Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

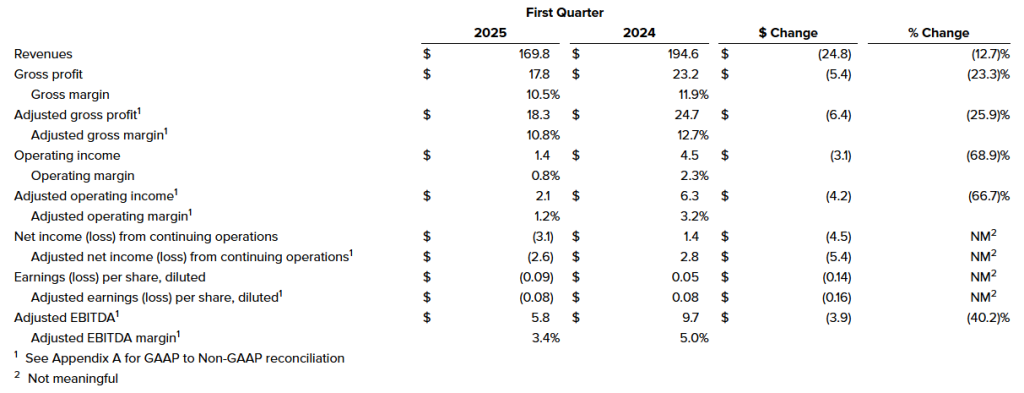

Performance Continues to Struggle. First quarter revenue declined 12.7% to $169.8 million from $194.6 million during the same prior year period. The revenue outperformed our estimate of $160.0 million. Operating income and adjusted operating income of $1.4 million and $2.1 million, respectively, decreased by $3.1 million and $4.2 million. Net loss totaled $3.1 million, or $0.09/share, and adjusted net loss totaled $2.6 million, or $0.08/share. Adjusted EBITDA declined to $5.8 million from $9.7 million.

Continued Headwinds. 2025 continues the trends of last year, with challenging global construction and agricultural end markets and lower customer demand across all segments. Furthermore, the recent policy changes and subsequent economic environment have temporarily driven further market confusion. ACT Research projects 2025 North American Class 8 truck production levels to be around 255,000 units compared to 333,372 in 2024, while the Construction and Agriculture markets are projected to be down 5-15% in 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

U.S. oil production is approaching a turning point, according to Diamondback Energy CEO Travis Stice. In a letter to shareholders this week, Stice warned that domestic output has likely peaked and will begin to decline in the coming months, citing falling crude prices and slowing industry activity as key factors.

“U.S. onshore oil production has likely peaked and will begin to decline this quarter,” Stice wrote. “We are at a tipping point for U.S. oil production at current commodity prices.”

The warning comes as U.S. crude prices have dropped roughly 17% this year, weighed down by fears of a global economic slowdown tied to President Donald Trump’s renewed tariffs and an aggressive supply push from OPEC+ producers. Prices for West Texas Intermediate (WTI) crude briefly surged 4% on Tuesday to $59.56 per barrel amid expectations that U.S. supply will tighten.

Stice emphasized that adjusted for inflation, oil is now cheaper than it has been in nearly every quarter since 2004—excluding the pandemic collapse in 2020. That pricing reality, he said, is forcing producers to slash spending and slow operations, threatening broader economic impacts.

Diamondback, a major producer in the Permian Basin and one of the largest independent oil companies in the U.S., has already reduced its capital spending by $400 million for the year. The company now plans to drill between 385 to 435 wells and complete 475 to 550, while maintaining reduced rig and crew levels.

“We’ve dropped three rigs and one completion crew, and expect to stay at those levels for most of Q3,” Stice said.

The U.S. shale boom of the last 15 years helped make the country the world’s top fossil fuel producer, outpacing even Saudi Arabia and Russia. That shift reshaped the U.S. economy, reduced reliance on foreign energy, and strengthened national security. But Stice now warns that this progress is at risk.

“Today’s prices, volatility and macroeconomic uncertainty have put this progress in jeopardy,” he said.

Fracking activity is already falling sharply. The number of completion crews is down 15% nationwide and 20% in the Permian Basin since January, Stice said. Oil-directed drilling rigs are expected to drop nearly 10% by the end of Q2, with further declines projected in the third quarter.

Adding to the pressure are rising costs tied to tariffs. Stice said Trump’s steel tariffs have added around $40 million annually to Diamondback’s expenses, raising well costs by about 1%. While some of this impact may be offset by operational efficiencies, the CEO warned that sustaining current output levels at lower prices may no longer be financially viable.

Stice likened the situation to approaching a red light while driving: “We are taking our foot off the accelerator. If the light turns green, we’ll hit the gas again—but we’re prepared to brake if needed.”

As the U.S. energy sector confronts an increasingly uncertain landscape, the prospect of declining domestic production is no longer just a possibility—it’s becoming a reality.

First quarter sales of $170 million, EPS of $(0.09), Adjusted EBITDA of $5.8 million Significantly improved free cash flow enables further debt paydown Updates guidance for full year 2025

NEW ALBANY, Ohio, May 06, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its first quarter ended March 31, 2025.

During the quarter, the Company completed a strategic reorganization of its operations into three segments: Global Seating, Global Electrical Systems, and Trim Systems and Components. The results and comparisons presented below reflect continuing operations unless otherwise noted.

First Quarter 2025 Highlights(Results from Continuing Operations; compared with prior year, where comparisons are noted)

Revenues of $169.8 million, down 12.7%, primarily due to softening in global Construction and Agriculture markets and North America Class 8 truck demand.

Operating income of $1.4 million, adjusted operating income of $2.1 million, down compared to operating income of $4.5 million and adjusted operating income of $6.3 million. The decrease in operating income was driven primarily by lower sales volumes offset by reductions in SG&A expense.

Net loss from continuing operations of $3.1 million, or $(0.09) per diluted share and adjusted net loss of $2.6 million, or $(0.08) per diluted share, compared to net income from continuing operations of $1.4 million, or $0.05 per diluted share and adjusted net income of $2.8 million, or $0.08 per diluted share.

Adjusted EBITDA of $5.8 million, down 40.2%, with an adjusted EBITDA margin of 3.4%, down from 5.0%.

Free cash flow of $11.2 million, up $17.7 million, due to better working capital management. Net debt decreased $11.7 million compared to the year end 2024 level.

Gross margin expansion of 250 basis points versus Q4 2024 due to operational efficiency improvements and conclusion of one-time cost drivers from 2024.

James Ray, President and Chief Executive Officer, said, “Our first quarter results demonstrate sequential improvement in margins and free cash flow. Cash generation and debt paydown remain key priorities for CVG, as we look to build on our strong free cash performance in the first quarter through further margin improvement, working capital reduction, and reduced capital expenditures. We are beginning to see the benefits of efforts made in 2024, including strategic divestments of non-core businesses, to transform CVG. These divestitures, as well as our priority on improving operational efficiency, have allowed us to streamline operations, lower our cost structure, and drive cash generation to pay down debt. Despite industry-wide and global macroeconomic headwinds, we are prioritizing strong execution from the top down within CVG focused on cost mitigation, margin improvement, and operational efficiency.”

Mr. Ray continued, “The actions we took last year position us well for the future. Change management is always difficult, and I would personally like to thank the entire CVG team for their efforts throughout the process. I would like to thank Bob Griffin, our current Chairman, for his contributions to CVG’s strategic goals and priorities over the years. I am also excited to continue working with Bill Johnson, a current board member who is expected to become the Chairman of the Board following Mr. Griffin’s retirement, effective May 15, 2025. While we acknowledge the current macroeconomic uncertainties and geopolitical environment, the transformation undertaken in 2024 makes CVG a lower cost, more nimble company, better positioned to navigate these challenges. We are committed to execution, delivery, and driving operational efficiency, while managing the potential impact of trade policy.”

Andy Cheung, Chief Financial Officer, added, “We are encouraged by the quarter-over-quarter improvement in our financial performance, as we start to see the benefits of our strategic portfolio realignment and operational efficiency efforts. However, given the economic environment and policy concerns, we are adjusting our outlook to reflect current market conditions. Our focused portfolio, now more closely aligned with our customers through our re-segmentation, positions us for improved value capture as end markets recover.”

First Quarter Financial Results from Continuing Operations (amounts in millions except per share data and percentages)

Consolidated Results from Continuing Operations

First Quarter 2025 Results

First quarter 2025 revenues were $169.8 million, compared to $194.6 million in the prior year period, a decrease of 12.7%. The overall decrease in revenues was due to lower sales as a result of a softening in customer demand across all segments.

Operating income in the first quarter 2025 was $1.4 million compared to $4.5 million in the prior year period. The decrease in operating income was attributable to the impact of lower sales volumes. First quarter 2025 adjusted operating income was $2.1 million, compared to $6.3 million in the prior year period.

Interest associated with debt and other expenses was $2.5 million and $2.2 million for the first quarter 2025 and 2024, respectively.

Net loss from continuing operations was $3.1 million, or $(0.09) per diluted share, for the first quarter 2025 compared to net income of $1.4 million, or $0.05 per diluted share, in the prior year period. First quarter 2025 adjusted net loss from continuing operations was $2.6 million, or $(0.08) per diluted share, compared to adjusted net income of $2.8 million, or $0.08 per diluted share.

On March 31, 2025, the Company had $32.4 million of outstanding borrowings on its U.S. revolving credit facility and no outstanding borrowings on its China credit facility, $20.2 million of cash and $102.5 million of availability from the credit facilities (subject to covenant limitations), resulting in total liquidity of $122.7 million.

First Quarter 2025 Segment Results

Global Seating Segment

Revenues were $73.4 million compared to $80.8 million for the prior year period, a decrease of 9.1%, due to lower sales volume as a result of decreased customer demand.

Operating income was $2.7 million, compared $2.8 million in the prior year period, a decrease of 3.0%, primarily attributable to lower sales volume and increased freight costs. First quarter 2025 adjusted operating income was $2.7 million compared to $2.8 million in the prior year period.

Global Electrical Systems Segment

Revenues were $50.5 million compared to $58.7 million in the prior year period, a decrease of 14.1%, primarily as a result of decreased customer demand.

Operating loss was $0.3 million compared to operating income of $0.4 million in the prior year period. The decrease in operating income was primarily attributable to lower sales volumes and unfavorable foreign exchange impacts. First quarter 2025 adjusted operating income was $0.2 million compared to $1.5 million in the prior year period.

Trim Systems and Components Segment

Revenues were $45.9 million compared to $55.1 million in the prior year period, a decrease of 16.6%, primarily as a result of decreased customer demand.

Operating income was $1.5 million compared to $4.2 million in the prior year period, a decrease of 63.5%. The decrease in operating income was primarily attributable to lower sales volume and increased freight costs. First quarter 2025 adjusted operating income was $1.6 million compared to $4.7 million in the prior year period.

Outlook

CVG updated the Company’s outlook for the full year 2025, based on current market conditions:

This outlook reflects, among others, current industry forecasts for North America Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 255,000 units. The 2024 actual Class 8 truck builds according to the ACT Research was 332,372 units.

Construction and Agriculture end markets are projected to decline approximately 5-15% in 2025. However, we expect the contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Wednesday, May 7, 2025, at 8:30 a.m. ET. Management intends to reference the Q1 2025 Earnings Call Presentation during the conference call. To participate, dial (800) 549-8228 using conference code 57416. International participants dial (289) 819-1520 using conference code 57416.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 57416#.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness, and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

Other Information

Throughout this document, certain numbers in the tables or elsewhere may not sum due to rounding. Rounding may have also impacted the presentation of certain year-on-year percentage changes.

Enhanced Buy-Side Revenue Demonstrating Business Segment Growth as Orange 142 Scales

19% Reduction in Operating Expenses Compared with 1Q24 Driven by Strategic Cost Saving Initiatives

Entered New Strategic Partnerships to Diversify and Expand Addressable Market

HOUSTON, May 6, 2025 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”) and Orange 142, LLC (“Orange 142”), today announced financial results for the first quarter ended March 31, 2025.

Mark D. Walker, Chairman and Chief Executive Officer, commented, “As we begin to move through 2025, we are focused on continuing to scale our buy-side solution while simultaneously rebuilding our sell-side business. During the first quarter, which is historically our weakest quarter, we recognized consolidated revenue of $8.2 million, supported primarily by buy-side revenue of $6.1 million which was up 6% compared to the prior year. Sequentially, first quarter sell-side revenue of $2.0 million is relatively comparable to fourth quarter 2024 sell-side revenue of $2.7 million, an encouraging trend given that (1) fourth quarter is typically the strongest quarter for the sell-side business based on seasonality and (2) our 2024 fourth quarter included $0.7 million of political spend. In the first quarter of 2025, we saw the continued impact of the disruption of our sell-side business in 2024, however, we are pleased by the ongoing commitment of our agency, brand and publisher partners to resume or increase activity with the Company once direct connections are fully integrated in the second half of 2025, and we are working diligently to restore this segment to previous levels.

“Our focus in 2025 is on driving growth and value for our shareholders,” Mr. Walker continued. “We’ve launched several initiatives to drive our progress, including revenue optimization efforts to diversify our revenue base and cost saving initiatives to drive reductions in operating expenses and enhance operational efficiencies. In the first quarter of 2025, we reduced operating expenses by nearly $1.5 million, or approximately 19% when compared to the first quarter of 2024. We continue to evaluate the optimal personnel and cost structure for our business.

“At the business unit level, the unification of our two buy side divisions into Orange 142 has allowed us to better service the small to mid-sized partners who represent a significant growth opportunity for our business. Moreover, our Colossus Connections, launched in the third quarter of 2024 to accelerate direct integration efforts with leading demand-side platforms, is progressing well, and as previously reported, we signed up two of the leading marketplace partners and we recently added two additional mid-tier partners who are near completion with integration. We expect to see the impact of these new partners on our revenues in the second half of 2025 once integration has been completed,” Mr. Walker stated.

“With our current visibility, we maintain our current revenue guidance of $90 million to $110 million for the full fiscal year of 2025 supported by growth across both our buy-side and sell-side segments. There is still a great deal of work to be done in a challenging and uncertain time, but we believe that we are well positioned with a revitalized model, prudent cost management strategies, and strong demand for our products and services to drive growth and value as we navigate the business back to profitability,” Mr. Walker concluded.

Keith Smith, President, commented, “We remain focused on strategically recalibrating and enhancing our business model to capitalize on new opportunities and meet the demands of our diverse partners. We faced significant challenges in 2024, and we are now emerging as a stronger, more nimble business intent on continuing to scale and expand our offerings. From a liquidity perspective, we continue to explore strategic opportunities to support key growth initiatives and drive long term value for our shareholders.”

First Quarter 2025 Highlights

Processed approximately 188 billion average monthly impressions through the sell-side advertising segment.

Sell-side advertisers increased 13% compared to the first quarter of 2024.

Sell-side media properties of 24,000 average per month in the first quarter of 2025 decreased 8% compared to the first quarter of 2024, increased 20% over the same period in 2023, and decreased 15% sequentially compared to the fourth quarter of 2024.

Buy-side advertising segment served over 220 customers in the first quarter of 2025.

Buy-side advertising revenue for the first quarter of 2025 included $1.2 million from customers in new verticals.

Continued to consider strategic opportunities to support key growth initiatives and drive long term value for shareholders.

First Quarter 2025 Financial Results

Revenue of $8.2 million decreased 63% compared to $22.3 million in the first quarter of 2024.

Sell-side advertising segment revenue of $2.0 million decreased 88% compared to $16.5 million in the first quarter of 2024. The decrease in sell-side advertising revenue was primarily related to a decrease in impression inventory when compared to the first quarter of 2024.

Buy-side advertising segment revenue of $6.1 million increased 6% compared to $5.8 million in the same period of 2024.

Gross profit was $2.4 million, or 29% of revenue, compared to $5.0 million, or 22% of revenue, in the first quarter of 2024.

Operating expenses of $6.3 million decreased $1.5 million, or 19%, compared with $7.8 million in the same period of 2024. The reduction in operating expenses was primarily driven by decreased payroll costs related to the Company’s internal reorganization and cost saving measures to lower certain ongoing expenses.

Operating loss was $3.9 million, compared to operating loss of $2.8 million in the prior year period.

Net loss was $5.9 million compared to net loss of $3.8 million in the first quarter of 2024.

Adjusted EBITDA1 loss was $3.0 million in the first quarter of 2025 compared to a loss of $1.7 million in the first quarter of 2024.

As of March 31, 2025, the Company held cash and cash equivalents of $1.8 million compared to $1.4 million as of December 31, 2024.

Financial Outlook

Based on current visibility and subject to general market factors, the Company is maintaining its full year guidance of $90 million to $110 million for full year 2025. This target is based on the expectation of consolidated revenue growth compared to full year 2024 driven by enhanced buy-side activity through Orange 142 and the ongoing recovery of the Company’s sell-side business rebuilds to historical revenue levels.

Diana Diaz, Chief Financial Officer, stated, “Our focus continues to be on optimizing performance, reducing our cost structure, and driving efficiencies as we navigate the business back to profitability. With our visibility today, we believe that we are well positioned to achieve our financial goals for the fiscal year.”

Conference Call and Webcast Details

Direct Digital will host a conference call today, May 6, 2025, at 5:00 p.m. Eastern Time to discuss the Company’s first quarter 2025 financial results. The live webcast and replay can be accessed at https://ir.directdigitalholdings.com/. Please access the website at least fifteen minutes prior to the call to register, download and install any necessary audio software. For those who cannot access the webcast, a replay will be available at https://ir.directdigitalholdings.com/ for a period of twelve months.

__________________________________

1“Adjusted EBITDA” and “Adjusted Operating Expenses” are non-GAAP financial measures. The section titled “Non-GAAP Financial Measures” below describes our usage of non-GAAP financial measures and provides reconciliations between historical GAAP and non-GAAP information contained in this press release.

This press release contains forward-looking statements within the meaning of federal securities laws that are subject to certain risks, trends and uncertainties. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Accordingly, any such statements are qualified in their entirety by reference to the information described under the caption “Risk Factors” and elsewhere in our most recent Annual Report on Form 10-K for the fiscal year ended December 31, 2024 (the “Form 10-K”) and subsequent periodic and or current reports filed with the Securities and Exchange Commission (the “SEC”).

The forward-looking statements contained in this press release are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. As you read and consider this press release, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (many of which are beyond our control) and assumptions.

Although we believe that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements. We believe these factors include, but are not limited to, the following: the restrictions and covenants imposed upon us by our credit facilities; the substantial doubt about our ability to continue as a going concern, which may hinder our ability to obtain future financing; our ability to secure additional financing to meet our capital needs; our ineligibility to file short-form registration statements on Form S-3, which may impair our ability to raise capital; our failure to satisfy applicable listing standards of the Nasdaq Capital Market resulting in a potential delisting of our common stock; costs, risks and uncertainties related to restatement of certain prior period financial statements; any significant fluctuations caused by our high customer concentration; risks related to non-payment by our clients; reputational and other harms caused by our failure to detect advertising fraud; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; our failure to manage our growth effectively; the difficulty in identifying and integrating any future acquisitions or strategic investments; any changes or developments in legislative, judicial, regulatory or cultural environments related to information collection, use and processing; challenges related to our buy-side clients that are destination marketing organizations and that operate as public/private partnerships; any strain on our resources or diversion of our management’s attention as a result of being a public company; the intense competition of the digital advertising industry and our ability to effectively compete against current and future competitors; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; as a holding company, we depend on distributions from Direct Digital Holdings, LLC (“DDH LLC”) to pay our taxes, expenses (including payments under the Tax Receivable Agreement) and any amount of any dividends we may pay to the holders of our common stock; the fact that DDH LLC is controlled by DDM, whose interest may differ from those of our public stockholders; any failure by us to maintain or implement effective internal controls or to detect fraud; and other factors and assumptions discussed in our Form 10-K and subsequent periodic and current reports we may file with the SEC.

Should one or more of these risks or uncertainties materialize, or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this press release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. New factors that could cause our business not to develop as we expect emerge from time to time, and it is not possible for us to predict all of them. Further, we cannot assess the impact of each currently known or new factor on our results of operations or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT) combines cutting-edge sell-side and buy-side advertising solutions, providing data-driven digital media strategies that enhance reach and performance for brands, agencies, and publishers of all sizes. Our sell-side platform, Colossus SSP, offers curated access to premium, growth-oriented media properties throughout the digital ecosystem. On the buy-side, Orange 142 delivers customized, audience-focused digital marketing and advertising solutions that enable mid-market and enterprise companies to achieve measurable results across a range of platforms, including programmatic, search, social, CTV, and influencer marketing. With extensive expertise in high-growth sectors such as Energy, Healthcare, Travel & Tourism, and Financial Services, our teams deliver performance strategies that connect brands with their ideal audiences.

At Direct Digital Holdings, we prioritize personal relationships by humanizing technology, ensuring each client receives dedicated support and tailored digital marketing solutions regardless of company size. This empowers everyone to thrive by generating billions of monthly impressions across display, CTV, in-app, and emerging media channels through advanced targeting, comprehensive data insights, and cross-platform activation. DDH is “Digital advertising built for everyone.”

All-American Wing Chain to Open 10 Locations in Country over Next Three Years

LOS ANGELES, May 06, 2025 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Buffalo’s Cafe and 17 other restaurant concepts, announces the expansion of Buffalo’s Cafe in France in partnership with the group behind Big M CIE, opening 10 units in the country with the first three units set to open by 2026. To coincide with the new locations, the beloved wing brand is unveiling a fast casual model with a smaller footprint to position itself for greater growth across the globe.

“The launch of a new Buffalo’s Cafe fast casual model in France represents a significant milestone in our growth trajectory of the brand, and opens up the door to additional expansion opportunities,” said Taylor Wiederhorn, Co-CEO and Chief Development Officer of FAT Brands. “This announcement also follows Medhi Bella and his team signing a commitment to open 30 Fatburger locations across France—opening a total of 40 locations with FAT Brands. We see a bright future ahead with this partnership as we continue to grow our iconic, all-American brands in the country.”

For 40 years, Buffalo’s Cafe has been known for its authentic Buffalo-style chicken wings, house-made wing sauces and family-friendly environment.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets and develops fast casual, quick-service, casual and polished casual dining restaurant concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Buffalo’s Cafe

Founded in 1985 in Roswell, Georgia, the family-themed casual dining chain, known for its world-famous chicken wings and 18 unique homemade wing sauces, burgers, wraps, steaks, and salads has been serving fresh southwestern themed cuisine for 40 years. Featuring a full bar and table service, Buffalo’s Cafe offers an unparalleled dining experience affording friends and family the flexibility to enjoy an intimate dinner together or to casually catch the next sporting event while enjoying robust menu offerings. Buffalo’s – Where Everyone Is Family™. For more information, visit www.buffalos.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the timing and performance of new store openings and area development agreements. Forward-looking statements reflect expectations of FAT Brands Inc. (“we” or “our”) concerning the future and are subject to significant business, economic and competitive risks, uncertainties and contingencies. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

May 6, 2025 – Vancouver, Canada – Century Lithium Corp. (TSXV: LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (“Century Lithium” or “the Company”) is pleased to provide an update on its 100%-owned lithium project, Angel Island (“Angel Island”) near Silver Peak, Nevada and the associated Lithium Extraction Facility (“Demonstration Plant”) in Amargosa Valley, Nevada.

“Century Lithium has continued to advance Angel Island through the Company’s Demonstration Plant,” said Bill Willoughby, Century Lithium President and CEO. “Our Demonstration Plant allows us to improve our technology through various avenues of testing, most recently with ARi, where recent results have exceeded our expectations.”

Advancements to the Demonstration Plant

Century Lithium has successfully completed testing at the Demonstration Plant in collaboration with Amalgamated Research, LLC (“ARi”) of Twin Falls, Idaho. This testing focused on new developments within the Direct Lithium Extraction (“DLE”) portion of Century Lithium’s process. These results exceeded expectations for lithium recovery and eluate grade produced from a primary step in the DLE process. The Company believes this could result in a substantial reduction in the estimated capital and operating costs at Angel Island.

Results from DLE Pilot Testing (November 2024–January 2025):

328 milligrams per liter (“mg/L”) lithium feed concentration

91.6% lithium recovery

575 mg/L eluate grade with a low Na:Li ratio of 0.6:1

Additional Technical Progress at the Demonstration Plant

An increase of lithium in eluate to 12 to 14 grams per liter (“g/L”) lithium concentration using specialty membranes in the concentration steps following DLE

Continued operation of the lithium carbonate (“Li2CO3”) circuit, resulting in 99.87% purity in Li2CO3 samples

Third-party evaluation is underway on Li2CO3 samples for use in producing lithium iron phosphate (“LFP”) batteries. LFP batteries have a high energy density and long cycle life and are used in solar, energy storage systems and long-range EV applications

Testing is underway for thermal pretreatment of Angel Island clay with the potential to significantly reduce hydrochloric acid use in the leach stage of processing

Qualified Person

Todd Fayram, MMSA-QP and Senior Vice President, Metallurgy of Century Lithium is the qualified person as defined by National Instrument 43-101 and has approved the technical information in this release.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced stage lithium company, focused on developing its wholly owned Angel Island project in Esmeralda County, Nevada, which hosts one of the largest sedimentary lithium deposits in the United States. The Company has utilized its patent-pending process for chloride leaching combined with direct lithium extraction to make battery-grade lithium carbonate product samples from Angel Island’s lithium-bearing claystone on-site at its Demonstration Plant in Amargosa Valley, Nevada.

Angel Island is one of the few advanced lithium projects in development in the United States to provide an end-to-end process to produce battery-grade lithium carbonate for the growing electric vehicle and battery storage market. Angel Island is currently in the permitting stage for a three-phase feasibility-level production plan expected to yield an estimated life-of-mine average of 34,000 tonnes per year of carbonate over a 40-year mine-life.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.

These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.com. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Private placement financing. Aurania Resources closed the second and final tranche of its non-brokered private placement financing. A total of 2,569,022 units of the company were sold under the second tranche at a price of C$0.30 per unit. Including the first tranche which closed on April 17, Aurania issued 5,751,921 units for gross proceeds of C$1,725,577. Net proceeds will be used to fund general working capital needs and may be used to pay mineral concession fees in Ecuador.

Terms of the offering. Each unit is composed of one common share and one common share purchase warrant. Each warrant entitles the holder to purchase one common share at an exercise price of C$0.55 for a period of 24 months following the closing of the date of issuance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strategy Working. V2X’s unique full-lifecycle, mission-driven strategy is working, resulting in not only an expanded opportunity set but significantly larger individual opportunities than in the past. The Company’s focus on enhancing mission effectiveness, extending asset utilization, reducing costs, and improving security and mission outcomes dovetails nicely with the focus of the DoD and the current Administration.

1Q25 Results. Revenue came in at $1.015 billion compared to $1.01 billion in 1Q24 and our $1.04 billion estimate, with 10% y-o-y growth in Indopacom the driver. Adjusted EBITDA was $67 million, down slightly from $69 million last year and in-line with our estimate. Adjusted EPS was $0.98, up from $0.90 last year and our $0.89 estimate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter financial results. FreightCar America earned adjusted net income of $1.604 million or $0.05 per share compared to our estimate of $1.223 million or $0.03 per share. The variance to our estimates were largely revenue and margin driven. As expected, revenue and rail car deliveries declined to $96.3 million and 710, respectively, compared to $161.1 million and 1,223 during the first quarter of 2023. Our estimates were $82.5 million and 700. During the quarter, a portion of RAIL’s railcar production capacity was utilized to build spare parts for its Aftermarket segment. Management expected lower deliveries to be reflected in first quarter revenues. Gross profit and margin improved to $14.4 million and 14.9%, respectively, compared to $11.4 million and 7.1% during the prior year period. Adjusted EBITDA increased to $7.3 million compared to $6.1 million during the first quarter of 2023. RAIL generated free cash flow of $12.5 million and ended the quarter with $54.1 million in cash.

Favorable outlook. First quarter sales activity was strong with 1,250 railcars ordered. With a backlog of 3,337 units valued at $318 million, we expect deliveries to accelerate throughout the year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In a major strategic shift, OpenAI announced Monday that it will no longer pursue a full for-profit transformation and will instead maintain its original nonprofit governance structure. The decision, which follows months of internal and external pressure, reaffirms the organization’s commitment to building artificial general intelligence (AGI) for the benefit of humanity — not just shareholders.

The announcement came in a letter from CEO Sam Altman, who cited conversations with civic leaders and discussions with the Attorneys General of California and Delaware as key factors behind the change. “We made the decision for the nonprofit to stay in control,” Altman wrote, emphasizing a renewed focus on public interest and ethical stewardship of AI technologies like ChatGPT.

OpenAI was originally founded in 2015 as a nonprofit with the ambitious goal of ensuring that AGI — artificial intelligence that can outperform humans across a broad range of tasks — would be developed safely and equitably. Over time, however, the organization layered on a “capped-profit” arm to attract commercial investment and scale operations. That for-profit entity will now be restructured into a public benefit corporation (PBC) — a legally recognized business type that must weigh public impact alongside financial returns.

Bret Taylor, chair of OpenAI’s nonprofit board, clarified that this new structure aims to balance mission and market. “The public benefit corporation model ensures we can grow while staying true to our founding purpose,” he said.

The move comes as OpenAI faces intensifying legal, political, and ethical scrutiny. One major flashpoint is an ongoing lawsuit filed by co-founder Elon Musk, who accused the company and Altman of straying from its original principles. While a federal judge recently dismissed several of Musk’s claims, parts of the case will proceed to trial next year. The lawsuit has amplified a broader debate over whether cutting-edge AI development should be governed by public-interest frameworks or private market incentives.

In addition to legal pressure, OpenAI has come under the microscope from the Attorneys General of California and Delaware — the two jurisdictions where the company operates and is incorporated. Advocacy groups and former employees had petitioned both states’ top law enforcement officials to intervene, arguing that OpenAI’s planned restructuring posed a risk to its charitable mission.

Critics feared a future in which OpenAI — armed with the capability to develop superhuman AI — could shift its focus toward profit maximization at the expense of public safety. These concerns, coupled with growing public reliance on ChatGPT (which now boasts over 400 million weekly users), helped fuel a backlash against the proposed governance changes.

Ultimately, the reversal signals that OpenAI is listening. By recommitting to nonprofit oversight, the company aims to rebuild trust and reinforce its identity as a mission-driven organization — even as it operates at the forefront of one of the world’s most powerful technological revolutions.

Whether this hybrid model can withstand the pressures of a $300 billion valuation and commercial demand remains to be seen. But for now, OpenAI has chosen public accountability over private control — a move that may shape the future of AI governance for years to come.

Key Points: – AMETEK will acquire FARO Technologies for $920M, paying $44/share in cash—a 40% premium. – FARO brings $340M in annual sales and advanced 3D metrology tools to AMETEK’s precision portfolio. – The deal is expected to close in H2 2025, strengthening AMETEK’s presence in industrial and tech-driven sectors.

AMETEK, a global leader in electronic instruments and electromechanical devices, has announced it will acquire FARO Technologies in an all-cash deal valued at approximately $920 million. The acquisition is set to enhance AMETEK’s portfolio in precision measurement and 3D imaging, reinforcing its strategy of expanding into high-growth technology segments.

Under the terms of the agreement, AMETEK will pay $44 per share in cash for FARO, representing a roughly 40% premium to FARO’s previous closing price. The deal implies an equity value of $846 million and an enterprise value of $920 million. The acquisition is expected to close in the second half of 2025, pending customary closing conditions and regulatory approvals.

FARO Technologies, headquartered in Lake Mary, Florida, is a prominent provider of 3D measurement, imaging, and realization technology. Its suite of products includes portable measurement arms, laser scanners, and laser trackers used widely across manufacturing, engineering, construction, and public safety applications. The company reported approximately $340 million in sales for 2024, making it a valuable addition to AMETEK’s electronic instruments segment.

“This acquisition aligns well with our strategy of investing in differentiated technology businesses with strong market positions and attractive growth characteristics,” said David Zapico, Chairman and CEO of AMETEK. “FARO’s innovative 3D measurement and imaging solutions will strengthen our presence in precision metrology and expand our reach into new markets and applications.”

FARO’s technologies are used in sectors ranging from aerospace and automotive to architecture and law enforcement—markets that AMETEK sees as key growth areas. The deal reflects AMETEK’s broader aim to build out its capabilities in high-precision, high-performance technologies that deliver value across complex industrial environments.

While FARO shares jumped 36% in pre-market trading following the announcement, AMETEK shares remained flat, reflecting a neutral reaction from investors. However, analysts noted that the acquisition could offer long-term synergies, particularly as AMETEK integrates FARO’s product line and customer relationships into its existing operations.

AMETEK has a track record of strategic, bolt-on acquisitions that complement its core businesses. The company recently reported better-than-expected earnings for Q1 2025, driven by improved margins and resilient demand despite ongoing inflationary pressures and global trade uncertainties. CEO David Zapico noted that AMETEK’s strong U.S. manufacturing footprint positions it well to benefit from shifting supply chain dynamics and tariff-related opportunities.

“The current trade environment is creating strategic openings for manufacturers like AMETEK,” Zapico said last week. “This acquisition allows us to serve a broader range of customers looking for advanced measurement technologies built in America.”

FARO will operate under AMETEK’s Electronic Instruments Group, a division known for producing advanced monitoring, testing, and analytical equipment for industries that demand high accuracy and reliability.

The acquisition further solidifies AMETEK’s position as a leader in precision instrumentation, while giving FARO the resources and scale to accelerate innovation and expand its market reach. With both companies emphasizing long-term value and technical excellence, the deal appears well-aligned for success.

This is a correction of the announcement. The initial exercise date and term of the warrants purchased in the private placement have been corrected to one year following issuance and have a term of six years from the initial issuance date. All other aspects of the announcement remain the same.

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company developing targeted immunotherapies for cancer, today announced that it has entered into definitive agreements for the purchase and sale of an aggregate of 719,999 shares of common stock at a purchase price of $1.50 per share, in a private placement to accredited investors and certain Company directors. Each share of common stock is being offered together with a warrant to purchase one share of common stock at an exercise price of $2.05 per share, which price represents the greater of the book or market value of the stock on the date the definitive agreements were executed (subject to customary adjustments as set forth in the warrants). The warrants are exercisable commencing one year following issuance and have a term of six years from the initial issuance date. The securities being sold to the Company directors participating in the offering are being issued pursuant to the Company’s 2021 Equity Incentive Plan. The private placement is expected to close on or about May 7, 2025, subject to the satisfaction of customary closing conditions.

The gross proceeds from the offering are expected to be approximately $1.08 million, prior to offering expenses payable by the Company. The Company intends to use the net proceeds from the offering for to fund the starting cost for Part C of the Phase II trial THIO -101 and for working capital.

The securities described above are being offered in a private placement under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”), and/or Regulation D promulgated thereunder and, along with the shares of common stock underlying the warrants, have not been registered under the Securities Act, or applicable state securities laws. Accordingly, the warrants and underlying shares of common stock may not be offered or sold in the United States except pursuant to an effective registration statement or an applicable exemption from the registration requirements of the Securities Act and such applicable state securities laws.

This press release shall not constitute an offer to sell or a solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is ateganosine (THIO), a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

Strong Order Intake Supports Reaffirmed Full Year Guidance

CHICAGO, May 05, 2025 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL) (“FreightCar America” or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today reported results for the first quarter ended March 31, 2025.

FirstQuarter 2025Highlights

Revenues of $96.3 million, consistent with expectations, decreased 40.2% from $161.1 million in the first quarter of 2024, with planned railcar deliveries of 710 units compared to 1,223 units in the prior-year period

Gross margin of 14.9% with gross profit of $14.4 million, compared to gross margin of 7.1% with gross profit of $11.4 million in the first quarter of 2024

Net income of $50.4 million, or $1.52 per share and Adjusted net income of $1.6 million, or $0.05 per share, primarily reflecting a $52.9 million non-cash adjustment due to change in warrant liability

Adjusted EBITDA of $7.3 million, compared to Adjusted EBITDA of $6.1 million in the first quarter of 2024, up 20.5%

Generated Operating Cash Flow of $12.8 million, compared to $25.3 million of cash used in the first quarter of 2024, a $38.1 million increase year over year

Generated Adjusted Free Cash Flow of $12.5 million, compared to $30.5 million of cash used in the first quarter of 2024, a $43.0 million increase year over year

Ended the quarter with a backlog of 3,337 units valued at $318 million

“We continued to solidify our position as the fastest-growing railcar manufacturer in North America, driven by strong commercial execution and operational discipline. In line with our expectations for the first quarter, we achieved robust margins, once again outperforming our industry peers, reflecting our commitment to differentiated product offerings and exceptional commercial discipline. Order activity remained strong, with 1,250 railcars ordered during the quarter valued at approximately $141 million, underscoring our ongoing momentum and expanding market share,” commented Nick Randall, President and Chief Executive Officer of FreightCar America.

Randall continued, “Looking forward, our healthy backlog and growing inquiry pipeline position us for a meaningful ramp up in deliveries for the remainder of the year. While the industry has experienced some delays in order placements, we have continued to capture significant market share through our agility and superior responsiveness to customer needs. We reaffirm our previously announced full-year guidance and remain confident in our ability to deliver profitable growth and increased market share, further strengthening our long-term competitive position.”

FiscalYear2025 Outlook

The Company has reaffirmed outlook for fiscal year 2025 as follows:

Fiscal2025 Outlook

Year-over-Year GrowthatMidpoint

Railcar Deliveries

4,500 – 4,900 Railcars

7.7%

Revenue

$530 – $595 million

0.6%

AdjustedEBITDA1

$43 – $49 million

7.0%

1. The Company does not provide a reconciliation of forward-looking Adjusted EBITDA guidance due to the inherent difficulty in forecasting and quantifying adjustments necessary to calculate such non-GAAP measure without unreasonable effort. Material changes to such adjustments, including warrant liability and non-core operating items, could affect future GAAP results.

Mike Riordan, Chief Financial Officer of FreightCar America, added, “We remain in a strong financial position, generating consistent operating and free cash flow, marking our fourth consecutive quarter of positive operating cash flow, while ending the quarter with over $50 million in cash on hand. Our disciplined approach continues to drive margin strength and consistent cash generation, reinforcing our balance sheet and providing significant financial flexibility. We are firmly on track to achieve our full year guidance targets and remain committed to sustainable value creation through continued operational efficiency, commercial execution and delivering positive free cash flow for the year.”

FirstQuarter 2025 ConferenceCall&Webcast Information

The Company will host a conference call and live webcast on Tuesday, May 6, at 11:00 a.m. (Eastern Time) to discuss its first quarter 2025 financial results. FreightCar America invites shareholders and other interested parties to listen to its financial results conference call.

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Forward-LookingStatements

This press release contains statements relating to our expected financial performance, financial condition, and/or future business prospects, events and/or plans that are “forward-looking statements” as defined under the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent our estimates and assumptions only as of the date of this press release. Our actual results may differ materially from the results described in or anticipated by our forward-looking statements due to certain risks and uncertainties. These risks and uncertainties relate to, among other things, the cyclical nature of our business; adverse geopolitical, economic and market conditions, including inflation; material disruption in the movement of rail traffic for deliveries; fluctuating costs of raw materials, including steel and aluminum; delays in the delivery of raw materials; our ability to maintain relationships with our suppliers of railcar components; our reliance upon a small number of customers that represent a large percentage of our sales; the variable purchase patterns of our customers and the timing of completion; delivery and customer acceptance of orders; the highly competitive nature of our industry; the risk of lack of acceptance of our new railcar offerings; potential unexpected changes in laws, rules, and regulatory requirements, including tariffs and trade barriers (including recent United States tariffs imposed or threatened to be imposed on China, Canada, Mexico and other countries and any retaliatory actions taken by such countries); and other competitive factors. The factors listed above are not exhaustive. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them. We expressly disclaim any duty to provide updates to any forward-looking statements made in this press release, whether as a result of new information, future events or otherwise.

Non-GAAPFinancialMeasures

This press release includes measures not derived in accordance with generally accepted accounting principles (“GAAP”), such as EBITDA, Adjusted EBITDA, Adjusted net income (loss), Adjusted EPS, Free cash flow and Adjusted free cash flow. These non-GAAP measures should not be considered in isolation or as a substitute for any measure derived in accordance with GAAP and may also be inconsistent with similar measures presented by other companies. Reconciliations of these measures to the applicable most closely comparable GAAP measures, and reasons for the Company’s use of these measures, are presented in the attached pages.