Sale demonstrates continued progress in Conduent’s strategy to streamline its portfolio to drive increased focus on its core capabilities and enable synergistic growth

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global technology-led business solutions and services company, today announced it has successfully completed the sale of its Curbside Management Solutions and Public Safety Solutions businesses to Modaxo, a division of Constellation Software Inc. (TSX: CSU). The signing of the transaction was announced on December 28, 2023. The sale has a purchase price of $230 million.

“This divestiture marks another significant step in our efforts to concentrate on our core capabilities and foster growth that benefits both our shareholders and clients,” said Cliff Skelton, Conduent President and CEO. “With the completion of this sale, our focus remains on a smooth transition for our team members and clients as we continue to execute our growth strategy and advance toward our deployable capital goal.”

As outlined during Conduent’s 2023 investor briefing, the company set on a course to rationalize its business portfolio to increase focus on core capabilities, become more nimble, and enhance shareholder and client value.

Conduent will also continue to drive innovation in its Road Usage Charging Solutions and Transit Solutions businesses to enable streamlined, high-volume mobility services. The sale to Modaxo has no impact on these businesses.

Additional details of the transaction are outlined in Conduent’s 8-K filed with the U.S. Securities and Exchange Commission (SEC) today.

About Conduent

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 59,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $100 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com .

Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

Forward-Looking Statements

This press release may contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. The words “anticipate,” “believe,” “estimate,” “expect,” “plan,” “intend,” “will,” “aim,” “should,” “could,” “forecast,” “target,” “may,” “continue to,” “endeavor,” “if,” “growing,” “projected,” “potential,” “likely,” “see,” “ahead,” “further,” “going forward,” “on the horizon,” “enable,” “strategy,” and similar expressions (including the negative and plural forms of such words and phrases), as they relate to us, are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. All statements other than statements of historical fact included in this press release are forward-looking statements, including, but not limited to, statements regarding Conduent’s focus on continuing to provide a seamless transition for team members and clients as Conduent executes its growth strategy and advances towards its deployable capital goal, expectations that Conduent will continue to drive innovation in its Road Usage Charging Solutions and Transit Solutions businesses to enable streamlined, high-volume mobility services, and Conduent’s strategy to streamline its portfolio to drive increased focus on its core capabilities and enable synergistic growth, as well as to rationalize its business portfolio to increase focus on core capabilities, become more nimble, and enhance shareholder and client value. These statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions, many of which are outside of our control, that could cause actual results to differ materially from those expected or implied by such forward-looking statements contained in this press release, any exhibits to this press release and other public statements we make. Important factors and uncertainties that could cause actual results to differ materially from those in our forward-looking statements include, but are not limited to: Conduent’s ability to realize the benefits anticipated from the sale of its curbside management and public safety businesses; unexpected costs, liabilities or delays in connection with the transaction; the significant transaction costs associated with the transaction; negative effects of the announcement, pendency or consummation of the transaction on the market price of our common stock or operating results, including as a result of changes in key customer, supplier, employee or other business relationships; the risk of litigation or regulatory actions; our inability to retain and hire key personnel; the risk that certain contractual restrictions contained in the definitive transaction agreement could adversely affect our ability to pursue business opportunities or strategic transactions; and other factors that are set forth in the “Risk Factors” and other sections of our Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with or furnished to the Securities and Exchange Commission. Any forward-looking statements made by us in this press release speak only as of the date on which they are made. We are under no obligation to, and expressly disclaim any obligation to, update or alter our forward-looking statements, whether because of new information, subsequent events or otherwise, except as required by law.

HOUSTON, April 30, 2024 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (NASDAQ: GLDD) today announced that it will release the financial results for its three months ended March 31, 2024 on Tuesday, May 7, 2024 at 7:00 a.m. C.D.T. A conference call with the Company will be held the same day at 9:00 a.m. C.D.T.

Investors and analysts are encouraged to pre-register for the conference call by using the link below. Participants who pre-register will be given a unique PIN to gain immediate access to the call. Pre-registration may be completed at any time up to the call start time.

The live call and replay can also be heard at https://edge.media-server.com/mmc/p/wkfzmfb4 or on the Company’s website, www.gldd.com, under Events on the Investor Relations page. A copy of the press release will be available on the Company’s website.

The Company Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 134-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

For further information contact: Tina Baginskis Director, Investor Relations 630-574-3024

NEW YORK, April 30, 2024 /PRNewswire/ — Travelzoo® (NASDAQ: TZOO), the club for travel enthusiasts, today announced that its board of directors has authorized the repurchase of up to 1,000,000 shares of the Company’s outstanding common stock.

Purchases may be made, from time to time, in the open market and will be funded from available cash. The number of shares to be purchased and the timing of purchases will be based on the level of Travelzoo’s cash balances, general business and market conditions, and other factors, including alternative investment opportunities.

About Travelzoo We, Travelzoo®, are the club for travel enthusiasts. Our 30 million members receive exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Original seed investor has remained top MAIA stockholder

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company developing targeted immunotherapies for cancer, today announced that independent director Ms. Adelina Louie Ngar Yee made an individual purchase of 19,665 shares, and warrants for 19,665 shares, of MAIA’s common stock as part of the Company’s recent private placement of common stock and warrants to accredited investors and certain Company directors. The securities sold to the Company directors participating in the offering were issued pursuant to the Company’s 2021 Equity Incentive Plan.

Vlad Vitoc, M.D., MAIA’s Chairman and Chief Executive Officer, commented, “As a top investor in MAIA, we extend our deep appreciation to Adelina for both her longstanding support as director and for her participation in this offering alongside director Stan Smith and other long-term stockholders.”

In previous public remarks, Ms. Louie stated her belief that MAIA is at the critical point of bringing life-changing therapies to large populations of cancer sufferers.

Ms. Louie has 30 years of service with HSBC Group in a variety of functions, principally with businesses of Global Banking and Markets including investment and securities management, asset management, and global research. Most recently she was the Chief Operating Officer of Internal Audit at HSBC Group.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

Vancouver, British Columbia–(Newsfile Corp. – April 30, 2024) – Maple Gold Mines Ltd. (TSXV: MGM) (OTCQB: MGMLF) (FSE: M3G) (“Maple Gold” or the “Company“) is pleased to provide an operational update related to the advancement of the Company’s gold projects located in Québec, Canada. Consistent with the Company’s value-oriented exploration strategy, the ongoing synthesis and reinterpretation of multiple exploration datasets by the Company’s revamped technical team is nearing completion, while management continues to significantly reduce costs and preserve capital as demonstrated in the Company’s audited financial results for the year ended December 31, 2023. The Company also announces that its Board of Directors has approved the issuance of annual equity incentive grants to certain employees, officers, directors and consultants.

Operational Update

Since late 2023, Maple Gold has been engaged in a systematic review and compilation of the extensive technical database on its entire ~400 km2 property package that straddles the fertile Casa Berardi Break and contains an established near-surface, multi-million ounce gold mineral resource as well as a past-producing high-grade gold mine complex. This critical re-evaluation is aimed at integrating all available geological, geophysical, geochemical and drilling data to improve target generation and drive exploration results. The Company’s technical team is nearing completion of a new 3D litho-structural model based on selective core relogging within mineralized zones, updated level plans, longitudinal and cross-sections, and detailed geophysical and geochemical data analysis that will support the focused ranking and prioritization of property-wide drill targets to be tested later this year. As part of this exercise, the Company has also initiated high-resolution drone magnetic surveys in selected areas, which will be completed in the next following weeks.

“With the support of our partner and key stakeholders, we have seized this golden opportunity to reposition the Company for future success by delivering a high-quality exploration model supported by a wealth of technical data while simultaneously right-sizing our business,” stated Kiran Patankar, President and CEO of Maple Gold. “We believe as strongly as ever in the compelling discovery potential offered by our strategically located district-scale gold projects. The culmination of these efforts is well-timed amid surging gold prices and increasing investment focus on organic growth through the drill bit.”

The Company has engaged with notable geological, geophysical and geochemical specialists to assist with the ongoing interpretation of the vast amount of exploration data that has been collected by Maple Gold and others over the past 50 years. This includes current members of the Company’s Technical Committee: Dr. Gérald Riverin, Mr. Maurice Tagami, P.Eng. and Mr. Paul Harbidge. The results of the geologic reinterpretation are being finalized and will be reported shortly. Drilling is expected to recommence later this year with full details to be provided in subsequent announcements.

Annual Equity Incentive Plan Grants

Pursuant to its Equity Incentive Plan (the “Plan”) dated December 17, 2020, as amended, and the policies of the TSX Venture Exchange, the Company’s Board of Directors granted stock options (“Options”), Restricted Share Units (“RSUs”) and Deferred Share Units (“DSUs”) to certain employees, officers, directors and consultants. The Company granted Options to purchase an aggregate of 4,000,000 common shares of the Company (each, a “Common Share”), with an exercise price of $0.08 per Common Share. Each Option grant vests in three equal tranches over a 24-month period. Once vested, each Option is exercisable into one Common Share for a period of five years from the date of the grant. The Company also granted a total of 3,250,000 RSUs and 725,000 DSUs. Each RSU grant vests in three equal tranches over a 24-month period. Once vested, each RSU and DSU entitles the holder thereof to receive either one Common Share, the cash equivalent of one Common Share or a combination of cash and Common Shares, as determined by the Company, net of applicable withholdings. DSUs may not be exercised until a director ceases to serve on the Company’s Board of Directors.

Further details regarding the Plan are set out in the Company’s Management Information Circular filed on May 15, 2023, which is available on SEDAR.

Qualified Person

The scientific and technical data contained in this press release was reviewed and prepared under the supervision of Jocelyn Pelletier, M.Sc., P.geo., Chief Geologist of Maple Gold. Mr. Pelletier has verified the data related to the exploration information disclosed in this press release through his direct participation in the work performed. Mr. Pelletier is a Qualified Person under National Instrument 43-101 Standards of Disclosure for Mineral Projects.

About Maple Gold

Maple Gold Mines Ltd. is a Canadian advanced exploration company in a 50/50 joint venture with Agnico Eagle Mines Limited to jointly advance the district-scale Douay and Joutel gold projects located in Québec’s prolific Abitibi Greenstone Gold Belt. The projects benefit from exceptional infrastructure access and boast ~400 km2 of highly prospective ground including an established gold resource at Douay (SLR 2022) that holds significant expansion potential as well as the past-producing Telbel and Eagle West mines at Joutel. In addition, the Company holds an exclusive option to acquire 100% of the Eagle Mine Property, a key part of the historical Joutel mining complex.

The district-scale property package also hosts a significant number of regional exploration targets along a 55-km strike length of the Casa Berardi Deformation Zone that have yet to be tested through drilling, making the project ripe for new gold and polymetallic discoveries. The Company is well capitalized and is currently focused on carrying out exploration and drill programs to grow resources and make new discoveries to establish an exciting new gold district in the heart of the Abitibi. For more information, please visit www.maplegoldmines.com.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS PRESS RELEASE.

Forward Looking Statements:

This press release contains “forward-looking information” and “forward-looking statements” (collectively referred to as “forward-looking statements”) within the meaning of applicable Canadian securities legislation in Canada, including statements about exploration work and results from current and future work programs. Forward-looking statements are based on assumptions, uncertainties and management’s best estimate of future events. Actual events or results could differ materially from the Company’s expectations and projections. Investors are cautioned that forward-looking statements involve risks and uncertainties. Accordingly, readers should not place undue reliance on forward-looking statements. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to Maple Gold Mines Ltd.’s filings with Canadian securities regulators available on www.sedarplus.ca or the Company’s website at www.maplegoldmines.com. The Company does not intend, and expressly disclaims any intention or obligation to, update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law.

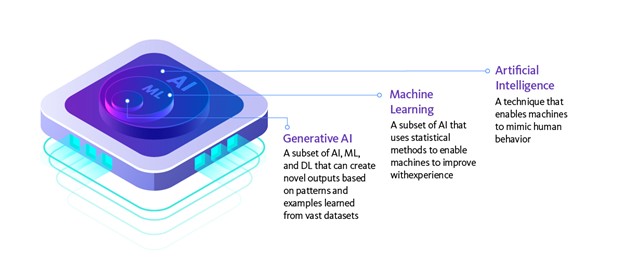

Initiative initially focused on generative AI implementation in healthcare claims management, customer service platforms and fraud detection

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global technology-led business solutions and services company, today announced an innovation initiative with Microsoft that will use Microsoft Azure OpenAI Service to bring the power of generative AI to drive quality, productivity and faster cycle times for Conduent’s global clients.

The innovative initiative initially is exploring generative AI implementation in healthcare claims management, customer service platforms and fraud detection, with three pilots underway. By integrating generative AI into its client offerings and internal operations, Conduent builds on its longstanding history of delivering technologies and solutions that improve client operating and cost performance, enhance customer experience and optimize business processes.

“With a heritage built on helping our clients improve their business performance through technologies such as automation, machine learning, and digitalization, we are excited to collaborate with Microsoft to develop the next generation of business solutions that will be powered by generative AI,” said Cliff Skelton, Conduent President and Chief Executive Officer. “We are focused on harnessing the potential of generative AI to further advance our solutions and capabilities leading to improved quality, efficiency and productivity for our clients and in our own operations.”

“Generative AI has the power to transform how businesses and organizations operate – serving as a force-multiplier to improve efficiencies and enhance customer experiences across a range of industries,” said Svetlana Reznik, GM Data & AI at Microsoft. “Our collaboration with Conduent will help accelerate AI adoption for their customers in a secure cloud environment.”

Creating innovation in business processes through generative AI As a BPaaS leader with a diversified portfolio of solutions and industries served, Conduent is in a unique position to evaluate and embed generative AI across a range of applications and sectors.

Through this AI initiative, Conduent and Microsoft will be collaborating on multiple use cases across a variety of business processes. These use cases will use dedicated instances of AI to protect Conduent’s and its clients’ data. The generative AI pilots underway include:

Intelligent data harvesting from healthcare claims documents for faster adjudication by implementing Azure AI Document Intelligence and Azure OpenAI Service

Increasing the volume and speed of fraud detection processing in payments by using Azure Data Factory and Azure OpenAI Service

Improving customer service agent responsiveness by using Azure AI Language Service, Azure AI Speech Service and Azure OpenAI Service

About Conduent Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 59,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $100 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com .

Trademarks Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

LOS ANGELES, April 29, 2024 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 13 other restaurant concepts, today announced that the Company will host a conference call to review its first quarter 2024 financial results on Wednesday, May 1, 2024 at 5:00 PM ET. A press release with first quarter 2024 financial results will be issued prior to the conference call that day.

The conference call can be accessed live over the phone by dialing 1-844-826-3035 from the U.S. or 1-412-317-5195 internationally. A replay will be available after the call until Wednesday, May 22, 2024, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 10187929. Hosting the call will be Andy Wiederhorn, Chairman, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call will also be webcast live from the corporate website at www.fatbrands.com, under the “Investors” section. A replay of the webcast will be available through the corporate website shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Dr. Smith has participated in every MAIA funding round

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company developing targeted immunotherapies for cancer, today announced that independent director Stan V. Smith, Ph.D. made an individual purchase of 147,492 shares, and warrants for 147,492 shares, of MAIA’s common stock as part of the Company’s recent private placement of common stock and warrants.

On April 23, 2024, MAIA entered into definitive agreements for the purchase and sale of an aggregate of 494,096 shares of common stock at a purchase price of $2.034 per share, in a private placement to accredited investors and certain Company directors. Each share of common stock was offered together with a warrant to purchase one share of common stock at an exercise price of $2.26 per share. The gross proceeds from the offering are approximately $1.0 million, prior to offering expenses payable by the Company. The securities sold to the Company directors participating in the offering were issued pursuant to the Company’s 2021 Equity Incentive Plan.

“Our independent directors continue to show their support and conviction for our new science which utilizes a novel dual mechanism of action for cancer therapy: telomere targeting and immunogenicity,” said Vlad Vitoc, M.D., MAIA’s Chairman and Chief Executive Officer. “We especially thank Stan for his unwavering participation in every round of MAIA’s financing dating back to 2022.”

Dr. Smith recently spoke about his confidence in MAIA, stating in part, “I am a big believer in MAIA’s telomere-targeting approach to cancer and its potential to disrupt the field of research and development for cancer therapies.”

Dr. Smith is president of Smith Economics Group, Ltd. in Chicago, providing economic and financial consulting nationwide. Trained at the University of Chicago and specializing in litigation economics, Dr. Smith co-authored the first textbook on the subject of economic damages. Dr. Smith has served as an adjunct professor at the University of Chicago and at DePaul University College of Law where he created the first course in the United States in forensic economics.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

SAN DIEGO, April 29, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the first quarter 2024 after the close of market on Tuesday, May 7th. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this OnlineForm. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

GAITHERSBURG, Md., April 29, 2024 /PRNewswire/ — YS Biopharma Co., Ltd. (Nasdaq: YS) (“YS Biopharma” or the “Company”), a global biopharmaceutical company dedicated to discovering, developing, manufacturing, and delivering new generations of vaccines and therapeutic biologics for infectious diseases and cancer, today announced that it received an extension of 180 calendar days (the “Extension Notice”) from The Nasdaq Stock Market LLC (“Nasdaq”) to regain compliance with the Nasdaq’s minimum $1.00 bid price requirement set forth in Nasdaq Listing Rule 5550(a)(2) for continued listing on The Nasdaq Capital Market (the “Bid Price Requirement”), following the expiration of the initial 180 calendar days period to regain compliance on April 22, 2024.

As previously announced, the Company received a written notification from Nasdaq dated October 24, 2023, indicating that because the closing bid price of the Company’s ordinary shares for the last 31 consecutive business days was below $1.00 per share, the Company was not in compliance with the Bid Price Requirement, and Nasdaq granted the Company a period of 180 calendar days, or until April 22, 2024, to regain compliance with the Bid Price Requirement.

As of the date hereof, the Company has not regained compliance with the Bid Price Requirement. That being said, pursuant to the Extension Notice, the Company is eligible for an additional 180 calendar day period, or until October 21, 2024, to regain compliance with the Bid Price Requirement. To regain compliance, the Company’s ordinary shares must have a closing bid price of at least US$1.00 per share for a minimum of 10 consecutive business days, at which point the matter will be closed. In the event that the compliance cannot be demonstrated by October 25, 2024, the staff of Nasdaq will provide written notification that the Company’s securities will be delisted.

The Company intends to monitor the closing bid price of its ordinary shares between now and October 21, 2024 and is considering its options in order to regain compliance with the Bid Price Requirement. The Extension Notice does not affect the Company’s business operations, its U.S. Securities and Exchange Commission reporting requirements, or its contractual obligations.

About YS Group

YS Group is a global biopharmaceutical company dedicated to discovering, developing, manufacturing, and delivering new generations of vaccines and therapeutic biologics for infectious diseases and cancer. It has developed a proprietary PIKA® immunomodulating technology platform and a new generation of preventive and therapeutic biologics targeting Rabies, Coronavirus, Hepatitis B, Influenza, Shingles, and other virus infections. YS Biopharma operates in China, the United States, Singapore, and the Philippines, and is led by a management team that combines rich local expertise and global experience in the biopharmaceutical industry. For more information, please visit investor.ysbiopharma.com.

This press release contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical or current fact included in this press release are forward-looking statements, including but not limited to statements regarding the expected growth of YS Biopharma, the development progress of all product candidates, the progress and results of all clinical trials, YS Biopharma’s ability to source and retain talent, and the cash position of YS Biopharma. Forward-looking statements may be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These statements are based on various assumptions, whether identified in this press release, and on the current expectations of YS Biopharma’s management and are not predictions of actual performance.

YS Biopharma cannot assure you the forward-looking statements in this press release will be accurate. These forward-looking statements are subject to a number of risks and uncertainties, including those included under the heading “Risk Factors” in the Post-effective Amendment No. 2 to the Company’s Registration Statement on Form F-1 filed with the SEC on January 23, 2024, and other filings with the SEC. There may be additional risks that YS Biopharma does not presently know or that YS Biopharma currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In light of the significant uncertainties in these forward-looking statements, nothing in this press release should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. The forward-looking statements in this press release represent the views of YS Biopharma as of the date of this press release. Subsequent events and developments may cause those views to change. However, while YS Biopharma may update these forward-looking statements in the future, there is no current intention to do so, except to the extent required by applicable law. You should, therefore, not rely on these forward-looking statements as representing the views of YS Biopharma as of any date subsequent to the date of this press release. Except as may be required by law, YS Biopharma does not undertake any duty to update these forward-looking statements.

This publication, authored by leading experts in inflammasome-mediated inflammation and neurology at University of Miami Miller School of Medicine, demonstrates that multiple inflammasome triggers (NLRP1 and pyrin) govern the inflammatory response in Alzheimer’s Disease (AD), and that release of inflammasome laden extracellular vesicles (EV) into the blood induce significant inflammation in cardiovascular cells.

ZyVersa is developing Inflammasome ASC Inhibitor IC 100 to inhibit multiple types of inflammasomes, including NLRP1 and pyrin, and their associated ASC specks that trigger damaging inflammation and its spread to surrounding tissues.

AD, a progressive neurodegenerative disease affecting 6.7 million people in the US, is associated with many comorbidities, especially heart disease and stroke, resulting in increased morbidity and mortality.

WESTON, Fla., April 29, 2024 (GLOBE NEWSWIRE) — ZyVersa Therapeutics, Inc. (Nasdaq: ZVSA, or “ZyVersa”), a clinical stage specialty biopharmaceutical company developing first-in-class drugs for treatment of inflammatory and renal diseases, announces that acclaimed inflammasome researchers from the University of Miami Miller School of Medicine and inventors of Inflammasome ASC Inhibitor IC 100, have published a scientific paper in the peer-reviewed journal, Frontiers in Molecular Neuroscience, highlighting how inflammasome-mediated inflammation in Alzheimer’s disease can trigger inflammation in the heart.

NLRP1, pyrin, caspase-1, and ASC were significantly elevated in the cortex of AD mice.

In AD mice, there was a heightened level of inflammatory proteins circulating in the body via EVs containing an inflammasome protein cargo.

Inflammasome activation was demonstrated in the heart of AD mice, associated with an increase in ASC oligomerization into specks.

In adoptive transfer experiments, EVs released from AD patients induced significant inflammation in cardiovascular cells when compared to EVs from healthy individuals.

“Our data provide evidence that there is a neural-cardiac axis mediated by EVs in AD. Therefore, inflammasomes may provide a novel therapeutic target for the treatment of cardiac comorbidities in AD and beyond,” said Juan Pablo de Rivero Vaccari, Associated Professor of Neurological Surgery and The Miami Project to Cure Paralysis at the University of Miami.

“This research reinforces the importance of attenuating activation of multiple types of inflammasomes that govern the inflammatory response in AD and mediating systemic inflammatory signals in EVs to control the spread of damaging inflammation to cardiovascular and other cells,” commented Stephen C. Glover, ZyVersa’s Co-founder, Chairman, CEO, and President. “ZyVersa’s Inflammasome ASC inhibitor IC 100 is designed to inhibit formation of multiple types of inflammasomes to attenuate initiation of the inflammatory cascade and to inhibit their associated ASC specks to reduce spread and perpetuation of damaging inflammation.”

To review a white paper summarizing the mechanism of action and preclinical data for IC 100, Click Here.

About Inflammasome ASC Inhibitor IC 100

IC 100 is a novel humanized IgG4 monoclonal antibody that inhibits the inflammasome adaptor protein ASC. IC 100 was designed to attenuate both initiation and perpetuation of the inflammatory response. It does so by binding to a specific region of the ASC component of multiple types of inflammasomes, including NLRP1, NLRP2, NLRP3, NLRC4, AIM2, and Pyrin. Intracellularly, IC 100 binds to ASC monomers, inhibiting inflammasome formation, thereby blocking activation of IL-1β early in the inflammatory cascade. IC 100 also binds to ASC in ASC Specks, both intracellularly and extracellularly, further blocking activation of IL-1β and the perpetuation of the inflammatory response that is pathogenic in inflammatory diseases. Because active cytokines amplify adaptive immunity through various mechanisms, IC 100, by attenuating cytokine activation, also attenuates the adaptive immune response.

About ZyVersa Therapeutics, Inc.

ZyVersa (Nasdaq: ZVSA) is a clinical stage specialty biopharmaceutical company leveraging advanced, proprietary technologies to develop first-in-class drugs for patients with renal and inflammatory diseases who have significant unmet medical needs. The Company is currently advancing a therapeutic development pipeline with multiple programs built around its two proprietary technologies – Cholesterol Efflux Mediator™ VAR 200 for treatment of kidney diseases, and Inflammasome ASC Inhibitor IC 100, targeting damaging inflammation associated with numerous CNS and other inflammatory diseases. For more information, please visit www.zyversa.com.

Certain statements contained in this press release regarding matters that are not historical facts, are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. These include statements regarding management’s intentions, plans, beliefs, expectations, or forecasts for the future, and, therefore, you are cautioned not to place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. ZyVersa Therapeutics, Inc (“ZyVersa”) uses words such as “anticipates,” “believes,” “plans,” “expects,” “projects,” “future,” “intends,” “may,” “will,” “should,” “could,” “estimates,” “predicts,” “potential,” “continue,” “guidance,” and similar expressions to identify these forward-looking statements that are intended to be covered by the safe-harbor provisions. Such forward-looking statements are based on ZyVersa’s expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements due to a number of factors, including ZyVersa’s plans to develop and commercialize its product candidates, the timing of initiation of ZyVersa’s planned preclinical and clinical trials; the timing of the availability of data from ZyVersa’s preclinical and clinical trials; the timing of any planned investigational new drug application or new drug application; ZyVersa’s plans to research, develop, and commercialize its current and future product candidates; the clinical utility, potential benefits and market acceptance of ZyVersa’s product candidates; ZyVersa’s commercialization, marketing and manufacturing capabilities and strategy; ZyVersa’s ability to protect its intellectual property position; and ZyVersa’s estimates regarding future revenue, expenses, capital requirements and need for additional financing.

New factors emerge from time-to-time, and it is not possible for ZyVersa to predict all such factors, nor can ZyVersa assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements included in this press release are based on information available to ZyVersa as of the date of this press release. ZyVersa disclaims any obligation to update such forward-looking statements to reflect events or circumstances after the date of this press release, except as required by applicable law.

This press release does not constitute an offer to sell, or the solicitation of an offer to buy, any securities.

Corporate, Media, and IR Contact: Karen Cashmere Chief Commercial Officer kcashmere@zyversa.com 786-251-9641

Large-Scale Nevada-based Lithium Project: three-phase production plan will generate a life-of-mine average of 34,000 tonnes per annum (tpa) of battery-quality lithium carbonate (Li2CO3)

Innovative Approach in Processing: patent-pending chloride leaching process combined with Direct Lithium Extraction (DLE), the Feasibility Study is supported by 2+ years of testing at the Company’s Pilot Plant

Mineral Resource Estimate: Measured and Indicated resources totaling 1,207.33 million tonnes (Mt) at an average grade of 957 parts per million (ppm) lithium (Li) containing 1.155 Mt of Li or 6.148 Mt of lithium carbonate equivalent (LCE)

Long 40-Year Mine Life: Proven and Probable Mineral Reserve Estimate totaling 287.65 Mt at an average grade of 1,149 ppm Li containing 0.330 Mt of lithium or 1.759 Mt of LCE

Initial Project: Phase 1 Capital Cost $1.537 billion for production capacity of 13,000 tpa LCE

Designed for Expansion: Phase 2 $0.651 billion for 28,000 tpa LCE, and Phase 3 $1.336 billion for 41,000 tpa LCE; Project expansions are capitalized with Project cash flow

Low Operating Cost: average operating cost $8,223/t of Li2CO3 produced, or $2,766/t after sales of surplus sodium hydroxide (NaOH)

After-tax IRR of 17.1% at $24,000/t Li2CO3: $3.01 billion after-tax net present value (NPV) at 8% discount rate and a 17.1% after-tax internal rate of return (IRR), using price assumptions of $24,000/t for Li2CO3 and $600/dry metric tonne (dmt) for NaOH

April 29, 2024 – Vancouver, Canada – Century Lithium Corp. (TSXV:LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (Century Lithium or the Company) is pleased to announce the results of a National Instrument 43-101 (NI 43-101) feasibility study (Feasibility Study, FS or Study) completed on its 100% owned Clayton Valley Lithium Project (Project) in Nevada, USA. The Feasibility Study was prepared by Wood Group USA, Inc. (Wood) and Global Resource Engineering, Ltd. (GRE). All currency amounts in this news release are presented in U.S. dollars.

“Century Lithium is proud to present our Feasibility Study. The Study indicates our Project has robust economics, made possible with our unique chlor-alkali and DLE processes” commented Bill Willoughby, President, and CEO. “Completion of the Study marks a major milestone for the Company and is the result of the dedicated work and efforts of our team of employees and consultants.”

“Our process technology was developed by way of many trials and successes at our Pilot Plant in Amargosa Valley. As one of the few lithium-focused Pilot Plants in North America, we continue to operate safely and recently passed two years of testing. The data generated to date supports the Feasibility Study, and we continue to test various conditions and ideas to improve our process flow sheet,” said Bill Willoughby.

With the Feasibility Study completed, the Company will now direct its focus on engineering and permitting. The Company is concurrently advancing discussions with government agencies, strategic partners, and other interested parties to provide funding to advance the Project and maximize the value to the Company’s shareholders that is reflected in the FS.

FEASIBILITY STUDY SUMMARY

The information in the following tables highlight the Project’s production and economic summaries.

Production Summary

Phase

Years

Mine tonnes per day (tpd)

Li2CO3 (tpa)

Capital Cost (B$)

1

1-5

7,500

13,000

$1.537

2

6-10

15,000

28,000

$0.651

3

11+

22,500

41,000

$1.336

Economic Summary

Units

Amount

Operating Costs (average)

$/t

8,223

Operating Costs (average w/NaOH credit)

$/t

2,766

After-tax NPV @ 8% Discount Rate

$ billion

3.01

After-tax IRR

%

17.1

RESOURCE AND RESERVES

The Mineral Resource and Reserve Estimates for the Project were updated for the Feasibility Study and built using geologic data and 1,318 lithium assays from 45 core holes drilled between 2017 and 2022. The constrained Measured and Indicated Resource Estimate is 1,207.33 Mt with an average grade of 957 ppm lithium and contains 1.155 Mt of Li or 6.148 Mt of LCE. The Proven and Probable Mineral Reserve Estimate was derived from the constrained Mineral Resources and contains 287.65 Mt with an average grade of 1,149 ppm lithium and contains 0.330 Mt of Li or 1.759 Mt of LCE and reflects an increase of 74.6 Mt and 0.48 Mt LCE compared to the 2021 Mineral Reserve Estimate. The Mineral Resources were generated with a pit shell that encompasses all mineralized material within the Property excluding all areas that will be used for Project infrastructure and placement of tailings, waste, and low-grade material.

Mineral Resource Estimate

Domain

Tonnes Above Cut-off (millions)

Li Grade (ppm)

Li Contained (million t)

LCE (million t)

Measured

858.38

990

0.849

4.524

Indicated

348.95

875

0.305

1.625

Measured & Indicated

1,207.33

957

1.155

6.148

Inferred

119.03

827

0.098

0.524

The effective date of the Mineral Resource Estimate is December 15, 2022. The QP for the estimate is Ms. Terre Lane, MMSA, an employee of GRE and independent of Century. The Mineral Resources are constrained by a pit shell with a 200 ppm Li cut-off and density of 1.505 g/cm3. The cut-off grade considers an operating cost of $16.90/t mill feed, process recovery of 83% and a long-term lithium carbonate price of $20,000/t. The Mineral Resource estimate was prepared in accordance with CIM Definition Standards (CIM, 2014) and the CIM Estimation of Mineral Resources and Mineral Reserves Best Practice Guidelines (CIM, 2019). Mineral Resource figures were rounded. One tonne of lithium = 5.323 tonnes lithium carbonate. Mineral Resources are inclusive of Mineral Reserves.

Mineral Reserve Estimate

Domain

Tonnes Above Cut-off (millions)

Li Grade (ppm)

Li Contained (million t)

LCE (million t)

Proven

266.39

1,147

0.306

1.626

Probable

21.26

1,174

0.025

0.133

Proven & Probable

287.65

1,149

0.330

1.759

The effective date of the Mineral Reserve Estimate is December 15, 2022. The QP for the estimate is Ms. Terre Lane, MMSA, an employee of GRE and independent of Century. The Mineral Reserve estimate was prepared in accordance with CIM) Definition Standards (CIM, 2014) and the CIM Estimation of Mineral Resources and Mineral Reserves Best Practice Guidelines (CIM, 2019). Mineral Reserves are reported within the final pit design at a mining cut-off of 900 ppm. The cut-off grade considers a mine operating cost of $1.98/t, a process operating cost of $14.27/t milled, a G&A cost of $0.65/t milled, process recovery of 83% and a long-term lithium carbonate price of $20,000/t. The cut-off of 900 ppm is an elevated cut-off selected for the mine production schedule as the elevated cutoff is 4.5 times higher than the break-even cut-off grade. Mineral Reserve figures have been rounded. One tonne of lithium = 5.323 tonnes lithium carbonate. Mineral Resources are inclusive of Mineral Reserves.

PROCESS METALLURGY & CHLOR-ALKALI PLANT

Metallurgical testing through 2020 focused on using sulfuric acid (H2SO4) to extract lithium from the clay. In late 2020, testing shifted to hydrochloric acid (HCl) for its improved compatibility with the deposit’s chemistry. These benefits included higher lithium extractions, lower reagent consumptions, significantly better filtration of solids, and the ability to utilize certain DLE technologies in the recovery and concentration of lithium from the leach solutions.

A key component of the Project with chloride-based leaching is a chlor-alkali plant. The chlor-alkali plant provides the ability to produce the key reagents HCl and NaOH on-site from the electrolysis of a sodium chloride (NaCl) solution. A chlor-alkali plant represents a greater capital investment relative to that of a sulfuric acid plant but has important environmental and economic benefits for the sustainability of the Project. These benefits include replacing the purchase and transportation of sulfur with regionally sourced salt, and a reduction in emissions and the physical footprint of the operation with dryer, non-sulfate tailings.

Additionally, the chlor-alkali plant will generate significant quantities of NaOH surplus to the Project’s operational needs and therefore available for sale. The chlor-alkali plant will utilize modern electrochemical cell technology thereby producing membrane grade sodium hydroxide without the energy consumption and environmental problems of older technologies. The surplus amounts of NaOH are inherent to the operation of the plant and the sales represent a significant offset to the Project’s operating costs.

PILOT PLANT

In 2021, Century Lithium constructed a Pilot Plant in Nevada to leach one tonne per day of lithium clay and produce a high-grade lithium chloride solution which is processed off-site at Saltworks Technologies, Inc. (Saltworks), at their Richmond, British Columbia processing plant to make battery-quality Li2CO3. To maximize lithium recovery, the Company purchased the license rights and pilot-stage equipment to DLE an ion-exchange-based process and incorporated it into the Pilot Plant. The DLE license is held in perpetuity and royalty free by the Project.

Throughout its Pilot Plant program, the Company has sought improvement in its process methods. The Company obtained a provisional patent in 2023 with the U.S. Patent and Trademark Office, U.S. Department of Commerce. The provisional patent is titled System and Method for Extracting Lithium from Clay and Other Materials in a Chloride Solution Using Individualized Pretreatments. The patent pending process encompasses the Company’s flowsheet and protects its methods of leaching lithium-bearing solids and handling solutions, precipitates, and residues.

LITHIUM EXTRACTION, RECOVERY & Li2CO3 PRODUCTION

A lithium recovery of 78% is used in the Feasibility Study, based on the data collected in over two years of operations at the Pilot Pant.

Feed material grades averaged 1,100 ppm

Leach solution samples varied from 200 to 320 ppm Li

Lithium extractions averaged 88% and varied from 80 to 95%

DLE lithium recoveries were typically above 90%

10% of the lithium in solution is retained in the moisture remaining in the tailings

Extraction rates do not account for losses downstream and are only indicative of the potential overall recovery. Work at the Pilot Plant continues to focus on reducing losses of lithium to tailings. A small loss of lithium from processing the DLE product solutions into Li2CO3, and the recycling of process solutions to the DLE and leach areas is anticipated.

During 2022 and 2023, Saltworks processed the DLE product solutions from the Pilot Plant and made battery-quality Li2CO3 at greater than 99.5% purity. Modifications at the Pilot Plant in mid-2023 increased lithium solution grades to over 14 grams per liter which simplified the flowsheet and eliminated the evaporation stage for production of Li2CO3.

PRODUCTION PLAN

The Project’s production plan comprises three equal phases of production rate increases, Phase 1 and Phase 2 production rates are maintained over five years each and Phase 3 is maintained for 30 years. This approach was selected to reduce capital exposure and risk by dividing the Project’s production schedule into realistic phases of construction and equipment installation. The plan fully utilizes the Project’s Mineral Reserve.

Phase 1 includes all work required to implement the Initial Project Plan including all necessary mining and processing infrastructure. The Phase 2 cost estimate focuses on an expansion within the footprint of Phase 1. Phase 3 development includes an additional processing plant and facilities not built in the previous phases and allows for a fourth phase of expansion.

LITHIUM CARBONATE AND SODIUM HYDROXIDE SALES PRICES

A price of $24,000/t of Li2CO3 is used in the Feasibility Study as the Project base case. This price is selected as a conservative mid-point between current market prices which are under $20,000/t Li2CO3 and forecast prices obtained from Benchmark Mineral Intelligence which are in the range of $23,000 to $39,000/t Li2CO3 during Phase 1 and $29,000 to $31,000/t Li2CO3 thereafter (Benchmark Mineral Intelligence, Lithium Forecast Q1 2024). The sales price is free on board (FOB) the Project site for battery quality Li2CO3.

NaOH is a product of the chlor-alkali process and a sales price of $600/dmt FOB the Project is used in the Feasibility Study as the Project base case. Based on the material mass balance, it is expected that surplus NaOH will be available for sale at rates of 120,000 to 360,000 dmt per annum, depending on Project Phase. This price is based on a February 2023 market study by Global Exchange and Trading, Inc. where it was determined the Project’s surplus NaOH can be readily sold in the western U.S. which currently relies heavily on imports arriving at west coast ports.

CAPITAL COST ESTIMATE

The basis for the capital cost estimate follows AACE Class 3 for feasibility studies. Contributors to the estimates are GRE (mining), Wood (process plant and infrastructure), ThyssenKrupp Nucera (chlor-alkali plant) and Century Lithium (property information and owners’ costs). The capital cost estimates by phase are summarized as follows.

Installed Capital Costs

Initial Phase 1 ($M)

Expansion Phase 2 ($M)

Expansion Phase 3 ($M)

Mining & Site Preparation

$64

$7

$27

Process Facilities

$517

$205

$477

Chlor-Alkali Plant

$496

$336

$496

Buildings, Services & Infrastructure

$130

$5

$42

Indirect & Owners Costs

$234

$72

$190

Contingency

$96

$27

$105

Total Capital Cost

$1,537

$651

$1,336

Notes: Totals may not sum due to rounding, Contingency and site Indirects for chlor-alkali plant is included in the Chlor-Alkali Plant line item, contingency for mining is included in the Contingency line item, indirect costs for mining are not included in the Indirects and Owner’s Costs line item

The Phase 2 capital costs represent the expansion of the process facilities and infrastructure established in Phase 1. The Phase 3 capital costs support an additional processing plant and facilities not built in the previous phases. In the Project schedule, a 2-year period is allocated for the time to construct and commission each phase.

Sustaining capital over the life of the Project is estimated at $315 million for tailings facility expansion and equipment replacements. These costs are in addition to the expansion capital costs shown above.

OPERATING COST ESTIMATES

The following information highlights the operating cost estimates for each phase in dollars per tonne of Li2CO3, before and after deducting sales of surplus NaOH.

Initial Phase 1 (7,500 tpd mill feed)

$ (000s)/y

$/t mill feed

$/t LCE

Mining

$13,754

$5.43

$1,205

Processing and G&A

$57,515

$21.01

$4,428

Chlor-Alkali Plant

$61,787

$22.57

$4,757

Total Operating Cost

$133,056

$49.01

$10,390

Less NaOH Sales (FOB mine)

$78,272

$28.95

$6,026

Net Operating Cost

$54,784

$20.06

$4,364

Note: Totals may not sum due to rounding

Expansion Phase 2 (15,000 tpd mill feed)

$ (000s)/y

$/t mill feed

$/t LCE

Mining

$24,901

$4.26

$766

Processing and G&A

$82,018

$14.98

$3,157

Chlor-Alkali Plant

$105,138

$19.20

$4,047

Total Operating Cost

$212,057

$38.44

$7,970

Less NaOH Sales (FOB mine)

$142,350

$26.00

$5,479

Net Operating Cost

$69,707

$12.44

$2,491

Note: Totals may not sum due to rounding

Expansion Phase 3 (22,500 tpd mill feed)

$ (000s)/y

$/t mill feed

$/t LCE

Mining

$22,064

$2.70

$561

Processing and G&A

$119,945

$14.60

$3,078

Chlor-Alkali Plant

$151,325

$18.43

$3,884

Total Operating Cost

$293,334

$35.73

$7,523

Less NaOH Sales (FOB mine)

$213,525

$25.99

$5,479

Net Operating Cost

$79,809

$9.74

$2,044

Note: Totals may not sum due to rounding

ECONOMIC MODEL AND SENSITIVITY

The cash flow model is developed using base prices of $24,000/t for Li2CO3 and $600/dmt for NaOH.

Average Annual Values

Units

Initial Phase 1

Expansion Phase 2

Expansion Phase 3

Li2CO3 Sales

t

11,885

26,753

39,098

NaOH Sales

dmt

130,488

237,250

355,875

Gross Sales

$ million

$282.4

$635.7

$929.0

Before-tax Cash Flow

$ million

$231.3

$553.3

$825.3

Lithium carbonate sales are the average over each Phase including ramp up to the stated production rate. Gross sales are revenues from Li2CO3 and NaOH sales are before operating costs and after royalty. Before-tax Cash Flow is gross sales minus operating costs. Taxes are applied at federal, state and county rates after allowances for amortization, depletion, and depreciation only. Possible tax credits under the U.S. Inflation Reduction Act or other programs are not included.

The Project base case generates a 17.1% after-tax IRR and NPV-8% of $3.01 billion. These results are sensitive to changes in operating assumptions including the sales price of Li2CO3.

At 75% of the base case, or $18,000/t LCE, the after-tax NPV@ 8% is $1.52 billion, and the after-tax IRR is 12.9%.

At 125% of the base case, or $30,000/t LCE, the after-tax NPV@ 8% is $4.47 billion, and the after-tax IRR is 20.9%.

For every $1,000/t change in the price of lithium carbonate, the after-tax NPV@8% changes by about $250 million.

Project Sensitivity

Units

75%

Base Case

125%

Lithium Price

$/t LCE

$18,000

$24,000

$30,000

NPV-8%

$ billion

$1.52

$3.01

$4.47

IRR

%

12.9

17.1

20.9

PROJECT ADVANCEMENT

The Company has completed multiple environmental studies in advance of permitting and is examining ways to optimize power requirements and incorporate alternative energy solutions.

The recommendations of the FS include continuing the permitting process, engaging with governmental agencies and other parties, and proceeding with detailed engineering to further advance the Project.

Among these steps, the Company has contacted the U.S. Department of Energy’s (DOE) Loan Programs Office (LPO) and plans to initiate the pre-application process under the Title Seven Clean Energy Financing program when the Feasibility Study report is complete.

CONFERENCE CALL

Century Lithium will host a live webcast and conference call for analysts and investors on Monday, April 29, 2024, at 11:00 am ET (8:00 am PT), followed by a question-and-answer session.

A replay of the webcast will be available on our website shortly following the conclusion of the conference call.

QUALITY ASSURANCE

The data in this news release was prepared in accordance with NI 43-101 standards by the following Qualified Persons (QP).

Terre Lane, Principal Mining Engineer, GRE, is an independent QP as defined by NI 43-101 and has reviewed and approved the contents of this news release and verified by site visits and personal examination the information and original documents that relate to preparation of the Mineral Resource Estimate, Mineral Reserve Estimate, mine plan, mine capital and operating cost estimation, economic analysis, and marketing.

Hamid Samari, Principal Geologist, GRE, is an independent QP as defined by NI43-101 and has reviewed and approved the contents of this news release and verified by site visits and personal examination the information and original documents that relate to preparation of the description of the deposit, geological setting, and mineralization, deposit type, exploration, drilling, sample preparation, analyses and security, and data verification.

Todd Fayram, Senior Vice President Metallurgy, Century Lithium, is a non-independent QP as defined by NI 43-101 and has reviewed and approved the contents of this news release and verified by site visits and personal examination the information and original documents that relate to preparation of the description of metallurgical testing, lithium recovery, and design operation and results of the Pilot Plant.

Alan Drake, Manager – Process Engineering, Wood, is an independent QP as defined by NI 43-101 and has reviewed and approved the contents of this news release and verified by site visits and personal examination the information and original documents that relate to preparation of the description and estimates related to recovery methods.

Haiming (Peter) Yuan, PE, PhD, Principal Geotechnical Engineer, WSP USA Environment & Infrastructure Inc., is an independent QP as defined by NI 43-101 and has reviewed and approved the contents of this news release and verified by site visits and personal examination the information and original documents that relate to preparation of the description related to infrastructure, environment and permitting.

Paul Baluch, Technical Director, Civil, Wood, is an independent QP as defined by NI 43-101 and has reviewed and approved the contents of this news release and verified by personal examination the information and original documents that relate to preparation of the description and estimates of infrastructure.

Farzad Kossari, Cost Estimating Manager, Wood, is an independent QP as defined by NI 43-101 and has reviewed and approved the contents of this news release and verified by personal examination the information and original documents that relate to preparation of the description and summary of capital and operating cost estimates.

Further information about the Project, including a description of the key assumptions, parameters, description of sampling methods, data verification and quality assurance (QA) / quality control (QC) programs, methods relating to Mineral Resources and Mineral Reserves and factors that may affect those estimates will be contained in a NI 43-101 Technical Report on the Feasibility Study of the Clayton Valley Lithium Project. Following Section 3.4 of NI 43-101 the report will be available on SEDAR+ and on the Company’s website within 45 days of the date of this news release.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced stage lithium company, focused on developing its 100%-owned Clayton Valley Lithium Project in west-central Nevada, USA. Century Lithium recently completed a Feasibility Study on its Clayton Valley Lithium Project and is currently in the permitting stage, with the goal of becoming a domestic producer of lithium for the growing electric vehicle and battery storage market.

ON BEHALF OF CENTURY LITHIUM CORP. WILLIAM WILLOUGHBY, PhD., PE President & Chief Executive Officer

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.

These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein. These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.com. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

MALVERN, Pa., April 29, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that Benjamin Bakall, MD, PhD, Director of Clinical Research at Associated Retina Consultants and Clinical Assistant Professor at the University of Arizona, College of Medicine—Phoenix will present data from the OCU400 Phase 1/2 clinical trial at the Retinal Cell and Gene Therapy Innovation Summit being held May 3, 2024 in Seattle, WA.

“I look forward to sharing more about my clinical experience with this novel modifier gene therapy with my peers and industry leadership during the summit,” said Dr. Bakall. “There remains a significant unmet need for patients with retinitis pigmentosa (RP) and I believe that this approach can offer a new therapeutic option to address the disease itself.”

The Retinal Cell and Gene Therapy Innovation Summit 2024 is jointly organized by the Foundation Fighting Blindness and the Oregon Health and Science University Casey Eye Institute. The Summit brings together representatives from the biotech and pharma industries, along with members of the medical and research communities, to discuss rapidly emerging ocular gene and cell therapies and strategize how to move the most advanced retinal disease therapies toward clinical utility.

Details on Dr. Bakall’s presentation are as follows:

PresentationTitle: “Nuclear Hormone Receptor-Based Gene Modifier Therapy: Safety and Efficacy from Phase 1/2 Clinical Trials for Retinitis Pigmentosa” Date: Friday, May 3, 2024 Time: 10:50 – 11:05 a.m. (PT) Location: Hyatt Regency Seattle

The OCU400 Phase 3 liMeliGhT clinical trial is currently underway and on track to meet the Company’s 2026 BLA and MAA approval targets. Between the U.S. and EU, nearly 300,000 people are affected by RP.

About OCU400 OCU400 is the Company’s gene-agnostic modifier gene therapy product based on NHR gene, NR2E3. NR2E3 regulates diverse physiological functions within the retina—such as photoreceptor development and maintenance, metabolism, phototransduction, inflammation and cell survival networks. Through its drive functionality, OCU400 resets altered/affected cellular gene networks and establishes homeostasis—a state of balance, which has the potential to improve retinal health and function in patients with RP.