Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second quarter financial results. FreightCar America generated adjusted net income of $3.8 million or $0.11 per share, compared to our estimate of $2.0 million or $0.06 per share. Second quarter revenue of $118.6 million exceeded our estimate of $100.6 million. Rail car deliveries were 939 units compared to 1,159 units during the prior year period and our estimate of 850. The year-over-year decline was attributed to a strategic shift in the product mix toward higher-margin rail cars. As a percentage of revenue, second quarter gross margin increased to 15.0% compared to 12.5% during the prior year period and our 12.7% estimate. Adjusted EBITDA amounted to $10.0 million compared to our $8.8 million estimate and represented an EBITDA margin of 8.4%. RAIL generated adjusted free cash flow of $7.9 million and ended the quarter with $61.4 million in cash and cash equivalents.

Favorable outlook. During the second quarter, RAIL received 1,226 new rail car orders valued at $106.9 million. With a backlog of 3,624 units valued at $316.9 million, we expect deliveries to accelerate throughout the year. During the quarter, RAIL increased utilization across its four production lines, enhanced productivity, and benefited from a higher-margin product mix. The company is advancing its growth strategy by investing in its tank car capabilities, which it expects to strengthen its cost position and support long-term accretive growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increasing longer-term rail car delivery estimates. While we have maintained our rail car delivery estimates for 2025 through 2027, we have increased our delivery estimates for 2028 through 2030. We now forecast rail car deliveries of 5,500, 5,750, and 6,000, respectively, compared with our prior estimates of 5,000, 5,000, and 5,000. While we had previously assumed that RAIL would operate four production lines with an aggregate capacity of 5,000 rail cars through 2030, we now assume the company will operate five production lines with a total capacity of 6,250 rail cars beginning in 2028. Our prior assumption had been that the company could begin producing a new line of higher-margin tank cars using existing capacity at the expense of lower margin products. Because we think tank cars could add an incremental 500 or more orders beginning in 2028, the tank cars would be incremental to existing orders with five production lines.

Updating earnings estimates. We forecast 2025 EBITDA and EPS of $45.9 million and $0.47, respectively, while our 2026 estimates are $48.6 million and $0.53. While our 2025 and 2026 EBITDA estimates are unchanged, we have increased our forward estimates, which may be found in the financial model at the end of this report. While our earnings estimates have increased, gross margin as a percentage of sales remains unchanged at 13.0%, 13.3%, 13.5%, and 13.8% in 2027, 2028, 2029, and 2030, respectively, while selling, general, and administrative expense as a percentage of sales increased modestly.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company listed in the U.S. capital markets. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 18 vessels (1 Newcastlemax and 17 Capesize) with an average age of approximately 13.4 years and an aggregate cargo carrying capacity of approximately 3,236,212 dwt. Upon completion of the delivery of the previously announced Capesize vessel acquisition, the Company’s operating fleet will consist of 19 vessels (1 Newcastlemax and 18 Capesize) with an aggregate cargo carrying capacity of approximately 3,417,608 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second Quarter 2025 Estimate Revisions. We are raising our Q2 2025 net revenue forecast to $36.5 million from $35.9 million, driven by stronger-than-expected time charter equivalent (TCE) rates. However, we are lowering our adjusted EBITDA and EPS estimates to $16.7 million and $0.11, respectively, from $17.3 million and $0.17, reflecting higher operating expenses of $29.1 million versus $27.5 million previously. The increase reflects a full quarter of the expanded fleet as well as higher-than-expected dry-docking activity.

Full-Year 2025 Estimate Changes. We are increasing our 2025 revenue forecast to $143.4 million from $142.9 million, as we expect improving rate momentum to continue through year-end. We are also raising our operating expense estimate to $113.9 million from $109.4 million, reflecting a greater number of anticipated dry-docking days. As a result, we are lowering our adjusted EBITDA projection to $67.7 million from $70.5 million and our EPS estimate to $0.51 from $0.74.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating second quarter estimates. We are raising our second quarter revenue and adjusted earnings per share estimates to $56.7 million and $3.87, respectively, from $54.0 million and $3.45. Additionally, we are increasing our adjusted EBITDA estimate to $38.5 million from $35.0 million. The upward revisions are driven by stronger-than-expected time charter equivalent (TCE) rates.

Full-year 2025 estimates. For the full-year 2025, we expect higher revenues and adjusted earnings per share estimates of $228.5 million and $15.47, respectively, up from $225.6 million and $15.05. We are raising our operating expense estimates to $83.0 million from $81.7 million, due to higher dry-docking expenses. Our full year adjusted EBITDA estimate has been increased to $153.1 million from $149.2 million. The increases in our estimates are largely due to higher TCE rates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second quarter estimates. We are lowering our Q2 2025 revenue and adjusted earnings per share estimates to $11.4 million and a loss of $1.23, respectively, from $14.1 million and a loss of $0.76. Additionally, we are reducing our operating expenses to $13.0 million from $14.4 million, as dry docking expenses have been pushed into the third quarter. Despite lower operating expenses, we are decreasing our adjusted EBITDA estimate to $1.6 million from $2.9 million. The decrease in our earnings estimates is mainly due to lower-than-expected time charter equivalent (TCE) rates.

Full-Year 2025 estimates. We are lowering our 2025 revenue and adjusted earnings per share estimates to $46.0 million and a loss of $4.41, respectively, from $50.3 million and a loss of $3.79. We are trimming our operating expenses to $51.4 million from $51.8 million, due to lower expected voyage expenses. Our adjusted EBITDA estimates were lowered to $5.6 million from $9.3 million. The lower estimates are driven by soft market rates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, June 18, 2025 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA, the “Company” or “Euroseas”), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today its results for the three-month period ended March 31, 2025 and declared a common stock dividend.

First Quarter 2025 Financial Highlights:

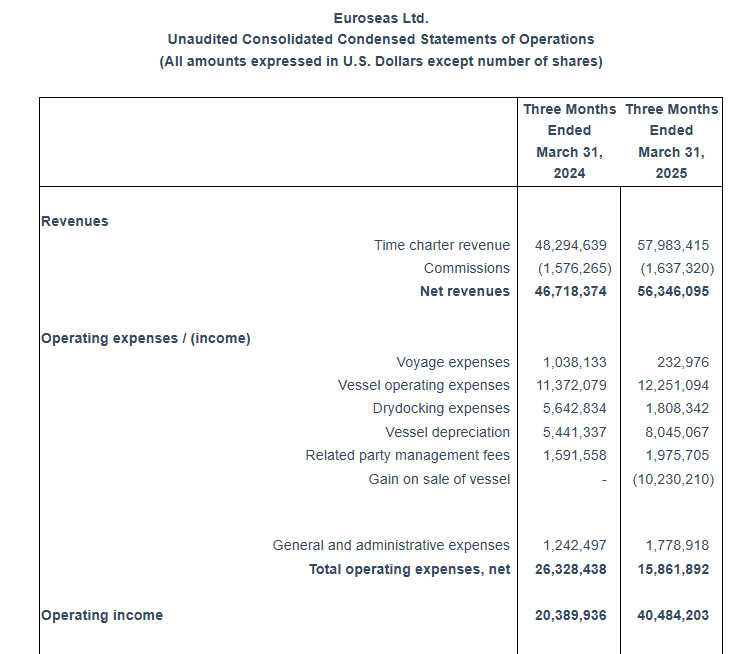

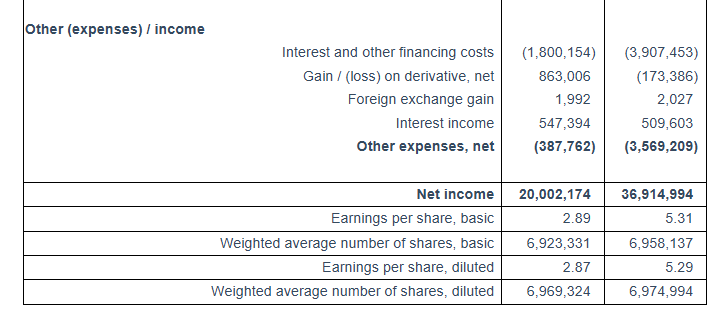

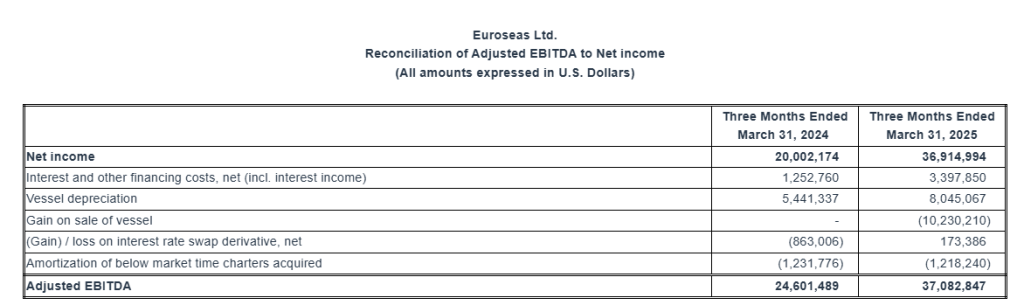

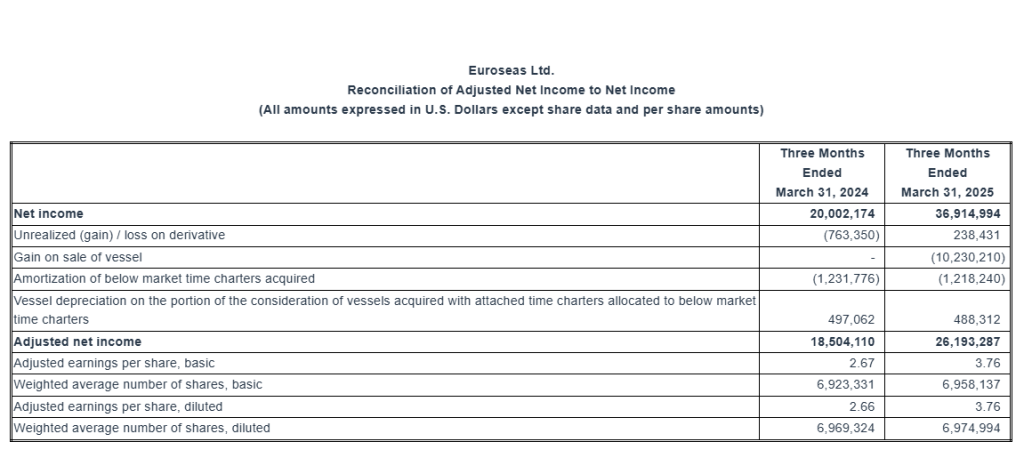

Total net revenues of $56.3 million. Net income of $36.9 million or $5.31 and $5.29 earnings per share basic and diluted, respectively. Adjusted net income1 for the period was $26.2 million or $3.76 per share basic and diluted.

Adjusted EBITDA1 was $37.1 million.

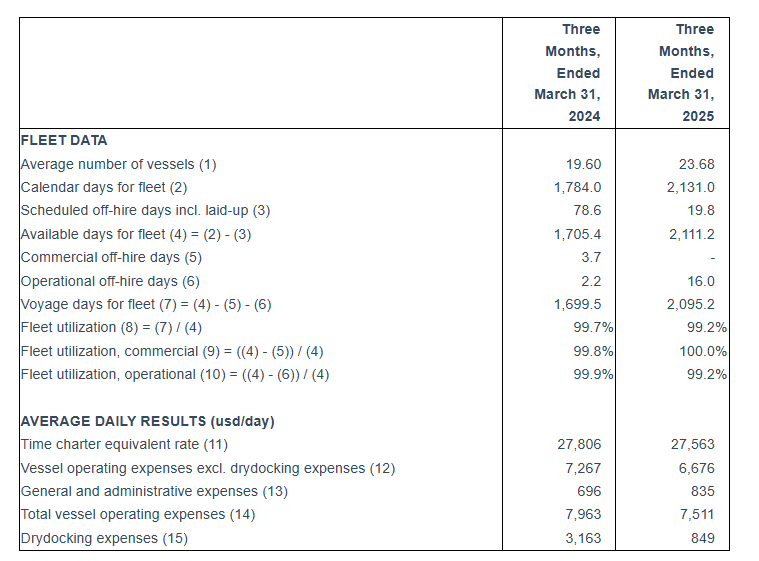

An average of 23.71 vessels were owned and operated during the first quarter of 2025 earning an average time charter equivalent rate of $27,563 per day.

Declared a quarterly dividend of $0.65 per share for the first quarter of 2025 payable on or about July 16, 2025 to shareholders of record on July 9, 2025, as part of the Company’s common stock dividend plan.

On March 17, 2025 the Company completed the spin-off of three of its subsidiaries containing its two older vessels, M/V Aegean Express and M/V Joanna, along with the proceeds from the earlier sale of the vessel M/V Diamantis P, into Euroholdings Ltd. (NASDAQ: EHLD). Beginning on March 18, 2025, Euroholdings Ltd. operates as an independent company.

On May 29, 2025, the Company announced that it has signed an agreement to sell M/V Marcos V, a 6,350 teu intermediate containership built in 2005, to an unaffiliated third party, for $50 million. The vessel is scheduled to be delivered to its buyer in October 2025. The Company is expected to recognize a gain on the sale in excess of $8.50 million, or $1.20 per share.

As of June 18, 2025 we had repurchased 463,074 of our common stock in the open market for a total of about $10.5 million, since the initiation of our share repurchase plan of up to $20 million announced in May 2022.

________________________ 1 Adjusted EBITDA, Adjusted net income and Adjusted earnings per share are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for Euroseas financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

Aristides Pittas, Chairman and CEO of Euroseas commented: “During the first quarter of 2025, the containership markets showed further strength, with both smaller and larger feeder segments seeing notable rate increases. This positive momentum has continued into the second quarter, with particularly strong gains in the smaller feeder segment. Market strength is also reflected in the secondhand S&P market, where demand for existing tonnage remains firm despite the continued delivery of newbuilds. Reflecting this dynamic, we successfully finalized the sale of one of our intermediate vessels, the M/V Marcos V, to an unaffiliated third party. The market strength is further reflected in our chartering activity resulting in almost 100% charter coverage for 2025 and in excess of 65% for 2026.

“Looking ahead, the containership sector may face notable challenges, primarily due to the high overall orderbook and the possibility that liner companies may resume transits through the Suez Canal. However, elevated geopolitical uncertainty driven by ongoing and escalating tensions between Iran and Israel compounded by uncertainty surrounding the U.S. Administration’s proposed tariffs add another layer of complexity. Specifically, on the supply-side while the orderbook remains high and represents the key challenge for the sector, it is heavily concentrated on larger vessel sizes. In contrast, the feeder and intermediate segments, where our fleet is concentrated, have historically low orderbooks; in addition, due to the higher proportion of older tonnage in these size segments, they are likely to experience a reduction in fleet supply over the coming years. This evolving fleet profile supports the view that, despite the potential risk of cascading from larger vessels, the fundamentals for feeder and intermediate containerships remain favorable.

“On the fleet growth front, we continue to consider ways of further modernizing our fleet. We will be soon retrofitting one more of our secondhand vessels with energy-saving devices. We have further improved our fleet profile by having transferred our two oldest ships to Euroholdings, a spin-off from our company, to pursue a separate independent market and investment strategy. Given our solid liquidity position, our Board has decided to maintain our high yielding quarterly dividend of $0.65 per share. We are also continuing our share buyback program, as our shares are trading at a substantial discount to our net asset value, despite the visibility of our revenues and earnings. As always, we remain committed to identifying attractive investment opportunities that enhance shareholder value and drive sustainable returns.”

Tasos Aslidis, Chief Financial Officer of Euroseas commented: “Our revenues for the first quarter of 2025 are increased by approximately 20% compared to the same period of 2024. This was mainly the result of the increased average number of vessels owned and operated in the first quarter of 2025, compared to the corresponding period of 2024. The Company operated an average of 23.68 vessels, versus 19.60 vessels during the same period last year. Net revenues amounted to $56.3 million for the first quarter of 2025 compared to $46.7 million for the first quarter of 2024.

“Total daily vessel operating expenses, including management fees, general and administrative expenses, but excluding drydocking costs, were $6,676 during the first quarter of 2025 compared $7,276 to the same quarter of last year. This was the result of the lower operating costs of the nine newbuilding vessels delivered during last year and in the first quarter of 2025. In the first quarter of 2024 the Company operated only five of these newbuilding vessels, while the rest were delivered gradually until January 2025.

“Adjusted EBITDA1 during the first quarter of 2025 was $37.1 million compared to $24.6 million achieved in the first quarter of last year.

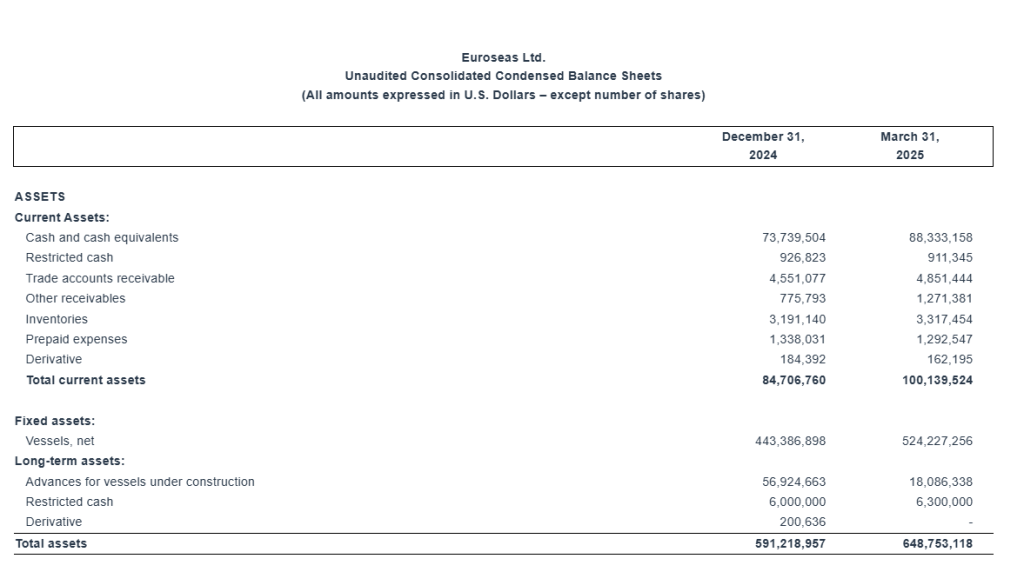

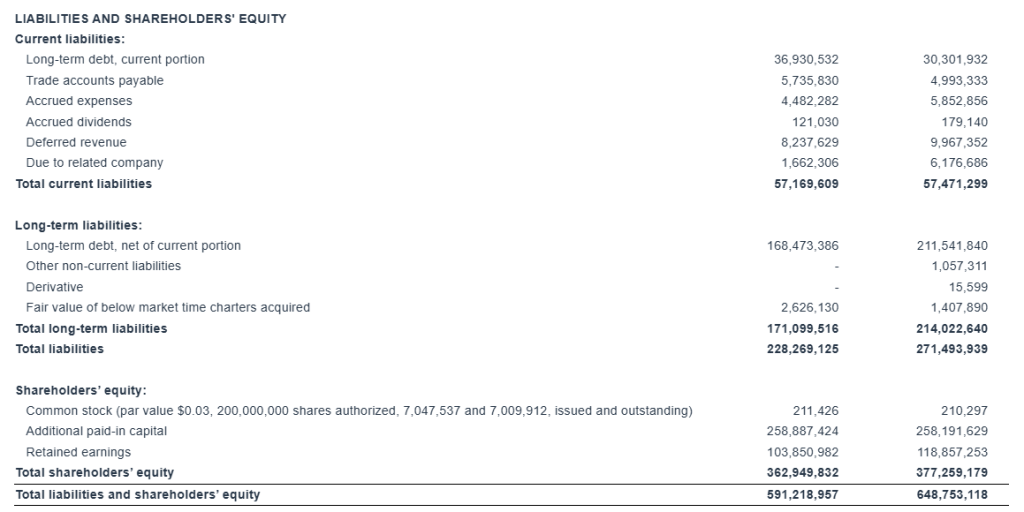

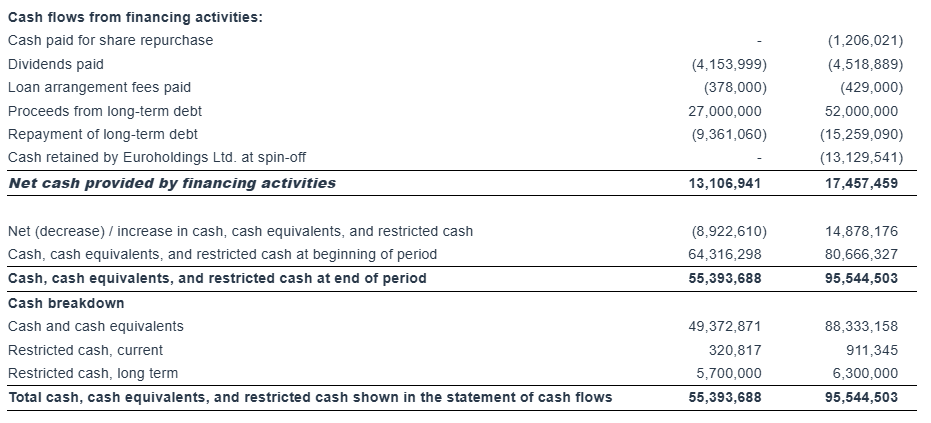

“As of March 31, 2025, our outstanding bank debt (before deducting the unamortized loan fees) was $244.0 million, versus restricted and unrestricted cash of approximately $95.5 million. As of the same date, our scheduled debt repayments over the next 12 months amounted to about $30.7 million (excluding the unamortized loan fees).”

First Quarter 2025 Results: For the first quarter of 2025, the Company reported total net revenues of $56.3 million representing an 20.6% increase over total net revenues of $46.7 million during the first quarter of 2024. On average, 23.68 vessels were owned and operated during the first quarter of 2025 earning an average time charter equivalent rate of $27,563 per day compared to 19.60 vessels in the same period of 2024 earning on average $27,806 per day. The Company reported a net income for the period of $36.9 million, as compared to a net income of $20.0 million for the first quarter of 2024.

Voyage expenses for the first quarter of 2025 amounted to $0.2 million as compared to voyage expenses of $1.0 million for the same period of 2024. The increased amount of 2024 is mainly attributable to bunkers consumption by three of our vessels (M/V “Synergy Antwerp”, M/V “Synergy Oakland” and M/V “Marcos”) during their drydock period.

Vessel operating expenses for the first quarter of 2025 amounted to $12.3 million as compared to $11.4 million for the same period of 2024. The increased amount is due to the higher number of vessels owned and operated in the first quarter of 2025 compared to the corresponding period of 2024.

Depreciation expense for the first quarter of 2025 amounted to $8.0 million compared to $5.4 million for the same period of 2024 due to the increased number of vessels in the Company’s fleet.

Related party management fees for the first quarter of 2025 increased to $2.0 million from $1.6 million for the same period of 2024 as a result of the higher number of vessels in our fleet and the adjustment for inflation in the daily vessel management fee, effective from January 1, 2025, increasing it from 810 Euros to 840 Euros.

In the first quarter of 2025 two of our vessels completed extensive repairs afloat for a total cost of $1.8 million. In the first quarter of 2024 three of our vessels completed their special survey with drydock for a total cost of $5.6 million.

General and administrative expenses slightly increased to $1.8 million in the first quarter of 2025, as compared to $1.2 million in the first quarter of 2024 due to increased professional fees and increased cost for our stock incentive plan.

Interest and other financing costs for the first quarter of 2025 amounted to $3.9 million. Capitalized interest charged on the cost of our newbuilding program was $0.1 million for the first quarter of 2025. For the same period of 2024 interest and other financing costs amounted $1.8 million and the capitalized interest charged on the cost of our newbuilding program was $1.4 million. This increase is due to the increased amount of debt in the current period compared to the same period of 2024. For the three months ended March 31, 2025 the Company recognized a $0.17 million loss on its interest rate swap contract, comprising a $0.07 million realized gain and a $0.24 million unrealized loss. For the three months ended March 31, 2024 the Company recognized a $0.86 million gain on its interest rate swap contracts, comprising a $0.10 million realized gain and a $0.76 million unrealized gain.

Adjusted EBITDA1 for the first quarter of 2025 was $37.1 million, compared to $24.6 million achieved for the first quarter of 2024, primarily higher revenues due to the higher number of vessels owned and operated.

Basic and diluted earnings per share for the first quarter of 2025 was $5.31 and $5.29, respectively, calculated on 6,958,137 basic and 6,974,994 diluted weighted average number of shares outstanding compared to basic and diluted earnings per share of $2.89 and $2.87, respectively for the first quarter of 2024, calculated on 6,923,331 basic and 6,969,324 diluted weighted average number of shares outstanding.

The adjusted earnings per share for the quarter ended March 31, 2025 would have been $3.76 per share basic and diluted, respectively, compared to adjusted earnings of $2.67 and $2.66 per share basic and diluted, respectively, for the first quarter of 2024. Usually, security analysts include Adjusted Net Income in their determination of published estimates of earnings per share.

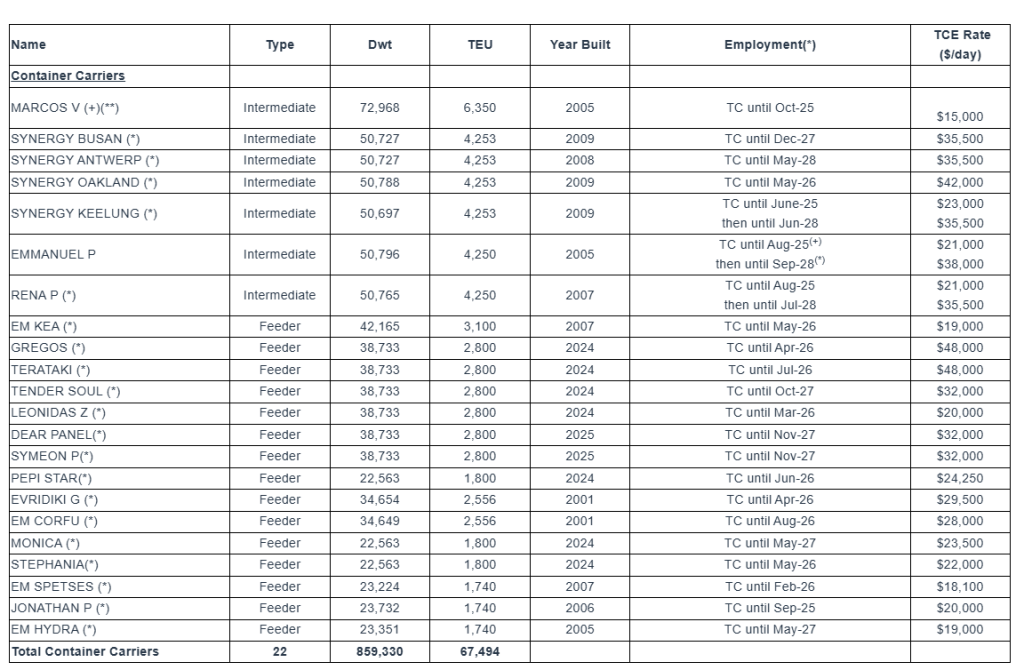

Fleet Profile: The Euroseas Ltd. fleet profile as of June 18, 2025 is as follows:

Summary Fleet Data:

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was in our possession including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up, vessels committed for sale or vessels that suffered unrepaired damages, are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up, or vessels that were committed for sale or suffered unrepaired damages.

(4) Available days. We define available days as the Calendar days in a period net of scheduled off-hire days as defined above. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Time charter equivalent rate, or TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating TCE is determined by dividing time charter revenue and voyage charter revenue, if any, net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract, or are related to repositioning the vessel for the next charter. TCE, which is a non-GAAP measure, provides additional meaningful information in conjunction with voyage revenues, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters and bareboat charters) under which the vessels may be employed between the periods. Our definition of TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which includes crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expenses are calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. TVOE is the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses is calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period, Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, Wednesday, June 18, 2025 at 09:30 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

Conference Call details: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “Euroseas” to the operator and/or conference ID 13754421. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio Webcast – Slides Presentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.euroseas.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2025, will also be available in PDF format minutes prior to the conference call and webcast, accessible on the company’s website (www.euroseas.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

Adjusted EBITDA Reconciliation:

Euroseas Ltd. considers Adjusted EBITDA to represent net income before interest and other financing costs, income taxes, depreciation, (gain) / loss on interest rate swap derivative, net, gain on sale of vessel, and amortization of fair value of below market time charters acquired. Adjusted EBITDA does not represent and should not be considered as an alternative to net income, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance and liquidity position and because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of financial costs, loss / (gain) on interest rate swaps, gain on sale of vessel, depreciation, and amortization of below market time charters acquired. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

Adjusted net income and Adjusted earnings per share Reconciliation: Euroseas Ltd. considers Adjusted net income to represent net income before unrealized (gain) / loss on derivative, gain on sale of vessel, amortization of below market time charters acquired and vessel depreciation on the portion of the consideration of vessels acquired with attached time charters allocated to below market time charters. Adjusted net income and Adjusted earnings per share are included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the aforementioned items, which may significantly affect results of operations between periods.

Adjusted net income and Adjusted earnings per share do not represent and should not be considered as an alternative to net income or earnings per share, as determined by GAAP. The Company’s definition of Adjusted net income and Adjusted earnings per share may not be the same as that used by other companies in the shipping or other industries. Adjusted net income and Adjusted earnings per share are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

About Euroseas Ltd. Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA.

Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

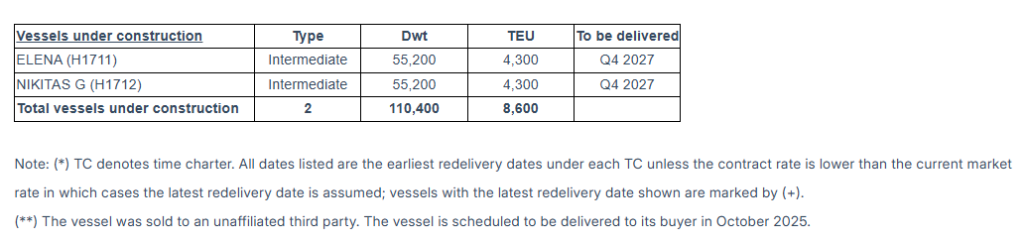

The Company has a fleet of 22 vessels, including 15 Feeder containerships and 7 Intermediate containerships. Euroseas 22 containerships have a cargo capacity of 67,494 teu. After the delivery of two intermediate containership newbuildings in the fourth quarter of 2027, Euroseas’ fleet will consist of 24 vessels with a total carrying capacity of 76,094 teu.

Forward Looking Statement This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for containerships, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

ATHENS, Greece, June 16, 2025 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today that it will release its financial results for the first quarter ended March 31, 2025, on June 18, 2025, before market opens in New York.

On the same day, Wednesday, June 18 at 9:30 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “Euroseas” to the operator and/or conference ID 13754421. Click here for additional participant International Toll-Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast‐Slides Presentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.euroseas.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2025, will also be available in PDF format minutes prior to the conference call and webcast, accessible on the company’s website (www.euroseas.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

AboutEuroseasLtd. Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements. The Company has a fleet of 22 vessels, including 15 Feeder containerships and 7 Intermediate containerships. Euroseas 22 containerships have a cargo capacity of 67,494 teu. After the delivery of two feeder containership newbuildings in the the fourth quarter of 2027, Euroseas’ fleet will consist of 24 vessels with a total carrying capacity of 76,094 teu.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New M/V Emmanuel P time charter contract. Euroseas Ltd. secured a new time charter contract for its 4,250 twenty-foot-equivalent (TEU) intermediate containership, M/V Emmanuel P, for a minimum of 36 months to a maximum period of 38 months, at the option of the charterer, at a gross daily rate of $38,000. The new contract represents a significant improvement compared to the previous rate of $21,000 per day. Following the completion of a scheduled drydock and installation of energy saving devices, the new charter is expected to commence upon delivery of the vessel from the shipyard in the first half of September.

Agreement to sell the M/V Marcos. Euroseas Ltd. recently signed an agreement to sell the M/V Marcos V, a 6,350 twenty-foot-equivalent unit (TEU) intermediate containership, to an unaffiliated third party for $50 million. The vessel will be delivered to the buyer in October 2025. ESEA expects to recognize a gain of ~$8.5 million, or $1.20 per share. The vessel was acquired in the fourth quarter of 2021 for $40 million. During its ownership, Euroseas Ltd. realized more than five times its original equity investment.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company listed in the U.S. capital markets. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 18 vessels (1 Newcastlemax and 17 Capesize) with an average age of approximately 13.4 years and an aggregate cargo carrying capacity of approximately 3,236,212 dwt. Upon completion of the delivery of the previously announced Capesize vessel acquisition, the Company’s operating fleet will consist of 19 vessels (1 Newcastlemax and 18 Capesize) with an aggregate cargo carrying capacity of approximately 3,417,608 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter results. Seanergy reported first-quarter net revenues of $24.2 million, slightly ahead of our estimate of $23.5 million, due to a higher-than-expected time charter equivalent (TCE) rate. Adjusted EBITDA and earnings per share (EPS) were $8.0 million and a loss of $0.27, respectively, compared to our estimates of $6.1 million and a loss of $0.38. The better-than-anticipated results are reflective of higher revenues as well as lower costs due to savings in general and administrative expenses.

Updating estimates. We are increasing our 2025 revenue estimates to $142.9 million from $142.5 million. Additionally, we are raising our adjusted EBITDA and EPS estimates to $70.5 million and $0.74, respectively, up from $68.1 million and $0.59. These revisions are reflective of management’s guidance of better-than-expected TCE rates and fewer dry-docking days, resulting in higher operating days and lower expenses.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full year 2024 financial results. FreightCar America generated 2024 adjusted net income to common stockholders of $4.5 million or $0.15 per share compared to a loss of $11.0 million or $(0.39) per share in 2023 and our estimate of $5.5 million or $0.17 per share. Gross margin as a percentage of revenue increased to 12.0% compared to 11.7% in FY 2023. Revenue and rail car deliveries increased to $559.4 million and 4,362 compared to $358.1 million and 3,022 in 2023. We had forecast revenue of $577.4 million and deliveries of 4,550. Adjusted EBITDA increased to $43.0 million compared to $20.1 million in 2023 and our estimate of $38.3 million. Full year adjusted free cash flow amounted to $21.7 million versus $(17.6) million in 2023.

Full Year 2025 corporate guidance. Management issued full year 2025 guidance. Railcar deliveries are expected to be in the range of 4,500 to 4,900, revenue is expected to be in the range of $530 million to $595 million, and adjusted EBITDA is expected to be in the range of $43 to $49 million. Compared to 2024, railcar deliveries, revenue, and adjusted EBITDA are expected to increase 7.7%, 0.6%, and 7.0%, respectively, at the midpoints of guidance. Our current 2025 estimates include railcar deliveries of 4,675 units, revenue of $580.6 million and EBITDA of $44.9 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, March 06, 2025 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA, the “Company” or “Euroseas”), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today that it has requested that the registration statement on Form 20-F of Euroholdings Ltd. (“Euroholdings”) be declared effective by the Securities and Exchange Commission on or around March 6, 2025. The Company also announced that the application of Euroholdings Ltd. for listing on the NASDAQ Capital Market under the symbol “EHLD” has been approved, subject to notice of issuance.

Currently, Euroholdings Ltd. is a wholly owned subsidiary of the Company. Shares of Euroholdings Ltd. will be distributed on or around March 17, 2025 (the “Distribution Date”) to shareholders of record of the Company as of March 7, 2025 (the “Record Date”). The Company’s shareholders will receive one share of common stock of Euroholdings Ltd. for every two and a half shares of common stock of the Company they own as of the Record Date. Fractional shares of common stock will not be distributed. Instead, the distribution agent will aggregate fractional shares of common stock into whole shares, sell such whole shares in the open market at prevailing rates promptly after our shares of common stock commence trading on the Nasdaq Capital Market, and distribute the net cash proceeds from the sales pro rata to each holder who would otherwise have been entitled to receive fractional shares of common stock in the distribution.

After the spin-off, the Company will continue owning and operating its fleet of 22-feder and intermediate-size container carrier vessels, while Euroholdings Ltd. will independently own and operate its fleet of two vessels.

Shares of Euroseas common stock will continue to trade “regular-way” on NASDAQ under the symbol “ESEA” through and after the March 17, 2025 Distribution Date. Any holder of shares of Euroseas common stock who sells Euroseas shares “regular way” through the close of trading on the March 17, 2025 Distribution Date will also be selling their right to receive shares of Euroholdings common stock in the distribution.

It is anticipated that Euroseas shares will also trade “ex-distribution” (that is, without the right to receive shares of Euroholdings common stock in the distribution) beginning on or about March 7, 2025, and continuing through the close of trading on March 17, 2025, under the symbol “ESEAV”. Beginning on March 18, 2025, “regular-way” trading in Euroseas stock will reflect the distribution of Euroholdings Ltd.

A “when-issued” public trading market for Euroholdings Ltd.’s common stock is expected to begin on or about March 7, 2025 on NASDAQ under the symbol “EHLDV” and continue through the close of trading on March 17, 2025. Beginning on March 18, 2025, “when-issued” trading under the symbol “EHLDV” will end and Euroholdings Ltd. will begin “regular-way” trading on NASDAQ under the symbol “EHLD”. Investors are encouraged to consult with their financial advisors regarding the specific implications of buying or selling Euroseas common stock on or before the Distribution Date.

Aristides Pittas, Chairman and CEO of Euroseas, commented: “We are excited with the spin-off and separate listing of our elder vessels into a separate publicly listed company, Euroholdings Ltd. This spin-off will allow both companies to pursue different investment strategies and different distributions to their shareholders. Management of each company will be able to set the appropriate performance indicators for its respective strategy and more effectively communicate it to investors and the financial community. We plan to take advantage of growth opportunities to increase the size of each company as we believe that they are both well positioned to do so both in terms of their capital structure and their contract mix.

“Specifically, Euroseas will continue focusing on operating container vessels with a lower environmental footprint by owning – on average – younger vessels, keep investing in retrofits of certain of its existing vessels to improve their efficiency and continuing its newbuilding program of modern, fuel-efficient containerships.

“Euroholdings will focus on managing elder vessels, likely, operating them to the end of their economic lives. It will also have the opportunity to explore investments in vessels in other sectors as well as other maritime opportunities. We expect for each of Euroseas and Euroholdings to be valued better separately than if they continue to operate together by offering more options to shareholders.”

Fleet Profile:

After the spin-off of Euroholdings Ltd., the Euroseas Ltd. fleet profile is as follows:

Name

Type

Dwt

TEU

Year Built

Employment(*)

TCE Rate ($/day)

Container Carriers

MARCOS V(*)

Intermediate

72,968

6,350

2005

TC until Aug-25

$15,000

SYNERGY BUSAN (*)

Intermediate

50,726

4,253

2009

TC until Dec-27

$35,500

SYNERGY ANTWERP (+)(*)

Intermediate

50,726

4,253

2008

TC until May-25 then until May-28

$26,500 $35,500

SYNERGY OAKLAND (*)

Intermediate

50,787

4,253

2009

TC until May-26

$42,000

SYNERGY KEELUNG (+)(*)

Intermediate

50,969

4,253

2009

TC until Jun-25 TC until Jun-28

$23,000 $35,500

EMMANUEL P(*)

Intermediate

50,796

4,250

2005

TC until Apr-25

$21,000

RENA P(*)

Intermediate

50,796

4,250

2007

TC until Apr-25

$21,000

EM KEA (*)

Feeder

42,165

3,100

2007

TC until May-26

$19,000

GREGOS (*)

Feeder

37,237

2,800

2023

TC until Apr-26

$48,000

TERATAKI(*)

Feeder

37,237

2,800

2023

TC until Jul-26

$48,000

TENDER SOUL (*)

Feeder

37,237

2,800

2024

TC until Oct-27

$32,000

LEONIDAS Z (*)

Feeder

37,237

2,800

2024

TC until Mar-26

$20,000

DEAR PANEL (*)

Feeder

37,237

2,800

2025

TC until Nov-27

$32,000

SYMEON P (*)

Feeder

37,237

2,800

2025

TC until Nov-27

$32,000

EVRIDIKI G (*)

Feeder

34,677

2,556

2001

TC until Apr-26

$29,500

EM CORFU (*)

Feeder

34,654

2,556

2001

TC until Aug-26

$28,000

PEPI STAR (*)

Feeder

22,262

1,800

2024

TC until Jun-26

$24,250

MONICA (*)

Feeder

22,262

1,800

2024

TC until May-25

$16,000

STEPHANIA K (*)

Feeder

22,262

1,800

2024

TC until May-26

$22,000

EM SPETSES (*)

Feeder

23,224

1,740

2007

TC until Feb-26

$18,100

JONATHAN P (*)

Feeder

23,351

1,740

2006

TC until Sep-25

$20,000

EM HYDRA (*)

Feeder

23,351

1,740

2005

TC until Mar-25

$13,000

Total Container Carriers

22

849,398

67,494

Vessels under construction

Type

Dwt

TEU

To be delivered

ELENA (H1711)

Intermediate

55,200

4,300

Q4 2027

NIKITAS G (H1712)

Intermediate

55,200

4,300

Q4 2027

Total under construction

2

110,400

8,600

Notes: (*) TC denotes time charter. Charter duration indicates the earliest redelivery date; all dates listed are the earliest redelivery dates under each TC unless the contract rate is lower than the current market rate in which cases the latest redelivery date is assumed; vessels with the latest redelivery date shown are marked by (+).

The Euroholdings Ltd. fleet profile is as follows:

Name

Type

Dwt

TEU

Year Built

Employment(*)

TCE Rate ($/day)

Container Carriers

JOANNA(**)

Feeder

22,301

1,732

1999

TC until Mar-26, then until Sep-26, then until Nov-26

$19,000 $9,500 $16,500

AEGEAN EXPRESS

Feeder

18,581

1,439

1997

TC until Oct-25

$16,700

Total Container Carriers

2

40,882

3,171

Notes: (*) TC denotes time charter. Charter duration indicates the earliest redelivery date. (**) Period to Nov-2026 is at the option of the charterer.

About Euroseas Ltd.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA.

Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Following the completion of the spin-off of three of the Company’s subsidiaries into Euroholdings Ltd., Euroseas will have a fleet of 22 vessels, including 15 Feeder containerships and 7 Intermediate containerships. Euroseas 22 containerships will have a cargo capacity of 67,494 teu. After the delivery of the two intermediate containership newbuildings in 2027, Euroseas’ fleet will consist of 24 vessels with a total carrying capacity of 76,094 teu.

Forward Looking Statement

This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for containerships, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

Key Points: – The major port strike on the U.S. Atlantic and Gulf coasts has tentatively ended after dock workers agreed to a 62% pay raise over six years. – The current contract has been extended through January 15, 2025, allowing time for further negotiations, particularly over unresolved issues like the use of automated machinery. – The brief strike disrupted supply chains, with billions of dollars of goods stranded offshore, but the immediate threat to inflation and layoffs has been averted with the resumption of port operations.

The major port strike that disrupted shipping operations along the U.S. Atlantic and Gulf coasts this week has come to a tentative resolution. Workers represented by the International Longshoremen’s Association (ILA) reached a tentative agreement on wages and a contract extension, temporarily halting the strike that had begun early Tuesday morning.

Tentative Deal Reached After Intense Negotiations

Under the tentative agreement, dock workers would receive a 62% pay raise over six years. The union had originally pushed for a 77% wage increase, while the shipping industry group initially offered 50%. Yesterday’s offer came after pressure from the Biden administration to raise wages and expedite a resolution.

The agreement extends the current contract until January 15, 2025, providing time for both sides to negotiate the new long-term contract. The strike had raised significant concerns over the supply of essential goods like fruits and automobiles and threatened to exacerbate inflation if prolonged.

Immediate Return to Work

The ILA and USMX issued a joint statement on Thursday evening, confirming that all job actions would cease immediately, and work covered under the Master Contract would resume. Despite the wage deal, some major issues remain unresolved, particularly around the use of automated machinery, a sticking point that will feature prominently in upcoming negotiations.

Economic Impact and Supply Chain Disruptions

This week’s brief strike marked the first time the ILA had walked out since 1977. The impact of the strike was already being felt across industries, with thousands of shipping containers diverted to incorrect ports and billions of dollars’ worth of goods left stranded offshore. A longer strike could have increased inflationary pressures on consumer goods and triggered layoffs due to supply chain disruptions. However, with operations resuming, the immediate threat to supply chains has been averted, and attention now shifts to the longer-term contract negotiations that will determine the future of port labor relations.

Key Points: – Dockworkers strike over pay and automation concerns, signaling rising labor tensions over technology. – Labor unions across various industries are pushing back against job displacement due to automation. – Experts predict the effects of automation will soon impact all sectors, not just manual labor jobs.

The ongoing dockworkers’ strike over demands for higher wages and a ban on automation marks the latest battle in the growing resistance to technology in the workplace. As automation and artificial intelligence (AI) continue to reshape industries, labor unions across the U.S. are beginning to take a stand, seeking to control how these advancements impact their livelihoods. Rather than allowing employers to dictate the changes, workers are pushing for a more equitable approach to technological progress, one that balances innovation with job security.

The dockworkers’ strike is part of a broader trend that has seen unions across various industries, from Hollywood writers to auto workers, rally against automation and AI’s encroachment on their jobs. In recent months, employees have walked off the job, demanding fairer working conditions and stronger protections against the displacement caused by these emerging technologies. These collective actions are not just about wages; they represent a broader anxiety about the future of work in an increasingly automated world.

“These labor movements are connected by a common thread of resistance to technology and automation,” says Alexander Hertel-Fernandez, an associate professor at Columbia University. “As unions begin to succeed in one sector, it builds momentum and encourages workers in other fields to push back as well.”

One of the primary concerns of the dockworkers is that automation could lead to massive job losses. The shipping industry, which traditionally relies heavily on human labor, is now seeing advancements in robotics and AI that threaten to replace workers with machines. If automation is fully implemented in ports, it could transform an industry once dominated by human labor into one driven by robotics. This shift raises fears about the future of jobs in the sector and the potential consequences for workers who may find themselves obsolete.

The effects of a prolonged strike are already being felt, with delays in cargo shipments, higher prices, and supply chain disruptions on the horizon. Critics of the strike argue that resisting automation is akin to fighting the tide of progress. However, labor advocates counter that the conversation should be less about resisting technology and more about ensuring that workers are not left behind in the process.

“We need to strike a balance between advancing technology and protecting workers’ livelihoods,” says Darrell West, a senior fellow at the Brookings Institution. West suggests that retraining programs for displaced workers could offer a potential solution. “Mandating retraining programs for employees affected by automation could allow them to transition into other roles within the company or industry, rather than simply being pushed out.”

While automation may currently be impacting sectors like shipping and manufacturing, its reach is expanding. West warns, “Eventually, this will happen across all industries.” Whether it’s manual labor or white-collar jobs, no one is immune from the disruptions caused by technological advancements. What we see with the dockworkers today could set a precedent for how other sectors respond when automation begins to threaten their jobs.

Ultimately, the dockworkers’ strike is not just about protecting jobs in the shipping industry—it’s about establishing a framework for how society handles the rapid rise of technology. The decisions made in this strike could shape the future of work for employees across various industries, many of whom are also at risk of displacement by automation.