Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Pioneering innovation. Century Lithium has developed a proprietary system for lithium extraction that reflects innovations developed at its lithium extraction facility or pilot plant. Century Lithium received a provisional patent protecting the company’s system and methods for extracting lithium solids, including clay.

Extracting lithium from solids. The company’s patent pending system is based on the extraction of lithium from solids using products of a chlor-alkali process, including hydrochloric acid and sodium hydroxide. Exclusive of the direct lithium extraction (DLE) process where lithium is recovered, protected intellectual property includes the method of treating lithium-bearing solids with chloride solution and the handing of solutions, precipitates, and residues. DLE using Li-Pro is a component process proprietary to Koch Technology Solutions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAU COLLEGE OF BUSINESS EXECUTIVE EDUCATION | KAYE PERFORMING ARTS AUDITORIUM

FEATURING MODERATED FIRESIDE CHAT WITH THE 43rd PRESIDENT OF THE UNITED STATES, GEORGE W. BUSH

SUNDAY DECEMBER 3

Official Kickoff / Early Registration – FAU College of Business Executive Education

Dusty May, NCAA Men’s Basketball; Coach of the Year – FAU Owls

Nico Pronk, President & CEO, Noble Capital Markets, Inc.

Cocktails and hors d’oeuvres

MONDAY DECEMBER 4

~60 public company executive team presentations, breakouts, one-and-ones – FAU College of Business Executive Education

The World is HOT – Impact of National and Global Events – Panel Presentation

Food and beverage throughout the day

“The After” evening networking event – Celebrate Noble’s 19th After in ‘23. Mingle with music, magic, motors, munchies, and high-flying antics. A vintage experience like no other! – Privaira Private Aviation Hangar, Boca Raton Airport

TUESDAY DECEMBER 5

~50 public company executive team presentations, breakouts, one-and-ones – FAU College of Business Executive Education

43rd President of the United States, George W. Bush, moderated fireside chat – Kaye Performing Arts Auditorium at FAU (ticket included with registration)

Food and beverage throughout the day

Conference closing remarks, Noble and FAU representatives (TBA)

WHO SHOULD ATTEND?

Individuals who are interested in meeting and networking with the executives who lead the companies that may shape our future

Individuals who are looking for early-stage investments in companies that can represent significant growth

Family offices, investment clubs and organizations, brokers and equity analysts, financial industry representatives

Institutional investors, hedge & mutual fund portfolio managers, private equity

Florida Atlantic University students, faculty, alumni

EARLY REGISTRATION (before September 15, 2023)

General Registration for all events: $399

Registration for all events PLUS VIP-best-in-house seating for President Bush (BVIP) $599 (ticket value alone, $350)

Discounted Registration for Investment groups/clubs and FINRA-licensed RRs, General $149 / BVIP $299

Each class of registration available in limited quantities. Pricing may increase and/or be discontinued at any time, without notice. Investment groups/clubs must be approved by Noble prior to offering member discounts. Ask your group/club leadership if they have applied for approval from Noble. Registered representatives must have current CRD #. Service providers do not qualify for rates shown above, regardless of class affiliation.

The following companies are confirmed for NobleCon19. Check back often, as new companies are added every week. Interested in presenting? Submit a request at the link above.

iCoreConnect, Inc. (Nasdaq: ICCT) recently underwent a business merger with FG Merger Corp. (Nasdaq: FGMC) and has since exhibited stability in the stock market. A notable event was a temporary halt in trading on Nasdaq due to a technical issue with the conversion of shares. However, trading resumed on August 30, 2023, after the issue was addressed. iCoreConnect is currently trending on various financial social media platforms and websites, reflecting heightened investor interest. Their stock price is up 206% since the start of the week as trading opened Friday.

iCoreConnect’s primary objective is to improve workflow productivity and practice profitability via its cloud-based software and technology solutions. Currently, the company has a portfolio of 16 SaaS enterprise solutions. Additionally, they’ve secured endorsements from over 100 state or regional healthcare associations in the U.S. Based on their recent statements, iCoreConnect has projected its revenue and annualized recurring revenue for 2023 and expressed interest in expanding into the ePrescription and insurance verification sectors.

To understand more about iCoreConnect’s activities, developments, and potential in the healthcare technology and enterprise solutions industry, a recent report from Noble Capital Markets Analyst Gergory Aurand provides a detailed analysis and overview.

After months of scrutiny, including a lawsuit filed by the Federal Trade Commission, the FTC has given drug giant Amgen the go-ahead to proceed with their planned acquisition of Horizon Therapeutics, a global biotechnology company focused on the discovery, development and commercialization of medicines that address critical needs for people affected by rare, autoimmune and severe inflammatory diseases.

The planned acquisition was originally announced late in 2022 but has been held up due to concerns that the deal may stifle competition in the pharmaceutical industry. One key point resolved in an agreement announced Friday stipulates that Amgen is prohibited from “bundling” two of Horizon’s key drugs. A “bundling” tactic could involve rebates or promotions to insurers for recommending or favoring those Horizon products.

Horizon Therapeutics is up slightly in early market trading on Friday following the announcement. The company currently has a market cap of $26.4bn. The merger, valued at $27.8bn, is expected to be completed in Q4 of 2023.

Explore Noble Capital Markets’ Biotechnology Analyst Robert LeBoyer’s coverage list for detailed analysis on other biotech stocks.

The U.S. jobs report for August is out, with 187,000 jobs added to the economy in August. This is slightly higher than the 170,000 economists had expected. On the other side, unemployment is up slightly, at 3.8%. This is 0.3% higher than economists had predicted. Wages increased slightly, up 0.2% month-over-month, and remain up more than 4% over last year.

About the U.S. Jobs Report

The U.S. jobs report, specifically the nonfarm payroll report, is a critical economic indicator that holds immense significance for both financial markets and policymakers. This report, typically released on the first Friday of each month by the U.S. Bureau of Labor Statistics, provides crucial insights into the health of the labor market in the United States.

The report serves as a barometer of economic health. It offers valuable data on the number of jobs created or lost in the previous month, the unemployment rate, and wage growth. This information helps economists and investors gauge the overall economic performance and can influence their outlook on future economic conditions. If job creation exceeds expectations, it can signal a robust economy, potentially leading to higher consumer spending and business investments.

This report also has a significant impact on financial markets. Stock, bond, and currency markets can experience substantial volatility on the day of the report’s release. Positive job growth can boost investor confidence and lead to stock market gains, while weaker-than-expected data can trigger market sell-offs. Additionally, the Federal Reserve closely monitors the jobs report when making decisions about interest rates and monetary policy, making it a key factor in shaping the direction of these markets in the medium to long term.

In summary, the U.S. jobs report is a vital economic indicator that provides insights into the labor market’s health and has a profound impact on financial markets, influencing investor sentiment, asset prices, and even central bank decisions. It is closely watched by economists, investors, and policymakers alike for its role in shaping economic outlooks and investment strategies.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Concessions are in good standing. In March, Aurania paid its annual concession fee in the amount of US$2,337,345 (C$3,165,349) to maintain its 207,764-hectare land package in Ecuador and has retained its interest in 94 concessions covering 93,300 hectares in Peru. On July 31 and during the first week of August, Dr. Keith Barron, Aurania’s CEO, met with Ecuador’s Minister of Energy and Mines and other government officials to discuss, among other things, options to recover concessions for which Aurania applied in 2016 and were initially held in reserve for Aurania by the government but subsequently not granted. Dr. Barron expects to return to Ecuador in September to resume discussions.

Pursuing an exploration license in France. In parallel with its activities in Ecuador, Aurania has applied for a 51 square kilometer exploration permit in the Brittany Peninsula of northwestern France. The Brittany Peninsula is part of the orogenic Variscan belt. The concession area, situated within the Morbihan Department, has historically been the site of significant high-grade gold finds. Aurania’s geologists visited the area and found numerous blocks of quartz and evidence of past mining activity.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

GeoVax Labs, Inc., a clinical-stage biotechnology company, develops human vaccines for infectious diseases and cancer in the United States and internationally. The company through its patented Modified Vaccinia Ankara-Virus Like Particle vaccine platform develops various vaccines. It is developing various vaccines that are in human clinical trials, and preclinical research and development phases, including vaccines against human immunodeficiency virus (HIV); Zika virus; malaria; and hemorrhagic fever viruses, such as Ebola, Sudan, Marburg, and Lassa, as well as therapeutic vaccines for chronic Hepatitis B infections and cancers. The company has collaboration and partnership agreements with the National Institute of Allergy and Infectious Diseases of the National Institutes of Health; the HIV Vaccines Trial Network; Centers for Disease Control and Prevention; United States Army Research Institute of Infectious Disease; U.S. Naval Research Laboratory; Emory University; University of Pittsburgh; Georgia State University Research Foundation; Peking University; University of Texas Medical Branch; the Institute of Human Virology at the University of Maryland; the Scripps Research Institute; the Burnet Institute; American Gene Technologies, Inc.; Viamune, Inc.; Vaxeal Holding SA; CaroGen Corporation; Virometix AG; and Leidos, Inc. GeoVax Labs, Inc. was founded in 2001 and is based in Smyrna, Georgia.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Patent Issuance Covers The GeoVax Ebolavirus. GeoVax announced the issuance of a US patent covering its ebolavirus vaccine made using its VLP (virus-like particle) technology. The vaccine uses an MVA viral vector to deliver genes to elicit an immune response against the virus. The patent claims cover multiple ebolavirus strains including Sudan ebolavirus, Zaire ebolavirus, Taï Forest ebolavirus, and Reston ebolavirus. We see this issuance as both a commercial and scientific milestone for GeoVax.

MVA-VLP Is A Novel Vaccine Technology Platform. The GeoVax MVA-VLP is a novel vaccine platform that delivers genes to produce VLPs within a person’s cells. After vaccination, the genes express the viral proteins which then assemble into VLPs. These VLPs are similar enough to the virus to be recognized and elicit immune protection but are not infectious or capable of replicating in the body. Preclinical studies have shown immune responses that are similar to live-attenuated virus vaccines, with both strong humoral and cellular immunity as well as greater safety from the MVA vector.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Eagle Bulk Shipping Inc. (“Eagle”) is a US-based drybulk owner-operator focused on the Supramax/Ultramax mid-size asset class, which ranges from 50,000 and 65,000 deadweight tons in size; these vessels are equipped with onboard cranes allowing for the self-loading and unloading of cargoes, a feature which distinguishes them from the larger classes of drybulk vessels and provides for greatly enhanced flexibility and versatility- both with respect to cargo diversity and port accessibility. The Company transports a broad range of major and minor bulk cargoes around the world, including coal, grain, ore, pet coke, cement, and fertilizer. Eagle operates out of three offices, Stamford (headquarters), Singapore, and Hamburg, and performs all aspects of vessel management in-house including: commercial, operational, technical, and strategic.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Estimates adjusted downward to reflect shipping weakness. We are lowering our assumed shipping rates in response to shipping rate declines and company guidance. Although EGLE had locked in 65% of its available shipping days at a rate near $16,000/day, the rate it received for the other shipping days was closer to $10,000/day. As a result, the average TCE day rate for the fleet of 52.8 vessels was closer to $14,000/day.

Lower shipping rates and thus revenues are partially offset by lower vessel operating costs. Operating expense is running between $6,300-$6,600 per shipping day, a decline from the first quarter. The lower costs lessen the impact of lower revenues in our models.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Is The Recession Here? Economic activity is slowing, taking pressure off of inflation. But, the Fed seems intent on pushing interest rates higher, likely through the balance of this year. As such, recent economic forecasts anticipate GDP to contract over the next few quarters. This does not paint a favorable picture for advertising in the very near term. But, given the increased likelihood of a recession, has timeliness in media stocks improved?

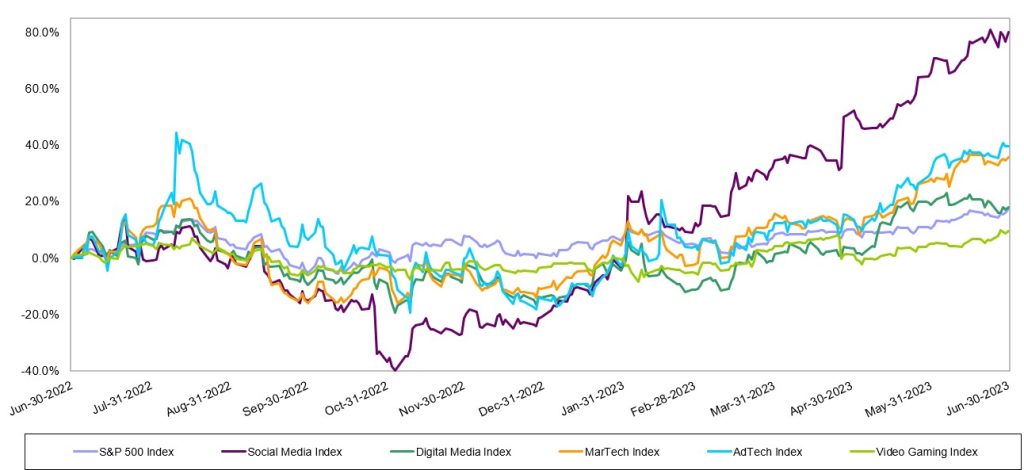

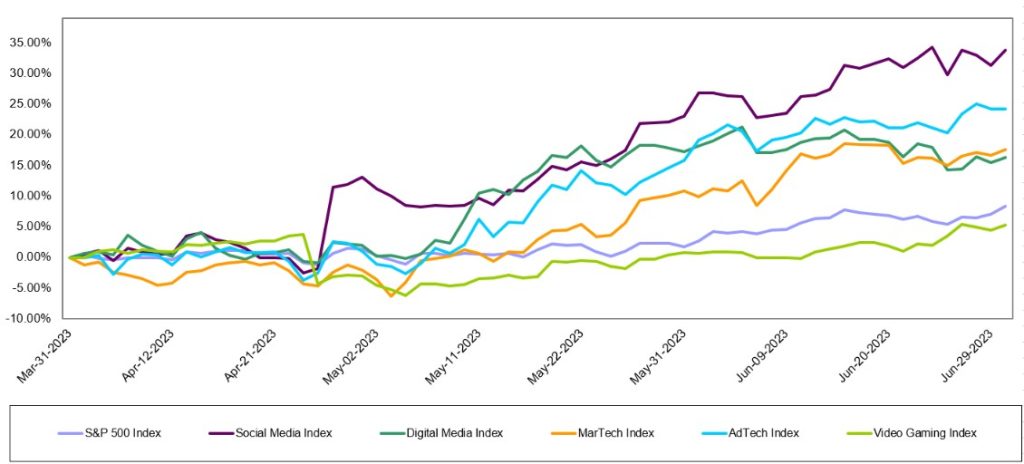

Digital Media & Technology:A broad based recovery? For the second quarter in a row, the best performing index was Noble’s Social Media Index, which increased by 34% in 2Q 2023, followed by Noble’s Ad Tech Index (+24%), MarTech Index (+18%), Digital Media Index (+16%), and Video Gaming Index (+5%). The largest stocks carried the performance in each of the indices. Can the stocks hold on to recent gains?

Broadcast Television: Are ad trends really improving? Recent reports indicate that television advertising is showing some improvement. While it is likely that Auto and Political advertising are bright spots, we remain skeptical that core advertising pacings are improving in the third quarter given the weak economic outlook. Nonetheless, the TV stocks appear to be cheap and we highlight a few of our key favorites.

Broadcast Radio:The pall over radio. Soft advertising trends heading into an economic downturn does not bode well for companies, like Audacy, that are in the midst of a financial restructuring. We believe that high debt leverage is the pall over the stocks. It is likely that many radio companies will go through a round of cost cutting to shore up cash flow in the midst of an economic downturn.

Publishing: Cash flow gurus. We do not believe that the Publishing industry will be spared from the weak advertising environment. The industry has a playbook for cutting costs, however, and has a history of maintaining cash flow through difficult times.

Overview

The Recession Is Here

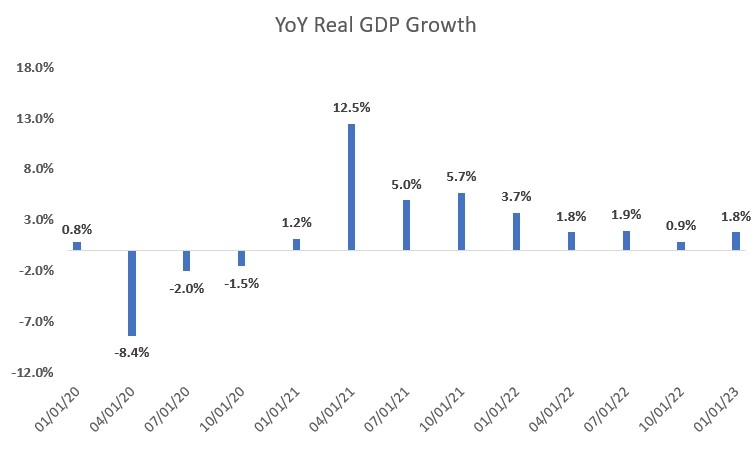

Figure #1 YoY Real GDP Growth illustrates that the economy grew post pandemic through the first quarter 2023, reflecting a rebounding economy, fueled by government spending. But, economic activity is slowing, taking pressure off of inflation. Nonetheless, the Fed seems intent on pushing interest rates higher, likely through the balance of this year. Most economists anticipate that the Fed will raise interest rates by 25 basis points two times in the second half of this year. Not only will the interest rate increases be a headwind for the economy, but government spending, a key driver to the economy this year, is likely to wane. Recent economic forecasts anticipate GDP to contract over the next few quarters, a classic definition of an economic recession. The Conference Board of Economic Forecasts anticipate that the US economy will contract -1.2% in Q3 2023, -1.9% in Q4 2023, and -1.1% in Q1 2024.

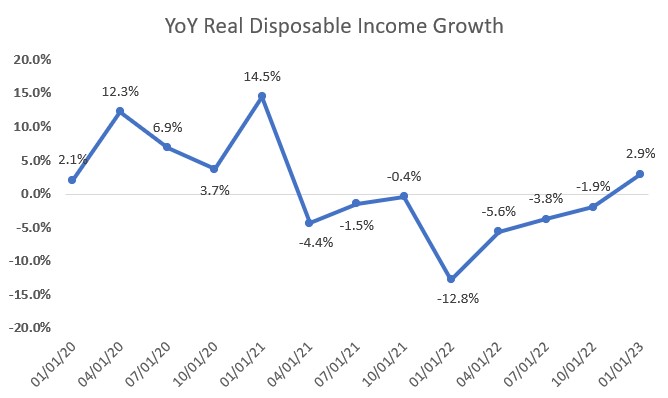

This does not paint a favorable picture for advertising in the very near term. Advertising is highly correlated to personal disposable income, particularly discretionary income. If consumers have discretionary income, companies advertise for them to spend. As Figure #2 YoY Real Disposable Income Growth highlights, disposable income has declined over the past 18 months. Not surprisingly, economically sensitive National advertising has been down nearly 4 quarters and at high double digit rates. Given the significant declines, as much as 25% in each quarter for the past year, National advertising trends should moderate, given that the comps get easier. As such, even with an economic downturn becoming more visible, it is possible that National advertising declines may moderate.

National advertisers tend to spend when there is light toward the end of an economic recession, when consumer personal disposable income shows signs that it will improve and consumers have the propensity to spend. In our view, that light at the end of the tunnel is still pretty dim given the economic forecast that anticipates a decline in GDP through the Q1 2024. While the visibility of an improvement in National advertising seems to have improved as we enter an economic downturn, especially given the easing comps and the benefit from Political advertising (expected to begin in Q3 2023), we think that it is too early to be optimistic. The length and severity of an economic downturn is not yet visible.

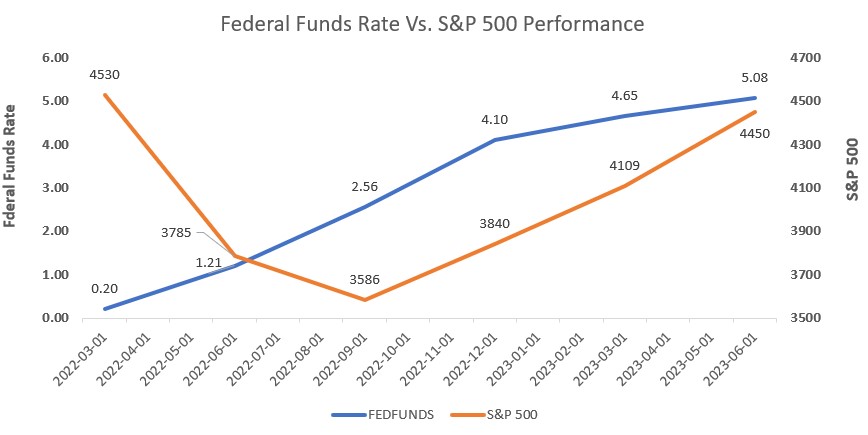

What does this mean for the stock market and for media stocks? Figure #3 Federal Funds Rate Vs. S&P 500 performance illustrates the recent increases in Fed Funds rates had little effect on the general stock market as measured by the S&P 500 Index. Unfortunately, late cycle and economically sensitive media companies declined or under performed the stock market. In spite of Fed Fund rate increases over the past year, the S&P 500 Index increased 18% in the last 12 months. The anticipation of an economic recession, however, weighed on media stocks. The stock performance of the various media sectors that we follow are discussed in this report, but have generally under performed the market. The exception to the poor performance were the Internet and Digital Media stocks, which had a broad based recovery. Is it possible that early cycle media stocks will outperform the general market in the near term? In our view, yes. But, this may mean that the general market may decline as media stocks decline less. Historically, it has been the case to buy media stocks in the midst of a recession as media stocks strongly outperform the general market in a economic recovery. But given the likely disappointment in revenue in the coming quarters, it is likely that media stocks will be volatile as investors weigh the near term revenue and earnings disappointments to the prospect of a revenue rebound in an improved economic scenario. This would suggest that if one would try to time the stocks, investors may want to wait a quarter or two, buy on the improved momentum. This may mean that one might miss the large gains. As such, for long term investors, we believe that we are nearer to the bottom and that the downside appears relatively limited, valuations appear compelling. But, given the anticipate volatility in the near term, media investors should look for opportunistic purchases and accumulate positions in our favorite media names highlighted in this report.

Figure #1 YoY Real GDP Growth

Source: Federal Reserve Bank of St. Louis

Figure #2 YoY Real Disposable Income Growth

Source: Federal Reserve Bank of St. Louis

Figure #3 Federal Funds Rate Vs. S&P 500 performance

Source: Federal Reserve Bank of St. Louis & Yahoo Finance

Digital Media & Technology

A Broad-Based Recovery in Shares

The Internet and Digital Media sectors rebounded nicely over the last 12 months (LTM). As Figure #4 LTM Internet & Digital Technology Performance illustrates, the Video Gaming index was the only sector that underperformed the S&P 500 over the last year. The S&P 500 Index was up 17.6% over the LTM, outperforming the Video gaming index’s increase of 9.7% and in line with Noble’s Digital Media Index increase of 18%. The MarTech Index and AdTech Index both performed strongly, increasing 35.8% and 39.8%, respectively. The Social Media index had the strongest performance of the indices, increasing an impressive 80.2% over the LTM.

Figure #4 LTM Internet & Digital Technology Performance

Source: Capital IQ

Despite macroeconomic headwinds that include higher interest rates, a regional banking crisis, elevated inflation and a war in Europe, the S&P 500 powered higher for the third quarter in a row. The S&P 500 Index continued its streak of steady increases, with an 8% increase in the Index in 2Q 2023, which followed a 7% increase in 1Q 2023 and a 7% increase in 4Q 2022. The broad index is up a healthy 24% since the end of the third quarter of 2022. The S&P 500 bottomed on October 12, 2022, and is up 26% from that date through mid-July.

The S&P 500’s performance was driven primarily by its largest constituents. As a market weighted index, the largest stocks have an outsized impact on its performance, and that was certainly the case in 2Q. Eight of the largest stocks in the S&P 500 Index were up in 2Q 2023 by 2x-3x or more than the Index’s 8% gain. Stocks that powered the Index higher included Nvidia (NVDA, +52%), Meta Platforms (a.k.a Facebook, META, +35%), Netflix (NFLX, +28%), Amazon (AMZN, +26%), Tesla (TSLA, +26%), Microsoft (MSFT, +18%), Apple (AAPL, +18%) and Google (GOOGL, +15%).

Noble’s Internet and Digital Media Indices, which are also market cap weighted, also powered higher thanks to the biggest constituents in their respective Indices. Each of these Indices posted double digital percent increases, with only the exception being Noble’s Video Gaming Index (+5%), which slightly underperformed the broader market/S&P Index. For the second quarter in a row, the best performing index was Noble’s Social Media Index, which increased by 34% in 2Q 2023, followed by Noble’s Ad Tech Index (+24%), MarTech Index (+18%), Digital Media Index (+16%), and Video Gaming Index (+5%).

Meta Powers the Social Media Index Higher

We attribute the strength of the Social Media Index to its largest constituent, Meta Platforms, whose shares increased by 35% in the second quarter. We noted last quarter that Meta appeared to be returning to its roots and focusing on profitability, rather than its nascent and riskier web3 initiatives. That return to its core strengths has been greatly rewarded by investors. Shares of Meta were up 225% from its 52-week low of $88.09 per share in early November through the end of June. Shares are up another 8% since the start of the third quarter with the launch of Threads, Meta’s answer to Twitter. Over 100 million people signed up for Threads within the first five days of its rollout. Meta has not yet begun to monetize this opportunity, but it will clearly add to its growth in coming quarters.

Ad Tech Stocks Embark on a Broad-Based Recovery Following a Difficult 2022

Noble’s AdTech Index increased by 24% in 2Q 2023, and this performance was very broad based, with 15 of the 24 stocks in the sector up, and a dozen of the stocks up by double digits. Ad Tech stocks that performed best during the quarter include Applovin (APP, +63%), Magnite (MGNI, +47%), Tremor International (TRMR, +37%), Pubmatic (PUBM, +32%), Double Verify (DV, +29%), The Trade Desk (+27%), and Integral Ad Science (IAS, +26%). Ad Tech stocks were the worst performing sector in our universe in 2022, with the index down 63% for the year in 2022. The strong performance in 2Q 2023 in many respects reflects a bounce back off multi-year lows for several stocks. Year-to-date, one standout in particular is Integral Ad Science, whose shares were up 104% in the first half of 2023.The company continues to expand its product suite, scale its social media offerings (i.e., for TikTok) and is well positioned to continue to benefit from the shift from linear TV to connected TV (CTV). The company is benefiting from new partnerships with YouTube and Netflix and shares likely benefited during the quarter from anticipation of the company’s mid-June analyst day presentation.

Noble’s MarTech Index was up 18%, with performance within the group also broad based. The Digital Media & Technology indices market-cap weighted performances in 2Q are illustrated in Figure #5 2Q Internet & Digital Technology Performance. Thirteen of the 20 stocks in the Index were up in the quarter. MarTech stocks that performed best during the quarter include Cardlytics (CDLX, +86%), Shopify (SHOP, +35%), Live Ramp (RAMP, +30%), Adobe (ADBE, +27%), and Hubspot (NUBS, +24%). One of the poor performers in the group was one of our closely followed stocks, Harte Hanks, which declined 42% in the latest quarter. The stock gave back nearly all of its 54% gains in the prior year. The weakness was due to a disappointing quarterly revenue outlook as the company indicated that it is seeing economic headwinds and more difficult second half comparables. Notably, the company has significant levers to maintain much of its favorable cash flow outlook and is well positioned for growth as those headwinds diminish. We believe that downside risk in the HHS shares appear limited and view the shares as among our favorite rebound plays. Overall, MarTech stocks were victims of their own success: the group traded at double digit revenue multiples in 2021, but the sector’s revenue multiples were more than halved in 2022. The group currently trades at 5.9x 2023E revenues, up from 4.1x 2023E revenues at the end of the first quarter, and 3.5x 2023E revenues at the start of the year. Current trading multiples are illustrated in Figure #7 MarTech Comparables.

Finally, the Digital Media Index was up 16% in 2Q 2023, and here again, the performance was broad based with 8 of the 12 stocks in the Index posting gains. Digital Media stocks that performed best during the quarter include Fubo TV (FUBO, +72%), Travelzoo (TZOO, +31%), Netflix (NFLX, +28%), Interactive Corp (IAC, +22%), and Spotify (SPOT, +20%). Year-to-date, the two best performing Digital Media stocks are Spotfiy (+103% YTD), which has shifted its priority to running a profitable company and took additional steps in 2Q to achieve it, for instance, by consolidating and streamlining several of its podcast company acquisitions from recent years. The second best performing Digital Media stock through the first half of the year was Travelzoo (TZOO), whose shares were up 77% in the first half of the year. The company continues to benefit from pent up demand that helped a surge in travel as the pandemic ebbed. Lodging and domestic travel demand rebounded first, but Travelzoo appears to be benefiting from cruises and international travel, where pent up demand took longer to recover. Management indicated that travel related advertising may increase as economic headwinds adversely affect hotel and air travel occupancy, forcing these travel businesses to offer discounts. We rate the TZOO shares as Outperform.

Figure #5 2Q Internet & Digital Technology Performance

Source: Capital IQ

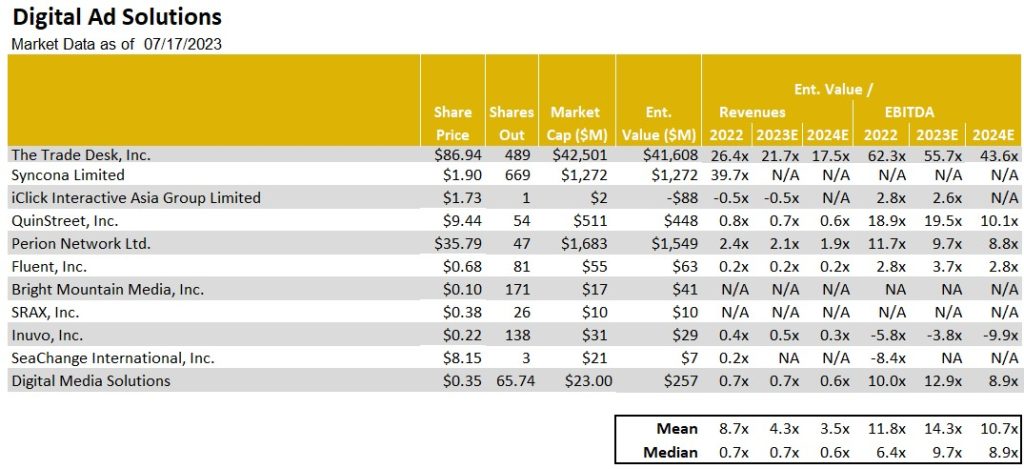

Figure #6 AdTech Comparables

Source: Company filings & Eikon

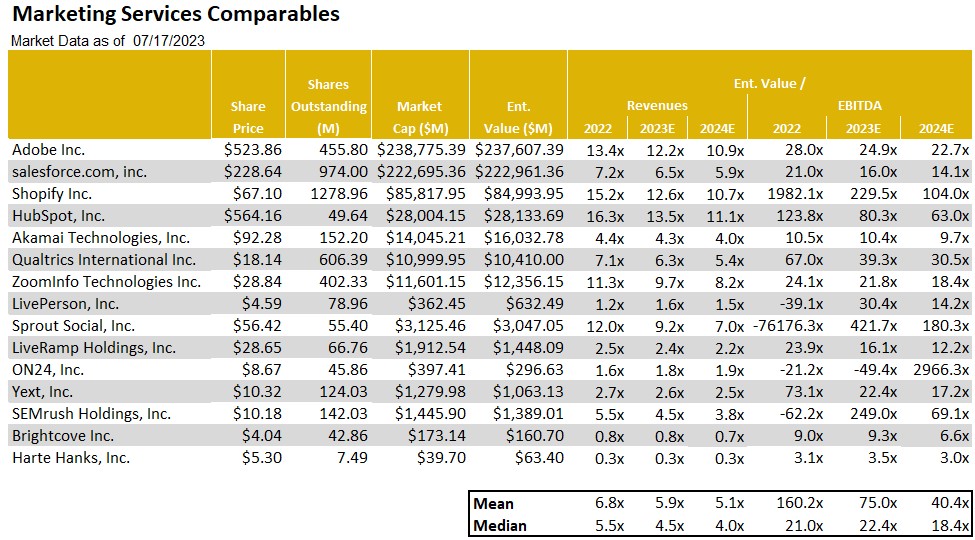

Figure #7 MarTech Comparables

Source: Noble estimates & Eikon

Traditional Media

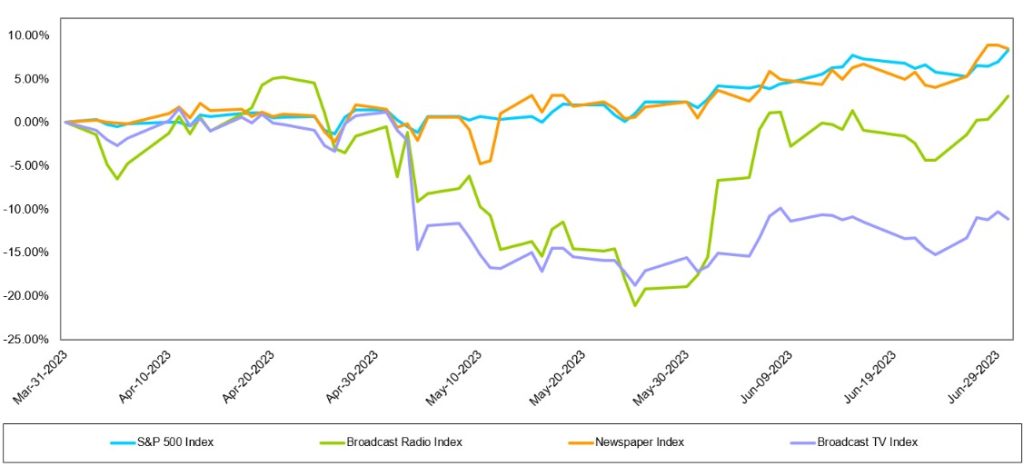

Traditional media stocks largely underperformed the general market over the LTM, the Radio sector was the hardest hit. As Figure #8 LTM Traditional Media Performance illustrates, the Noble Radio Index decreased 37.7% over the LTM, compared with the general market increasing 17.6%, as measured by the S&P 500 over the same period. The Television Index was down 14.8% and the Publishing index outperformed the general market, increasing 28.4% over the LTM. Notably, there were company stock performance disparities within each sector, highlighted later in this report. Given the indices are market cap weighted, larger market capitalized companies skewed the indices’ performance.

The traditional media industry is still finding its footing in the difficult economic environment, given the indices performance in Q2. While the Newspaper and Radio indices performed better in Q2 than Q1, the TV Index did not. The general market, as measured by the S&P 500, increased 8.3% over the last quarter and outperformed all but one traditional media sector. The Newspaper Index, which increased 8.5% over the same period narrowly outperformed the general market. The TV Index was the hardest hit traditional media sector and decreased -11.1%. While the Radio index underperformed the market in Q2, it improved upon a difficult Q1 and increased 3.1%, as illustrated in Figure #9 Q2 Traditional media performance.

Figure #8 LTM Traditional Media Performance

Source: Capital IQ

Figure #9 Q2 Traditional Stock Performance

Source: Capital IQ

Broadcast Television

Are ad trends really improving?

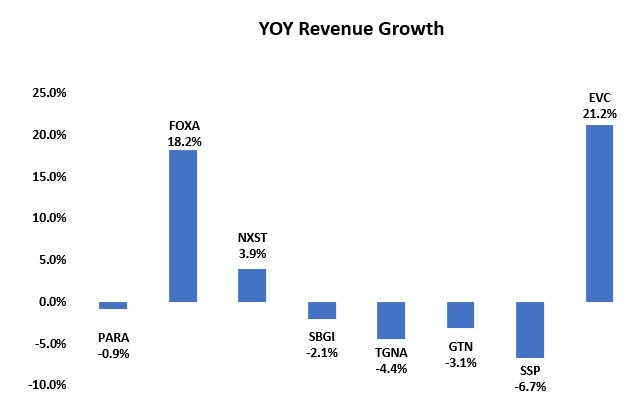

The TV Index underperformed the general market in the second quarter. While none of the stocks in the TV Index increased in the second quarter, many performed better than the market cap weighted return of -11.1%. Fox Corporation (FOXA; down 0.1%), E.W Scripps (SSP; down 2.8%), Nexstar (NXST; down 3.5%) and Gray Television (GTN; down 9.6%) were among the best performing stocks in the hard-hit TV index. The stocks hit the hardest in Q2 were Sinclair Broadcast Group (SBGI; down 19.5%) and Entravision (EVC; down 27.4%). Given the recent turmoil in TV stock performances we view the depressed prices as a potential opportunity given the prospect of an advertising recovery over the next few quarters.

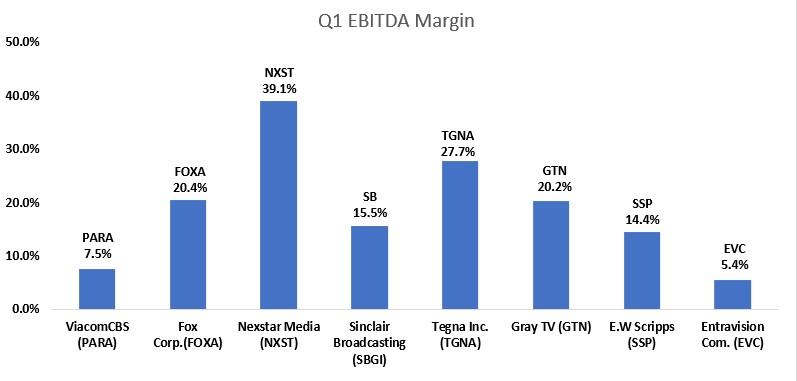

While there have been some recent reports indicating that television advertising is improving, possibly related to increased political advertising and Auto advertising in the third quarter, we remain skeptical that the improvement is sustainable given the prospect of a weakening economy. Nonetheless, the TV stocks appear cheap. One of our favorites in the index is Entravision (EVC) which is among the industry leaders in revenue growth as illustrated in Figure #10 TV Q1 YoY Revenue Growth. While the EVC shares had a poor performance in Q2, down 27.4%, the shares had increased 26% in Q1. Entravision’s revenue growth is the product of a robust digital business that comprises approximately 80% of total revenue. We believe that the recent under performance is related to Meta’s (Facebook’s) announcement that it plans to implement efficiencies, implying that it may take margin away from some of its advertising agencies, like Entravision, which represents Facebook in Latin America. In our view, Entravision is in a strong position to push back on that prospect given its favorable business relationship with the company. Given the influx of lower margin digital revenues, Entravision’s EBITDA margin is much lower than industry peers, illustrated in Figure #11 TV Industry Q1 EBITDA Margin. But, importantly, the company has one of the better revenue and cash flow growth profiles.

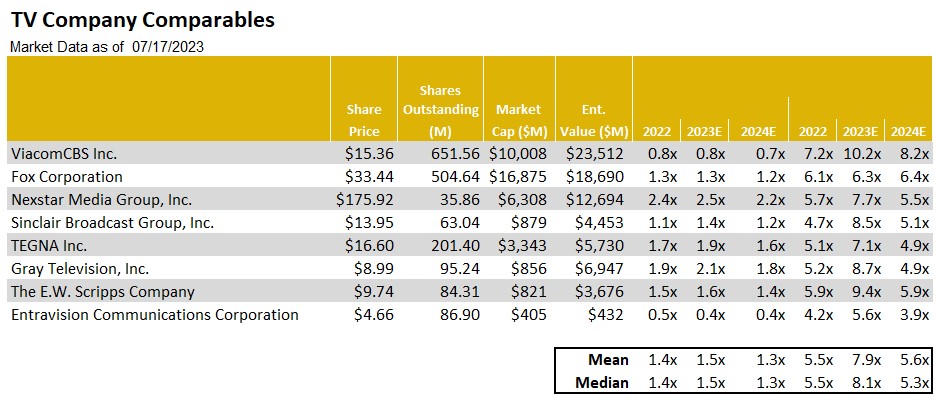

Figure #12 TV Company Comparablesillustrates the trading levels of the companies in the index. Some of our favorites Entravision (EVC) and E.W Scripps (SSP) trade at multiples well below the industry peer group highs. While E.W Scripps had modest year over year revenue decline, we believe it will benefit from favorable Retransmission revenue, strong Political advertising and improved margins in 2024. Given the SSP shares low float, the shares tend to underperform when industry is out of favor and outperform when the industry is back in favor. As for Entravision, we view the company’s digital transformation favorably and, notably, the shares are trading at a modest 3.9 times Enterprise Value to our 2024 Adj. EBITDA estimate. In our view, there appearas to be limited downside risk. The EVC shares and SSP shares, in our view, both offer a favorable risk reward relationship.

Figure #10 TV Q1 YoY Revenue Growth

Source: Company filings

Figure #11 TV Industry Q1 EBITDA Margin

Source: Company filings & Eikon

Figure #12 TV Company Comparables

Source: Noble Estimates & Eikon

Broadcast Radio

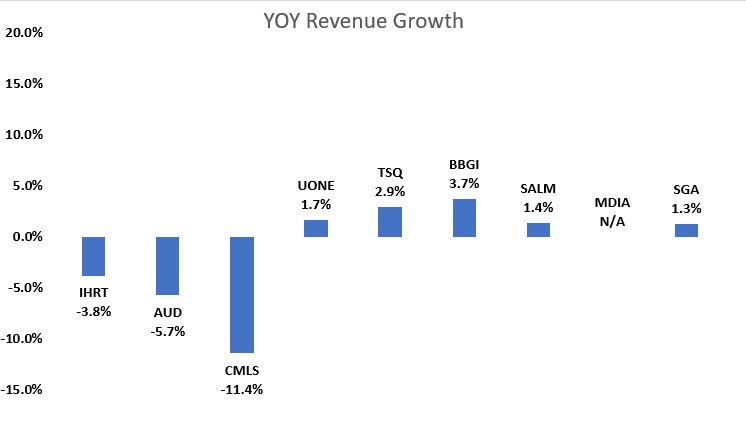

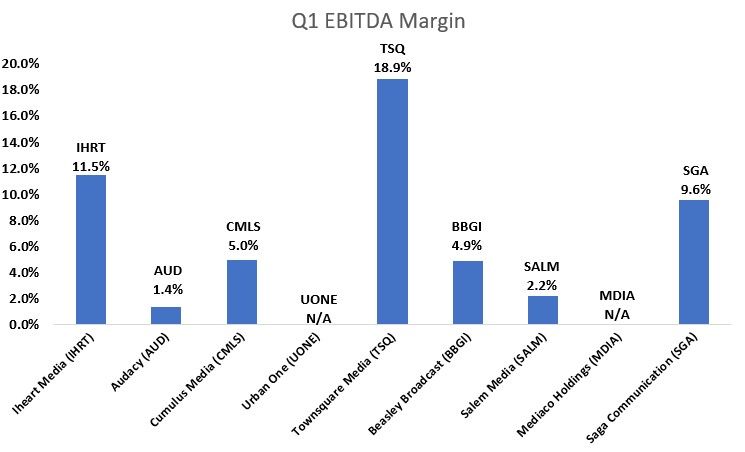

While the Radio Index underperformed the S&P 500 in Q2, it was an improvement from a difficult Q1. Notably, there were a few strong performances in the market cap weighted index. Beasley Broadcast Group (BBGI, up 24.4%) , Cumulus Media (CMLS, up 11.1%) and Townsquare (TSQ, up 48.9%) all strongly outperformed the S&P 500 in Q2. The largest stocks in the group did not perform well in the quarter skewing the index lower, Audacy (AUD, up 2.6%) and iHeart Media (IHRT, down 6.7%). The second quarter stock performances were a mixed bag and largely did not reflect the first quarter operating results. As Figure #13 Radio Q1 YoY Revenue Growth illustrates, most companies had modest revenue growth. The larger Radio companies that rely more on National advertising had the greatest declines of YoY revenue. With CMLS being the exception, the larger Radio companies underperformed relative to Radio companies with a stronger digital and highly localized presence. Figure #14 Radio Industry Q1 EBITDA Margin Margins illustrate that the margins for the industry remain relatively healthy.

Some of our favorite Radio stocks have strong digital businesses and highly localized footprints, which provides some shelter from weakness in national advertising. Those stocks included Townsquare, Beasley Broadcast Group, Salem Media (SALM; down 12.1%) and Saga Communications (SGA, down 3.9%). While the shares of Saga Communications (SGA) were down 3.9%, the performance did not reflect its favorable first quarter operating results. Importantly, Saga grew revenues a modest 1.3% and had an above average Q1 EBITDA margin of 9.6%. Saga has a highly localized footprint, as approximately 90% of revenues come from local sources. Furthermore, the company has been placing more importance on growing a profitable digital business in recent years. While Saga’s Digital business is early in its development, management is focused on growing digital revenues from 7.5% of total revenue in Q1 to 20% of total revenue over the next couple years. Additionally, we believe the company is likely to maintain a strong cash position given the economic uncertainty.

We view Townsquare Media (TSQ), Salem Media (SALM), Beasley Broadcast (BBGI) and Saga Communications (SGA) as among our favorites in the industry given the diverse revenue streams and localized footprints. While these companies are not immune to the economic headwinds, we believe that its Digital businesses and local footprints should offer some ballast to its more sensitive Radio business. Beasley’s recent digital revenue growth has been robust, digital revenue was 17% of total revenue in Q1 and is expected to reach 20% to 30% of total revenue for full year 2023. In the case of Salem, 30% of its revenues are from reliable block programming.

We believe that Radio advertising pacings likely will be problematic in the second half given the economic headwinds. Unlike Television, the industry does not benefit as much from Political advertising. As such, we expect that advertising pacings likely will be lower in Q3 than the Q2 results. It is likely that many radio companies, especially those with higher debt leverage, will implement cost cutting measures. With many of the radio companies already relatively lean from the Pandemic, it is likely that such measures will be difficult.

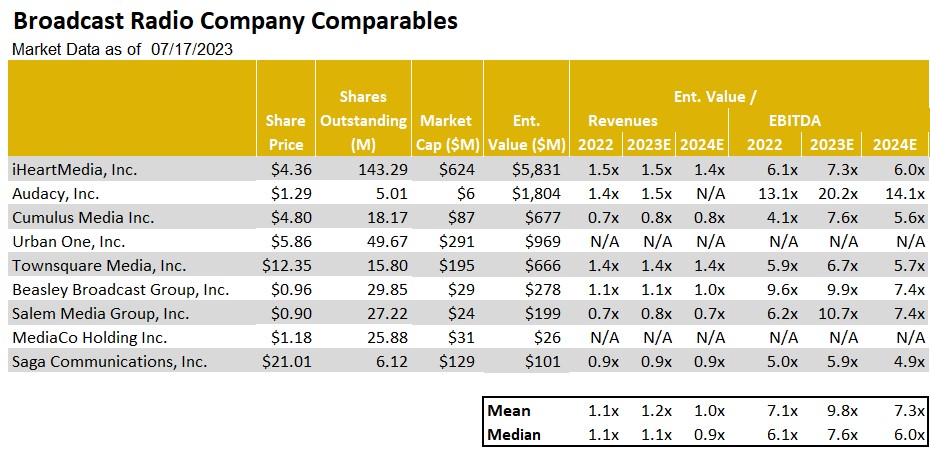

As Figure #15 Radio Company Comparables illustrates, the shares of Townsquare and Saga are among the cheapest in the industry, trading below peer group averages. Notably, Townsquare implemented a hefty dividend in Q1, providing the unique opportunity to get a return of capital while waiting for a turn toward more favorable fundamentals. As such, the shares of TSQ tops our list of favorites. We also view the shares of Saga as among our favorites. The company is early in its transition toward digital and has a lot of headroom for enhanced revenue growth.

Figure #13 Radio Q1 YoY Revenue Growth

Source: Company filings

Figure #14 Radio Industry Q1 EBITDA Margin

Source: Company filings & Eikon

Figure #15 Radio Company Comparables

Source: Noble estimates & Eikon

Publishing

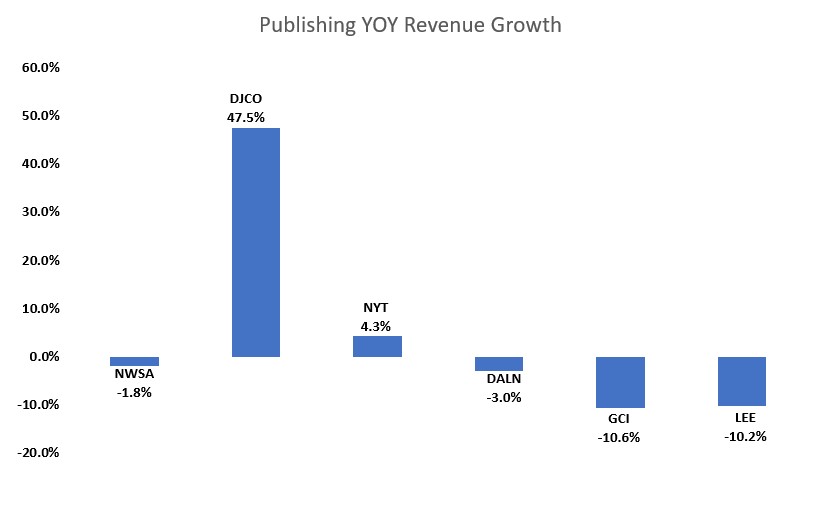

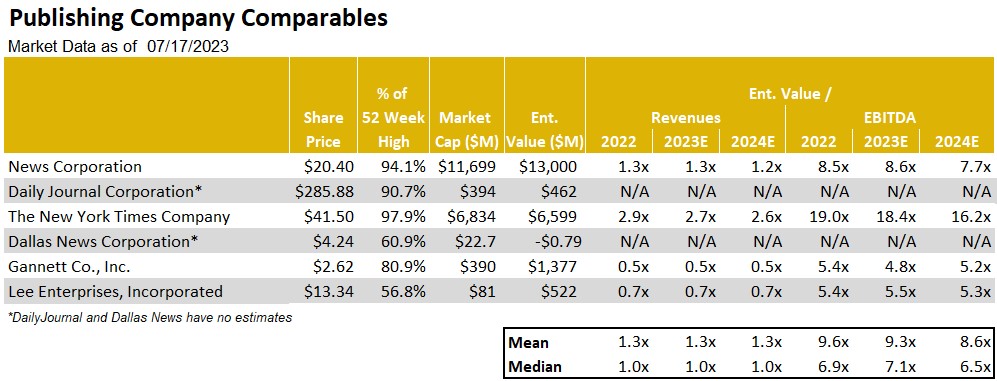

The Publishing industry is no exception to the advertising weakness that is impacting the broader Media landscape. As such, revenues are likely to continue to decline, despite an already weak performance in the first quarter of the year. Figure #16 Publishing Q1 YoY Revenue Growth illustrates the predominantly negative trends in the industry in the most recently reported quarter. The advertising challenges are hitting the traditional Print side of the publishing business hardest. For example, Lee Enterprises (LEE), one of our favorites in the industry, reported a 10% Print advertising revenue decline for the quarter ended March 31st, while Digital advertising grew a modest 2%. The company’s adj. EBITDA generation fell 15% compared with a more moderate 2% drop in total company revenues.

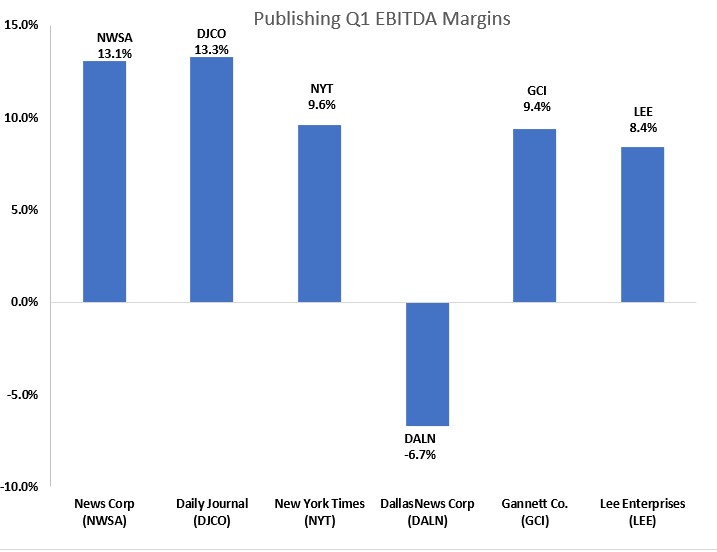

Not surprisingly, the dampened industry revenue resulted in lower industry cash flow generation with EBITDA margins averaging in the 10% range, as illustrated in Figure #17 Publishing Industry Q1 EBITDA Margins. Yet despite the constraints on cash flow generation on Lee and the other Publishers, we believe the companies have the ability to cut costs to help offset the pressure on cash flow generation. In particular, companies could cut costs in their Print manufacturing and distribution operations, reducing overhead in the same business segments where revenues are expected to lag. Publishing companies have a playbook on cutting legacy print costs and have the ability to maintain cash flow. However, cost cuts can take time to go into full effect, which could result in poor cash flow performance over the next quarter or so.

In spite of the nearer term economic headwinds impacting the operating performance of the industry, we believe that the industry is near an inflection point towards revenue growth. This dynamic is related to the degree of the recovery in its digital media businesses, a key driver to the industry’s overall revenue performance. While there are secular challenges to the industry’s print business, digital revenues account for an increasing portion of total revenues. For companies like Lee Enterprises, digital accounts for over 38% of total revenues in the most recent quarter. In our view, publishing companies will be a player in the advertising recovery as economic prospects improve. Furthermore, we believe that stock valuations are compelling.

Figure #18 Publishing Company Comparables illustrates the Publishing companies trading levels. Notably, the New York Times (NYT) trades well above the levels of the rest of its peers. In comparison, Lee and Gannett appear to be compelling. However, both Lee and Gannett are highly levered. Yet, in our view, Lee’s debt profile has several favorable characteristics, such as a fixed 9% annual rate, no fixed principal payments, no performance covenants and a 25 year maturity. Given that the LEE shares trade near 5.3 times enterprise value to our 2024 adj. EBITDA forecast, we believe the shares offer limited downside risk. With a favorable Digital transformation of the business well underway, we believe the LEE shares could close the valuation gap with some of its higher trading peers. As such, the LEE shares represent one of our favorites in the industry, especially as the economic downturn bottoms out and the prospect for a recovery begins to come to the forefront. As such, the LEE shares are among our favorite recovery plays.

Figure #16 Publishing Q1 YoY Revenue Growth

Source: Company filings & Eikon

Figure #17 Publishing Industry Q1 EBITDA Margins

Source: Company filings & Eikon

Figure # 18 Publishing Company Comparables

Source: Noble estimates & Eikon

The following companies are highlighted in this report. Click on the links for additional information and disclosures.

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Energy Stocks underperformed the market in the second quarter. Energy stocks declined 2.0% in the 2023 second quarter, underperforming the 8.3% rise in the S&P 500 Index. The decline comes after several years of strong performances for energy stocks and reflects a 6.6% decrease in oil prices. Oil drilling activity has begun to pick up but remains well below historical high levels. Interestingly, the recent increase in active drilling rigs has not led to increased production. This may be a sign that the improvement in drilling techniques has begun to slow. Or it may simply represent a reduction in prime drilling targets.

We expect oil prices to remain above our long-term forecast of $60/bbl. for the foreseeable future. The combination of limited drilling, rising demand associated with improving economic conditions, and OPEC production cuts bodes well for oil prices. We believe oil prices will remain above our long-term projections of $60 per barrel for the foreseeable future.

The story for natural gas is less positive but improving. Natural gas prices have been on a downward trend for the last twelve months. Some of the decline can be attributed to warm weather this winter. Drillers have been slow to respond to low gas prices but have cut back activity since April. New LNG export capacity is coming online soon and should boost natural gas demand.

We believe the outlook for energy companies remains favorable. Oil prices are high and do not show signs of falling due to sharp production decline rates, rising demand due to improving global economic conditions, and active OPEC production cuts. Natural gas prices are low but should improve with a return to more normal weather, a reduction in supply due to less drilling activity, and an increase in demand for LNG exports. We believe the case for smaller cap energy stocks is especially strong.

Energy Stocks

Energy stocks, as measured by the XLE Energy Index, declined 2.0% in the 2023 second quarter, underperforming the 8.3% rise in the S&P 500 Index. The decline comes after several years of strong performances for energy stocks and reflects a 6.6% decrease in oil prices. The decline in oil prices came despite two OPEC production cuts and signs of improving global economic conditions.

Oil Prices

Figure #1

Drilling activity has begun to pick up but remains well below historical high levels. Interestingly, the recent increase in active drilling rigs has not led to increased production. This may be a sign that the improvement in drilling techniques has begun to slow. Or it may simply represent a reduction in prime drilling targets. Either way, it seems that cyclical oil price patterns of the past have become more muted. Drillers are taking a longer-term view of prices. We believe improved energy company fiscal discipline will lead to a period of prolonged high oil prices.

Figure #2

Stated another way, production from recently drilled wells does not increase production levels but goes to replace production declines from existing wells. As drillers shift to horizontal wells with longer laterals and increased fracking activity, oil production shifts towards the earlier years of a well’s life. However, that means that the production decline after initial production is greater, and more wells must be drilled just to replace production. The chart below, while somewhat dated, shows Permian Basin oil production separated by the year wells came on-line. The chart shows that in 2022, more than half of all oil production came from wells drilled in 2021 or 2022.

Figure #3

Source: Novi Labs

The combination of limited drilling, rising demand associated with improving economic conditions, and OPEC production cuts bodes well for oil prices. We believe oil prices will remain above our long-term projections of $60 per barrel for the foreseeable future.

Natural Gas Prices

The story for natural gas is less positive. Natural gas prices have been on a downward trend for the last twelve months. With the decline, we are beginning to hear reports of production curtailment. Some of the decline can be attributed to warm weather this winter. Natural gas storage levels are running above historical levels for this time of year. Drillers have been slow to respond to low gas prices. Active rigs targeting gas formations in the United States remained between 150 and 160 through April. However, since then, the rig count has plunged to the current level of 124.

Figure #4

The decline in natural gas prices in recent years has come despite a dramatic increase in natural gas exports in recent years. This trend continues with an additional 1 TCF/year of U.S. export capacity scheduled to come online by 2025. Whether or not that has an impact on natural gas prices remains to be seen.

Figure #5

Outlook

We believe the outlook for energy companies remains favorable. Oil prices are high and do not show signs of falling due to sharp production decline rates, rising demand due to improving global economic conditions, and active OPEC production cuts. Natural gas prices are low but should improve with a return to more normal weather, a reduction in supply due to less drilling activity, and an increase in demand for LNG exports. We believe the case for smaller cap energy stocks is especially strong. Major oil companies are facing increasing pressure to focus on renewable energy instead of producing more carbon-based fuel. Smaller cap energy companies are less tethered and often able to acquire and exploit properties being ignored by the majors.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. ANJESO is the first and only 24-hour, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Gregory Aurand, Senior Vice President, Equity Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Who is TeraImmune? The privately-held company is based in Germantown, Maryland and is focused on novel regulatory T cells (Tregs) therapies for autoimmune disease. TeraImmune has an approved FDA IND for their TI-168 autologous Factor VIII (FVIII) T-cell receptor Treg cell therapy to eliminate clotting factor FVIII inhibitors in Hemophilia A patients. The combined company anticipates moving this IND to a Phase 1/2a trial, and also expects to advance the development of TeraImmune’s innovative immune-cell therapies platform designed for conditions that suppress unwanted immune reactions.

Why the acquisition? TeraImmune is largely composed of former NIH researchers with scientific expertise who have developed a novel therapeutic platform, but have limited clinical development experience. Baudax Bio’s team has a proven ability in executing and progressing clinical trials. The combined company pipeline will now carry a promising therapy that is expected to move into clinicals (TI-168; FVIII inhibitors), as well as have an expected IND filing (BX3000; NMB reversal agent) that will also move into clinicals. The acquisition could also help resolve Baudax Bio’s Nasdaq deficiency issues by providing additional equity.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initial Bom Lugar well successful. Alvopetro completed its BL-06 well encountering a larger-than-expected pay zone confirming previously announced results for the well. The well is important because it is 100% owned and is primarily oil unlike current wells in the Cabure Field. Alvopetro management spoke about the well results in a recent Noble-sponsored non deal road show in St. Louis and New York.

The well will lead to expanded drilling. Alvopetro was very pleased with the results and said that successful production testing would lead to an expanded development drilling program. Management had previously indicated that it plans to drill two developmental wells in Bom Lugar in 2023. In the press release, management indicated its intent to mobilize the drilling rig to the Murucututu natural gas field while the Bom Lugar well is production tested.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.