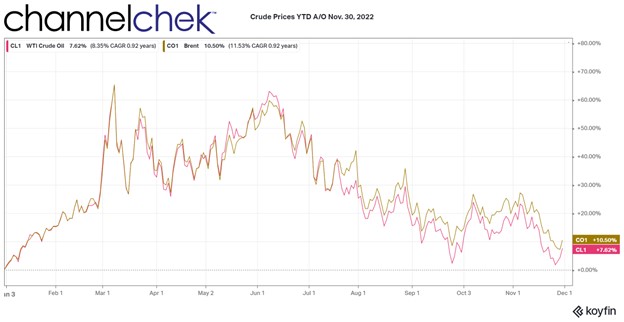

Will Russia Make the EU an Acceptable Counter Offer?

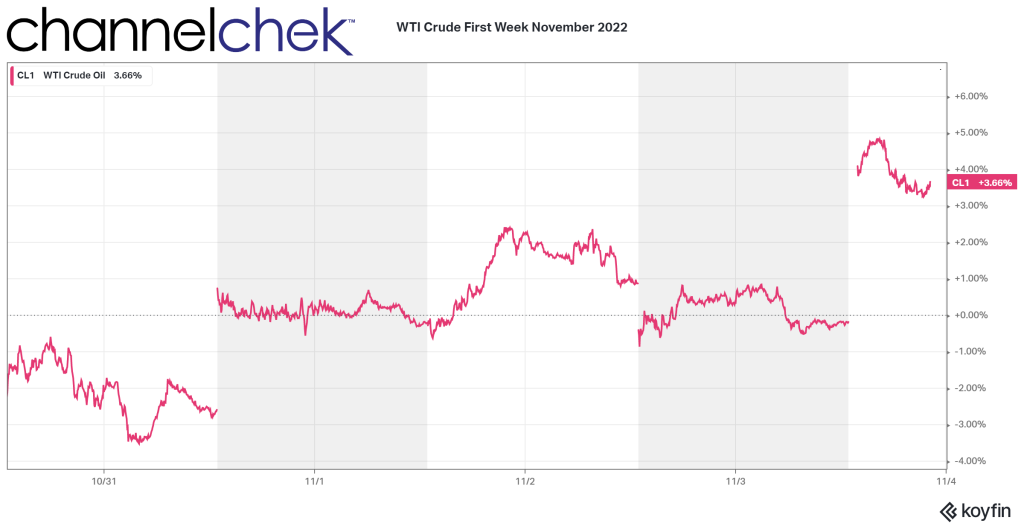

On Sunday, OPEC+ voted to maintain the previous level of output. This is known in OPEC vernacular as a “rollover,” it will allow the group time to experience and assess the market impact of the price cap of $60 a barrel on Russian oil. The $60 EU price cap is scheduled to begin Monday, December 5th.

Otherwise, it will be a quiet week in terms of data and Fed governor speeches. After a flurry of talks out of Fed executives last week, mostly pointing to a tapering of increases, the Fed is now in a blackout period until after the December 13-14 meeting and announcement.

Monday 12/5

- 9:45 AM ET, PMI Composite Final Consensus Outlook A little less contraction is the call for the PMI Service’s November final, at a consensus of 46.3 versus 46.1 at mid-month.

- 10:00 AM ET, Factory Orders are seen rising to a 0.7 percent gain in October. This would follow a 0.4 percent gain in September. The upward adjustment is in part due to Durable Goods orders for October, which have already been released and are one of two major components of this report. Durable Goods rose 1.0 percent in the month, which was stronger than expected. Factory Orders are a true leading indicator of future economic activity.

- 10:00 AM ET, ISM Services Industries has been slow, having reported 54.4 in October and expectations of 53.5 for November.

Tuesday 12/6

- 8:30 AM ET, International Trade in Goods and Services, a deficit of $80.0 billion is expected in October for total goods and services, which would compare with a $73.3 billion deficit in September. Advance data on the goods side of October’s report showed a more than $7 billion deepening in the deficit.

Wednesday 12/7

- 7:00 AM ET, MBA Mortgage Applications are expected to show that the composite index down 0.8%, the purchase index has gained 3.8%, and the refinance index is down 12.9%. The MBA compiles various mortgage loan indexes. The purchase applications index measures applications at mortgage lenders. This is a leading indicator for single-family home sales and housing construction, along with related industries that are impacted by a changing housing market.

- 8:30 AM ET, Productivity and Costs for third-quarter are expected to show non-farm productivity rising 0.4 percent versus a scant 0.3 percent annualized gain in the first estimate. Unit labor costs, which slowed from 8.9 percent in the second quarter to 3.5 percent in the first estimate for the third quarter, are expected to rise at a 3.3 percent rate in the second estimate.

- 10:30 AM ET, EIA Petroleum Status report. The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products.

- 3:00 PM ET Consumer credit is expected to increase $27.3 billion in October versus a $25.0 billion increase in September. Changes in consumer credit indicate the state of consumer finances and signal future spending patterns. The report includes credit cards, vehicle loans, and student loans; mortgages are not included.

- Productivity measures the growth of labor efficiency in producing the economy’s goods and services. Unit labor costs reflect the labor costs of producing each unit of output. Both are followed as indicators of future inflationary trends

Thursday 12/8

- 8:30 AM ET, Jobless Claims for the December 3 week are expected to come in at a 228,000 four-week moving average, versus 225,000 in the prior week. Employment is one of the Fed’s mandates; as such, any number that significantly varies from consensus could alter the market’s thinking.

- 10:00 AM ET, ISM Manufacturing Index was 50.2 in October; the ISM Manufacturing Index has been gradually slowing to nearly breakeven. November’s consensus is 49.9.

- 10:00 AM ET, Construction spending is expected to fall 0.2 percent in October. This would be dramatic relative to September’s modest 0.2 percent gain.

- 10:30 AM ET, The Energy Information Administration (EIA) provides weekly information on natural gas stocks in underground storage for the U.S. and five regions of the country. The level of inventories helps determine prices for natural gas products.

- 4:30 PM ET, The Fed’s balance sheet is a weekly report presenting a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. The report is officially named Factors Affecting Reserve Balances, otherwise known as the “H.4.1” report; investors have taken a recent interest in this weekly report as it shows if the Fed is on track with quantitative tightening plans.

Friday 12/9

- 8:30 AM ET, Producer Price Index or PPI, after moderating in October, PPI is expected to rise 0.2 percent on the month in November and 7.2 percent on the year. These would compare with 0.2 and 8.0 percent in October, which were both lower than expected. When excluding food and energy, prices are expected to also rise 0.2 percent on the month and 5.9 percent on the year.

- 10:00 AM ET, Consumer Sentiment is expected to remain unchanged at 56.8 after a rebound in November’s final report.

- 10:00 AM ET, Wholesale Inventories (second estimate for October) is expected to be unchanged from the first estimate at 0.8%.

What Else

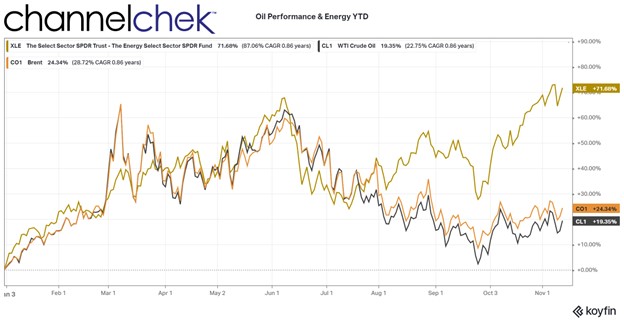

The focus until mid-month is likely to be how interest rate markets trade with a new sense that the Fed is slowing its tightening pace. Also in high focus this week, markets are expected to pay attention to how oil prices play out with the EU plan and perhaps a forthcoming Russian proposal.

Sources