Research News and Market Data on BODI

November 10, 2025

Net Income Reported for First Time Since Going Public in 2021

Revenues, Net Income and Adjusted EBITDA Better Than Guidance

Gross Margin of 75%-up 730bps over prior year

Eighth Consecutive Quarter of Positive Adjusted EBITDA

Clear Visibility to Positive Free Cash Flow For the Full Year

EL SEGUNDO, Calif.–(BUSINESS WIRE)– The Beachbody Company, Inc. (NASDAQ: BODi) (“BODi” or the “Company”), a leading fitness and nutrition company, today announced financial results for its third quarter ended September 30, 2025.

Carl Daikeler, BODi’s Co-Founder and Chief Executive Officer, commented:

“Our strategic transformation continues to deliver better than expected results. As we continue building a more efficient operating model, we are pleased to have generated net income for the first time since becoming a public company in 2021. We have executed a significant turnaround focused on strengthening our financial position, significantly lowering our break-even point, and enabling the company to capitalize on the operating leverage that is now built into the business. Our improved financial position allows us to leverage our robust innovation pipeline that we have developed with a goal of returning the company to topline growth.”

“Looking ahead, we’re building on a solid foundation with eight consecutive quarters of positive adjusted EBITDA and clear visibility to positive free cash flow for the full year. Our strengthened balance sheet positions us to expand distribution into new channels and capitalize on the significant opportunities in the health and wellness market. BODi is uniquely positioned to help more people achieve their fitness goals while driving sustainable growth for our shareholders.”

Third Quarter 2025 Results

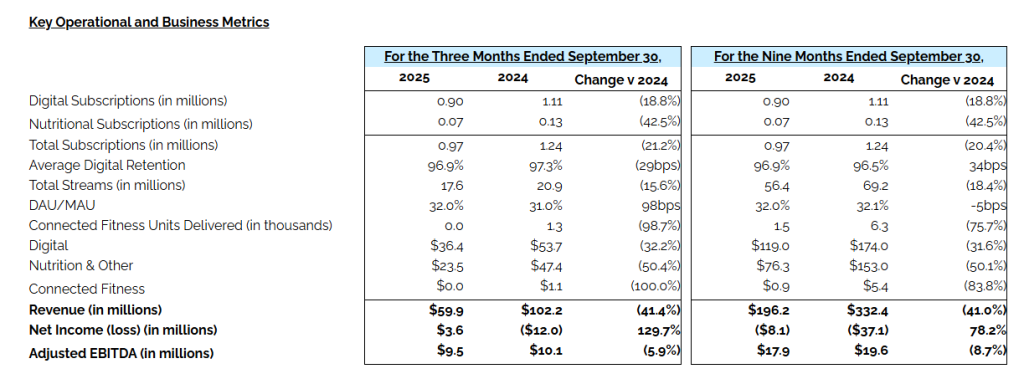

- Total revenue was $59.9 million compared to $102.2 million in the prior year period.

- Digital revenue was $36.4 million compared to $53.7 million in the prior year period and digital subscriptions totaled 0.90 million in the third quarter.

- Nutrition and Other revenue was $23.5 million compared to $47.4 million in the prior year period and nutritional subscriptions totaled 0.07 million in the third quarter.

- Connected Fitness revenue was $0.0 million compared to $1.1 million in the prior year period as we ceased the sale of bike inventory in the first quarter of 2025.

- Gross margin was 74.6% compared to 67.3% in the prior year period.

- Total operating expenses were $39.7 million compared to $81.8 million in the prior year period, which included $9.2 million of restructuring related costs.

- Operating income improved by $18.0 million to $5.0 million, the Company’s first operating income since going public, compared to an operating loss of $13.0 million in the prior year period.

- Net income was $3.6 million, the Company’s first net income since going public, compared to a net loss of $12.0 million in the prior year period, which included $9.2 million of restructuring related costs.

- Adjusted EBITDA 1 was $9.5 million compared to $10.1 million in the prior year period.

- Cash provided by operating activities for the nine months ended September 30, 2025 was $16.8 million compared to cash provided by operating activities of $9.3 million in the prior year period, and cash used in investing activities was $3.7 million compared to cash provided by investing activities of $1.6 million in the prior year period. Free cash flow 1 was $13.1 million compared to $5.3 million in the prior year period.

The prior year periods do not reflect the impact of the pivot in our business model that the Company announced on September 30, 2024 and executed in the fourth quarter of 2024, so results are not directly comparable with the prior periods.

1Definitions of (1) Adjusted EBITDA, (2) free cash flow and (3) net cash position, and reconciliations to the comparable GAAP metrics, are at the end of this release.

Conference Call and Webcast Information

BODi will host a conference call at 5:00pm ET on Monday, November 10, 2025, to discuss its financial results and matters other than past results, such as guidance. To participate in the live call, please dial (833) 470-1428 (U.S. & Canada) and provide the conference identification number: 828838. The conference call will also be available to interested parties through a live webcast at https://investors.thebeachbodycompany.com/.

A replay of the call will be available until November 17, 2025, by dialing (866) 813-9403 (U.S & Canada). The replay passcode is 739586.

After the conference call, a webcast replay will remain available on the investor relations section of the Company’s website for one year.

About BODi and The Beachbody Company, Inc.

Originally known as Beachbody, BODi has been innovating structured step-by-step home fitness and nutrition programs for 26 years with products such as P90X, Insanity, and 21-Day Fix, plus the first premium superfood nutrition supplement, Shakeology. Since its inception in 1999 BODi has helped over 30 million customers pursue extraordinary life-changing results. The BODi community includes millions of people helping each other stay accountable to goals of healthy weight loss, improved strength and energy, and resilient mental and physical well-being. For more information, please visit TheBeachBodyCompany.com.

Safe Harbor Statement

This press release of The Beachbody Company, Inc. (“we,” “us,” “our,” and similar terms) contains “forward-looking” statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are statements other than statements of historical facts and statements in future tense. These statements include but are not limited to, statements regarding our future performance and our market opportunity, including expected financial results for the second quarter and full year, our business strategy, our plans, and our objectives and future operations.

Forward-looking statements are based upon various estimates and assumptions, as well as information known to us as of the date hereof, and are subject to risks and uncertainties. Accordingly, actual results could differ materially due to a variety of factors, including: our ability to effectively compete in the fitness and nutrition industries; our ability to successfully acquire and integrate new operations; our reliance on a few key products; market conditions and global and economic factors beyond our control; intense competition and competitive pressures from other companies worldwide in the industries in which we operate; and litigation and the ability to adequately protect our intellectual property rights. You can identify these statements by the use of terminology such as “believe”, “plans”, “expect”, “will”, “should,” “could”, “estimate”, “anticipate” or similar forward-looking terms. You should not rely on these forward-looking statements as they involve risks and uncertainties that may cause actual results to vary materially from the forward-looking statements. For more information regarding the risks and uncertainties that could cause actual results to differ materially from those expressed or implied in these forward-looking statements, as well as risks relating to our business in general, we refer you to the “Risk Factors” section of our Securities and Exchange Commission (SEC) filings, including those risks and uncertainties included in the Form 10-K filed with the SEC on March 28, 2025 and any subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K, which are available on the Investor Relations page of our website at https://investors.thebeachbodycompany.com and on the SEC website at www.sec.gov.

All forward-looking statements contained herein are based on information available to us as of the date hereof and you should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, performance, or achievements. We undertake no obligation to update any of these forward-looking statements for any reason after the date of this press release or to conform these statements to actual results or revised expectations, except as required by law. Undue reliance should not be placed on forward-looking statements.

Investor Relations

IR@BODi.com

Source: The Beachbody Company, Inc.