ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth Quarter Results. Revenue for the quarter totaled $57.8 million, nearing the top of management’s guidance and in-line with our estimate of $58 million. Net income totaled $3.0 million, or $0.06 per diluted share, an improvement from a loss of $2.9 million or $0.06 per share, last year. We estimated a net loss of $0.2 million or breakeven per share. Adjusted EBITDA was $6.5 million, the midpoint of management’s guidance and above our estimate of $6 million.

More Cash in Hand. ISG generated cash from operations of $6.6 million during the quarter, and with the sale of the automation unit last quarter, had total cash on hand of $23.1 million at the end of the quarter, up 138% from the prior quarter. Debt declined to 25% y-o-y to $59.2 million as of December 31, 2024. Management maintained a goal of 2.0-2.5x debt to EBITDA ratio.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Capital Infusion. Last night, after the market closed, Comtech Telecommunications announced a new $40 million capital infusion from the current holders of Comtech’s convertible preferred and subordinated debt, or White Hat Capital and Magnetar Financial. The new capital infusion is made on the same terms and conditions as the prior subordinated debt investment.

Uses. Of the $40 million infusion, $27.3 million is being used to prepay the senior secured term loan and $3.2 million to reduce the revolving credit facility, with a waiver of the prepayment penalties that would have been owed in accordance with the terms of the credit agreement.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mr. Long’s Proven Track Record in Driving E-Commerce Growth and Innovation Includes Leadership Roles at Walmart, Ashley Furniture, and Amazon

Mr. Long will Collaborate with the Existing E-commerce Management Team and Founders to Expand SKYX ‘s Sales and Market Penetration of Its Disruptive Advance and Smart Home Plug & Play Technologies in the U.S. and Canadian Markets

MIAMI, March 03, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 97 issued and pending patents globally and a portfolio of over 60 lighting and home décor websites, announces today that Huey Long, former Director of Amazon E-Commerce, Senior Vice President of Walmart, and Executive Vice President at Ashley Furniture, has joined SKYX to lead its e-commerce platform.

Mr. Long will work together with the existing e-commerce management team and founders to drive innovation and expand sales and market penetration of SKYX’s advanced and smart home plug & play technologies across the U.S. and Canadian markets.

Long is renowned for his strategic vision and operational excellence across advanced business ecosystems. With over 28 years of experience in e-commerce, omnichannel retail, and global sourcing, he brings a wealth of expertise and leadership to SKYX. His career includes pivotal roles at industry-leading companies, including as Director at Amazon.com, where he spearheaded the development of Amazon Basics, the company’s first private brand initiative. Additionally, he has served as Senior Vice President at Walmart Stores Inc., General Merchandise Manager at Sam’s Club, and Executive Vice President at Ashley Furniture.

Commenting on his appointment, Huey Long said, “I am honored to join SKYX and work with its e-commerce management team and founders at such an exciting time. The company’s commitment to innovation with its game-changing plug & play technologies aligns perfectly with my passion for driving value through innovation, strategic transformation, and operational excellence. I look forward to driving growth and further expanding the market penetration of SKYX’s technologies in the U.S. and Canadian markets. SKYX’s disruptive and smart platform technologies present a unique opportunity for recurring revenues.”

Rani Kohen, Founder/Inventor and Executive Chairman, of SKYX Platforms, said, “Huey’s extensive experience in e-commerce and omnichannel retail makes him uniquely positioned to drive the next phase of growth of our advanced and smart home plug & play platform technologies. We are excited to have Huey on board and look forward to his leadership as we continue to grow our market penetration.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a global leader in providing artificial intelligence (“AI”) and augmented reality (“AR”) Software-as-a-Service (“SaaS”) solutions to beauty and fashion industries, today announced its unaudited financial results for the three months and the full year ended December 31, 2024.

Highlights for the Three Months Ended December 31, 2024

Total revenuewas $15.9 million for the three months ended December 31, 2024, compared to $14.1 million in the same period of 2023, an increase of 12.4%. The increase was primarily due to growth momentum in the revenue of AI- and AR- cloud solutions and mobile app subscriptions.

Gross profitwas $11.8 million for the three months ended December 31, 2024, compared with $11.5 million in the same period of 2023, an increase of 2.5%.

Net income was $1.1 million for the three months ended December 31, 2024, compared to a net income of $1.4 million during the same period of 2023, a decrease of 21.8%.

Adjusted net income (non-IFRS)1was $2.3 million for the three months ended December 31, 2024, compared to adjusted net income (non-IFRS) of $2.1 million in the same period of 2023, an increase of 8.2%.

Operating cash flowwas $3.3 million in the fourth quarter of 2024, compared to $3.1 million in the same period of 2023, an increase of 3.4%.

The Company’s YouCam mobile beauty app and web active subscribers grew by 14.3% year-over-year, reaching a record high of over 1 million active subscribers as of end of 2024.

As of December 31, 2024, the Company’s cumulative customer base included 732 brand clients, with over 822,000 digital stock keeping units (“SKUs”) for makeup, haircare, skincare, eyewear, watches and jewelry products, compared to 708 brand clients and over 806,000 digital SKUs as of September 30, 2024. The number of Key Customers2of the Company remained stable at 151, as of both December 31, 2024, compared and September 30, 2024 due to the stability of our enterprise business.

Highlights for the Year Ended December 31, 2024

Total revenuewas $60.2 million for the year ended December 31, 2024, compared to $53.5 million in the same period of 2023, an increase of 12.5%.

Gross profitwas $46.9 million for the year ended December 31, 2024, compared with $43.1 million in the same period of 2023, an increase of 8.9%.

Net incomewas $5.0 million for the year ended December 31, 2024, compared to a net income of $5.4 million during the same period of 2023, a decrease of 7.3%.

Adjusted net income (non-IFRS)was $8.3 million for the year ended December 31, 2024, compared to adjusted net income (non-IFRS) of $7.0 million in the same period of 2023, an increase of 18.6%.

Operating cash flowwas $13.0 million for the year ended December 31, 2024, compared to $13.6 million in the same period of 2023, a decrease of 4.2%.

Ms. Alice H. Chang, the Founder, Chairwoman, and Chief Executive Officer of Perfect commented, “We are pleased to report solid double-digit growth, positive net income, healthy cash flow, and a strong balance sheet for 2024, fully meeting our previous guidance. This remarkable performance is a testament to our team’s resilience and the visionary leadership of our management. By capitalizing on market opportunities and expanding our total addressable market, we are not only attracting new clients but also laying the foundation for sustained long-term growth. Our commitment to innovation ensures that we will continue to deliver cutting-edge solutions that meet evolving market demands. With a comprehensive strategy in place, we are excited about the future and confident in our ability to create ongoing value for all our stakeholders.”

Financial Results for the Three Months Ended December 31, 2024 and for the Full Year 2024

Revenue

Total revenue was $15.9 million for the three months ended December 31, 2024, compared to $14.1 million in the same period of 2023, an increase of 12.4%. Full-year revenue was $60.2 million in 2024, compared to $53.5 million in 2023, an increase of 12.5%.

AI- and AR- cloud solutions and subscription revenue was $15.1 million for the three months ended December 31, 2024, compared to $12.0 million in the same period of 2023, an increase of 25.4%. Full-year AI- and AR- cloud solutions and subscription revenue was $53.8 million in 2024, compared with $44.8 million in 2023, an increase of 20.2%. The double digit growth was driven by the robust momentum in the growth of YouCam mobile beauty app subscription, stable demand for the Company’s online virtual product try-on solutions from brand customers, and the growing popularity among consumers of Generative AI technologies and AI editing features for photos and videos. The Company’s YouCam mobile beauty app and web active subscribers grew by 14.3% year-over-year, once again reaching a record high of over 1 million active subscribers as of the end of the fourth quarter of 2024. This increase reflected the sustained demand in the Company’s YouCam mobile beauty app services from subscribers and users.

Licensing revenue was $0.5 million for the three months ended December 31, 2024, compared to $1.8 million in the same period of 2023, a decrease of 72.2%. Full year licensing revenue was $5.2 million for 2024, compared with $7.5 million for 2023, a decrease of 30.8%. The Company anticipates that this legacy non-recurring revenue will become increasingly immaterial as it continues to prioritize enhancing its market leadership in offering AI- and AR-based SaaS subscription solutions for brands and customers.

Gross Profit

Gross profit was $11.8 million for the three months ended December 31, 2024, compared with $11.5 million in the same period of 2023, an increase of 2.5%. Despite the increase in gross profit, our gross margin decreased to 74.1% for the three months ended December 31, 2024, from 81.3% in the same period of 2023. Full-year gross profit was $46.9 million in 2024, compared with $43.1 million in 2023, an increase of 8.9%. Full-year 2024 gross margin slightly decreased to 78.0% in 2024 from 80.6% in 2023. The decrease in gross margin was primarily due to the increase in third-party payment processing fees paid to digital distribution partners, such as Google and Apple, due to the steady growth in our YouCam mobile app subscription revenue.

Total Operating Expenses

Total operating expenses were $12.2 million for the three months ended December 31, 2024, compared with $12.7 million in the same period of 2023, a decrease of 3.6%. The decrease was primarily due to declines in research and development (“R&D”) expenses and general and administrative (“G&A”) expenses in the fourth quarter of 2024. Full-year total operating expenses were $50.1 million in 2024, compared with $48.8 million in 2023, an increase of 2.7%. The increase was primarily due to increases in sales and marketing expenses and R&D expenses, which were mostly offset by a decrease in general and administrative expenses.

Sales and marketing expenseswere $6.9 million for the three months ended December 31, 2024, compared to $6.7 million during the same period of 2023, an increase of 3.6%. Full-year sales and marketing expenses were $28.2 million for 2024, compared to $25.7 million in 2023, an increase of 9.7%. This increase was primarily due to an increase in marketing events and advertising expenses related to our mobile apps and cloud computing

Research and development expenseswere $2.8 million for the three months ended December 31, 2024, compared to $3.0 million during the same period of 2023, a decrease of 8.3%. The decrease primarily resulted from streamlining of certain R&D processes and optimizing expenses. Full-year R&D expenses were $12.0 million for 2024, compared to $11.5 million in 2023, an increase of 4.7%. The increases resulted from increases in R&D headcount and related personnel costs.

General and administrative expenseswere $1.8 million for the three months ended December 31, 2024, compared to $3.0 million during the same period of 2023, a significant decrease of 41.0%. Full-year G&A expenses were $8.5 million for 2024, compared to $11.6 million in 2023, a decrease of 26.6%. The significant decrease was primarily due to reduced corporate insurance premium and external professional service fees.

Net Income

Net income was $1.1 million for the three months ended December 31, 2024, compared to a $1.4 million during the same period of 2023. Full-year net income was $5.0 million for 2024, compared to $5.4 million for 2023. The positive net income was supported by our steady revenue growth and effective cost control.

Adjusted Net Income (Non-IFRS)

Adjusted net income was $2.3 million for the three months ended December 31, 2024, compared to $2.1 million in the same period of 2023, an increase of 8.2%. Full-year adjusted net income was $8.3 million for 2024, compared to $7.0 million for 2023.

Liquidity and Capital Resource

As of December 31, 2024, the Company’s cash and cash equivalents remained stable at $127.1 million (or $165.9 million when including money market funds of $2.7 million and 6-month time deposits of $36.0 million, which are classified as current financial assets at fair value through profit or loss and current financial assets at amortized cost under IFRS), compared to $127.2 million as of September 30, 2024 (or $163.2 million when including time deposits).

The Company had a positive operating cash flow of $3.3 million in the fourth quarter of 2024, compared to $3.1 million in the same period of 2023. The Company had a positive operating cash flow of $13.0 million in the full year of 2024, compared to $13.6 million in 2023. The Company continues to invest in growth while maintaining a healthy cash reserve to support business operations underscoring the Company’s operational health and sustainability.

Recent Developments

As previously announced by the Company, on December 23, 2024, Perfect entered into an agreement with Farfetch, a leading global marketplace for the luxury fashion industry, pursuant to which Perfect agreed to acquire 100% of the equity interests in Wannaby Inc. (“Wannaby”), which is a pioneer in augmented reality and computer vision technologies, specializing in virtual try-on solutions for the fashion industry.

On January 8, 2025, Perfect completed the acquisition Wannaby. Wannaby is now a wholly-owned subsidiary of Perfect.

Business Outlook for 2025

Based on the growth momentum in both YouCam mobile apps and web subscriptions and enterprise SaaS solution demands, the Company anticipates a year-over-year total revenue growth rate of 13% to 14.5% for 2025, compared to 2024.

Note that this forecast is based on the Company’s current assessment of the market and operational conditions, and that these factors are subject to change.

Conference Call Information

The Company’s management will hold an earnings conference call at 7:30 p.m. Eastern Time on February 26, 2025 (7:30 a.m. Taipei Time on February 27, 2025) to discuss the financial results. For participants who wish to join the call, please complete online registration using the link provided below in advance of the conference call. Upon registering, each participant will receive a participant dial-in number and a unique access PIN, which can be used to join the conference call.

A live and archived webcast of the conference call will also be available at the Company’s investor relations website at https://ir.perfectcorp.com.

About Perfect Corp.

Founded in 2015, Perfect Corp. is a beautiful AI Company and global leader in enterprise SaaS solutions. As an innovative powerhouse in using artificial intelligence (AI) to transform the beauty and fashion industries, Perfect empowers major beauty, skincare, fashion, jewelry, and watch brands and by providing consumers with omnichannel shopping experiences through augmented reality (AR) product try-ons and AI-powered skin diagnostics. With cutting-edge technologies such as Generative AI, real-time facial and hand 3D AR rendering and cloud solutions, Perfect enables personalized, enjoyable, and engaging shopping journey. In addition, Perfect also operates a family of YouCam consumer apps for photo, video and camera users, centered on unleashing creativity with AI-driven features for creation, beautification and enhancement. With the help of technologies, Perfect helps brands elevate customer engagement, increase conversion rates, and propel sales growth. Throughout this journey, Perfect maintains its unwavering commitment to environmental sustainability and fulfilling social responsibilities. For more information, visit https://ir.perfectcorp.com/.

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act, that are based on beliefs and assumptions and on information currently available to Perfect. In some cases, you can identify forward-looking statements by the following words: “may,” “will,” “could,” “would,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing,” “target,” “seek” or the negative or plural of these words, or other similar expressions that are predictions or indicate future events or prospects, although not all forward-looking statements contain these words. Any statements that refer to expectations, projections or other characterizations of future events or circumstances, including strategies or plans, are also forward-looking statements. These statements involve risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by these forward-looking statements. These statements are based on Perfect’s reasonable expectations and beliefs concerning future events and involve risks and uncertainties that may cause actual results to differ materially from current expectations. These factors are difficult to predict accurately and may be beyond Perfect’s control. Forward-looking statements in this communication or elsewhere speak only as of the date made. New uncertainties and risks arise from time to time, and it is impossible for Perfect to predict these events or how they may affect Perfect. In addition, risks and uncertainties are described in Perfect’s filings with the Securities and Exchange Commission. These filings may identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. Perfect cannot assure you that the forward-looking statements in this communication will prove to be accurate. There may be additional risks that Perfect presently does not know or that Perfect currently does not believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by Perfect, its directors, officers or employees or any other person that Perfect will achieve its objectives and plans in any specified time frame, or at all. Except as required by applicable law, Perfect does not have any duty to, and does not intend to, update or revise the forward-looking statements in this communication or elsewhere after the date of this communication. You should, therefore, not rely on these forward-looking statements as representing the views of Perfect as of any date subsequent to the date of this communication.

Use of Non-IFRS Financial Measures

This press release and accompanying tables contain certain non-IFRS financial measures, including adjusted net income, as supplemental metrics in reviewing and assessing Perfect’s operating performance and formulating its business plan. Perfect defined these non-IFRS financial measures as follows:

Adjusted net income (loss) is defined as net income (loss) excluding one-off transaction costs3 , non-cash equity-based compensation, and non-cash valuation (gain)/loss of financial liabilities. Starting from the first quarter of 2024, we no longer exclude foreign exchange gain (loss) from adjusted net income (loss). As we transitioned to using the U.S. dollar as the functional currency for certain subsidiaries in 2023, our foreign exchange gains (losses), which historically have predominantly been unrealized, have not been material since 2023. For a reconciliation of adjusted net income (loss) to net income (loss), see the reconciliation table included elsewhere in this press release.

Non-IFRS financial measures are not defined under IFRS and are not presented in accordance with IFRS. Non-IFRS financial measures have limitations as analytical tools, which possibly do not reflect all items of expense that affect our operations. Share-based compensation expenses have been and may continue to be incurred in our business and are not reflected in the presentation of the non-IFRS financial measures. In addition, the non-IFRS financial measures Perfect uses may differ from the non-IFRS measures used by other companies, including peer companies, and therefore their comparability may be limited. The presentation of these non-IFRS financial measures is not intended to be considered in isolation from or as a substitute for the financial information prepared and presented in accordance with IFRS. The items excluded from our adjusted net income are not driven by core results of operations and render comparison of IFRS financial measures with prior periods less meaningful. We believe adjusted net income provides useful information to investors and others in understanding and evaluating our results of operations, as well as providing a useful measure for period-to-period comparisons of our business performance. Moreover, such non-IFRS measures are used by our management internally to make operating decisions, including those related to operating expenses, evaluate performance, and perform strategic planning and annual budgeting.

SKYX Advanced and Smart Plug & Play Technologies to be utilized in Cavco’s High-End Premium Manufactured Homes at the World Largest Builders’ Show IBS

Since its Inception Cavco Homes is Estimated to Have Sold Nearly 1 Million Homes and Close to 20,000 Homes Annually During the Past Years

As SKYX Continues to Increase its U.S. and Canada Market Penetration, its Technologies will be Used in Cavco’s High-End Homes including the New Leading Premium Homes Skye View and Bungalow Models, in Show Village during the International Builders’ Show in Las Vegas February 25-27, 2025

MIAMI, Feb. 24, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 97 issued and pending patents globally and over 60 lighting and home décor websites, announces it will collaborate with Cavco Industries, Inc., a U.S. leading prefabricated home manufacturer to utilize SKYX’s advanced and smart plug & play technologies in Cavco’s premium prefabricated homes during the International Builders’ Show (IBS). SKYX’s technologies will be used in Cavco’s high-end homes, including their new leading premium homes Skye View and Bungalow models, in Show Village during the International Builders’ Show place in Las Vegas from February 25-27, 2025.

SKYX’s advance and smart plug & play platform technologies makes homes and buildings become advanced, safe, and smart instantly while significantly saving time and cost as well as adding substantial value to developers and homeowners.

Cavco is a leading U.S. manufacturer of prefabricated homes. As a publicly traded company, it ranks among the largest producers of manufactured and modular homes in the nation, renowned for its high-quality, premium designs. Cavco specializes in designing and producing factory-built housing products, which are distributed through an extensive network of independent and company-owned retailers. Since its inception, it is estimated that Cavco has sold nearly one million homes, with recent annual sales approaching 20,000 units.

Tim Gage, National Vice President of Cavco’s Park Models, and Specialty Homes said, “We are excited to utilize SKYX’s game-changing safe plug and play technology in our Cavco Park Model prefabricated homes at the IBS Pro Builder Show Village. We welcome people to visit our premium homes including our Skye View and Bungalow models to see how we utilize SKYX’s technologies. I strongly believe that the SKYX technology can become the standard for new construction, as it provides, safety, time saving, and smart capabilities, while advancing and adding significant value to our homes.”

Rani Kohen, Founder/Inventor and Executive Chairman, of SKYX Platforms, said, “We are truly excited to collaborate with a U.S. leading premium prefabricated home manufacturer such as Cavco during the world’s largest building show, IBS. This is another step toward our goal of making homes and buildings become advanced, safe, and smart as the new standard. We look forward to continuing to demonstrate our advanced smart platform technology’s ability to make homes and buildings become smarter and safer instantly, while significantly advancing buildings and saving time and costs for developers.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

The Three Projects Will Include an 80 Story High-Rise Building in the Miami Brickell District at 1040 South Miami Ave, Two Buildings in Clearwater Beach, and a Project in Jupiter Florida, Totaling Over 400 High-End Luxury Units

SKYX is Expected to Supply Forte Development with Over 12,000 Smart and Plug & Play Products Across Three Luxury Projects, Including Ceiling Outlet Receptacles, Lighting, Ceiling Fans, Recessed Lights, EXIT Signs, Emergency Lights, Downlights, and Indoor/Outdoor Wall Lights

SKYX’s Technologies Provide Opportunities for Recurring Revenues Through Upgrades, Interchangeability, Monitoring and Subscriptions and More

MIAMI, Feb. 20, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive smart platform technology company with more than 97 issued and pending patents globally and over 60 lighting and home décor websites, announces that it will start supplying its technologies to Forte Developments’ upcoming high-end luxury projects, including an 80-story building in Miami located at the Brickell district, two buildings in Clearwater Beach and a project in Jupiter, Florida.

Forte Developments is a leading high-end luxury condo and home development company. Forte’s developments include well-known luxury buildings in Palm Beach and Miami, Florida, as well as in The Hamptons, New York, among others.

During the course of the three projects, SKYX is expected to deliver over 12,000 of its products, representing a variety of its advanced and smart platform technology plug & play platform products. SKYX is expected to start supplying its products during the second half of 2025.

Marius Fortelni CEO and Founder of Forte Developments said: “We are excited to develop our ultra-high-end luxury upcoming projects utilizing SKYX’s game-changing advanced, smart, and safe plug and play technologies. I strongly believe that SKYX’s disruptive ceiling platform technologies will become the standard for new construction as they provide smart capabilities, safety and time savings, while adding significant value to our homes and buildings.” Link to Forte’s website here: https://fortedevelopmentus.com/

Rani Kohen, Founder/Inventor and Executive Chairman, of SKYX Platforms, said: “We are excited to work with a high-end condo developer such as Forte Developers. This is another step toward our goal of making homes and buildings become advanced, safe, and smart as the new standard. We look forward to continuing to demonstrate our advanced smart platform technology’s ability to make homes and buildings become smart and safe instantly, while significantly advancing buildings and saving time and cost to developers.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Key Points: – Broadcom and Taiwan Semiconductor Manufacturing Co. (TSMC) are reportedly considering independent deals that could split Intel. – Intel has lost billions in market value after falling behind in the AI-driven semiconductor boom. – Despite a 60% slump in 2024, Intel shares have climbed 29% this year, with a 12% rally on Tuesday.

Intel shares surged 12% on Tuesday following a report from The Wall Street Journal that Broadcom and Taiwan Semiconductor Manufacturing Co. (TSMC) are contemplating bids that could potentially split the struggling chip giant. This marked Intel’s best single-day performance since March 2020, fueling renewed investor interest in the company’s future.

According to sources cited by The Wall Street Journal, Broadcom is evaluating a deal to acquire Intel’s chip design and marketing unit, while TSMC is considering a stake or full control of Intel’s manufacturing facilities. These discussions are still in their early stages, with no official bids filed and negotiations remaining largely informal.

Intel, once a dominant force in the semiconductor industry, has faced significant challenges in recent years. As the artificial intelligence boom propelled competitors such as Nvidia and AMD to new heights, Intel struggled to keep pace. The company has shed billions in market value, unable to capitalize on the AI-driven demand that has reshaped the sector.

In August 2024, Intel suffered its worst stock market day in five decades, with shares plummeting to their lowest level since 2013 following disappointing quarterly results. The company’s struggles prompted major cost-cutting measures, including a 15% reduction in its workforce. Amid these difficulties, Intel’s board ousted CEO Pat Gelsinger in December, citing waning investor confidence in his ability to steer the company back to profitability.

The prospect of Broadcom and TSMC acquiring different segments of Intel signals a possible strategic shift for the embattled chipmaker. Broadcom, known for its aggressive acquisition strategy, could benefit from Intel’s chip design expertise and established market presence. Meanwhile, TSMC, the world’s largest contract chipmaker, would strengthen its global semiconductor manufacturing footprint by securing Intel’s production facilities.

Investors responded positively to the news, with Intel shares soaring 12% on Tuesday. The rally extended the stock’s year-to-date gains to 29%, offering some relief after a brutal 2024 that saw a 60% decline in share value. Meanwhile, Broadcom shares fell 2%, while TSMC experienced a modest dip of less than 1%.

The potential breakup of Intel comes amid broader geopolitical concerns surrounding semiconductor production. The U.S. government has intensified efforts to safeguard domestic chip manufacturing, with Vice President JD Vance recently affirming that AI chip production will be protected from foreign adversaries. This sentiment boosted Intel’s stock last week, as the company remains a key player in the U.S. semiconductor supply chain.

As Intel navigates its uncertain future, the reported interest from Broadcom and TSMC could present an opportunity for the company to restructure and regain competitiveness in the rapidly evolving semiconductor industry.

New Business Signings ACV (2) : Q4 $137M / FY $485M

Net ARR Activity Metric (2) (TTM): $92M

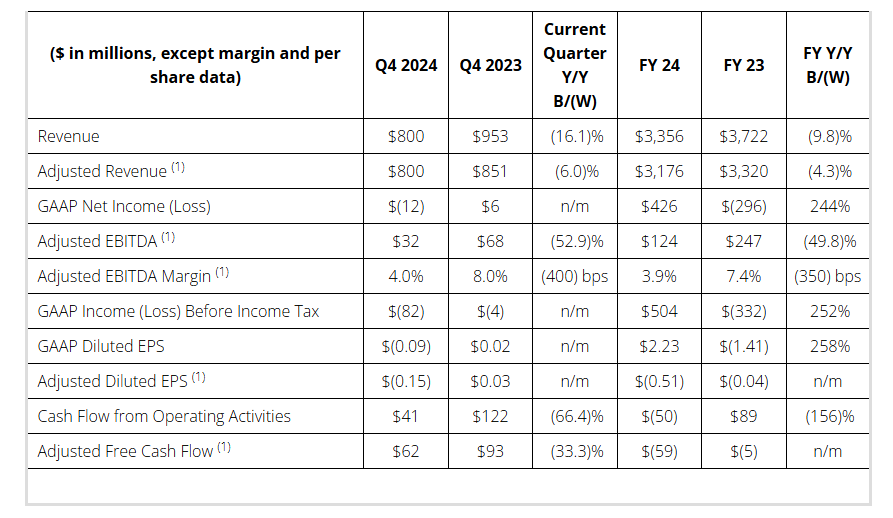

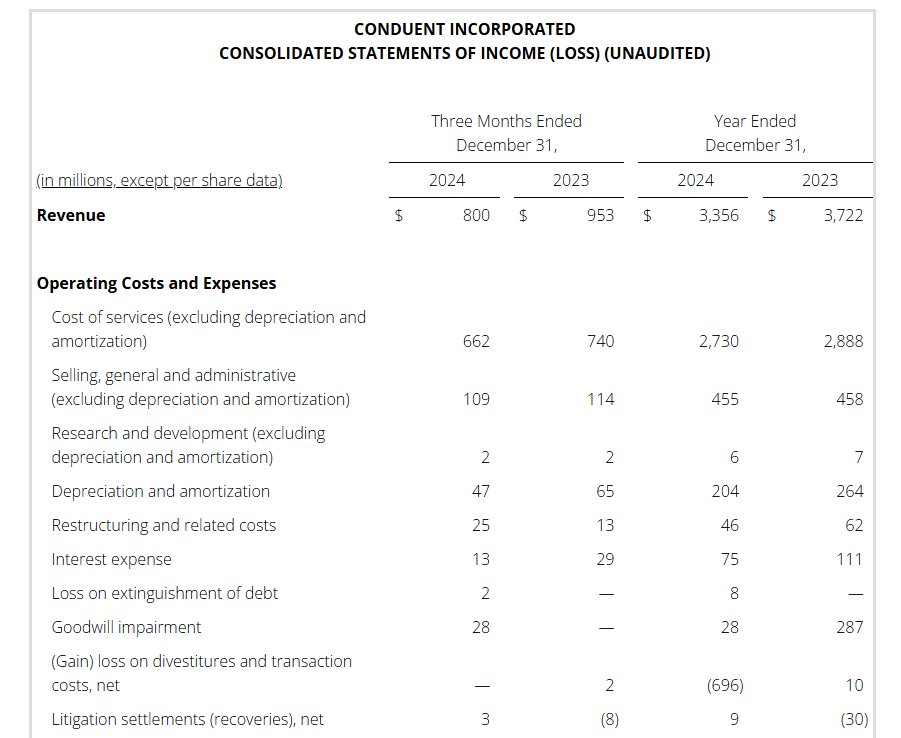

FLORHAM PARK, N.J., Feb. 12, 2025 — Conduent Incorporated (Nasdaq: CNDT), a global technology-led business process solutions and services company, today announced its fourth quarter and full year 2024 financial results.

Cliff Skelton, Conduent President and Chief Executive Officer stated, “2024 proved to be broadly in line with what we planned for. It was a year we said would be characterized by a continued shift to growth, with a focus on new leadership, a rationalized portfolio, improved industry recognition, and improved client retention. It was all of that and more, enhanced by divestitures with solid multiples and a 50% reduction in debt compared to year-end 2023.”

“From a numbers perspective, while timing drove a slightly weaker top line finish to the year, it was offset by an EBITDA margin on the high end of expectations. Quarterly Adjusted Revenue improved sequentially for the past three quarters and Adjusted EBITDA also increased over the past three quarters.”

“We remain bullish on achieving expectations in 2025. We continue to see opportunities for a further rationalized portfolio and remain focused on delivering outstanding service to our valued client base.”

Key Financial Q4 & Full Year 2024 Results

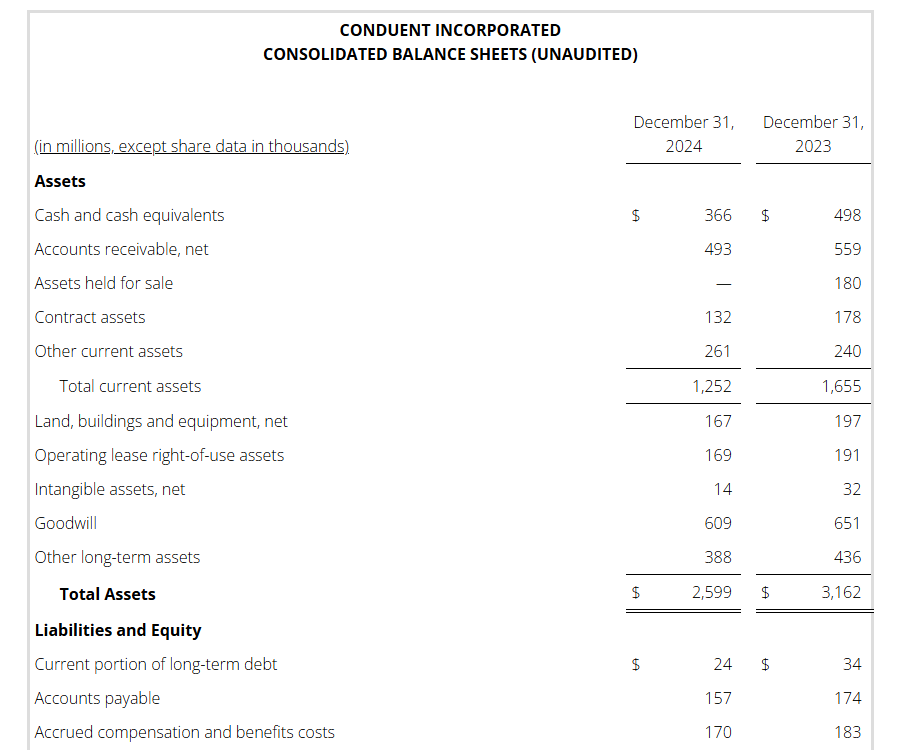

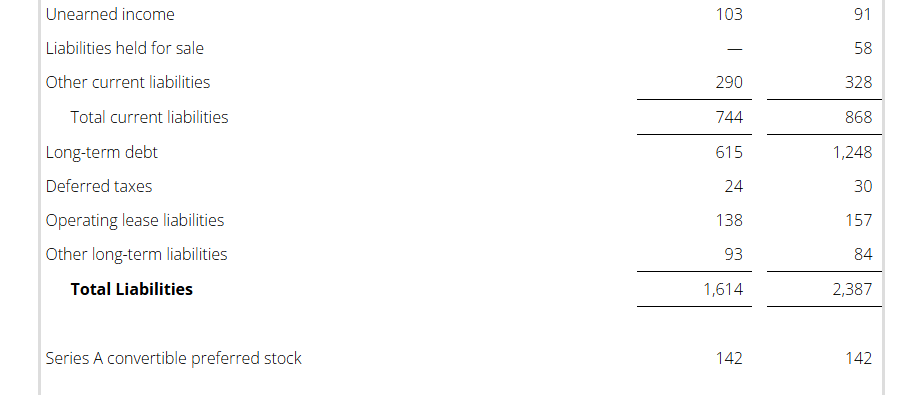

Performance Commentary During 2024, the Company completed three divestitures as part of its portfolio rationalization strategy. The transfer of the BenefitWallet portfolio was completed during the second quarter of 2024 for a total purchase price of $425 million. During the second quarter of 2024, the company also completed the sale of the Curbside Management and Public Safety businesses with a purchase price of $230 million, $50 million of which is deferred to the first half of 2025. During the third quarter of 2024, the company completed the sale of the Casualty Claims Solutions Business and received $224 million of cash consideration.

Also, during 2024, the Company used a portion of the proceeds from the divested businesses to voluntarily prepay all of the principal of the Term Loan B and $137 million of the Term Loan A.

Conduent’s liquidity position remains strong with long-dated debt maturities and a modest net leverage ratio.

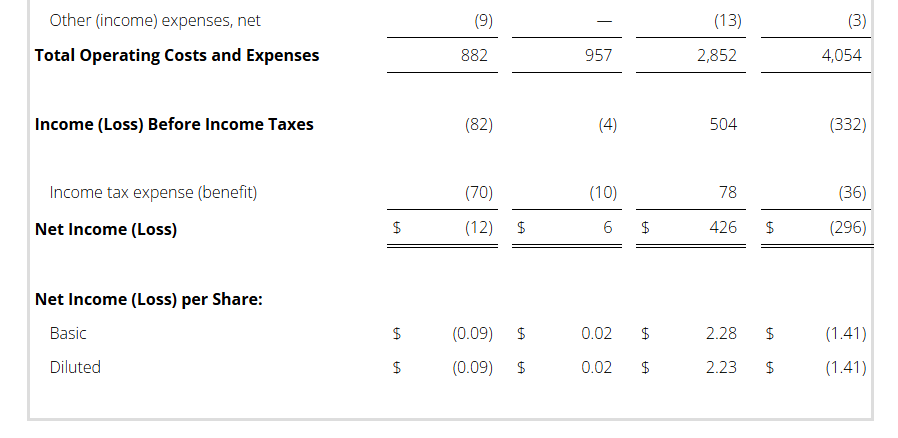

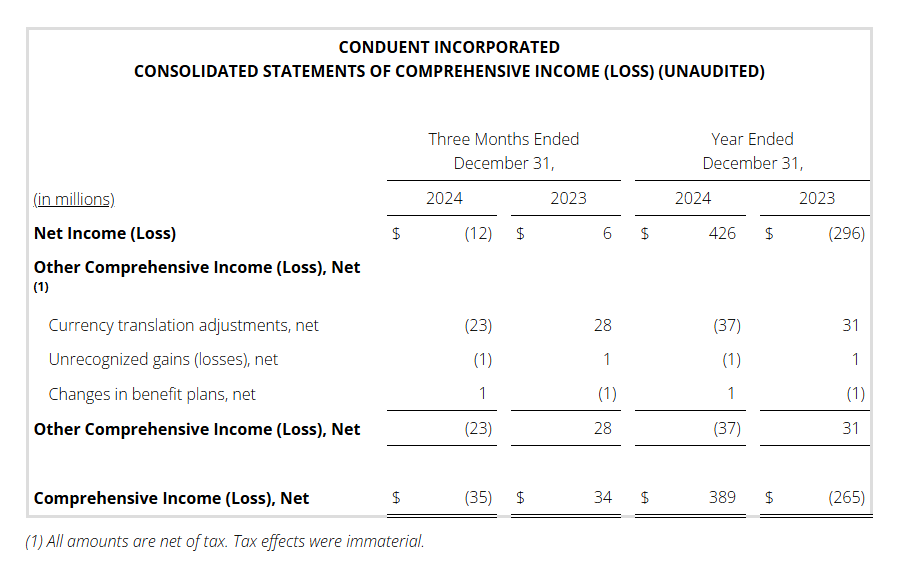

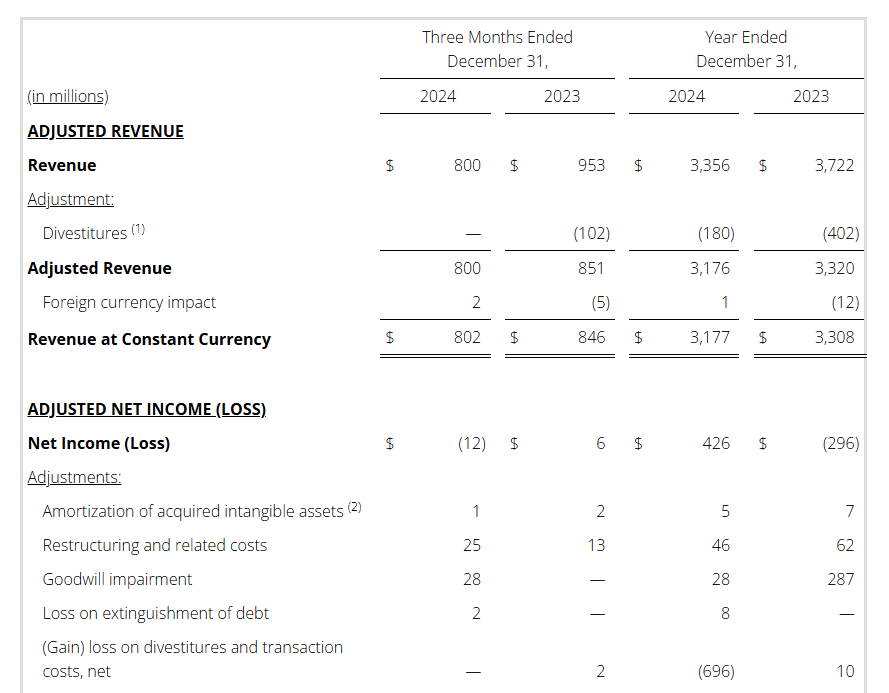

Full year 2024 pre-tax income (loss) was $504 million versus $(332) million in the prior year. This increase is primarily driven by the gain on the sale of the three divested businesses noted above, as well as a goodwill impairment in the prior year.

During 2024 the Company completed its previously approved $75 million share repurchase program and bought back a total of 52 million shares of common stock, including approximately 38 million shares purchased from Carl Icahn and affiliates.

Additional Q4 & Full Year 2024 Performance Highlights

Conduent achieved several milestones in technology-led solutions, operational excellence and culture, including:

Announced several implementations and advanced solutions in Transportation including expanded 3D fare gates, open payment digital wallet fare collection and all-electronic express lane tolling for clients in the US and Europe;

Implemented several digital payment solutions for several states that combat fraud and disburse payments to those in need;

Integrated AI-driven solutions by TALON and Jellyvision’s ALEX with Conduent’s Life@Work Connect Experience Platform to enhance employee benefits decisions;

Collaborated with Microsoft on an initiative across the Conduent portfolio to drive innovation using Microsoft Azure OpenAI Services;

Earned Leader Recognition from:

Information Services Group (ISG) as a U.S. and Europe “Leader” in its 2024 Contact Center – Customer Experience Services Provider Lens™ report; and

NelsonHall’s NEAT Report for Healthcare Payer Operational Transformation; CX Services Transformation – Cost Optimization Focus; and Multi-Process HR Transformation Services for Large Enterprises.

Earned Recognition for Industry Leadership and Culture:

“GovTech Top 100 Company” for the third consecutive year;

Newsweek Top 100 Most Loved Workplaces for third consecutive year;

“Best Place to Work for Disability Inclusion” (Disability Equality Index); and

Forbes’ list of America’s Best Employers for Diversity for the fourth consecutive year.

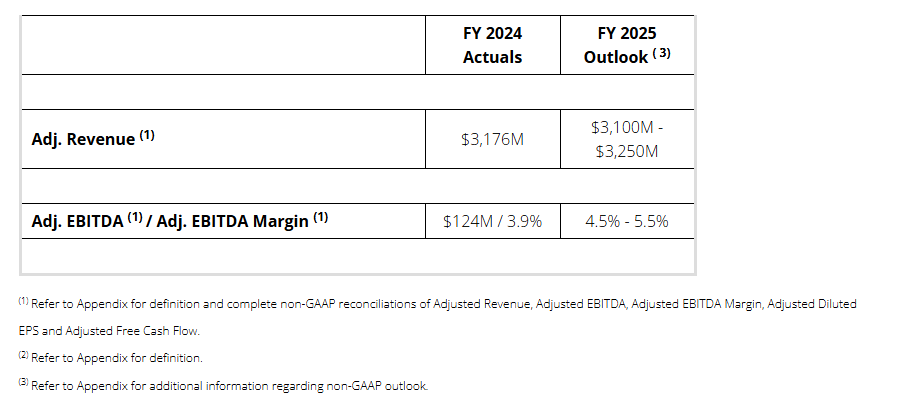

FY 2025 Outlook

Conference Call Management will present the results during a conference call and webcast on February 12, 2025 at 9:00 a.m. ET.

The call will be available by live audio webcast along with the news release and online presentation slides at https://investor.conduent.com/.

The conference call will also be available by calling 877-407-4019 toll-free. If requested, the conference ID for this call is 13750544.

The international dial-in is 1-201-689-8337. The international conference ID is also 13750544.

A recording of the conference call will be available by calling 1-877-660-6853 three hours after the conference call concludes. The replay ID is 13750544.

The telephone recording will be available until February 26, 2025.

About Conduent Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 56,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling approximately 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing over 13 million tolling transactions every day. Learn more at www.conduent.com.

Non-GAAP Financial Measures We have reported our financial results in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In addition, we have discussed our financial results using non-GAAP measures. We believe these non-GAAP measures allow investors to better understand the trends in our business and to better understand and compare our results. Accordingly, we believe it is necessary to adjust several reported amounts, determined in accordance with U.S. GAAP, to exclude the effects of certain items as well as their related tax effects. Management believes that these non-GAAP financial measures provide an additional means of analyzing the results of the current period against the corresponding prior period. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, our reported results prepared in accordance with U.S. GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a substitute for comparable U.S. GAAP measures and should be read only in conjunction with our Consolidated Financial Statements prepared in accordance with U.S. GAAP. Our management regularly uses our non-GAAP financial measures internally to understand, manage and evaluate our business and make operating decisions. Providing such non-GAAP financial measures to investors allows for a further level of transparency as to how management reviews and evaluates our business results and trends. These non-GAAP measures are among the primary factors management uses in planning for and forecasting future periods. Compensation of our executives is based in part on the performance of our business based on certain of these non-GAAP measures. Refer to the “Non-GAAP Financial Measures” section attached to this release for a discussion of these non-GAAP measures and their reconciliation to the reported U.S. GAAP measures.

Forward-Looking Statements

This press release, any exhibits or attachments to this release, and other public statements we make may contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. The words “anticipate,” “believe,” “estimate,” “expect,” “expectations,” “in front of us,” “plan,” “intend,” “will,” “aim,” “should,” “could,” “forecast,” “target,” “may,” “continue to,” “looking to continue,” “endeavor,” “if,” “growing,” “projected,” “potential,” “likely,” “see,” “ahead,” “further,” “going forward,” “on the horizon,” “as we progress,” “going to,” “path from here forward,” “think,” “path to deliver,” “from here,” and similar expressions (including the negative and plural forms of such words and phrases), as they relate to us, are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. All statements other than statements of historical fact included in this press release or any attachment to this press release are forward-looking statements, including, but not limited to, statements regarding our financial results, condition and outlook; changes in our operating results; general market and economic conditions; and our projected financial performance, including all statements made under the section captioned “FY 2025 Outlook” within this release. These statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions, many of which are outside of our control, that could cause actual results to differ materially from those expected or implied by such forward-looking statements contained in this press release, any exhibits to this press release and other public statements we make.

Important factors and uncertainties that could cause our actual results to differ materially from those in our forward-looking statements include, but are not limited to: government appropriations and termination rights contained in our government contracts, the competitiveness of the markets in which we operate and our ability to renew commercial and government contracts, including contracts awarded through competitive bidding processes; our ability to recover capital and other investments in connection with our contracts; our reliance on third-party providers; risk and impact of geopolitical events and increasing geopolitical tensions (such as the war in the Ukraine and conflict in the Middle East), macroeconomic conditions, natural disasters and other factors in a particular country or region on our workforce, customers and vendors; our ability to deliver on our contractual obligations properly and on time; changes in interest in outsourced business process services; claims of infringement of third-party intellectual property rights; our ability to estimate the scope of work or the costs of performance in our contracts; the loss of key senior management and our ability to attract and retain necessary technical personnel and qualified subcontractors; our failure to develop new service offerings and protect our intellectual property rights; our ability to modernize our information technology infrastructure and consolidate data centers; expectations relating to environmental, social and governance considerations; utilization of our stock repurchase program; risks related to our use of artificial intelligence; the failure to comply with laws relating to individually identifiable information and personal health information; the failure to comply with laws relating to processing certain financial transactions, including payment card transactions and debit or credit card transactions; breaches of our information systems or security systems or any service interruptions; our ability to comply with data security standards; developments in various contingent liabilities that are not reflected on our balance sheet, including those arising as a result of being involved in a variety of claims, lawsuits, investigations and proceedings; risks related to recently completed divestitures including the (i) transfer of the Company’s BenefitWallet’s health savings account, medical savings account and flexible spending account portfolio, (ii) the sale of the Company’s Curbside Management and Public Safety Solutions businesses and (iii) the sale of the Company’s Casualty Claims Solutions business, including but not limited to the Company’s ability to realize the benefits anticipated from such transactions, unexpected costs, liabilities or delays in connection with such transactions, and the significant transaction costs associated with such transactions; risk and impact of potential goodwill and other asset impairments; our significant indebtedness and the terms of such indebtedness; our failure to obtain or maintain a satisfactory credit rating and financial performance; our ability to obtain adequate pricing for our services and to improve our cost structure; our ability to collect our receivables, including those for unbilled services; a decline in revenues from, or a loss of, or a reduction in business from or failure of significant clients; fluctuations in our non-recurring revenue; increases in the cost of voice and data services or significant interruptions in such services; our ability to receive dividends or other payments from our subsidiaries; and other factors that are set forth in the “Risk Factors” section, the “Legal Proceedings” section, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section and other sections in our 2024 Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with or furnished to the Securities and Exchange Commission. Any forward-looking statements made by us in this release speak only as of the date on which they are made. We are under no obligation to, and expressly disclaim any obligation to, update or alter our forward-looking statements, whether because of new information, subsequent events or otherwise, except as required by law.

###

Appendix

Definitions

Net ARR Activity Metric (TTM)

Projected Annual Recurring Revenue (ARR) for contracts signed in the prior 12 months, less the annualized impact of any client losses, contractual volume and price changes, and other known impacts for which the company was notified in that same time period, which could positively or negatively impact results. The metric annualizes the net impact to revenue. Timing of revenue impact varies and may not be realized within the forward 12-month timeframe. The metric is for indicative purposes only. This metric excludes non-recurring revenue signings. This metric is not indicative of any specific 12 month timeframe.

New Business Annual Contract Value (ACV): (New Business TCV / contract term) multiplied by 12.

New Business Total Contract Value (TCV): Estimated total future revenues from contracts signed during the period related to new logo, new service line or expansion with existing customers.

TTM: Trailing twelve months.

PBT: Profit before tax.

Non-GAAP Financial Measures

We have reported our financial results in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In addition, we have discussed our financial results using non-GAAP measures.

We believe these non-GAAP measures allow investors to better understand the trends in our business and to better understand and compare our results. Accordingly, we believe it is necessary to adjust several reported amounts, determined in accordance with U.S. GAAP, to exclude the effects of certain items as well as their related tax effects. Management believes that these non-GAAP financial measures provide an additional means of analyzing the results of the current period against the corresponding prior period. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, the Company’s reported results prepared in accordance with U.S. GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a substitute for comparable U.S. GAAP measures and should be read only in conjunction with our Consolidated Financial Statements prepared in accordance with U.S. GAAP. Our management regularly uses our non-GAAP financial measures internally to understand, manage and evaluate our business and make operating decisions, and providing such non-GAAP financial measures to investors allows for a further level of transparency as to how management reviews and evaluates our business results and trends. These non-GAAP measures are among the primary factors management uses in planning for and forecasting future periods. Compensation of our executives is based in part on the performance of our business based on certain of these non-GAAP measures.

Management cautions that amounts presented in accordance with Conduent’s definition of non-GAAP financial measures may not be comparable to similar measures disclosed by other companies because not all companies calculate non-GAAP measures in the same manner.

A reconciliation of the following non-GAAP financial measures to the most directly comparable financial measures calculated and presented in accordance with U.S. GAAP are provided below.

These reconciliations also include the income tax effects for our non-GAAP performance measures in total, to the extent applicable. The income tax effects are calculated under the same accounting principles as applied to our reported pre-tax performance measures under Accounting Standards Codification 740, which employs an annual effective tax rate method. The noted income tax effect for our non-GAAP performance measures is effectively the difference in income taxes for reported and adjusted pre-tax income calculated under the annual effective tax rate method. The tax effect of the non-GAAP adjustments was calculated based upon evaluation of the statutory tax treatment and the applicable statutory tax rate in the jurisdictions in which such charges were incurred.

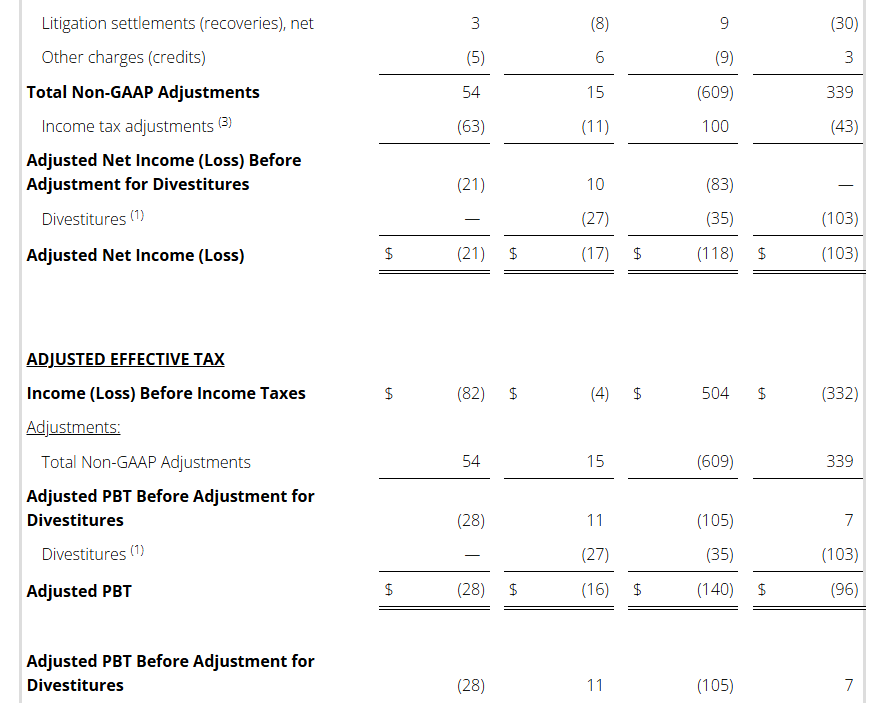

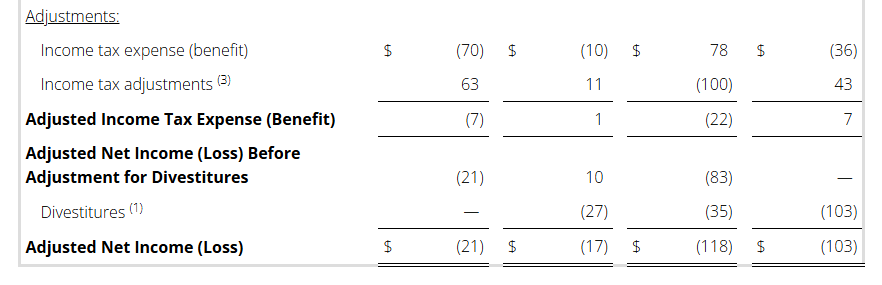

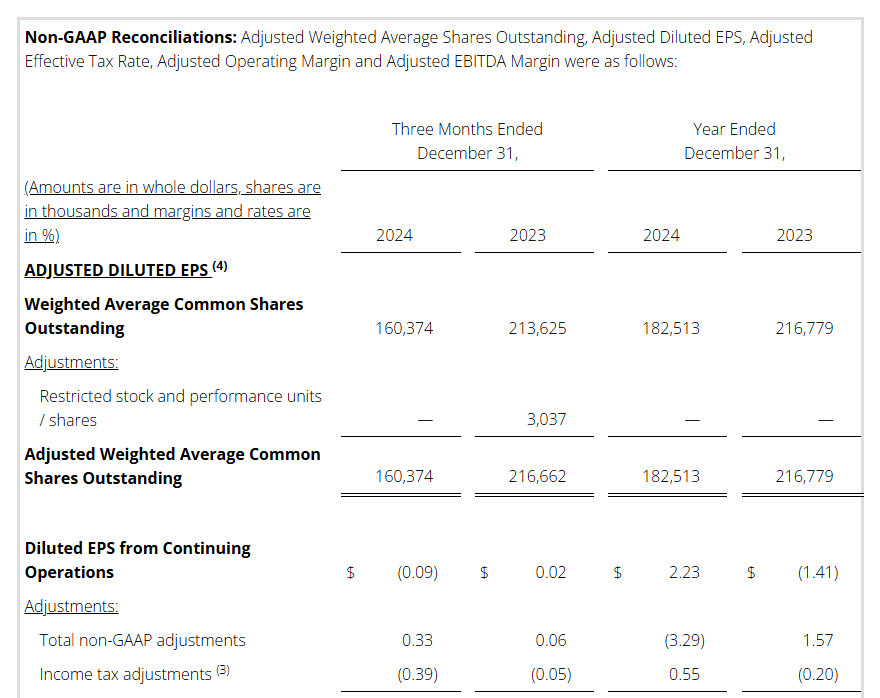

Adjusted Revenue, Adjusted Profit Before Tax, Adjusted Net Income (Loss), Adjusted Diluted Earnings per Share, Adjusted Weighted Average Common Shares Outstanding, and Adjusted Effective Tax Rate

We make adjustments to Revenue, Net Income (Loss) before Income Taxes for the following items, as applicable, to the particular financial measure, for the purpose of calculating Adjusted Revenue, Adjusted Profit Before Tax, Adjusted Net Income (Loss), Adjusted Diluted Earnings per Share, Adjusted Weighted Average Common Shares Outstanding, and Adjusted Effective Tax Rate:

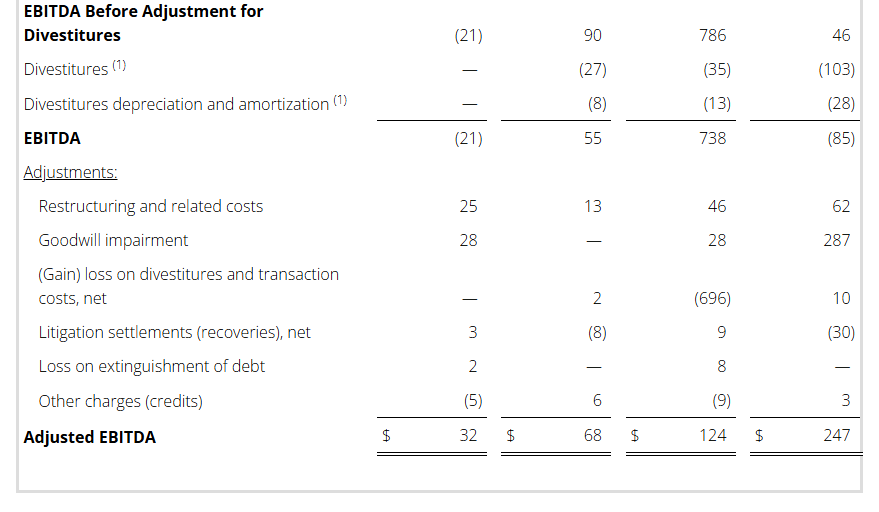

Amortization of acquired intangible assets. The amortization of acquired intangible assets is driven by acquisition activity, which can vary in size, nature and timing as compared to other companies within our industry and from period to period.

Restructuring and related costs. Restructuring and related costs include restructuring and asset impairment charges as well as costs associated with our strategic transformation program.

Goodwill impairment. This represents goodwill impairment charges arising from annual or interim goodwill testing.

(Gain) loss on divestitures and transaction costs, net. Represents (gain) loss on divested businesses and transaction costs.

Litigation settlements (recoveries), net represents settlements or recoveries for various matters subject to litigation.

Loss on extinguishment of debt. This represents write-off related debt issuance costs related to prepayments of debt.

Other charges (credits). This includes Other (income) expenses, net on the Consolidated Statements of Income (loss) and other adjustments.

Divestitures. Revenue and Adjusted EBITDA of divested businesses are excluded.

The Company provides adjusted net income and adjusted EPS financial measures to assist our investors in evaluating our ongoing operating performance for the current reporting period and, where provided, over different reporting periods, by adjusting for certain items which may be recurring or non-recurring and which in our view do not necessarily reflect ongoing performance. We also internally use these measures to assess our operating performance, both absolutely and in comparison to other companies, and in evaluating or making selected compensation decisions.

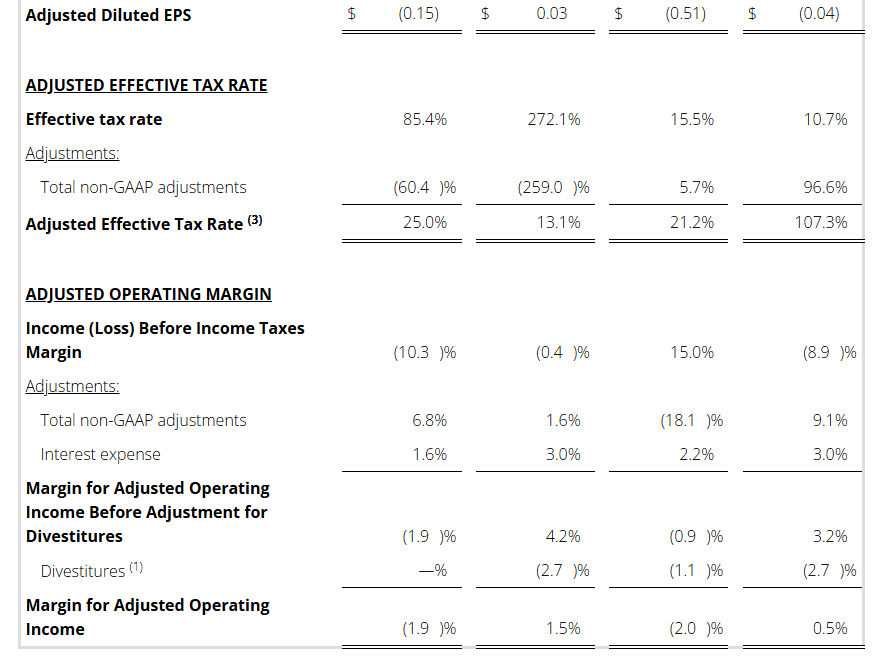

Management believes that the adjusted effective tax rate, provided as supplemental information, facilitates a comparison by investors of our actual effective tax rate with an adjusted effective tax rate which reflects the impact of the items which are excluded in providing adjusted net income and certain other identified items, and may provide added insight into our underlying business results and how effective tax rates impact our ongoing business.

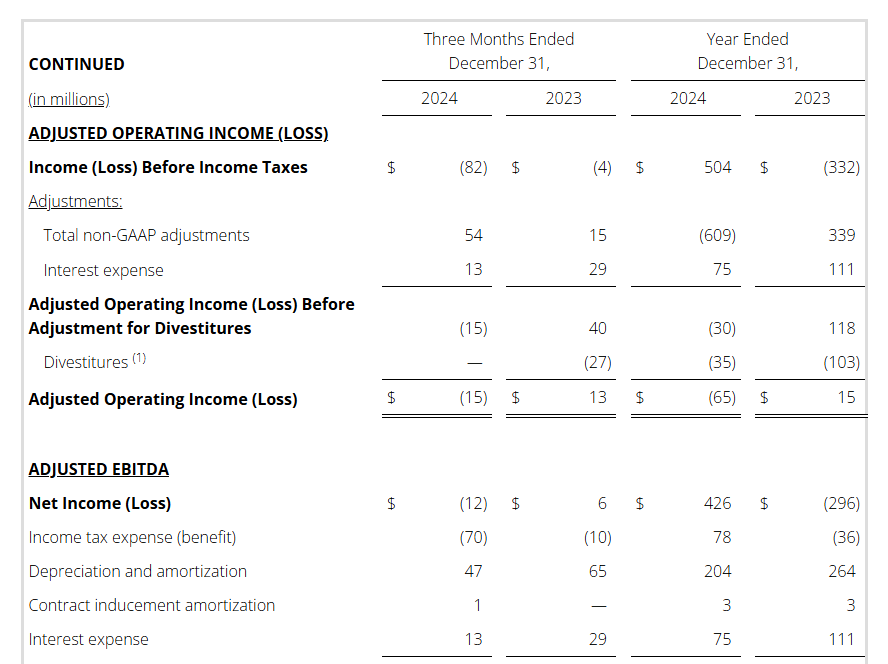

Adjusted Revenue, Adjusted Operating Income and Adjusted Operating Margin

We make adjustments to Revenue, Costs and Expenses and Operating Margin for the following items, as applicable, for the purpose of calculating Adjusted Revenue, Adjusted Operating Income and Adjusted Operating Margin:

Amortization of acquired intangible assets.

Restructuring and related costs.

Interest expense. Interest expense includes interest on long-term debt and amortization of debt issuance costs.

Goodwill impairment.

Loss on extinguishment of debt.

(Gain) loss on divestitures and transaction costs, net.

Litigation settlements (recoveries), net.

Other charges (credits).

Divestitures.

We provide our investors with adjusted revenue, adjusted operating income and adjusted operating margin information, as supplemental information, because we believe it offers added insight, by itself and for comparability between periods, by adjusting for certain non-cash items as well as certain other identified items which we do not believe are indicative of our ongoing business, and may also provide added insight on trends in our ongoing business.

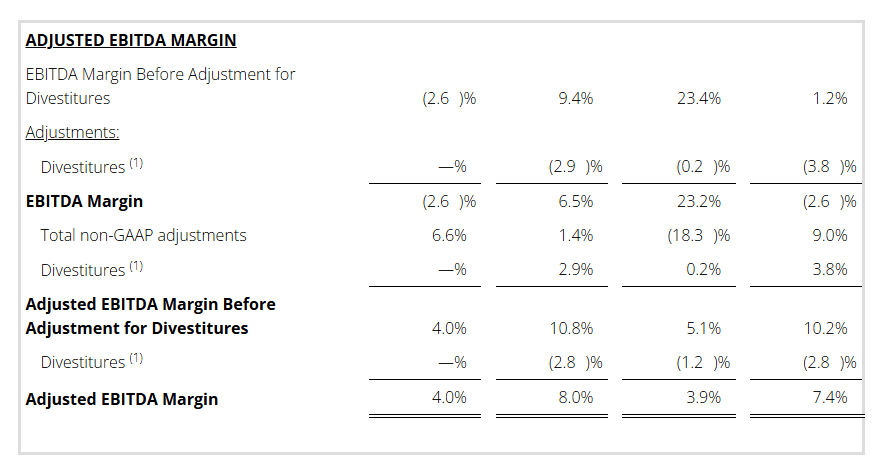

Adjusted EBITDA and EBITDA Margin

We use Adjusted EBITDA and Adjusted EBITDA Margin as an additional way of assessing certain aspects of our operations that, when viewed with the U.S. GAAP results and the accompanying reconciliations to corresponding U.S. GAAP financial measures, provide a more complete understanding of our on-going business. Adjusted EBITDA represents income (loss) before interest, income taxes, depreciation and amortization and contract inducement amortization adjusted for the following items. Adjusted EBITDA Margin is Adjusted EBITDA divided by revenue or adjusted revenue, as applicable.

Restructuring and related costs.

Goodwill impairment.

Loss on extinguishment of debt.

(Gain) loss on divestitures and transaction costs, net.

Litigation settlements (recoveries), net.

Other charges (credits).

Divestitures.

Adjusted EBITDA is not intended to represent cash flows from operations, operating income (loss) or net income (loss) as defined by U.S. GAAP as indicators of operating performance.

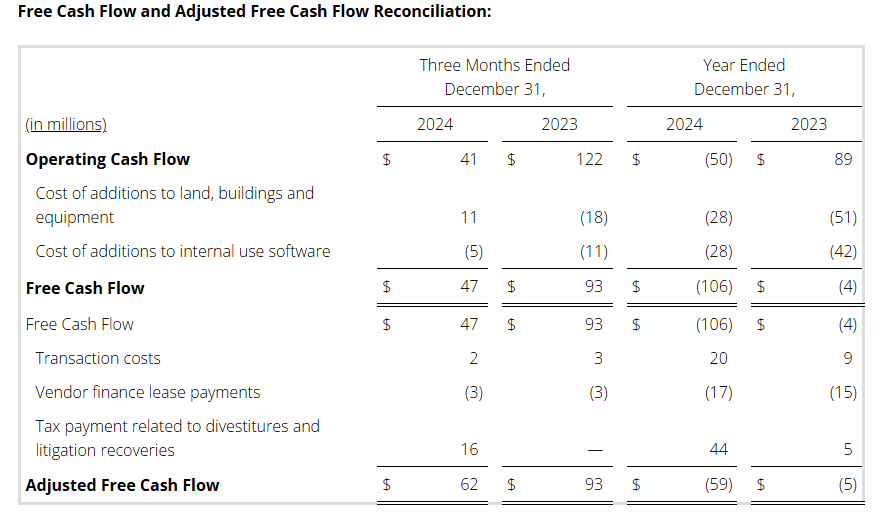

Free Cash Flow

Free Cash Flow is defined as cash flows from operating activities as reported on the consolidated statement of cash flows, less cost of additions to land, buildings and equipment, cost of additions to internal use software, and proceeds from sales of land, buildings and equipment, as applicable. We use the non-GAAP measure of Free Cash Flow as a criterion of liquidity. We use Free Cash Flow as a measure of liquidity to determine amounts we can reinvest in our core businesses, such as amounts available to make acquisitions and invest in land, buildings and equipment and internal use software, after required payments on debt. In order to provide a meaningful basis for comparison, we are providing information with respect to our Free Cash Flow reconciled to cash flow provided by operating activities, which we believe to be the most directly comparable measure under U.S. GAAP.

Adjusted Free Cash Flow

Adjusted Free Cash Flow is defined as Free Cash Flow from above plus adjustments for litigation insurance recoveries, transaction costs, taxes paid on gains from divestitures and litigation recoveries, proceeds from failed sale-leaseback transactions and certain other identified adjustments, as applicable. We use Adjusted Free Cash Flow, in addition to Free Cash Flow, to provide supplemental information to our investors concerning our ability to generate cash from our ongoing operating activities; by excluding these items, we believe we provide useful additional information to our investors to help them further understand our ability to generate cash period-over-period as well as added information on comparability to our competitors. Such as with Free Cash Flow information, as so adjusted, it is specifically not intended to provide amounts available for discretionary spending. We have added certain adjustments to account for items which we do not believe reflect our core business or operating performance, and we computed all periods with such adjusted costs.

Revenue at Constant Currency

To better understand trends in our business, we believe that it is helpful to adjust revenue to exclude the impact of changes in the translation of foreign currencies into U.S. Dollars. We refer to this adjusted revenue as “constant currency.” Currency impact is determined as the difference between actual growth rates and constant currency growth rates. This currency impact is calculated by translating the current period activity in local currency using the comparable prior-year period’s currency translation rate.

Non-GAAP Outlook

In providing the Full Year 2025 outlook for Adjusted EBITDA and Adjusted EBITDA Margin we exclude certain items which are otherwise included in determining the comparable U.S. GAAP financial measure. A description of the adjustments which historically have been applicable in determining Adjusted EBITDA and Adjusted EBITDA Margin is reflected in the table below. We are providing such outlook only on a non-GAAP basis because the company is unable without unreasonable efforts to predict with reasonable certainty the totality or ultimate outcome or occurrence of these adjustments for the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to reported results. We have provided an outlook for Adjusted Revenue only on a non-GAAP basis using foreign currency translation rates as of fiscal year end due to the inability to, without unreasonable efforts, accurately predict foreign currency impact on revenues. Full Year 2025 Outlook for Adjusted Free Cash Flow is provided as a factor of expected Adjusted EBITDA, and such outlook is only available on a non-GAAP basis for the reasons described above. For the same reason, we are unable to provide a GAAP expected adjusted tax rate, which adjusts for our non-GAAP adjustments. Non-GAAP Reconciliations: Adjusted Revenue, Revenue at Constant Currency, Adjusted Net Income (Loss), Adjusted Effective Tax, Adjusted Operating Income (Loss) and Adjusted EBITDA were as follows (see footnotes on last page of Non-GAAP reconciliations):

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a global leader in providing augmented reality (“AR”) and artificial intelligence (“AI”) Software-as-a-Service (“SaaS”) solutions to beauty and fashion industries, today announced that it plans to release its financial results for the full year of 2024 before U.S. markets open on Wednesday, February 26, 2025 and to hold a conference call at 7:30 p.m. Eastern Time the same day on February 26, 2025 (or 8:30 a.m. Taipei Standard Time the following day on February 27, 2025).

The Company’s management will discuss the financial results and latest developments during the conference call. For participants who wish to join the call, please complete online registration using the link provided below in advance of the conference call. Upon registration, each participant will receive a participant dial-in number and a unique access PIN, which can be used to join the conference call.

A live and archived webcast of the conference call will also be available at the Company’s investor relations website at https://ir.perfectcorp.com.

About Perfect Corp.

Perfect Corp. (NYSE: PERF) leverages ‘Beautiful AI’ innovations to make our world more beautiful. As a pioneer and leader in the space, Perfect Corp. works with over 650 partners around the globe to empower brands to embrace the digital-first world by transforming shopping journeys through digital tech innovations. Perfect Corp.’s suite of enterprise solutions delivers synergistic, technology-driven experiences that facilitate sustainable, ultra-personalized, and engaging shopping journeys through hyper-realistic virtual try-ons, AI-powered skin analyses, personalized product recommendation tools and many more Beautiful AI innovations. For more information, visit https://ir.perfectcorp.com/.

Conni will be integrated into multiple Conduent platforms to boost clients’ productivity, enhance quality, and elevate customer experience

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global leader in technology-driven business solutions and services, launches Conni, an innovative GenAI virtual assistant developed as part of the company’s AI initiative. Leveraging Microsoft Azure OpenAI Service, Conni is designed to enhance the quality of results and improve customer experience across Conduent platforms for companies and government agencies.

“We will continue to embed AI and generative AI within our solutions to drive functionality. New features like Conni build on Conduent’s strategy of integrating advanced technologies, such as automation, machine learning, and digitalization to drive better outcomes for our clients,” said Cliff Skelton, President and Chief Executive Officer at Conduent. “In our Human Capital Solutions business, Conni is deployed to help employees navigate their benefits. By enhancing the employee experience, Conni can drive improved satisfaction and help reduce HR-related inquiries.”