GABY Inc. is a California-focused retail consolidator and the owner of Mankind Dispensary, one of the oldest licensed dispensaries in California. Mankind is a well-known, and highly respected dispensary with deep roots in the California cannabis community operating in San Diego, California. GABY curates and sells a diverse portfolio of products, including its own proprietary brands, Lulu’s™ and Kind Republic™ through Mankind, manufactures Kind Republic, and distributes all its proprietary brands through its wholly owned subsidiary, GABY Manufacturing. A pioneer in the industry with a multi-vertical retail foundation, and a strong management team with experience in retail, consolidation, and cannabis, GABY is poised to grow its retail operations both organically and through acquisition.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Revenue. GABY reported third quarter revenue of $5.35 million (all figures in U.S. $), down from $7.6 million reported last year, although adjusted for the closure of the wholesale distribution business, revenue was down $1.3 million, or 20%. Net loss was $3.76 million, or a loss of $0.01 per share, compared to a loss of $3.41 million, or a loss of $0.01 per share, year-over-year. A still difficult operating environment due to lower pricing and reduced demand combined with increased competition and forex losses impacted results.

A Ray of Light? Notably, on a sequential basis, revenue was up $0.2 million, or 4%, from the second quarter of 2022, potentially indicating an upturn in the depressed California market. Gross margin increased to 46.5% from 43.2%, sequentially, and was up from 39.3% year-over-year. The Mankind dispensary experienced a 2.5% growth in the number of transactions to 74,331, with a consistent average transaction value of $70 when comparing 2Q22 with 3Q22.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Pharma’s Expensive Gaming of the Drug Patent System is Successfully Countered by the Medicines Patent Pool, Which Increases Global Access and Rewards Innovation

Biomedical innovation reached a new era during the COVID-19 pandemic as drug development went into overdrive. But the ways that brand companies license their patented drugs grant them market monopoly, preventing other entities from making generics so they can exclusively profit. This significantly limits the reach of lifesaving drugs, especially to low- and middle-income countries, or LMICs.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Lucy Xiaolu Wang, Assistant Professor of Resource Economics, UMass Amherst

Drug Patents in the Global Landscape

Patents are designed to provide incentives for innovation by granting monopoly power to patent holders for a period of time, typically 20 years from the application filing date.

However, this intention is complicated by strategic patenting. For example, companies can delay the creation of generic versions of a drug by obtaining additional patents based on slight changes to its formulation or method of use, among other tactics. This “evergreens” the company’s patent portfolio without requiring substantial new investments in research and development.

Furthermore, because patents are jurisdiction-specific, patent rights granted in the U.S. do not automatically apply to other countries. Firms often obtain multiple patents covering the same drug in different countries, adapting claims based on what is patentable in each jurisdiction.

To incentivize technology transfer to low- and middle-income countries, member nations of the World Trade Organization signed the 1995 Agreement on Trade-Related Aspects of Intellectual Property Rights, or TRIPS, which set the minimum standards for intellectual property regulation. Under TRIPS, governments and generic drug manufacturers in low- and middle-income countries may infringe on or invalidate patents to bring down patented drug prices under certain conditions. Patents in LMICs were also strengthened to incentivize firms from high-income countries to invest and trade with LMICs.

The 2001 Doha Declaration clarified the scope of TRIPS, emphasizing that patent regulations should not prevent drug access during public health crises. It also allowed compulsory licensing, or the production of patented products or processes without the consent of the patent owner.

One notable example of national patent law in practice after TRIPS is Novartis’ anticancer drug imatinib (Glivec or Gleevec). In 2013, India’s Supreme Court denied Novartis’s patent application for Glivec for obviousness, meaning both experts or the general public could arrive at the invention themselves without requiring much skill or thought. The issue centered on whether new forms of known substances, in this case a crystalline form of imatinib, were too obvious to be patentable. At the time, Glivec had already been patented in 40 other countries. As a result of India’s landmark ruling, the price of Glivec dropped from 150,000 INR (about US$2,200) to 6,000 INR ($88) for one month of treatment.

Patent Challenges and Pools

Although TRIPS seeks to balance incentives for innovation with access to patented technologies, issues with patents still remain. Drug cocktails, for example, can contain multiple patented compounds, each of which can be owned by different companies. Overlapping patent rights can create a “patent thicket” that blocks commercialization. Treatments for chronic conditions that require a stable and inexpensive supply of generics also pose a challenge, as the cost burden of long-term use of patented drugs is often unaffordable for patients in low- and middle-income countries.

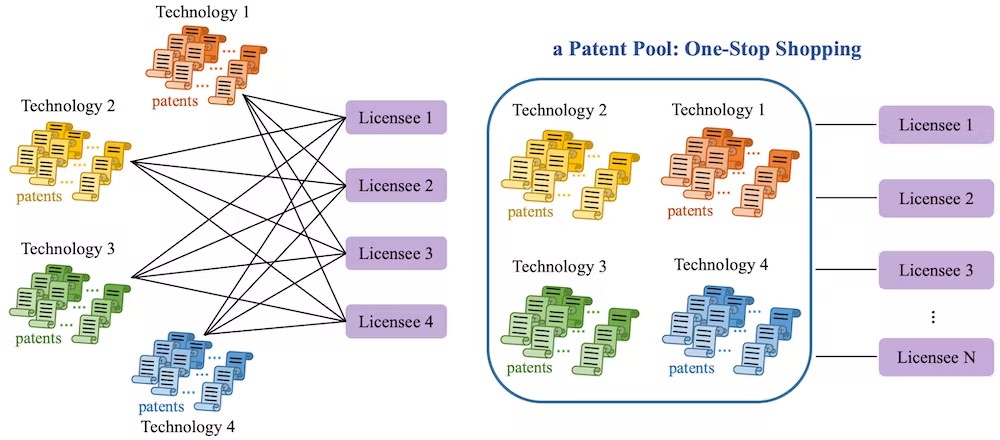

One solution to these drug access issues is patent pools. In contrast to the currently decentralized licensing market, where each technology owner negotiates separately with each potential licensee, a patent pool provides a “one-stop shop” where licensees can get the rights for multiple patents at the same time. This can reduce transaction costs, royalty stacking and hold-up problems in drug commercialization.

Patent pools were first used in 1856 for sewing machines and were once ubiquitous across multiple industries. Patent pools gradually disappeared after a 1945 U.S. Supreme Court decision that increased regulatory scrutiny, hindering the formation of new pools. Patent pools were later revived in the 1990s in response to licensing challenges in the information and communication technology sector.

Patent pools create a one-stop shop for multiple patients, allowing multiple licensees to enter the market. Lucy Xiaolu Wang, CC BY-NC-ND

The Medicines Patent Pool

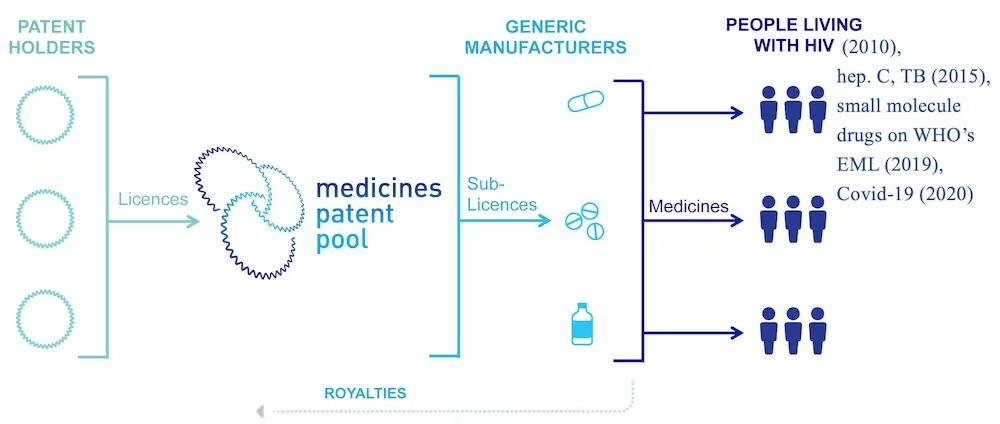

Despite many challenges, the first patent pool created for the purpose of promoting public health formed in 2010 with support from the United Nations and Unitaid. The Medicines Patent Pool, or MPP, aims to spur generic licensing for patented drugs that treat diseases disproportionately affecting low- and middle-income countries. Initially covering only HIV drugs, the MPP later expanded to include hepatitis C and tuberculosis drugs, many medications on the World Health Organization’s essential medicines list and, most recently, COVID-19 treatments and technologies.

But how much has the MPP improved drug access?

I sought to answer this question by examining how the Medicines Patent Pool has affected generic drug distribution in low- and middle-income countries and biomedical research and development in the U.S. To analyze the MPP’s influence on expanding access to generic drugs, I collected data on drug licensing contracts, procurement, public and private patents and other economic variables from over 100 low- and middle-income countries. To analyze the MPP’s influence on pharmaceutical innovation, I examined data on new clinical trials and new drug approvals over this period. This data spanned from 2000 to 2017.

The Medicines Patent Pool works as an intermediary between branded drug companies and generic licensees, increasing access to drugs. Lucy Xiaolu Wang, CC BY-NC-ND i

I found that the MPP led to a 7% increase in the share of generic drugs supplied to LMICs. Increases were greater in countries where drugs are patented and in countries outside of sub-Saharan Africa, where baseline generic shares are lower and can benefit more from market-based licensing.

I also found that the MPP generated positive spillover effects for innovation. Firms outside the pool increased the number of trials they conducted on drug cocktails that included MPP compounds, while branded drug firms participating in the pool shifted their focus to developing new compounds. This suggests that the MPP allowed firms outside the pool to explore new and better ways to use MPP drugs, such as in new study populations or different treatment combinations, while brand name firms participating in the pool could spend more resources to develop new drugs.

The MPP was also able to lessen the burden of post-market surveillance for branded firms, allowing them to push new drugs through clinical trials while generic and other independent firms could monitor the safety and efficacy of approved drugs more cheaply.

Overall, my analysis shows the MPP effectively expanded generic access to HIV drugs in developing countries without diminishing innovation incentives. In fact, it even spurred companies to make better use of existing drugs.

Technology Licensing for COVID-19 and Beyond

Since May 2020, the Medicines Patent Pool has become a key partner of the World Health Organization COVID-19 Technology Access Pool, which works to spur equitable and affordable access to COVID-19 health products globally. The MPP has not only made licensing for COVID-19 health products more accessible to low- and middle-income countries, but also helped establish an mRNA vaccine technology transfer hub in South Africa to provide the technological training needed to develop and sell products treating COVID-19 and beyond.

Licensing COVID-19-related technologies can be complicated by the large amount of trade secrets involved in producing drugs derived from biological sources. These often require additional technology transfer beyond patents, such as manufacturing details. The MPP has also worked to communicate with brand firms, generic manufacturers and public health agencies in low- and middle-income countries to close the licensing knowledge gap.

Questions remain on how to best use licensing institutions like the MPP to increase generic drug access without hampering the incentive to innovate. But the MPP is proving that it is possible to align the interests of Big Pharma and generic manufacturers to save more lives in developing countries. In October 2022, the MPP signed a licensing agreement with Novartis for the leukemia drug nilotinib – the first time a cancer drug has come under a public health-oriented licensing agreement.

The Small Cap Effect Suggests Oversized Gains if You Weed Out Certain Stocks

According to a June 5th article in the Wall Street Journal, “small-cap stocks are priced for jumbo gains.” The Journal explains that small-caps have experienced lower average volatility than large-caps during periods of market stress. Examples are the 2013 “taper tantrum,” when investors turned bearish after the Federal Reserve said that it would reduce bond purchases; also the United Kingdom’s Brexit referendum in 2016; and the Covid-19 pandemic. This fact is counter-intuitive to what investors expect from what are considered the riskier securities.

The Journal reports that one prominent money manager predicts that the smaller companies will outshine large-caps by close to four percentage points a year over the next five years. They also report a large investment bank is even more bullish on small-caps for the coming decade.

What are Small-Caps?

Small-caps are most commonly defined as companies with lower-than-average market capitalizations. This is most often defined as between $300 million and $2 billion. However, the index that is often quoted to reflect small-cap stocks overall performance is the Russell 2000 Small-cap Index (RUT). The stocks represented in the RUT have a median market cap of $1 billion and the largest stands near $13 billion. Well outside of the range of the more common definition.

Small-Cap Effect

The small-cap effect was documented decades ago and demonstrates the propensity of small companies to produce higher average returns than companies over extended holding periods. The thought process includes the idea that small companies are riskier, so additional expected return is necessary to compensates investors for taking extra risk.

But the past decade has left the small caps with a lot of catching up to do. The large-company Russell 1000 (RUI) has beaten the small-company Russell 2000 by three points a year over the past decade, returning an average of 13.1%.

The lack of comparative performance is not because small-caps have been bad performers. Larger companies, particularly those at the very top, had a fantastic run during that decade. Now, there’s an ongoing debate over whether the small-cap effect is still valid, if it is, there is much catching up to do in terms of performance. Time will tell what direction and pace prices change moving forward. It is unknowable right now. What is knowable is that many small-caps are currently cheap.

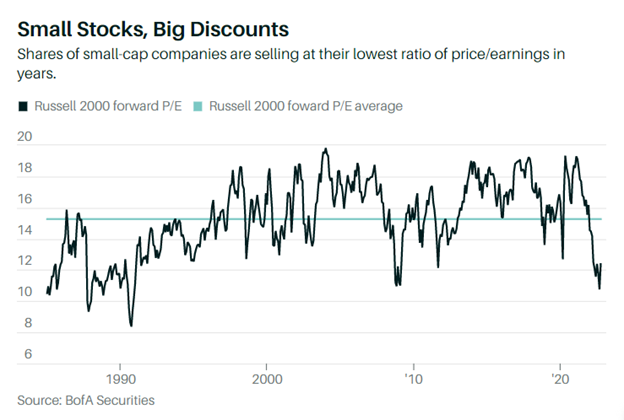

According to the Wall Street Journal, The Russell 2000 is flirting with 20 times earnings, a hair above its long-term average and certainly not deep value territory. But weed out the index’s unprofitable companies and statistical outliers, and the price/earnings ratio drops to about 12, versus a long-term average of 15.

This adjustment to the index make-up makes sense for two reasons. One is that 33% of Russell 2000 members today have negative earnings, up from 20% a decade ago, and at a record high. But there’s a bigger reason to exclude unprofitable companies when sizing up the Russell 2000: The adjusted P/E has been a better predictor of future returns than the unadjusted one, (based on a B of A analysis of data going back to 1985. Right now, the adjusted P/E has B of A to predicting 12% annual returns for small-caps over the coming decade. That’s five points more than it sees for large-caps. The analysts calculate that small-caps are 30% cheaper than large-caps now. This would be the biggest discount since the dot-com stock bubble more than two decades ago.

What do Equity Analysts Think?

On December 15th, 2022 – 9:00am EST there will be a rare opportunity to hear from analysts covering different sectors of the small-cap space.

At no cost for investors, the well-recognized veteran analysts will highlight how they set their price targets and market ratings. And the underlying fundamental reasons to consider an investment. As an attendee, you can get further involved by submitting your own questions. And learn which stocks the research analysts may favor.

This is the season to set your sites on maximizing returns in the coming year and the years that follow. This event is online and free, courtesy of Noble Capital Markets and Channelchek.

Get ahead of your investments in the coming year by attending this special event, learn how by going here now.

Will Russia Make the EU an Acceptable Counter Offer?

On Sunday, OPEC+ voted to maintain the previous level of output. This is known in OPEC vernacular as a “rollover,” it will allow the group time to experience and assess the market impact of the price cap of $60 a barrel on Russian oil. The $60 EU price cap is scheduled to begin Monday, December 5th.

Otherwise, it will be a quiet week in terms of data and Fed governor speeches. After a flurry of talks out of Fed executives last week, mostly pointing to a tapering of increases, the Fed is now in a blackout period until after the December 13-14 meeting and announcement.

Monday 12/5

9:45 AM ET, PMI Composite Final Consensus Outlook A little less contraction is the call for the PMI Service’s November final, at a consensus of 46.3 versus 46.1 at mid-month.

10:00 AM ET, Factory Orders are seen rising to a 0.7 percent gain in October. This would follow a 0.4 percent gain in September. The upward adjustment is in part due to Durable Goods orders for October, which have already been released and are one of two major components of this report. Durable Goods rose 1.0 percent in the month, which was stronger than expected. Factory Orders are a true leading indicator of future economic activity.

10:00 AM ET, ISM Services Industries has been slow, having reported 54.4 in October and expectations of 53.5 for November.

Tuesday 12/6

8:30 AM ET, International Trade in Goods and Services, a deficit of $80.0 billion is expected in October for total goods and services, which would compare with a $73.3 billion deficit in September. Advance data on the goods side of October’s report showed a more than $7 billion deepening in the deficit.

Wednesday 12/7

7:00 AM ET, MBA Mortgage Applications are expected to show that the composite index down 0.8%, the purchase index has gained 3.8%, and the refinance index is down 12.9%. The MBA compiles various mortgage loan indexes. The purchase applications index measures applications at mortgage lenders. This is a leading indicator for single-family home sales and housing construction, along with related industries that are impacted by a changing housing market.

8:30 AM ET, Productivity and Costs for third-quarter are expected to show non-farm productivity rising 0.4 percent versus a scant 0.3 percent annualized gain in the first estimate. Unit labor costs, which slowed from 8.9 percent in the second quarter to 3.5 percent in the first estimate for the third quarter, are expected to rise at a 3.3 percent rate in the second estimate.

10:30 AM ET, EIA Petroleum Status report. The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products.

3:00 PM ET Consumer credit is expected to increase $27.3 billion in October versus a $25.0 billion increase in September. Changes in consumer credit indicate the state of consumer finances and signal future spending patterns. The report includes credit cards, vehicle loans, and student loans; mortgages are not included.

Productivity measures the growth of labor efficiency in producing the economy’s goods and services. Unit labor costs reflect the labor costs of producing each unit of output. Both are followed as indicators of future inflationary trends

Thursday 12/8

8:30 AM ET, Jobless Claims for the December 3 week are expected to come in at a 228,000 four-week moving average, versus 225,000 in the prior week. Employment is one of the Fed’s mandates; as such, any number that significantly varies from consensus could alter the market’s thinking.

10:00 AM ET, ISM Manufacturing Index was 50.2 in October; the ISM Manufacturing Index has been gradually slowing to nearly breakeven. November’s consensus is 49.9.

10:00 AM ET, Construction spending is expected to fall 0.2 percent in October. This would be dramatic relative to September’s modest 0.2 percent gain.

10:30 AM ET, The Energy Information Administration (EIA) provides weekly information on natural gas stocks in underground storage for the U.S. and five regions of the country. The level of inventories helps determine prices for natural gas products.

4:30 PM ET, The Fed’s balance sheet is a weekly report presenting a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. The report is officially named Factors Affecting Reserve Balances, otherwise known as the “H.4.1” report; investors have taken a recent interest in this weekly report as it shows if the Fed is on track with quantitative tightening plans.

Friday 12/9

8:30 AM ET, Producer Price Index or PPI, after moderating in October, PPI is expected to rise 0.2 percent on the month in November and 7.2 percent on the year. These would compare with 0.2 and 8.0 percent in October, which were both lower than expected. When excluding food and energy, prices are expected to also rise 0.2 percent on the month and 5.9 percent on the year.

10:00 AM ET, Consumer Sentiment is expected to remain unchanged at 56.8 after a rebound in November’s final report.

10:00 AM ET, Wholesale Inventories (second estimate for October) is expected to be unchanged from the first estimate at 0.8%.

What Else

The focus until mid-month is likely to be how interest rate markets trade with a new sense that the Fed is slowing its tightening pace. Also in high focus this week, markets are expected to pay attention to how oil prices play out with the EU plan and perhaps a forthcoming Russian proposal.

MALVERN, Penn., Dec. 02, 2022 (GLOBE NEWSWIRE) — Baudax Bio, Inc. (the “Company” or “Baudax Bio”) (NASDAQ: BXRX), a pharmaceutical company focused on therapeutics for acute care settings, today announced the pricing of a public offering of an aggregate of 1,042,787 shares of its common stock (or pre-funded warrants in lieu thereof), Series A-3 warrants to purchase up to 1,042,787 shares of common stock and Series A-4 warrants to purchase 1,042,787 shares of common stock, at a combined public offering price of $4.795 per share (or pre-funded warrant) and accompanying warrants. The Series A-3 warrants will have an exercise price of $4.50 per share, will be exercisable immediately upon issuance and will expire five years from the date of issuance, and the Series A-4 warrants will have an exercise price of $4.50 per share, will be exercisable immediately upon issuance and will expire thirteen months from the date of issuance. The closing of the offering is expected to occur on or about December 6, 2022, subject to the satisfaction of customary closing conditions.

H.C. Wainwright & Co. is acting as the exclusive placement agent for the offering.

The gross proceeds from the offering, before deducting the placement agent’s fees and other offering expenses, are expected to be approximately $5 million. The Company intends to use the net proceeds from this offering for working capital, pipeline development activities and general corporate purposes.

The securities described above are being offered pursuant to a registration statement on Form S-1 (File No. 333-268251), which was declared effective by the Securities and Exchange Commission (the “SEC”) on December 2, 2022. The offering is being made only by means of a prospectus which forms a part of the effective registration statement. A preliminary prospectus relating to the offering has been filed with the SEC. Electronic copies of the final prospectus, when available, may be obtained on the SEC’s website at http://www.sec.gov and may also be obtained by contacting H.C. Wainwright & Co., LLC at 430 Park Avenue, 3rd Floor, New York, NY 10022, by phone at (212) 856-5711 or e-mail at placements@hcwco.com.

The Company also has agreed that certain existing warrants to purchase up to an aggregate of 374,108 shares of common stock of the Company that were previously issued to an investor in November 2020, January 2021, June 2021, December 2021, March 2022, May 2022 and September 2022, at exercise prices ranging from $21.00 to $43.60 per share and expiration dates ranging from October 2023 to September 2027, will be amended effective upon the closing of the offering so that the amended warrants will have a reduced exercise price of $4.50 per share and will expire five years following the closing of the offering.

This press release shall not constitute an offer to sell or a solicitation of an offer to buy any of the securities described herein, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

About Baudax Bio

Baudax Bio is a pharmaceutical company focused on innovative products for hospital and related settings. The Company has a pipeline of innovative pharmaceutical assets including two clinical-stage, novel neuromuscular blocking (NMBs) agents, one in a Phase II study and an additional unique NMB in a dose escalation Phase I study, as well as a proprietary chemical reversal agent specific to these NMBs. Baudax Bio has received approval for and marketed ANJESO®, the first and only 24-hour, intravenous (IV) COX-2 preferential non-opioid, non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. For more information, please visit www.baudaxbio.com.

Forward Looking Statements

This press release contains forward-looking statements that involve risks and uncertainties. Such forward-looking statements reflect Baudax Bio’s expectations about its future performance and opportunities that involve substantial risks and uncertainties. When used herein, the words “anticipate,” “believe,” “estimate,” “may,” “upcoming,” “plan,” “target,” “goal,” “intend” and “expect” and similar expressions, as they relate to Baudax Bio or its management, are intended to identify such forward-looking statements. Forward-looking statements may include, without limitation, statements regarding the consummation of the offering, the satisfaction of the closing conditions of the offering and the use of net proceeds therefrom. These forward-looking statements are based on information available to Baudax Bio as of the date of publication on this internet site, including Baudax Bio’s ability to realize any anticipated benefits from the reverse stock split, including maintaining its listing on the Nasdaq Capital Market and attracting new investors. These risks and uncertainties include, among other things, risks related to market, economic and other conditions, the ongoing economic and social consequences of the COVID-19 pandemic, Baudax Bio’s ability to advance its current product candidate pipeline through pre-clinical studies and clinical trials, Baudax Bio’s ability to raise future financing for continued development of its product candidates such as BX1000, BX2000 and BX3000, Baudax Bio’s ability to pay its debt and satisfy conditions necessary to access future tranches of debt, Baudax Bio’s ability to comply with the financial and other covenants under its credit facility, Baudax Bio’s ability to manage costs and execute on its operational and budget plans, Baudax Bio’s ability to achieve its financial goals; Baudax Bio’s ability to comply with all listing requirements of the Nasdaq Capital Market; and Baudax Bio’s ability to obtain, maintain and successfully enforce adequate patent and other intellectual property protection. These forward-looking statements should be considered together with the risks and uncertainties that may affect Baudax Bio’s business and future results included in Baudax Bio’s filings with the Securities and Exchange Commission at www.sec.gov. These forward-looking statements are based on information currently available to Baudax Bio, and Baudax Bio assumes no obligation to update any forward-looking statements except as required by applicable law.

Investor Relations Contact: Argot Partners Sam Martin / Kaela Ilami (212) 600-1902 baudaxbio@argotpartners.com

Corporate Presentation to Highlight Company’s Gene Therapies for Cancer and Diabetes

AUSTIN, Texas — (December 2, 2022) — Genprex, Inc. (“Genprex” or the “Company”) (NASDAQ: GNPX), a clinical-stage gene therapy company focused on developing life-changing therapies for patients with cancer and diabetes, today announced that its Executive Vice President, General Counsel and Chief Strategy Officer, Catherine Vaczy, will be providing an overview of the Company’s gene therapies for cancer and diabetes at the following investor conference in December 2022.

Ms. Vaczy will be available for Q&A following the presentation and for in-person one-on-one meetings with investors at the RHK Disruptive Growth Conference.

About Genprex, Inc.

Genprex, Inc. is a clinical-stage gene therapy company focused on developing life-changing therapies for patients with cancer and diabetes. Genprex’s technologies are designed to administer disease-fighting genes to provide new therapies for large patient populations with cancer and diabetes who currently have limited treatment options. Genprex works with world-class institutions and collaborators to develop drug candidates to further its pipeline of gene therapies in order to provide novel treatment approaches. Genprex’s oncology program utilizes its proprietary, non-viral ONCOPREX® Nanoparticle Delivery System, which the Company believes is the first systemic gene therapy delivery platform used for cancer in humans. ONCOPREX encapsulates the gene-expressing plasmids using lipid nanoparticles. The resultant product is administered intravenously, where it is then taken up by tumor cells that express tumor suppressor proteins that are deficient in the body. The Company’s lead product candidate, REQORSA™ (quaratusugene ozeplasmid), is being evaluated as a treatment for non-small cell lung cancer (NSCLC) (with each of these clinical programs receiving a Fast Track Designation from the Food and Drug Administration) and for small cell lung cancer. Genprex’s diabetes gene therapy approach is comprised of a novel infusion process that uses an endoscope and an adeno-associated virus (AAV) vector to deliver Pdx1 and MafA genes to the pancreas. In models of Type 1 diabetes, the genes express proteins that transform alpha cells in the pancreas into functional beta-like cells, which can produce insulin but are distinct enough from beta cells to evade the body’s immune system. In Type 2 diabetes, where autoimmunity is not at play, it is believed that exhausted beta cells are also rejuvenated and replenished.

Cautionary Language Concerning Forward-Looking Statements

Statements contained in this press release regarding matters that are not historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty. These forward-looking statements should, therefore, be considered in light of various important factors, including those set forth in Genprex’s reports that it files from time to time with the Securities and Exchange Commission and which you should review, including those statements under “Item 1A – Risk Factors” in Genprex’s Annual Report on Form 10-K for the year ended December 31, 2021.

Because forward-looking statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Such statements include, but are not limited to, statements regarding: the timing and success of Genprex’s clinical trials and regulatory approvals, including the extent and impact of the COVID-19 pandemic; the effect of Genprex’s product candidates, alone and in combination with other therapies, on cancer and diabetes; Genprex’s future growth and financial status; Genprex’s commercial and strategic partnerships, including those with its third party manufacturers and their ability to successfully perform and scale up the manufacture of its product candidates; and Genprex’s intellectual property and licenses.

These forward-looking statements should not be relied upon as predictions of future events and Genprex cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur. If such forward-looking statements prove to be inaccurate, the inaccuracy may be material. You should not regard these statements as a representation or warranty by Genprex or any other person that Genprex will achieve its objectives and plans in any specified timeframe, or at all. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release. Genprex disclaims any obligation to publicly update or release any revisions to these forward-looking statements, whether as a result of new information, future events or otherwise, after the date of this press release or to reflect the occurrence of unanticipated events, except as required by law.

CALGARY, AB, Dec. 1, 2022 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.015 per common share payable on December 30, 2022, to shareholders of record at the close of business on December 15, 2022. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

NEW ALBANY, Ohio, Dec. 01, 2022 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI) announced today that Harold Bevis, President and Chief Executive Officer, and Andy Cheung, Executive Vice President and Chief Financial Officer, will present virtually at the Sidoti December Small-Cap Virtual Conference on December 7, 2022, at 9:15 a.m. ET. A link to the webcast can be accessed through the investor section of the Company’s website at cvgrp.com. The presentation materials will be posted on the Company Website and be archived there for a period of 30 days.

Management will also meet virtually with investors registered for the conference.

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

Seanergy Maritime Holdings Corp. is the only pure-play Capesize ship-owner publicly listed in the US. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 17 Capesize vessels with an average age of approximately 12 years and aggregate cargo carrying capacity of approximately 3,011,083 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP” and its Class B warrants under “SHIPZ”.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter results reflect a drop in shipping pricing, as expected. Shipping rates have fallen sharply in the last few quarters. Although management took some steps to lock in pricing this summer, it should be pointed out that the bulk of its fleet is on spot or indexed rates. We lowered our estimates in October to reflect weakening industry fundamentals, so weaker results were largely anticipated.

Slightly better-than-expected results reflect increased operating days. Seanergy brought several vessels into dry dock for repairs and upgrades in previous quarters. As a result, it was able to keep its ships active in the most recent quarter. The result was an increase in operating days above our expectations leading to higher-than-expected revenues.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Going for the gold. Maple Gold released results from drilling completed at the Douay Gold Project during the first half of 2022 totaling 7,800 meters. Douay is held by a 50/50 joint venture between the company and Agnico Eagle Mines Limited. The first year of drilling focused primarily on infill drilling. The second year focused on “quantum leap” style exploration with additional step-outs, deep drilling, and testing discovery targets. The same approach will be taken next year to define the extent and potential of the mineralized system at Douay. An additional ~10,000 meters of drilling has been completed at the Eagle and Telbel mine properties with assays pending.

Favorable drill results. Ten of twelve holes returned intercepts over 0.45 grams of gold per tonne, and seven returned intercepts greater than 1.0 gram of gold per tonne. Hole DO-22-322A in the Nika Zone intersected 9.8 grams of gold over 1 meter from 584 meters depth along with other positive intercepts that support depth continuity of the intrusive hydrothermal gold system at Douay. Sediment-hosted gold showings at the NE IP Target provided support for a new gold zone four kilometers to the northeast of the current Douay mineral resource area. Hole DO-22-326 in the Central Zone returned four intercepts greater than 1 gram of gold per tonne, including 3.0 grams of gold per tonne over 1.0 meter from only 67 meters downhole.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Harte Hanks (NASDAQ: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers. Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony, and IBM among others. Headquartered in Chelmsford, Massachusetts , Harte Hanks has over 2,500 employees in offices across the Americas, Europe and Asia Pacific .

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A tuck-in acquisition. On December 1, 2022, the company completed an acquisition of InsideOut Solutions, a firm that specializes in third party inbound and outbound sales, for $7.5 million. The acquisition complements the company’s Marketing and Customer Care segments nicely, while expanding cross selling capabilities. The pruchase price is an attractive 3 to 4 times adj. EBITDA, post synergies.

Substantial synergies. The acquisition of InsideOut will broaden the scope of services offered by the company, creating more cross selling and lead generating opportunities. With a robust new business pipeline, management expects InsideOut 2023 revenue growth between 20% to 25%. The business is expected to be cash flow positive, generating $2 million to $2.5 million in EBITDA.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Private placement financing. Aurania closed the first tranche of its private placement financing of up to 4,444,444 units of the company for gross proceeds of up to C$2,000,000. In aggregate, 2,417,166 units were sold at a price of C$0.45 per unit for gross proceeds of C$1,087,725. Each unit is comprised of one common share and one common share purchase warrant that entitles the holder to purchase one common share at an exercise price of C$0.75 per warrant share at any time until November 29, 2024. Aurania received an extension by the TSX Venture Exchange to close the second tranche by January 9, 2023, although we believe it will likely close by mid-December.

Drilling begins at Tatasham. Aurania has commenced its drilling program at the Tatasham porphyry copper target. We expect the company to drill up to four holes for a total of 2,700 meters, or an average depth of 675 meters per hole. Because Tatasham is a blind geophysical target with no mineralization at surface, we expect drilling will be an iterative process subject to refinement. Following Tatasham, the company anticipates drilling at the Awacha porphyry copper target.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Darknet Markets Generate Millions in Revenue Selling Stolen Personal Data, Supply Chain Study Finds

It is common to hear news reports about large data breaches, but what happens once your personal data is stolen? Our research shows that, like most legal commodities, stolen data products flow through a supply chain consisting of producers, wholesalers and consumers. But this supply chain involves the interconnection of multiple criminal organizations operating in illicit underground marketplaces.

The stolen data supply chain begins with producers – hackers who exploit vulnerable systems and steal sensitive information such as credit card numbers, bank account information and Social Security numbers. Next, the stolen data is advertised by wholesalers and distributors who sell the data. Finally, the data is purchased by consumers who use it to commit various forms of fraud, including fraudulent credit card transactions, identity theft and phishing attacks.

This trafficking of stolen data between producers, wholesalers and consumers is enabled by darknet markets, which are websites that resemble ordinary e-commerce websites but are accessible only using special browsers or authorization codes.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Christian Jordan Howell

Assistant Professor in Cybercrime, University of South Florida and David Maimon, Professor of Criminal Justice and Criminology, Georgia State University.

We found several thousand vendors selling tens of thousands of stolen data products on 30 darknet markets. These vendors had more than US$140 million in revenue over an eight-month period.

The stolen data supply chain, from data theft to fraud. Christian Jordan Howell, CC BY-ND

Darknet Markets

Just like traditional e-commerce sites, darknet markets provide a platform for vendors to connect with potential buyers to facilitate transactions. Darknet markets, though, are notorious for the sale of illicit products. Another key distinction is that access to darknet markets requires the use of special software such as the Onion Router, or TOR, which provides security and anonymity.

Silk Road, which emerged in 2011, combined TOR and bitcoin to become the first known darknet market. The market was eventually seized in 2013, and the founder, Ross Ulbricht, was sentenced to two life sentences plus 40 years without the possibility of parole. Ulbricht’s hefty prison sentence did not appear to have the intended deterrent effect. Multiple markets emerged to fill the void and, in doing so, created a thriving ecosystem profiting from stolen personal data.

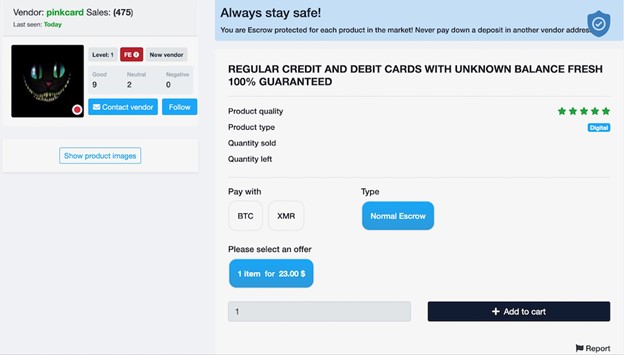

Example of a stolen data ‘product’ sold on a darknet market. Screenshot by Christian Jordan Howell, CC BY-ND

Stolen Data Ecosystem

Recognizing the role of darknet markets in trafficking stolen data, we conducted the largest systematic examination of stolen data markets that we are aware of to better understand the size and scope of this illicit online ecosystem. To do this, we first identified 30 darknet markets advertising stolen data products.

Next, we extracted information about stolen data products from the markets on a weekly basis for eight months, from Sept. 1, 2020, through April 30, 2021. We then used this information to determine the number of vendors selling stolen data products, the number of stolen data products advertised, the number of products sold and the amount of revenue generated.

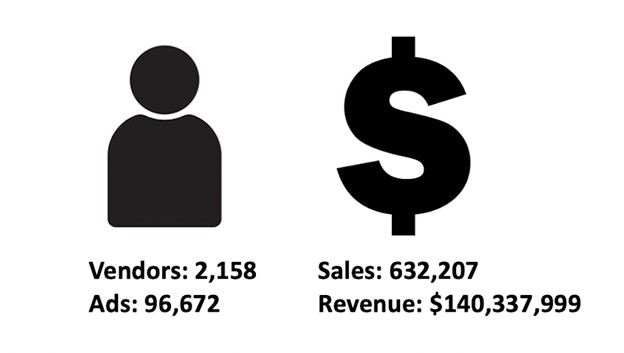

In total, there were 2,158 vendors who advertised at least one of the 96,672 product listings across the 30 marketplaces. Vendors and product listings were not distributed equally across markets. On average, marketplaces had 109 unique vendor aliases and 3,222 product listings related to stolen data products. Marketplaces recorded 632,207 sales across these markets, which generated $140,337,999 in total revenue. Again, there is high variation across the markets. On average, marketplaces had 26,342 sales and generated $5,847,417 in revenue.

The size and scope of the stolen data ecosystem over an eight-month period. Christian Jordan Howell, CC BY-ND

After assessing the aggregate characteristics of the ecosystem, we analyzed each of the markets individually. In doing so, we found that a handful of markets were responsible for trafficking most of the stolen data products. The three largest markets – Apollon, WhiteHouse and Agartha – contained 58% of all vendors. The number of listings ranged from 38 to 16,296, and the total number of sales ranged from 0 to 237,512. The total revenue of markets also varied substantially during the 35-week period: It ranged from $0 to $91,582,216 for the most successful market, Agartha.

For comparison, most midsize companies operating in the U.S. earn between $10 million and $1 billion annually. Both Agartha and Cartel earned enough revenue within the 35-week period we tracked them to be characterized as midsize companies, earning $91.6 million and $32.3 million, respectively. Other markets like Aurora, DeepMart and White House were also on track to reach the revenue of a midsize company if given a full year to earn.

Our research details a thriving underground economy and illicit supply chain enabled by darknet markets. As long as data is routinely stolen, there are likely to be marketplaces for the stolen information.

These darknet markets are difficult to disrupt directly, but efforts to thwart customers of stolen data from using it offers some hope. We believe that advances in artificial intelligence can provide law enforcement agencies, financial institutions and others with information needed to prevent stolen data from being used to commit fraud. This could stop the flow of stolen data through the supply chain and disrupt the underground economy that profits from your personal data.