The Majority of Fed Policymakers are Still Concerned About Inflation

The minutes of the July 25-26 FOMC meeting were released and showed ongoing concerns about U.S. inflation are still front and center on the minds of most policymakers. During the July meeting, Federal Reserve officials were still focused on rising prices expressing that more rate hikes could be necessary unless conditions change. The July meeting had resulted in a quarter percentage point rate hike; the minutes are being looked at by market participants to get a sense of the Fed’s next steps.

While the Fed says it is data dependent, so a surprisingly weak economic report or lower-than-expected inflation statistics could change the Fed’s hawkish stance at the next meeting, if economic conditions remain unchanged or get stronger, the Fed is likely to keep applying the economic brakes by raising rates.

“With inflation still well above the Committee’s longer-run goal and the labor market remaining tight, most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy,” the meeting summary stated.

The increase in the Fed Funds rate after the last meeting brought the key interest rate to its highest level in 22 years, 5.25%-5%.

The Fed has held for more than 18 months that they are targeting a 2% inflation rate. During that time, key inflation indicators have been as high as 9%. Depending on the measure used, inflation at the last read was between 3% and 4%.

“In discussing the policy outlook, participants continued to judge that it was critical that the stance of monetary policy be sufficiently restrictive to return inflation to the Committee’s 2% objective over time,” according to the Fed’s recent release.

The Fed always risks overdoing it during a tightening policy period. So, while members agreed inflation is “unacceptably high,” there were indications “that a number of tentative signs that inflation pressures could be abating.”

As written in the release, “Almost all” the meeting participants, which includes nonvoting members, were in favor of the July rate increase. However, a couple of members opposed and suggested the Committee could skip a hike to monitor how previous hikes play out in inflation indicators. Navigating economic activity and price levels is not a precise science, and there is a lag between actions and impact.

“Participants generally noted a high degree of uncertainty regarding the cumulative effects on the economy of past monetary policy tightening,” the minutes said.

The minutes did indicate that the economy was expected to slow and unemployment likely will rise somewhat. Of note is a retraction in an earlier forecast that troubles in the banking industry could lead to a mild recession this year. A number of smaller banks found themselves challenged and even requiring government assistance in March.

The minutes indicated that the policymakers are also watching the health of the commercial real estate (CRE) market as they raise rates. Specifically cited were “risks associated with a potential sharp decline in CRE valuations that could adversely affect some banks and other financial institutions, such as insurance companies, that are heavily exposed to CRE. Several participants noted the susceptibility of some nonbank financial institutions” such as money market funds and the like.

Looking Forward

Federal Open Market Committee members emphasized the two-sided risks of easing too quickly and risking higher inflation against tightening too much and sending the economy into contraction. The most current data shows that while inflation is still 50% or more from the central bank’s 2% target, it has made marked progress since peaking above 9% in June 2022. Examples are the Consumer Price Index (CPI), ran at a 3.2% annual rate through July. The Personal Consumption Expenditures (PCE) price index core was at 4.6%.

In their consideration of appropriate monetary policy actions at this meeting, participants concurred that economic activity had been expanding at a moderate pace. The labor market remained very tight, with robust job gains in recent months and the unemployment rate still low, but there were continuing signs that supply and demand in the labor market were coming into better balance. Participants also noted that tighter credit conditions facing households and businesses were a source of headwinds for the economy and would likely weigh on economic activity, hiring, and inflation. However, the extent of these effects remained uncertain. Although inflation had moderated since the middle of last year, it remained well above the Committee’s longer-run goal of 2%, and participants remained resolute in their commitment to bring inflation down to the Committee’s 2% objective.

Take Away

While the Fed will react to incoming data when they decide at the September 19-20 FOMC meeting, the minutes from the July meeting suggest that if there is little change in economic activity, the majority of members are apt to vote to hike rates once more.

Image: US Treasury Secretary Janet Yellen in Las Vegas, Nevada, US, on Monday, Aug. 14, 2023.

China’s Economic slowdown is a “Risk Factor” for US, Says Treasury Secretary Yellen

A month after returning from her visit to China, U.S. Secretary of the Treasury Janet Yellen opened up about the interplay between the two countries’ economies, the risks the Chinese slowdown has on the U.S., and a side trip she took courtesy of ingesting magic mushrooms. Addressing growing concerns over the economic downturn in the world’s second-largest economy, and possible spillover effects to the U.S., the Treasurer was optimistic about her country’s path.

China and U.S.

Amidst the growing concerns surrounding China’s economic prospects, including a 5% devaluation of the yuan, and across-the-board weakening economic indicators, China now has the worst-performing currency in Asia after the yen.

Treasury Secretary Yellen, speaking in Las Vegas, seemed to be undoing some of the recent strong talk from U.S. President Biden at a fundraiser on August 11. Biden referred to China’s economic issues as a “ticking time bomb” and referred to Communist Party leaders as “bad folks.” The U.S. President expressed concerns about China’s slowed growth and elevated unemployment rate. She was speaking at a press conference following a speech in Las Vegas. Yellen referred to China’s economic woes as a “risk factor” for the US, a risk that she believes won’t significantly undermine the overall prospects of the American economy.

As Yellen touted the economic policy achievements of the Biden administration, she highlighted the resilient state of the US economy.

Risks to U.S.

In classic economist style, Yellen hedged her “low risk” comments by suggesting there is a possibility that while China’s slowdown will primarily impact its neighboring Asian nations, there will inevitably be some repercussions for the United States.

Yellen strongly emphasized uncertainty, “That said, I feel very good about US prospects overall. Let’s call that a risk, she said, signalling her measured optimism amidst the uncertainties linked to China’s economic trajectory. Yellen underscored the unexpectedly robust state of the U.S. labor market despite the Federal Reserve’s aggressive rate-hiking campaign – one of the most vigorous tightening efforts in decades.

Janet Yellen spoke on CNN about her meal in China

Psychedelic Side Trip?

While in Beijing, Yellen made a bit of a stir both in China and in her home country for having been seen easting a psychedelic mushroom-based dish called Jian shou qing, or “see hand blue”, a fungi dish known for being hallucinogenic.

Yellen spoke about her experiences on CNN. She recognized the humor of the episode but said that the cooked food had no side effects.

Take Away

The U.S. economy is likely to be impacted by trade with the world’s second-largest economy. According to the U.S. Treasury Secretary, weakness in China will be somewhat contagious. She remains cautious but optimistic that the robust state of growth and employment in the U.S will serve to minimize negative effects.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 results. The company reported Q2 revenue of $9.9 million and adj. EBITDA of a loss of $4.7 million, both of which were below our forecast. We anticipated $22.5 million in revenue and positive adj. EBITDA of $4.0 million. In our view, the miss was largely a result of the timing of the company’s releases.

Looking ahead to Q4. Despite the negative adj. EBITDA in the quarter, the company remains on track to release ARK: Survival Ascended in October of this year. Survival Ascended is a re-release of the company’s flagship game with several updates, powered by Unreal Engine 5. The company is also slated to re-release all 5 ARK DLCs using Unreal Engine 5, subsequent to the release of ARK: Survival Ascended.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

PDS Reports 2Q23. PDS reported a 2Q23 loss of $11.5 million or $(0.37) per share and ended the quarter with $60.6 million in cash. Importantly, PDS completed the filing of its final clinical trial design required for the Phase 3 VERSATILE-003 trial testing PDS0101 in head and neck cancer, a milestone that should allow the start of the trial before YE2023.

The Phase 3 VERSATILE-003 Trial On Track To Start In 2023. PDS completed the FDA filing for the final protocols for the Phase 3 VERSATILE-003 trial, meeting the expected milestone. This filing includes the study design and manufacturing data (CMC section) that should allow the trial to begin before year-end. The trial will test the combination of PDS0101 with Keytruda (pembrolizumab, from Merck) against Keytruda alone in patients with HPV16+ head and neck cancer.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Awards. Friday and then on Monday, Great Lakes was awarded two new contracts worth a combined $49.2 million, according to the Department of Defense daily contract award notification. Combined with two end of July awards worth $36.7 million, Great Lakes has received some $86 million of new business in the last couple of weeks. We remain optimistic the awards pace will speed up, at least through the Federal government’s fiscal 2023 year-end.

Award 1. Great Lakes was awarded a $22.1 million firm-fixed-price contract for dredging in the Mississippi River. Work will be performed in Plaquemines, Louisiana, with an estimated completion date of December 17, 2023. Fiscal 2023 civil operation and maintenance funds in the amount of $22.1 million were obligated at the time of the award. U.S. Army Corps of Engineers, New Orleans, Louisiana, is the contracting activity.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Trials Expected To Begin In 2H23. Cocrystal reported a 2Q23 loss of $4.2 million or $(0.41) per share, ending the quarter with about $32.4 million in cash. During the quarter, the company selected its protease inhibitor CDI-988 for testing against norovirus. A clinical trial was previously planned to test CD1-988 against SARS-CoV-19, the virus that causes COVID-19. The company has received clearance to begin clinical testing for both indications in Australia. The Phase 2a clinical trial in influenza A is also expected to begin in 2H23.

CDI-988 Moves To Clinical Trials. CDI-988 is a novel 3CL protease inhibitor that targets an enzyme needed in the early steps of viral reproduction. It has been in development against SARS-CoV-2, the virus that causes COVID-19. Earlier this month, CDI-988 was also selected as the lead molecule to be tested against norovirus. A Phase 1 trial has been designed to test safety, tolerability, and pharmacokinetics in both indications. The trial will be conducted in Australia, where clinical testing was approved in May 2023. First data from the trial is expected in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q23. Revenue was $737,398, down from $1.4 million a year ago. Average monthly revenue per subscriber declined to $64.27 from $75.21 due to a higher level of promotional members during 2Q23. Blackboxstocks reported a net loss of $1.4 million for the quarter, or a loss of $0.45 per share, compared to a net loss of $1.3 million, or a loss of $0.40 per share in 2Q22. Adjusted EBITDA was a loss of $1.0 million, similar to the adjusted EBITDA loss in the year ago quarter.

Subscriber Counts. The average member count for the second quarter of 2023 was 3,937 compared to 5,482 for the second quarter of 2022 and 3,555 for the first quarter of 2023. The sequential stabilization of the member count reflects lower churn, while changes to marketing are expected to have a positive impact on the growth trajectory going forward.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

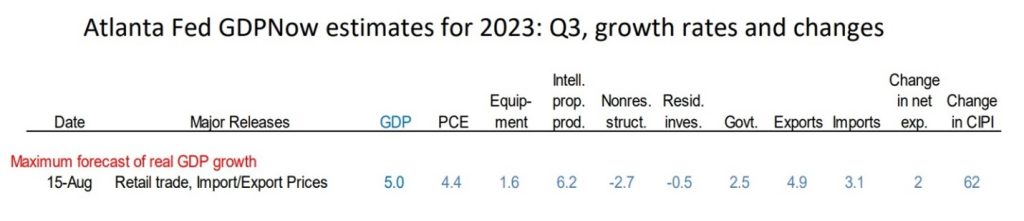

GDPNow from the Atlanta Federal Reserve Has a Surprising Forecast

If good news is bad, The Atlanta Federal Reserve’s GDPNow report is horrible – that’s how good it is. GDPNow is a model for estimating Gross Domestic Product (GDP). Created and published by the Federal Reserve Bank of Atlanta, it has been fairly accurate in recent years. An estimate of third-quarter US GDP released on August 15th forecasts that growth is increasing dramatically – inflation is also shown to inch up in the forecast.

The Indicator

GDPNow uses recently published economic data to update a model to estimate GDP, a statistic that is reported with a significant lag to the input data.The output, or forecast, is an aggregation of other current economic indicators within the quarter. The data is entered into the mathematical model to calculate a GDP estimate at that specific point in time. There are still 45 days left in the third quarter, but up until now, this is what it calculated the growth to have been. As time passes and more reports are issued, more economic indicators are fed into the model. These reports come from the US Bureau of Labor Statistics, the US Census Bureau, the Institute for Supply Management, and the US Department of the Treasury. The accumulated data contributes to the historical accuracy of GDPNow’s calculations in relation to the GDP reports that the US Bureau of Economic Analysis (BEA) releases.

The Current Forecast

The GDPNow model’s latest estimates show the real GDP growth (seasonally adjusted annual rate) in the third quarter of 2023 is 5.0 percent on August 15, up from 4.1 percent where the estimate stood on August 8. Included in the model are recent releases from the US Census Bureau, the US Bureau of Labor Statistics, and the US Department of the Treasury’s Bureau of the Fiscal Service.

The model also provides other forecasts, from statistics, that will present themselves during the quarter and be finalized after the quarter ends. This includes third-quarter real Personal Consumption Expenditures (PCE). Remember that PCE is the Federal Reserve’s favored inflation gauge. The PCE inflation forecast, by this model, has been near accurate. It’s latest forecast is for it to rise to 4.4% annualized.

Take Away

There are a lot of mixed signals in the market recently, savings is down, consumer borrowing is up, interest rates out on the yield curve have finally moved up, and there are some fund managers that are extremely bearish, while bullishness is on the rise on the prospect of a soft or undetectable economic landing in the US.

The GDPNow snapshot of where a mathematical model shows where we may be now has no human intervention. It is created by a model without the kinds of bias that could cause a human to overweigh one factor over another. The most recent report shows tremendous growth and an uptick in inflation. In today’s financial marketplace, where the markets still sell-off on good economic news and rally on bad, it’s uncertain what this means for the markets. But it is important for investors to understand that others view this and weigh it in their own expectations.

Ark Invest Warns of a Deflationary Ripple that Could Spread Around the Globe

Pricing, whether it be of the stock market, private placements, or other alternative investments is impacted by investor demand, and demand is the result of differing views. Cathie Wood, the Ark Investment Management CEO, has held the view that the U.S. and global economies are close to a deflationary spiral. She pointed to more evidence this week, and sounded the alarm for the potential dire consequences of the Federal Reserve’s ongoing rate tightening measures. According to Wood, deflation tied to China and actions by the U.S. central bank could set off a chain reaction of deflation-induced economic slowdowns, not just within the United States but across international markets.

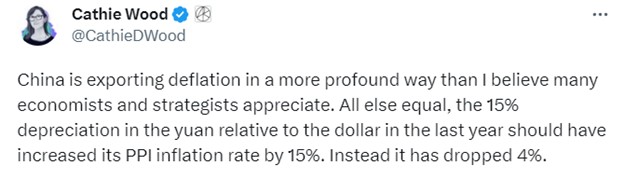

Ms. Wood, the 67-year-old market veteran, who falls in the category of celebrity investor, has many fans and followers. She shared her concerns in a string of posts on X, the platform formerly known as Twitter. Wood stated, “China is exporting deflation in a more profound way than I believe many economists and strategists appreciate.”

She explained that producer prices in China, the world’s second largest economy, were impacted by the U.S. dollar strengthening by 15% against the Chinese yuan, despite the devaluation adding around 15% to Chinese PPI, the Chinese reported a decline in the PPI inflation measure by 4%.

Wood expressed China is exporting deflation. She posted that, under normal circumstances, the 15% depreciation of the yuan against the dollar in 2022 should have led to a 15% increase in China’s annual producer inflation rate. Since it instead dropped 4%, In her math, this is creating near a 20% downdraft on prices of Chinese goods.

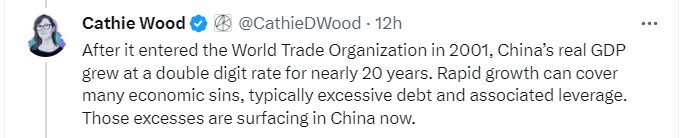

Turning her focus to China’s economic trajectory, Wood recounted the country’s impressive growth following its entry into the World Trade Organization in 2001. Over nearly two decades, China’s real GDP experienced a sustained double-digit expansion. However, Wood pointed out that rapid growth often conceals underlying economic vulnerabilities, including excessive debt and leverage. Her firm believes these vulnerabilities are now creating cracks in China’s economy.

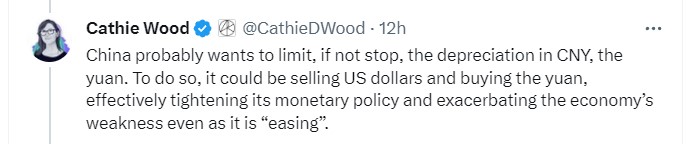

Wood suggested that China might attempt to halt the depreciation of the yuan. However, this would necessitate selling off U.S. dollars and acquiring yuan, which, in turn, tightens monetary policy and fuels the economy’s fragility, even amid efforts to stimulate it.

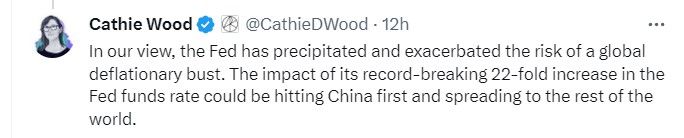

Ark Invest’s CEO posted, “The Fed has precipitated and exacerbated the risk of a global deflationary bust.” Drawing attention to the central bank’s remarkable 22-fold increase in the Fed funds rate, Wood warned that the repercussions of this move would first impact China and subsequently ripple through the rest of the world.

Recent economic data from China underscores the challenges it currently faces. Second-quarter GDP growth came in at 6.3%, falling short of the 7.3% projection by economists. Furthermore, new bank loans for July plummeted by 89% month-over-month, marking the lowest level since 2009, according to data from the People’s Bank of China.

The deflationary trend is evident in inflation figures as well. July inflation data showed both consumer and producer price inflation rates in negative territory.

Adding to the concerns, a trio of data released from the China National Bureau of Statistics revealed lackluster performance. Retail sales rose by a modest 2.5% year-over-year in July, well below the anticipated 4.5% increase. Industrial Production also lagged, with a 3.7% rise compared to the consensus estimate of 4.4%. Moreover, fixed asset investment figures raised further questions about the country’s economic health.

Take Away

There are certainly competing inflation forecasts opposing those coming out of Cathie Wood’s firm. However, her warnings do serve as a reminder, from a veteran in the asset management business, of the interconnectedness of global economies and the potential ramifications of central bank policy decisions. As markets continue to navigate the crosscurrents, attention remains on policymakers and economic indicators for signs of any change in trends.

On track to begin a Phase 2a trial in the second half of 2023with CC-42344 for the treatment ofpandemic and seasonal influenza A

Selected the novel protease inhibitor CDI-988 as development lead inthe oral norovirus program

CDI-988, the first potential dual coronavirus-norovirus oral antiviral, was cleared by the Australian regulatory agency for evaluation in healthy volunteers

BOTHELL, Wash., Aug. 14, 2023 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) (Cocrystal or the Company) reports financial results for the three and six months ended June 30, 2023, and provides updates on its antiviral pipeline, upcoming milestones and business activities.

“This is an eventful time for Cocrystal with notable advancements in developing our pipeline of highly promising antivirals,” said Sam Lee, Ph.D., President and co-CEO of Cocrystal. “With our novel oral PB2 inhibitor CC-42344 for the treatment of pandemic and seasonal influenza A, we are building on the favorable data from our Phase 1 trial with the submission of an application for UK MHRA (Medicine and Healthcare Products Regulatory Agency) approval to begin a Phase 2a human challenge trial later this year.

“In our COVID-19 program, we received approval from the Australian regulatory agency in late May to begin a first-in-human trial with our novel, broad-spectrum oral protease inhibitor CDI-988. Earlier this month we announced the selection of CDI-988 as our lead oral norovirus candidate. This Phase I study is designed to access the safety, tolerability, and pharmacokinetics of CDI-988 for both our COVID-19 and our norovirus programs. We expect to report top-line data of CDI-988 Phase 1 study in 2024.”

“We have a number of significant near-term inflection points with our three leading antiviral programs including the commencement of multiple clinical trials,” said James Martin, CFO and co-CEO. “I’m pleased to report that under our cost-efficient business model, we believe our current cash position is sufficient to fund our planned operations for the next 12 months.”

Antiviral Product Pipeline Overview

We are developing therapeutics that inhibit the viral replication function of RNA viruses that cause acute and chronic diseases. Our drug discovery process focuses on the highly conserved regions of the viral enzymes and inhibitor-enzyme interactions at the atomic level. It differs from traditional, empirical medicinal chemistry approaches that often require iterative high-throughput compound screening and lengthy hit-to-lead processes. By designing and selecting antiviral drug candidates that interrupt the viral replication process and have specific binding characteristics, we seek to develop drugs that are effective against both the virus and mutants of the virus, and also have reduced off-target interactions that may cause undesirable clinical side effects.

Influenza Programs

Influenza is a severe respiratory illness caused by the influenza A or B virus that results in disease outbreaks mainly during the winter months. The global seasonal influenza market including diagnostics, treatments and vaccines is projected to reach up to $27.95 billion by 2029, according to Data Bridge Market Research.

Pandemic and Seasonal Influenza A

Our novel oral PB2 inhibitor CC-42344 has shown excellent antiviral activity against influenza A strains including pandemic and seasonal strains, as well as strains that are resistant to Tamiflu® and Xofluza®.

In March 2022 we initiated enrollment in a randomized, double-controlled, dose-escalating Phase 1 trial to evaluate the safety, tolerability and pharmacokinetics (PK) of orally administered CC-42344 in healthy adults.

In April 2022 we announced preliminary Phase 1 trial data demonstrating a favorable safety and PK profile in the first two cohorts in the single-ascending-dose portion of the study.

In July 2022 we reported PK results from the single-ascending-dose portion of the study that support once-daily dosing.

In December 2022 we reported favorable safety and tolerability results from the CC-42344 Phase 1 trial.

We entered into an agreement with a UK-based clinical research organization to conduct a Phase 2a human challenge study to evaluate safety, and viral and clinical measures of orally administered CC-42344 in influenza A-infected subjects.

We submitted an application to the United Kingdom Medicines and Healthcare Products Regulatory Agency to conduct the Phase 2a human challenge study and, pending clearance, we expect to initiate the study in the second half of 2023.

Preclinical development is underway with an inhaled formulation of CC-42344 as a potential treatment and prophylaxis for influenza A. We expect to complete active pharmaceutical ingredient (API) manufacturing in preparation for toxicity studies, and to begin the Phase 1 clinical trial in the first half of 2024.

Pandemic and Seasonal Influenza A/B Program

In January 2019 we entered into an Exclusive License and Research Collaboration Agreement with Merck Sharp & Dohme Corp. (Merck) to discover and develop certain proprietary influenza antiviral agents that are effective against both influenza A and B strains. This agreement includes milestone payments of up to $156 million plus royalties on sales of products discovered under the agreement.

In January 2021 we announced completion of all research obligations under the agreement, making Merck solely responsible for further preclinical and clinical development of these compounds.

In early 2023 Merck notified us of its intent to continue development of the proprietary compounds discovered under this agreement and of their filing on behalf of both companies of multiple U.S. and international patent applications associated with these compounds. Merck continues to be responsible for managing the patents.

COVID-19 and Other Coronavirus Programs

By targeting viral replication enzymes and protease, we believe it is possible to develop effective treatments for all diseases caused by coronaviruses including COVID-19, Severe Acute Respiratory Syndrome (SARS) and Middle East Respiratory Syndrome (MERS). Our main SARS-CoV-2 protease inhibitors showed potent in vitro pan-viral activity against common human coronaviruses, rhinoviruses and respiratory enteroviruses that cause the common cold, as well as against noroviruses that can cause symptoms of acute gastroenteritis.

Oral Protease Inhibitor CDI-988

In August 2023 we announced the selection of CDI-988 as our lead candidate for development as a potential oral treatment for SARS-CoV-2. Designed and developed using our proprietary structure-based drug discovery platform technology, CDI-988 targets a highly conserved region in the active site of SARS-CoV-2 3CL (main) protease required for viral RNA replication.

CDI-988 exhibited superior in vitro potency against SARS-CoV-2 with activity maintained against variants of concern, and demonstrated a safety profile and PK properties that are supportive of once-daily dosing.

In May 2023 we announced approval of our application to the Australian regulatory agency for a planned randomized, double-blind, placebo-controlled Phase 1 trial in healthy volunteers.

We believe the FDA’s guidance for further development of our antiviral candidate CDI-45205 (described below) assists us in designing a subsequent Phase 2 trial for CDI-988.

Intranasal/Pulmonary Protease Inhibitor CDI-45205

CDI-45205 is our novel SARS-CoV-2 3CL (main) protease inhibitor and was among the broad-spectrum viral protease inhibitors we obtained from Kansas State University Research Foundation (KSURF) under an exclusive license agreement announced in April 2020. We believe the protease inhibitors obtained from KSURF have the ability to inhibit the inactive SARS-CoV-2 polymerase replication enzymes into an active form.

CDI-45205 and several analogs showed potent in vitro activity against the main SARS-CoV-2 variants, surpassing the activity observed with the original Wuhan strain of the virus.

CDI-45205 demonstrated good bioavailability in mouse and rat PK studies via intraperitoneal injection, and no cytotoxicity against a variety of human cell lines. CDI-45205 also demonstrated a strong synergistic effect with the FDA-approved COVID-19 medicine remdesivir.

In January 2022 we received guidance from the FDA regarding further preclinical and clinical development of CDI-45205, which provides a clearer pathway for future development.

An IND-enabling study is ongoing with CDI-45205.

Replication Inhibitors

We are using our proprietary structure-based drug discovery platform technology to discover replication inhibitors for orally administered therapeutic and prophylactic treatments for SARS-CoV-2. Replication inhibitors hold potential to work with protease inhibitors in combination therapy regimens.

Norovirus Program

In August 2023 we announced our selection of the novel broad-spectrum 3CL protease inhibitor CDI-988 as our lead potential oral treatment for norovirus. CDI-988 is approved for evaluation in a first-in-human trial in healthy volunteers in Australia, and that trial is expected to serve as the Phase 1 trial for both our norovirus and our coronavirus programs.

With no approved treatments or vaccines, norovirus represents a significant unmet medical need. It is a highly contagious infection and is the most common cause of acute gastroenteritis, accounting for nearly one in five cases. According to the Centers for Disease Control and Prevention (CDC), an estimated 685 million cases and an estimated 200,000 deaths are attributed to norovirus each year worldwide, with an estimated societal cost of $60 billion.

Hepatitis C Program

We are seeking a partner to advance development of CC-31244 following the successful completion of a Phase 2a trial. This compound has shown favorable safety and preliminary efficacy in a triple-regimen Phase 2a trial in combination with Epclusa (sofosbuvir/velpatasvir) for the ultra-short duration treatment of individuals infected with the hepatitis C virus (HCV).

HCV is a viral infection of the liver that causes both acute and chronic infection. The World Health Organization estimated that 58 million people worldwide had chronic HCV infection in 2019.

Corporate Updates

In April we announced the appointment of Fred Hassan to our Board of Directors. Mr. Hassan’s distinguished 40-year career includes serving in senior executive and director positions at global pharmaceutical companies and leading investment firms. He currently is Chairman of the investment firm Caret Group and a Director of Warburg Pincus LLC, a global private equity firm.

In April we completed a $4.0 million private placement offering of common stock with Mr. Hassan and Phillip Frost, M.D., a Company co-founder and director, who currently is Chairman and CEO of OPKO Health.

Second QuarterFinancial Results

Research and development (R&D) expenses for the second quarter of 2023 were $2.8 million, compared with $2.4 million for the second quarter of 2022. The increase was primarily due to preparations for a Phase 2a clinical trial with CC-42344 for pandemic and seasonal influenza A, and preparations for advancing CDI-988’s COVID-19 and norovirus programs toward a Phase 1 clinical trial.

General and administrative (G&A) expenses for the second quarter of 2023 were $1.5 million, compared with $1.4 million for the second quarter of 2022, with the increase primarily due to professional fees and general corporate cost increases.

The net loss for the second quarter of 2023 was $4.2 million, or $0.41 per share, compared with the net loss for the second quarter of 2022 of $24.4 million, or $3.00 per share. The second quarter of 2022 included a legal settlement of $1.6 million, which was returned to the Company in the third quarter of 2023 following a successful appeal of the trial court’s summary judgment ruling. In the second quarter of 2022, the Company also recorded a non-cash goodwill impairment of $19.1 million.

Six Month Financial Results

R&D expenses for the six months ended June 30, 2023 were $6.7 million, compared with $5.2 million for the first six months of 2022. G&A expenses for the six months ended June 30, 2023 and 2022 were unchanged at $2.7 million.

During the first six months of 2022, the Company recorded a $19.1 million non-cash goodwill impairment. There was no comparable impairment charge during the first six months of 2023.

The net loss for the six months ended June 30, 2023 was $9.4 million, or $1.03 per share. The net loss for the six months ended June 30, 2022 was $28.6 million, or $3.48 per share, and reflected the litigation expense and non-cash impairment charge described above.

Cocrystal reported unrestricted cash as of June 30, 2023 of $32.4 million, compared with $37.1 million as of December 31, 2022. Net cash used in operating activities for the first six months of 2023 was $8.7 million. The Company had working capital of $34.1 million and 10.2 million common shares outstanding as of June 30, 2023. During the second quarter of 2023, the Company raised $4.0 million in a private placement offering of common stock that was priced “at-the-market” under Nasdaq Listing Rules.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), noroviruses and hepatitis C viruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our plans for the future development of preclinical and clinical drug candidates, our expectations regarding future characteristics of the product candidates we develop, the expected time of achieving certain value-driving milestones in our programs, including, preparation, commencement and advancement of clinical studies for certain product candidates in 2023 and beyond, the viability and efficacy of potential treatments for coronavirus and other diseases, expectations for the markets for certain therapeutics, our ability to execute our clinical and regulatory goals and deploy regulatory guidance towards future studies, the expected sufficiency of our cash balance to advance our programs and fund our planned operations, and our liquidity. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from the risks arising from interest rate increases in response to inflation, uncertainty in the financial markets, the possibility of a recession and the Ukraine war on our Company, our collaboration partners, and on the U.S., U.K., Australia and global economies, including manufacturing and research delays arising from raw materials and labor shortages, supply chain disruptions and other business interruptions including any adverse impacts on our ability to obtain raw materials and test animals as well as similar problems with our vendors and our current and any future CROs and contract manufacturing organizations (CMOs), the ability of our CROs to recruit volunteers for, and to proceed with, clinical studies, our reliance on Merck for further development in the influenza A/B program under the license and collaboration agreement, our and our collaboration partners’ technology and software performing as expected, financial difficulties experienced by certain partners, the results of any current and future preclinical and clinical trials, general risks arising from clinical trials, receipt of regulatory approvals, regulatory changes, development of effective treatments and/or vaccines by competitors, including as part of the programs financed by the U.S. government, potential mutations in a virus we are targeting which may result in variants that are resistant to a product candidate we develop, and the outcome of the ongoing litigation with the insurance company. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2022. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Operating lease right-of-use assets, net (including $72 and $99 respectively, to related party)

167

274

Total assets

$

35,419

$

40,840

Liabilities and stockholders’ equity

Current liabilities:

Accounts payable and accrued expenses

$

1,421

$

976

Current maturities of finance lease liabilities

–

7

Current maturities of operating lease liabilities (including $62 and $59 respectively, to related party)

166

233

Total current liabilities

1,587

1,216

Long-term liabilities:

Operating lease liabilities (including $10 and $42 respectively, to related party)

10

57

Total liabilities

1,597

1,273

Commitments and contingencies

Stockholders’ equity:

Common stock, $0.001 par value; 150,000 shares authorized as of June 30, 2023, and December 31, 2022; 10,174 and 8,143 shares issued and outstanding as of June 30, 2023 and December 31, 2022

10

8

Additional paid-in capital

341,957

337,489

Accumulated deficit

(308,145

)

(297,930

)

Total stockholders’ equity

33,822

39,567

Total liabilities and stockholders’ equity

$

35,419

$

40,840

COCRYSTAL PHARMA, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in thousands, except per share data)

Three months ended June 30,

Six months ended June 30,

2023

2022

2023

2022

Operating expenses:

Research and development

3,661

2,361

7,568

5,233

General and administrative

1,538

1,375

2,742

2,708

Legal settlement

–

1,600

–

1,600

Impairments

–

19,092

–

19,092

Total operating expenses

5,199

24,428

10,310

28,633

Loss from operations

(5,199

)

(24,428

)

(10,310

)

(28,633

)

Other income (expense):

Interest income (expense), net

140

–

140

(1

)

Foreign exchange loss

33

(1

)

(45

)

(14

)

Change in fair value of derivative liabilities

–

1

–

12

Total other expense, net

173

–

95

(3

)

Net loss

$

(5,026

)

$

(24,428

)

(10,215

)

(28,636

)

Net loss per common share, basic and diluted

$

(0.50

)

$

(3.00

)

(1.12

)

(3.48

)

Weighted average number of common shares outstanding, basic and diluted

Successful submission of final clinical protocol and supporting CMC information to FDA to initiate Phase 3 VERSATILE-003 trial in the fourth quarter 2023

Biomarker data from VERSATILE-002 to be presented at ESMO 2023

Company to host conference call and webcast today at 8:00 AM EDT

PRINCETON, N.J., Aug. 14, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB) (PDS Biotech or the Company), a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer immunotherapies and infectious disease vaccines based on the Company’s proprietary T cell activating platforms, will discuss its financial results for the quarter ended June 30, 2023 and provide a business update on its conference call today.

Recent Business Highlights: PDS0101 Lead Drug Candidate

VERSATILE-003: Submitted the final Phase 3 clinical protocol and supporting Chemistry, Manufacturing and Controls (CMC) information to the U.S. Food and Drug Administration (FDA) to enable initiation of the VERSATILE-003 randomized, controlled multicenter study of PDS0101 in combination with Merck’s anti-PD-1 therapy, KEYTRUDA® (pembrolizumab) in patients with human papillomavirus (HPV) 16-positive recurrent and/or metastatic head and neck cancer in the fourth quarter 2023

VERSATILE-002: Phase 2 open-label, multicenter study of PDS0101 in combination with KEYTRUDA® in patients with human papillomavirus (HPV) 16-positive recurrent and/or metastatic head and neck cancer

Announced clinical immune response data to be presented at upcoming European Society for Medical Oncology (ESMO) Congress 2023

Biomarker data highlighting HPV16-specific killer and helper T cell responses will be presented

Presented interim data at the 2023 American Society of Clinical Oncology (ASCO) annual meeting, demonstrating a 12-month overall survival rate of 87%, with only 8% of patients experiencing Grade 3 treatment-related adverse events, and no reports of more severe Grade 4 or 5 adverse events

Achieved the efficacy threshold in Stage 2 of this clinical trial for the naïve patient arm

14 patients in the immune checkpoint inhibitor (ICI) naïve arm experienced either a complete response or partial response on two consecutive scans 9-12 weeks apart, constituting a confirmed objective response. This result suggests that PDS0101 has a statistically significant additive effect over published results of ICI monotherapy

Completed enrollment in the ICI naïve arm and expect final data readout in mid-2024

PDS0301 + docetaxel: Phase 2, open label, single-arm trial of PDS0301 in combination with docetaxel in metastatic castration sensitive and castration resistant prostate cancer, led by the National Cancer Institute (NCI)

Announced selection of abstract for oral presentation by the NCI at the upcoming Cytokines 2023 Annual Meeting on October 15-18, 2023

The Phase 2 clinical trial is investigating the safety, immune responses, and clinical activity of the combination in metastatic prostate cancer patients

First clinical trial of an immunocytokine with docetaxel in prostate cancer patients

Business Highlights

PDS Biotech was added to the broad-market Russell 2000® and Russell 3000® Indexes in June 2023

“We continue to make significant strides with our lead candidate, PDS0101, specifically with the regulatory and clinical activities necessary to initiate the VERSATILE-003 trial, as well as with progression of the Phase 2 VERSATILE-002 clinical trial,” stated Dr. Frank Bedu-Addo, CEO of PDS Biotech. “In the second quarter, at ASCO 2023, we presented interim data from VERSATILE-002 which revealed an impressive estimated 12-month overall survival rate of 87% and a progression-free survival of 10.4 months, while maintaining a favorable safety profile when PDS0101 is combined with KEYTRUDA®. The reported 12-month overall survival rate for immune checkpoint inhibitors is 30-50%. These encouraging findings fuel our enthusiasm as we prepare to initiate the Phase 3 VERSATILE-003 clinical trial in which patient overall survival will be the primary trial outcome in the fourth quarter of 2023.”

Dr. Bedu-Addo further commented, “In addition to our enthusiasm for PDS0101, we are thrilled about the prospects of PDS0301 which we believe may potentially overcome some of the key safety and efficacy limitations of current cytokines. We are excited about the NCI’s abstract acceptance at the upcoming Cytokines 2023 annual meeting. We anticipate these results have the potential to offer valuable insights into the use of PDS0301 in conjunction with chemotherapy for various solid tumors, presenting a promising avenue for future development and commercialization possibilities.”

Second Quarter 2023 Financial Results

Net loss for the three months ended June 30, 2023 was approximately $11.5 million, or ($0.37) per basic share and diluted share, compared to a net loss of approximately $5.8 million, or ($0.20) per basic share and diluted share, for the three months ended June 30, 2022. The higher net loss this quarter was primarily due to costs incurred in connection with our research and development programs.

Research and development expenses increased to $8.0 million for the three months ended June 30, 2023 from $3.8 million for the three months ended June 30, 2022. The increase of $4.2 million is primarily attributable to an increase of $1.4 million in clinical trials, $0.5 million in personnel costs, including $0.2 million in non-cash stock-based compensation, and $2.3 million in manufacturing expenses.

General and administrative expenses increased to $4.7 million for the three months ended June 30, 2023 from $3.3 million for the three months ended June 30, 2022. The increase of $1.4 million is primarily attributable to an increase of $0.5 million in personnel costs, including $0.4 million in non-cash stock-based compensation and $0.9 million in professional fees.

Cash and cash equivalents as of June 30, 2023, totaled approximately $60.6 million. Based on the company’s cash resources, PDS Biotech believes this amount is sufficient to fund operations and research and development programs for 12 months following the filing of the Company’s June 2023 Quarterly Report on Form 10-Q which will be filed as of the date of this press release.

Conference Call and Webcast

The conference call is scheduled to begin at 8:00 AM EDT today, August 14, 2023. Participants should dial 877-407-3088 (United States) or 201-389-0927 (International) and reference conference ID 13731437. To access the webcast, please use the following link. The event will be archived in the investor relations section of PDS Biotech’s website for six months.

About PDS Biotechnology PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune® T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce and shrink tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials and will be advancing into a Phase 3 clinical trial in combination with KEYTRUDA® for the treatment of recurrent/metastatic HPV16-positive head and neck cancer in 2023. Our Infectimune® based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

About Versamune® Versamune® is a novel investigational T cell activating platform which effectively stimulates a precise immune system response to a cancer-specific protein. Versamune® based investigational immunotherapies promote a potent targeted T cell attack against cancers expressing the protein. They are given by subcutaneous injection and can be combined with standard of care treatments. Clinical data suggest that Versamune® based investigational immunotherapies, such as PDS0101, demonstrate meaningful disease control by reducing and shrinking tumors, delaying disease progression and/or prolonging survival. Versamune® based immunotherapies have demonstrated minimal toxicity to date that may allow them to be safely combined with other treatments. We believe Versamune® based investigational immunotherapies represent a transformative treatment approach for cancer patients to provide improved efficacy, safety and tolerability.

About PDS0101 PDS0101, PDS Biotech’s lead candidate, is a novel investigational human papillomavirus (HPV)-targeted immunotherapy that stimulates a potent targeted T cell attack against HPV-positive cancers. PDS0101 is given by subcutaneous injection alone or in combination with other immunotherapies and cancer treatments. In a Phase 1 study of PDS0101 in monotherapy, the treatment demonstrated the ability to generate multifunctional HPV16 targeted CD8 and CD4 T cells with minimal toxicity. Interim data suggests PDS0101 generates clinically effective immune responses and the combination of PDS0101 with other treatments can demonstrate significant disease control by reducing or shrinking tumors, delaying disease progression, and/or prolonging survival. The combination of PDS0101 with other treatments does not appear to compound the toxicity of other agents.

About PDS0301 PDS0301 is a novel investigational tumor-targeting antibody-conjugated Interleukin 12 (IL-12) that enhances the proliferation, potency and longevity of T cells in the tumor microenvironment. PDS0301 is given by a subcutaneous injection. PDS0301 is designed to improve the safety profile of IL-12 and to enhance the anti-tumor response.

Forward Looking Statements This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the other risks, uncertainties, and other factors described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in the documents we file with the U.S. Securities and Exchange Commission. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® and Infectimune® are registered trademarks of PDS Biotechnology Corporation.

KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

Common stock, $0.00033 par value, 75,000,000 shares authorized at June 30, 2023 and December 31, 2022, 30,868,188 shares and 30,170,317 shares issued and outstanding at June 30, 2023 and December 31, 2022, respectively

10,188

9,956

Additional paid-in capital

155,187,231

145,550,491

Accumulated deficit

(122,753,230

)

(101,558,417

)

Total stockholders’ equity

32,444,189

44,002,030

Total liabilities and stockholders’ equity

$

63,754,250

$

77,007,923

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARY

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

Three Months Ended June 30,

Six Months Ended June 30,

2023

2022

2023

2022

Operating expenses:

Research and development expenses

$

8,004,852

$

3,761,646

$

13,848,538

$

8,922,961

General and administrative expenses

4,691,321

3,331,006

8,270,049

6,648,913

Total operating expenses

12,696,173

7,092,652

22,118,587

15,571,874

Loss from operations

(12,696,173

)

(7,092,652

)

(22,118,587

)

(15,571,874

)

Interest income (expenses), net

Interest income

750,654

74,547

1,479,995

80,247

Interest expense

(995,397

)

–

(1,962,242

)

–

Interest income (expenses), net

(244,743

)

74,547

(482,247

)

80,247

Loss before income taxes

(12,940,916

)

(7,018,105

)

(22,600,834

)

(15,491,627

)

Benefit for income taxes

1,406,021

1,198,905

1,406,021

1,198,905

Net loss and comprehensive loss

(11,534,895

)

(5,819,200

)

(21,194,813

)

(14,292,722

)

Per share information:

Net loss per share, basic and diluted

$

(0.37

)

$

(0.20

)

$

(0.69

)

$

(0.50

)

Weighted average common shares outstanding, basic, and diluted

VERSATILE-003 will evaluate PDS0101 in combination with KEYTRUDA® in recurrent or metastatic HPV16-positive head and neck cancer

PDS Biotech anticipates initiating the VERSATILE-003 trial in the fourth quarter of 2023

PRINCETON, N.J., Aug. 14, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB) (PDS Biotech or the Company), a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer immunotherapies and infectious disease vaccines based on the Company’s proprietary T cell activating platforms, today announced the submission to the U.S. Food and Drug Administration (FDA) of an updated Chemistry, Manufacturing and Controls (CMC) package and a Phase 3 multicenter registrational protocol to the company’s Investigational New Drug (IND) submission to evaluate the combination of PDS0101 and KEYTRUDA® (pembrolizumab), Merck’s anti-PD-1 therapy, for the treatment of recurrent or metastatic human papillomavirus (HPV) 16-positive head and neck squamous cell carcinoma (HNSCC). The protocol was developed in accordance with guidance from the FDA on key elements of the Phase 3 program to support the eventual submission of a Biologics License Application (BLA).

The Phase 3 trial, named VERSATILE-003, is a randomized, active comparator-controlled study designed to investigate the safety and efficacy of PDS0101 combined with KEYTRUDA® compared to KEYTRUDA® monotherapy in immune checkpoint inhibitor (ICI)-naïve patients with recurrent or metastatic HPV16-positive HNSCC. The primary efficacy endpoint for VERSATILE-003, per the protocol, is overall survival (OS). The Phase 3 study is expected to involve approximately 90-100 clinical sites globally. PDS Biotech anticipates initiating the VERSATILE-003 Phase 3 trial in the fourth quarter of 2023.

“Submission of the protocol and supportive CMC documents for this Phase 3 registrational trial is an important milestone for PDS Biotech and our VERSATILE-003 program investigating PDS0101 in combination with KEYTRUDA® as a potential treatment for recurrent or metastatic HPV16-positive HNSCC,” stated Dr. Lauren V. Wood, PDS Biotech’s Chief Medical Officer. “Interim data from our ongoing VERSATILE-002 Phase 2 clinical trial have been very encouraging, with impressive interim OS and PFS results. With VERSATILE-003, we have an opportunity to confirm the Phase 2 results from VERSATILE-002 in a controlled, Phase 3 clinical trial comparing the combination of PDS0101 and KEYTRUDA® to KEYTRUDA® monotherapy.”

About PDS0101

PDS0101, PDS Biotech’s lead candidate, is a novel investigational human papillomavirus (HPV)-targeted immunotherapy that stimulates a potent targeted T cell attack against HPV-positive cancers. PDS0101 is given by subcutaneous injection alone or in combination with other immunotherapies and cancer treatments. In a Phase 1 study of PDS0101 in monotherapy, the treatment demonstrated the ability to generate multifunctional HPV16-targeted CD8 and CD4 T cells with minimal toxicity. Interim data suggest PDS0101 generates clinically effective immune responses, and the combination of PDS0101 with other treatments can demonstrate significant disease control by reducing or shrinking tumors, delaying disease progression and/or prolonging survival. The combination of PDS0101 with other treatments does not appear to compound the toxicity of other agents.

About VERSATILE-002

VERSATILE-002 is a single-arm Phase 2 trial evaluating the safety and efficacy of PDS0101, an HPV16-targeted investigational T cell-activating immunotherapy that leverages PDS Biotech’s proprietary Versamune® technology, in combination with Merck’s anti-PD-1 therapy, KEYTRUDA® (pembrolizumab). The combination is being evaluated in immune checkpoint inhibitor (ICI)-naïve and ICI-refractory patients with recurrent/metastatic HPV16-positive head and neck squamous cell carcinoma (HNSCC) and was granted Fast Track designation by the Food and Drug Administration in June 2022.

Interim efficacy and safety data were presented at the 2023 American Society of Clinical Oncology (ASCO) Annual Meeting for ICI-naïve patients. Preliminary data from the first 34 patients demonstrated a 12-month overall survival rate of 87% and median progression free survival of 10.4 months. No Grade 4 or higher treatment related adverse events were observed, and Grade 3 treatment related adverse events were observed in 8% of patients.

About VERSATILE-003

VERSATILE-003 is a randomized, controlled Phase 3 trial evaluating the safety and efficacy of PDS0101 in combination with Merck’s anti-PD-1 therapy, KEYTRUDA® (pembrolizumab) versus KEYTRUDA® monotherapy. The combination is being evaluated in immune checkpoint inhibitor (ICI)-naïve patients with recurrent/metastatic HPV16-positive head and neck squamous cell carcinoma (HNSCC) and was granted Fast Track designation by the Food and Drug Administration in June 2022.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune® T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce and shrink tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials and will be advancing into a Phase 3 clinical trial in combination with KEYTRUDA® for the treatment of recurrent/metastatic HPV16-positive head and neck cancer in 2023. Our Infectimune® based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the other risks, uncertainties, and other factors described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in the documents we file with the U.S. Securities and Exchange Commission. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® and Infectimune® are trademarks of PDS Biotechnology Corporation. KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics and diagnostics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of immunology, rare disease, infectious disease, and central nervous system (CNS) product candidates. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-15001 which is a humanized monoclonal antibody targeting CD40-ligand being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the second half of 2022. Tonix’s rare disease portfolio includes TNX-29002 for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan-Drug Designation by the FDA. Tonix’s infectious disease pipeline includes a vaccine in development to prevent smallpox and monkeypox called TNX-8013, next-generation vaccines to prevent COVID-19, and an antiviral to treat COVID-19. Tonix’s lead vaccine candidates for COVID-19 are TNX-1840 and TNX-18504, which are live virus vaccines based on Tonix’s recombinant pox vaccine (RPV) platform. TNX-35005 (sangivamycin, i.v. solution) is a small molecule antiviral drug to treat acute COVID-19 and is in the pre-IND stage of development. TNX-102 SL6, (cyclobenzaprine HCl sublingual tablets), is a small molecule drug being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix expects to initiate a Phase 2 study in Long COVID in the second quarter of 2022. The Company’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL, is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022. Finally, TNX-13007 is a biologic designed to treat cocaine intoxication that is expected to start a Phase 2 trial in the second quarter of 2022. TNX-1300 has been granted Breakthrough Therapy Designation by the FDA.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.