Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Drilling nearing completion. Defense Metals released results for the first two drill holes, representing 720 meters of drilling, associated with the company’s ongoing 2022 diamond drill program. To date, 15 drill holes, representing 4,800 meters of drilling, have been completed. In aggregate, the company expects to complete 5,000 meters of drilling in 18 holes to upgrade existing resource categories. The company is completing remaining pit slope geotechnical and hydrogeological holes. The initial results were favorable and demonstrate continuity of mineralization over significant widths. Investors should expect a steady flow of assay results from the company in the weeks and months ahead.

Encouraging drill results. Hole WI22-64 returned a broad mineralized intercept of high-grade dolomite carbonate in the upper portions of the hole, and mixed mineralized xenolithic dolomite carbonate and syenite at depth averaging 1.78% total rare earth oxide (TREO) over 192 meters, including 3.13% TREO over 73 meters. The partial assays reported for WI22-64, one of the deepest holes drilled to date, are from surface to a depth of 284 meters. Results for the remaining 101 meters to the end of hole at 384.5 meters are expected shortly. Hole WI22-62 collared 120 meters to the north of WI22-64, intersected a 109-meter interval of mineralized dolomite carbonatite returning 1.39% TREO over 167 meters, including 2.29% TREO over 48 meters.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

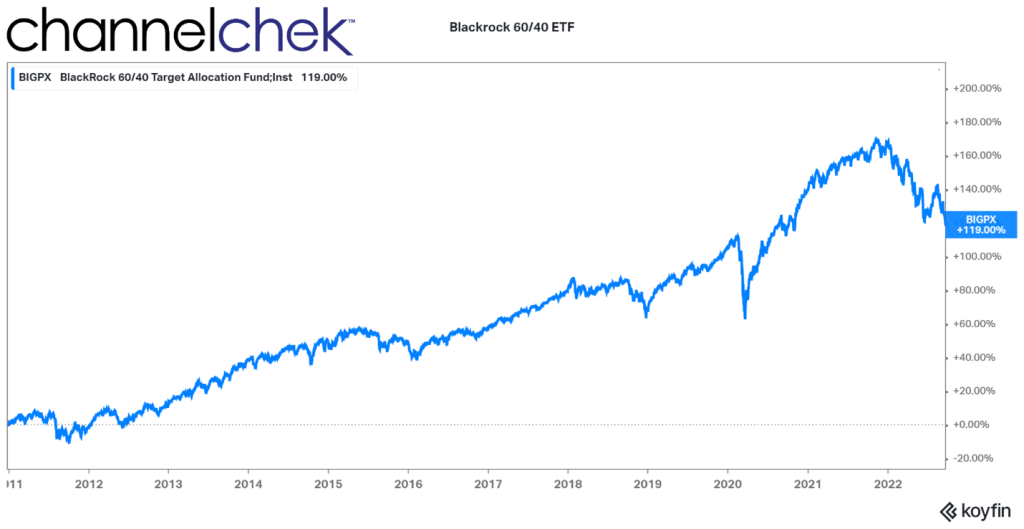

Owning a Balanced Diversified Investment Portfolio Has Been Like Watching a Train Wreck

From the time that most realized the Fed would aggressively deal with inflation, watching the classic 60/40 balanced portfolio has been like watching a slow train wreck.

Diversification, balance, a 60/40 allocation have been the marching orders from those “in the know.” But what do you do when you’re terribly sure that the 40% in bonds will be worth less tomorrow, and the 60% in a standard stock index is more likely to be down than up? This is the question investors, wealth managers, and retirees have been faced with since early in 2022. The Chair of the Federal Reserve promised to raise rates, so the 40% allocation in bonds has been almost guaranteed by a Federal agency to perform worse than cash in your pillow case, and when interest rates rise, the economy does worse, which at first weighs down stock indexes.

Advisors want their customers to sleep better at night, so they tell them not to worry, no one can call the market, you don’t want to miss the up days. Every time, the markets have bailed them out, and there is no reason not to think that there won’t continue to be eventual increases on one side or the other of the investment pie chart. Meanwhile, missing predictable down periods are just as important to exceptional long-term results as being invested when values rise.

60/40 101

The classic portfolio of 60% stocks and 40% bonds touted in articles by wealth managers and certified by textbooks on investing may no longer provide the same level of returns that it delivered previously. Or it may be going through a period where the direction of stocks and bonds is highly correlated – and it will at some point turn the corner to balanced performance.

From the 1980s until recently, a portfolio of 60% stocks and 40% bonds did well for investors and for good reason. The mix consistently provided investors with attractive risk-adjusted returns, with total returns often equal to or better than those of the S&P 500 Index and with lower volatility. In a more natural market, rates come down (bond bull market) when the economy is weak, which brings stock prices down (stock bear market) and visa versa. The investor always has positions in a bull market to partially offset losses from the other side of the portfolio.

Recent History of Balanced Portfolios

But this strategy hasn’t really worked for decades. Many haven’t noticed because its not working has benefitted investors. Debt and equity prices have moved in the same direction. Both stocks and bonds have reached new highs through last year. Investors aren’t critical when they’re making money, but both markets joined hands long ago and have been mostly moving in the same direction. Here’s your evidence; in 1982, a 30 year-treasury bond was issued, paying over 14%. Today the 30-year is paying 3.65%. So the bond market, with slight ups and downs, has been strong for most of the last 40 years. The S&P 500 in 1982 closed at 120. Today, the same index is at 3,675. Both markets, although not always trading hand in hand, more often than not rise and fall together.

Image: 60:40 Blackrock portfolio performance since 2011 (Koyfin

60/40 in 2022

The protection of hiding behind a broad, diversified index of stocks and conservative (supposedly uncorrelated) bonds is certainly showing its weakness this year. Persistent structural inflation adding to interest rates and negative GDP growth have battered both markets. It exposes that 60/40 is not perfect and that set-it and forget-it could cause many to have large drawdowns that will require huge percentage increases in the future.

What to Do

When the most powerful mover of assets transparently says they are going to do something that will impact the markets, believe that the odds are that they will. In other words, don’t fight the Fed. This could mean a slight to a total reduction in bonds, why watch your bond portfolio become a train wreck. And if you are in bond funds, a move to individual bonds offers the solace of at least knowing they mature at par.

The stock portfolio is trickier. The equities market will turn around when there are signs that the economy has bottomed out. Currently, there are some signs of weakness, but mostly expectations of great weakness as we know the Fed is resolved to tame inflation. Investors will race to be first in on the most recent dip. Selectively picking stocks that have a good reason to outperform now and be strong later when bullishness returns is likely smarter than holding a broad-based index. The broad-based economy is headed lower, so it stands to reason the broad-based indexes have further to fall.

Don’t be a stranger to analysts’ reports on individual companies. Expert, unbiased analysis of sectors and individual stocks can help you uncover those that are unlinked to negative world events or are taking advantage of global changes.

Cash was trash when rates were near zero. Currently, a three-month T-Bill yields around 3.75%. Other short and safe securities are closer to 4%. When there is a recognizable turnaround, you’ll want ammunition. Keep some dry powder to be able to pounce; today’s short interest rates provide returns above those expected in the major indexes. Check with your broker to find out how to invest in short-term agencies, T-Bills, or broker CDs so you are ready for when the Fed says they are in a wait-and-see mode, for when GDP shows we are clearly not in a recession, for when corporate earnings are on the rise, and for when interest rates on bonds are closer to a level that produces low inflation numbers.

Take Away

Stocks and bonds have mostly been moving in the same direction for a very long time. Both were moving up, so no one noticed.

Cash is also an option in any portfolio, and you’re now getting paid more. If the Fed continues to suggest rates are rising, it practically ensures lower bond prices. Move to cash or carefully selected equities. Look for quality analysis of sectors and stocks before jumping into a stock. News stories, statistics, and often research and analysis on small-cap opportunities are available for those signed-up for Channelchek emails, along with many other no-cost perks.

Decision To Switch Ethereum To Proof-Of-Stake May Have Been Based On Misleading Energy FUD

After countless delays, the Ethereum “Merge” finally took place last week, switching the blockchain protocol from proof-of-work (PoW) to proof-of-stake (PoS).

What this means, in brief, is that Ethereum’s native coin, Ether (ETH)—the world’s second largest digital asset following Bitcoin (BTC)—can no longer be mined using a graphics processing unit (GPU). Instead, participants can choose to “stake” their ETH on the network. The Ethereum network then selects which of these participants, known as “validators,” gets to validate transactions, and if such validations are found to be accurate and legitimate, participants are rewarded with new ETH blocks.

This article was republished with permission from Frank Talk, a CEO Blog by Frank Holmes of U.S. Global Investors (GROW). Find more of Frank’s articles here – Originally published September 21, 2022

So what’s the catch? Well, there are a couple of big ones:

1) To become a validator, participants must stake at least 32 ETH, the equivalent of $43,000 at today’s prices, and

2) They must stake them for years.

You can see, then, how the Merge has transformed ETH from a decentralized asset, available to any young gamer with access to a decent GPU, to more of a centralized, oligarchic asset, controlled by a relatively few participants who already own tens of thousands of dollars’ worth of ETH.

In fact, as CoinDesk reported last week, two large validators were responsible for over 40% of the new ETH blocks that were added in the hours post-Merge. Those validators are crypto exchange platform Coinbase and crypto staking service Lido Finance.

PoS Puts Ether in Regulators’ Crosshairs

But wait, there’s more. By converting to PoS, Ether risks being seen by U.S. regulators as a proof-of-security asset. Last Friday, the White House published its first-ever crypto regulatory framework, just a day after the merge was completed.

Gary Gensler, head of the Securities and Exchange Commission (SEC), has said on numerous occasions that PoW assets such as BTC are commodities, not securities, and should therefore not be regulated as securities.

That’s not the case with PoS, according to Gensler. Last week, the SEC chief commented that digital assets that allow investors to stake their holdings in exchange for new coins may qualify them as securities. The implication, of course, is that oversight of these coins may end up being just as rigorous as that of stocks, bonds, ETFs and other highly regulated assets. Besides ETH, other popular PoS cryptocurrencies include Cardano, Polkadot and Avalanche.

The May crash of Terra’s Luna coin, which triggered the collapse of overleveraged crypto lenders such as Celsius, Voyager and Three Arrows Capital, was a major driver of this year’s crypto winter. Lenders’ promises of high returns on investment have landed them in financial and legal hot water. It’s very important that the Ethereum Foundation not make the same mistakes and invite the same level of scrutiny.

As we like to say at U.S. Global Investors, government policy is a precursor to change. But the change, in this case, may not turn out to be favorable. Regulatory pronouncements could add to volatility within the nascent cryptocurrency industry.

In the table below, you can see that ETH was one of the most volatile assets for the one-day and 10-day trading periods as of August 31—more volatile, in fact, than BTC and shares of Tesla. I can’t help believing that’s due to investors’ apprehension of the merge and the regulatory uncertainty that surrounds it.

The DNA of Volatility

Standard Deviation For One-Year, As of August 30, 2022

ONE-DAY

TEN-DAY

Gold Bullion

±1%

±3%

S&P 500

±1%

±4%

Bitcoin

±4%

±11%

Tesla

±4%

±13%

Ethereum

±5%

±15%

MicroStrategy

±6%

±19%

Energy FUD Contributed to Decision to Transition to PoS

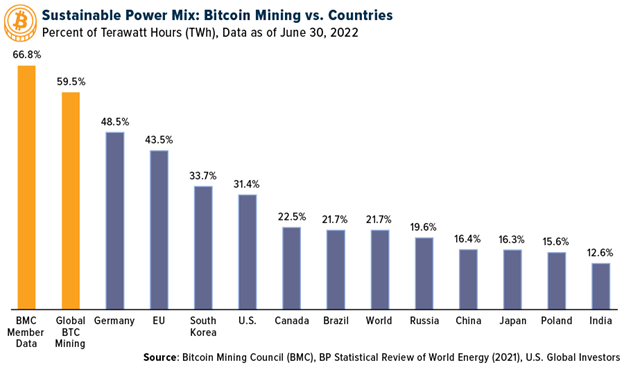

If everything I’ve said up until this point is the case, why did Ethereum decision-makers choose to switch to PoS in the first place? Simply put, they folded under pressure from misleading charges that crypto mining, particularly BTC mining, consumes too much energy and is bad for the environment.

This is FUD, or fear, uncertainty and doubt. Yes, BTC mining requires electricity, but compared to nearly every other major industry—including finance and insurance, household appliances and gold mining—energy consumption is incredibly negligible, according to the Bitcoin Mining Council (BMC). What’s more, the BMC found that global BTC miners collectively use a higher sustainable energy mix than every major economy on the planet.

Supporters of the ETH Merge say that the move to PoS could cut the network’s energy usage by as much as 99.5%. None other than the World Economic Forum (WEF) praised the success of the merge last week, writing that crypto “has been waiting for a recalibration towards sustainability… for Web3 climate innovators, the new generation of environmental advocates, as well as U.S. climate efforts more broadly.”

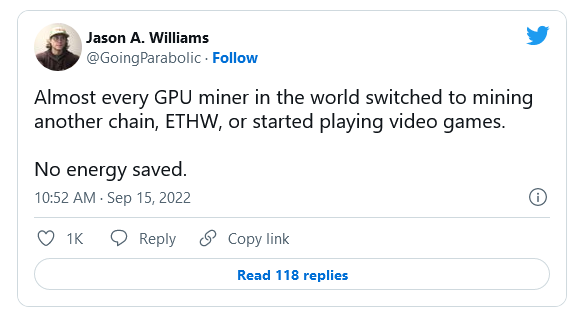

But as many PoW proponents have rightfully pointed out, the GPUs that were previously used to mine ETH will likely now be used for other purposes post-merge, including mining other coins, high-performance computing and gaming. In reality, little to no energy will have been offset.

The question is: Who is funding the FUD about PoW and energy usage? It’s a complicated question.

Last week, a group of environmental activists, including Greenpeace and the Environment Working Group (EWG), announced that it plans to spend $1 million on a new campaign to encourage Bitcoin to follow ETH’s lead and move to PoS. The campaign, titled “Change the Code, Not the Climate,” falsely claims that BTC “fuels” the climate crisis.

This is the same covert tactic used by Russian president Vladimir Putin, who over the years has funded environmental groups and non-governmental organizations (NGOs) in the West in an effort to discredit and undermine the U.S. fracking industry.

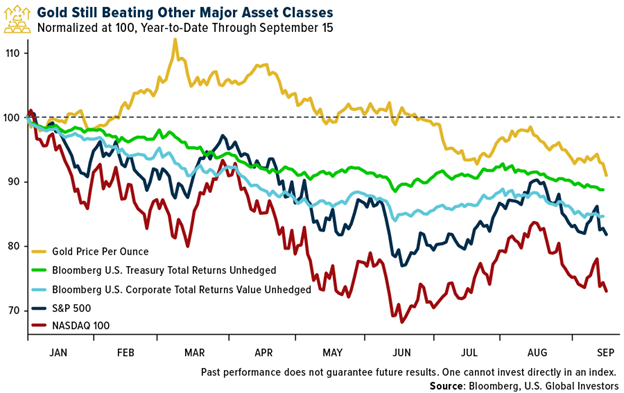

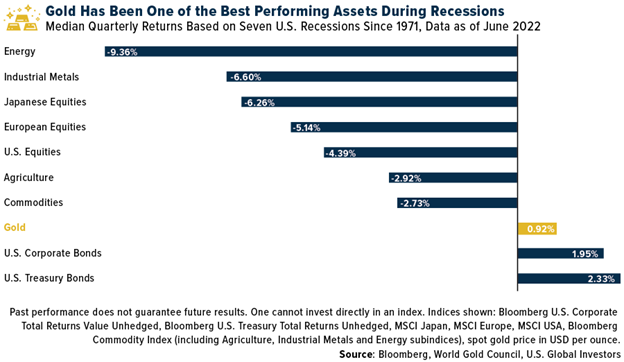

Surprise! Gold Is Still One of the Best Performing Assets of 2022

Switching gears, I want to say a few words on gold. BTC’s analogue cousin hit its lowest price since 2020 last week even as inflation remains near 40-year highs and recession fears persist. As I write this, the yellow metal is trading at around $1,666 an ounce, approximately 19% off its peak in March this year.

Some investors may read this and jump to the conclusion that gold is no longer a valuable asset during times of economic and financial uncertainty, but they would be mistaken. Although gold is down for the year, it’s nevertheless outperforming most major asset classes including Treasury bonds, U.S. corporate bonds, the S&P 500 and tech stocks. The precious metal has therefore helped investors mitigate losses in other areas of their portfolio.

The latest report by the World Gold Council (WGC) also makes the case that gold could be a powerful investment in the face of a potential economic recession. The London-based group compared the performance of a number of asset classes during the past seven U.S. recessions going back to 1971, and it found that gold performed the best on average aside from government and corporate bonds.

That said, I still recommend a 10% weighting in gold, with 5% in bullion (bars, coins, jewelry) and 5% in high-quality gold mining stocks and funds. Remember to rebalance on a regular basis.

US Global Investors Disclaimer

The Bloomberg US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint but are part of a separate Short Treasury Index. The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers. The NASDAQ-100 Index is a modified capitalization-weighted index of the 100 largest and most active non-financial domestic and international issues listed on the NASDAQ. The MSCI Japan Index is a free-float weighted equity JPY index. It was developed with a base value of 100 as of December 31, 1969. The MSCI Europe Index in EUR is a free-float weighted equity index measuring the performance of Europe Developed Markets. It was developed with a base value of 100 as of December 31, 1998. The MSCI USA Index is a free-float weighted equity index. It was developed with a base value of 100 as of December 31, 1969. Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification. The S&P 500 is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Standard deviation is a quantity calculated to indicate the extent of deviation r a group as a whole.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/22): Tesla Inc.

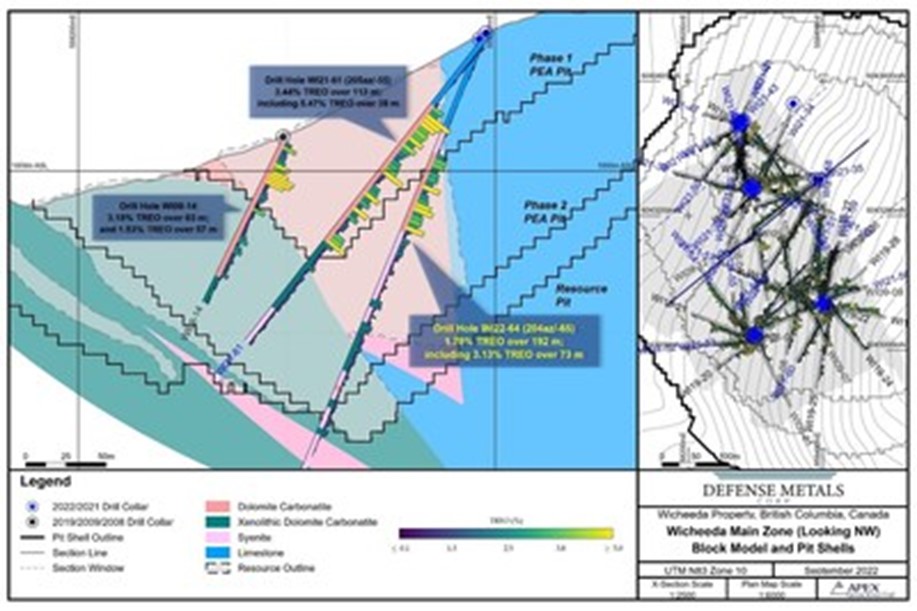

VANCOUVER, BC, Sept. 22, 2022 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company“) ( TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce results for the first two drill holes totalling 720 metres from the Company’s 2022 diamond drill program that is still underway. To date, a total of 15 drill holes totalling 4,800 metres have been completed of a planned 18 holes totalling 5,000 metres (96% complete) designed to upgrade existing resource categories. Drill holes WI22-64 and WI22-62, the first and third holes drilled, were collared from the two sites within the northern area of the Wicheeda Rare Earth Element (REE) deposit.

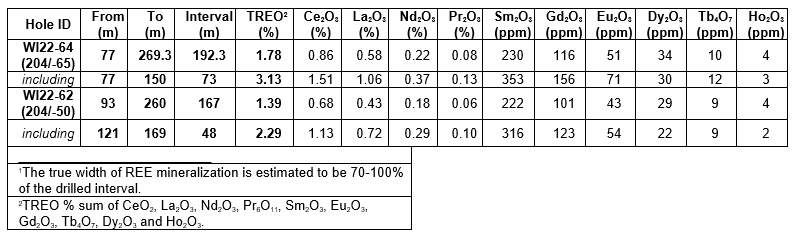

Infill drill hole WI22-64 (-65o dip / 204o azimuth) drilled southwest to depth within central area of the deposit yield a broad mineralized intercept of high-grade dolomite carbonate higher in the hole, and mixed mineralized xenolithic dolomite carbonate and syenite at depth averaging 1.78% total rare earth oxide (TREO) over 192 metres; including 3.13% TREO over 73 metres1 (Figure 1). The assays reported for WI22-64, one of the deepest holes drilled to date on the Wicheeda Project are partial from surface to a downhole depth of 284 metres. Assay results for the remaining 101 metres to end of hole at 384.5 metres are expected in the coming days.

Drill hole WI21-64 (-50o dip / 204o azimuth) collared 120 metres to the north of WI21-64, intersected a 109 metre drilled interval of mineralized dolomite carbonatite above a mixed xenolithic dolomite carbonatite and syenite at depth returning 1.39% TREO over 167 metres; including 2.29% TREO over 48 metres1 (Figure 2).

Kristopher Raffle, P.Geo. and Director and QP of Defense Metals stated: “We are pleased to have started receiving assays for our ongoing 2022 Wicheeda REE Deposit infill drilling campaign. These initial results compare very favourably to our PEA mineral resource cut-off of 0.5% TREO and continue to demonstrate continuity of mineralization over significant widths. We expect additional results in the coming days, weeks, and months ahead. With the 2022 drill campaign now 96% complete, we look forward to finishing a small number of remaining pit slope geotechnical and hydrogeological holes designed to inform any Preliminary Feasibility Studies.”

The 100% owned 4,244-hectare Wicheeda REE Property, located approximately 80 km northeast of the city of Prince George, British Columbia, is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, the CN railway, and major highways.

The Wicheeda REE Project yielded a robust 2021 preliminary economic assessment technical report (PEA) that demonstrated an after-tax net present value (NPV@8%) of $517 million, and 18% IRR3. A unique advantage of the Wicheeda REE Project is the production of a saleable high-grade flotation-concentrate. The PEA contemplates a 1.8 Mtpa (million tonnes per year) mill throughput open pit mining operation with 1.75:1 (waste:mill feed) strip ratio over a 19 year mine (project) life producing and average of 25,423 tonnes REO annually. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

____________________________

3 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Methodology and QA/QC

The analytical work reported on herein was performed by ALS Canada Ltd. (ALS) at Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (QA/QC) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (BC) Principal and Consultant of APEX Geoscience Ltd. of Edmonton, AB, a director of Defense Metals and a “Qualified Person” as defined in NI 43-101. Mr. Raffle verified the data disclosed which includes a review of the sampling, analytical and test data underlying the information and opinions contained therein.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward‐looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, drill results including anticipated timeline of such results/assays, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, Wicheeda site visit and expected outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward‐looking statements or forward‐looking information, except as required by law.

SOURCE Defense Metals Corp.

For further information: Todd Hanas, Bluesky Corporate Communications Ltd., Vice President, Investor Relations, Tel: (778) 994 8072, Email: todd@blueskycorp.ca

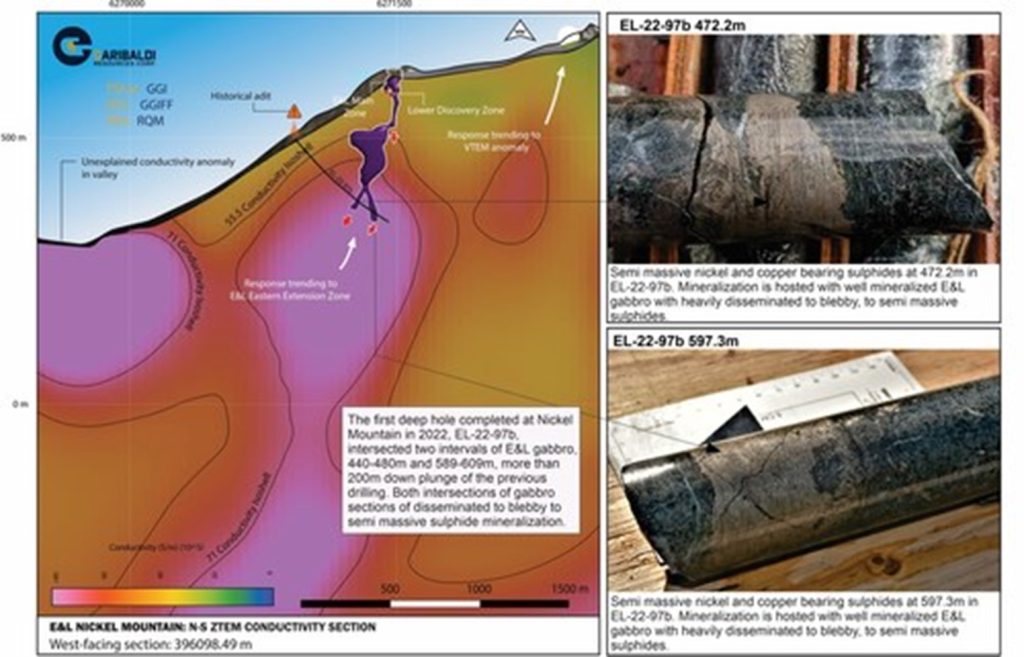

VANCOUVER, BC, Sept. 22, 2022 /CNW/ – Garibaldi Resources ( TSXV: GGI) (the “Company” or “Garibaldi“) is pleased to announce that diamond drill-hole EL-22-97b has intersected nickel-bearing disseminated and semi-massive sulphide mineralization. The mineralization is hosted by taxitic and orbicular-textured gabbro and pyroxene peridotite 205 meters down-trend of the previous deepest mineralized intercept at E&L on Nickel Mountain. The drill hole targeted the down plunge extension of the eastern zone of the E&L Intrusion, coincident with a large-scale low resistivity / elevated conductivity ZTEM anomaly identified last season by Geotech’s deep-penetrating ZTEM survey.

Figure 1 – West facing section showing drill trace EL-22-97b which intersected two intervals of E&L gabbro 200m down plunge of previous drilling . Both intersections of gabbro contain sections of well mineralized E&L gabbro with disseminated, blebby, and semi massive sulphide. The gabbro sections occur along the plane of the E&L intrusion coincident with a large scale ZTEM resistivity anomaly more than 3 km in depth. (CNW Group/Garibaldi Resources Corp.)

Garibaldi’s 2022 drill program is focused on testing several large-scale low resistivity ZTEM anomalies within the Company’s 100% owned E&L nickel-copper-cobalt massive sulphide project. E&L mineralization also contains gold, silver, platinum group metals platinum, palladium (PGM’S) together with rhodium, iridium, and ruthenium (collectively termed PGEs). The 180 sq. km. claim group is centered in the heart of the Eskay District within the Golden Triangle of Northwest British Columbia.

The latest intercept is in the plane of the E&L Intrusion, and rests immediately below the Eastern Extension mineralization associated with a differentiated sequence of peridotitic and gabbroic rocks. The complex orbicular textures in the gabbros are characteristic of the E&L Intrusion in both the Eastern Extension and the newly identified root zone ~200m below. The target was drilled as a major step-out from the known intrusion to establish whether a low resistivity ZTEM anomaly beneath E&L corresponds to the plane of additional mineralized segments of the intrusion within the plane of prospective geology. The discovery of mineralized taxitic and orbicular-textured gabbros and pyroxene peridotite expands the potential scale of mineralization well below the previously drill tested 600 x 650 meter plane of the mineralized E&L Intrusion. Most importantly, drill hole EL-22-97b demonstrates the potential for mineralization coincident with the plane of the E&L intrusion at depth within the anomalous zone identified by the ZTEM survey.

Exploration Highlights:

Hole EL-22-97b extends E&L mineralization more than 205 meters down trend from previous drilling. The drill hole was collared 383m downslope from EL-20-91 and 92, and 216m east of and below the adit, cutting through the plane of the E&L Intrusion, allowing for more efficient drilling operations and providing an optimal Bore-hole Electro-Magnetic (BH-EM) platform for surveying.

E&L intrusion rock types were intercepted from 440 – 480m, and 589 – 609m with semi-massive sulphides occurring at 472.2 and 597.3m. Portable XRF measurements taken on these sulphide grains returned 2.8% Ni and 1.1% Ni, respectively. *

The sulphide-bearing rocks of the intrusion plunge for more than 800 meters and remain open beneath the E&L Intrusion.

These intercepts of mineralized E&L type rocks are in the plane of the E&L Intrusion, and coincide with the footprint of the previously modelled ZTEM anomaly, which extends for more than 3 km.

The drill hole was designed to test the plane of the E&L Intrusion at depth below previous drilling and successfully intercepted two intervals of E&L gabbro, which contain sections of disseminated, blebby and semi massive sulphides.

The hole has been lined from top to bottom with PVC to facilitate Borehole Electromagnetic surveys.

Jeremy Hanson, Garibaldi VP-Exploration, stated: “We are very encouraged by the results from EL-22-97b, we took a 200m step-out down plunge and intercepted multiple intervals of mineralized E&L type intrusive rocks with disseminated and semi-massive nickel bearing sulphides. Typically, when we find disseminated and semi-massive sulphides, massive sulphides are not too far away.”

Dr. Peter Lightfoot, Technical Advisor to Garibaldi, stated: “The complex assemblage of taxitic and orbicular-textured gabbros together with olivine pyroxenite encountered in drill hole EL-22-97b indicates that the E&L mineral system extends to depth along the predicted planar path. Significant exploration step-outs to test this plane will greatly improve our efforts to locate extensions of mineral zones using borehole EM methods.”

Nickel Mountain Section

Steve Regoci, Garibaldi CEO stated “This first hole, provides strong support for the proposition that ZTEM responses may represent the expression of a mineralized system. We’re anxious to drill test the deep seated ZTEM targets along the 15km base metal corridor of the NMGC to Mount Shirley for sulphide minerals.”

EL-22-97 was initially collared upslope of the adit at 396390 mE 6271118mN, 1567 masl, at 367°/-70° but failed to progress through difficult ground at 232m. The hole was abandoned well before target depth. EL-22-97b was recollared 213m downslope at 396442 mE, 6270938mN, 1463m masl at 342°/-50°. This hole succeeded to target depth and encountered mineralization at the initial area of interest targeted in EL-22-97.

Quality Assurance/Quality Control (QA/QC)

Garibaldi Resources has applied a rigorous quality assurance/quality control program at the E&L Nickel Mountain Project using best industry practice. All core is logged by a geoscientist and selected intervals sampled. HQ and NQ drill core is sawn in half and each sample half is placed in a marked sample bag with a corresponding sample tag then sealed. The remaining half core is retained in core boxes that are stored at a secure facility in Smithers, British Columbia. Chain of custody of samples is recorded and maintained for all samples from the drill to the laboratory.

All diamond drilling sample batches included 5% QA/QC samples consisting of certified blanks, standards and field duplicates. Multiple certified ore assay laboratory standards and one blank standard were used in the process. Samples were submitted to SGS Canada Inc. in Vancouver, British Columbia, an ISO 9001: 2008 certified lab, for base metal, sulphur and precious metal analysis using Inductivity Coupled Plasma (ICP), Fire Assay (FA) and Leco methods. Samples were prepared by crushing the entire sample to 75% passing 2mm, riffle splitting 250g and pulverizing the split to better than 85% passing 75 microns. Gold, platinum and palladium were analyzed using a 30-gram fire assay and ICP-AES. Total sulphur and total carbon were analyzed using a Leco method. Nickel, copper, cobalt, silver and base metals were analyzed by sodium peroxide fusion and ICP-MS. The performance on the blind standards, blanks and duplicates achieved high levels of accuracy and reproducibility and has been verified by Jeremy Hanson, a qualified person as defined by NI-43-101. *XRF measurements were taken with a Niton XL5. XRF measurements analyze a very small, select section of material approximately 0.16cm2 per measurement and results are not representative of the overall rock or material.

Qualified Person & Data Verification

Jeremy Hanson, P.Geo., a qualified person as defined by NI- 43-101, has supervised the preparation of and reviewed and approved of the disclosure of information in this news release. Mr. Hanson has verified the data, including drilling, sampling, test and recovery data, by supervising all of such procedures. There are no known factors that could materially affect the reliability of data collected and verified under his supervision. No quality assurance/quality control issues have been identified to date.

About Garibaldi

Garibaldi Resources Corp. is an active Canadian-based junior exploration company focused on creating shareholder value through discoveries and strategic development of its assets in some of the most prolific mining regions in British Columbia and Mexico.

We seek safe harbor.

GARIBALDI RESOURCES CORP.

Per: “Steve Regoci” Steve Regoci, President

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or the accuracy of this release

SOURCE Garibaldi Resources Corp.

For further information: GARIBALDI RESOURCES CORP., 1150 – 409 Granville Street, Vancouver, BC V6C 1T2, Telephone: (604) 488-8851, Website: GaribaldiResources.com

NEW YORK, NY / ACCESSWIRE / September 22, 2022 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME)(TSXV:GAME), a data-driven, gaming, media and influencer marketing platform company, today announced that is has extended convertible debentures that were due to expire in October and November 2022 with an aggregate principal amount of US$1,250,000. The original convertible debentures had an annual interest rate of 10% per annum and a conversion price of US$8.90 per share.

In place of the expiring convertible debentures, the Company has issued a new convertible debenture with an aggregate principal amount of US$1,250,000 which expires on August 31, 2025, carries an annual interest rate of 7% per annum and is convertible into common shares of the Company at a conversion price of US$1.10 per share.

Each of the expiring convertible debentures and the replacement convertible debenture is beneficially held by a director of the Company. The participation of a director in the amendment of the convertible debentures constitutes a “related party transaction” as such term is defined by Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101”). The Company is relying on an exemption from the formal valuation requirements and the minority shareholder approval requirements under MI 61-101 as the fair market value of the amendment of the convertible debentures does not exceed 25% of the market capitalization of the Company.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME) (TSXV:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Cautionary Statement on Forward-Looking Information

This news release contains forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Engine to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. In respect of the forward-looking information contained herein, Engine has provided such statements and information in reliance on certain assumptions that management believed to be reasonable at the time. Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements stated herein to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Actual results could differ materially from those currently anticipated due to a number of factors and risks. Accordingly, readers should not place undue reliance on forward-looking information contained in this news release.

The forward-looking statements contained in this news release are made as of the date of this release and, accordingly, are subject to change after such date. Engine does not assume any obligation to update or revise any forward-looking statements, whether written or oral, that may be made from time to time by us or on our behalf, except as required by applicable law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Investor Relations Contact:

Shannon Devine MZ North America Main: 203-741-8811 GAME@mzgroup.us

NEWTOWN, Pa., Sept. 22, 2022 (GLOBE NEWSWIRE) — Onconova Therapeutics, Inc. (NASDAQ: ONTX), (“Onconova”), a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer, today announced that the Company will be participating in-person in the Ladenburg Thalmann 2022 Healthcare Conference, which is taking place at the Sofitel Hotel in New York, NY.

Steven Fruchtman, M.D., President & CEO of Onconova, will present a corporate overview to include an update on the company’s portfolio, followed by a 10-minute analyst-led fireside chat, on September 29th, 2022, at 12:00 p.m. ET. The presentation can be viewed here or on the “Corporate Events and Presentations” section of the Onconova website and will be archived for 90 days. Dr. Fruchtman and other members of the Onconova management team will also be available for in-person one-on-one meetings during the conference on September 29th, 2022. Those interested in requesting a meeting should contact their Ladenburg Thalmann representative.

About Onconova Therapeutics, Inc.

Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company has proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation.

Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in two separate and complementary Phase 1 dose-escalation and expansion studies. These trials are currently underway in the United States and China.

Onconova’s product candidate rigosertib is being studied in an investigator-sponsored study program, including in a dose-escalation and expansion Phase 1/2a investigator-sponsored study with oral rigosertib in combination with nivolumab for patients with KRAS+ non-small cell lung cancer.

Approximately 40% of Long COVID Patients Experience Multi-Site Pain Similar to Overlapping Chronic Pain Syndromes Fibromyalgia and ME/CFS

Approximately 50% of Long COVID Patients with Multi-Site Pain and Sleep Disturbance Use Opiates

CHATHAM, N.J., Sept. 22, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a clinical-stage biopharmaceutical company, today announced data from a retrospective observational database study in patients diagnosed with Long COVID at the International Association for the Study of Pain (IASP) 2022 World Congress on Pain, being held September 20-23, 2022, in Toronto, Canada. The study was motivated to identify the frequency of symptoms of multi-site pain, fatigue and insomnia in Long COVID patients because these are the hallmarks of Overlapping Chronic Pain Syndromes like fibromyalgia and myalgic encephalomyelitis/chronic fatigue syndrome (ME/CFS). A copy of the poster is available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com.

The poster presentation titled, “Retrospective Observational Database Study of Patients with Long COVID with Multi-site Pain, Fatigue, and Insomnia: A Real-World Analysis of Symptomatology and Opioid Use,” include data from the study showing that:

Approximately 40% of patients with symptoms of Long COVID had fibromyalgia-like multi-site pain.

The rate of opioid use in Long COVID patients with multi-site pain was 34%, compared to 19% of Long COVID patients without multi-site pain.

In patients with multi-site pain, opioid use increased to approximately 50% of patients when sleep disturbance was also present.

“The recently released U.S. HHS National Research Action Plan on Long COVID1 repeatedly addresses the overlap of Long COVID with ME/CFS, which, like fibromyalgia is one of the overlapping chronic pain syndromes with central sensitization,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “Previously, central sensitization had been observed in approximately two-thirds of Long COVID patients2. The data from the new retrospective study revealed that U.S. Long COVID patients are turning to opioids for symptomatic relief, revealing the urgency to provide effective non-opioid, non-addictive analgesics that address multi-site pain. Currently, there is no therapy approved by the U.S. Food and Drug Administration for the treatment of multi-site pain associated with Long COVID.”

In August 2022, the Company announced that the first participant was enrolled in the Phase 2 PREVAIL study of TNX-102 SL as a potential treatment for patients with Long COVID syndrome (Long COVID) whose symptoms overlap with fibromyalgia. Long COVID is known officially as Post-Acute Sequelae of COVID-19 (PASC).

Dr. Lederman added, “TNX-102 SL is a centrally-acting non-opioid analgesic with no recognized abuse potential that has shown to decrease daily pain in a Phase 3 study of fibromyalgia. The finding that approximately 40% of Long COVID patients have fibromyalgia-like multi-site pain symptoms in the retrospective observational database study suggests that we should be able to recruit a robust cohort of participants to test the effects of TNX-102 SL in treating multi-site pain in Long COVID in our ongoing Phase 2 study.”

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the first half of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the fourth quarter of 2022. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform. A Phase 1 study of the COVID-19 vaccine is expected to be initiated in the second half of 2023.

*All ofTonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Allegiant owns 100% of 10 highly-prospective gold projects in the United States, seven of which are located in the mining-friendly jurisdiction of Nevada. Three of Allegiant’s projects are farmed-out, providing for cost reductions and cash-flow. Allegiant’s flagship, district-scale Eastside project hosts a large and expanding gold resource and is located in an area of excellent infrastructure. Preliminary metallurgical testing indicates that both oxide and sulphide gold mineralization at Eastside is amenable to heap leaching.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Reverse Circulation (RC) drilling program. Allegiant completed a 32-hole RC drill program focusing on two areas outside the Original Pit Zone, including the East Pediment and Western Anomaly. Twenty-one holes were drilled on the East Pediment at an average depth of 203 meters and 11 holes were drilled on the Western Anomaly at an average depth of 223 meters. The company will conduct a follow-up RC drill program consisting of approximately 20 holes for a total of 5,000 additional meters of drilling. The rig is expected to arrive on site around October 20.

East Pediment discovery. Drilling on the East Pediment encountered mineralized rhyolite with assays returning values above 0.1 gram of gold per tonne over 51.5 meters of the 242-meter length of Hole ES-258. Intercepts include 86.4 to 93.9 meters averaging 1.3 grams of gold per tonne, including 86.4 to 87.9 meters averaging 4.4 grams of gold per tonne, along with 197 to 229 meters averaging 0.28 grams of gold per tonne. Allegiant intends to drill a grid pattern of offset holes in all directions around Hole ES-258 in late October 2022. The best intercepts associated with the West Anomaly were 34.8 to 45.4 meters averaging 0.93 grams of gold per tonne in Hole ES-268 and 76.7 to 83.8 meters averaging 1.4 grams of gold in Hole ES-264.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 103 facilities totaling approximately 83,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Asset Sale. The GEO Group has sold its minority equity interest in the government-owned Ravenhall Correctional Centre in Australia for approximately $84.4 million in gross proceeds, or about $75 million after-tax. GEO, as part of a consortium, originally began developing the Ravenhall facility in late 2014, with the facility opened in late 2017.

Use of Proceeds. GEO will use the proceeds, along with available cash on hand, to repay all of the remaining $146.9 million outstanding principal of its Term Loan B and its Tranche 3 Term Loan, both due March 23, 2024. Along with the repayment of the 5.125% senior notes due 2023, GEI has now reduced outstanding debt maturing prior to 2026 to approximately $23 million, a significant accomplishment, in our view.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Homeowners With Low Rates May Keep Inventories Low and Prices Stable

For many, the largest single asset they own is their home. While many investors are concerned about what rising interest rates may mean for investments in the stock market, homeowners are keenly aware that rates can directly impact home prices as most borrow to buy. The amount they can borrow is directly related to their cash flow, so the purchase price they can afford rises and falls with mortgage rates. This impacts demand and offer prices. But what does it do for the supply side of the pricing mechanism?

Rate Increases and Homes on the Market

Mortgage rates over the past year have risen from the low 3% range to the low 6% range for traditional 30-year loans. Typically the period in the rate cycle when mortgages begin to rise corresponds to a Fed tightening cycle, as it has in 2022. While rates were lower, buyers were able to afford “more house” and allowed sellers to push up asking prices – or in some cases, buyers would have had a bidding war driving up a home’s price.

As rates increase and it then costs borrowers more each month for the same price, buyers lessen. Home prices initially don’t decline as quickly as sellers would like as home sellers are stickier on the way down than they are on the way up. As with any investment, until you book your profit/loss, it’s just paper gains/losses. And homeowners don’t like to think of themselves as having “lost” thousands because their house once would have fetched more. So home buyers sit and wait, which in the past has caused inventories to increase. Eventually, there is capitulation among homeowners, and many houses hit the market with lower prices attached to them.

This has not happened yet during this rate cycle, and there is an underlying reason that may prevent it from happening. Existing homes are not entering the market as expected.

Homes for Sale are Scarce

The Wall Street Journal published an investigative piece on the real estate market and how Homeowners with low mortgage rates are stubbornly refusing to sell their homes because it would mean they’d have to borrow at much higher rates for wherever they may move.

The Journal reported that housing inventories had risen somewhat from record lows earlier in 2022. But this is primarily because they aren’t selling as quickly. The number of newly listed homes from mid-August to mid-September fell 19% from the same weeks last year. This suggests that those that may have sold to move for any reason are staying put.

The explanation for this unexpected phenomenon is that most that have purchased or refinanced their homes in the past few years have historically low mortgage rates. Imagine having 2.75% locked in for 30 years and knowing that if you purchase the home in the next town with the extra bedroom, your rate will be 6.25%. Potential sellers are opting to make do.

Homes will always enter the market regardless of dynamics. People die, change jobs, get divorced, the kids move out, etc. But, if those who have the option not to move decide to stay in larger percentages than in the past, it could keep the inventory of homes for sale below normal levels. The low supply could keep home prices elevated.

Another option someone who would like to move has is to rent. Rents have been quite high; this would serve to reduce the upward pressure on tenants. It would also keep homes from entering the market, allowing them to retain values better than might be expected with higher mortgage rates.

The scarcity of homes on the market is one of the primary reasons home prices have retained their high levels, despite seven straight months of declining sales in a period when interest rates have roughly doubled since December.

Handcuffed by Low Rates

There is a term used on Wall Street for employees that feel they can’t leave their company because they have vesting interests worth too much. For example, my friend Katherine was granted stock options from her company, the ability to exercise the options vested over a few years. At any point, if she left to take another position, or as she told me she wanted to do, raise children, she would have been leaving a huge sum of future stock or cash behind. Homeowners with mortgages near 3% when rates are near 6% have found their situation similarly handcuffs them and drives greed-based behavior.

Today Millions of Americans are locked in historically low borrowing rates. As of July 31, nearly nine of every ten first-lien mortgages had an interest rate below 5%, and more than two-thirds had a rate below 4%, according to mortgage-data firm Black Knight Inc. About 83% of those mortgages are 30-year fixed rates.

Can it Last?

Homeowners looking for more space are now more likely to add on than they had been before. For those looking to scale down, they may find that it isn’t worth it. In an analysis of four major metro areas—Atlanta, Chicago, Los Angeles, and Washington—Redfin found that homeowners with mortgage rates below 3.5% were less likely to list their homes for sale during August compared with homeowners with higher rates.

It is difficult to predict any market, and there is very little history to look back on when rates have been increased this quickly. Sam Khater, the chief economist for Freddie Mac, told the Wall Street Journal an analysis he did in 2016 of past periods of rising rates showed a decline in sales in which a buyers’ prior mortgage rate was more than 2% below their new mortgage rates. But there was no change if the difference between the rates was less than two percentage points. We are likely to retain more than a 2% margin for some time based on how low homeowners’ mortgages now are. Perhaps until many of the loans are paid off.

Gary Gensler Backs off on Payment-For-Order-Flow, But Promises Something More Comprehensive

The Securities and Exchange Commission (SEC) chairman has softened his harsh talk against the brokerage practice of payment-for-order-flow (PFOF). While securities brokers and investors in the industry breathed a sigh of relief with the news that the practice won’t be banned, firms like Robinhood (HOOD), Etrade (ETFC), and Charles Schwab (SCHW) may have something else to worry about.

About PFOF

There are harsh critics of the practice of PFOF, and there are strong advocates. Proponents of the model say it provides investors more liquidity, while those that oppose the practice question if retail traders are getting the best price.

In a nutshell, what this compensation system does is when investors place trades for stocks, ETFs, and options, the broker uses market makers to execute the order. To compete for price and execution, market makers in the securities offer rebates back to retail brokers. The rebates add to the broker’s profit, which is in part what allows for “free trades.” Additionally, the net cost per share to the investor is often still below most other methods readily available to them.

PFOF provides a significant revenue stream for retail brokers that offer zero-commission trading. Stocks of these brokerage firms have been under downward pressure with the uncertainty of whether the practice that is banned in other countries would be banned in the U.S. The news that it won’t be banned is seen as positive by those in the online broker industry.

New Direction for PFOF

After harping on the idea of banning PFOF, SEC officials (as reported by Bloomberg) have indicated that a ban is no longer being considered. That has been followed by their promise that other changes to the execution mechanism are on the way.

While the final SEC plans for payment-for-order-flow are not known, it is expected that they will allow these brokers to conduct business, and it is not expected to be more profitable for the brokers – most expect it to make it more difficult to maintain current earnings. The Commission is, if nothing else, expected to propose changes that could affect the complicated system of the rebates designed to increase market makers’ trading volume. Additionally, the regulator is weighing a plan to force brokers to disclose more about how much trading with them costs compared with benchmarks, a metric known as price improvement. The metric would allow customers to be able to compare one firm to another.

The SEC may also better clarify requirements for brokerages on what is “best execution” of stock transactions. The scope of the overhaul by the SEC remains to be seen.

The SEC is expected to introduce its plan in the coming months, according to Bloomberg. The plan is likely to make the system more transparent and more competitive and to include regulations lowering access fees that exchanges charge the brokers to execute trades.

Co-Branded Burger and Wings Pairing to Expand Footprint in California’s Capital City

LOS ANGELES, Sept. 21, 2022 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Fatburger, Buffalo’s Express and 15 other restaurant concepts, announces a new development deal to open six new franchised locations in the Sacramento area. In partnership with franchisee Raj Pooni, the co-branded Fatburger and Buffalo’s Express locations will open over the next six years with the first location set to open by the end of 2023.

“Fatburger is synonymous with California, so it is only fitting for us to expand further around the capital city, Sacramento,” said Taylor Wiederhorn, Chief Development Officer of FAT Brands. “We are also pleased to have an existing franchise partner, Raj Pooni, who operates a Round Table Pizza location in the area, to open these new units. This speaks to our synergistic growth model of having our franchisees diversify their restaurant portfolios with additional FAT Brands concepts.”

Ever since the first Fatburger opened in Los Angeles 70 years ago, the chain has been known for its delicious, grilled-to-perfection and cooked to order burgers. Founder Lovie Yancey believed that a big burger with everything on it is a meal in itself; at Fatburger “everything” is not just the usual roster of toppings. Burgers can be customized with everything from bacon and eggs, to chili and onion rings. In addition to its famous burgers, the Fatburger menu also includes Fat and Skinny Fries, sweet potato fries, scratch-made onion rings, Impossible™ Burgers, turkeyburgers, hand-breaded crispy chicken sandwiches, and hand-scooped milkshakes made from 100% real ice cream.

From the Buffalo’s Express menu, patrons can choose bone-in or boneless wings accompanied by a range of original sauces. All of Buffalo’s Express’ wings are accompanied by celery, carrots, and blue cheese, ranch or honey mustard dressing.

For more information or to find a Fatburger near you, please visit www.fatburger.com. For more information or to find a Buffalo’s Express near you, please visit www.buffalos.com.

###

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Fatburger

An all-American, Hollywood favorite, Fatburger is a fast-casual restaurant serving big, juicy, tasty burgers, crafted specifically to each customer’s liking. With a legacy spanning 70 years, Fatburger’s extraordinary quality and taste inspire fierce loyalty amongst its fan base, which includes a number of A-list celebrities and athletes. Featuring a contemporary design and ambience, Fatburger offers an unparalleled dining experience, demonstrating the same dedication to serving gourmet, homemade, custom-built burgers as it has since 1952 – The Last Great Hamburger Stand™.

About Buffalo’s Express

Founded in 1985 in Roswell, Georgia, Buffalo’s Express is a fast casual chain known for its world-famous chicken wings and proprietary wing sauces. Co-branded with over 100 Fatburger restaurants to date, Buffalo’s Express’ significant growth can be attributed to its high-quality menu offerings and unparalleled dining experience. Featuring a contemporary design and ambience, whether guests are dining-in or having take-out/delivery, Buffalo’s Express offers friends and families the flexibility to enjoy their world-famous chicken wings however they prefer. Buffalo’s Express – Where Everyone is Family™.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the timing and performance of new store openings. Forward-looking statements reflect expectations of FAT Brands Inc. (“we”, “our” or the “Company”) concerning the future and are subject to significant business, economic and competitive risks, uncertainties and contingencies, including but not limited to uncertainties surrounding the severity, duration and effects of the COVID-19 pandemic. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.