on Monday, August 19, 2024, after the stock market closes. Senior management will host a live webcast and conference call to review the results on Tuesday, August 20, 2024, at 10 a.m. ET.

To register for the earnings call, please click here. Additionally, participants can join the conference call by dialing 1-800-289-0459 (passcode: 633917).

The Company will issue a press release regarding Second Quarter 2024 earnings prior to the conference call. The press release will be posted on the Bit Digital website at www.bit-digital.com.

About Bit Digital

Bit Digital, Inc. is a sustainable platform for digital assets and artificial intelligence (“AI”) infrastructure headquartered in New York City. Our bitcoin mining operations are located in the US, Canada, and Iceland. For additional information, please contact ir@bit-digital.com or visit our website at www.bit-digital.com.

Investor Notice

Investing in our securities involves a high degree of risk. Before making an investment decision, you should carefully consider the risks, uncertainties and forward-looking statements described under “Risk Factors” in Item 3.D of our most recent Annual Report on Form 20-F for the fiscal year ended December 31, 2023. If any material risk was to occur, our business, financial condition or results of operations would likely suffer. In that event, the value of our securities could decline and you could lose part or all of your investment. The risks and uncertainties we describe are not the only ones facing us. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations. In addition, our past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results in the future. Future changes in the network-wide mining difficulty rate or bitcoin hash rate may also materially affect the future performance of Bit Digital’s production of bitcoin. Actual operating results will vary depending on many factors including network difficulty rate, total hash rate of the network, the operations of our facilities, the status of our miners, and other factors.

Safe Harbor Statement

This press release may contain certain “forward-looking statements” relating to the business of Bit Digital, Inc., and its subsidiary companies. All statements, other than statements of historical fact included herein are “forward-looking statements.” These forward-looking statements are often identified by the use of forward-looking terminology such as “believes,” “expects,” or similar expressions, involving known and unknown risks and uncertainties. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. Investors should not place undue reliance on these forward-looking statements, which speak only as of the date of this press release. The Company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in the Company’s periodic reports that are filed with the Securities and Exchange Commission and available on its website at http://www.sec.gov. All forward-looking statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by these factors. Other than as required under the securities laws, the Company does not assume a duty to update these forward-looking statements.

Company delivers 66% year-over-year revenue growth with record profitability at new plant, raises full year guidance

Secured ~3,000 orders, including first tank car conversion order

CHICAGO, Aug. 12, 2024 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL) (“FreightCar America” or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today reported results for the second quarter ended June 30, 2024.

Second Quarter 2024 Highlights

Revenues of $147.4 million on 1,159 railcar deliveries, an increase of 66% compared to revenues of $88.6 million on 760 railcar deliveries in the second quarter of 2023

Gross margin of 12.5% with gross profit of $18.4 million, compared to gross margin of 14.6% with gross profit of $13.0 million in the second quarter of 2023

Net Income of $8.2 million, or $0.11 per diluted share and Adjusted net income of $6.3 million, or $0.05 per diluted share, accounting primarily for a non-cash item associated with a change in fair market value of warrant liability and a cash item associated with a litigation settlement

Adjusted EBITDA of $12.1 million, compared to Adjusted EBITDA of $8.0 million in the second quarter of 2023

Delivered its 10,000th railcar manufactured at the Castaños facility

Received net orders for approximately 3,000 railcars within the quarter, including a multi-year order to convert over 1,000 tanks cars

“We are very pleased to report our strongest performance yet for revenue, gross profit and Adjusted EBITDA since opening our state-of-the-art facility in 2020. Importantly, these results follow the previously reported 99% growth in revenue and 192% growth in Adjusted EBITDA in the first quarter,” commented Nick Randall, President and Chief Executive Officer of FreightCar America. “Our multiyear turnaround has been a tremendous success, and our focus is on driving growth across our diversified product portfolio as we continue to maximize efficiencies across our value streams.”

Randall continued, “We built a world-class manufacturing campus that is both efficient and flexible. Our customers see this as evidenced by our largest order intake since starting the facility and our recently announced milestone of shipping our 10,000th railcar manufactured at the campus. Furthermore, and consistent with our growth plans, we are pleased to also announce that our order backlog now includes tank cars. Tank cars represent a very important part of the market and are fully aligned with our growth strategy. In summary, we are pleased with the quarter, the year-to-date, and especially with where we see ourselves headed.”

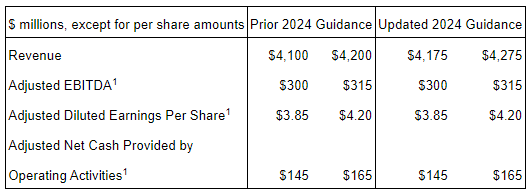

Fiscal Year 2024 Outlook

The Company has updated its outlook for fiscal year 2024 as follows:

Fiscal 2024 Outlook

Year-over-Year Growth at Midpoint

Revenue

$560 – $600 million

62.0%

Adjusted EBITDA

$35 – $39 million

84.1%

Railcar Deliveries

4,300 – 4,700 Railcars

48.9%

Mike Riordan, Chief Financial Officer of FreightCar America, commented, “With our facility complete and all production lines fully operational, we are well on track to achieve the operating performance we envisioned. Given this, combined with the significant order activity in the second quarter, we are raising our full year revenue and delivery guidance to between $560 million and $600 million and 4,300 to 4,700 railcars, respectively. Further, we are increasing our full year Adjusted EBITDA guidance to between $35 million and $39 million. With a strong pipeline of orders, we are well-positioned to leverage our operational efficiencies and cash flow generation to deliver profitable growth for our shareholders.”

Second Quarter 2024 Conference Call & Webcast Information

The Company will host a conference call and live webcast on Tuesday, August 13 at 11:00 a.m. (Eastern Time) to discuss its second quarter 2024 financial results. FreightCar America invites shareholders and other interested parties to listen to its financial results conference call via the following live and recorded methods:

Teleconference: Dial-in numbers for the live Conference Call are (877) 407-0789 or (201) 689-8562. Please call in at least 10 minutes prior to the start time of the call. An audio replay may be accessed at (844) 512-2921 or (412) 317-6671; Passcode: 13747591.

About FreightCar America

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Forward-Looking Statements

This press release contains statements relating to our expected financial performance, financial condition, and/or future business prospects, events and/or plans that are “forward-looking statements” as defined under the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent our estimates and assumptions only as of the date of this press release. Our actual results may differ materially from the results described in or anticipated by our forward-looking statements due to certain risks and uncertainties. These risks and uncertainties relate to, among other things, the cyclical nature of our business; adverse economic and market conditions including inflation; material disruption in the movement of rail traffic for deliveries; fluctuating costs of raw materials including steel and aluminum; delays in the delivery of raw materials; our ability to maintain relationships with our suppliers of railcar components; our reliance upon a small number of customers that represent a large percentage of our sales; the variable purchase patterns of our customers and the timing of completion, delivery and customer acceptance of orders; the highly competitive nature of our industry; the risk of lack of acceptance of our new railcar offerings, and other competitive factors. The factors listed above are not exhaustive. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them. We expressly disclaim any duty to provide updates to any forward-looking statements made in this press release, whether as a result of new information, future events or otherwise.

Non-GAAP Financial Measures

This press release includes measures not derived in accordance with generally accepted accounting principles (“GAAP”), such as EBITDA, Adjusted EBITDA, Adjusted net loss and Adjusted EPS. These non-GAAP measures should not be considered in isolation or as a substitute for any measure derived in accordance with GAAP and may also be inconsistent with similar measures presented by other companies. Reconciliations of these measures to the applicable most closely comparable GAAP measures, and reasons for the Company’s use of these measures, are presented in the attached pages.

Q2 operating earnings of $12.2 million; $28.1 million on an adjusted basis, up 95%

Q2 revenue down following sale of European staffing operations; up 0.6% on an organic basis

Q2 adjusted EBITDA margin increased 170 basis points to 3.7% driven by meaningful reduction in operating expenses resulting from business transformation initiatives and sale of European staffing operations

Company expects further expansion of EBITDA margin from the May 31, 2024 acquisition of Motion Recruitment Partners, LLC (“MRP”)

TROY, Mich. , Aug. 08, 2024 (GLOBE NEWSWIRE) — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced results for the second quarter of 2024.

Peter Quigley, president and chief executive officer, announced revenue for the second quarter of 2024 totaled $1.06 billion, a 13.1% decrease compared to the corresponding quarter of 2023 resulting primarily from the sale of the company’s European staffing operations on January 2, 2024. Excluding the impact of the sale of the European staffing operations and the recent acquisition of MRP, revenue improved 0.6% on an organic basis reflecting the continuing impact of customers’ more guarded approach to hiring and initiating new projects or capital spending. MRP revenue is included in reported revenue upon acquisition beginning in June 2024 and added 400 bps to reported year-over-year revenue growth.

Kelly reported operating earnings in the second quarter of 2024 of $12.2 million, compared to earnings of $6.2 million reported in the second quarter of 2023. Adjusted earnings were $28.1 million in the second quarter of 2024. The $15.9 million increase from reported earnings includes a loss on the sale of our European staffing operations, charges related to transformation actions and the sale of our European staffing operations, an impairment charge related to excess leased property and a gain on the sale of assets related to the Ayers Group. The acquisition of MRP added $1.5 million of earnings from operations in the second quarter of 2024. Adjusted earnings in the second quarter of 2023 were $14.2 million. The $8.0 million increase from reported earnings included transformation related charges and an asset impairment charge. The European staffing operations produced $1 million of earnings from operations on an adjusted basis in the second quarter of 2023.

Earnings per share in the second quarter of 2024 were $0.12 compared to earnings per share of $0.20 in the second quarter of 2023. Included in earnings per share in the second quarter of 2024 were a loss on the sale of EMEA staffing operations and a gain on the sale of Ayers Group, net of tax of $0.16, as well as transaction costs related to the acquisition of MRP, restructuring charges associated with our transformation and an asset impairment charge, net of tax, of $0.43. Included in the earnings per share in the second quarter of 2023 are $0.16 per share related to restructuring charges and an asset impairment charge, net of tax. On an adjusted basis, earnings per share were $0.71 in the second quarter of 2024, a significant improvement from $0.36 per share in the corresponding quarter of 2023.

“In the second quarter, employers continued to take a cautious approach to hiring, though customer demand stabilized on a sequential basis across much of our business – a development that is reflected in Kelly’s organic revenue for the quarter,” said Quigley. “As we continued to navigate uncertain market conditions, we remained focused on what we can control. Our ongoing growth and efficiency initiatives increased Kelly’s EBITDA margin in the first half of the year to 3.4% on an organic, adjusted basis – at the midpoint of our initial expectation for EBITDA margin expansion which we established one year ago. This improvement, combined with the scale and capabilities we added through our recent acquisition of MRP, position Kelly to accelerate profitable growth as market conditions improve.”

Kelly also reported that on August 7, its board of directors declared a dividend of $0.075 per share. The dividend is payable on September 4, 2024, to stockholders of record as of the close of business on August 21, 2024.

In conjunction with its second-quarter earnings release, Kelly has published a financial presentation on the Investor Relations page of its public website and will host a conference call at 9 a.m. ET on August 8 to review the results and answer questions. The call may be accessed in one of the following ways:

Via the telephone (877) 692-8955 (toll free) or (234) 720-6979 (caller paid) Enter access code 5728672 After the prompt, please enter “#”

A recording of the conference call will be available after 1:30 p.m. ET on August 8, 2024, at (866) 207-1041 (toll-free) and (402) 970-0847 (caller-paid). The access code is 2784290#. The recording will also be available at kellyservices.com during this period.

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements that are not historical facts, including statements about Kelly’s financial expectations, are forward-looking statements. Factors that could cause actual results to differ materially from those contained in this release include, but are not limited to, (i) changing market and economic conditions, (ii) disruption in the labor market and weakened demand for human capital resulting from technological advances, loss of large corporate customers and government contractor requirements, (iii) the impact of laws and regulations (including federal, state and international tax laws), (iv) unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, (v) litigation and other legal liabilities (including tax liabilities) in excess of our estimates, (vi) our ability to achieve our business’s anticipated growth strategies, (vii) our future business development, results of operations and financial condition, (viii) damage to our brands, (ix) dependency on third parties for the execution of critical functions, (x) conducting business in foreign countries, including foreign currency fluctuations, (xi) availability of temporary workers with appropriate skills required by customers, (xii) cyberattacks or other breaches of network or information technology security, and (xiii) other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “target,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. All information provided in this press release is as of the date of this press release and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 500,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2023 was $4.8 billion. Learn more at kellyservices.com.

Continued profitability improvement and stronger pace of new business wins driven by strategic transformation plan

Company reaffirms full year 2024 outlook

CHARLOTTE, N.C., Aug. 07, 2024 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, today reported its financial results for the second quarter ended June 30, 2024.

Highlights

Strategic transformation program drove enhanced results, fourth consecutive quarter of improved year-over-year performance;

Second quarter net sales of $123.0 million, down 1.8% versus prior year, driven primarily by unfavorable foreign exchange impacts and rationalization of unprofitable business in Mobile Solutions;

Second quarter operating loss of $2.1 million, an improvement of 47.5% versus prior year;

Second quarter adjusted EBITDA of $13.4 million, an improvement of 27.6% versus prior year;

Secured new business awards of $34.3 million year-to-date; and

Subsequent to quarter-end, the company executed the sale of its lone non-core plastics plant and used $15.4 million of proceeds to pay down debt.

“NN delivered another quarter of improvement, driven by the execution of our strategic transformation plan which is yielding observable momentum across key focus areas of profitability enhancement, operational performance, and accelerated new business wins,” said Harold Bevis, President and Chief Executive Officer. “Our committed efforts to strengthen profitability were evident in the quarter, as our $13.4 million of adjusted EBITDA reflected solid growth over the prior year, which is the fourth consecutive quarter of year-over-year improvement. On a trailing-twelve-month basis we have delivered adjusted EBITDA of $49.2 million, an improvement of 28.7% year-over-year. Our focus on improved operating performance and productivity has helped drive solid margin expansion, advancing our profitability and overcoming the strategic rationalization of volumes which impacted our top-line.”

Mr. Bevis continued, “We continue to see strong momentum in our commercial efforts as we have won nearly $18 million of new business awards in the second quarter and $97 million over the last six quarters. We are on pace to deliver our 2024 targets for new business wins. The electrical, industrial, and medical markets remain unchanged, healthy, and growing. However, the global auto market is recalibrating the choices of powertrain and low-cost country production.”

Mr. Bevis concluded, “We are pleased with our overall performance for the quarter and remain highly confident in our ability to accelerate our transformation and pace of growth. We are delivering significantly improved plant level performance, which is strengthening our profitability and new business win platform. In the near term, we remain highly focused on optimizing our capital structure and lowering our cost of capital through a strategic refinancing which is currently underway. We are also focusing our commercial growth agenda on expanding our electrical business, across auto and non-auto end markets, as well as our high-value NN Medical business in low-cost geographies. I would like to recognize the efforts of our global team members in supporting our ongoing transformation, as we thank them for delivering results as our improved performance is generated through their hard work.”

Second Quarter GAAP Results Net sales were $123.0 million, a decrease of 1.8% from the second quarter of 2023, which was primarily due to rationalized volume at plants undergoing transformations and unfavorable foreign exchange effects of 0.8% or $1.0 million, partially offset by the net impact of contractual pricing provisions.

Loss from operations was $2.1 million compared to a loss from operations of $4.0 million in the second quarter of 2023. The decrease in loss from operations was primarily due to improved operating performance within several facilities.

Income from operations for Power Solutions was $5.3 million compared to income from operations of $2.6 million for the same period in 2023. Loss from operations for Mobile Solutions was $1.6 million compared to loss from operations of $1.5 million for the same period in 2023.

Net loss was $2.2 million compared to net loss of $14.4 million for the same period in 2023. The decrease in net loss was primarily due to non-cash derivative mark-to-market gains recognized during the current quarter compared to losses recognized in the second quarter of 2023.

Second Quarter Adjusted Results Adjusted income from operations for the second quarter of 2024 was $2.1 million compared to adjusted income from operations of $1.3 million for the same period in 2023. Adjusted EBITDA was $13.4 million, or 10.9% of sales, compared to $10.5 million, or 8.4% of sales, for the same period in 2023.

Adjusted net loss was $0.8 million, or $0.02 per diluted share, compared to adjusted net loss of $3.3 million, or $0.08 per diluted share, for the same period in 2023. Free cash flow was a use of cash of $1.3 million compared to a generation of cash of $3.0 million for the same period in 2023.

Power Solutions Net sales for the second quarter of 2024 were $50.2 million compared to $48.1 million in the second quarter of 2023, an increase of 4.3%, or $2.1 million. The increase in sales was primarily due to higher precious metals pass-through pricing and inflation pricing, partially offset by lower volume during the current quarter.

Adjusted income from operations was $8.0 million compared to adjusted income from operations of $5.6 million in the second quarter of 2023. The increase in adjusted income from operations was primarily due to favorable production volumes and improved operating performance.

Mobile Solutions Net sales for the second quarter of 2024 were $72.9 million compared to $77.2 million in the second quarter of 2023, a decrease of 5.6%, or $4.3 million. The decrease in sales was primarily due to lower volume at facilities undergoing transformations, contractual reduction in customer pricing, and unfavorable foreign exchange effects.

Adjusted loss from operations was $0.7 million compared to adjusted income from operations of $0.2 million in the second quarter of 2023. The decrease in adjusted income from operations was primarily due to lower production volumes.

Updated 2024 Outlook NN is reaffirming its full-year 2024 outlook previously provided in its news release on July 2, 2024.

Revenue in the range of $465 million to $485 million;

Adjusted EBITDA in the range of $47 million to $51 million;

Free cash flow in the range of $8 million to $12 million; and

New business wins in the range of $55 million to $70 million.

Chris Bohnert, Senior Vice President and Chief Financial Officer, commented, “NN continued to make significant progress on its transformation goals in the quarter and we are maintaining our full year 2024 guidance ranges as market fundamentals and our improved operating performance have been in line with our previous expectations. Additionally, optimizing NN’s capital structure and the proactive strategic re-financing of our term loan remains a top priority for our team in the near-term and will be a key next step in our transformational strategy.”

Conference Call NN will discuss its results during its quarterly investor conference call on August 8, 2024, at 10 a.m. ET. The call and supplemental presentation may be accessed via NN’s website, www.nninc.com. The conference call can also be accessed by dialing 1-877-255-4315 or 1-412-317-6579. For those who are unavailable to listen to the live broadcast, a replay will be available shortly after the call until August 8, 2025.

NN discloses in this press release the non-GAAP financial measures of adjusted income (loss) from operations, adjusted EBITDA, adjusted net income (loss), adjusted net income (loss) per diluted common share, and free cash flow. Each of these non-GAAP financial measures provides supplementary information about the impacts of restructuring and integration expense, acquisition and transition expenses, foreign exchange impacts on inter-company loans, amortization of intangibles and deferred financing costs, and other non-operating impacts on our business.

The financial tables found later in this press release include a reconciliation of adjusted income (loss) from operations, adjusted operating margin, adjusted EBITDA, adjusted EBITDA margin, adjusted net income (loss), adjusted net income (loss) per diluted share, free cash flow to the U.S. GAAP financial measures of income (loss) from operations, net income (loss), net income (loss) per diluted common share, and cash provided (used) by operating activities.

About NN, Inc. NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and Asia. For more information about the company and its products, please visit www.nninc.com.

Except for specific historical information, many of the matters discussed in this press release may express or imply projections of revenues or expenditures, statements of plans and objectives or future operations or statements of future economic performance. These statements may discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition, or state other information relating to NN, Inc. (the “Company”) based on current beliefs of management as well as assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “possible,” “potential,” “predict,” “project” or other similar words, phrases or expressions. Forward-looking statements involve a number of risks and uncertainties that are outside of management’s control and that may cause actual results to be materially different from such forward-looking statements. Such factors include, among others, general economic conditions and economic conditions in the industrial sector; the impacts of pandemics, epidemics, disease outbreaks and other public health crises on our financial condition, business operations and liquidity; competitive influences; risks that current customers will commence or increase captive production; risks of capacity underutilization; quality issues; material changes in the costs and availability of raw materials; economic, social, political and geopolitical instability, military conflict, currency fluctuation, and other risks of doing business outside of the United States; inflationary pressures and changes in the cost or availability of materials, supply chain shortages and disruptions, the availability of labor and labor disruptions along the supply chain; our dependence on certain major customers, some of whom are not parties to long-term agreements (and/or are terminable on short notice); the impact of acquisitions and divestitures, as well as expansion of end markets and product offerings; our ability to hire or retain key personnel; the level of our indebtedness; the restrictions contained in our debt agreements; our ability to obtain financing at favorable rates, if at all, and to refinance existing debt as it matures; our ability to secure, maintain or enforce patents or other appropriate protections for our intellectual property; new laws and governmental regulations; the impact of climate change on our operations; and cyber liability or potential liability for breaches of our or our service providers’ information technology systems or business operations disruptions. The foregoing factors should not be construed as exhaustive and should be read in conjunction with the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Company’s filings made with the Securities and Exchange Commission. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law. New risks and uncertainties may emerge from time to time, and it is not possible for the Company to predict their occurrence or how they will affect the Company. The Company qualifies all forward-looking statements by these cautionary statements.

With respect to any non-GAAP financial measures included in the following document, the accompanying information required by SEC Regulation G can be found in the back of this document or in the “Investors” section of the Company’s web site, www.nninc.com, under the heading “News & Events” and subheading “Presentations.”

Investor & Media Contacts: Joe Caminiti or Stephen Poe, Investors Tim Peters or Emma Brandeis, Media NNBR@alpha-ir.com 312-445-2870

BRENTWOOD, Tenn., Aug. 07, 2024 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today its second quarter 2024 financial results.

Financial Highlights – Second Quarter 2024

Total revenue of $490.1 million

CoreCivic Safety revenue of $455.4 million

CoreCivic Community revenue of $30.3 million

CoreCivic Properties revenue of $4.4 million

Net income of $19.0 million; Adjusted Net Income of $21.8 million

Diluted earnings per share of $0.17; Adjusted Diluted EPS of $0.20

Normalized FFO per diluted share of $0.42, an increase of 27%

Adjusted EBITDA of $83.9 million, an increase of 16%

Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, commented, “CoreCivic carried its strong operating momentum into the second quarter of 2024. Revenue increased 6% versus the second quarter of 2023, with federal, state, and local revenues all increasing. Occupancy increased to 74.3% from 70.3% in the prior year quarter, and our cost management initiatives are proving effective.”

“In addition to our solid quarterly financial results,” Hininger added, “we are also proud of our continued progress toward our capital structure targets. During the quarter, we repurchased 1.3 million shares of our common stock for a total cost of $20.1 million. Through a thoughtful and disciplined capital allocation strategy, we ended the quarter with leverage, measured as net debt to Adjusted EBITDA, at 2.5x for the trailing twelve months – placing us at the midpoint of our target leverage range of 2.25x to 2.75x that we established in August 2020. Our balance sheet strength and readily available bed capacity position us well to respond to the dynamics of our industry.”

“Finally, we want to recognize the accomplishments of our South Texas Family Residential Center (South Texas Facility) in Dilley, Texas over the past decade. As we previously disclosed, U.S. Immigrations & Customs Enforcement (ICE) will discontinue using this facility as of August 9, 2024. The South Texas Facility was created in collaboration with ICE and a third-party lessor to address the unique challenges posed by then unprecedented levels of family immigration in 2014. This pioneering facility was initially designed to provide a family-oriented environment, featuring educational, medical, dining and athletic facilities. During 2021, this facility’s mission shifted to detention of single adults. We appreciate the trust placed in CoreCivic to launch this unique facility, and we appreciate our excellent leadership and staff at the South Texas Facility, whom we have offered employment opportunities at other facilities within the CoreCivic portfolio.”

Second Quarter 2024 Financial Results Compared With Second Quarter 2023

Net income in the second quarter of 2024 was $19.0 million, or $0.17 per diluted share, compared with net income in the second quarter of 2023 of $14.8 million, or $0.13 per diluted share. However, when adjusted for special items, Adjusted Net Income for the second quarter of 2024 improved to $21.8 million, or $0.20 per diluted share (Adjusted Diluted EPS), compared with Adjusted Net Income in the second quarter of 2023 of $13.6 million, or $0.12 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The increased adjusted earnings per share amounts resulted from higher federal, state, and local populations, particularly at our facilities serving ICE, combined with lower interest expense and a decrease in shares of common stock outstanding, both resulting from our capital allocation strategy. These earnings increases were achieved despite being partially offset by the expiration of our leases with the California Department of Corrections and Rehabilitation (CDCR) at our California City Correctional Center on March 31, 2024, and with the Oklahoma Department of Corrections (ODC) at our North Fork Correctional Facility on June 30, 2023, which collectively accounted for a per share reduction of $0.06.

We continue to realize improvements in our cost structure, both as a result of operating leverage stemming from improving facility occupancy versus the prior year, as well as from other initiatives, particularly those related to labor attraction and retention. The costs of registry nursing, temporary labor resources, including associated travel expenses, overtime and incentives, declined meaningfully from the prior year quarter as well as sequentially.

Revenue from ICE, our largest government partner, increased 10.5% compared with the second quarter of 2023, when the impact of Title-42 restrictions remained. Under Title 42, which ended May 11, 2023, asylum-seekers and anyone crossing the border without proper documentation or authority were denied entry at the United States border to contain the spread of COVID-19. Revenue from ICE declined slightly versus the first quarter of 2024, reflecting a slight decline in ICE detention populations nationwide. During the second quarter of 2024, revenue from ICE was $151.0 million compared to $136.7 million during the second quarter of 2023, and compared to $153.8 million during the first quarter of 2024.

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $79.8 million in the second quarter of 2024. Adjusted EBITDA, which excludes special items, was $83.9 million in the second quarter of 2024, compared with $72.1 million in the second quarter of 2023. The increase in Adjusted EBITDA was attributable to an increase in occupancy, combined with a general reduction in temporary staffing incentives and related labor costs, partially offset by the expiration of the leases with the CDCR at the California City facility and with the ODC at the North Fork facility.

Funds From Operations (FFO) for the second quarter of 2024 was $43.8 million. Normalized FFO, which excludes special items, increased to $46.6 million, or $0.42 per diluted share, in the second quarter of 2024, compared with $37.8 million, or $0.33 per diluted share, in the second quarter of 2023, representing an increase in Normalized FFO per share of 27%. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA, further improved by a reduction in interest expense resulting from our debt reduction strategy that is not reflected in Adjusted EBITDA, as well as a 2% reduction in weighted average shares outstanding compared with the prior year quarter.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Business Updates

Capital Strategy

Share Repurchases. During 2022, our Board of Directors approved a share repurchase program authorizing the Company to repurchase up to $225.0 million of our common stock. On May 16, 2024, our Board of Directors authorized an additional $125.0 million in shares of our common stock for our share repurchase program, increasing the total aggregate authorization to $350.0 million. During the three months ended June 30, 2024, we repurchased 1.3 million shares of our common stock at an aggregate purchase price of $20.1 million, excluding fees, commissions and other costs related to the repurchases. Since the share repurchase program was authorized, through June 30, 2024, we have repurchased a total of 14.1 million shares at an aggregate price of $172.1 million, or $12.20 per share, excluding fees, commissions and other costs related to the repurchases.

As of June 30, 2024, we had $177.9 million remaining under the share repurchase program. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the Board of Directors from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our Board of Directors in its discretion at any time. As a result of ICE’s discontinued use of the South Texas Facility and the impact such discontinuation will have on our leverage ratios, we intend to prioritize the use of our free cash flow to further reduce our debt, although we may exercise discretion in repurchasing additional shares of our common stock in accordance with the repurchase program.

Debt Refinancing. On April 15, 2024, we redeemed the remaining $98.8 million outstanding principal balance of our 8.25% senior unsecured notes due 2026 (the 2026 Notes), at a redemption price of 104.125% of the principal amount, plus accrued and unpaid interest on such notes to, but not including April 15, 2024, resulting in a charge of $4.1 million reported during the second quarter of 2024. This redemption completed the refinancing transactions begun during the first quarter of 2024 with the underwritten registered public offering of $500 million aggregate principal amount of 8.25% senior unsecured notes due 2029 (the 2029 Notes). The net proceeds from the offering of the 2029 Notes, amounting to $490.3 million, together with borrowings under our revolving credit facility and cash on hand, were used to fund the tender offer for, and subsequent redemption of, the 2026 Notes, which had an outstanding principal balance of $593.1 million. Following the completion of the tender offer of $494.3 million, or 83.3% of the aggregate principal amount of the 2026 Notes then-outstanding during the first quarter of 2024, and the redemption of the remaining $98.8 million principal balance outstanding during the second quarter of 2024, we have no debt maturities until 2027, when $243.7 million principal amount of our 4.75% senior unsecured notes mature.

Contract Updates

New Management Contract with State of Montana. On July 25, 2024, following a competitive bid process, we received a Notice of Intent to Award a new management contract from the state of Montana to care for additional residents at CoreCivic facilities. During the third quarter of 2024, we anticipate receiving 120 residents at our 1,896-bed Saguaro Correctional Facility in Eloy, Arizona, doubling the population from the state of Montana residing at this facility under an existing management contract. As of June 30, 2024, we also cared for approximately 1,000 residents from Hawaii, and nearly 600 residents from the state of Idaho at the Saguaro Correctional Facility. Should the state of Montana need additional capacity, the State may approve the utilization of any other facility we own or operate, subject to availability. The Notice of Intent to Award a management contract is an expansion of our relationship with the state of Montana, where we also manage the fully occupied company-owned Crossroads Correctional Center in Shelby, Montana for the state of Montana pursuant to a separate management contract.

South Texas Family Residential Center. As disclosed on June 10, 2024, we received notification from ICE that the agency intends to terminate an inter-governmental service agreement (IGSA) for services at the South Texas Facility on August 9, 2024. We lease the facility and the site upon which it was constructed from a third-party lessor, and we have provided notice of lease termination to the lessor, also effective August 9, 2024. Total revenue at this facility was $39.3 million and $156.6 million for the three months ended June 30, 2024 and the twelve months ended December 31, 2023, respectively. The impact of this contract termination is included in our updated 2024 financial guidance.

2024 Financial Guidance

CoreCivic previously withdrew its financial guidance during the second quarter of 2024. Based on current business conditions, we are providing the following financial guidance for the full year 2024:

Guidance Full Year 2024

• Net income

$42.0 million to $50.4 million

• Adjusted Net Income

$65.6 million to $73.6 million

• Diluted EPS

$0.37 to $0.45

• Adjusted Diluted EPS

$0.58 to $0.66

• FFO per diluted share

$1.28 to $1.36

• Normalized FFO per diluted share

$1.48 to $1.56

• EBITDA

$268.0 million to $274.6 million

• Adjusted EBITDA

$302.4 million to $308.4 million

During 2024, we expect to invest $70.0 million to $76.0 million in capital expenditures, consisting of $30.0 million to $31.0 million in maintenance capital expenditures on real estate assets, $32.0 million to $35.0 million for maintenance capital expenditures on other assets and information technology, and $8.0 million to $10.0 million for other capital investments, including costs to prepare an idle facility for activation in the possible event an opportunity presents.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the second quarter of 2024. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the third quarter of 2024. Written materials used in the investor presentations will also be available on our website beginning on or about August 26, 2024. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, August 8, 2024, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BIdd7601382fc644b791a9a7cfbbe4f556. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for over 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government, including as a consequence of the United States Department of Justice not renewing contracts as a result of President Biden’s Executive Order on Reforming Our Incarceration System to Eliminate the Use of Privately Operated Criminal Detention Facilities, impacting utilization primarily by the United States Federal Bureau of Prisons and the United States Marshals Service, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (v) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a continuing rise in labor costs; fluctuations in interest rates and risks of operations; (vi) government budget uncertainty, the impact of the debt ceiling and the potential for government shutdowns and changing budget priorities; (vii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; (viii) our ability to have met and maintained qualification for taxation as a real estate investment trust, or REIT, for the years we elected REIT status; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services, except as may be required by law.

Second Quarter Revenue of $1.7 Billion with GAAP EPS of $(0.12); Adjusted EPS of $0.56

Progress on Project Core to Drive Future Cost Savings and Implementing Growth Initiatives

Company Repurchased $191 Million of Shares Year to Date

Company Provides Update on Varis Sale Process

BOCA RATON, Fla.–(BUSINESS WIRE)–Aug. 7, 2024– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the second quarter ended June 29, 2024.

Second Quarter 2024 Summary(1)(2)(3)

Total reported sales of $1.7 billion, down 10% versus the prior year on a reported basis. The decrease in reported sales is largely related to lower sales in its Office Depot Division, primarily due to 58 fewer retail locations in service compared to the previous year and reduced transactions, as well as lower sales in its ODP Business Solutions Division

GAAP operating income of approximately $400 thousand and net income (loss) from continuing operations of $(4) million, or $(0.12) per diluted share, versus $60 million and $43 million, respectively, or $1.09 per diluted share, in the prior year period

Adjusted operating income of $33 million, compared to $67 million in the second quarter of 2023; adjusted EBITDA of $57 million, compared to $95 million in the second quarter of 2023

Adjusted net income from continuing operations of $20 million, or adjusted diluted earnings per share from continuing operations of $0.56, versus $48 million or $1.22, respectively, in the prior year period

Operating cash flow from continuing operations of $(1) million and adjusted free cash flow of $5 million, versus $(8) million and $(24) million, respectively, in the prior year period

Repurchased nearly 2.4 million shares at a cost of $104 million in the second quarter of 2024; Repurchased a total of approximately $141 million of shares when including purchases made in the second quarter and post quarter through the current date

$831 million of total available liquidity including $190 million in cash and cash equivalents, of which $10 million is presented in Current assets held for sale related to the Varis Division, at quarter end

“We are executing Project Core while taking actions to improve top-line trends in both our B2B and B2C businesses,” said Gerry Smith, chief executive officer of The ODP Corporation. “Our performance in the quarter was below our expectations, impacted by more cautious business spending and weaker consumer activity, along with new customer onboarding challenges impacting revenue traction at ODP Business Solutions. Additionally, retail store traffic trends, while improving sequentially, remained sluggish. Although market challenges impacted Office Depot and ODP Business Solutions, we continued to see progress in Veyer, as they executed across their growth strategies, attracting new third-party customers and improving their external EBITDA. Furthermore, we continued to buy back our shares, returning over $100 million of our stock in the quarter and over $190 million year to date,” he added.

“While we are pacing below our prior expectations for the year, we are not standing still. We’re taking actions to improve our top-line trajectory and we remain focused on capturing the long-term opportunities derived by our strong value proposition, solid balance sheet, and flexible foundation. In addition to our efforts under Project Core, which we expect will create over $100 million in annual cost savings when fully implemented, we are executing on initiatives to accelerate sales pipeline conversion, drive additional avenues for growth with existing customers, and leverage our deep customer relationships to solve more of their procurement challenges. This is what we call the Power of 1 – the ability to add value to our customers through offering one more product or suite of products to help them succeed. For example, we recently were awarded a sizeable order for standalone air conditioning units for a government entity — something not top of mind when you think of ODP Business Solutions, but it showcases the trust customers have in our capabilities to source, deliver, and solution during a time of need – all through the Power of 1. Additionally, we are set early for the upcoming back-to-school season and well positioned with our Education 365 approach, connecting customers within the education sector.”

“Although we are disappointed by our first half performance and outlook for the remainder of the year, we are committed to driving growth back into the business, remaining focused on converting the numerous opportunities in our pipeline, strengthening our position in the second half of the year and having impact in 2025 and beyond. We have several prospects at both ODP Business Solutions and Veyer that we expect to close in the second half that will boost revenue growth velocity as we exit this year. With these opportunities, coupled with our full realization of Project Core, we expect to exit 2024 with a stronger profile,” he continued.

“Despite the near term top-line challenges, we remain committed and encouraged about the future and confident in our operational excellence approach. Our team remains focused on executing the necessary steps to position us for long term growth and profitability,” Smith concluded.

Consolidated Results

Reported (GAAP) Results Total reported sales for the second quarter of 2024 were $1.7 billion, a decrease of 10% compared with the same period last year, driven by lower sales in both its consumer and business-to-business (B2B) divisions. Lower sales in its consumer division, Office Depot, was primarily due to 58 fewer stores in service compared to last year related to planned store closures, as well as lower retail and online consumer traffic and transactions. Sales at ODP Business Solutions Division were lower compared to last year, largely driven by macroeconomic factors causing more cautious spending among business customers, as well as continued challenges related to the onboarding of new customers and fewer transactions. Meanwhile, Veyer provided strong logistics support for the ODP Business Solutions and Office Depot Divisions and continued to execute across its growth strategy, delivering supply chain and procurement solutions to new third-party customers and driving external EBITDA.

The Company reported GAAP operating income of approximately $400 thousand in the second quarter of 2024, down compared to GAAP operating income of $60 million in the prior year period. Operating results in the second quarter of 2024 included $33 million of charges, primarily related to $25 million in net merger and restructuring expenses and $8 million non-cash asset impairment primarily related to the operating lease right-of-use (ROU) assets associated with the Company’s retail store locations. Net loss from continuing operations was $4 million, or $(0.12) per diluted share in the second quarter of 2024, down compared to net income from continuing operations of $43 million, or $1.09 per diluted share in the second quarter of 2023.

Adjusted (non-GAAP) Results(1) Adjusted results for the second quarter of 2024 exclude charges and credits totaling $33 million as described above and the associated tax impacts.

Second quarter 2024 adjusted EBITDA was $57 million compared to $95 million in the prior year period. This included depreciation and amortization of $24 million and $25 million in the second quarter of 2024 and 2023, respectively

Second quarter 2024 adjusted operating income was $33 million, down compared to $67 million in the second quarter of 2023

Second quarter 2024 adjusted net income from continuing operations was $20 million, or $0.56 per diluted share, compared to $48 million, or $1.22 per diluted share, in the second quarter of 2023, a decrease of 54% on a per share basis

Division Results

ODP Business Solutions Division Leading B2B distribution solutions provider serving small, medium and enterprise level companies with an annual trailing-twelve-month revenue of nearly $4 billion.

Reported sales were $917 million in the second quarter of 2024, down 8% compared to the same period last year. The decrease in sales was related primarily to weaker macroeconomic conditions, more cautious business spending, new customer onboarding challenges, and lower sales conversion

Total adjacency category sales, including cleaning and breakroom, furniture, technology, and copy and print, were 43% of total ODP Business Solutions’ sales

Continued strong pipeline of potential new business and implementing several initiatives to regain top-line traction

Operating income was $29 million in the second quarter of 2024, down 36% compared to the same period last year on a reported basis. As a percentage of sales, operating income margin was 3%, down 140 basis points compared to the same period last year

Office Depot Division Leading provider of retail consumer and small business products and services distributed via Office Depot and OfficeMax retail locations and an eCommerce presence.

Reported sales were $799 million in the second quarter of 2024, down 12% compared to the prior year on a reported basis. Lower sales were partially driven by 58 fewer retail outlets in service associated with planned store closures, as well as lower demand relative to last year in major product categories and lower online sales. The Company closed 9 retail stores in the quarter and had 894 stores at quarter end. Sales were down 7% on a comparable store basis

Store and online traffic were lower year over year due to macroeconomic factors causing sluggish consumer activity

Operating income was $17 million in the second quarter of 2024, compared to operating income of $35 million during the same period last year, driven primarily by the flow through impact from lower sales. As a percentage of sales, operating income was 2%, down 170 basis points compared to the same period last year

Veyer Division Nationwide supply chain, distribution, procurement and global sourcing operation supporting Office Depot and ODP Business Solutions, as well as third-party customers. Veyer’s assets and capabilities include 8 million square feet of infrastructure through a network of distribution centers, cross-docks, and other facilities throughout the United States; a global sourcing presence in Asia; a large private fleet of vehicles; and next-day delivery to 98.5% of US population.

In the second quarter of 2024, Veyer provided support for its internal customers, ODP Business Solutions and Office Depot, as well as its third-party customers, generating sales of $1.2 billion

Operating income was $5 million in the second quarter of 2024, compared to $6 million in the prior year period driven by the flow through impact of lower sales to internal customers partially offset by the contribution related to services to external third-party customers

In the second quarter of 2024, sales generated from third-party customers were in-line with the same period last year and EBITDA generated from third-party customers increased by 17% year over year, resulting in sales of $10 million and EBITDA of $4 million

Share Repurchases

The Company continued to execute under its previously announced $1 billion share repurchase authorization valid through March 31, 2027. During the second quarter of 2024, the Company repurchased nearly 2.4 million shares at a cost of $104 million. Since the end of the second quarter of 2024, the Company repurchased additional shares for $37 million.

“Our capital allocation strategy balances investing in the future of our business while continuing to enhance value for shareholders through share repurchases under our buyback authorization,” stated Anthony Scaglione, executive vice president and chief financial officer of The ODP Corporation. “We have executed under this approach, investing in our business and repurchasing over $190 million of our stock thus far in 2024. Moving forward, we will continue to balance our capital allocation strategy remaining mindful of market conditions and business performance as we continue to drive our low-cost business model through Project Core.”

The number of shares to be repurchased under the authorization in the future and the timing of such transactions will depend on a variety of factors, including market conditions, regulatory requirements, and other corporate considerations. The new share repurchase authorization could be suspended or discontinued at any time as determined by the Board of Directors.

Balance Sheet and Cash Flow

As of June 29, 2024, ODP had total available liquidity of approximately $831 million, consisting of $190 million in cash and cash equivalents, including $10 million that is presented in Current assets held for sale related to the Varis Division, and $641 million of available credit under the Fourth Amended Credit Agreement. Total debt was $183 million.

For the second quarter of 2024, cash used in operating activities of continuing operations was $1 million, which included $25 million in restructuring spend, compared to cash used in operating activities of continuing operations of $8 million in the second quarter of the prior year, which included $1 million in restructuring spend. The year-over-year change in operating cash flow is largely related to the timing of certain working capital items.

Capital expenditures in the second quarter of 2024 were $19 million versus $17 million in the prior year period, reflecting continued growth investments in the Company’s digital transformation, distribution network, and eCommerce capabilities. Adjusted Free Cash Flow(3) was $5 million in the second quarter of 2024, compared to $(24) million in the prior year period.

Progress on Project Core

As the Company previously announced, Project Core is a plan designed to create further efficiencies throughout its business, focused on driving enhanced operating results and shareholder value. This broad-based plan includes cost improvement actions across the entire enterprise, optimizing its organizational structure to support future growth of the business. The Company continues to make significant progress under Project Core and is in position to realize in-year savings of approximately $50 million and annualized savings of over $100 million when fully implemented. Restructuring and related charges associated with these actions are now estimated to be in the range of $40 million to $50 million, excluding those related to the Varis Division, and are expected to be substantially incurred throughout 2024.