Tesla’s “Investor Day” Reveals that Opportunities Exist in Ancillary EV Businesses

Investors may have absorbed more ideas from Elon Musk at Tesla’s Investor Day about related opportunities outside of Telsa (TSLA) than in the company itself. The founder was not as forthcoming as expected; however, he did confirm Tesla’s plans to build a fifth car assembly plant in Mexico. He also made reference to a next-gen vehicle and rolled out a $ 1-a-day subscription for owners in some regions for unlimited charging. Autonomous driving updates along with safety numbers were revealed, and how and why Tesla is going to solidify its supply chain and provide itself uninterrupted battery-grade lithium was of particular interest to investors in the metals and mining industries.

Musk on Metals and Mines

It was thought that both those attending in person and those streaming would be treated to a Tesla plan to acquire a mining operation in North or South America amid rampant demand for the material crucial to battery EVs. To respond to the speculation, Musk said the EV manufacturer is “mulling” the takeover of a miner. The miner most often discussed in relation to Tesla is Sigma Lithium Corp. (SGML).

What was more concrete on the battery manufacturing supply chain issue, is it was made clear Tesla is more focused on refining lithium than on mining it. The CEO of the most valuable car company in the world said the “limiting factor” is refining lithium, not actually finding it, as no country has a monopoly on deposits.

Not all investors and analysts can make it to the PDAC Mineral Exploration and Mining Conference in Toronto. In order for our subscribers to stay in the loop, Noble Capital Markets will be attending PDAC conference meetings and then interviewing select executives. This will be captured on video for the exclusive benefit of Channelchek subscribers (no cost). Learn more about the Channelchek Takeaway Series at PDAC.

Tesla has already broken ground on what will be a lithium refinery in Texas, it plans to start output within 12 months. According to a presentation by Drew Baglino, SVP of Tesla’s Powertrain and Energy Engineering department, the EV giant wants to process lithium concentrates into battery-grade lithium chemicals at the refinery in Texas.

As for the EV battery metal nickel, it’s only needed for “aircraft, long-range cars or trucks,” Musk said. “The vast majority of heavy lifting” of EV batteries will be iron-based batteries, and there’s plenty of iron in the world, he said.

The EV Industry Unfolding

Automakers are increasingly pushing into partnerships and ownership of the mining of commodities needed for their end product. Those that vertically integrate early will have their pick among the miners that are a better fit – and potentially priced before demand accelerates. Recently the car company Stellantis took a 14% stake in a subsidiary of McEwen Mining (MUX) that produces copper. And General Motors is said to be negotiating a stake in Vale SA’s base metals unit. In January, GM conditionally okayed a $650-million pact with Lithium Americas (LACCA) to develop a US lithium deposit.

Take Away

Telsa’s Investor Day included updates on autonomous cars and presentations that showed off the company executives, but it didn’t leave a buzz in the EV industry.

It was confirmed that EV manufacturers are eying companies that produce the ingredients they need for their cars to have power. Investors may want to explore producers of lithium, copper, cobalt, and nickel. Especially those closest to EV battery manufacturing facilities.

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) announced today that it plans to report its fourth quarter 2022 financial results after the market closes on March 8, 2023.

The company also plans to host a teleconference to discuss its results on March 8, 2023 at 4:00 PM Central Time. To access the teleconference, please dial (888) 770-7291, and then ask to be joined to the Salem Media Group Fourth Quarter 2022 call or listen to the webcast.

A replay of the teleconference will be available through March 22, 2023 and can be heard by dialing (800) 770-2030 – replay pin number 2413416, or on the investor relations portion of the company’s website, located at investor.salemmedia.com.

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

HOUSTON, March 1, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that the Company will be participating in the 35th Annual Roth Conference scheduled for March 12-14, 2023 at The Ritz Carlton, Laguna Niguel in Dana Point, California.

Mark D. Walker, Chairman & Chief Executive Officer of Direct Digital Holdings, Keith Smith, President of Direct Digital Holdings, and Susan Echard, Chief Financial Officer of Direct Digital Holdings, will be attending on behalf of the Company and available for meetings during the conference.

Mark D. Walker will participate in a fireside chat with Darren Aftahi, Managing Director and Senior Research Analyst, at 12:30 PM-12:55 PM PT on Tuesday, March 14, 2023.

Keith Smith will participate on an IPO Readiness panel discussion hosted by James O’Grady, Partner, Lowenstein Sandler LLP, at 10:00 AM-10:55 AM PT on Tuesday, March 14, 2023.

For more information, or to schedule a meeting with management, please reach out to your Roth MKM representative.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, video, CTV, in-app and other media channels. Direct Digital Holdings is the ninth black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

National Cancer Institute (NCI)-led research of PDS0301, a novel investigational tumor-targeting IL-12 fusion protein, shows dose-dependent, immune responses and association with improved clinical outcomes

FLORHAM PARK, N.J., March 01, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, announced that clinical research conducted by the NCI, one of the Institutes of the National Institutes of Health, was published in the peer-reviewed journal, International Immunopharmacology. The clinical study assessed immune changes in relation to the dose level and dosing schedule of PDS0301 (NHS-IL12), a novel investigational fusion protein consisting of a tumor-targeting antibody conjugated to Interleukin 12 (IL-12). The study also evaluated the correlation of several treatment-related immunological changes with clinical responses.

As described in the paper, titled, “Immune correlates with response in patients with metastatic solid tumors treated with a tumor-targeting immunocytokine NHS-IL12,” the researchers at the NCI evaluated a subset of 23 patients with advanced cancers who participated in a Phase 1 clinical trial of PDS0301. Patients were dosed every 2 weeks with PDS0301 at one of two levels – 12.0 mcg/kg and 16.8 mcg/kg – or every 4 weeks at 16.8 mcg/kg to identify dosing amounts and regimens of PDS0301 that correlate with higher levels of immune activation, including quantities of CD8 T cells, immune suppressive T regulatory cells, natural killer cells (NK) and natural killer T cells (NKT).

Patients receiving the higher dose of PDS0301 generated “a more robust immune activation compared to a lower dose,” including a greater expansion of NK, NKT, and CD8 T cells. Additionally, patients treated with the higher dose at two-week intervals had a greater response than patients receiving treatment every four weeks in the study. Importantly, greater increases were seen at the higher dose level in the serum pro-inflammatory cytokines IFNγ and TNFα, and soluble PD-1 (sPD-1). Studies found that increases in sPD-1 post-therapy have been associated with improved survival in various cancers and may indicate re-activation of CD8 T cells.

The ability to limit exposure of IL-12 in the circulating blood, and to increase its presence within the tumors constitutes a significant advancement in the development of cytokine-based immunotherapy. “The research published by the NCI demonstrates the potential of PDS0301 as a tumor-targeting IL-12 and its ability to stimulate immune activation and increase the frequency of CD8 T cells and certain NK cell subsets to potentially overcome the immunosuppressive tumor microenvironment,” stated Dr. Lauren V. Wood, Chief Medical Officer of PDS Biotech. “Importantly, this study appears to demonstrate the safety and tolerability of biologically active doses of PDS0301 and reports increases in specific immune cells that were associated with PDS0301 administration and improved clinical outcomes.”

The publication also summarizes clinical results from a study combining PDS0301, with a checkpoint inhibitor and PDS0101, PDS Biotech’s HPV-targeted immunotherapy that has been shown to promote induction of multifunctional, tumor-infiltrating killer T-cells. In this study in advanced HPV-positive anal, cervical, head and neck, vaginal, and vulvar cancers patients with checkpoint inhibitor refractory disease, 63% of patients who received the 16.8 mcg/kg dose had an objective response.

About PDS0301

PDS0301 is a novel investigational tumor-targeting Interleukin 12 (IL-12) that enhances the proliferation, potency and longevity of T cells in the tumor microenvironment. Together with Versamune® based immunotherapies PDS0301 works synergistically to promote a targeted T cell attack against cancers. PDS0301 is given by a simple subcutaneous injection. Clinical data suggest the addition of PDS0301 to Versamune® based immunotherapies may demonstrate significant disease control by shrinking tumors and/or prolonging survival in recurrent/metastatic cancers with poor survival prognosis.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, PDS0301, and Infectimune™ T cell-activating platforms. We believe our targeted Versamune® and PDS0301 based candidates have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to our currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; the success of the Company’s license agreements, including the potential for the clinical and nonclinical data available under the Company’s exclusive license agreement with Merck KGaA to aid in the development of the Versamune® platform; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control, including unforeseen circumstances or other disruptions to normal business operations arising from or related to COVID-19. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

MELVILLE, N.Y. – March 1, 2023– Comtech (NASDAQ: CMTL) today announced that it plans to release its second quarter fiscal 2023 results after the market closes on Thursday, March 9, 2023.

At 5:00 p.m. ET that day, Ken Peterman, Comtech’s Chief Executive Officer and President, will hold a conference call to discuss the Company’s second quarter fiscal 2023 results, operations, and business trends. A real-time webcast of the call will be available to the public at the investor relations section of the Comtech web site at www.comtech.com. Alternatively, investors can access the conference call by dialing (800) 225-9448 (domestic) or (203) 518-9708 (international) and using the conference I.D. of “Comtech.” A replay of the call will also be available by dialing (800) 839-3516 or (402) 220-7238 through Friday, March 24, 2023.

About Comtech

Comtech Telecommunications Corp. is a leading global technology company providing terrestrial and wireless network solutions, next-generation 9-1-1 emergency services, satellite and space communications technologies, and cloud native capabilities to commercial and government customers around the world. Our unique culture of innovation and employee empowerment unleashes a relentless passion for customer success. With multiple facilities located in technology corridors throughout the United States and around the world, Comtech leverages our global presence, technology leadership, and decades of experience to create the world’s most innovative communications solutions.For more information, please visit www.comtech.com.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

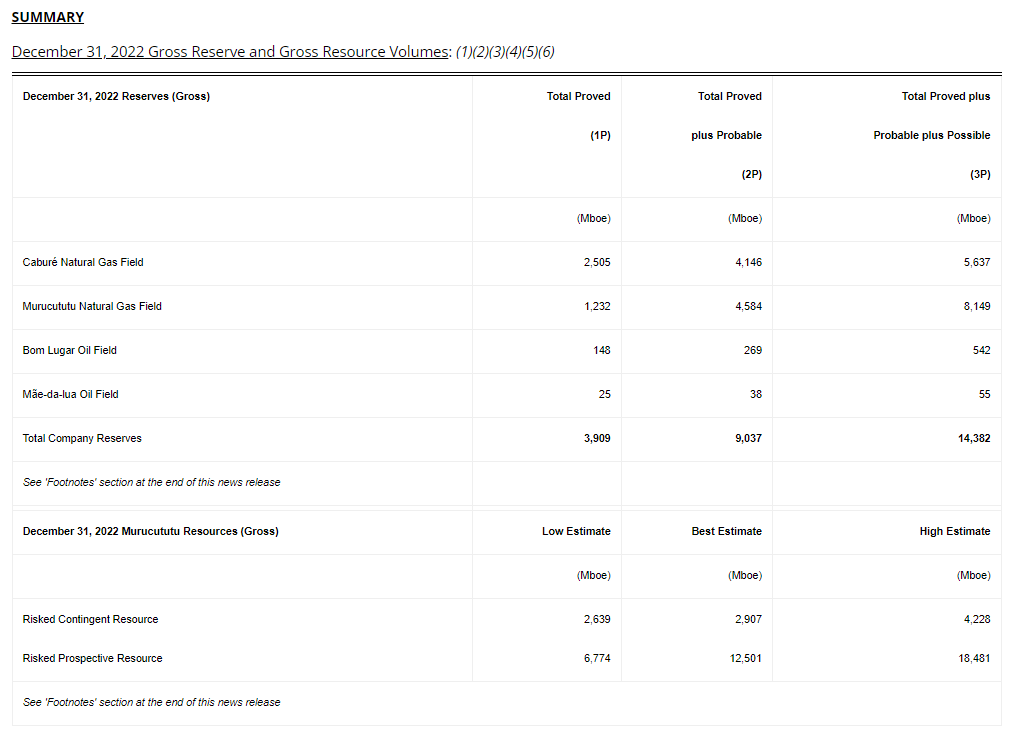

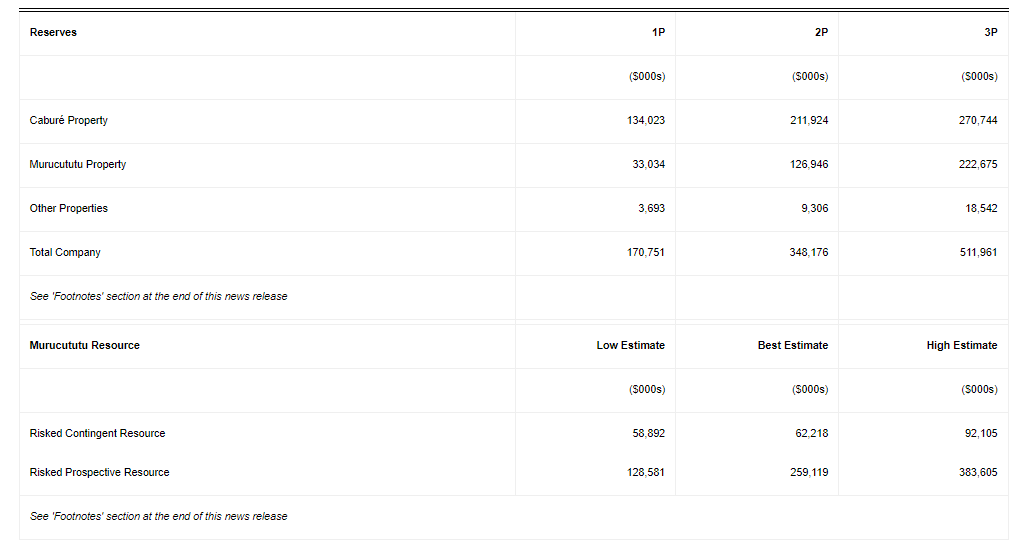

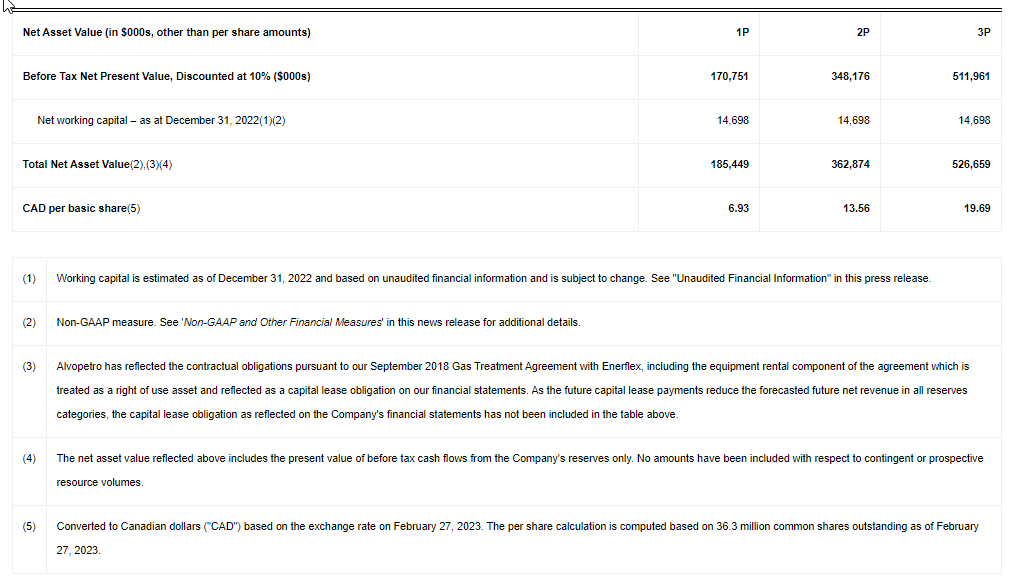

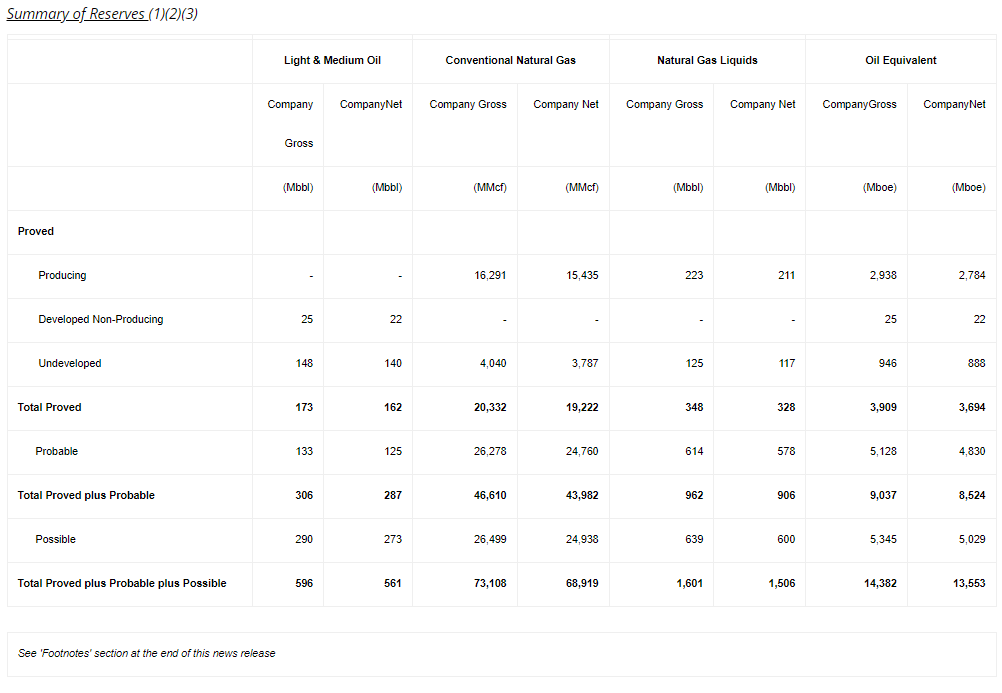

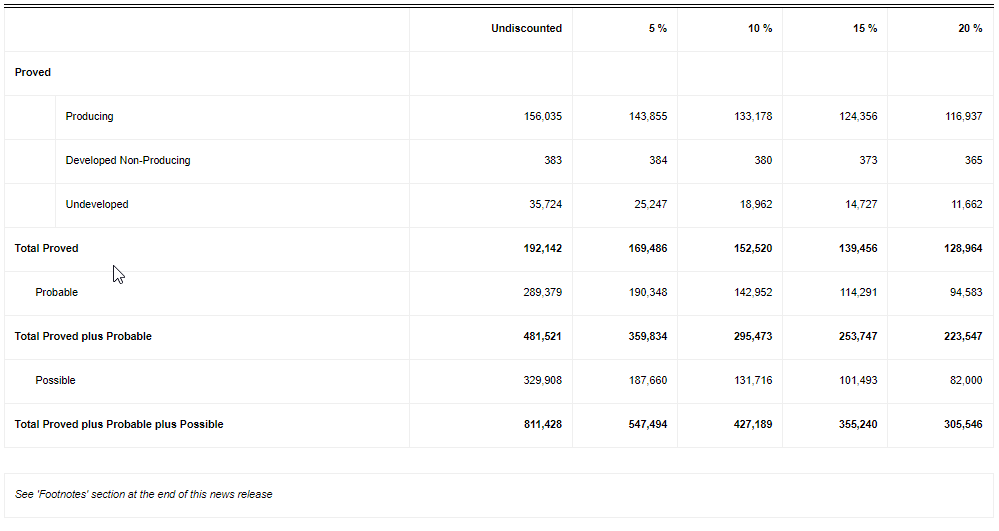

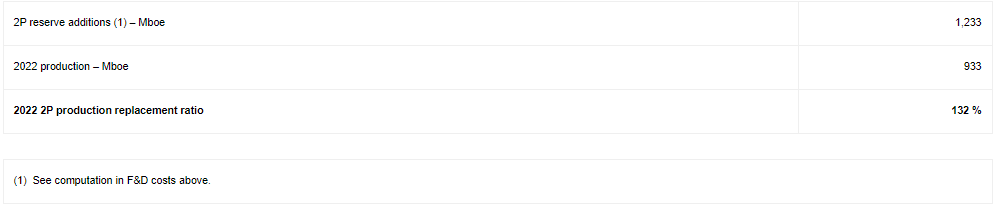

CALGARY, AB, Feb. 28, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces our reserves as at December 31, 2022 with total proved plus probable (“2P”) reserves of 9.0 MMboe and a before tax net present value discounted at 10% of $348.2 million. 2P reserve additions replaced 132% of 2022 production. 2P reserve volumes increased by 3%, despite 0.9 MMboe of production in 2022, due to reserve additions associated mainly with two additional Murucututu development locations (previously included in contingent resources). The before tax net present value of our 2P reserves (discounted at 10%) increased by 17% from December 31, 2021, due to reserve additions and increases in forecasted natural gas prices. Alvopetro also announces the December 31, 2022 assessment of the Company’s Murucututu natural gas resource with risked best estimate contingent resource of 2.9 MMboe and risked best estimate prospective resource of 12.5 MMboe. The Murucututu natural gas contingent and prospective resource values (risked best estimate net present value before tax, discounted at 10%) are $62.2 million and $259.1 million, respectively. The reserves and resources data set forth herein is based on an independent reserves and resources assessment and evaluation prepared by GLJ Ltd. (“GLJ”) dated February 27, 2023 with an effective date of December 31, 2022 (the “GLJ Reserves and Resources Report”).

All references herein to $ refer to United States dollars, unless otherwise stated.

December 31, 2022 GLJ Reserves and Resource Report Highlights

2P net present value before tax discounted at 10% increased 17% to $348.2 million.

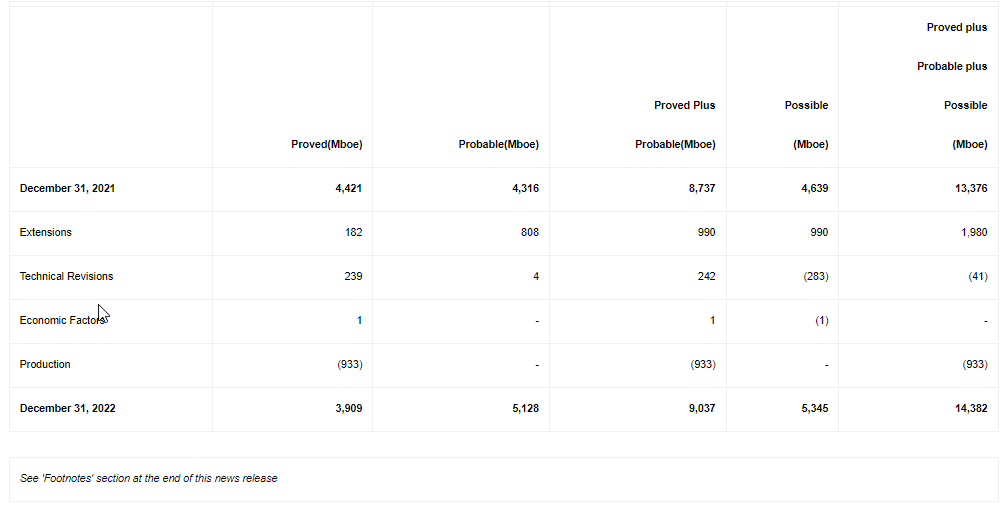

Proved reserves (“1P”) decreased 12% to 3.9 MMboe and 2P reserves increased 3% to 9.0 MMboe after 0.9 MMboe of production in 2022.

2P production replacement ratio(1) of 132%.

2P F&D costs(1) estimated at $28.66/boe.

2P recycle ratio(1) estimated at 2.1 times.

2P Net Asset Value(1) of CAD$13.56/share ($9.99/share) before any potential from contingent or prospective resources.

Risked best estimate contingent resource of 2.9 MMboe (NPV10 $62.2 million) and risked best estimate prospective resource of 12.5 MMboe (NPV10 $259.1 million).

Corey Ruttan, President and Chief Executive Officer, commented:

“Our 2022 year-end reserves and resource evaluations highlight the continued strong profitability from our Caburé natural gas field and the long-term potential of our Murucututu project. The increase in forecasted cash flows reflects the impact of reserve additions associated with our near-term development plans on our Murucututu asset and increases in forecasted natural gas prices under our long-term gas sales agreement. Our 2023 capital program is focused on lower risk development opportunities including accelerated activity on our Murucututu asset targeting the long-term natural gas potential of this field.”

(1)

Refer to the sections entitled “Oil and Natural Gas Advisories – Other Metrics” and “Non-GAAP and Other Financial Measures” for additional disclosures and assumptions used in calculating production replacement ratio, F&D costs, recycle ratio, net asset value and net asset value per share.

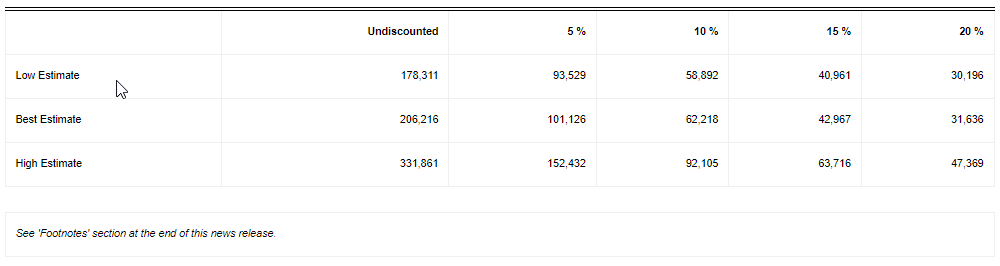

Net Present Value Before Tax Discounted at 10%:(1)(2)(3)(4)(5)(6)(7)(8)

NET ASSET VALUE

Following the December 31, 2022 reserves evaluation, based on the before tax net present value of Alvopetro’s 2P reserves (discounted at 10%), our total 2P net asset value is $362.9 million; CAD$13.56 per common share outstanding. Our 2P net asset value of $362.9 million is before including the before tax net present value (discounted at 10%) of our risked best estimate risked contingent resource of $62.2 million and our risked prospective resource of $259.1 million from the Murucututu natural gas field.

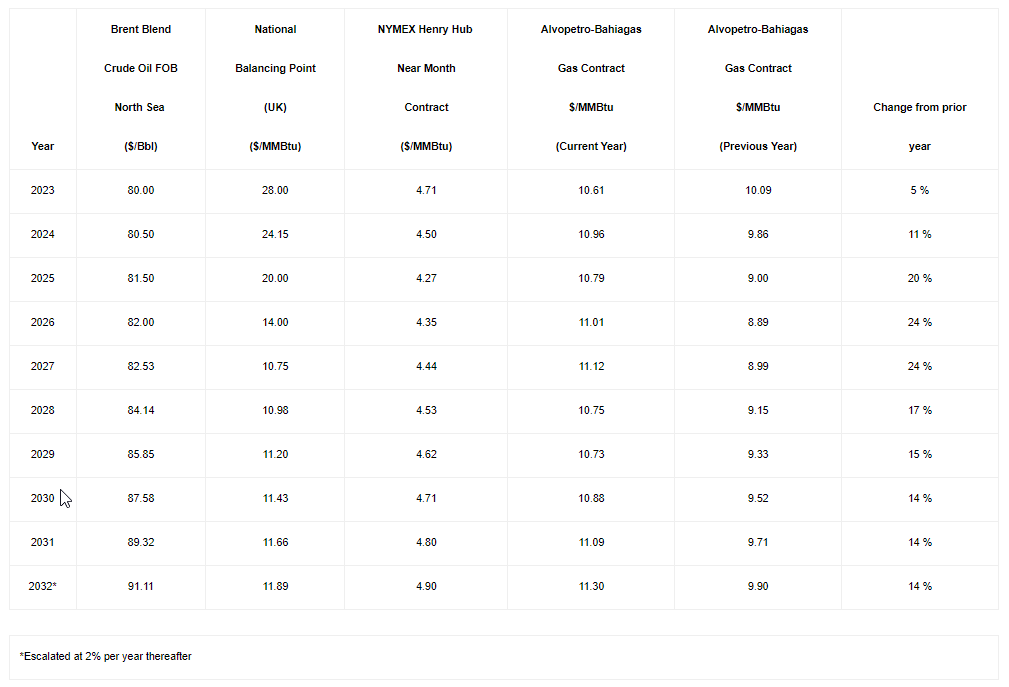

PRICING ASSUMPTIONS – FORECAST PRICES AND COSTS

GLJ employed the following pricing and inflation rate assumptions as of January 1, 2023 in the GLJ Reserves and Resources Report in estimating reserves and resources data using forecast prices and costs.

As of February 1, 2023, Alvopetro’s contracted natural gas price under the terms of our long-term gas sales agreement is based on the ceiling price within the contract and is forecasted to remain at the ceiling price until 2027. The ceiling price incorporates assumed US inflation of 3% in 2023 and 2% thereafter.

GLJ RESERVES AND RESOURCES REPORT

The GLJ Reserves and Resources Report has been prepared in accordance with the standards contained in the Canadian Oil and Gas Evaluation Handbook (“COGEH”) that are consistent with the standards of National Instrument 51-101 (“NI 51-101”). GLJ is a qualified reserves evaluator as defined in NI 51-101. The GLJ Reserves and Resources Report was an evaluation of all reserves of Alvopetro including our Caburé and Caburé Leste natural gas fields (collectively referred to as our Caburé natural gas field), our Murucututu natural gas project (previously referred to as Gomo), as well as our Bom Lugar and Mãe-da-lua oil fields. The GLJ Reserves and Resources Report also includes an evaluation of the gas resources of our Murucututu natural gas. In addition to the reserves assigned to our two existing Murucututu wells (197-1 and 183-1) and four additional development locations, contingent resource was assigned to the area in proximity to our existing Murucututu reserves, deemed to be discovered. The area mapped by 3D seismic west and north of the area defined as contingent was assigned prospective resource. Additional reserves and resources information as required under NI 51-101 will be included in the Company’s Annual Information Form for the 2022 fiscal year which will be filed on SEDAR by April 30, 2023.

December 31, 2022 Reserves Information:

Summary of Reserves (1)(2)(3)

Summary of Before Tax Net Present Value of Future Net Revenue – $000s(1)(2)(3)(7)(8)

Summary of After Tax Net Present Value of Future Net Revenue – $000s(1)(2)(3)(7)(8)

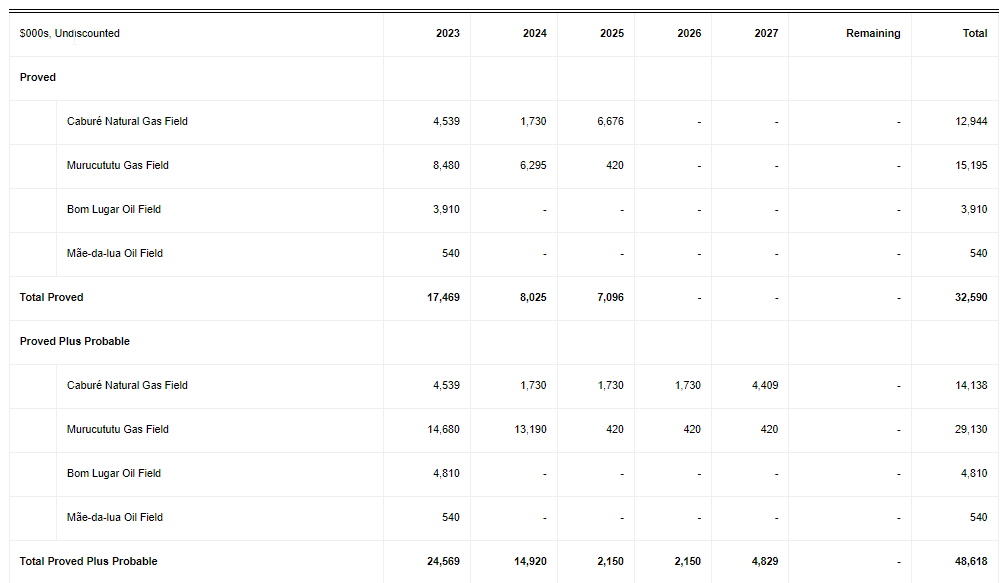

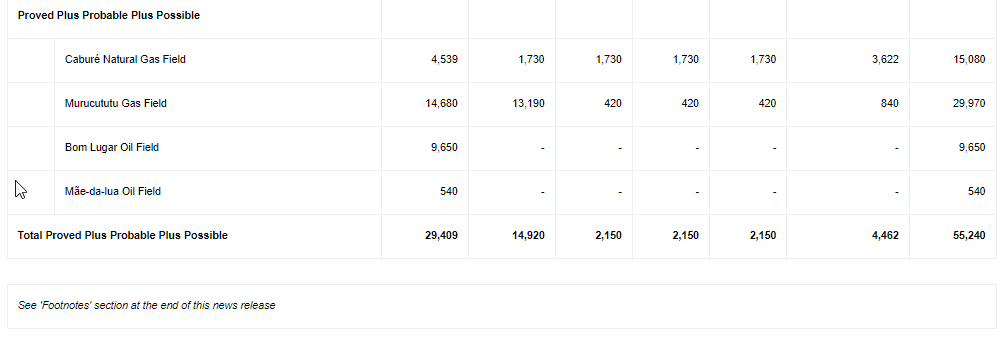

Future Development Costs (1)(2)(3)(7)(8)

The table below sets out the total development costs deducted in the estimation of future net revenue attributable to proved reserves, proved plus probable reserves and proved plus probable plus possible reserves (using forecast prices and costs), by field, in the GLJ Reserves and Resources Report. Total development costs include capital costs for drilling and facility and pipeline expenditures but excludes abandonment and reclamation costs.

Under each reserve category, Alvopetro has elected to reflect 100% of the contractual obligations pursuant to our Gas Treatment Agreement with Enerflex, including all operating, capital, and related financing costs for the full duration of the agreement. These costs are mainly attributable to the Caburé field and also represent the majority of the future development costs for the Caburé field in the table below. The future costs associated with equipment rental are also reflected as a capital lease obligation on our financial statements. Also included in future development costs for the Caburé field are two step-out wells and expansion of the unit facilities.

The future development costs for the Murucututu field in the proved category are for two development locations in the field and the stimulation of the 197(1) well. In the probable and possible categories, there are future development costs for two additional development locations. Also included in the Murucututu future development costs for all reserve categories are a portion of the anticipated contractual obligations associated with the expansion of the gas treatment facility. The future development costs for Bom Lugar in the proved category include costs for one development well and facilities upgrade. A second development well is included in the future development costs for the possible category for Bom Lugar. Future development costs at the Mãe-da-lua field relate to a stimulation of the existing producing well.

Reconciliation of Alvopetro’s Gross Reserves (Before Royalty) (1)(2)(3)(8)

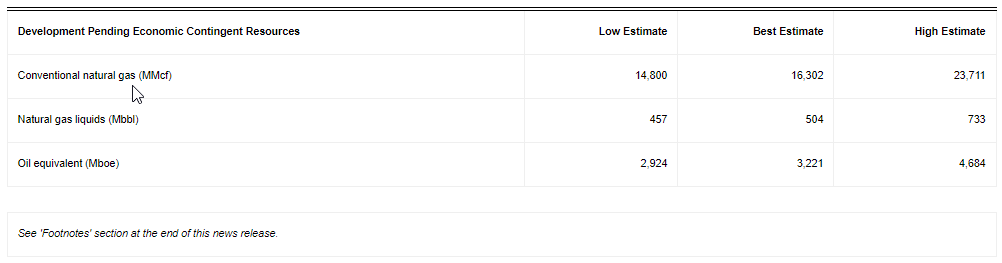

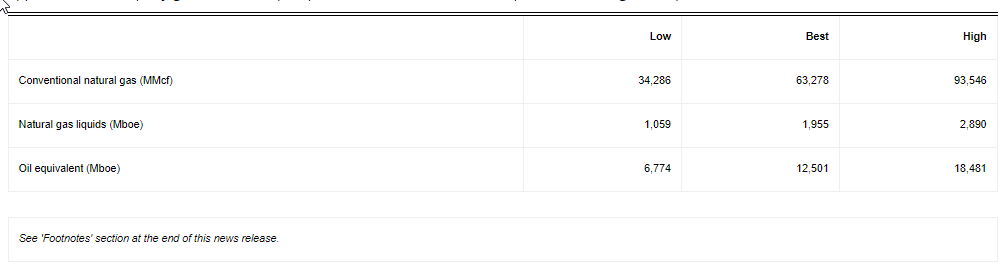

December 31, 2022 Murucututu Contingent Resources Information:

Summary of Unrisked Company Gross Contingent Resources (1)(2)(5)(6)

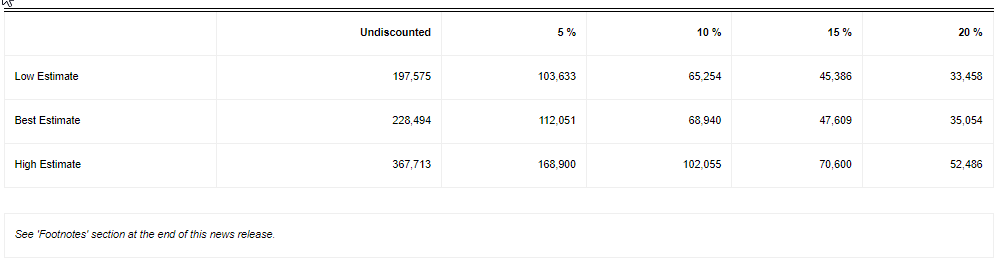

Summary of Before Tax Net Present Value of Future Net Revenue of Unrisked Contingent Resources- $000s (1)(2)(5)(6)(7)(8)

The GLJ Contingent Resource Report for Murucututu assumes capital deployment starting in 2024 for the drilling of wells with total project costs of $19.1 million and first commercial production in 2024. The information presented herein is based on company net project development costs. The recovery technology assumed for purposes of the estimate is based on established technologies utilized repeatedly in the industry.

There can be no certainty that the project will be developed on the timelines discussed herein. The project is based on a pre-development study. Development of the project is dependent on several contingencies as further described in this news release. Significant positive factors relevant to the estimate include existing production in close proximity, proximity to infrastructure, existing long-term gas sales agreement and corporate commitment to the project. Significant negative factors relevant to the estimate include reservoir performance and the economic viability of the project (with sensitivity to low commodity prices), access to and amount of capital required to develop resources at an acceptable cost, and regulatory approvals for planned activities including stimulations and new infrastructure developments.

Summary of Development Pending Risked Company Gross Contingent Resources(1)(2)(5)(6)

The GLJ Reserves and Resources Report estimates the Chance of Development as the product of two main contingencies associated with the project development, which are: 1) the probability of corporate sanctioning, which GLJ estimates at 95%; 2) the probability of finalization of a development plan, which GLJ estimates at 95%. The product of these two contingencies is 90%. As there is no risk related to discovery, the Chance of Commerciality for the contingent resource is therefore 90% which is the risk factor that has been applied to the Development Risked company gross contingent resources and the net present value figures reported below.

Summary of Development Pending Risked Before Tax Net Present Value of Future Net Revenue of Contingent Resources- $000s(1)(5)(6)(7)(8)

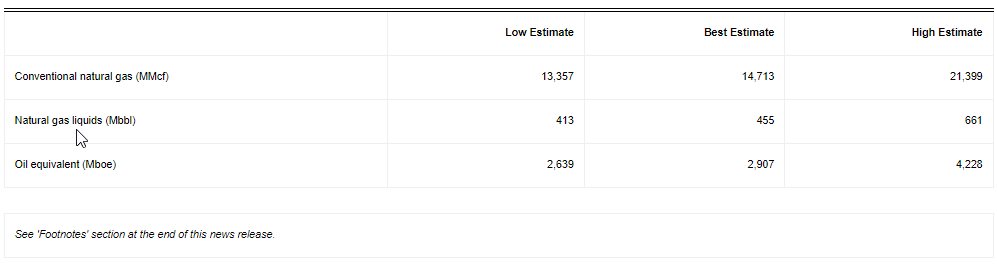

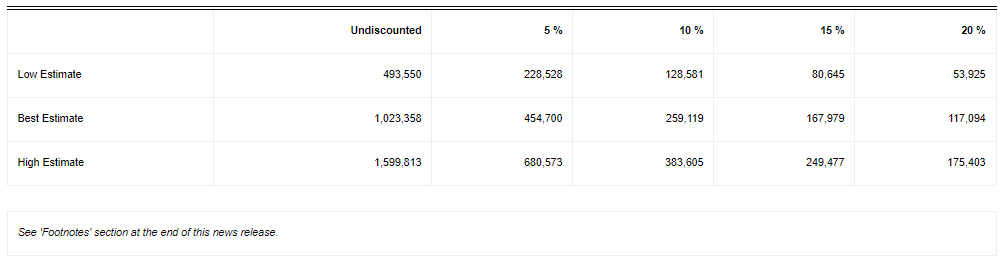

December 31, 2022 Murucututu Prospective Resources Information:

Summary of Unrisked Company Gross Prospective Resources (1)(2)(4)(6)

Summary of Before Tax Net Present Value of Future Net Revenue of Unrisked Prospective Resources – $000s (1)(4)(6)(7)(8)

The GLJ Reserves and Resources Report for Murucututu prospective resources assumes capital deployment starting in 2025 for the drilling of wells, expansion of field facilities, and additional pipeline capacity, with total project costs of $70.0 million and first commercial production in 2025. The information presented herein is based on company project development costs. The recovery technology assumed for purposes of the estimate is based on established technologies utilized repeatedly in the industry.

There can be no certainty that the project will be developed on the timelines discussed herein. Development of the project is dependent on several contingencies as further described in this news release. The project is based on a conceptual study. Significant positive factors relevant to the estimate include existing production in close proximity, proximity to infrastructure, existing long-term gas sales agreement and corporate commitment to the project. Significant negative factors relevant to the estimate include reservoir performance and the economic viability of the project (with sensitivity to low commodity prices), access to and amount of capital required to develop resources at an acceptable cost, and regulatory approvals for planned activities including stimulations and new infrastructure developments.

Summary of Development Risked Company Gross Prospective Resources(1)(2)(4)(6)

The GLJ Reserves and Resources Report estimates the Chance of Commerciality as the product between the Chance of Discovery and the Chance of Development. The Chance of Discovery of the prospective resources has been assessed at 90%, while the Chance of Development has been assessed as the same as for the Contingent Resources described above at 90%. The resulting Chance of Commerciality is 81%, which has been applied to the company gross unrisked prospective resources and the net present value figures reported below.

Summary of Development Risked Before Tax Net Present Value of Future Net Revenue of Prospective Resources- $000s(1)(4)(6)(7)(8)

UPCOMING 2022 RESULTS AND LIVE WEBCAST

Alvopetro anticipates announcing its 2022 fourth quarter and year-end results on March 21, 2023 after markets close and will host a live webcast to discuss the results at 9:00 am Mountain time, on March 22, 2023. Details for joining the event are as follows:

The webcast will include a question and answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to socialmedia@alvopetro.com.

CORPORATE PRESENTATION

Alvopetro’s updated corporate presentation is available on our website at:

References to Company Gross reserves or Company Gross Resources means the total working interest share of remaining recoverable reserves or resources held by Alvopetro before deductions of royalties payable to others and without including any royalty interests held by Alvopetro.

(2)

The tables above are a summary of the reserves of Alvopetro and the net present value of future net revenue attributable to such reserves as evaluated in the GLJ Reserves and Resources Report based on forecast price and cost assumptions. The tables summarize the data contained in the GLJ Reserves and Resources Report and as a result may contain slightly different numbers than such report due to rounding. Also due to rounding, certain columns may not add exactly.

(3)

Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

(4)

Prospective Resources are defined in the COGE Handbook as those quantities of petroleum estimated, as of a given date, to be potentially recoverable from undiscovered accumulations by application of future development projects. Prospective resources have both an associated chance of discovery and a chance of development. There is no certainty that any portion of the prospective resources will be discovered and even if discovered, there is no certainty that it will be commercially viable to produce any portion. Prospective Resources are further subdivided in accordance with the level of certainty associated with recoverable estimates assuming their discovery as described in footnote 11.

(5)

Contingent Resources are defined in the COGE Handbook as those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but are not currently considered to be commercially recoverable due to one or more contingencies. Contingencies may include factors such as economic, legal, environmental, political and regulatory matters or a lack of markets. It is also appropriate to classify as contingent resources the estimated discovered recoverable quantities associated with a project in the early evaluation stage. Contingent Resources are further classified in accordance with the level of certainty associated with the estimates as described in footnote 11 and may be subclassified based on project maturity and/or characterized by their economic status. The Contingent Resources estimated in the GLJ Reserves and Resources Report are classified as “economic contingent resources”, which are those contingent resources that are currently economically recoverable. All such resources are further sub-classified with a project status of “development pending”, meaning that resolution of the final conditions for development are being actively pursued. The recovery estimates of the Company’s contingent resources provided herein are estimates only and there is no guarantee that the estimated resources will be recovered. There is uncertainty that it will be commercially viable to produce any portion of the resources. Actual recovered resource may be greater than or less than the estimates provided herein.

(6)

Low Estimate: This is considered to be a conservative estimate of the quantity that will actually be recovered. It is likely that the actual remaining quantities recovered will exceed the low estimate. If probabilistic methods are used, there should be at least a 90 percent probability (P90) that the quantities actually recovered will equal or exceed the low estimate.Best Estimate: This is considered to be the best estimate of the quantity that will actually be recovered. It is equally likely that the actual remaining quantities recovered will be greater or less than the best estimate. If probabilistic methods are used, there should be at least a 50 percent probability (P50) that the quantities actually recovered will equal or exceed the best estimate.High Estimate: This is considered to be an optimistic estimate of the quantity that will actually be recovered. It is unlikely that the actual remaining quantities recovered will exceed the high estimate. If probabilistic methods are used, there should be at least a 10 percent probability (P10) that the quantities actually recovered will equal or exceed the high estimate.

(7)

The net present value of future net revenue attributable to Alvopetro’s reserves and resources are stated without provision for interest costs and general and administrative costs, but after providing for estimated royalties, production costs, development costs, other income, future capital expenditures, well abandonment and reclamation costs for only those wells assigned reserves and material dedicated gathering systems and facilities. The net present values of future net revenue attributable to Alvopetro’s reserves and resources estimated by GLJ do not represent the fair market value of those reserves. Other assumptions and qualifications relating to costs, prices for future production and other matters are summarized herein. The recovery and reserve and resource estimates of the Company’s reserves and resources provided herein are estimates only and there is no guarantee that the estimated reserves and resources will be recovered. Actual reserves and resources may be greater than or less than the estimates provided herein.

(8)

GLJ’s January 1, 2023 escalated price forecast is used in the determination of future gas sales prices under Alvopetro’s long-term gas sales agreement and for all forecasted oil sales and natural gas liquids sales. See https://www.gljpc.com/sites/default/files/pricing/Jan23.pdf for GLJ’s price forecast.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this news release are in United States dollars, except as otherwise noted.

Abbreviations:

1P = proved reserves2P = proved plus probable reserves3P = proved plus probable plus possible reservesCAD = Canadian dollarsF&D = finding and development costsFDC = future development costs;Mbbl = thousands of barrelsMboe = thousand barrels of oil equivalentMMbtu = million British Thermal UnitsMMcf = million cubic feetMMcf/d = million cubic feet per dayMMboe = million barrels of oil equivalent$000s = thousands of U.S. dollars

Oil and Natural Gas Advisories

Oil and Natural Gas Reserves

The disclosure in this news release summarizes certain information contained in the GLJ Reserves and Resources Report but represents only a portion of the disclosure required under NI 51-101. Full disclosure with respect to the Company’s reserves as at December 31, 2022 will be included in the Company’s annual information form for the year ended December 31, 2022 which will be filed on SEDAR (www.sedar.com) on or before April 30, 2023. All net present values in this press release are based on estimates of future operating and capital costs and GLJ’s forecast prices as of December 31, 2022. The reserves definitions used in this evaluation are the standards defined by COGEH reserve definitions and are consistent with NI 51-101 and used by GLJ. The net present values of future net revenue attributable to the Alvopetro’s reserves estimated by GLJ do not represent the fair market value of those reserves. Other assumptions and qualifications relating to costs, prices for future production and other matters are summarized herein. The recovery and reserve estimates of the Company’s reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual reserves may be greater than or less than the estimates provided herein. Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

Contingent Resources

This news release discloses estimates of Alvopetro’s contingent resources and the net present value associated with net revenues associated with the production of such contingent resources as included in the GLJ Reserves and Resources Report. There is no certainty that it will be commercially viable to produce any portion of such contingent resources and the estimated future net revenues do not necessarily represent the fair market value of such contingent resources. Estimates of contingent resources involve additional risks over estimates of reserves. Full disclosure with respect to the Company’s contingent resources as at December 31, 2022 will be contained in the Company’s annual information form for the year ended December 31, 2022 which will be filed on SEDAR (www.sedar.com) on or before April 30, 2023.

Prospective Resources

This news release discloses estimates of Alvopetro’s prospective resources included in the GLJ Reserves and Resources Report. There is no certainty that any portion of the prospective resources will be discovered and even if discovered, there is no certainty that it will be commercially viable to produce any portion. Estimates of prospective resources involve additional risks over estimates of reserves. The accuracy of any resources estimate is a function of the quality and quantity of available data and of engineering interpretation and judgment. While resources presented herein are considered reasonable, the estimates should be accepted with the understanding that reservoir performance subsequent to the date of the estimate may justify revision, either upward or downward. Full disclosure with respect to the Company’s prospective resources as at December 31, 2022 will be contained in the Company’s annual information form for the year ended December 31, 2022 which will be filed on SEDAR (www.sedar.com) on or before April 30, 2023.

Boe Disclosure

The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Other Metrics

This press release contains metrics commonly used in the oil and natural gas industry, which have been prepared by management, including “F&D costs”, “net asset value”, “net asset value per share”, “operating netback per boe”, “production replacement ratio” and “recycle ratio”. These terms do not have a standardized meaning and may not be comparable to similar measures presented by other companies, and therefore should not be used to make such comparisons.

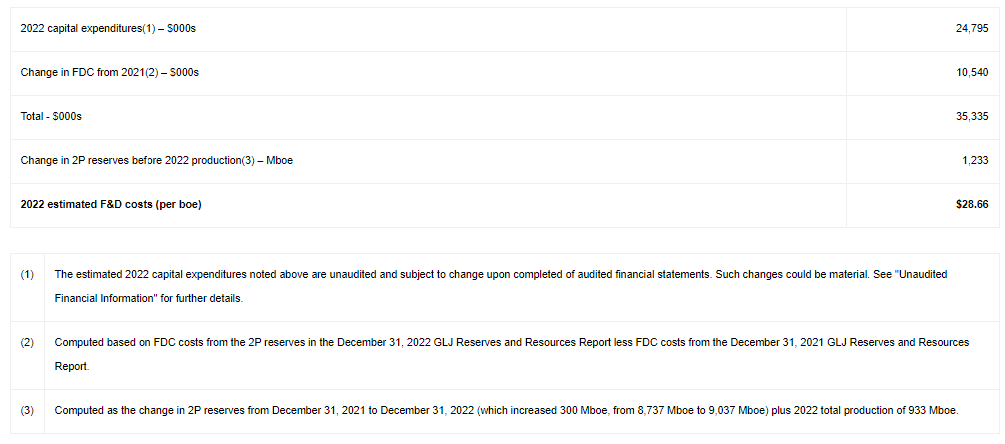

“F&D costs” are reflected on a per barrel of oil equivalent and are calculated as the sum of capital expenditures in the current year plus the change in FDC for the period, divided by the change in reserves in the period, before current year production. The estimated 2022 F&D costs are computed as follows:

“Net asset value” is based on the before tax net present value of the Company’s reserves as at December 31, 2022, discounted at 10% plus the Company’s net working capital balance estimated as of December 31, 2022. Net working capital is a capital management measure. See “Non-GAAP and Other Financial Measures” below for further details. The estimated net working capital as of December 31, 2022 is unaudited and subject to change upon completion of audited financial statements for the year-ended December 31, 2022. Such changes could be material. See “Unaudited Financial Information” for further details.

“Net asset value per share” is based on the computation of net asset value divided by basic shares outstanding of 36,311,579 adjusted to Canadian dollars based on the foreign exchange rate on February 27, 2023.

“Operating netback per boe” is a non-GAAP financial measure and operating netback per boe is a non-GAAP financial ratio. See “Non-GAAP and Other Financial Measures” below for further details. Alvopetro’s operating netback for the year ended December 31, 2022 is estimated at $59.43 per boe. This estimate is based on unaudited financial information and subject to change upon completion of audited financial statements for the year-ended December 31, 2022. Such changes could be material. See “Unaudited Financial Information” for further details.

“Production replacement ratio” is calculated as total reserve additions divided by current year production. Alvopetro’s 2P production replacement ratio in 2022 is calculated as:

“Recycle ratio” is calculated by dividing the estimated 2022 operating netback by estimated F&D costs per boe for the year. The Company’s estimated 2022 recycle ratio is calculated as follows:

Management uses these oil and gas metrics for its own performance measurements and to provide shareholders with measures to compare our operations over time. Readers are cautioned that the information provided by these metrics, or that can be derived from the metrics presented in this press release, should not be relied upon for investment or other purposes.

Forward-Looking Statements and Cautionary Language

This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning plans relating to the Company’s operational activities, proposed development activities and the timing for such activities, capital spending levels and future capital costs, the expected natural gas price, gas sales and gas deliveries under Alvopetro’s long-term gas sales agreement. The forward-looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning the timing of regulatory licenses and approvals, equipment availability, the success of future drilling, completion, testing, recompletion and development activities, the performance of producing wells and reservoirs, well development and operating performance, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, the outlook for commodity markets and ability to access capital markets, foreign exchange rates, general economic and business conditions, the impact of the COVID-19 pandemic, weather and access to drilling locations, the availability and cost of labour and services, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Unaudited Financial Information

Certain financial and operating information included in this news release for the year ended December 31, 2022 including, without limitation, 2022 capital expenditures and the impact on F&D costs, working capital, recycle ratio and operating netback, are based on estimated unaudited financial results for the year then ended, and are subject to the same limitations as discussed under Forward Looking Statements and Cautionary Language set out in this news release. These estimated amounts may change upon the completion of audited financial statements for the year ended December 31, 2022 and changes could be material.

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this news release should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s most recent MD&A which may be accessed through the SEDAR website at www.sedar.com .

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback (a non-GAAP financial measure calculated as natural gas, oil and condensate revenues less royalties and production expenses) divided by total sales volumes (barrels of oil equivalent). More details on the method of calculation is provided in the “Operating Netback per boe” section of the Company’s MD&A. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe). The Company’s operating netback per boe is estimated at $59.43 per boe for the year ended December 31, 2022. This amount is unaudited and subject to change as further discussed in the section “Unaudited Financial Information”.

Capital Management Measures

Net Working Capital

Net working capital is computed as current assets less current liabilities. Net working capital is a measure of liquidity, is used to evaluate financial resources. The Company’s net working capital as of December 31, 2022 is estimated at $14.7 million. This amount is unaudited and subject to change as further discussed in the section “Unaudited Financial Information”.

Boca Raton, FL, March 1, 2023 (GLOBE NEWSWIRE) — In a joint statement, Noble Capital Markets, Inc. (“Noble”) and Florida Atlantic University announced today that NobleCon19 – Noble’s 19th Annual Small Cap Investor Conference – will be held at the University’s College of Business Executive Education facility, Dec. 3-5, 2023, in Boca Raton, Florida. The 52,000 square foot, state-of-the-art facility was opened August 2020.

Noble has worked with the University for over a decade and was instrumental in the development of their Financial Analyst Program, and Noble’s Intern Program has generated great assets with graduates from the University. “We are extremely proud of our long-standing relationship with Florida Atlantic University,” said Nico Pronk, Noble’s President & CEO. “This new collaboration certainly elevates it to a whole new level.”

Vegar Wiik, Executive Director of the College of Business, Executive Education agrees, stating “Our vision for the College and this magnificent structure is to effectively integrate our curriculum with established businesses. Daniel Gropper, dean of FAU’s College of Business, said the financial industry is an important, integral part of the economy. “I can’t think of a better way to expose our students to the importance of emerging growth companies than to have 100 plus executive teams in the halls of our campus,” he said.

The entire College of Business Executive Education facility will transform into NobleCon19. Each presentation room will accommodate investors, in tiered seating with personal monitors. High-definition cameras, full-room microphones (to capture audience questions), three large screens, and full webcasting capabilities will offer the most technologically advanced conference environment on the circuit. Attendees will also experience similarly equipped rooms for panel presentations, private breakouts, and meetings, and in large gathering spaces, both indoors and out, as well as 800 free covered parking spaces. Florida Atlantic University is centrally located in Boca Raton, off I-95, only minutes from the Boca Raton Airport, and less than half an hour from Fort Lauderdale International Airport. Privaira, located at Boca Raton Airport is the official private air charter company for NobleCon19. A wide range of hotel accommodations are available within a five-mile radius, from economy to the ultra-luxurious “The Boca Raton.” Noble will be working with several properties to offer NobleCon19 attendees discounted rates.

The format of NobleCon will include company presentations followed by fire-side chats with Noble analysts, and select one-on-one meetings for qualified investors only, as well as several industry panel presentations. On the networking side, Noble is planning for informative keynote speakers and live entertainment, in an effort expand the business day in a more casual, conversational environment. All company presentations and panel discussions will be digitally streamed and made available exclusively on www.channelchek.com – Noble’s proprietary investment community portal.

Who should attend? Public companies from any business sector with market capitalizations of below $3-4 billion. Private companies planning a capital raise, considering becoming public, or an M&A event. NobleCon19 will suit every level of investor; high net worth individuals, family offices, self-directed investors, private equity, RIAs, financial advisors, equity analysts, and institutional investors. www.NobleCon19.com

About Florida Atlantic University

Florida Atlantic University, established in 1961, officially opened its doors in 1964 as the fifth public university in Florida. Today, the University serves more than 30,000 undergraduate and graduate students across six campuses located along the southeast Florida coast. In recent years, the University has doubled its research expenditures and outpaced its peers in student achievement rates. Through the coexistence of access and excellence, FAU embodies an innovative model where traditional achievement gaps vanish. FAU is designated a Hispanic-serving institution, ranked as a top public university by U.S. News & World Report and a High Research Activity institution by the Carnegie Foundation for the Advancement of Teaching. For more information, visit www.fau.edu.

About Noble Capital Markets

Noble Capital Markets, Inc. was incorporated in 1984 as a full-service SEC / FINRA registered broker-dealer, dedicated exclusively to serving underfollowed emerging growth companies through investment banking, wealth management, trading & execution, and equity research activities. Over the past 39 years, Noble has raised billions of dollars for companies and published more than 45,000 equity research reports. www.noblecapitalmarkets.comcontact@noblecapitalmarkets.com

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Weaker than expected Yauricocha financial results. Sierra Metals’ subsidiary Sociedad Minera Corona S.A, whose principal asset is the Yauricocha mine in Peru, recently filed its financial results for the fourth quarter and full year 2022. Fourth quarter and full year EBITDA were $(6.1) million and $14.2 million, respectively, compared with $19.0 million and $88.0 million during the prior year periods. Recall Sierra holds an 81.8% interest in Corona whose financial results have not been adjusted for the 18.2% non-controlling interest.

Lowering estimates. We have lowered our fourth quarter and full year 2022 EBITDA and EPS estimates to reflect weaker than expected performance at the Yauricocha mine in Peru. We forecast fourth quarter EBITDA and EPS of $(3.5) million and $(0.07), respectively, compared to our previous estimates of $0.4 million and $(0.05). For the full year, we project EBITDA of $10.0 million and a loss per share of $(0.17) compared with our previous estimates of $13.9 million and $(0.15), respectively. Our 2023 EBITDA and EPS estimates remain unchanged at $37.3 million and $(0.04). While our quarterly estimates reflect steady improvement, operational uncertainty associated with production at the company’s mines clouds our confidence in 2023 estimates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product, Covaxin, is a killed-virus vaccine for COVID-19 in-licensed from Bharat Biotech (India). The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Financial Results Were Within Expectations. Ocugen reported 4Q22 and FY2022 Net Loss of $21.9 million or $(0.10) per share, and $81.4 million or $(0.38) per share for FY2022. Cash on hand as of December 31 was $90.9 million or $0.41 per share, which management projects will fund operations through 1Q24. On its quarterly conference call, management discussed recent milestones and development programs in gene therapy, cellular therapy, and vaccines.

Ophthalmology Programs Are Advancing. Ocugen filed an IND for OCU200 to begin Phase 1 clinical trial in diabetic macular edema (DME), meeting the expected timeframe. Trial enrollment is expected to begin in 2Q23. A second IND filing is expected during 2Q23 for OCU410 in dry AMD and OCU410ST in Stargardt disease. The Phase 1/2 dose testing OCU400 in retinitis pigmentosa (RP) escalation phase previously completed enrollment for the RP cohort, with enrollment continuing in the Leber congenital amaurosis (LCA) patient cohort. Phase 3 is expected to start by year-end 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Favorable crushing and grinding test results. Defense Metals reported favorable crushing and grinding (comminution) results using multiple samples extracted from the Wicheeda deposit. The results will help determine the design of the crushing and grinding plant which will be included in the company’s Wicheeda REE project preliminary feasibility study (PFS) that is expected to be completed in the first quarter of 2024.

The importance of starting off right. Crushing and grinding is the first step in processing mined material where ore is reduced to sand-like particles suitable for upgrading by flotation or other means. It accounts for a fairly significant percentage of the mineral processing plant energy requirements, production cost, and carbon emission profile.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile application. Codere currently operates in its core markets of Spain, Italy, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence in the region.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q4, better than expected. The company reported year-over-year Q4 net gaming revenue growth of 70% to €37.7 million, illustrated in Figure #1 Q4 Results. The quarterly revenue growth marked an acceleration compared with Q3 revenue growth of 54%. Notably, full-year net gaming revenue of €123 million was better than guidance of €115 million to €120 million.

CEO change, strong management bench. The company announced that Moshe Edree will step down as CEO and begin serving as Executive Vice Chairman. Aviv Sher is assuming the role of CEO, having previously served as the company’s COO. Mr. Sher has worked in the industry for more than 15 years.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Most vaccines, from measles to Covid-19, require a series of multiple shots before the recipient is considered fully vaccinated. To make that easier to achieve, MIT researchers have developed microparticles that can be tuned to deliver their payload at different time points, which could be used to create “self-boosting” vaccines.

In a new study, the researchers describe how these particles degrade over time, and how they can be tuned to release their contents at different time points. The study also offers insights into how the contents can be protected from losing their stability as they wait to be released.

Using these particles, which resemble tiny coffee cups sealed with a lid, researchers could design vaccines that would need to be given just once, and would then “self-boost” at a specified point in the future. The particles can remain under the skin until the vaccine is released and then break down, just like resorbable sutures.

This type of vaccine delivery could be particularly useful for administering childhood vaccinations in regions where people don’t have frequent access to medical care, the researchers say.

“This is a platform that can be broadly applicable to all types of vaccines, including recombinant protein-based vaccines, DNA-based vaccines, even RNA-based vaccines,” says Ana Jaklenec, a research scientist at MIT’s Koch Institute for Integrative Cancer Research. “Understanding the process of how the vaccines are released, which is what we described in this paper, has allowed us to work on formulations that address some of the instability that could be induced over time.”

This approach could also be used to deliver a range of other therapeutics, including cancer drugs, hormone therapy, and biologic drugs, the researchers say.

Jaklenec and Robert Langer, the David H. Koch Institute Professor at MIT and a member of the Koch Institute, are the senior authors of the new study, which appears today in Science Advances. Morteza Sarmadi, a research specialist at the Koch Institute and recent MIT PhD recipient, is the lead author of the paper.

Staggered Drug Release

The researchers first described their new microfabrication technique for making these hollow microparticles in a 2017 Science paper. The particles are made from PLGA, a biocompatible polymer that has already been approved for use in medical devices such as implants, sutures, and prosthetic devices.

To create cup-shaped particles, the researchers create arrays of silicon molds that are used to shape the PLGA cups and lids. Once the array of polymer cups has been formed, the researchers employed a custom-built, automated dispensing system to fill each cup with a drug or vaccine. After the cups are filled, the lids are aligned and lowered onto each cup, and the system is heated slightly until the cup and lid fuse together, sealing the drug inside.

This technique, called SEAL (StampEd Assembly of polymer Layers), can be used to produce particles of any shape or size. In a paper recently published in the journal Small Methods, lead author Ilin Sadeghi, an MIT postdoc, and others created a new version of the technique that allows for simplified and larger-scale manufacturing of the particles.

In the new Science Advances study, the researchers wanted to learn more about how the particles degrade over time, what causes the particles to release their contents, and whether it might be possible to enhance the stability of the drugs or vaccines carried within the particles.

“We wanted to understand mechanistically what’s happening, and how that information can be used to help stabilize drugs and vaccines and optimize their kinetics,” Jaklenec says.

Their studies of the release mechanism revealed that the PLGA polymers that make up the particles are gradually cleaved by water, and when enough of these polymers have broken down, the lid becomes very porous. Very soon after these pores appear, the lid breaks apart, spilling out the contents.

“We realized that sudden pore formation prior to the release time point is the key that leads to this pulsatile release,” Sarmadi says. “We see no pores for a long period of time, and then all of a sudden we see a significant increase in the porosity of the system.”

The researchers then set out to analyze how a variety of design parameters, include the size and shape of the particles and the composition of the polymers used to make them, affect the timing of drug release.

To their surprise, the researchers found that particle size and shape had little effect on drug release kinetics. This sets the particles apart from most other types of drug delivery particles, whose size plays a significant role in the timing of drug release. Instead, the PLGA particles release their payload at different times based on differences in the composition of the polymer and the chemical groups attached the ends of the polymers.

“If you want the particle to release after six months for a certain application, we use the corresponding polymer, or if we want it to release after two days, we use another polymer,” Sarmadi says. “A broad range of applications can benefit from this observation.”

Stabilizing the Payload

The researchers also investigated how changes in environmental pH affect the particles. When water breaks down the PLGA polymers, the byproducts include lactic acid and glycolic acid, which make the overall environment more acidic. This can damage the drugs carried within the particles, which are usually proteins or nucleic acids that are sensitive to pH.

In an ongoing study, the researchers are now working on ways to counteract this increase in acidity, which they hope will improve the stability of the payload carried within the particles.

To help with future particle design, the researchers also developed a computational model that can take many different design parameters into account and predict how a particular particle will degrade in the body. This type of model could be used to guide the development of the type of PLGA particles that the researchers focused on in this study, or other types of microfabricated or 3D-printed particles or medical devices.

The research team has already used this strategy to design a self-boosting polio vaccine, which is now being tested in animals. Usually, the polio vaccine has to be given as a series of two to four separate injections.

“We believe these core shell particles have the potential to create a safe, single-injection, self-boosting vaccine in which a cocktail of particles with different release times can be created by changing the composition. Such a single injection approach has the potential to not only improve patient compliance but also increase cellular and humoral immune responses to the vaccine,” Langer says.

This type of drug delivery could also be useful for treating diseases such as cancer. In a 2020 Science Translational Medicine study, the researchers published a paper in which they showed that they could deliver drugs that stimulate the STING pathway, which promotes immune responses in the environment surrounding a tumor, in several mouse models of cancer. After being injected into tumors, the particles delivered several doses of the drug over several months, which inhibited tumor growth and reduced metastasis in the treated animals.

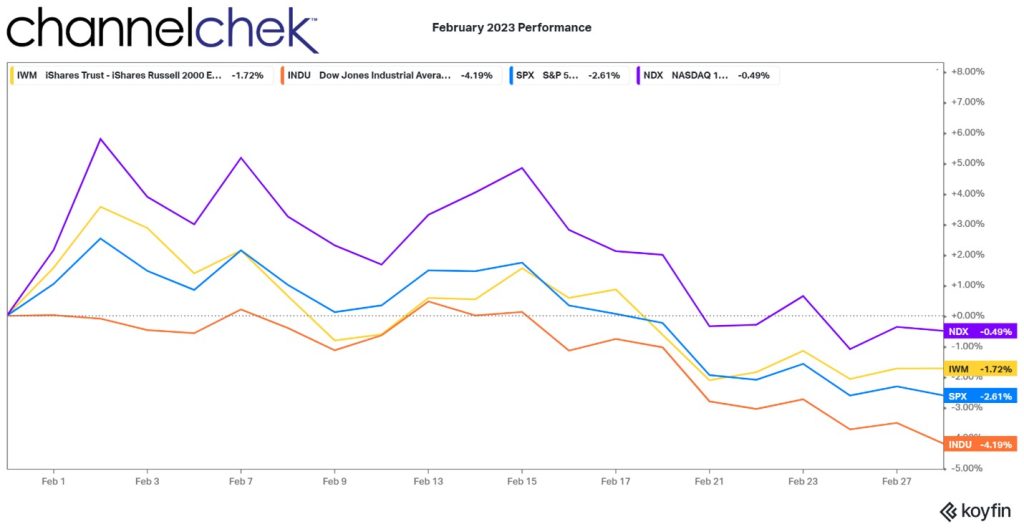

Stock Market Performance – Looking Back at February, Forward to March

The months seem to go by quickly. And as satisfying as January was for most stock market investors, February left people with 2022 flashbacks. High inflation, or what more inflation could mean for monetary policy, again was the culprit weighing on investors’ minds and account values. One consideration is that investors are now entering March and are faced with very negative sentiment. This could actually be bullish and may lead the major indexes on a wave upward.

The next scheduled FOMC meeting is March 21-22. By then, we will have seen another round of inflation numbers as CPI (March 14) and the PCE index (March 15) are both released during the same week, otherwise known as the ides of March. While the Fed is wrestling with stubborn inflation, it is keeping an eye on the strong labor markets. Although low unemployment is desirable, tight labor markets are helping to drive prices up. The Fed is looking to find a better balance.

The three broad stock market indices (S&P 500, Nasdaq 100, and Russell 2000) are positive on the year, the Dow went negative on the 21st of February. The Nasdaq 100 and Russell 2000 have gained 9.70% and 8.22% respectively year-to-date, while the S&P is a positive 3.21% and the Dow Industrials is a negative 1.45%.

Each of the four closely watched indexes shown above began falling off as soon as January ended. It has only totalled a partial reversal, but the overall negative sentiment rose through February.

Viewing the indices from a year-to-date perspective, all but the Dow are well above their historical average pace.

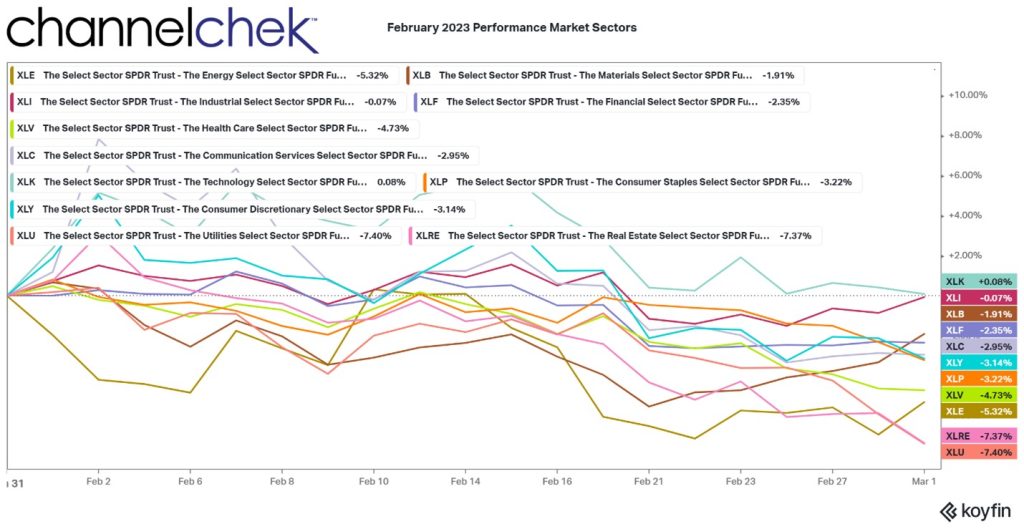

Of the 11 S&P market sectors (SPDRs) only one was in positive territory for the month. This is Technology (XLK) and was barely positive at .08%. That is followed by Industrials (XLI), which fell a mere .07%. This demonstrates the flaw in using the Dow 30 Industrials (declined 4.07%) which is not as broad of an index or a great gauge of stock market direction. The third top performer was Financials (XLF) which returned a negative 2.26%. Financial firms tend to benefit from higher yields, especially if the yield curev steepens, the curve currently has negative spreads out longer.

Of the worst performers are Utilities (XLU), down 7.45%. Many investors in utilities these stocks for dividend yield; as US government bonds pay more interest, they make utility stocks less attractive. Real Estate is also affected by higher rates as underlying assets (properties) decline and the attractiveness of its dividends diminish with high rates available elsewhere. The Energy sector (XLE) was the third worst. Energy is taking its lead from what is happening between Russia and the rest of Europe.

Looking Forward

Income and consumer spending have held strong in early 2023. This would seem to put off any chance of a recession beginning this quarter or next. Earnings reported for the fourth quarter have been mixed. Public companies are dealing with their own increased costs of doing business.

The Fed raising rates one, two, or three more times in 2023 is fully expected. What became less certain is whether they will continue to rely on 25bp increments or if another 50bp is on tap in March or beyond. The Fed began raising rates last March, a large impact has yet to be felt, and it is not expected to take a wait-and-see approach soon.

February’s small decline after a large January run-up is not unusual activity. In fact the short month has typically been one of the worst of the year for the U.S. stock market. Historically, the S&P 500 has performed better in March and April. How much better? Since 1928, the S&P 500 has averaged a 0.5% gain in March and a 1.4% gain in April.

Take-Away