Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Guided by AI. Total revenue for the Company grew 266% y-o-y, driven by higher realized bitcoin price and from the Company’s AI business. The Company recognized $8.1 million of revenue during the quarter and reported a gross margin of 61%. With the potential increase of the segment’s AI contract earlier in the year, we expect the performance of the segment to rival its mining revenue in the coming quarters.

Mining Side. Bit Digital’s bitcoin mining revenue was $21.9 million, a 168% increase from the previous year, as a higher hash rate coupled with the higher bitcoin price drove the revenue. As noted in our previous report, the active hash rate was 2.76 EH/s as of April 30, 2024. The Company has a total of 48,898 miners owned or operating for a total maximum hash rate of 4.2 EH/s. We believe the Company is well on its way towards its active hash goal of 6.0 EH/s.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The latest data from the Bureau of Labor Statistics provided a glimmer of hope in the battle against stubbornly high inflation. The Consumer Price Index (CPI) rose by 0.3% in April compared to the previous month, marking the slowest monthly increase in three months. On an annual basis, consumer prices climbed 3.4%, a slight deceleration from March’s 3.5% rise.

These figures indicate that inflationary pressures may be starting to abate, albeit gradually. The monthly increase came in lower than economists’ forecasts of a 0.4% uptick, while the annual rise matched expectations. After months of persistently elevated inflation, any signs of cooling are welcomed by consumers, businesses, and policymakers alike.

The slight easing of inflation was driven by a moderation in some key components of the CPI basket. Notably, the shelter index, which includes rents and owners’ equivalent rent, experienced a slowdown in its annual growth rate, rising 5.5% year-over-year compared to the previous month’s higher rate. However, shelter costs remained a significant contributor to the monthly increase in core prices, excluding volatile food and energy components.

Speaking of core inflation, it also showed signs of cooling, with prices rising 0.3% month-over-month and 3.6% annually, slightly lower than March’s figures. Both measures met economists’ expectations, providing further evidence that the overall inflationary trend may be moderating.

One area that continued to exert upward pressure on prices was energy costs. The energy index jumped 1.1% in April, matching March’s increase, with gasoline prices rising by 2.8% over the previous month. However, it’s worth noting that energy prices can be volatile and subject to fluctuations in global markets and geopolitical factors.

On the other hand, food prices remained relatively stable, with the food index increasing by 2.2% annually but remaining flat from March to April. Within this category, prices for food at home decreased by 0.2%, while prices for food away from home rose by 0.3%.

The April inflation report had a positive impact on financial markets, with investors anticipating a potential easing of monetary policy by the Federal Reserve later this year. The 10-year Treasury yield fell about 6 basis points, and markets began pricing in a roughly 53% chance of the Fed cutting rates at its September meeting, up from about 45% the previous month.

While the April data provided some respite from the relentless climb in consumer prices, it’s important to remember that inflation remains well above the Fed’s 2% target. The battle against inflation is far from over, and the central bank has reiterated its commitment to maintaining tight monetary policy until price stability is firmly established.

As markets and consumers digest the latest inflation report, all eyes will be on the Fed’s upcoming policy meetings and any potential shifts in their stance. A sustained cooling of inflationary pressures could pave the way for more accommodative monetary policy, but any resurgence in price growth could prompt further tightening measures.

In the meantime, businesses and households alike will continue to grapple with the effects of elevated inflation, adjusting their spending and investment decisions accordingly. The April data offers a glimmer of hope, but the road to price stability remains long and arduous.

Want small cap opportunities delivered straight to your inbox? Channelchek’s free newsletter will give you exclusive access to our expert research, news, and insights to help you make informed investment decisions.

Cash dividends of $0.15 per share consisting of a quarterly cash dividend of $0.025 per share for Q1 2024 and a special cash dividend of $0.125 per share

Total cash dividends of $1.60 per share, or $29.6 million, declared since March 2022

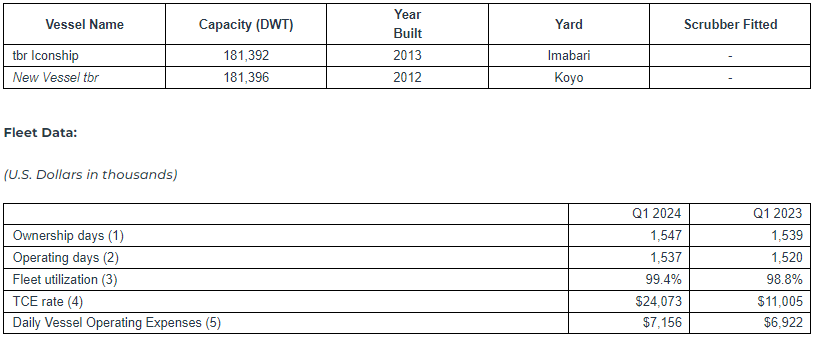

Acquisition of two Japanese Capesize vessels, built in 2013 and 2012, with estimated deliveries in Q2 and H2 2024, respectively

New financing and refinancing transactions of $58.3 million

ATHENS, Greece, May 15, 2024 (GLOBE NEWSWIRE) — Seanergy Maritime Holdings Corp. (“Seanergy” or the “Company”) (NASDAQ: SHIP), announced today its financial results for the first quarter ended March 31, 2024. The Company also declared a quarterly cash dividend of $0.025 per common share and a special cash dividend of $0.125 per common share for the first quarter of 2024.

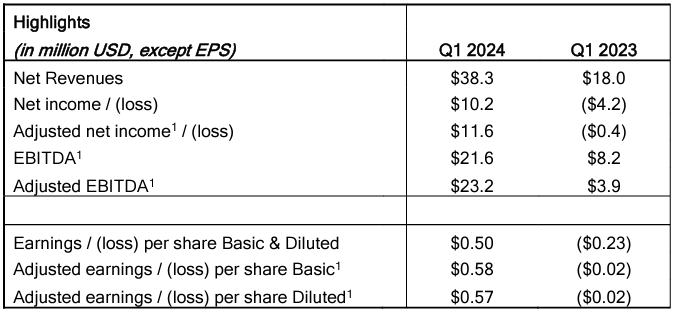

For the quarter ended March 31, 2024, the Company generated Net Revenues of $38.3 million, compared to $18.0 million in the first quarter of 2023. Net Income and Adjusted Net Income for the quarter were $10.2 million and $11.6 million, respectively, compared to Net Loss of $4.2 million and Adjusted Net Loss of $0.4 million in the first quarter of 2023. EBITDA and Adjusted EBITDA for the quarter were $21.6 million and $23.2 million, respectively, compared to $8.2 million and $3.9 million, respectively, for the same period of 2023. The daily Time Charter Equivalent (“TCE”2) of the fleet for the first quarter of 2024 was $24,073, compared to $11,005 in the same period of 2023.

Cash and cash-equivalents and restricted cash, as of March 31, 2024, stood at $24.2 million. Stockholders’ equity at the end of the first quarter was $240.6 million. Long-term debt (senior loans, finance lease liability and other financial liabilities) net of deferred charges stood at $223.2 million, while the book value of the fleet, including a chartered-in vessel and the advances for vessels acquisitions, was $442.0 million.

__________________________ 1 Adjusted earnings / (loss) per share, Adjusted Net Income / (loss), EBITDA and Adjusted EBITDA are non-GAAP measures. Please see the reconciliation below of Adjusted earnings / (loss) per share, Adjusted Net Income / (loss), EBITDA and Adjusted EBITDA to net income, the most directly comparable U.S. GAAP measure. 2 TCE rate is a non-GAAP measure. Please see the reconciliation below of TCE rate to net revenues from vessels, the most directly comparable U.S. GAAP measure.

Stamatis Tsantanis, the Company’s Chairman & Chief Executive Officer, stated:

“We are pleased to report that in the first quarter of 2024 we achieved record profits on the back of the continuing positive momentum in the Capesize market. This was mainly driven by higher iron ore exports, healthy coal volumes, as well as certain geopolitical events.

“Seanergy generated a net income of $10.2 million, compared to a net loss of $4.2 million in the same period of 2023, as our fleet performed in line with the market with a daily time charter equivalent of approximately $24,000.

“In light of our strong performance and consistent with our commitment to rewarding our shareholders, our Board authorized paying a quarterly and special cash dividend of $0.15 per share. With these dividends, we have declared total cash dividends of $1.60 per share, or $29.6 million, since March 2022. Given the strong Capesize outlook, we are optimistic that we are well-positioned to continue executing on our clear corporate strategy, which entails rewarding our shareholders generously while growing and renewing our fleet.

“With regard to our guidance for the second quarter of 2024, based on current FFA levels, we expect our daily TCE to be equal to approximately $26,400, likely outperforming the Capesize market thanks to our proactive hedging strategy. Looking beyond that, for the second half of the year we have converted about 33% of our ownership days to a fixed daily rate of approximately $30,000. We remain vigilant on market developments and are keen to secure attractive daily rates that offer high returns on capital.

“Moving on to fleet developments since our last quarterly update, in March we agreed to acquire an additional Capesize vessel built in 2012 in Japan for a price of $35.6 million that we expect to fund through a combination of cash on hand and debt. Delivery is expected to take place in the second half of 2024, while we continue to evaluate opportunities to add high-performing ships to our fleet. Furthermore, we recently obtained credit committee approval from one of our close lending partners for a new sale and leaseback agreement to finance the previously announced acquisition of the M/V Iconship along with the refinancing of an existing facility at a considerably lower interest margin.

“To conclude with a brief market update, contrary to regular seasonality, the first quarter of 2024 was the strongest of the past decade for Capesize earnings. Brazilian iron ore exports rose about 12% year on year and were the highest since 2019, while coal seaborne trade remained at very high levels. The limited vessel orderbook of the past years seems to be contributing to a gradually improving supply and demand balance, while the geopolitical uncertainty related to the Red Sea crisis has also been marginally constructive for Capesize earnings. On a forward-looking note, the current orderbook suggests fleet growth of about 2% per year for 2025 and 2026, which will likely be surpassed by vessel demand growth according to most industry sources. Longer term, the commitment of major miners to future growth projects as well as the limits on fleet growth brought about by stricter environmental regulations are expected to lead to strong market conditions.

“Seanergy has proven its ability to execute on its fleet growth plan and with its high-quality vessels, strong balance sheet and successful commercial strategy, is well positioned to continue creating shareholder value.”

Company Fleet:

(1) The Company has the option to convert the index-linked rate to fixed for periods ranging between 1 and 12 months, based on the prevailing Capesize FFA Rate for the selected period.

(2) The latest redelivery date does not include any additional optional periods.

(3) The vessel is operated by the Company on the basis of a 12-month bareboat charter-in contract with the owners of the vessel, including a purchase option at the end of the bareboat charter.

Vessels to be delivered:

(1) Ownership days are the total number of calendar days in a period during which the vessels in a fleet have been owned or chartered in. Ownership days are an indicator of the size of the Company’s fleet over a period and affect both the amount of revenues and the amount of expenses that the Company recorded during a period.

(2) Operating days are the number of available days in a period less the aggregate number of days that the vessels are off-hire due to unforeseen circumstances. Available days are the number of ownership days less the aggregate number of days that our vessels are off-hire due to major repairs, dry-dockings, lay-up or special or intermediate surveys. Operating days include the days that our vessels are in ballast voyages without having finalized agreements for their next employment. The Company’s calculation of operating days may not be comparable to that reported by other companies.

(3) Fleet utilization is determined by dividing operating days by ownership days for the relevant period. Fleet Utilization is used to measure a company’s ability to efficiently find suitable employment for its vessels and minimize the number of days that its vessels are off-hire for unforeseen events. We believe it provides additional meaningful information and assists management in making decisions regarding areas where we may be able to improve efficiency and increase revenue and because we believe that it provides useful information to investors regarding the efficiency of our operations.

(4) TCE rate is defined as the Company’s net revenue less voyage expenses during a period divided by the number of the Company’s operating days during the period. Voyage expenses include port charges, bunker (fuel oil and diesel oil) expenses, canal charges and other commissions. The Company includes the TCE rate, which is not a recognized measure under U.S. GAAP, as it believes it provides additional meaningful information in conjunction with net revenues from vessels, the most directly comparable U.S. GAAP measure, and because it assists the Company’s management in making decisions regarding the deployment and use of our vessels and because the Company believes that it provides useful information to investors regarding our financial performance. The Company’s calculation of TCE rate may not be comparable to that reported by other companies. The following table reconciles the Company’s net revenues from vessels to the TCE rate.

(In thousands of U.S. Dollars, except operating days and TCE rate)

(5) Vessel operating expenses include crew costs, provisions, deck and engine stores, lubricants, insurance, maintenance and repairs. Daily Vessel Operating Expenses are calculated by dividing vessel operating expenses, excluding pre delivery costs, by ownership days for the relevant time periods. The Company’s calculation of daily vessel operating expenses may not be comparable to that reported by other companies. The following table reconciles the Company’s vessel operating expenses to daily vessel operating expenses.

(In thousands of U.S. Dollars, except ownership days and Daily Vessel Operating Expenses)

Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”) represents the sum of net income / (loss), Interest and finance costs, net, depreciation and amortization and income taxes, if any, during a period. EBITDA is not a recognized measurement under U.S. GAAP. Adjusted EBITDA represents EBITDA adjusted to exclude stock-based compensation, loss on forward freight agreements, net, loss on extinguishment of debt, and the gain on sale of vessel, which the Company believes are not indicative of the ongoing performance of its core operations.

EBITDA and adjusted EBITDA are presented as we believe that these measures are useful to investors as a widely used means of evaluating operating profitability. Management also uses these non-GAAP financial measures in making financial, operating and planning decisions and in evaluating the Company’s performance. EBITDA and adjusted EBITDA as presented here may not be comparable to similarly titled measures presented by other companies. These non-GAAP measures should not be considered in isolation from, as a substitute for, or superior to, financial measures prepared in accordance with U.S. GAAP.

Adjusted Net income / (loss) Reconciliation and calculation of Adjusted Earnings / (loss) Per Share

(In thousands of U.S. Dollars, except for share and per share data)

To derive Adjusted Net Income / (loss) and Adjusted Earnings / (loss) Per Share, both non-GAAP financial measures, from Net Income / (loss), we exclude non-cash items, as provided in the table above. We believe that Adjusted Net Income / (loss) and Adjusted Earnings / (loss) Per Share assist our management and investors by increasing the comparability of our performance from period to period since each such measure eliminates the effects of such non-cash items as stock based compensation, loss on extinguishment of debt and other items which may vary from year to year, for reasons unrelated to overall operating performance. In addition, we believe that the presentation of the respective measure provides investors with supplemental data relating to our results of operations, and therefore, with a more complete understanding of factors affecting our business than with GAAP measures alone. Our method of computing Adjusted Net Income / (loss) and Adjusted Earnings / (loss) Per Share may not necessarily be comparable to other similarly titled captions of other companies due to differences in methods of calculation.

Second Quarter 2024 TCE Guidance:

As of the date hereof, approximately 79% of the Company fleet’s expected operating days in the second quarter of 2024 have been fixed at an estimated TCE of approximately $27,115. Assuming that for the remaining operating days of our index-linked T/Cs, the respective vessels’ TCE will be equal to the average Forward Freight Agreement (“FFA”) rate of $24,200 per day (based on the FFA curve of April 29, 2024), our estimated TCE for the second quarter of 2024 will be approximately $26,4083. The following table provides the break-down of index-linked charter and fixed-rate charters in the second quarter of 2024:

3 This guidance is based on certain assumptions and there can be no assurance that these TCE estimates, or projected utilization will be realized. TCE estimates include certain floating (index) to fixed rate conversions concluded in previous periods. For vessels on index-linked T/Cs, the TCE realized will vary with the underlying index, and for the purposes of this guidance, the TCE assumed for the remaining operating days of the quarter for an index-linked T/C is equal to the average FFA rate of $24,200 based on the curve of April 29, 2024. Spot estimates are provided using the load-to-discharge method of accounting. The rates quoted are for days currently contracted. Increased ballast days at the end of the quarter will reduce the additional revenues that can be booked based on the accounting cut-offs and therefore the resulting TCE will be reduced accordingly.

First Quarter and Recent Developments:

Distribution of Q4 2023 Dividend and Declaration of Q1 2024 Dividends

On April 10, 2024, the Company paid a quarterly dividend of $0.025 per share and a special dividend of $0.075 per share, for the fourth quarter of 2023, to all shareholders of record as of March 25, 2024.

Continuing its quarterly dividend payments, the Company has declared a quarterly cash dividend of $0.025 per common share for the first quarter of 2024 payable on or about July 10, 2024 to all shareholders of record as of June 25, 2024. In addition, the Company has declared a special dividend of $0.125 per common share to all shareholders of record as of June 25, 2024 which will be paid on or about July 10, 2024.

At-The-Market Offering Program

Since the filing of the Company’s annual report, the Company has issued and sold 267,585 common shares at an average price of $9.67 per share, resulting in gross proceeds of $2.6 million under the up to $30.0 million “at-the-market” equity offering program initiated in December 2023 with B. Riley as sales agent.

As of May 13, 2024, the Company had 20,779,660 common shares issued and outstanding.

Vessel Transactions and Commercial Updates

Vessel Acquisitions

On February 5, 2024, the Company agreed to acquire a 181,392 dwt Capesize bulk carrier, built in 2013 in Japan, which will be renamed M/V Iconship. The purchase price of $33.7 million is expected to be funded through cash on hand and the AVIC Sale & leaseback agreement. The M/V Iconship is expected to be delivered to the Company within June 2024.

On March 18, 2024, the Company agreed to acquire a 181,396 dwt Capesize bulk carrier, built in 2012 in Japan. The purchase price of $35.6 million is expected to be funded through a combination of cash on hand and debt financing. The vessel is expected to be delivered to the Company between July and October 2024.

M/V Knightship – Time charter extension

In May 2024, the charterer of the M/V Knightship exercised the second optional period extending the time charter which will commence in December 2024. The extension period is for a minimum of 11 months to a maximum of 13 months, while all other main terms of the time charter remain the same.

Financing Updates

AVIC Sale & leaseback agreement

The Company obtained credit committee approval from one of its close lending partners for three separate sale and leaseback agreements of $58.3 million in aggregate to refinance the sale and leaseback agreements with CMBFL, secured by the M/Vs Hellasship and Patriotship, and to partially finance the acquisition of the M/V Iconship. The vessels will be sold and chartered back on a bareboat basis for a five-year period commencing on each delivery date. The Company will have continuous options to repurchase the vessels at predetermined prices at any time of the bareboat charter. At the end of the bareboat period, Seanergy will have the obligation to purchase the vessels for an aggregate amount of approximately $31.5 million. Each financing will bear interest of 3-month term SOFR plus 2.55% per annum. The new interest rate will be approximately 120 bps lower than the rate of the refinanced sale and leaseback agreements. In aggregate for the three vessels, the charterhire principals will amortize over twenty consecutive quarterly installments, averaging approximately $1.3 million per quarter. The agreements are subject to the completion of definitive documentation.

Conference Call:

The Company’s management will host a conference call to discuss financial results on May 15, 2024 at 10:00 a.m. Eastern Time.

Audio Webcast:

There will be a live, and then archived, webcast of the conference call available through the Company’s website. To listen to the archived audio file, visit our website, following the Webcasts & Presentations section under our Investor Relations page. Participants to the live webcast should register on the Seanergy website approximately 10 minutes prior to the start of the webcast, following this link.

Conference Call Details:

Participants have the option to register for the call using the following link. You can use any number from the list or add your phone number and let the system call you right away.

Provided Positive, Updated Data from Phase 2 VERSATILE-002 Clinical Trial with Versamune® HPV in Combination with KEYTRUDA® in Recurrent or Metastatic Head and Neck Cancer

Expanded Global Intellectual Property Surrounding Versamune® Platform

PRINCETON, N.J., May 15, 2024 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB) (“PDS Biotech” or the “Company”), a late-stage immunotherapy company focused on transforming how the immune system targets and kills cancers and the development of infectious disease vaccines, today provided a business update and reported financial results for the first quarter of 2024. The press release will be available in the Investor Relations section of the Company’s website at www.pdsbiotech.com.

Recent Developments

Hosted a Key Opinion Leader event on May 8, 2024, during which prominent experts in head and neck squamous cell cancer (“HNSCC”) discussed positive, updated VERSATILE-002 data and the unmet need in HPV16-positive HNSCC. A replay of the event can be found here.

Announced updated results from the VERSATILE-002 Phase 2 trial evaluating first line treatment of patients with HPV16-positive recurrent or metastatic HNSCC using Versamune® HPV + KEYTRUDA® (pembrolizumab) (n=53).

Median overall survival is 30 months; Published results for immune checkpoint inhibitors are 7-18 months.

The cohort met its primary endpoint of best overall response (BOR).

BOR by investigator assessment is 34% (Combined Positive Score (CPS) ≥1; n=18/53); 48% (CPS≥20; n=10/21); Published results for ICIs are <20% (CPS>1) and <25% (CPS≥20).

CPS is used to assess PD-L1 expression

Progression free survival is 6.3 months (CPS≥1); 14.1 months (CPS≥20); Published results for immune checkpoint inhibitors 2-3 months.

VERSATILE-002 data to date indicate a durable response in first line recurrent or metastatic HNSCC patients with CPS≥1.

The combination of Versamune® HPV + pembrolizumab was well tolerated.

Announced an updated clinical strategy with a two-part registrational trial focused on the triple combination of Versamune® HPV + PDS01ADC + pembrolizumab as a first line treatment in HPV16-positive recurrent or metastatic HNSCC.

PDS01ADC is the Company’s novel, investigational tumor-targeting IL-12-fused antibody-drug conjugate (ADC), which has shown promise in a clinical trial of Versamune® HPV + PDS01ADC + an investigational ICI conducted by the National Cancer Institute.

Part one of the clinical trial will focus on dose optimization with a data readout based on safety and objective response rate.

The randomized second part of the trial will include an interim data readout with overall survival as its primary endpoint.

Further strengthened management with the addition of Stephan Toutain, M.S., MBA, as Chief Operating Officer. Mr. Toutain brings extensive operational and commercial experience to PDS Biotech.

Versamune® Platform Intellectual Property

Company received patents granted by the Israel Patent Office and IP Australia that will extend protections for the Company’s novel investigational T cell activating Versamune® platform through Dec. 2038 and Nov. 2036, respectively.

The Israel Patent Office granted patent No. 275154 titled, “Methods and compositions comprising cationic lipids for stimulating type I interferon genes,” extending protections for compositions using the Versamune® platform and comprising of cationic lipid for activating type I interferons. This patent covers all formulations and compositions that include Versamune to activate a T cell response.

IP Australia granted patent No. 2016354590 titled, “Lipids as synthetic vectors to enhance antigen processing and presentation ex-vivo in dendritic cell therapy.” This patent covers the use of Versamune® compositions that reduce the populations of immune suppressive cells in the tumor and its application for the development of dendritic cell-based approaches to immunotherapy.

First Quarter 2024 Financial Results Reported net loss was approximately $10.6 million, or $0.30 per basic share and diluted share, for the three months ended March 31, 2024, compared to a net loss of $9.7 million, or $0.32 per basic share and diluted share, for the three months ended March 31, 2023. The increase was due to higher operating and net interest expenses.

Research and development expenses increased to approximately $6.7 million for the three months ended March 31, 2024, from $5.8 million for the three months ended March 31, 2023. The increase of $0.9 million was primarily attributable to an increase of $1.2 million in clinical studies and medical affairs offset by a decrease of $0.1 million in personnel costs, $0.1 million in professional fees and $0.1 million in manufacturing expenses.

General and administrative expenses decreased to approximately $3.4 million for the three months ended March 31, 2024, from approximately $3.6 million for the three months ended March 31, 2023. The decrease of $0.2 million was primarily attributable to an increase of $0.3 million in professional fees offset by a decrease of $0.5 million in personnel costs.

Total operating expenses increased to approximately $10.1 million for the three months ended March 31, 2024 from $9.4 million for the three months ended March 31, 2023.

Net interest expenses increased to approximately $0.5 million for the three months ended March 31, 2024 from $0.2 million for the three months ended March 31, 2023.

Cash and cash equivalents as of March 31, 2024, totaled approximately $66.6 million.

About PDS Biotechnology PDS Biotechnology is a late-stage immunotherapy company focused on transforming how the immune system targets and kills cancers and the development of infectious disease vaccines. The Company plans to initiate a pivotal clinical trial in 2024 to advance its lead program in advanced head and neck squamous cell cancers (HNSCC). PDS Biotech’s lead program is a proprietary dual-acting combination of IL-12 fused antibody drug conjugate (ADC) PDS01ADC and T-cell activator Versamune® HPV in regimen with a standard-of-care immune checkpoint inhibitor. We believe that proof-of-concept long-term data have shown positive survival results and tumor shrinkage with this combination and indicate favorable tolerability.

We believe that with a novel investigational “inside-outside” mechanism, the PDS01ADC and Versamune® HPV immunotherapy has shown compelling results with potential to successfully disrupt a tumor’s inside defenses, while also generating potent, targeted killer T-cells to attack the tumor from the outside. We believe that data from more than 350 patients, as well as ongoing clinical trials across multiple tumor types and standard treatment regimens, have validated the potential for both platforms and point to potential broad utility.

Our Infectimune® based vaccines have demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T-cell responses, including long-lasting memory T-cell responses in pre-clinical studies to date. For more information, please visit www.pdsbiotech.com.

Forward Looking Statements This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS01ADC, PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS01ADC, PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; the Company’s ability to continue as a going concern; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the other risks, uncertainties, and other factors described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in the documents we file with the U.S. Securities and Exchange Commission. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® and Infectimune® are registered trademarks of PDS Biotechnology Corporation.

Keytruda® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

Second research site selected to enhance enrollment in the Phase 2a clinical trial for Cholesterol Efflux MediatorTM VAR 200 in patients with diabetic kidney disease planned to begin H1-2024.

GLP toxicology studies for Inflammasome ASC Inhibitor IC 100 scheduled to begin H1-2024, with planned Investigational New Drug (IND) submission Q4-2024, and Phase 1 clinical trial initiation Q1-2025.Atherosclerosis preclinical data readout for Inflammasome ASC Inhibitor IC 100 on schedule for H1-2024.

Initiation of preclinical study to assess Inflammasome ASC Inhibitor IC 100 for obesity-associated metabolic comorbidities scheduled to begin Q2-2024 with completion expected by year’s end.

Raised $2.7 million from exercising of investor warrants.

WESTON, Fla., May 15, 2024 (GLOBE NEWSWIRE) — ZyVersa Therapeutics, Inc. (Nasdaq: ZVSA, or “ZyVersa”), a clinical-stage specialty biopharmaceutical company developing first-in-class drugs for the treatment of renal and inflammatory diseases with high unmet medical needs, reports financial results for the quarter ended March 31, 2024 and provides business update.

“We are pleased to announce that ZyVersa is on track to achieve key development milestones over the next 3 quarters,” stated Stephen C. Glover, ZyVersa’s Co-founder, Chairman, CEO, and President. “Our Phase 2a clinical trial with Cholesterol Efflux MediatorTM VAR 200 in diabetic kidney disease is expected to enroll the first patient(s) within the next few months, with initial data read-out in the second half of the year. Inflammasome ASC Inhibitor IC 100’s indication expansion studies are nearing completion for atherosclerosis, expected to conclude in June, and obesity-associated metabolic comorbidities, expected to conclude by year’s end. IND preparation has been initiated for IC 100, with submission targeted for year’s end, and initiation of a phase 1 clinical trial in first quarter 2025. We believe achievement of these milestones is a key inflection point for ZyVersa and for shareholder value.”

BUSINESS Update

CHOLESTEROL EFFLUX MEDIATORTM VAR 200 FOR RENAL DISEASE

Phase 2a clinical trial in diabetic kidney disease is on target to begin H1-2024

CRO, George Clinical, was engaged in December 2023 to initiate and manage the trial.

A central Institutional Review Board (IRB) approved the clinical trial protocol for trial initiation.

Two clinical research sites have been selected, with contracting nearing completion.

Enrollment of first patient(s) is expected in the next few months.

INFLAMMASOME ASC INHIBITOR IC 100 FOR INFLAMMATORY DISEASES

Inflammasome ASC Inhibitor IC 100’s preclinical program nearing completion, with GLP toxicology studies expected to begin H1-2024. IND submission is planned for Q4-2024, followed by initiation of a Phase 1 clinical trial in Q1-2025.

Data from a scientific collaboration with an undisclosed partner to assess the potential of Inflammasome ASC Inhibitor IC 100 as a treatment for atherosclerosis in a well-established animal model is expected in June.

A scientific collaboration with inflammasome and neurology experts at University of Miami Miller School of Medicine to assess the potential of Inflammasome ASC Inhibitor IC 100 as a treatment for obesity-associated metabolic comorbidities is expected to begin in Q2-2024, with completion in Q4-2024.

In vitro preclinical research funded by The Michael J. Fox Foundation (MJFF) and conducted by researchers at University of Miami (UM) Miller School of Medicine supported Inflammasome ASC Inhibitor IC 100’s mechanism of action and potential to block damaging neuroinflammation that induces neural degeneration in Parkinson’s disease. At the suggestion of MJFF, UM researchers are developing a grant request to further the research in an established animal model.

FIRST QUARTER FINANCIAL RESULTS

Net losses were approximately $2.8 million for the three months ended March 31, 2024, with an improvement of $0.7 million or 20.2% compared to a net loss of approximately $3.5 million, for the three months ended March 31, 2023.

Based on its current operating plan, ZyVersa expects its cash of $2.0 million as of March 31, 2024 will be sufficient to fund its operating expenses and capital expenditure requirements on a month-to-month basis. ZyVersa will need additional financing to support its continuing operations and to meet its stated milestones. ZyVersa will seek to fund its operations and clinical activity through public or private equity or debt financings or other sources, which may include government grants, collaborations with third parties or outstanding warrant exercises. During Q1, ZyVersa raised approximately $2.7 million from investors exercising in-the-money warrants.

Research and development expenses were $0.5 million for the three months ended March 31, 2024, a decrease of $0.5 million or 51.4% from $1.1 million for the three months ended March 31, 2023. The decrease is attributable to lower manufacturing costs of IC 100 of $0.4 million and lower research and development payroll costs of $0.2 million due to fewer employees. This was offset by an increase in CRO fees of $0.1 million for VAR 200.

General and administrative expenses were $2.3 million for the three months ended March 31, 2024, a decrease of $1.2 million or 34.6% from $3.5 million for the three months ended March 31, 2023. The decrease is primarily attributable to a decrease of $0.4 million in payments for the Effectiveness Failure related to the PIPE shares, a decrease of $0.4 million for bonus accruals, a $0.2 million decrease in accounting fees and a $0.1 million decrease in director and officer insurance.

About ZyVersa Therapeutics, Inc.

ZyVersa (Nasdaq: ZVSA) is a clinical stage specialty biopharmaceutical company leveraging advanced, proprietary technologies to develop first-in-class drugs for patients with renal and inflammatory diseases who have significant unmet medical needs. The Company is currently advancing a therapeutic development pipeline with multiple programs built around its two proprietary technologies – Cholesterol Efflux Mediator™ VAR 200 for treatment of kidney diseases, and Inflammasome ASC Inhibitor IC 100, targeting damaging inflammation associated with numerous CNS and peripheral inflammatory diseases. For more information, please visit www.zyversa.com.

Certain statements contained in this press release regarding matters that are not historical facts, are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. These include statements regarding management’s intentions, plans, beliefs, expectations, or forecasts for the future, and, therefore, you are cautioned not to place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. ZyVersa Therapeutics, Inc. (“ZyVersa”) uses words such as “anticipates,” “believes,” “plans,” “expects,” “projects,” “future,” “intends,” “may,” “will,” “should,” “could,” “estimates,” “predicts,” “potential,” “continue,” “guidance,” and similar expressions to identify these forward-looking statements that are intended to be covered by the safe-harbor provisions. Such forward-looking statements are based on ZyVersa’s expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements due to a number of factors, including ZyVersa’s plans to develop and commercialize its product candidates, the timing of initiation of ZyVersa’s planned preclinical and clinical trials; the timing of the availability of data from ZyVersa’s preclinical and clinical trials; the timing of any planned investigational new drug application or new drug application; ZyVersa’s plans to research, develop, and commercialize its current and future product candidates; the clinical utility, potential benefits and market acceptance of ZyVersa’s product candidates; ZyVersa’s commercialization, marketing and manufacturing capabilities and strategy; ZyVersa’s ability to protect its intellectual property position; and ZyVersa’s estimates regarding future revenue, expenses, capital requirements and need for additional financing.

New factors emerge from time-to-time, and it is not possible for ZyVersa to predict all such factors, nor can ZyVersa assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements included in this press release are based on information available to ZyVersa as of the date of this press release. ZyVersa disclaims any obligation to update such forward-looking statements to reflect events or circumstances after the date of this press release, except as required by applicable law.

This press release does not constitute an offer to sell, or the solicitation of an offer to buy, any securities.

– OLC Demonstrates Bioequivalence to Lanthanum Carbonate –

– Additional Poster Highlights Key Features of OLC as Perceived by Renal Dieticians –

LOS ALTOS, Calif., May 15, 2024 (GLOBE NEWSWIRE) — Unicycive Therapeutics, Inc. (Nasdaq: UNCY), a clinical-stage biotechnology company developing therapies for patients with kidney disease (the “Company or “Unicycive”), today announced that two posters related to the Company’s lead product candidate, oxylanthanum carbonate (OLC), were presented at the National Kidney Foundation (NKF) Spring Clinical Meeting. OLC is a next-generation lanthanum-based phosphate binding agent utilizing proprietary nanoparticle technology being developed for the treatment of hyperphosphatemia in patients with chronic kidney disease (CKD).

“The NKF Spring Clinical Meeting was an important meeting for Unicycive as we were able to present data from the OLC bioequivalence study and our second poster was featured as a top-rated submission,” said Shalabh Gupta, MD, Chief Executive Officer of Unicycive. “Phosphate binders are integral to the management of hyperphosphatemia in patients with CKD and their effectiveness is adversely affected by non-adherence and limitations of phosphate binding capacity relative to dietary intake. Our data confirms that OLC is bioequivalent to lanthanum carbonate (LC) by showing similar outcomes in both groups with respect to mean change in urinary phosphate excretion. Importantly, OLC demonstrated a well-tolerated safety profile with no serious adverse events. This data is important as it serves as one of the key components for our New Drug Application filing with the FDA under the 505(b)(2) regulatory pathway.”

Dr. Gupta, concluded, “We are grateful to Dr. Hill Gallant who delivered a poster presentation on a survey of renal dieticians who play a critical role in helping patients manage serum phosphate and are close witnesses to patients’ experiences and challenges with phosphate management. The findings of the survey concluded that strategies that reduce pill burden and increase ease of use for patients are needed, reinforcing our belief that, if approved, the characteristics of OLC including the reduction of pill volume may increase compliance and improve the quality of life for patients living with this condition.”

Presentation Details:

Title: Two-Way Crossover Study to Establish Pharmacodynamic Bioequivalence Between Oxylanthanum Carbonate and Lanthanum Carbonate Lead Author: Vandana Mathur, MD Results: The poster presentation described the results of the randomized, crossover bioequivalence study comparing OLC with lanthanum carbonate (LC). The study was a Phase 1, single-center, randomized 1:1, open-label, controlled, 2-way crossover study designed to demonstrate the pharmacodynamic (PD) equivalence between two phosphate binders: orally administered OLC as compared to LC. Both treatments were administered at doses of one 1000 mcg tablet three-times-a-day (TID) in healthy volunteers who received the same standardized meals to control for daily phosphate intake. OLC tablets are swallowed whole as opposed to the LC tablets that must be chewed completely. The study consisted of a screening period, two dosing periods separated by a 14-day washout period, and a follow-up period 7 days after last study drug dose. The primary PD variable was Least Squares (LS) mean change in urinary phosphate excretion from baseline (48hrs prior to dosing) to Evaluation Period (Days 1-3). The baseline characteristics were balanced between OLC/LC and LC/OLC sequences. LS mean change from baseline for OLC (-320.4mg/day) was similar to the LS mean change from BL for LC (-324.0mg/day). The 90% confidence interval for the LS mean change in urinary phosphate excretion from baseline (test-reference) was (-37.83, 45.12), which was entirely contained within the predefined ±20% acceptance range of (-64.80, 64,80). There were no serious adverse events (SAEs) and no treatment discontinuations. The incidence of treatment-emergent adverse events (TEAEs) and related AEs were also the same in both groups at 35% and 25%, respectively.

Title:Renal Dietitians Perceive Phosphate Binder and Low-Phosphate Diet Non-Compliance as Top Reasons for Above Target Serum Phosphorous Concentrations Lead Author: Kathleen Hill Gallant, PhD, RD Results: The poster presentation delivers results of a recent dietitian survey evaluating perceived reasons for noncompliance to phosphate binder (PB) therapy and identifies the most appealing potential aspects of OLC. The poster concluded that strategies that reduce pill burden and increase ease of use for patients may promote PB treatment compliance, which may improve patient outcomes. OLC, which is a smaller tablet that can be swallowed whole without chewing, may address compliance issues seen with current PBs. In fact, 47% of dieticians noted the high perceived potency of OLC and 34% noted its perceived lower number of pills required as the most appealing aspects of OLC.

Recent studies reported PB non-adherence rates of up to 78% in patients with end-stage kidney disease on dialysis. For the analysis, 100 renal dietitians were surveyed and there were several key findings. The most common reasons for phosphate levels above the target range were non-compliance to PB prescription (36%) or low phosphate diet (34%). The two leading reasons for PB discontinuation were too many pills and formulation issues. One-third of dietitians attributed non-compliance with patients forgetting to take their PBs with meals or snacks and 16% attributed it to high pill burden.

About Oxylanthanum Carbonate (OLC)

Oxylanthanum carbonate is a next-generation lanthanum-based phosphate binding agent utilizing proprietary nanoparticle technology being developed for the treatment of hyperphosphatemia in patients with chronic kidney disease (CKD). OLC has over forty issued and granted patents globally. Its potential best-in-class profile may have meaningful patient adherence benefits over currently available treatment options as it requires a lower pill burden for patients in terms of number and size of pills per dose that are swallowed instead of chewed. Based on a survey conducted in 2022, Nephrologists stated that the greatest unmet need in the treatment of hyperphosphatemia with phosphate binders is a lower pill burden and better patient compliance.1 The global market opportunity for treating hyperphosphatemia is projected to be in excess of $2.5 billion in 2023, with the United States accounting for more than $1 billion of that total. Despite the availability of several FDA-cleared medications, 75 percent of U.S. dialysis patients fail to achieve the target phosphorus levels recommended by published medical guidelines.

Unicycive is seeking FDA approval of OLC via the 505(b)(2) regulatory pathway. As part of the clinical development program, two clinical studies were conducted in over 100 healthy volunteers. The first study was a dose-ranging Phase I study to determine safety and tolerability. The second study was a randomized, open-label, two-way crossover bioequivalence study to establish pharmacodynamic bioequivalence between OLC and Fosrenol. Based on the topline results of the bioequivalence study, pharmacodynamic (PD) bioequivalence of OLC to Fosrenol was established.

Fosrenol® is a registered trademark of Shire International Licensing BV. 1Reason Research, LLC 2022 survey. Results here.

About Hyperphosphatemia

Hyperphosphatemia is a serious medical condition that occurs in nearly all patients with End Stage Renal Disease (ESRD). If left untreated, hyperphosphatemia leads to secondary hyperparathyroidism (SHPT), which then results in renal osteodystrophy (a condition similar to osteoporosis and associated with significant bone disease, fractures and bone pain); cardiovascular disease with associated hardening of arteries and atherosclerosis (due to deposition of excess calcium-phosphorus complexes in soft tissue). Importantly, hyperphosphatemia is independently associated with increased mortality for patients with chronic kidney disease on dialysis. Based on available clinical data to date, over 80% of patients show signs of cardiovascular calcification by the time they become dependent on dialysis.

Dialysis patients are already at an increased risk for cardiovascular disease (because of underlying diseases such as diabetes and hypertension), and hyperphosphatemia further exacerbates this. Treatment of hyperphosphatemia is aimed at lowering serum phosphate levels via two means: (1) restricting dietary phosphorus intake; and (2) using, on a daily basis, and with each meal, oral phosphate binding drugs that facilitate fecal elimination of dietary phosphate rather than its absorption from the gastrointestinal tract into the bloodstream.

About Unicycive Therapeutics

Unicycive Therapeutics is a biotechnology company developing novel treatments for kidney diseases. Unicycive’s lead drug candidate, oxylanthanum carbonate (OLC), is a novel investigational phosphate binding agent being developed for the treatment of hyperphosphatemia in chronic kidney disease patients on dialysis. UNI-494 is a patent-protected new chemical entity in late preclinical development for the treatment of acute kidney injury. For more information, please visit Unicycive.com and follow us on LinkedIn and YouTube.

Forward-looking statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified using words such as “anticipate,” “believe,” “forecast,” “estimated” and “intend” or other similar terms or expressions that concern Unicycive’s expectations, strategy, plans or intentions. These forward-looking statements are based on Unicycive’s current expectations and actual results could differ materially. There are several factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, clinical trials involve a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials may not be predictive of future trial results; our clinical trials may be suspended or discontinued due to unexpected side effects or other safety risks that could preclude approval of our product candidates; risks related to business interruptions, which could seriously harm our financial condition and increase our costs and expenses; dependence on key personnel; substantial competition; uncertainties of patent protection and litigation; dependence upon third parties; and risks related to failure to obtain FDA clearances or approvals and noncompliance with FDA regulations. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including: the uncertainties related to market conditions and other factors described more fully in the section entitled ‘Risk Factors’ in Unicycive’s Annual Report on Form 10-K for the year ended December 31, 2023, and other periodic reports filed with the Securities and Exchange Commission. Any forward-looking statements contained in this press release speak only as of the date hereof, and Unicycive specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise.

Total revenue was €50.4 mm in Q1 2024, while net gaming revenue1 was €53.0 mm in the period, 34% above Q1 2023.

Mexico revenue was €23.8 mm in Q1 2024, while net gaming revenue was €26.6 mm in the period, 51% above Q1 2023.

Spain revenue (and net gaming revenue) reached €22.3 mm in Q1 2024, 21% above Q1 2023.

Net income was €3.4 mm in Q1 2024 versus a net loss of €1.3 mm in Q1 2023.

Total cash position of €38.5 mm as of March 31, 2024.

Increasing full year 2024 net gaming revenue outlook to €195-210 mm and reiterating plan to be Adj. EBITDA and cash flow positive for the full year in 2024.

Madrid, Spain and Tel Aviv, Israel, May 15, 2024 – (GLOBE NEWSWIRE) Codere Online (Nasdaq: CDRO / CDROW, the “Company”), a leading online gaming operator in Spain and Latin America, has released its preliminary unaudited2 financial results for the quarter ended March 31, 2024.

Below are the main financial and operating metrics of the period.

Quarter ended March 31

2023

2024

Chg. %

Net Gaming Revenue (EUR mm)1

Spain

18.4

22.3

21%

Mexico

17.6

26.6

51%

Other

3.5

4.1

17%

Total

39.5

53.0

34%

Avg. Monthly Active Players (000s)3

Spain

40.2

50.0

24%

Mexico

49.6

62.5

26%

Other

34.2

30.6

(11%)

Total

123.9

143.2

16%

Aviv Sher, CEO of Codere Online, commented on the results, “We are off to a strong start in 2024, with net gaming revenue of €53 million in the first quarter, 34% above that of last year and once again our highest ever quarterly figure. Our focus on Mexico and Spain continues to yield impressive results, with net gaming revenue in Mexico growing by 51% in the first quarter to nearly €27 million. In Spain, meanwhile, net gaming revenue grew by 21% to over €22 million. In both markets, our targeted marketing efforts allowed us to grow our active customer base by c. 25% as a result of the acquisition of higher quality customers (i.e. lower churn) but also with an increased spend per active.”

Oscar Iglesias, CFO of Codere Online, stated, “Once again, top line growth exceeded our expectations in the first quarter, with Mexico continuing to put distance on Spain as our largest market by revenue. We are particularly excited, however, to see Mexico now also contributing positive Adjusted EBITDA for the first time. This, together with a strong performance by Spain, allowed us to generate €1.7 million in total Adjusted EBITDA in the first quarter, which represents a significant step towards achieving our full year profitability targets.”

Mr. Iglesias further added, “On the back of this strong performance in the first quarter and based on recent trading activity, we now expect to generate between €195-210 million of net gaming revenue in 2024, and reaffirm that we expect to generate positive Adjusted EBITDA and cash flow for the full year in 2024.”

Recent Events

Launch in Mendoza

We have recently obtained final regulatory authorization and expect to launch operations soon in the Province of Mendoza.

Mendoza is the 5th most populated province in Argentina with over 2 million people.

This launch will further increase our presence in the country, where we started operations in the City of Buenos Aires in December 2021, and continue pursuing a license in the Province of Buenos Aires.

Rayados Renewal

On March 15, 2024, Codere Online agreed to extend its relationship with the Monterrey Rayados Football Club as its Official Betting Partner for the next four seasons.

With this renewal, Codere Online also became the Main Sponsor of the women’s team, Rayadas.

Codere Online expects to continue to deliver on its growth plan in Latin America, relying on this and other sponsorships and local activations.

Board Appointment

On April 9, 2024, the Board of Directors of Codere Online appointed Daniel Valdez as a member of the Board and the Audit Committee.

Mr. Valdez previously served as a member of the Board between the consummation of the business combination in November 2021 and August 2023.

Conference Call Information

Codere Online’s management will host a conference call to discuss the results and provide a business update at 8:30 am US Eastern Time today, May 15, 2024. Dial-in details as well as the audio webcast and presentation will be accessible on Codere Online’s website at www.codereonline.com. A recording of the webcast will also be available following the conference call.

Reconciliation of Revenue (IFRS) to Net Gaming Revenue (non-IFRS)

Quarter ended March 31

Figures in EUR mm

2023

2024

Chg. %

Total

Revenue

37.6

50.4

34%

(+) Accounting Adjustments4

1.9

2.6

37%

Net Gaming Revenue

39.5

53.0

34%

Spain

Revenue

18.4

22.3

21%

(+) Accounting Adjustments4

–

–

n.m.

Net Gaming Revenue

18.4

22.3

21%

Mexico

Revenue

15.8

23.8

51%

(+) Accounting Adjustments4

1.8

2.7

50%

Net Gaming Revenue

17.6

26.6

51%

Other

Revenue

3.4

4.3

26%

(+) Accounting Adjustments4

0.1

(0.2)

n.m.

Net Gaming Revenue

3.5

4.1

17%

About Codere Online Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile applications. Codere currently operates in its core markets of Spain, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence in Spain and throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence.

About Codere Group Codere Group is a multinational group devoted to entertainment and leisure. It is a leading player in the private gaming industry, with four decades of experience and with presence in seven countries in Europe (Spain and Italy) and Latin America (Argentina, Colombia, Mexico, Panama, and Uruguay).

Note on Rounding. Due to decimal rounding, numbers presented throughout this report may not add up precisely to the totals and subtotals provided, and percentages may not precisely reflect the absolute figures.

Forward-Looking Statements Certain statements in this document may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, statements regarding Codere Online Luxembourg, S.A. and its subsidiaries (collectively, “Codere Online”) or Codere Online’s or its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this document may include, for example, statements about Codere Online’s financial performance and, in particular, the potential evolution and distribution of its net gaming revenue; any prospective and illustrative financial information; and changes in Codere Online’s strategy, future operations and target addressable market, financial position, estimated revenues and losses, projected costs, prospects and plans.

These forward-looking statements are based on information available as of the date of this document and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing Codere Online’s or its management team’s views as of any subsequent date, and Codere Online does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, Codere Online’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. There may be additional risks that Codere Online does not presently know or that Codere Online currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Some factors that could cause actual results to differ include (i) changes in applicable laws or regulations, including online gaming, privacy, data use and data protection rules and regulations as well as consumers’ heightened expectations regarding proper safeguarding of their personal information, (ii) the impacts and ongoing uncertainties created by regulatory restrictions, changes in perceptions of the gaming industry, changes in policies and increased competition, and geopolitical events such as war, (iii) the ability to implement business plans, forecasts, and other expectations and identify and realize additional opportunities, (iv) the risk of downturns and the possibility of rapid change in the highly competitive industry in which Codere Online operates, (v) the risk that Codere Online and its current and future collaborators are unable to successfully develop and commercialize Codere Online’s services, or experience significant delays in doing so, (vi) the risk that Codere Online may never achieve or sustain profitability, (vii) the risk that Codere Online will need to raise additional capital to execute its business plan, which may not be available on acceptable terms or at all, (viii) the risk that Codere Online experiences difficulties in managing its growth and expanding operations, (ix) the risk that third-party providers, including the Codere Group, are not able to fully and timely meet their obligations, (x) the risk that the online gaming operations will not provide the expected benefits due to, among other things, the inability to obtain or maintain online gaming licenses in the anticipated time frame or at all, (xi) the risk that Codere Online is unable to secure or protect its intellectual property, and (xii) the possibility that Codere Online may be adversely affected by other political, economic, business, and/or competitive factors. Additional information concerning certain of these and other risk factors is contained in Codere Online’s filings with the U.S. Securities and Exchange Commission (the “SEC”). All subsequent written and oral forward-looking statements concerning Codere Online or other matters and attributable to Codere Online or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements above.

Financial Information and Non-GAAP Financial Measures Codere Online’s financial statements are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”), which can differ in certain significant respects from generally accepted accounting principles in the United States of America (“U.S. GAAP”).

This document includes certain financial measures not presented in accordance with U.S. GAAP or IFRS (“non-GAAP”), such as, without limitation, net gaming revenue and Adjusted EBITDA. These non-GAAP financial measures are not measures of financial performance in accordance with U.S. GAAP or IFRS and may exclude items that are significant in understanding and assessing Codere Online’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to revenue, net income, cash flows from operations or other measures of profitability, liquidity or performance under U.S. GAAP or IFRS. You should be aware that Codere Online’s presentation of these measures may not be comparable to similarly-titled measures used by other companies. In addition, the audit of Codere Online’s financial statements in accordance with PCAOB standards, may impact how Codere Online currently calculates its non-GAAP financial measures, and we cannot assure you that there would not be differences, and such differences could be material.

Codere Online believes that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends in comparing Codere Online’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. Reconciliations of non-GAAP financial measures to their most directly comparable measure under IFRS are included herein.

This document may include certain projections of non-GAAP financial measures. Codere Online is unable to quantify certain amounts that would be required to be included in the most directly comparable U.S. GAAP or IFRS financial measures without unreasonable effort, due to the inherent difficulty and variability of accurately forecasting the occurrence and financial impact of the various adjusting items necessary for such comparable measures or such reconciliation that have not yet occurred, are out of our control, or cannot be reasonably predicted, ascertained or assessed, which could have a material impact on its future IFRS financial results. Consequently, no disclosure of estimated comparable U.S. GAAP or IFRS measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included.

Use of Projections This document contains financial forecasts with respect to Codere Online’s business and projected financial results, including net gaming revenue and adjusted EBITDA. Codere Online’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this document, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this document. These projections should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. See “Forward-Looking Statements” above. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of Codere Online or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this document should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved.

For further information on the limitations and assumptions underlying these projections, please refer to Codere Online’s filings with the SEC.

Preliminary Information This document contains figures, financial metrics, statistics and other information that is preliminary and subject to change (the “Preliminary Information”). The Preliminary Information has not been audited, reviewed, or compiled by any independent registered public accounting firm. This Preliminary Information is subject to ongoing review including, where applicable, by Codere Online’s independent auditors. Accordingly, no independent registered public accounting firm has expressed an opinion or any other form of assurance with respect to the Preliminary Information. During the course of finalizing such Preliminary Information, adjustments to such Preliminary Information presented herein may be identified, which may be material. Codere Online undertakes no obligation to update or revise the Preliminary Information set forth in this document as a result of new information, future events or otherwise, except as otherwise required by law. The Preliminary Information may differ from actual results. Therefore, you should not place undue reliance upon this Preliminary Information. The Preliminary Information is not a comprehensive statement of financial results, and should not be viewed as a substitute for full financial statements prepared in accordance with IFRS. In addition, the Preliminary Information is not necessarily indicative of the results to be achieved in any future period.

No Offer or Solicitation This document does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor will there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities will be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933, as amended, or an exemption therefrom.

Industry and Market Data In this document, Codere Online relies on and refers to certain information and statistics obtained from publicly available information and third-party sources, which it believes to be reliable. Codere Online has not independently verified the accuracy or completeness of any such publicly-available and third-party information, does not make any representation as to the accuracy or completeness of such data and does not undertake any obligation to update such data after the date of this document. You are cautioned not to give undue weight to such industry and market data.

Contacts:

Investors and Media Guillermo Lancha Director, Investor Relations and Communications Guillermo.Lancha@codere.com (+34) 628 928 152

1 Net Gaming Revenue is a non-IFRS measure. Please see reconciliation of Net Gaming Revenue to Revenue at the end of the report. 2 See “Preliminary Information” below. 3 Average Monthly Active Players include real money (i.e. exclude free bets) sports betting and casino actives.

4 Figures primarily reflect differences in recognition of revenue related to certain partner and affiliate agreements in place in Colombia, VAT impact from entry fees in Mexico and the impact from the application of inflation accounting (IAS 29) in Argentina.

MALVERN, Pa., May 15, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that dosing is complete in the second cohort of its Phase 1/2 GARDian clinical trial for OCU410ST (AAV-hRORA)—a modifier gene therapy candidate being developed for Stargardt disease as a one-time treatment for life.

“The completion of dosing for Cohort 2 participants signifies an important clinical milestone for our pioneering modifier gene therapy,” said Huma Qamar, MD, MPH, Chief Medical Officer of Ocugen. “We are encouraged by the ongoing positive safety and tolerability profile demonstrated by OCU410ST, enabling us to consider higher doses in patients as we progress with the dose-escalation study. We look forward to sharing preliminary safety and efficacy data from Phase 1 of the clinical trial.”

Six patients with Stargardt disease have been dosed in the Phase 1/2 clinical trial to date. An additional three patients will be dosed with the high dose (Cohort 3) of OCU410ST in the dose-escalation phase.

“There remains a great unmet medical need for patients with Stargardt disease, which is the most common inherited retinal disease affecting the center of the vision and does not have any FDA-approved treatment options. OCU410ST is a novel modifier gene therapy that provides hope to these patients,” said Benjamin Bakall, MD, PhD, Director of Clinical Research at Associated Retina Consultants and Clinical Assistant Professor at University of Arizona, College of Medicine – Phoenix. “I am excited that we completed dosing of the last patient in Cohort 2, who received medium dose of this novel therapeutic leveraging a gene-agnostic approach, at Associated Retina Consultants (ARC) in Phoenix, AZ with the surgical team led by Dr. Mark Kwong, Medical Director of ARC.”

A Data and Safety Monitoring Board meeting will convene next month to review the 4-week safety data of the medium dose cohort before proceeding with Cohort 3 (high dose), which is the final dose in the Phase 1 dose-escalation study.

The GARDian clinical trial will assess the safety and efficacy of unilateral subretinal administration of OCU410ST in subjects with Stargardt disease and will be conducted in two phases. Phase 1 is a multicenter, open-label, dose-ranging study consisting of three dose levels [low dose (3.75×1010 vg/mL), medium dose (7.5×1010 vg/mL), and high dose (2.25×1011 vg/mL)]. Phase 2 is a randomized, outcome accessor-blinded, dose-expansion study in which adult and pediatric subjects will be randomized in a 1:1:1 ratio to either one of two OCU410ST dose groups or to an untreated group.

Ocugen is committed to finding solutions for people with inherited retinal disease for whom no effective treatment options exist. While an orphan disease, Stargardt affects approximately 100,000 people in the United States and Europe combined.

The Company expects to provide a clinical trial update for OCU410ST in the third quarter of 2024.

About Stargardt Disease Stargardt disease is a genetic eye disorder that causes retinal degeneration and vision loss. Stargardt disease is the most common form of inherited macular degeneration. The progressive vision loss associated with Stargardt disease is caused by the degeneration of photoreceptor cells in the central portion of the retina called the macula.

Decreased central vision due to loss of photoreceptors in the macula is the hallmark of Stargardt disease. Some peripheral vision is usually preserved. Stargardt disease typically develops during childhood or adolescence, but the age of onset and rate of progression can vary. The retinal pigment epithelium (RPE), a layer of cells supporting photoreceptors, is also affected in people with Stargardt disease.