Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Reported With Pipeline Update. Cocrystal reported a 3Q22 loss of $5.7 million or $0.70 per share. The product pipeline continues to make progress, with the first data from its influenza vaccine, CC-42344, scheduled for presentation in December. Two COVID-19 programs continue in preclinical studies, with an IND filing expected in 1Q23. The company ended the quarter with $42.1 million in cash.

Influenza Trial Data To Be Presented. Enrollment has been completed in the Phase 1 study for CC-42344 for seasonal and pandemic influenza. Safety and pharmacokinetic data is scheduled for presentation at the World Antiviral Congress in December 2022. The trial results will be submitted to regulatory authorities in the United Kingdom for a Phase 2a human challenge study to determine efficacy, expected to begin in 2H23.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q Results. Revenue for the quarter was $1.22 million, a decrease from last year’s $1.47 million and in-line with our estimate of $1.21 million. The average users were down as well in the quarter, 5,197 compared to 5,535 a year ago and 6,181 in the second quarter. The Company reported a net loss of $1.31 million, or ($0.10) per share, versus a net loss of $505,976 or ($0.05) last year. We estimated a net loss of $1.29 million or ($0.10).

Tough Environment, but a Silver Lining. Continued poor performance in the stock market, along with high inflation and sluggish GDP, has caused the Company to see decreases in overall performance year-over-year. However, the Company will have a Black Friday/Cyber Monday promotion that we believe will attract new users and bring back past users.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

BioSig Technologies is a medical technology company commercializing a proprietary biomedical signal processing platform designed to improve signal fidelity and uncover the full range of ECG and intra-cardiac signals (www.biosig.com). The Company’s first product, PURE EP(TM) System is a computerized system intended for acquiring, digitizing, amplifying, filtering, measuring and calculating, displaying, recording and storing of electrocardiographic and intracardiac signals for patients undergoing electrophysiology (EP) procedures in an EP laboratory.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

BioSig reported 3Q 2022 results. The Company reported $135,000 of revenues in the quarter that recognized $127,000 in product sales and $8,000 in service revenue. We were looking for $980,000 in product revenues and $49,000 in service revenue. The third quarter EPS loss of $0.14 matched our expected loss per share.

Marketing activities are ramping up. PURE EP technology was featured in a physician presentation at the Kansas City Heart Rhythm Symposium held August 20-21, 2022. In late September 2022, the Company released its most advanced software, known as PURE EP Software Version 6 with ACCUVIZ Module. The new Version 6 software was introduced at the Cleveland Clinic Global EP Summit held September 23-24, 2022. In addition, the Company was invited to attend and sponsor the Venice Arrhythmias 2022 Congress that met October 13-15 in Venice Italy.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

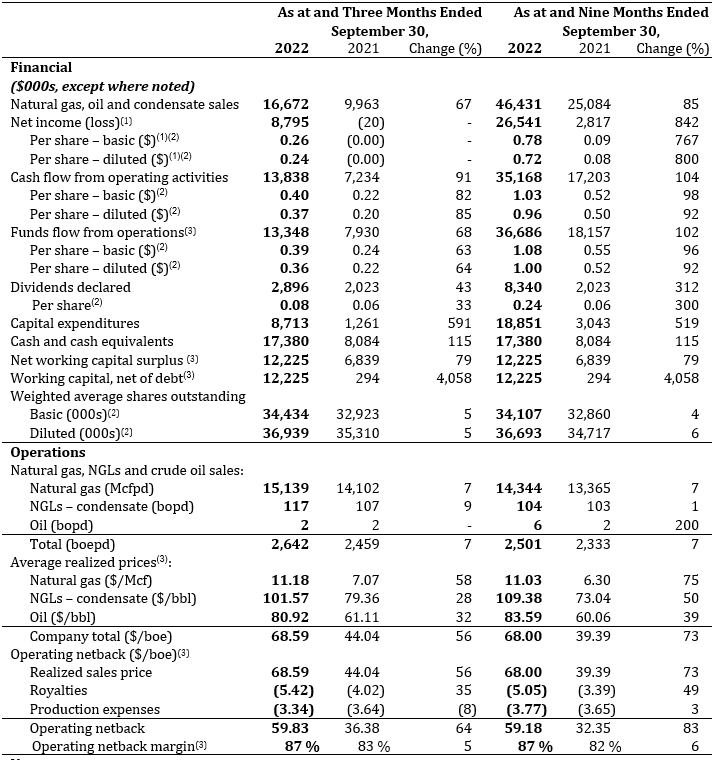

Alvopetro reported 2022-3Q results significantly higher than last year and above our expectations. Revenues rose 67% due to a 7% increase in production and a 58% increase in gas prices. Higher sales translated into higher cash flow ($13.8 million versus $7.2 million) and earnings ($8.8 million versus $0.0).

Results were due to operations improvements and are likely to continue. The company expanded its gas processing facilities in July raising capacity to 3,000 boe/d. With quarterly results, management indicated that October total production averaged 2,720 boe/d, a nice rise above 2022-3Q levels of 2,642 boe/d.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Large-Cap and Small-Cap Stock Return Probabilities

According to Ibbotson Associates’ Stocks, Bonds, Bill and Inflation, small Capitalization stocks outperform Large Capitalization stocks over the long term. (Although there is not a set definition for a Small Cap stock, generally speaking Small Cap stocks are those with a market capitalization below $2 billion today, while Large Cap stocks refer to the S&P 500.) Over the 1926-2018 period, Small Caps produced an average annual return of 11.0% compared to 9.99% for Large Capitalization stocks. (1) But, since 2010, Small Cap stocks have underperformed their Large Cap brethren. From the beginning of 2010 through the end of 2019 the S&P 500 rose 185.2% while the Russell 2000 (a proxy for small cap stocks) was up 145.8%. Over the last decade, the S&P 500 outperformed the Russell 2000 in 6 of the ten years. In 2019, the S&P 500 produced a 28.9% return compared to 23.7% for the Russell 2000. Has the time come for Small Cap stocks to outperform Large Cap stocks?

Positives

Relative Valuation Levels. Valuations for Small Caps are at their most attractive levels since June 2003 relative to Large Caps, according to data from Jefferies Financial Group. Historically, Small Caps have outperformed Large Caps by an average of 6% over the following year when the valuation gaps widens this much. (2)

New Index Highs Are a Historic Positive Sign. This past Thanksgiving, the Russell 2000 hit a new 52-week high after nearly 15 months without breaching it. FactSet and LPL Research data indicate that of the last 11 times the Russell 2000 index hit a new 52-week high, returns for the index were up an average 17% over the next 12 months 10 of those times. (3)

Higher Rate of Earnings Growth. Small Cap stocks produce a higher rate of earnings growth over time than Large Caps. Over the 1987-2017 period, Small Caps average annual recurring earnings growth was 8.15% versus 7.44% for Large Caps. (4)

Positives of Small Caps. As one would expect, most Small Caps are young companies with less international exposure than Large Caps. (5) Small Caps have less research coverage than Large Caps, providing a greater potential of market inefficiencies. (6) Ownership of Small Cap stock is typically concentrated in the hands of founders or management, a group that may be more motivated to increase shareholder value than the highly dispersed ownership of Large Cap shares.

Drawbacks

Higher Returns are due to Higher Risk. According to Alpha Wealth Strategies, Small Caps higher return over time comes with a standard deviation (a measure of risk) of 31.28 compared to just 19.76 for Large Cap stocks. (7) So, yes, an investor is receiving a higher return over time from Small Cap stocks, but the investor is assuming higher risk to achieve those returns.

Greater Volatility. As an example of the greater volatility of Small Caps, the Russell 2000 posted 65 intraday moves of 1% or more in the first 10 months of 2019, double that of the S&P 500. (2)

More Susceptible to Economic Shocks. Given their smaller size, lack of business diversification, and limited access to capital, Small Cap companies have historically been more susceptible to economic shocks. In times of economic uncertainty, many investors flock to Lage Cap stocks that are easier to trade and do not suffer from Small Caps’ business limitations. (8)

Small Caps Risks Relative to Large Caps. Among the greater risks of Small Caps is they tend to be more leveraged than Large Cap stocks with less operational efficiency and pricing power. (3) Small Caps also typically have less liquidity than Large Caps, meaning it may be tougher for investors to either build a position or quickly exit a holding. (6)

The Balanced Case:

While Small Cap stocks make up roughly just 10% of the overall U.S. equity market capitalization, they constitute the vast majority of publicly traded firms. And while Small Cap stocks are more volatile than Large Cap stock, over the last 93 years Small Caps generated positive returns in 68% of the years, compared to 73% of the time for Large Caps. Over the period, Small Caps produced a best one-year return of 142.87% and a 1-year worst return of a negative 58.01%, compared to 53.99% and a negative 43.34% for Large Caps. (7) Given Small Caps superior long-term investment returns compared to Large Caps, Small Caps would appear to be fertile shopping ground for long-term oriented investors.

Billions in Artemis Program Budget Could Cause these Companies to Rocket

What companies could gain from the Artemis missions to the moon?

The multibillion-dollar Artemis program has been unfolding over the past several years. The most recent success is the 322-foot-tall Space Launch System (SLS), the most powerful rocket NASA has developed, and the Orion spacecraft. This is all designed to, in time, safely carry astronauts to the moon’s orbit and provide a platform for the U.S. to return to the moon’s surface for the first time since 1972.

The mission of Artemis One is to test a powerful NASA rocket called the Space Launch System, as well as the Orion spacecraft that the rocket will ferry into orbit. After the Florida launch, NASA plans to use the SLS rocket to direct Orion on a route around the moon, after which the vehicle’s crewless capsule will return to Earth and parachute into the Pacific Ocean. Those steps represent another trial geared toward ensuring the Orion crew module can safely bring astronauts back from orbit.

The initial mission will help set the stage for a crewed mission to the moon that NASA hopes to conduct as early as 2025. These efforts will entail higher technology and special equipment designed especially for a unique purpose. With billions being spent, investors may ask what companies may benefit. Obviously, the major contractors, then subcontractors and material suppliers.

The cost of SLS is shown above. Additionally, the cost to assemble, integrate, prepare and launch the SLS and its payloads are funded separately under Exploration Ground Systems, currently at about $600 million per year. (Source:Wikipedia)

Major Contractors

Keeping in mind that an unsuccessful launch could weigh on these companies, as much as they may be propelled by continued success, these are prime contractors. NASA’s prime contractors for the rock launch system is Aerojet Rocketdyne (AJRD), Boeing (NYSE: BA), and Northrop Grumman (NOC). As a note, AJRD showed up as one of 5 portfolio holdings of hedge fund manager Michael Burry.

Lockheed Martin (LMT) is the prime contractor on the Orion spacecraft, while NASA’s prime contractors for the rocket launch system include Redwire’s (RDW) critical sun sensor components and advanced optical imaging technologies, they will be launching on NASA’s Orion spacecraft as a part of the space agency’s Artemis One mission. Aeva Technologies (AEVA) is also involved with a LiDAR-based mobile terrain-mapping and navigation system for lunar and other planet exploration, while KULR Technology Group (KULR) has a battery safety contract with NASA to test its lithium-ion cells going into battery packs designed for the Artemis Program.

Raytheon Technologies'(RTX) was selected to advance spacewalking capabilities in low-Earth orbit and on the Moon. Goodyear Tire & Rubber (GT) has been contracted to develop tires to perform on the lunar surface.

Rocket Lab (RKLB) has been called upon to test new orbits around the moon. For communications, Lockheed Martin (LMT), Amazon (AMZN), and Cisco (CSCO) are working in conjunction to develop a new voice, AI, and tablet-based video technologies for use around the moon.

The companies being called upon is expected to grow rapidly after scientific experiments begin on the moon’s surface.

CALGARY, AB, Nov. 15, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV:ALV); (OTCQX: ALVOF) is pleased to announce a 50% increase in our quarterly dividend, to US$0.12 per common share, an intention to launch a share buyback program under a normal course issuer bid (“NCIB”) and operating and financial results for the third quarter of 2022 including another record quarter of funds flow from operations of $13.3 million. We will host a live webcast to discuss Q3 2022 results on Wednesday November 16, 2022, beginning at 9:00 am Mountain time.

President & CEO, Corey C. Ruttan commented:

“With continued strong operating and financial results, and with our debt now fully repaid, we are pleased to announce a 50% increase in our quarterly dividend following on the 33% increase earlier this year. Our dividend program and the proposed NCIB will provide us with maximum flexibility to meet our strategy to maintain a balanced organic growth and stakeholder return model.”

All references herein to $ refer to United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Quarterly Dividend Increased 50% to $0.12 per Share

Alvopetro is pleased to announce that our Board of Directors has approved a 50% increase in our quarterly dividend, to $0.12 per common share, payable in cash on January 13, 2023, to shareholders of record at the close of business on December 30, 2022. This dividend is designated as an “eligible dividend” for Canadian income tax purposes.

Dividend payments to non-residents of Canada will be subject to withholding taxes at the Canadian statutory rate of 25%. Shareholders may be entitled to a reduced withholding tax rate under a tax treaty between their country of residence and Canada. For further information, see Alvopetro’s website at https://alvopetro.com/Dividends-Non-resident-Shareholders.

Normal Course Issuer Bid

In connection with our long-standing balanced and disciplined stakeholder return and organic growth model, our Board has provided approval to submit an application to launch a share buyback program under a NCIB, subject to securities law and customary approvals. Once approved, the NCIB, combined with our quarterly dividends, will provide us with flexibility in managing our returns to stakeholders.

Financial and Operating Highlights – Third Quarter of 2022

Daily sales averaged 2,642 boepd in Q3 2022, a 7% increase from the Q3 2021 average of 2,459 boepd and a 12% increase from the Q2 2022 average of 2,359 boepd. The expansion of our gas processing facility was completed at the end of July and available processing capacity has now increased to 500,000 m3/d (18 MMcfpd) contributing to higher volumes in the quarter.

As of August 1, 2022, Alvopetro’s natural gas price has been reset to the new ceiling price of $10.22/MMBtu. Due to the appreciation of the BRL in the first half of 2022 compared to second half of 2021, the BRL contracted price remained consistent at BRL1.94/m3. With all natural gas sales in Q3 2022 at the ceiling price, our average realized natural gas price increased to $11.18/Mcf compared to the Q3 2021 average price of $7.07/Mcf. Higher commodity prices and higher daily sales volumes resulted in a 67% increase in our natural gas, condensate and oil revenue compared to Q3 2021.

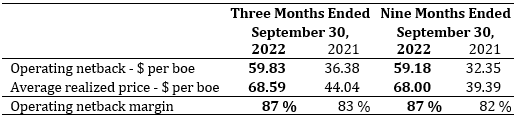

Our operating netback was $59.83 per boe in Q3 2022, an improvement of $23.45 per boe from Q3 2021 (+64%). Despite consistent BRL denominated natural gas pricing, our operating netback decreased $4.13 per boe from Q2 2022 (-6%) due to the devaluation of the BRL relative to the USD and lower Brent pricing on condensate.

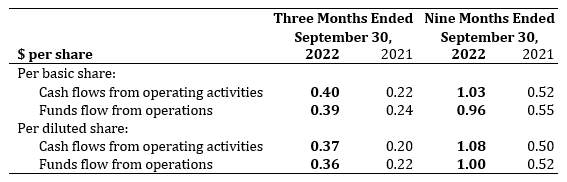

We generated cash flows from operating activities of $13.8 million ($0.40 per basic share and $0.37 per diluted share) and funds flows from operations of $13.3 million ($0.39 per basic share and $0.36 per diluted share), increases of $6.6 million and $5.4 million, respectively compared to Q3 2021.

We reported net income of $8.8 million in Q3 2022 compared to a loss of $0.02 million in Q3 2021.

Capital expenditures totaled $8.7 million, and included drilling costs for our 183-B1, 182-C2 and Unit-C wells, testing costs on our 182-C1 well, long lead purchases and development costs on our Murucututu project.

All outstanding warrants were exercised in the quarter, with 1,342,978 warrants exercised by way of cashless exercise and 1,342,978 warrants exercised at a strike price of $1.80 per share. Alvopetro received cash proceeds of $2.4 million and issued a total of 2,081,616 common shares on the exercise.

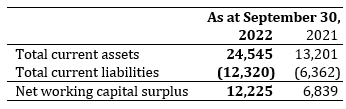

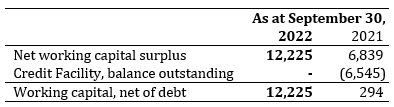

We repaid the final $2.5 million outstanding on the credit facility and the facility has now been cancelled. As at September 30, 2022, we had a net working capital surplus of $12.2 million, including $17.4 million in cash and cash equivalents.

Our October 2022 sales volumes averaged 2,720 boepd based on field estimates, with natural gas sales of 15.6MMcfpd and natural gas liquids from condensate of 124 bopd.

The following table provides a summary of Alvopetro’s financial and operating results for three and nine months ended September 30, 2022 and September 30, 2021. The consolidated financial statements with the Management’s Discussion and Analysis (“MD&A) are available on our website at www.alvopetro.com and will be available on the System for Electronic Document Analysis and Retrieval (SEDAR) website at www.sedar.com.

Notes:

The 2021 comparative periods in the table above have been restated. See “Restatement of the 2021 Comparative Period” section within the MD&A and Note 14 of the unaudited interim condensed consolidated financial statements for the three and nine months ended September 30, 2022 for further details.

Per share amounts are based on weighted average shares outstanding other than dividends per share, which is based on the number of common shares outstanding at each dividend record date. The weighted average number of diluted common shares outstanding in the computation of funds flow from operations and cash flows from operating activities per share is the same as for net income per share.

See “Non-GAAP and Other Financial Measures” section within this news release.

Third Quarter 2022 Results Webcast

Alvopetro will host a live webcast to discuss Q3 2022 financial results at 9:00 am Mountain time on November 16, 2022. Details for joining the event are as follows:

The webcast will include a question-and-answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to socialmedia@alvopetro.com.

Long-term Incentive Compensation Grants

In connection with our long-term incentive compensation program, Alvopetro’s Board of Directors (the “Board”) has approved the annual rolling grants to officers, directors and certain employees under Alvopetro’s Omnibus Incentive Plan. A total of 536,000 stock options, 122,000 restricted share units (“RSUs”) and 40,000 deferred share units (“DSUs”) were approved by the Board and are expected to be granted on November 24, 2022. Of the total grants, 248,000 stock options, 101,000 RSUs and 40,000 DSUs were granted to directors and officers. Each stock option, RSU and DSU entitles the holder to purchase one common share. Each stock option granted will have an exercise price based on the volume weighted average trading price of Alvopetro’s shares on the TSX Venture Exchange for the five (5) consecutive trading days up to and including November 24, 2022. All stock options, RSUs and DSUs granted expire five (5) years from the date of the grant.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Abbreviations:

bbls

=

barrels

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

BRL

=

Brazilian Real

m3

=

cubic metre

Mcf

=

thousand cubic feet

Mcfpd

=

thousand cubic feet per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

NGLs

=

natural gas liquids

Q2 2022

=

three months ended June 30, 2022

Q3 2021

=

three months ended September 30, 2021

Q3 2022

=

three months ended September 30, 2022

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this report should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s MD&A which may be accessed through the SEDAR website at www.sedar.com.

Non-GAAP Financial Measures

Operating netback

Operating netback is calculated as natural gas, oil and condensate revenues less royalties and production expenses. This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations.

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback divided by total sales volumes (barrels of oil equivalent). This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe).

Operating netback margin

Operating netback margin is calculated as operating netback per boe divided by the realized sales price per boe. Operating netback margin is a measure of the profitability per boe relative to natural gas, oil and condensate sales revenues per boe and is calculated as follows:

Funds Flow from Operations Per Share

Funds flow from operations per share is a non-GAAP ratio that includes all cash generated from operating activities and is calculated before changes in non-cash working capital, divided by the weighted the weighted average shares outstanding for the respective period. For the periods reported in this news release the cash flows from operating activities per share and funds flow from operations per share is as follows:

Capital Management Measures

Funds Flow from Operations

Funds flow from operations is a non-GAAP capital management measure that includes all cash generated from operating activities and is calculated before changes in non-cash working capital. The most comparable GAAP measure to funds flow from operations is cash flows from operating activities. Management considers funds flow from operations important as it helps evaluate financial performance and demonstrates the Company’s ability to generate sufficient cash to fund future growth opportunities. Funds flow from operations should not be considered an alternative to, or more meaningful than, cash flows from operating activities however management finds that the impact of working capital items on the cash flows reduces the comparability of the metric from period to period. A reconciliation of funds flow from operations to cash flows from operating activities is as follows:

Net Working Capital

Net working capital is computed as current assets less current liabilities. Net working capital is a measure of liquidity, is used to evaluate financial resources, and is calculated as follows:

Working Capital Net of Debt

Working capital net of debt is computed as net working capital surplus decreased by the carrying amount of the Credit Facility. Working capital net of debt is used by management to assess the Company’s overall financial position.

Supplementary Financial Measures

“Average realized natural gas price – $/Mcf” is comprised of natural gas sales as determined in accordance with IFRS, divided by the Company’s natural gas sales volumes.

“Average realized NGL – condensate price – $/bbl” is comprised of condensate sales as determined in accordance with IFRS, divided by the Company’s NGL sales volumes from condensate.

“Average realized oil price – $/bbl” is comprised of oil sales as determined in accordance with IFRS, divided by the Company’s oil sales volumes.

“Average realized price – $/boe” is comprised of natural gas, condensate and oil sales as determined in accordance with IFRS, divided by the Company’s total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Production expenses per boe” is comprised of production expenses, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

BOE Disclosure

The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6 Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this MD&A are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Forward-Looking Statements and Cautionary Language

This news release contains forward-looking information within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning the Company’s dividend policy, plans for dividends in the future, and the timing and taxation of such dividends, the Company’s intention to proceed with an NCIB, plans relating to the Company’s operational activities, the expected natural gas price, gas sales and gas deliveries under Alvopetro’s long-term gas sales agreement, exploration and development prospects of Alvopetro, the expected timing of certain of Alvopetro’s testing and operational activities, future results from operations, and the Company’s plans for dividends in the future. Forward-looking statements are necessarily based upon assumptions and judgments with respect to the future including, but not limited to, expected approvals and timing thereof with respect to an NCIB, equipment availability, the timing and results of testing the 183-B1 well, the 182-C2 well and the Unit C well, the success of future drilling, completion, recompletion and development activities, foreign exchange rates, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, the timing of regulatory licenses and approvals, general economic and business conditions, forecasted demand for oil and natural gas, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. In addition, the declaration, timing, amount and payment of future dividends remain at the discretion of the Board of Directors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our restated annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

SOURCE Alvopetro Energy Ltd.

For further information: Corey C. Ruttan, President, Chief Executive Officer and Director, or Alison Howard, Chief Financial Officer, Phone: 587.794.4224, Email: info@alvopetro.com, www.alvopetro.com, TSX-V: ALV, OTCQX: ALVOF

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (BVL or Bolsa de Valores de Lima: SMT) (“Sierra Metals” or the “Company”) will host a conference call on Wednesday November 16th, 2022, at 8:00am EST to provide attendees the opportunity to ask questions with respect to the Company’s financial results for Q3 2022. The Company held its Q3 2022 earnings call earlier today, but due to technical issues attendees were not able to ask questions. Details of the November 16th, 2022 conference call are as follows:

Via phone:

To ensure your participation, please call approximately five minutes prior to the scheduled start time of the call.

Canada dial-in number (Toll Free): 1 833 950 0062 Canada dial-in number (Local): 1 226 828 7575 US dial-in number (Toll Free): 1 844 200 6205 US dial-in number (Local): 1 646 904 5544 All other locations: +1 929 526 1599

Access code: 272699

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company with Green Metal exposure including copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. The Company has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT”.

For further information regarding Sierra Metals, please visit www.sierrametals.com.

This press release contains forward-looking information within the meaning of Canadian and United States securities legislation, including with respect to timing of the conference call. Forward-looking information relates to future events or the anticipated performance of Sierra and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra to be materially different from any anticipated performance expressed or implied by such forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 16, 2022 for its fiscal year ended December 31, 2021 and other risks identified in the Company’s filings with Canadian securities regulators and the United States Securities and Exchange Commission, which filings are available at www.sedar.com and www.sec.gov, respectively.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations, and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

Motorsport Games to Report Third Quarter 2022 Financial Results

MIAMI, Nov. 15, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world will report financial results for the third quarter ended September 30, 2022 on Friday, November 18, 2022, after market close. Management will host a conference call and webcast on the same day at 5:00 p.m. ET to discuss the results.

Participants may access the live webcast on the Company’s investor relations website at https://ir.motorsportgames.com under “Events.” The call may also be accessed by dialing 1 (877) 407-0784 from the U.S., or by dialing 1 (201) 689-8560 internationally.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

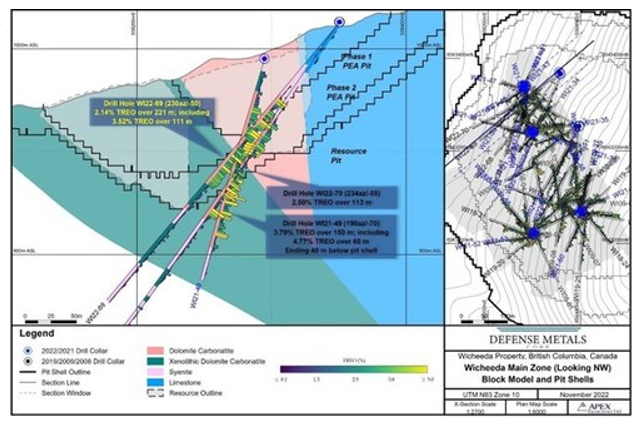

VANCOUVER, BC, Nov. 15, 2022 /PRNewswire/ – Defense Metals Corp. (“Defense Metals” or the “Company“; (TSX-V: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce additional partial Rare Earth Element (“REE“) assay results from one additional core hole, totalling 353 metres (m), collared within the northern area of Defense Metals’ 100% owned Wicheeda REE Deposit.

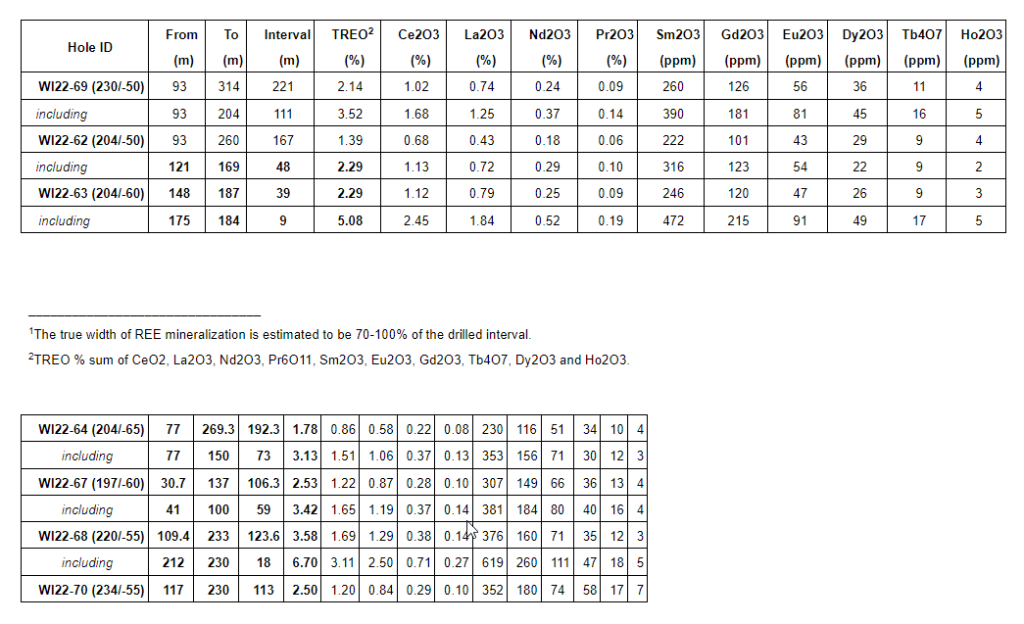

Infill drill hole WI22-69 (-50o dip / 230o azimuth) was drilled southwest within the northern area of the deposit intersected a broad zone of mineralized dolomite carbonatite averaging 2.14% total rare earth oxide (“TREO”) over 221 metres (m)1; including a higher-grade interval averaging 3.52% TREO over 111 m (Figure 1).

With over 5,500 m of drilling in 18 holes now complete as part of the 2022 Wicheeda resource delineation and pit geotechnical program, the Company has released assays for a total of 2,493 m in 7 holes. Assays for the remaining 11 holes totalling 3,017 m are expected in the coming weeks and months.

Luisa Moreno, President, and Director of Defense Metals stated: “With these additional assay results our 2022 drilling continues to yield significant intervals of the high-grade REE dolomite carbonatite (DC) lithology. Recent flotation variability testwork has shown this type of mineralization consistently delivers high grade mineral concentrates greater than 40% TREO, at recoveries in excess of 80% (see Defense Metals news release dated October 17, 2022). All the drill holes released to date have included significant REE mineralized DC intervals. As such Defense Metals is confident the 2022 drilling results will contribute positively to the planned Preliminary Feasibility Study (PFS).”

The 100% owned 4,244 hectare Wicheeda REE Property, located approximately 80 km northeast of the city of Prince George, British Columbia, is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, the CN railway, and major highways.

The Wicheeda REE Project yielded a robust 2021 preliminary economic assessment technical report (PEA) that demonstrated an after-tax net present value (NPV@8%) of $517 million, and 18% IRR3. A unique advantage of the Wicheeda REE Project is the production of a saleable high-grade flotation-concentrate. The PEA contemplates a 1.8 Mtpa (million tonnes per year) mill throughput open pit mining operation with 1.75:1 (waste:mill feed) strip ratio over a 19 year mine (project) life producing and average of 25,423 tonnes REO annually. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

Methodology and QA/QC

The analytical work reported on herein was performed by ALS Canada Ltd. (ALS) at Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (QA/QC) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (BC) Principal and Consultant of APEX Geoscience Ltd. of Edmonton, AB, a director of Defense Metals and a “Qualified Person” as defined in NI 43-101. Mr. Raffle verified the data disclosed which includes a review of the sampling, analytical and test data underlying the information and opinions contained therein.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

____________________________

3 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, drill results including anticipated timeline of such results/assays, the Company’s plan to commence the PFS, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

Conference Call Tuesday November 15, 2022 at 11:00 AM (EST)

(All $ figures reported in USD)

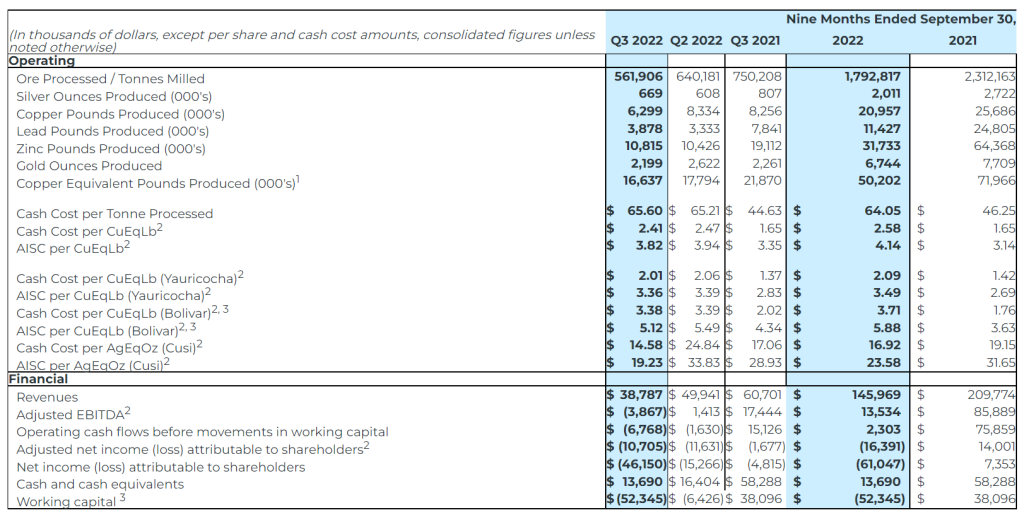

Revenue from metals payable of $38.8 million in Q3 2022, a 36% decrease from $60.7 million in Q3 2021 and a 22% decrease from the previous quarter, due to lower throughput at Yauricocha and slower ramp up at Bolivar as a result of a flooding event and operational restrictions due to limited ventilation in the Bolivar NorthWest zone.

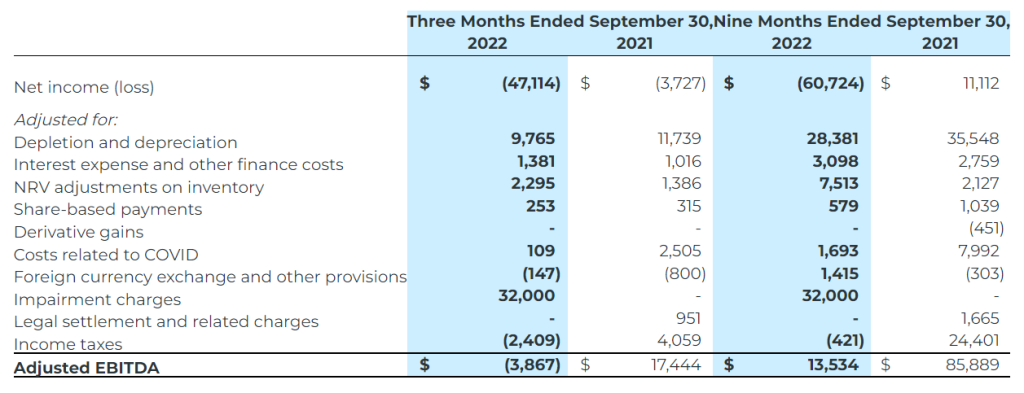

Adjusted EBITDA of $(3.9) million in Q3 2022, compared to $17.4 million in Q3 2021 and $1.4 million in Q2 2022.

Net loss attributable to shareholders for Q3 2022 of $46.2 million, or $(0.28) per share (basic and diluted), compared to a net loss of $4.8 million, or ($0.03) per share in Q3 2021, and a net loss of $15.3 million or $(0.09) per share in Q2 2022.

Net loss for Q3 2022 and 9M 2022 includes an impairment charge of $25.0 million ($nil for Q3 2021 and 9M 2021) for the Bolivar mine and $7.0 million ($nil for Q3 2021 and 9M 2021) for the Cusi mine.

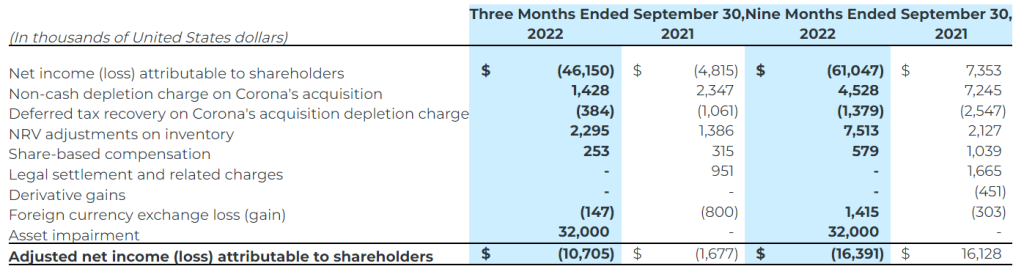

Adjusted net loss attributable to shareholders(1) of $10.7 million, or $(0.07) per share for Q3 2022, compared to adjusted net loss of $1.7 million or $(0.01) per share for Q3 2021 and an adjusted net loss of $11.6 million, or $0.07 per share for Q2 2022.

$13.7 million of cash and cash equivalents and working capital of $(52.3) million1 as at September 30, 2022.

Net Debt of $73.6 million as at September 30, 2022.

Suspension of production and financial guidance remains in effect.

1 The negative working capital is largely due to the reclassification of the long-term portion of the credit facility as current, resulting from the breach of certain debt covenants as at September 30, 2022. The Company is seeking accommodation from the lending banks in the form of waivers for this non-compliance.

A shareholder conference call will be held Tuesday, November 15, 2022, at 11:00 AM (EST). Click here to register.

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (BVL or Bolsa de Valores de Lima: SMT) (NYSE AMERICAN: SMTS) (“Sierra Metals” or “the Company”) today reported revenue of $38.8 million, a 36% decline from Q3 2021 and a 22% decline from Q2 2022, and adjusted EBITDA of $(3.9) million, a 122% decrease from Q3 2021 and a 379% decrease from Q2 2022 on throughput of 561,906 tonnes and metal production of 16.6 million copper equivalent pounds for the three-month period ended September 30, 2022.

Luis Marchese, CEO of Sierra Metals, commented, “the unexpected events during our latest quarter have made for another challenging period at Sierra Metals.

We have all been deeply impacted by the tragic mudslide incident at Yauricocha. As our primary objective remains the safety and well-being of all employees and contractors, a rigorous safety assurance process continues at the mine. Although production is ramping up, full production can only be reached once this process is complete.

In the coming months, we will continue to incorporate ore from the high-grade Fortuna zone and work towards recovery of tonnage at the Yauricocha Mine. In addition, exploration efforts will continue, both inside the mine for near term reach and in brownfield locations in close proximity to operations, in order to generate new exploration targets.”

He continued, “at Bolivar, unexpected flooding during most of the quarter in addition to the operational restrictions due to limited ventilation at the Bolivar NorthWest zone, negatively impacted throughput and grades.

On a consolidated basis, the Company’s revenues and EBITDA decreased 36% and 122%, respectively due to a 24% decrease in copper equivalent production when compared to the same quarter last year, coupled with a reduction in all metals prices, except zinc.”

He concluded, “Recent setbacks at both the Yauricocha and Bolivar Mines have prevented us from achieving full production and our turnaround goals within the initially proposed timeline, leading to suspended 2022 operating guidance. These unexpected challenges have culminated in the liquidity issues facing the Company. The Special Committee of our Board diligently continues its strategic review process. In the meantime, we remain disciplined in our approach to day-to-day operations.”

The following table displays selected financial and operational information for the three months and nine months ended September 30, 2022 compared to the corresponding periods for 2021 and the three months ended June 30, 2022:

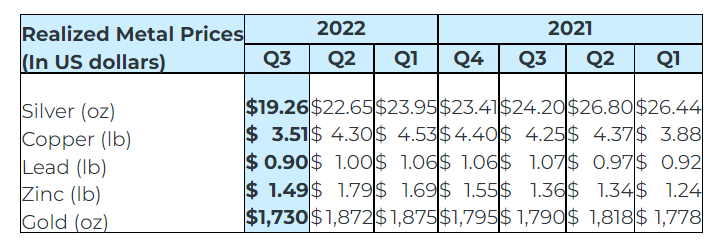

The following table shows the Company’s realized selling prices for the three months ended September 30, 2022, and each of the last six quarters:

Q3 2022 Consolidated Operating Highlights

Copper equivalent production of 16.6 million pounds; a 24% decrease from Q3 2021 and a 7% decrease from Q2 2022.

Consolidated Q3 2022 throughput of 561,906 tonnes was a 25% decrease over the Q3 2021 throughput of 750,208 tonnes. As compared to Q2 2022, consolidated throughput was 12% lower for Q3 2022.

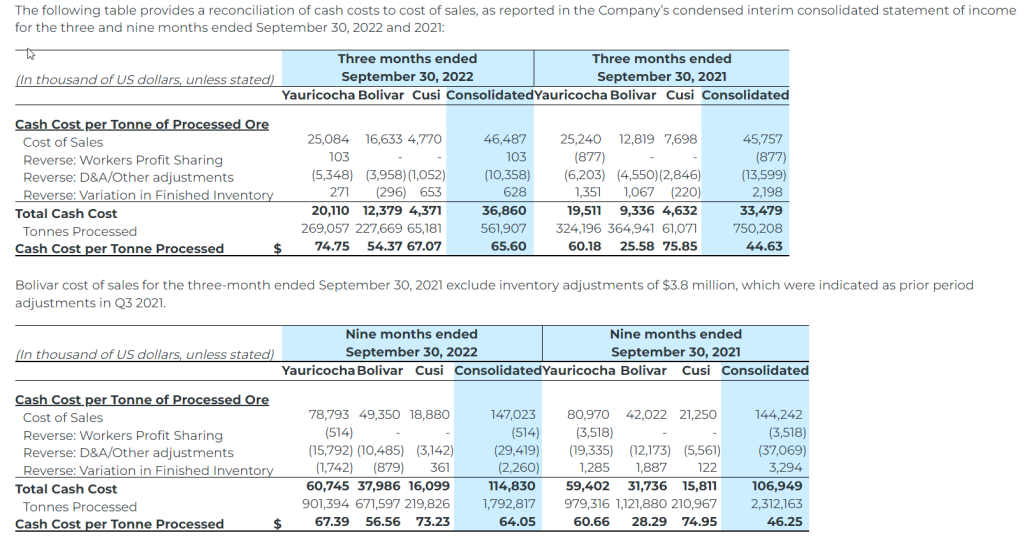

Throughput from the Yauricocha Mine during Q3 2022 was 269,057 tonnes, a 17% decline when compared to Q3 2021 due to the suspension of mining activity and work stoppages during the quarter, which resulted in a 31% decrease in copper equivalent pounds produced. Declining grades due to restricted access to non-permitted areas of the mine also affected production. When compared to the previous quarter, throughput declined by 15%.

At the Bolivar Mine, throughput was 227,669 tonnes during Q3 2022. When compared to Q3 2021, throughput at Bolivar was 38% lower and while grades were higher for silver and gold, they were not enough to offset the lower throughput, resulting in a 16% decrease in copper equivalent pounds produced. Operational ramp up has been slower than expected due to unforeseen flooding in the Bolivar NorthWest zone during the quarter. When compared to Q2 2022, an 11% decrease in throughput, along with lower grades in copper and silver, resulted in a 10% decrease in copper equivalent pound production.

At Cusi, throughput was 65,180 tonnes during Q3 2022. When compared to Q3 2021, a 7% increase in throughput, combined with higher head grades for all metals except lead, resulted in a 22% increase in silver equivalent ounces production. Cusi suffered from an unexpected flooding event that restricted access to the lower areas of the mine during the second quarter. At the beginning of Q3, access to the lower levels of the mine was still limited. While throughput was 2% lower, it was offset by higher grades in all metals, resulting in a 32% increase in silver equivalent ounces produced.

Q3 2022 Consolidated Financial Highlights

Revenues Declined Due to Decrease in Metal Sales and a Drop in Metals Prices

Revenue from metals payable of $38.8 million in Q3 2022 or a decrease of 36% over the revenue of $60.7 million in Q3 2021 due to the decrease in metal sales and the drop in average realized prices for all metals, except zinc, as compared to Q3 2021.

Revenues for Q3 2022 were 22% lower than the revenue of $49.9 million in Q2 2022, as lower production from the Yauricocha and Bolivar Mines impacted metal sales quantities. The average realized prices for Q3 2022 decreased for copper (18%), zinc (17%), lead (10%), silver (15%) and gold (8%) as compared to the same during Q2 2022.

Cost of Operations Increased at Yauricocha and Bolivar Due to Lower Throughput

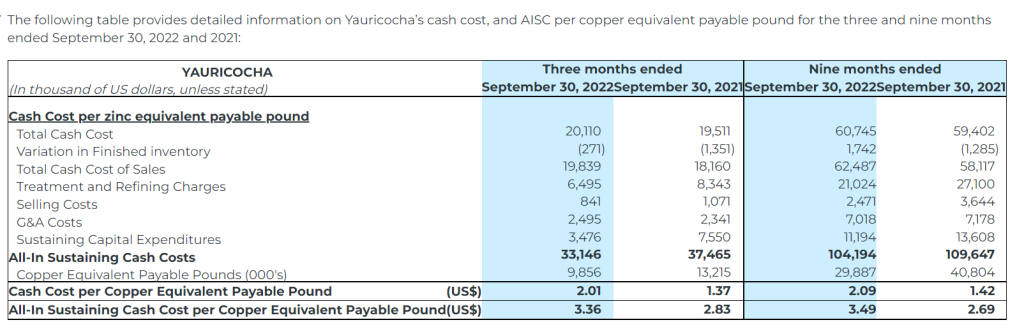

Yauricocha’s cash cost per copper equivalent payable pound was $2.01 (Q3 2021 – $1.37), and AISC (as defined herein) per copper equivalent payable pound of $3.36 (Q3 2021 – $2.83) for Q3 2022. The increase in cash costs and AISC was mainly a result of the 25% decrease in copper equivalent payable pounds as compared to Q3 2021. Despite 14% fewer copper equivalent payable pounds in Q3 2022 as compared to Q2 2022, cash cost and AISC per copper equivalent pound decreased from $2.06 and $3.39 respectively in Q2 2022, due to lower cost of sales and sustaining costs.

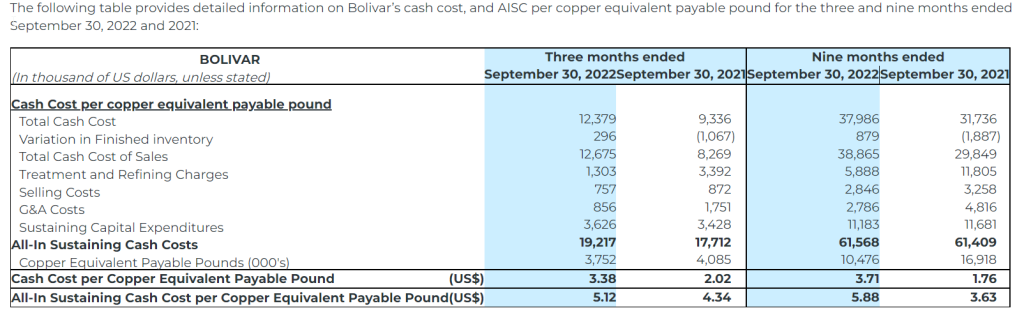

Bolivar’s cash cost per copper equivalent payable pound was $3.38 (Q3 2021 – $2.02), and AISC per copper equivalent payable pound was $5.12 (Q3 2021 – $4.34) for Q3 2022 due to higher operating costs per tonne and an 8% decrease in the copper equivalent payable pounds compared to Q3 2021. Bolivar’s Q3 2022 cash cost and AISC per copper equivalent pound decreased however from $3.39 and $5.49 respectively in Q2 2022.

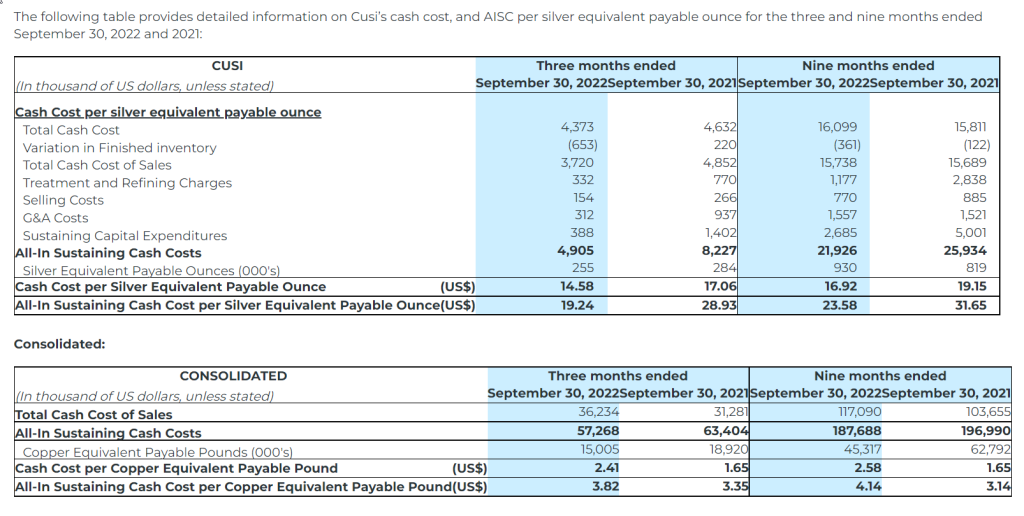

Cusi’s Q3 2022 cash cost per silver equivalent payable ounce decreased to $14.58 from $17.06 in Q3 2021 as a result of higher grades. AISC per silver equivalent payable ounce decreased to $19.23 (Q3 2021 – $28.93). Unit costs decreased during Q3 2022, despite fewer silver equivalent payable ounces, as a result of lower operating costs per tonne and lower sustaining costs during Q3 2022 as compared to Q3 2021.

EBITDA, Net Income and Cash Flow Generation Impacted by Lower Revenues and Higher Operating Costs

Adjusted EBITDA(1) decreased 122% to $(3.9) million for Q3 2022 compared to $17.4 million in Q3 2021 and a 379% decrease compared to $1.4 million in the previous quarter. The decrease in EBITDA is related to drop in revenues attributable to lower production and higher operating costs during Q3 2022.

Net loss attributable to shareholders for Q3 2022 was $46.2 million or $(0.28) per share (basic and diluted), compared to net loss of $4.8 million or $(0.03) per share (basic and diluted) in Q3 2021 and net loss of $15.3 million or $(0.09) per share (basic and diluted) in Q2 2022.

Adjusted net loss attributable to shareholders(1) of $10.7 million, or $(0.07) per share for Q3 2022, compared to adjusted net loss of $1.7 million or $(0.01) per share for Q3 2021 and adjusted net loss of $11.6 million, or $0.0 per share for Q2 2022.

Operating cash flow before movements in working capital of $(6.8) million for Q3 2022 as compared to $15.1 million of cash generated from operating activities in Q3 2021 and $(1.6) million in Q2 2022. The decrease resulted from lower revenue and higher costs during the quarter.

Cash and cash equivalents of $13.7 million and working capital of $(52.3) million as at September 30, 2022 compared to $34.9 million and $17.3 million, respectively, at the end of 2021. The negative working capital is largely the result of the reclassification of the long-term portion of the credit facility to current, as the Company defaulted on certain debt covenants as of September 30, 2022. The Company is seeking accommodation from the lending banks in the form of waivers for this non-compliance. If the Company is unable to obtain such waivers for the current and any potential future breaches of its debt covenants, it could materially and adversely affect the Company’s future operations, cash flows, earnings, results of operations, financial condition and the economic viability of its projects.

Cash and cash equivalents decreased during the nine-month period ended September 30, 2022 due to $31.2 million used in investing activities offset by $6.1 million of cash generated from operating activities and $3.8 million of cash generated from financing activities.

Financing activities included $25.0 million received from Banco de Credito del Peru (“BCP”) and Banco Santander by the Company’s subsidiary, Sociedad Minera Corona, to finance the repayment of the installments of $18.8 million on the original credit facility received from BCP.

1 This is a non-IFRS performance measure. See the Non-IFRS Performance Measures section of the MD&A.

Project Development

Mine development at Bolivar during Q3 2022 totaled 2,080 meters, which included 1,265 meters of development to prepare stopes for mine production, and 815 meters to development of ramps; and

Mine development at Cusi during Q3 2022 totaled 631 meters.

Exploration Update

Peru:

Approximately 2,532 meters of diamond drilling was completed during Q3 2022 in the Fortuna North, Katty and Violeta zones with the aim to replace and increase the depleted mineral resources. Additionally, approximately 2,000 meters of greenfield exploration drilling was completed in the Tucumachay prospect.

Mexico:

Bolivar

At Bolivar during Q3 2022, 18,318 meters were drilled in the Bolivar West, Bolivar NorthWest, the Cieneguita zones and El Gallo Superior encountering skarn intersections with mineralization. Additionally, infill drilling of 4,479 meters was completed in the Bolivar West, El Gallo Inferior and Bolivar NorthWest zones;

Cusi

During Q3 2022, the Company completed 2,196 meters of infill drilling to support the development of the Santa Rosa de Lima vein and NE Trend.

Covid-19 Update And Outlook

The COVID-19 pandemic has impacted the Company’s operations over the past two years. While there are still concerns regarding the newer variants of the virus, there is reduced pressure on the operations due to relaxed measures as the Company has achieved almost 100% vaccination rate for its employees at all locations. The additional costs related to COVID dropped to $1.7 million during the nine-month period ended September 30, 2022 as compared to $8.0 million spent during the comparative nine-month period of 2021.

Impairment Charge

Lower market capitalization due to the drop in the Company’s share price, declining metal prices, lower production and consequent decrease in profitability were considered as indicators of impairment as on September 30, 2022. The Company performed an impairment analysis for each of its cash generating units (“CGU”) using Life of Mine (“LOM”), which incorporate current operational practices, long term metal prices based on recent analyst consensus and productivity assumptions, based on recent operating experience at the mines.

The Company updated the Bolivar LOM using updated information from the mine performance, required capex, metal prices and discount rate, and concluded that an impairment of $25.0 million was required for the Bolivar CGU.

The Cusi LOM was updated for the latest metal prices and discount rate. Following this analysis, management concluded that an impairment of $7.0 million was needed for the Cusi CGU as on September 30, 2022.

The updated Yauricocha LOM did not indicate any impairment as at September 30, 2022.

Suspended Guidance

In addition to the delays in the anticipated turnaround at the Bolivar mine due to the unexpected flooding in the Bolivar NW zone during the quarter, the Company also experienced production delays at the Yauricocha mine as a result of the mudslide incident and ensuing community blockade in September. Although mining restarted in parts of Yauricocha in October, the Company is following due assurance processes to ensure safe operations in the remaining sections of the mine. In view of these delays, the Company has suspended its production and financial guidance for 2022.

Strategic Review Process

In response to liquidity challenges from an accumulation of operational losses and negative cashflows, primarily from its Mexican operations, the Company announced, on October 18, 2022, the formation of a Special Committee and the initiation of a strategic review process.

The mandate of the Special Committee, comprised of its independent directors, includes exploring, reviewing and considering options to optimize the operations of the Company and possible financing, restructuring and strategic options in the best interests of the Company. Financial and legal advisors with particular expertise in turnaround and restructuring matters have been engaged to advise on this process.

The Company has engaged CIBC Capital Markets as a financial advisor in this process.

Delisting

As previously announced, the Company will voluntarily delist its common shares from the New York Stock Exchange American (“NYSE”) and the Bolsa de Valores de Lima (“BVL”). The final day of trading on the NYSE was today, November 14, 2022 with shares to be suspended from trading before market open on November 15, 2022.

The Company is continuing to pursue its BVL delisting and suspension from trading is anticipated later during the year. An update will be provided once a final trading date of the common shares on the BVL has been confirmed.

The Company’s common shares will continue to be listed and traded in Canadian dollars on the Toronto Stock Exchange.

Conference Call and Webcast

Sierra Metals’ senior management will host a conference call on Tuesday, November 15, 2022, at 11:00 AM (EDT) to discuss the Company’s financial and operating results for the three months ended September 30, 2022.

Via Webcast:

A live audio webcast of the meeting will be available on the Company’s website:

The webcast, along with presentation slides, will be archived for 180 days on www.sierrametals.com.

Via phone:

For those who prefer to listen by phone, dial-in instructions are below. To ensure your participation, please call approximately five minutes prior to the scheduled start time of the call.

Canada dial-in number (Toll Free): 1 833 950 0062 Canada dial-in number (Local): 1 226 828 7575 US dial-in number (Toll Free): 1 844 200 6205 US dial-in number (Local): 1 646 904 5544 All other locations: +1 929 526 1599

Access code: 991150

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance

Non-IFRS Performance Measures

The non-IFRS performance measures presented do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be directly comparable to similar measures presented by other issuers.

Non-IFRS reconciliation of adjusted EBITDA

EBITDA is a non-IFRS measure that represents an indication of the Company’s continuing capacity to generate earnings from operations before taking into account management’s financing decisions and costs of consuming capital assets, which vary according to their vintage, technological currency, and management’s estimate of their useful life. EBITDA comprises revenue less operating expenses before interest expense (income), property, plant and equipment amortization and depletion, and income taxes. Adjusted EBITDA has been included in this document. Under IFRS, entities must reflect in compensation expense the cost of share-based payments. In the Company’s circumstances, share-based payments involve a significant accrual of amounts that will not be settled in cash but are settled by the issuance of shares in exchange for cash. As such, the Company has made an entity specific adjustment to EBITDA for these expenses. The Company has also made an entity-specific adjustment to the foreign currency exchange (gain)/loss. The Company considers cash flow before movements in working capital to be the IFRS performance measure that is most closely comparable to adjusted EBITDA.

The following table provides a reconciliation of adjusted EBITDA to the condensed interim consolidated financial statements for the three and nine months ended September 30, 2022 and 2021:

Non-IFRS reconciliation of adjusted net income

The Company has included the non-IFRS financial performance measure of adjusted net income, defined by management as the net income attributable to shareholders shown in the statement of earnings plus the non-cash depletion charge due to the acquisition of Corona and the corresponding deferred tax recovery and certain non-recurring or non-cash items such as share-based compensation and foreign currency exchange (gains) losses. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors may want to use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS.

The following table provides a reconciliation of adjusted net income to the condensed interim consolidated financial statements for the three and nine months ended September 30, 2022 and 2021:

Cash cost per silver equivalent payable ounce and copper equivalent payable pound

The Company uses the non-IFRS measure of cash cost per silver equivalent ounce and copper equivalent payable pound to manage and evaluate operating performance. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

All-in sustaining cost per silver equivalent payable ounce and copper equivalent payable pound

All‐In Sustaining Cost (“AISC”) is a non‐IFRS measure and was calculated based on guidance provided by the World Gold Council (“WGC”) in June 2013. WGC is not a regulatory industry organization and does not have the authority to develop accounting standards for disclosure requirements. Other mining companies may calculate AISC differently as a result of differences in underlying accounting principles and policies applied, as well as differences in definitions of sustaining versus development capital expenditures.

AISC is a more comprehensive measure than cash cost per ounce/pound for the Company’s consolidated operating performance by providing greater visibility, comparability and representation of the total costs associated with producing silver and copper from its current operations.

The Company defines sustaining capital expenditures as, “costs incurred to sustain and maintain existing assets at current productive capacity and constant planned levels of productive output without resulting in an increase in the life of assets, future earnings, or improvements in recovery or grade. Sustaining capital includes costs required to improve/enhance assets to minimum standards for reliability, environmental or safety requirements. Sustaining capital expenditures excludes all expenditures at the Company’s new projects and certain expenditures at current operations which are deemed expansionary in nature.”

Consolidated AISC includes total production cash costs incurred at the Company’s mining operations, including treatment and refining charges and selling costs, which forms the basis of the Company’s total cash costs. Additionally, the Company includes sustaining capital expenditures and corporate general and administrative expenses. AISC by mine does not include certain corporate and non‐cash items such as general and administrative expense and share-based payments. The Company believes that this measure represents the total sustainable costs of producing silver and copper from current operations and provides the Company and other stakeholders of the Company with additional information of the Company’s operational performance and ability to generate cash flows. As the measure seeks to reflect the full cost of silver and copper production from current operations, new project capital and expansionary capital at current operations are not included. Certain other cash expenditures, including tax payments, dividends and financing costs are also not included.

Additional non-IFRS measures

The Company uses other financial measures, the presentation of which is not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. This includes:

Operating cash flows before movements in working capital – excludes the movement from period-to-period in working capital items including trade and other receivables, prepaid expenses, deposits, inventories, trade and other payables and the effects of foreign exchange rates on these items.

This term does not have a standardized meaning prescribed by IFRS, and therefore the Company’s definition is unlikely to be comparable to similar measures presented by other companies. The Company’s management believes that their presentation provides useful information to investors because cash flows generated from operations before changes in working capital excludes the movement in working capital items. This, in management’s view, provides useful information of the Company’s cash flows from operations and is considered to be meaningful in evaluating the Company’s past financial performance or its future prospects. The most comparable IFRS measure is cash flows from operating activities.

Qualified Persons

Américo Zuzunaga, FAusIMM (Mining Engineer) Vice President, Technical is a Qualified Person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company with Green Metal exposure including increasing copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. Sierra Metals has recently had several new key discoveries and still has many more exciting brownfield exploration opportunities at all three Mines in Peru and Mexico that are within close proximity to the existing mines. Additionally, the Company also has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com.

This press release contains forward-looking information within the meaning of Canadian and United States securities legislation, including with respect to timing of the conference call, exploration and production plans and the delisting of the Company’s common shares. Forward-looking information relates to future events or the anticipated performance of Sierra and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra to be materially different from any anticipated performance expressed or implied by such forward-looking information.