Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Two newbuilds. Euroseas announced contracts for the construction of two 2,800 TEU high-reefer containership newbuilds, with deliveries expected sequentially in the second and third quarters of 2028. The total acquisition price for each of the two newbuild vessels is $46.35 million, with financing expected to include a combination of debt and equity.

Strategic expansion. The vessels will be built to EEDI Phase 3 and IMO NOx Tier III standards and will be equipped with more than 1,000 reefer plugs, optimizing them for high-reefer-density trades. This enhances Euroseas’ exposure to growing refrigerated cargo demand. Importantly, the agreement includes options for up to four additional vessels of similar design, with either reefer or conventional configurations. In our view, this aligns with the company’s strategy of modernizing and diversifying its fleet, lowering the average age, and improving environmental efficiency.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

WEST HARRISON, N.Y.–(BUSINESS WIRE)– Sky Harbour Group Corporation (NYSE: SKYH, SKYH WS) (“SHG” or the “Company”), an aviation infrastructure company building the first nationwide network of Home Base Operator (HBO) campuses for business aircraft, announced the release of its audited financial results for the year ended December 31, 2025 on Form 10-K. The Company also announced the filing of its unaudited financial results for the year ended December 31, 2025 for Sky Harbour Capital (Obligated Group) with MSRB/EMMA. Please see the following links to access the filings:

Financial Highlights on a Consolidated Basis include:

Constructed Assets or In-Construction exceeded $328 million as of December 31, 2025.

2025 full-year consolidated revenues increased 87% as compared to the prior year.

Net cash used in operating activities was reported at $2.3 million for 2025, versus $9.1 million used in 2024.

Strong liquidity and capital resources consisted of consolidated cash and U.S. Treasuries totaling $48 million and $200 million of availability under the J.P. Morgan term bank facility as of December 31st, 2025.

Refer to 10-K for presentation of full-year GAAP net income and Adjusted EBITDA (Non-GAAP) results.

Sky Harbour met guidance of reaching operating cash flow/adjusted EBITDA run-rate breakeven on a consolidated basis by year end 2025, driven by the positive cash flows generated from campuses opened in 2025 and the receipt last December of $5.9 million in upfront rent payment as part of a single hangar lease renewal.

Financial Highlights at Sky Harbour Capital (Obligated Group) include:

Full year Obligated Group Revenues increased 49% in 2025 as compared to 2024.

Net cash provided by operating activities reached positive $15.7 million in 2025, an increase from $6.5 million in 2024, driven by new campus openings, increased occupancy, increased rents and the upfront receipt of $5.9 million in rent in December 2025 as part of a lease extension with an existing tenant.

Debt Service Coverage Tests, calculated as per the Bond Indenture for the period ending December 31, 2025, and as budgeted for 2026, are both in compliance with covenant ratios.

Cash and U.S. Treasuries at the Obligated Group totaled $24 million as of December 31, 2025, with the future capital expenditures on the remaining construction at OPF phase II and Addison phase II to be covered from expected Obligated Group revenues through the end of construction, proceeds of the 2026 Series Bonds and capital contributions from the Company as needed.

Update on Site Acquisition

Sky Harbour currently has campuses operating at Houston’s Sugar Land Regional Airport (SGR), Nashville International Airport (BNA), Miami Opa-Locka Executive Airport (OPF), San Jose Mineta International Airport (SJC), Camarillo Airport (CMA), Phoenix Deer Valley Airport (DVT) Dallas’s Addison Airport (ADS), and Denver’s Centennial Airport (APA).

Sky Harbour currently has campuses in construction at Bradley International Airport (BDL), Salt Lake City International Airport (SLC), the second phase at OPF, and the second phase at ADS and campuses in development at Chicago Executive Airport (PWK), Hudson Valley Regional Airport (POU), New York Stewart International Airport (SWF), Orlando Executive Airport (ORL), Dulles International Airport (IAD), Trenton-Mercer Airport (TTN), Portland-Hillsboro Airport (HIO), Long Beach Airport (LGB), and Fort Worth Meacham International Airport (FTW).

We met our prior guidance of nine additional ground leases in 2025, for a total portfolio of 23 airport ground leases announced by year end. In addition, we secured new land leases at two existing airports. Once fully developed, the 23 ground leases are expected to include approximately 4 million in aggregate rentable square feet.

Update on Construction and Development Activities

As reported on our monthly construction reports filed with MSRB/EMMA and available on our website, the first phases at DVT, APA and ADS were completed and began operations in 2025. We are currently in construction at the second phases at OPF and ADS as well as BDL in Hartford, CT, and SLC in Salt Lake City, UT. Please see the following link for the last month construction report: https://emma.msrb.org/P11937008-P11478849-P11929703.pdf

Phase I in POU, ORL and TTN are expected to start construction in the coming months. The Company has significantly increased resources dedicated to development and construction in anticipation of the upcoming surge in activity.

Update on Leasing Activities

Occupancy is at or near 100% in all campuses opened prior to 2025, with the newer campuses at DVT, ADS and APA at 77%, 84%, and 35% respectively as of March 16th, 2026.

The pre-leasing program is now in operation, with leases and LOIs in place at some of the campuses in development.

Update on Airport Operations

During the fourth quarter the Company focused on optimizing their recently opened campuses as occupancy increased, and on launching portfolio-wide initiatives to deliver superior service and safety while targeting improved cost efficiencies.

Funding and Capital Formation

In September 2025, Sky Harbour completed the previously announced $200 million 5-year SOFR based bank facility with J.P. Morgan (“JPMorgan Facility”). We also entered into a floating-for-fixed interest rate swap with an affiliate of J.P. Morgan that effectively locked in the cost of our draws to approximately 4.73%. Although there were no draws at year end, we have subsequently drawn $17.9 million as of March 15th, 2026 to cover capital expenditures at BDL and to reimburse ourselves for a portion of the issuance costs. We expect to continue to draw in the coming weeks and months as we accelerate our construction program.

On February 12, 2026, we closed on a $150 million private activity tax-exempt financing issued through the Public Finance Authority (the “2026 Series Bonds”). The 2026 Series Bonds were issued at par with a 6.00% fixed interest rate, are subordinated to the 2021 Series Bonds and the JPMorgan Facility and have a mandatory tender on January 1, 2031 (5-year financing). We have invested the net proceeds of the 2026 Series Bonds in short and medium US Treasury bills and notes until these funds are used to fund capital expenditures or pay interest on the bonds.

The combined net proceeds of this issuance are expected to be combined with the expected draws from the JPMorgan Facility and other available cash to fully fund the capital expenditures of our next six projects totaling over one million of rentable hangar square footage. Combined with the existing or soon to be completed one million rentable square feet of hangar space, our funded projects total over 2.1 million rentable square feet.

CEO, Tal Keinan commented: “The Company is generating operating cash at an increasing rate as additional hangar campuses come online. More than 1,000,000 square feet of new hangar development is fully funded, and our construction resources are prepared to meet the upcoming surge with growing speed and cost-efficiency. The Sky Harbour HBO offering is the solution of choice for the country’s top flight departments. Our focus for 2026 is scale.”

About Sky Harbour

Sky Harbour Group Corporation is an aviation infrastructure company developing the first nationwide network of Home-Basing campuses for business aircraft. The company develops, leases, and manages general aviation hangar campuses across the United States. Sky Harbour’s Home-Basing offering aims to provide private and corporate residents with the best physical infrastructure in business aviation, coupled with dedicated service, tailored specifically to based aircraft, offering the shortest time to wheels-up in business aviation. To learn more, visit www.skyharbour.group.

Forward Looking Statements

Certain statements made in this release are “forward looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including statements about the financial condition, results of operations, earnings outlook and prospects of SHG, including statements regarding our expectations for future results, our expectations for future ground leases, our expectations on future construction and development activities and lease renewals, and our plans for future financings. When used in this press release, the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. The forward-looking statements are based on the current expectations of the management of Sky Harbour Group Corporation (the “Company”) as applicable and are inherently subject to uncertainties and changes in circumstances. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. For more information about risks facing the Company, see the Company’s annual report on Form 10-K for the year ended December 31, 2025 and other filings the Company makes with the SEC from time to time. The Company’s statements herein speak only as of the date hereof, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators

We use a number of metrics, including annualized revenue run rate per leased rentable square foot, to help us evaluate our business, measure our performance, identify trends affecting our business, formulate business plans, and make strategic decisions. Our key performance indicators may be calculated in a manner different than similar key performance indicators used by other issuers. These metrics are estimated operating metrics and not projections, nor actual financial results, and are not indicative of current or future performance.

While macro headlines continue to dominate investor attention, small-cap specialty pharma company Collegium Pharmaceutical (NASDAQ: COLL) is quietly executing a disciplined growth strategy — and its latest move is hard to ignore.

The Stoughton, Massachusetts-based company announced a definitive agreement to acquire AZSTARYS, an FDA-approved ADHD treatment, from privately held Corium Therapeutics for $650 million in cash at closing, with the potential for up to $135 million in additional milestone payments tied to future commercial and regulatory targets. The deal is expected to close in the second quarter of 2026.

What Is AZSTARYS and Why Does It Matter?

AZSTARYS is a central nervous system stimulant combining immediate-release and long-acting components in a single capsule, approved for patients aged six and older with Attention Deficit Hyperactivity Disorder. It is one of the more differentiated products in the ADHD space precisely because of that dual-mechanism delivery — something that sets it apart from a crowded field of single-mechanism competitors.

The commercial traction is already there. AZSTARYS generated more than 760,000 prescriptions in 2025, and Collegium projects the drug will contribute over $50 million in pro forma net revenue in just the second half of 2026 — assuming the deal closes on schedule. Six Orange Book-listed patents, most of which do not expire until December 2037, provide long-runway exclusivity that gives this asset real staying power on Collegium’s balance sheet.

Collegium already markets Jornay PM, a delayed-release methylphenidate treatment for ADHD. Adding AZSTARYS gives the company two commercially differentiated products targeting the same condition but with distinct dosing profiles — a smart way to expand market penetration without cannibalizing existing revenue.

The deal structure reflects that discipline. Collegium plans to fund the acquisition using cash on hand and a previously arranged $300 million delayed-draw term loan, with management projecting post-close net leverage of approximately two times estimated 2026 combined adjusted EBITDA. Run-rate cost synergies are expected to exceed $50 million within twelve months of closing, driven by Collegium leveraging its existing ADHD commercial infrastructure rather than building a parallel one from scratch.

The transaction has been unanimously approved by the boards of both companies and is subject to customary regulatory approvals, including Hart-Scott-Rodino clearance.

At a market cap of approximately $1.15 billion, Collegium is doing something many larger companies struggle with — making acquisitions that are both strategically coherent and financially disciplined. The AZSTARYS deal is not a moonshot. It is a calculated bet on a proven, revenue-generating asset with durable patent protection in a therapeutic category — ADHD — that continues to see strong and growing demand across both pediatric and adult patient populations.

Needham & Company reaffirmed its Buy rating on COLL this week with a price target of $56, representing meaningful upside from the stock’s current trading range near $36. The broader analyst consensus sits at Buy, though the stock has traded down from its 52-week high near $51 amid broader market volatility.

For investors focused on the small and microcap space, Collegium’s approach offers a case study in how companies under $2 billion in market cap can use M&A not as a hail mary, but as a precision tool for compounding long-term value.

Reported updated results from 12 patients with type 1 diabetes treated with tegoprubart following islet transplantation in UChicago Medicine-led study

Presented 24-month follow-up data from Phase 1b long-term extension study which continues to support the favorable safety and tolerability profile of tegoprubart

Tegoprubart granted Orphan Drug designation by the FDA for the prevention of allograft rejection in liver transplantation

IRVINE, Calif., March 19, 2026 (GLOBE NEWSWIRE) — Eledon Pharmaceuticals, Inc. (“Eledon”) (Nasdaq: ELDN) today reported its fourth quarter and full year 2025 operating and financial results and reviewed recent business highlights.

“Over the past year, Eledon has made significant progress advancing tegoprubart, our anti-CD40L antibody, as a potential next-generation immunosuppressive therapy across multiple transplantation settings,” said David-Alexandre C. Gros, M.D., Chief Executive Officer of Eledon. “The over 100 patients treated across our transplantation programs to date provide a growing body of evidence that reinforces our conviction that tegoprubart can address key safety and efficacy issues with current standard-of-care transplant immunosuppression. Looking ahead, we anticipate multiple important milestones this year, including regulatory engagement to support advancement into Phase 3 development in kidney transplantation, initiation of an additional islet transplantation trial in type 1 diabetes, and the start of a clinical trial in liver transplantation.”

Fourth Quarter 2025 and Recent Corporate Developments

Announced that tegoprubart has been granted Orphan Drug designation by the U.S. Food and Drug Administration (FDA) for the prevention of allograft rejection in liver transplantation. Tegoprubart previously received Orphan Drug designation from the FDA for the prevention of allograft rejection in pancreatic islet cell transplantation and for the treatment of amyotrophic lateral sclerosis (ALS).

Presented 24-month follow-up data from eight patients enrolled in the Phase 1b long-term extension trial evaluating tegoprubart in kidney transplantation at the American Society of Transplant Surgeons Winter Symposium. The data continue to support the favorable safety and tolerability profile of tegoprubart with no episodes of biopsy-proven acute rejection, graft loss, death, new-onset diabetes mellitus, or de novo donor-specific antibody formation reported during the study period. Mean estimated glomerular filtration rate (eGFR) increased over the measurement period, from 67.0 mL/min/1.73 m² at 12 months to 74.2 mL/min/1.73 m² at 24 months.

Reported updated results from 12 patients with type 1 diabetes treated with tegoprubart as the core immunosuppressant following islet transplantation in an investigator-initiated trial conducted at the University of Chicago Medicine Transplant Institute. All 10 patients who were more than four weeks post-transplant achieved 100% insulin independence and a most recent hemoglobin A1C (HbA1c) below 6.0%, with a mean most recent HbA1c across the 10 patients of approximately 5.35%. Tegoprubart-based immunosuppression was generally well tolerated with reported post-transplant immunosuppression-related adverse events successfully treated by lowering the mycophenolic acid dose, if necessary. There were no rejection episodes, and no patients developed de novo donor-specific HLA antibodies. Additionally, no evidence of nephrotoxicity, hypertension or neurotoxicity, which are commonly associated with tacrolimus-based immunosuppression regimens, was observed. The study continues to generate significant patient demand with inquiries received from several hundred T1D patients.

Anticipated Upcoming Milestones

Receive FDA guidance on the Phase 3 trial design assessing tegoprubart in kidney transplantation, followed by initiation of the Phase 3 trial pending regulatory alignment.

Report long-term data from Phase 1 and Phase 2 BESTOW studies evaluating tegoprubart in kidney transplantation.

Receive FDA regulatory guidance on path to market for tegoprubart in islet cell transplantation and xenotransplantation.

Initiate an investigator-led study evaluating tegoprubart for the prevention of organ rejection in patients with renal dysfunction receiving an islet cell transplant.

Initiate an investigator-led study evaluating tegoprubart for the prevention of organ rejection in patients receiving a de novo liver transplant.

Initiate an investigator-led study evaluating tegoprubart for kidney transplant tolerance induction.

Full Year 2025 Financial Results

Research and development (R&D) expenses for the year ended December 31, 2025 were $66.3 million, including $4.2 million of non-cash stock-based compensation expense, compared to $52.0 million, including $4.3 million of non-cash stock-based compensation expense, for the comparable period in 2024. The increase was primarily driven by continued advancement of the tegoprubart clinical development programs, including expanded clinical trial activity and manufacturing scale-up, as well as increased personnel to support these efforts.

General and administrative expenses for the year ended December 31, 2025 were $17.0 million, including $6.2 million of non-cash stock-based compensation expense, compared to $18.6 million, including $8.8 million of non-cash stock-based compensation expense, for the comparable period in 2024. The decrease was primarily driven by lower stock-based compensation expense, partially offset by higher professional services and personnel-related costs.

Net loss for the year ended December 31, 2025 was $45.6 million, or $0.52 per basic share of common stock, compared to a net loss of $36.2 million, or $0.66 per basic share of common stock, for the comparable period in 2024. The 2025 net loss included a non-cash gain of $33.4 million from changes in the fair value of warrant liabilities, while the 2024 net loss included a non-cash gain of $30.9 million from such changes. Excluding the non-cash items related to changes in the fair value of warrant liabilities, Eledon would have recorded a net loss of $79.1 million for the year ended December 31, 2025 and $67.1 million for the year ended December 31, 2024.

About Eledon Pharmaceuticals and tegoprubart

Eledon Pharmaceuticals, Inc. is a clinical stage biotechnology company that is developing immune-modulating therapies for the management and treatment of life-threatening conditions. The Company’s lead investigational product is tegoprubart, an anti-CD40L antibody with high affinity for the CD40 Ligand, a well-validated biological target that has broad therapeutic potential. The central role of CD40L signaling in both adaptive and innate immune cell activation and function positions it as an attractive target for non-lymphocyte depleting, immunomodulatory therapeutic intervention. The Company is building upon a deep historical knowledge of anti-CD40 Ligand biology to conduct preclinical and clinical studies in kidney allograft transplantation, xenotransplantation, islet cell transplantation, liver transplantation and amyotrophic lateral sclerosis (ALS). Eledon is headquartered in Irvine, California. For more information, please visit the Company’s website at www.eledon.com.

Follow Eledon Pharmaceuticals on social media: LinkedIn; Twitter

Forward-Looking Statements

This press release contains forward-looking statements that involve substantial risks and uncertainties. Any statements about the company’s future expectations, plans and prospects, including statements about planned clinical trials, the development of product candidates, expected timing for initiation of future clinical trials, expected timing for receipt of data from clinical trials, the company’s capital resources and ability to finance planned clinical trials, as well as other statements containing the words “believes,” “anticipates,” “plans,” “expects,” “estimates,” “intends,” “predicts,” “projects,” “targets,” “looks forward,” “could,” “may,” and similar expressions, constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are inherently uncertain and are subject to numerous risks and uncertainties, including: our short operating history and shifts in our business strategy; our operating losses since inception; our need for additional funding to develop our lead drug candidate and our ability to secure additional funding on acceptable terms or at all; the impact of issuances of our common stock, including in the possibility of dilution or a decline in our stock price; our ability to successfully develop our product candidates; unfavorable global economic and financial market conditions; the regulatory environment of our business and our ability to obtain required regulatory approvals; results of non-clinical studies and clinical trials, and risks that non-clinical studies or early clinical trials may not be predictive of results of later-stage clinical trials; delays or difficulties in enrollment of patients in clinical trials; our ability to attract and retain our executives and key employees; legislation of the pharmaceutical and healthcare industries; cybersecurity and data privacy risks; the ability of our products to achieve marketing approval; competition in our industry; our ability to obtain insurance coverage; our dependence on contract research organizations; our ability to protect our intellectual property; public health crises; our ability to maintain proper and effective internal control over financial reporting and other risks disclosed in our Annual Report on Form 10-K for the year ended December 31, 2025, filed with the Securities and Exchange Commission on March 19, 2026. Actual results may differ materially from those indicated by such forward-looking statements as a result of various factors. These risks and uncertainties, as well as other risks and uncertainties that could cause the company’s actual results to differ materially from the forward-looking statements contained herein, are discussed in our Annual 10-K, and other filings with the U.S. Securities and Exchange Commission, which can be found at www.sec.gov. Any forward-looking statements contained in this press release speak only as of the date hereof and not of any future date, and the company expressly disclaims any intent to update any forward-looking statements, whether as a result of new information, future events or otherwise.

CULVER CITY, Calif., March 19, 2026 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail Games” or the “Company”), a leading global independent developer and publisher of interactive digital entertainment, today announced financial results for the fourth quarter and full year ended December 31, 2025.

Fourth Quarter 2025 and Recent Operational Highlights

ARK Franchise Updates:

ARK: Survival Evolved (“ASE”):

Units sold were approximately 579,248 for the fourth quarter 2025

During the fourth quarter of 2025, average daily active users (“DAU”) was 105,468 and peak DAU was 137,404

ARK: Survival Ascended (“ASA”):

Units sold were approximately 691,872 for the fourth quarter 2025

During the fourth quarter of 2025, average DAU was 91,123 and peak DAU was 147,572

Launched ARK Lost Colony DLC

Launched ‘ARK x Teenage Mutant Ninja Turtles’ Cosmetic Pack in collaboration with Look North World

ARK: Ultimate Mobile Edition (“ARK Mobile”):

Surpassed 10 million downloads as of December 31, 2025

During the fourth quarter of 2025, average DAU was 129,861

2026 / 2027 ASA Content Roadmap

2026

ARK World Creator (scheduled for May 2026)

ARK Bob’s True Tales – Tides of Fortune (scheduled for June 2026)

ARK Genesis Part 1 (ASA remake)

ARK Survival of the Fittest (“SOTF”)

ARK Dragontopia (scheduled for December 2026)

2027

ARK Atlantis

ARK Bob’s True Tales – Galaxy Wars

ARK Legacy of Santiago

Game Portfolio Updates:

2026 Games Developers Conference (“GDC”)

Introduced PixARK Worlds, a new title in development that features revolutionary user-generated content designed to expand the ARK universe onto the Nintendo Switch 2

Revealed event-exclusive trailer for upcoming AAA title For The Stars

Unveiled new indie title, Gobby Gang

Bellwright surpassed 1 million downloads on Steam Early Access, announced console port plans to Xbox and PlayStation, and launched the Maiden Voyage update. Following the launch of the update, the title achieved its highest Steam concurrent user peak of the year and sold over 166,000 units in Q4 2025

Launched Echoes of Elysium on Steam Early Access in partnership with Loric Games

Participated in the Steam Winter Sale, resulting in double digit sales multiples for ASA and Bellwright

Launched Rebel Engine in partnership with Seven Leaf Clover. The title demonstrated notable creator engagement, partnering with VTuber Hakos Baelz and Spanish gaming creator Joseju

Announced strategic collaboration with Noiz at TwitchCon to strengthen gaming portfolio visibility with streamers

Business Updates:

Minted the first official $USDO stablecoin during the Company’s December 2025 Investor Day

Debuted Golden Poop, a commemorative digital meme collectible created to humorously acknowledge gaming culture and industry satire

As of December 31, 2025, SaltyTV released 100+ short film dramas

Three of SaltyTV’s titles were recognized by the International Short Drama Association:

My Ex’s Best Friend recognized for Best Revenge-Driven Narrative

Hollywood Heartthrob recognized for Most Charismatic Screen Presence

Faux Fiancé recognized for Best Destiny-Bound Narrative

Management Commentary

“The fourth quarter provided strong visibility into the momentum we expect across the ARK franchise over the next two years. In addition to launching ARK: Lost Colony, ASA’s first standalone DLC expansion pack, we introduced robust ASA content and DLC roadmap during our December Investor Day. The 2026 slate includes the ARK SOTF remake, ARK World Creator for consoles,ARK Bob’s True Tales – Tides of Fortune, the ASA remake of ARK Genesis Part 1, and ARK:Dragontopia. Since launching in October 2023, ASA has surpassed 4 million units sold, and our expanded roadmap reflects our commitment to sustained franchise growth and increased revenue visibility through 2027.

“Beyond ARK, we are continuing to invest, advance, and scale our broader game portfolio. We are particularly encouraged by the meaningful progress made across our developing AAA games; For The Stars, Nine Yin Sutra: Immortal, and Nine Yin Sutra: Wushu. AAA games are high-budget, high-profile projects that are designed to deliver expansive worlds, cutting-edge visuals, and robust marketing campaigns that far exceed those of typical indie releases. These games, while still in development, represent Snail’s investment and expansion into other AAA games outside of ASE and ASA. These three games have represented a core pillar of our long-term investment strategy over the past few years. Being classified as an AAA game, we believe these titles offer substantial upside with an attractive profit margin profile compared to many of our other games. The progress made has been encouraging, and we are excited to continue developing and sharing updates. At the recent GDC event, we shared an event-exclusive trailer for For The Stars that provided some early insights into the gameplay and concept art.

“Across our other business units, we also made meaningful progress. We minted the first official $USDO stablecoin during the Investor Day and debuted the Golden Poop digital collectible coin. We are currently working towards a potential partnership opportunity tied to our stablecoin initiative and look forward to sharing additional information later this year. Within our short film vertical, SaltyTV has now released 100+ short film dramas, with three productions receiving recognition from the International Short Drama Association. Our Interactive Films division also expanded into narrative-driven game development in 2025, which we view as a strategic adjacency that builds on existing creative capabilities.

“We remain excited about our gaming pipeline for the next two years. ARK will continue to remain the foundational backbone of our company, while we also invest in and grow other arms of the business. Many of our projects are approaching the final stages of development, and we believe we are well-positioned to broaden our portfolio, diversify revenue streams, and drive long-term shareholder value.”

Fourth Quarter 2025 Financial Highlights

Net revenues were $25.1 million compared to $26.2 million in the same period last year. The decrease was primarily due to a decrease in deferred revenues that were recognized in 2025 of $3.5 million, partially offset by increases in ARK sales of $1.3 million and an increase in Bellwright sales of $1.2 million.

Total units sold were 1.5 million units compared to 1.3 million units in the same period last year, primarily driven by an increase in sales of ASA of 0.2 million units, an increase in Bellwright sales of 0.1 million units, partially offset by a decrease in sales of ASE and our other titles of 0.1 million units.

Net loss was $(0.9) million compared to net income of $1.1 million in the same period last year, primarily due to a decrease in gross profit of $1.7 million and an increase in operating expenses of $2.8 million, partially offset by an increase in other income (expense) of $2.0 million and benefit from income taxes of $0.5 million.

Bookings were $20.8 million compared to $17.0 million in the same period last year. The increase was primarily due to a lower portion of sales deferred in 2025. Changes in deferred revenues decreased by $4.9 million while net revenue decreased $1.1 million.

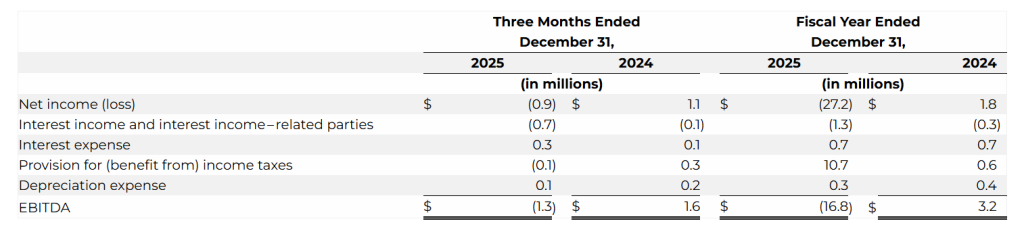

EBITDA was $(1.3) million compared to $1.6 million in the same period last year. The decrease was primarily due to an increase in operating expenses of $2.8 million.

As of December 31, 2025, unrestricted cash was $8.6 million compared to $7.3 million as of December 31, 2024.

Full Year 2025 Financial Highlights

Net revenues were $81.2 million compared to $84.5 million in the same period last year. The decrease was primarily due to a decrease in recognition of deferred revenues of $15.5 million related to the ARK franchise, decrease in Bellwright and Myth of Empires sales of $1.5 million and $1.3 million respectively, partially offset by an increase in ASA sales of $11.3 million, ARK Mobile sales of $2.4 million, and revenue generated from the SaltyTV application of $0.8 million.

Total units sold increased 32.7% to 6.3 million units compared to 4.7 million units in the same period last year, primarily driven by an increase in ARK franchise units sold by 1.7 million units, partially offset by a slight decrease in Bellwright and West Hunt sales of 0.1 million units.

Net loss was $(27.2) million compared to net income of $1.8 million in the same period last year, primarily due to a non-cash tax expense related to the full valuation of our deferred tax assets of $10.1 million, increase in general and administrative expenses of $5.2 million, increase in research and development of $2.9 million, increase in advertising and marketing of $3.7 million, and impairment expenses of $1.5 million.

Bookings increased 16.2% to $87.8 million compared to $75.7 million in the same period last year. The increase was primarily due to the increased ASA sales driven by the launch of ARK: Lost Colony, ARK: Astraeos, and ASE’s first sales event in June 2025 since the price drop in August 2023.

EBITDA was $(16.8) million compared to $3.2 million in the same period last year. The decrease was due to the increase in general and administrative expenses of $5.2 million, an increase in research and development of $2.9 million, an increase in advertising and marketing of $3.7 million and an additional $1.5 million in impairment expenses.

Use of Non-GAAP Financial Measures

In addition to the financial results determined in accordance with U.S. generally accepted accounting principles, or GAAP, Snail believes Bookings and EBITDA, as non-GAAP measures, are useful in evaluating its operating performance. Bookings and EBITDA are non-GAAP financial measures that are presented as supplemental disclosures and should not be construed as alternatives to net income (loss) or revenue as indicators of operating performance, nor as alternatives to cash flow provided by operating activities as measures of liquidity, both as determined in accordance with GAAP. Snail supplementally presents Bookings and EBITDA because they are key operating measures used by management to assess financial performance. Bookings adjusts for the impact of deferrals and, Snail believes, provides a useful indicator of sales in a given period. Management believes Bookings and EBITDA are useful to investors and analysts in highlighting trends in Snail’s operating performance, while other measures can differ significantly depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which Snail operates and capital investments.

Bookings is defined as the net amount of products and services sold digitally or physically in the period. Bookings is equal to revenues, excluding the impact from deferrals. Below is a reconciliation of total net revenue to Bookings, the closest GAAP financial measure.

We define EBITDA as net income (loss) before (i) interest expense, (ii) interest income, (iii) provision for (benefit from) income taxes and (iv) depreciation expense. The following table provides a reconciliation from net income (loss) to EBITDA:

Webcast Details

The Company will host a webcast at 4:30 PM ET today to discuss its fourth quarter and full year 2025 financial and operational results. Participants may access the live webcast and replay via the link here or on the Company’s investor relations website at https://investor.snail.com/.

Forward-Looking Statements

This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future results of Snail’s business, financial condition, results of operations, liquidity, plans and objectives. The statements Snail makes regarding the following matters are forward-looking by their nature: Snail’s 2026 / 2027 ASA content roadmap; plans to port Bellwright to the Xbox and Playstation consoles; Snail’s announced strategic collaboration with Noiz and its potential to strengthen the visibility of Snail’s gaming portfolio with streamers; the momentum Snail expects across the ARK franchise over the next two years and the visibility regarding the same provided by Snail’s fourth quarter; Snail’s expanded roadmap and commitment to sustained franchise growth and increased revenue visibility through 2027; Snail’s continued investment, advancement, and scaling of its broader game portfolio; progress made across the development of AAA games; the intention for AAA games to deliver expansive worlds, cutting-edge visuals, and robust marketing campaigns that far exceed those of typical indie releases; Snail’s investment and expansion into other AAA games outside of ASE and ASA and the potential for its existing AAA games to form a core pillar of its long-term investment strategy; For The Stars, Nine Yin Sutra: Immortal, and Nine Yin Sutra: Wushu offering substantial upside with an attractive profit margin profile compared to many of our other games; the occurrence and timing of a potential partnership opportunity tied to Snail’s stablecoin initiative; Snail’s interactive films division serving as a strategic adjacency and building on Snail’s existing creative capabilities; ARK remaining the foundational backbone of Snail and its gaming pipeline; Snail investing in and growing other arms of its business; Snail’s in-house projects are approaching the final stages of development; Snail being positioned to broaden its portfolio, diversify revenue streams, and drive long-term shareholder value;and assumptions underlying any of the foregoing.

Further information on risks, uncertainties and other factors that could affect Snail’s financial results and business include Snail’s ability to strengthen its gaming portfolio’s visibility; its ability to expand and grow its franchise and increase its revenue; and the risks that are included in its filings with the Securities and Exchange Commission (the “SEC”) from time to time, including its annual reports on Form 10-K and quarterly reports on Form 10-Q filed, or to be filed, with the SEC. You should not rely on these forward-looking statements, as actual outcomes and results may differ materially from those expressed or implied in the forward-looking statements as a result of such risks and uncertainties. All forward-looking statements in this press release are based on management’s beliefs and assumptions and on information currently available to Snail, and Snail does not assume any obligation to update the forward-looking statements provided to reflect events that occur or circumstances that exist after the date on which they were made.

About Snail, Inc.

Snail, Inc. (Nasdaq: SNAL) is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs, and mobile devices. For more information, please visit: https://snail.com/.

Investor Contact:

John Yi and Steven Shinmachi Gateway Group, Inc. 949-574-3860 SNAL@gateway-grp.com

New home sales rang in 2026 with a troubling signal. January sales of newly built homes collapsed 17.6% month over month to a seasonally adjusted annualized rate of 587,000 units — the slowest pace since 2022 — according to data released Thursday by the U.S. Census Bureau. The drop was far steeper than analysts had projected, and it arrived against a backdrop that was supposed to be improving.

Year over year, sales were down 11.3%, with December’s already-soft numbers revised even lower. For homebuilders — many of them small and mid-cap companies already managing tight margins and bloated inventory — the report adds urgency to a housing sector that has yet to find solid footing.

The January data reflects signed contracts from a period when the average 30-year fixed mortgage rate was hovering between 6% and 6.2%, according to Mortgage News Daily. Rates have since climbed to 6.36%, meaning conditions in the months ahead are unlikely to produce a meaningful rebound without a catalyst. The Federal Reserve’s decision Wednesday to hold rates steady at 3.5%–3.75% — with the dot plot pointing to just one cut in 2026 — offers little relief for rate-sensitive buyers sitting on the sidelines.

To move inventory, builders have been reaching deeper into their toolkits. The median price of a new home sold in January fell to $400,500, a decline of 6.8% year over year. Yet the discounts aren’t clearing the market fast enough. Inventory climbed to a 9.7-month supply, up from eight months in December and 7.8% higher than a year ago. Completed homes sitting unsold are now near levels not seen since 2009.

The pain is spreading into March. An estimated 37% of builders cut prices in March, up from 36% in February, according to the National Association of Home Builders. Nearly two-thirds of builders are deploying additional incentives including mortgage rate buydowns to pull buyers across the finish line — a strategy that protects top-line revenue while quietly compressing margins.

Sales declined across every region, but the drops were not equal. The Northeast and Midwest could partially blame harsh winter weather. The West has no such excuse — sales there fell nearly 22% from December, suggesting demand destruction that runs deeper than seasonal disruption. Sun Belt markets, after years of speculative overbuilding, continue to be among the hardest hit.

For investors tracking small and mid-cap homebuilders, the January report is a reminder that volume recovery and margin recovery are not the same story. Companies relying heavily on incentive-driven sales risk deteriorating earnings quality even as unit counts look stable. With the Fed on hold, mortgage rates sticky above 6%, and consumer confidence still fragile, the setup for the spring selling season — typically the industry’s most critical window — looks challenged at best.

The pent-up demand is real. The question is whether affordability conditions improve fast enough to release it before builder balance sheets feel the weight.

STAFFORD, Texas, March 19, 2026 (GLOBE NEWSWIRE) — Greenwich LifeSciences, Inc. (Nasdaq: GLSI) (the “Company”), a clinical-stage biopharmaceutical company focused on its Phase III clinical trial, FLAMINGO-01, which is evaluating Fast Track designated GLSI-100, an immunotherapy to prevent breast cancer recurrences, today announced the initiation of new clinical sites in the US.

The Phase III clinical trial has recently been activated at City of Hope, one of the largest and most advanced cancer research and treatment organizations in the United States – specifically at its network sites in Los Angeles and Orange counties, Arizona, Atlanta, and Illinois. Principal investigator at City of Hope, Hope S. Rugo, M.D., continues her participation on the Steering Committee. Her prior site at University of California San Francisco, where she is Professor Emeritus, is still participating in the study.

Dr. Rugo is division chief of breast medical oncology and a professor in the Department of Medical Oncology & Therapeutics Research at City of Hope. She also serves as director of the Women’s Cancers Program for City of Hope’s national network of cancer centers. A world-renowned expert in breast cancer and clinical trial design and execution, Dr. Rugo oversees women’s cancer research initiatives and clinical care at City of Hope. She is focused on expanding breast cancer clinical trials, advancing translational research, and standardizing care to improve patient outcomes. She is deeply committed to improving access to innovative new therapies for breast cancer patients everywhere and takes a compassionate, collaborative approach in her work.

Dr. Rugo has been directly involved in numerous projects that have established new standards of care for breast cancer. She has served on the steering committees of multiple clinical trials that led to the approval of agents such as PARP inhibitors, CDK4/6 inhibitors, PI3K inhibitors, checkpoint inhibitors, and antibody-drug conjugates, among others. Additionally, Dr. Rugo has led several studies aimed at minimizing therapy-related toxicity. She also served as co-chair of the Triple Negative Working Group of the Translational Breast Cancer Research Consortium, where she spearheaded groundbreaking multicenter clinical trials in collaboration with researchers, pharmaceutical companies, and clinical providers. As a physician-scholar with more than 500 peer-reviewed publications, Dr. Rugo served on the editorial board of the American Society of Clinical Oncology’s Education Committee, which included co-chairing the creation of new guidelines for the hormonal treatment of metastatic breast cancer.

Dr. Rugo commented, “I am excited to open this important trial across our City of Hope sites, expanding treatment opportunities for our patients with high-risk early stage HER2 positive breast cancer. It is truly an honor to now represent City of Hope on the Steering Committee. This study aligns with City of Hope’s interest in and the importance of harnessing the host immune system to reduce the risk of breast cancer recurrence.”

Last year City of Hope launched a national clinical trials model that includes clinical sites across the United States in order to accelerate cancer research.

Dr. Jaye Thompson, VP Clinical and Regulatory Affairs, commented, “We are honored to have Dr. Rugo, a globally recognized leader in breast cancer, now participating in FLAMINGO-01 through her leadership at City of Hope. Her site’s expertise and commitment to advancing patient care, which I personally experienced when training these sites, is invaluable as we continue to study GLSI-100. The four City of Hope locations also strengthen our study footprint in some regions of the US where we were not previously covered, providing the study with access to additional population centers.”

CEO Snehal Patel commented, “We started working with Dr. Rugo when she was the breast cancer leader at UCSF and joined our Phase III study and Steering Committee. We quickly benefited from her recommendations as the study was starting up and expanding into Europe. Her extensive experience in developing novel therapies, while minimizing toxicities, will guide us through the development of GLSI-100 as an effective and safe vaccine to prevent metastatic breast cancer in high-risk breast cancer survivors. With the addition of these new sites at City of Hope, planned expansion of US Oncology/Sarah Cannon sites, addition of sites in new countries, including potentially the United Kingdom and Canada, the total sites participating in FLAMINGO-01 could increase from the current 160 sites to up to 190-200 sites.”

About FLAMINGO-01 Open Label Phase III Data

More than 1,000 patients have been screened with a current screen rate of approximately 800 patients per year. The 250 patient non-HLA-A*02 arm is now fully enrolled, where all patients received GLSI-100, which is 5 times more treated patients and recurrence rate data than the approximately 50 patients treated in the Phase IIb trial. The Primary Immunization Series (PIS), which includes the first 6 GLSI-100 injections over the first 6 months and is required to reach peak protection, is followed by 5 booster injections given every 6 months to prolong the immune response, thereby providing longer-term protection.

In the non-HLA-A*02 arm, a preliminary analysis of recurrence rates after the PIS is completed shows an approximately 70-80% reduction in recurrence rate.

This observation is trending similarly to the Phase IIb trial results and hazard ratio where HLA-A*02 patients were treated and where breast cancer recurrences were reduced up to 80% compared to a 20-50% reduction in recurrence rate by other approved products.

The immune response at baseline prior to any GLSI-100 treatment, the increasing immune response during the PIS, and the safety profile of non-HLA-A*02 patients is trending similarly to the HLA-A*02 arms of FLAMINGO-01 and to the Phase IIb study.

Analysis of the open label data from FLAMINGO-01 has been conducted in a manner that maintains the study blind. The open label recurrence rate, immune response, and safety data is based on the patients enrolled to date in FLAMINGO-01 and the data provided by the clinical sites so far, which is not completed or fully reviewed, and is thus preliminary. While comparing any preliminary FLAMINGO-01 data to the Phase IIb clinical trial data may be possible, these preliminary results are not a prediction of future results, and the results at the end of the study may differ.

About GLSI-100 Phase IIb Study

In the prospective, randomized, single-blinded, placebo-controlled, multi-center (16 sites led by MD Anderson Cancer Center) Phase IIb clinical trial of HLA-A*02 breast cancer patients, 46 HER2/neu 3+ over-expressor patients were treated with GLSI-100, and 50 placebo patients were treated with GM-CSF alone. After 5 years of follow-up, there was an 80% or greater reduction in cancer recurrences in the HER2/neu 3+ patients who were treated with GLSI-100, followed, and remained disease free over the first 6 months, which we believe is the time required to reach peak immunity and thus maximum efficacy and protection. The Phase IIb results can be summarized as follows:

80% or greater reduction in metastatic breast cancer recurrence rate over 5 years of follow-up with a peak immune response at 6 months and well-tolerated safety profile.

The PIS elicited a potent immune response as measured by local skin tests and immunological assays.

About FLAMINGO-01 and GLSI-100

FLAMINGO-01 (NCT05232916) is a Phase III clinical trial designed to evaluate the safety and efficacy of Fast Track designated GLSI-100 (GP2 + GM-CSF) in HER2 positive breast cancer patients who had residual disease or high-risk pathologic complete response at surgery and who have completed both neoadjuvant and postoperative adjuvant trastuzumab based treatment. The trial is led by Baylor College of Medicine and currently includes US and European clinical sites from university-based hospitals and academic and cooperative networks with plans to open up to 150 sites globally. In the double-blinded arms of the Phase III trial, approximately 500 HLA-A*02 patients are planned to be randomized to GLSI-100 or placebo, and up to 250 patients of other HLA types are planned to be treated with GLSI-100 in a third arm. The trial has been designed to detect a hazard ratio of 0.3 in invasive breast cancer-free survival, where 28 events will be required. An interim analysis for superiority and futility will be conducted when at least half of those events, 14, have occurred. This sample size provides 80% power if the annual rate of events in placebo-treated subjects is 2.4% or greater.

For more information on FLAMINGO-01, please visit the Company’s website here and clinicaltrials.gov here. Contact information and an interactive map of the majority of participating clinical sites can be viewed under the “Contacts and Locations” section. Please note that the interactive map is not viewable on mobile screens. Related questions and participation interest can be emailed to: flamingo-01@greenwichlifesciences.com

About Breast Cancer and HER2/neu Positivity

One in eight U.S. women will develop invasive breast cancer over her lifetime, with approximately 300,000 new breast cancer patients and 4 million breast cancer survivors. HER2 (human epidermal growth factor receptor 2) protein is a cell surface receptor protein that is expressed in a variety of common cancers, including in 75% of breast cancers at low (1+), intermediate (2+), and high (3+ or over-expressor) levels.

About Greenwich LifeSciences, Inc.

Greenwich LifeSciences is a clinical-stage biopharmaceutical company focused on the development of GP2, an immunotherapy to prevent breast cancer recurrences in patients who have previously undergone surgery. GP2 is a 9 amino acid transmembrane peptide of the HER2 protein, a cell surface receptor protein that is expressed in a variety of common cancers, including expression in 75% of breast cancers at low (1+), intermediate (2+), and high (3+ or over-expressor) levels. Greenwich LifeSciences has commenced a Phase III clinical trial, FLAMINGO-01. For more information on Greenwich LifeSciences, please visit the Company’s website at www.greenwichlifesciences.com and follow the Company’s Twitter at https://twitter.com/GreenwichLS.

Forward-Looking Statement Disclaimer

Statements in this press release contain “forward-looking statements” that are subject to substantial risks and uncertainties. All statements, other than statements of historical fact, contained in this press release are forward-looking statements. Forward-looking statements contained in this press release may be identified by the use of words such as “anticipate,” “believe,” “contemplate,” “could,” “estimate,” “expect,” “intend,” “seek,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “target,” “aim,” “should,” “will,” “would,” or the negative of these words or other similar expressions, although not all forward-looking statements contain these words. Forward-looking statements are based on Greenwich LifeSciences Inc.’s current expectations and are subject to inherent uncertainties, risks and assumptions that are difficult to predict, including statements regarding the intended use of net proceeds from the public offering; consequently, actual results may differ materially from those expressed or implied by such forward-looking statements. Further, certain forward-looking statements are based on assumptions as to future events that may not prove to be accurate. These and other risks and uncertainties are described more fully in the section entitled “Risk Factors” in Greenwich LifeSciences’ Annual Report on the most recent Form 10-K for the year ended December 31, 2024, and other periodic reports filed with the Securities and Exchange Commission. Forward-looking statements contained in this announcement are made as of this date, and Greenwich LifeSciences, Inc. undertakes no duty to update such information except as required under applicable law.

Investor & Public Relations Contact for Greenwich LifeSciences Dave Gentry RedChip Companies Inc. Office: 1-800-RED CHIP (733 2447) Email: dave@redchip.com

Preclinical results in therapy-resistant HER2-low breast cancer models demonstrate enhanced antitumor activity and reversal of resistance with PLK1 inhibition

SAN DIEGO, March 19, 2026 (GLOBE NEWSWIRE) — Cardiff Oncology, Inc. (Nasdaq: CRDF), a clinical-stage biotechnology company leveraging PLK1 inhibition to develop novel therapies across a range of cancers, today announced that new preclinical data highlighting the potential of its highly specific oral PLK1 inhibitor, onvansertib, in combination with trastuzumab deruxtecan (T-DXd) will be presented at the American Association for Cancer Research Annual Meeting 2026, taking place April 17-22, 2026 in San Diego, California.

The poster presentation will showcase findings demonstrating that onvansertib enhanced the antitumor activity of T-DXd and reversed resistance in therapy-resistant HER2-low breast cancer models.

Poster Presentation Details:

Title:PLK1 inhibitor onvansertib potentiates the antitumor efficacy of trastuzumab deruxtecan (T-DXd) and reverses its resistance in therapy-resistant HER2-low breast cancer models

Date & Time: April 19, 2026 | 2:00 PM – 5:00 PM PT

Abstract Number: 329

The poster will be made available on the Scientific Publications page of the Company’s website following the presentation.

About Onvansertib Onvansertib is a highly specific, oral PLK1 inhibitor currently in mid-stage clinical development for RAS-mutated metastatic colorectal cancer. It is also being evaluated in multiple other cancers through investigator-initiated studies, including metastatic pancreatic ductal adenocarcinoma (mPDAC), small cell lung cancer (SCLC), triple-negative breast cancer (TNBC), and chronic myelomonocytic leukemia (CMML).

About Cardiff Oncology, Inc. Cardiff Oncology is a clinical-stage biotechnology company advancing innovative cancer treatments focused on PLK1 inhibition, a validated oncology target with practice-changing potential. Our lead asset, onvansertib, is a highly specific, oral PLK1 inhibitor currently being evaluated in a Phase 2 trial for first-line treatment of RAS-mutated metastatic colorectal cancer (“mCRC”), addressing a large, underserved patient population with high unmet need. Onvansertib is also under investigation in other PLK1-driven cancers through ongoing investigator-initiated trials and has shown robust single agent clinical activity in hard-to-treat tumors. By targeting tumor vulnerabilities, we aim to overcome treatment resistance and deliver improved clinical outcomes for patients.

VANCOUVER, BC, March 19, 2026 – Nicola Mining Inc. (the “Company” or “Nicola”) (TSX: NIM) (OTCQB: HUSIF) (FSE: HLIA) is pleased to announce that Warren Wagner has completed his Master of Science (M.Sc.) thesis, at the university of British Columba’s (UBC) Mineral Deposit Research Unit (MRDU), on the New Craigmont copper project[1]. His thesis is titled The Skarn to Porphyry Transition: Establishing Links Between Skarn and Porphyry-Type Mineralization at New Craigmont British Columbia. The full publication and supplementary data tables are available for download on the UBC website: https://open.library.ubc.ca/soa/cIRcle/collections/ubctheses/24/items/1.0451531

The purpose of the thesis was to examine the potential connection between the historically mined Craigmont skarn and undiscovered porphyry systems in the surrounding area. Using field observations, petrography, whole-rock and mineral chemistry, and integrated geochronology, Warren’s thesis has redefined Craigmont as a porphyry-linked skarn system genetically tied to multi-pulsed Late Triassic magmatism within the Guichon Creek batholith’s Border Phase.

Mineral ages determined through geochronology lab work defined two discrete hydrothermal stages: massive calcsilicate skarn alteration at ~215 Ma related to the earliest Border Phase intrusions and overprinting, vein-hosted porphyry-type mineralization at ~209 Ma associated with later, oxidized intrusions.

Potassic, phyllic, calc-potassic, and propylitic alteration styles indicate the presence of a larger porphyry system proximal to the skarn deposit. Epidote mineral chemistry from propylitic assemblages further supports this. New Craigmont epidote contains elevated porphyry indicator trace elements consistent with other porphyry deposits in British Columbia and worldwide. Finally, epidote mineral chemistry systematics within the Guichon Creek batholith reveal that New Craigmont contains a separate, porphyry centre, unrelated to those of the Highland Valley district. The study also highlights the importance of structural permeability and reactive Nicola Group host rocks in focusing hydrothermal fluids and controlling the distribution of skarn and porphyry-style mineralization.

Conclusions of the study have positive implications for ongoing exploration at New Craigmont. The study confirms Nicola’s ongoing hypothesis that the historical skarn is driven by a nearby porphyry system. Detailed geochemistry work has helped narrow exploration to broadly two regions within the property: West Craigmont (where the Draken target is located), and east of the historical mine (where the Jotun target is located). Nicola is integrating MRDU data into ongoing vectoring work and target generation.

Peter Espig, CEO of Nicola, stated, “We applaud Warren and MRDU on two years of fruitful work at our New Craigmont Copper Project. The thesis’ conclusion aligns with our growing confidence in our three years of geological work, mapping and 2025 porphyry vectoring. Given the size of our land package and location, which includes sharing Guichon Batholith with Highland Valley Copper, the prospect of having one or more porphyries at New Craigmont is increasingly compelling, as highlighted in the thesis. We are very encouraged to commence our 2026 Exploration Program.”

Qualified Person

The scientific and technical disclosures included in this news release have been reviewed and approved by Will Whitty, P.Geo., who is the Qualified Person as defined by NI 43-101. Mr. Whitty is Vice President, Exploration for the Company.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the TSX-V Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia. It has signed Mining and Milling Profit Share Agreements with high-grade BC-based gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a property that hosts historical high-grade copper mineralization and covers an area of over 10,800 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Take Private Proposal. Perfect Corp. received a preliminary, non-binding proposal from a consortium led by CEO Alice H. Chang and CyberLink to take the company private at $1.95 per share. The transaction would be funded through rollover equity, company cash, and potential debt. The board intends to form a special committee to evaluate the proposal, and there is no assurance that a transaction will be completed.

Ownership structure supports a high likelihood of completion. The consortium controls approximately 53.4% of shares and 81.2% of voting power. In our view, this significantly increases the likelihood of a transaction, subject to special committee approval.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Star Equity’s fourth quarter and full-year financial results reflect positive momentum and improvement over the prior year quarter, largely driven by the August 2025 merger. Overall, 2025 was a transformational year for Star. The merger strengthened the Company’s operating and financial position and accelerated the growth strategy.

4Q25 Results. Fourth quarter 2025 revenue of $56.8 million rose 69% y-o-y, but was slightly below our $58 million estimate. Adjusted EBITDA increased to $2.2 million versus $0.9 million last year. We had projected $2.3 million. Adjusted net loss was $0.10/sh, compared to adjusted net income of $0.04/sh in 4Q24.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

SelectQuote Local. SelectQuote announced SelectQuote Local, a new franchise model designed to complement its core telephonic insurance distribution platform by offering in-person sales and support. Management indicated the initiative leverages the company’s existing marketing, technology, and carrier relationships, positioning it as a natural extension of the platform rather than a shift in strategy.

Complementary model and TAM expansion. In our view, SelectQuote Local is unlikely to cannibalize the company’s core call center operations, as it targets a distinct subset of consumers who prefer in-person engagement. We believe the company can leverage excess lead flow and brand recognition to support early franchise success without significant incremental marketing investment. Additionally, we expect the in-person model could enhance cross-sell opportunities with Healthcare Services, as local relationships may improve customer engagement and trust.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Kuya Silver is significantly scaling its exploration efforts at Bethania. The company has expanded its fully funded 2026 drill program to approximately 20,000 meters, making it the largest drilling campaign in the project’s history. By combining 10,000 meters of surface and 10,000 meters of underground drilling, Kuya seeks to extend known mineralization near existing operations and test new district scale targets, positioning the project for meaningful resource growth.

High-grade regional targets highlight strong expansion potential. Exploration has identified multiple vein systems beyond the current mine area, with high priority prospects such as Millococha, Tito PH, and Carmelitas demonstrating encouraging grades and geological continuity. These areas, supported by historic artisanal mining and recent sampling, suggest the presence of a broader mineralized system that could materially increase the overall resource base.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.