The FOMC May Now Apply Less Brake Pedal to the Economy

The Federal Open Market Committee (FOMC) voted to raise overnight interest rates from a target of 4.75% – 5.00%. to the new target of 5.00% – 5.25%. This 25bp move was announced at the conclusion of the Committee’s May 2023 meeting. The monetary policy shift in bank lending rates had been expected but concerns of the impact of tightening on some economic sectors, including banking, had been called into question and left Fed-watchers unsure if the Fed would clearly indicate a pause in the tightening cycle. Inflation which had been easing somewhat going into the last FOMC held in March has since reversed direction and remains elevated.

As for the U.S. banking system, which is part of the Federal Reserves responsibility, the FOMC statement reads, “The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain.”

As for inflation which is hovering at more than twice the Fed’s target, the post FOMC statement reads, “The Committee remains highly attentive to inflation risks.” Both of these quotes can be viewed as not trying to panic markets in either direction.

There were few clues given in the statement about any next move, causing some to believe that the Fed is now going to take a wait-and-see position as previous rate hikes play out in the economy. The statement was shorter than previous releases following a two-day FOMC meeting, but it ended with the following forward-looking actions:

“In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.”

Fed Chair Powell generally shares more thoughts on the matter during a press conference beginning at 2:30 after the statement.

Are Treasuries the Safe Bet Investors Think They Are?

Are US Treasury bonds worth owning? US Treasury debt is considered one of the safest investments in the world. The securities are issued by the US government and are backed by the full faith and credit of the US Treasury – guaranteed at the same level as the dollar bills in your wallet. These bonds are a popular investment choice for individuals, institutions, and governments in times of economic uncertainty. But, as with other investments, they are market priced by the combined wisdom of the marketplace. So the return, or what is sometimes referred to as “the risk-free rate,” may not measure up to the potential that stock market investors expect.

Why Allocate to Treasuries

US Treasury bonds are considered a safe haven investment because they are perceived to have a low risk of default. This is because the US government has never defaulted on its debt, and it has the ability to raise taxes and print money to meet its obligations. In addition, the US dollar remains the world’s reserve currency, this makes US Treasury bonds highly liquid and easily tradable.

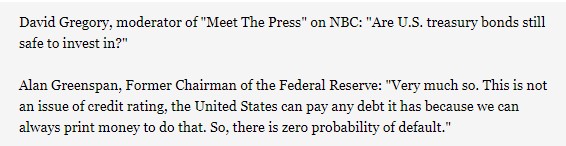

Image: Fmr. Fed Chairman Greenspan, Meet the Press interview, August 2011

During periods of low economic clarity, investors that are not required to invest in low-risk investments will weigh US Treasury returns against expected returns in other markets. As interest rates approach or exceed expected inflation US Treasuries become more attractive to investors, both individual and institutional. This is because they provide a reliable source of income (semiannual interest payments) at times of market volatility, and at maturity, owners know exactly what they will receive (face value plus the last interest payment). For example, during the global financial crisis of 2008-2009, investors flocked to the safety of US Treasury bills, notes, and bonds as a safe haven. This drove down yields and pushed up bond prices.

There are three main Treasury Securities, TIPS are not included below, they are T-Notes and have unique risks, so, therefore, deserve a separate presentation.

Treasury Bills:

Maturity: Typically less than one year (usually 4, 8, 13, 26, or 52 weeks)

Yield: Discounted yield, historically lower than T-notes and T-bonds

Size: Available in denominations of $1,000 or more

Treasury Notes:

Maturity: 2 to 10 years

Yield: Par plus interest historically higher than T-bills and lower than T-bonds

Size: Avaialable in denominations of $1,000 or more

Treasury Bonds:

Maturity: 10 to 30 years

Yield: Normally higher than T-bills and T-notes

Size: Avaialable in denominations of $1,000 or more

Overall, the main difference between these securities is their maturity. T-bills have the shortest maturity and are discounted at purchase to provide the yield, while T-bonds have the longest. T-notes fall in between. Additionally, their yields are calculated on an actual number of days held over the actual number of days in the year. The US Treasury yield curve, above which other bonds are priced, depends on market conditions and economic expectations.

Can Not Avoid Risk

Despite their reputation for safety, US Treasury bonds are not without risk. In December of 2021, the 10 year US Treasury note had a market yield of 1.70%. Just ten months later the same bond sold at a yield of 4.21%. This represents an actual loss over the ten month period for those selling the bond then. For those holding until maturity, when they will receive full face value, investors would have to hold more than eight years during which they will be earning a measly 1.7%. This is interest rate risk, the time period used to explain was a recent extreme example of how Treasuries still have very real risk. This is why a good bank investment portfolio manager will do stress tests and scenario analysis of the banks portfolio using extreme conditions.

Another risk is credit rating. In 2011, for example, the credit rating agency Standard & Poor’s downgraded the US government’s credit from AAA to AA+. This was the first time and continues to be the only time the US government has been downgraded. The downgrade was based on concerns about the government’s ability to address its long-term fiscal challenges, including high levels of debt and political gridlock.

Similar conditions may be playing out now as the debt ceiling has been raised quite a bit since 2009, and large buyers such as China are seeking alternative investments for their reserve balances.

Inflation is another risk that is quite real. As in the earlier example of the USTN 10-year yielding 1.7% in December 2021, during the following year, CPI rose 6.5%. this is another recent example of how investing in a low-rate environments can erode the purchasing power of the interest income and principal payments from US Treasury bonds. If the rate of inflation exceeds the yield on the bonds, investors can actually experience a negative real return.

If the government is seen as possibly not being able to pay interest on maturing securities, as is the case during debt ceiling standoffs, US Treasuries coming due may experience illiquidity problems as bids for maturing debt that may not get paid on time will be weak.

Although US Treasury bonds are highly liquid and easily tradable, there may be periods when the market for the bonds becomes illiquid. This can make it difficult for investors to sell their bonds at a fair price, especially during times of market stress or uncertainty.

How to Invest in Treasuries

Investors can buy US Treasury bonds directly from the US government (treasurydirect.gov) or through a broker. The bonds are issued and market priced at auctions on a regular schedule. Individual investors typically will bid to own securities at the average auction price. Savvy institutions and individuals may contact their broker and bid at the auction and hope to win an allotment.

Investors can also invest in US Treasury bonds through mutual funds or exchange-traded funds (ETFs). These funds don’t offer the benefit of holding to maturity or some of the tax planning strategies that can benefit those holding a security and not a fund.

Take Away

US Treasury bonds are considered a safe haven investment in times of economic uncertainty. They are backed by the full faith and credit of the US government and are considered one of the safest investments in the world. While they are not without risk, they remain a popular choice for investors seeking a reliable source of income and capital preservation. The US government’s credit rating was downgraded once, but investors continue to have confidence in US Treasury bonds due to the idea that they may not be safe, but they are likely the safest place to store savings.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Indonesia Energy Filed Its 20-F (Foreign) Document with the SEC Providing Financial Data. Due to drilling and production delays, revenue growth has been slower than projected. The company continues to report negative cash flow and earnings as limited revenues are hard pressed to cover G&A costs. The result was a $4.5 million loss from operations for the year, an EBITDA loss of $3.5 million, and negative net income of $3.1 million ($0.35 per share). The results were below our expectations, although the Indo story is really one of operating developments, not near-term results.

Operations are quiet. The filing largely repeated previously stated plans for drilling in the Kruh Block (4 in 2024, 6 in 2025, and 4 in 2026). INDO has drilled four wells in the Kruh Block, the last of which is still awaiting final flow test results but expected to be put in production mid 2023. After the last well, the company put new drilling on hold to complete additional seismic studies. Importantly, limited production has meant that it may not be able to fully recover costs spent under the revenue sharing agreement (INDO has filed for an extension).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Newegg Commerce, Inc. (NASDAQ: NEGG), founded in 2001 and based in the City of Industry, Calif., near Los Angeles, is a leading global online retailer for PC hardware, consumer electronics, gaming peripherals, home appliances, automotive and lifestyle technology. Newegg also serves businesses’ e-commerce needs with marketing, supply chain and technical solutions in a single platform. For more information, please visit Newegg.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 results. The company reported better-than-expected Q4 results. Total revenue of $480.6 million beat our estimate of $439.2 million by 9%, and adj. EBITDA of $5.1 million was significantly better than our forecast of $0.1 million.

Still a challenging sales environment. Following a difficult 2022, persistent macroeconomic concerns appear to be putting pressure on the consumer electronics market. As such, management noted that 2023 could face similar challenges to 2022. The company initiated cost-cutting measures with the aim of offsetting some of the adverse revenue impacts on cash flow.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Co-CEOs. FAT Brands announced Ken Kuick and Rob Rosen as Co-CEOs, effective May 5, 2023. As previously announced, Andy Wiederhorn will step down as CEO and continue in his role as Chairman of the Board, where he will focus on the strategic direction of the company, the allocation of capital, and ensuring the management team executes the Company’s business plan while maintaining quality restaurant operations.

Staying In-House. Currently, Mr. Kuick is Chief Financial Officer of the Company and Mr. Rosen holds the position of Executive Vice President of Capital Markets. Both played an integral role alongside Mr. Wiederhorn in driving the growth of FAT Brands. Both will continue in their current roles as well as assuming the Co-CEO role. With their in-depth knowledge and contribution to the growth of FAT Brands, we believe the choice of Mr. Kuick and Mr. Rosen to be a win for the Company.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. ANJESO is the first and only 24-hour, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Gregory Aurand, Senior Vice President, Equity Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

$4 million gross proceeds. Baudax Bio closed its public offering of 3,478,262 common shares (or pre-funded warrants) at $1.15 per share. Each share was accompanied by a Series A-5 warrant to purchase one share and a Series A-6 warrant to purchase one share, both exercisable at $1.15. The Series A-5 warrant is exercisable immediately and expires five years from issuance. The Series A-6 warrant is also exercisable immediately and expires 18 months from issuance. The offering was pursuant to an S-1 filing effective April 26, 2023.

Funding needs. As part of the restructured credit agreement, the Company needed capital for upcoming debt payments and related minimum liquidity requirements. The proceeds will also be used for advancing the NMB pipeline. We expect continued funding needs and have incorporated a higher share count into our outlook.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The US debt limit is the total amount of money the United States government is authorized to borrow to meet its existing obligations. These include interest on debt, Social Security, military costs, government payroll, utilities, tax refunds, and all costs associated with running the country.

The debt limit is not designed to authorize new spending commitments. Its purpose is to provide adequate financing for existing obligations that Congress, through the years, has approved. While taxes provide revenue to the US Treasury Department, taxation has not been adequate since the mid-1990s to satisfy US spending. This borrowing cap, the so-called debt ceiling, is the maximum congressional representatives have deemed prudent each year, and has always been raised to avert lost faith in the US and its currency.

Failing to increase the debt limit would have catastrophic economic consequences. It would cause the government to default on its legal obligations – which has never happened before. Default would bring about another financial crisis and threaten the financial well-being of American citizens. Since a default would be much more costly than Congress meeting to approve a bump up in the borrowing limit, which the President could then sign, it is likely that any stand-offf will be resolved on time.

Congress has always acted when called upon to raise the debt limit. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt.

How Does this Apply Today?

According to the Congressional Budget Office, tax receipts through April have been less than the CBO anticipated in February. The Budget Office now estimates that there is a significantly elevated risk that the US Treasury will run out of funds in early June 2023. The US Treasury Secretary has even warned that after June 1, the US will have trouble meeting its obligations. The implications could include a credit rating downgrade in US debt which could translate to higher interest rates. If US Treasury obligations, the so-called “risk free” investments, does not pay bondholders on time (interest), then the entire underpinning of an economy that relies on the faith in its economic system, could quickly unravel.

What Took Us Here?

On January 19, 2023, the statutory limit on the amount of debt that the Department of the Treasury could issue was reached. At that time, the Treasury announced a “debt issuance suspension period” during which, under the law, can take “extraordinary measures” to borrow additional funds without breaching the debt ceiling.

The Treasury Dept. and the CBO projected that the measures would likely be exhausted between July and September 2023. They warned that the projections were uncertain, especially since tax receipts in April were a wildcard.

It’s now known that receipts from income tax payments processed in April were less than anticipated. Making matters more difficult, the Internal Revenue Service (IRS) is quickly processing tax return payments.

If the debt limit is not raised or suspended before the extraordinary measures are exhausted, the government will ultimately be unable to pay its obligations fully. As a result, the government will have to delay making payments for some activities, default on its debt obligations, or both.

What Now?

The House of Representatives passed a package to raise the debt ceiling by $1.5 trillion in late April. The bill, includes spending cuts, additional work requirements in safety net programs, and other measures that are unpopular with Democrats. To pass, the Senate, which has a Democratic majority, would have to pass it. Democratic Senator Chuck Schumer described the chances as “dead on arrival.”

House Speaker McCarthy has accepted an invitation from President Biden to meet on May 9 to discuss debt ceiling limits. The position the White House is maintaining is that it will not negotiate over the debt ceiling. The President’s party is looking for a much higher debt ceiling that allows for greater borrowing powers.

In the past, debt ceiling negotiations have often gone into the night on the last day and have suddenly been resolved in the nick of time. Treasury Secretary Yellen made mention of this and warned that past debt limit impasses have shown that waiting until the last minute can cause serious harm, including damage to business and consumer confidence as well as increased short-term borrowing costs for taxpayers. She added that it also makes the US vulnerable in terms of national security.

Expect volatility in all markets as open discussions and likely disappointments will heat up beginning at the May 9th meeting between McCarthy and Biden.

IBM Will Stop Hiring Professionals For Jobs Artificial Intelligence Might Do

Will AI take jobs and replace people in the future? Large companies are now making room for artificial intelligence alternatives by reducing hiring for positions that AI is expected to be able to fill. Bloomberg reported earlier in May that International Business Machines (IBM) expects to pause the hiring for thousands of positions that could be replaced by artificial intelligence in the coming years.

IBM’s CEO Arvind Krishna said in an interview with Bloomberg that hiring will be slowed or suspended for non-customer-facing roles, such as human resources, which makes up make up 26,000 positions at the tech giant. Watercooler talk of how AI may alter the workforce has been part of discussions in offices across the globe in recent months. IBM’s policy helps define in real terms the impact AI will have. Krishna said he expects about 30% of nearly 26,000 positions could be replaced by AI over a five-year period at the company, that’s 7,800 supplanted by AI.

IBM employs 260,000 people, the positions that involve interacting with customers and developing software are not on the chopping block Krishna said in the interview.

Image credit: Focal Foto (Flickr)

Global Job Losses

In a recent Goldman Sachs research report titled, Generative AI could raise global GDP by 7%, it was shown that 66% of all occupations could be partially automated by AI. This could, over time, allow for more productivity. The report’s specifics are written on the contingency that “generative AI delivers on its promised capabilities.” If it does, Goldman believes 300 million jobs could be threatened in the U.S. and Europe. If AI evolves as promised, Goldman estimates that one-fourth of current work could be accomplished using generative AI.

Sci-fi images of a future where robots replace human workers have existed since the word robot came to life in 1920. The current quick acceleration of AI programs, including ChatGPT and other OpenAI.com products, has ignited concerns that society is not yet ready to reckon with a massive shift in how production can be met without payroll.

Should Workers Worry?

Serial entrepreneur Elon Musk is one of the most vocal critics of AI. He is one of the founders of OpenAI, and the robot division at Tesla. In April, Musk claimed in an interview with Tucker Carlson on Fox News that he believes tech executives like Google’s Larry Page are “not taking AI safety seriously enough.” Musk asserts that he’s been called a “speciesist” for raising alarm bells about AI’s impact on humans, his concern is so great that he is moving forward with his own AI company—X.AI. This, he says, is in response to the recklessness of tech firms.

IBM now has digital labor solutions which help customers automate labor-intensive tasks such as data entry. “In digital labor, we are helping finance, accounting, and HR teams save thousands of hours by automating what used to belabor intensive data-entry tasks,” Krishna said on the company’s earnings call on April 19. “These productivity initiatives free up spending for reinvestment and contribute to margin expansion.”

Technology and innovation have always benefitted households in the long term. The industrial revolution, and later the technology revolution, at first did eliminate jobs. Later the human resources made available by machines increased productivity by freeing up people to do more. Productivity, or increased GDP, is equivalent to a wealthier society as GDP per capita increases.

TORONTO–(BUSINESS WIRE)– Largo Inc. (“Largo” or the “Company”) (TSX: LGO) (NASDAQ: LGO) announces today that Andrea Weinberg has been appointed as an independent director to the Company’s Board of Directors (“Board”).

Largo Announces the Appointment of Andrea Weinberg to its Board of Directors (Photo: Business Wire)

J. Alberto Arias, Chairman of Largo’s Board of Directors commented: “Andrea’s extensive knowledge of the metals sector, global financial markets, and specifically Brazil, her native country where she resides, makes her an excellent addition to our Board of Directors. With Andrea, the Board has gained an invaluable member who will assist the Company in enhancing value for Largo shareholders.” He continued: “In addition, Andrea most recently served on the board of Largo Physical Vanadium Corp. (“LPV”) during its founding, providing her with a thorough understanding of both the vanadium market fundamentals and the innovative business model we developed between Largo, Largo Clean Energy and LPV. It is our view that LPV has the potential to substantially improve the competitiveness of the vanadium flow battery industry in the future and the prospects of vanadium demand in general.”

Andrea Weinberg commented: “As the vanadium industry enters an exciting new phase of growth, largely driven by the world’s decarbonization needs and clean energy transition, it is my pleasure to join Largo’s Board of Directors and work closely with the management team and other Board members to execute on the Company’s two-pillar business strategy. Largo has developed a compelling business proposition to help advance a low-carbon future and I am excited to be a part of it going forward.”

Ms. Weinberg is a Director of Cosan, a Brazilian holding company of logistics, gas, fuels, lubricants and mining assets in Brazil. She has over 25 years of experience in the financial markets working at companies such as BTG Pactual, BlackRock for Latin American and Global Emerging Market funds, AllianceBernstein and Dynamo Administradora de Recursos covering commodities (metals & mining, pulp and paper and oil), amongst other things. Before joining the buyside industry, Ms. Weinberg worked as a sell side analyst at Merrill Lynch (2004-2007) and Goldman Sachs (1998-2004) covering the Metals & Mining sector. Ms. Weinberg holds a Bachelor of Science in Chemical Engineering from Universidade Federal do Rio de Janeiro and a Master’s Degree in Financial Engineering & Operations Research from Columbia University.

About Largo

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURETM and VPURE+TM products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing an ilmenite concentration plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Largo’s common shares trade on the Nasdaq Stock Market and on the Toronto Stock Exchange under the symbol “LGO”. For more information on the Company, please visit www.largoinc.com.

Investor Relations Alex Guthrie Senior Manager, External Relations +1.416.861.9778 aguthrie@largoinc.com

SeniorFAT BrandsExecutivesAppointed to Lead Global Restaurant Franchising Company

LOS ANGELES, May 01, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. announces Ken Kuick and Rob Rosen as Co-CEOs, effective May 5, 2023. As previously announced, Andy Wiederhorn will step down as CEO and continue in his role as Chairman of the Board, where he will focus on the strategic direction of the company, the allocation of capital, and ensuring the management team executes the Company’s business plan while maintaining quality restaurant operations.

Joining FAT Brands in 2021, Mr. Kuick, Chief Financial Officer, and Mr. Rosen, Executive Vice President of Capital Markets, have both played an integral role in the growth of the Company with a focus on strategic growth initiatives, including acquisitions and driving company profitability. Mr. Kuick and Mr. Rosen will also continue in their respective roles as Chief Financial Officer and Executive Vice President of Capital Markets while assuming the Co-CEO role. Together, they will focus on driving forward the Company’s overarching goals of increasing organic growth through new store openings, growing the utilization of its manufacturing facility, and bolstering the success of high-growth brands, including Twin Peaks.

Mr. Kuick’s past roles include Chief Financial Officer, Noodles & Company, Chief Accounting Officer, VICI Properties, and Chief Accounting Officer, Caesars Entertainment Operating Company, a subsidiary of Caesars Entertainment. Mr. Rosen is a Wall Street veteran with over 30 years of experience in structured finance, banking, lending, and portfolio management. Mr. Rosen has held positions at Fleet Bank, Kidder Peabody, and Bank of Tokyo, and has 20 years of experience with Black Diamond Capital Management in a variety of management, board-level, and advisory capacities.

“Over the last few years, Ken and Rob have played a tremendous role in the unprecedented growth of FAT Brands,” said Andy Wiederhorn, CEO of FAT Brands. “Their financial acumen and track record for hitting key company benchmarks make them well-positioned to take on the CEO role together. I look forward to continuing to work with Ken and Rob in the Chairman of the Board position to aid in the continued success of FAT Brands.”

“Andy is a great leader and I’m extremely humbled to take on this new responsibility and drive forward the key goals of the company,” said Ken Kuick, Chief Financial Officer of FAT Brands. “We are fortunate to have such a talented team at FAT Brands and I see great opportunity ahead in building upon our positioning as one of the largest restaurant companies in the U.S.”

“I’m honored to take on the Co-CEO position of a company that continues to surpass growth expectations,” said Rob Rosen, Executive Vice President of Capital Markets at FAT Brands. “In the near term, Ken and I will look to build on the strong foundation FAT Brands has already laid, which includes our robust growth pipeline, exciting innovations, and a commitment to our franchisees and customers.”

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements reflect expectations of FAT Brands Inc. (“we”, “our” or the “Company”) concerning future events and are subject to significant business, economic and competitive risks, uncertainties and contingencies, including but not limited to uncertainties surrounding the severity, duration and effects of the COVID-19 pandemic. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) announced today the appointment of Carolyn Cassidy as General Manager of its five-station radio group and of Salem Surround in Tampa and Sarasota, Florida.

Cassidy is currently the General Manager of Salem’s Columbus, OH operation, she will retain those responsibilities in addition to her new role as GM in Tampa/Sarasota. In her extensive broadcasting background, Cassidy has served in sales leadership and General Management roles in Colorado Springs, Denver, Cape Cod, Vermont and Ohio. Carolyn has been an active member of the board of the Ohio Association of Broadcasters and has been twice recognized by Radio Ink magazine as a General Manager of the Year.

Salem Media Group Regional Vice President Val Carolin commented, “As we worked to fill the big shoes that Barb Yoder has worn so effectively these past 12 years as General Manager, we were thrilled to learn that Carolyn had a strong desire to return to her Florida roots and serve the communities in her home state. Carolyn has proven herself to be a tireless leader with a deep commitment to service. She’s a hard and smart worker who gets involved and gets things done. I’m confident that the dedication and the skills she possesses will prove to be a great fit for our strong Tampa/Sarasota operation.”

Cassidy commented, “I’m honored to be leading our talented Tampa/Sarasota team. The vision that Dave Santrella and Allen Power have laid out for the growth of our Company is clear and is one that we are striving to achieve here in Tampa Bay and beyond. We look forward to the future and to building upon the success that Barb Yoder and her great team have created. This is a customer focused operation that strives to deliver strong results for our partners by activating effective, individualized digital and broadcast solutions. I started my radio career in the sunshine state, so it is wonderful to be home!”

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Operational Update. MustGrow released 4Q22 and full year 2022 operating results at the end of last week. As we have just provided an update on the Company following management’s webinar presentation, we will just highlight key elements of the results here.

Financial Results. Zero revenue and a loss of $1.0 million, or a loss of $0.02/sh for the fourth quarter., similar to the 4Q21 loss, although EPS loss last year was $0.03 due to fewer outstanding shares. The 4Q22 loss was about 1/2 of the 3Q22 loss due to lower stock comp expense and professional fees expense. For the full year, MustGrow reported revenue of $6,479 and a net loss of $5.6 million, or a loss of $0.11/sh, compared to a loss of $3.1 million, or a loss of $0.07/sh in 2021.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The taming of monetary policy necessary to slow price inflation has triggered a corrective trend in the valuation of financial instruments. Many big banks in the United States have substantially increased their use of an accounting technique that allows them to avoid marking certain assets at their current market value, instead using the face value in their balance sheet calculations. This accounting technique consists of announcing that they intend to hold such assets to maturity.

As of the end of 2022, the bank with the largest amount of assets marked as “held to maturity” relative to capital was Charles Schwab. Apart from being structured as a bank, Charles Schwab is a prominent stockbroker and owns TD Ameritrade, another prominent stockbroker. Charles Schwab had over $173 billion in assets marked as “held to maturity.” Its capital (assets minus liabilities) stood at under $37 billion. At that time, the difference between the market value and face value of assets held to maturity was over $14 billion.

If the accounting technique had not been used the capital would have stood at around $23 billion. This amount is under half the $56 billion Charles Schwab had in capital at the end of 2021. This is also under 15 percent of the amount of assets held to maturity, under 10 percent of securities, and under 5 percent of total assets. An asset ten years from maturity is reduced in present value by 15 percent with a 3 percent increase in the interest rate. An asset twenty years from maturity is reduced in present value by 15 percent with a 1.5 percent increase in the interest rate.

The interest rates for long-term financial instruments have remained relatively stable throughout the first quarter of 2023, but this may be subject to change as many of the long-term assets of recently failed Silicon Valley Bank and Signature Bank must be sold off for the Federal Deposit Insurance Corporation to replenish its liquidity. The long-term interest rate is also heavily dependent on inflation expectations, as with higher inflation a higher nominal rate is necessary to obtain the same real rate. It is also important to remember that the US Congress has persisted in not raising the debt ceiling for the government, which is currently projected to not be able to meet all its obligations by August. This could impact the value of treasuries held by the banks.

Other banks that may be close to an effective insolvency include the Bank of Hawaii and the Banco Popular de Puerto Rico (BPPR). The Bank of Hawaii’s hypothetical shortfall as of the end of 2022 already exceeded 60 percent of its capital. The BPPR has over double its capital in assets held to maturity. All three banks—Bank of Hawaii, BPPR, and Charles Schwab—have lost between one-third and one-half of their market capitalization over the last month.

It is difficult to say with certainty whether they are indeed secretly close to insolvency as they may have some form of insurance that could absorb some of the impact from a loss of value in their assets, but if this were the case it is not clear why they would need to employ this questionable accounting technique so heavily. The risk of insolvency is currently the highest it’s been in over a decade.

Central banks can solve liquidity problems while continuing to raise interest rates and fight price inflation, but they cannot solve solvency problems without pivoting monetary policy or through blatant bailouts, which could increase inflation expectations, exacerbating the problem of decreasing valuations of long-term assets. In the end, the Federal Reserve might find that the most effective way to preserve the entire system is to let the weakest fail.