U.S. oil production is approaching a turning point, according to Diamondback Energy CEO Travis Stice. In a letter to shareholders this week, Stice warned that domestic output has likely peaked and will begin to decline in the coming months, citing falling crude prices and slowing industry activity as key factors.

“U.S. onshore oil production has likely peaked and will begin to decline this quarter,” Stice wrote. “We are at a tipping point for U.S. oil production at current commodity prices.”

The warning comes as U.S. crude prices have dropped roughly 17% this year, weighed down by fears of a global economic slowdown tied to President Donald Trump’s renewed tariffs and an aggressive supply push from OPEC+ producers. Prices for West Texas Intermediate (WTI) crude briefly surged 4% on Tuesday to $59.56 per barrel amid expectations that U.S. supply will tighten.

Stice emphasized that adjusted for inflation, oil is now cheaper than it has been in nearly every quarter since 2004—excluding the pandemic collapse in 2020. That pricing reality, he said, is forcing producers to slash spending and slow operations, threatening broader economic impacts.

Diamondback, a major producer in the Permian Basin and one of the largest independent oil companies in the U.S., has already reduced its capital spending by $400 million for the year. The company now plans to drill between 385 to 435 wells and complete 475 to 550, while maintaining reduced rig and crew levels.

“We’ve dropped three rigs and one completion crew, and expect to stay at those levels for most of Q3,” Stice said.

The U.S. shale boom of the last 15 years helped make the country the world’s top fossil fuel producer, outpacing even Saudi Arabia and Russia. That shift reshaped the U.S. economy, reduced reliance on foreign energy, and strengthened national security. But Stice now warns that this progress is at risk.

“Today’s prices, volatility and macroeconomic uncertainty have put this progress in jeopardy,” he said.

Fracking activity is already falling sharply. The number of completion crews is down 15% nationwide and 20% in the Permian Basin since January, Stice said. Oil-directed drilling rigs are expected to drop nearly 10% by the end of Q2, with further declines projected in the third quarter.

Adding to the pressure are rising costs tied to tariffs. Stice said Trump’s steel tariffs have added around $40 million annually to Diamondback’s expenses, raising well costs by about 1%. While some of this impact may be offset by operational efficiencies, the CEO warned that sustaining current output levels at lower prices may no longer be financially viable.

Stice likened the situation to approaching a red light while driving: “We are taking our foot off the accelerator. If the light turns green, we’ll hit the gas again—but we’re prepared to brake if needed.”

As the U.S. energy sector confronts an increasingly uncertain landscape, the prospect of declining domestic production is no longer just a possibility—it’s becoming a reality.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full-year 2024 financial results. Hemisphere Energy reported full-year net income and earnings per share of C$33.1 million and C$0.33, respectively, slightly above our estimates of C$32.3 million and C$0.32. The variance is mainly due to stronger oil pricing of $79.48, compared to our estimate of $76.31. Year-over-year, oil and natural gas revenue increased ~18% to C$79.7 million from C$67.7 million. This increase was driven by increased production and more robust pricing of 3,436 barrels of oil equivalent per day (boe/d) and $79.48, respectively, compared to 3,125 boe/d and $74.07. Likewise, adjusted funds flow (AFF) increased 16% in 2024 to C$45.8 million from C$39.4 million in 2023. We had forecast AFF of C$45.4 million.

Updating estimates. Based on lower crude oil price estimates, we are lowering our 2025 net income and earnings per share estimates to C$30.3 million and C$0.29, respectively, from C$37.2 million and C$0.37. Additionally, we are decreasing our adjusted funds flow estimate to C$42.9 million from C$50.6 million. We are maintaining our 2025 average daily production estimate of 3,900 boe/d, an increase of ~14% over 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – April 3, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that its board of directors has approved the declaration of a special dividend to shareholders.

Special Dividend

Given the strong financial position and performance outlook of the Company, Hemisphere’s board of directors has approved the declaration of a special dividend of C$0.03 per common share, in accordance with its dividend policy. The special dividend will be paid on April 28, 2025, to shareholders of record on April 17, 2025, and is designated as an eligible dividend for Canadian income tax purposes. It is in addition to the Company’s quarterly base dividend of C$0.025 per common share.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood EOR methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation, or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a special dividend will be paid to shareholders on April 28, 2025, to shareholders of record on April 17, 2025.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the timing for payment of the special dividend; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in project timelines and workstreams; changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Oil prices took a dramatic hit on Thursday, tumbling over 7% as panic selling gripped financial markets. The sharp decline followed former President Donald Trump’s announcement of sweeping new tariffs and an unexpected supply increase from OPEC+, both of which fueled uncertainty about global demand and market stability.

By mid-morning, West Texas Intermediate (WTI) crude oil (CL=F), the U.S. benchmark, had fallen 7.5% to around $66.10 per barrel, while Brent crude (BZ=F), the global benchmark, dropped below $70 per barrel. This marked one of the largest single-day declines in recent months and signaled a potential shift in market sentiment.

The steep decline was largely driven by fear and uncertainty rather than immediate changes in supply and demand fundamentals, according to market analysts.

“Current discussions about an expected increase in oil production by the OPEC+ and uncertainties about the real impact of the recently announced tariffs are creating downward pressure on oil prices,” said Francisco Penafiel, managing director of investment banking at Noble Capital Markets. “We feel this volatility will continue at least in the near term, until we start measuring the effects from the tariffs and favorable oil market fundamentals prevail over fears of a global economic downturn affecting global demand.”

“The panic selling that’s occurring is very likely an over-exaggeration of the true fundamentals,” said Dennis Kissler, senior vice president for trading at BOK Financial Securities. “Near term, however, there’s a lot of unknowns, so you’re seeing a lot of funds unwind positions.”

Investors had been bullish on oil prices in recent weeks, expecting geopolitical tensions and supply constraints to keep the market tight. However, the combination of Trump’s aggressive trade policies and OPEC+’s decision to boost production has introduced fresh concerns about oversupply and weaker global demand.

Adding to the selloff, the Organization of Petroleum Exporting Countries (OPEC) and its allies, known as OPEC+, announced they would increase oil production by 411,000 barrels per day starting in May.

While markets had anticipated some additional supply, the move was larger than expected, deepening losses in crude prices.

With global supply now expected to rise and demand potentially slowing due to economic uncertainty, traders are recalibrating their outlooks for oil prices heading into the second half of 2025.

Trump’s new tariff policies have raised concerns about the broader impact on economic growth. While energy imports were not specifically targeted in the latest round of tariffs, the indirect effects could be significant.

China, the world’s largest crude importer, now faces a 54% tariff on U.S. goods. If the Chinese economy slows as a result, its demand for oil could weaken, further pressuring global crude markets.

Before Thursday’s selloff, oil prices had been rising due to Trump’s pressure on Iran, Venezuela, and Russia to curb their oil exports. This rally had already driven U.S. gas prices to their highest levels since September, with the national average nearing $3.25 per gallon.

With oil prices now plunging, the outlook remains uncertain. If crude prices continue to fall, gas prices could stabilize or even decline. However, if global trade tensions persist and economic growth slows, oil demand could remain under pressure in the months ahead.

For now, investors are bracing for more volatility as geopolitical risks and market uncertainty take center stage.

Key Points: – Oil prices remain vulnerable to the global trade war, impacting Gulf economies dependent on crude exports. – Currency pegs to the U.S. dollar pose challenges, particularly for countries with high external debt. – New trade corridors, particularly between the Gulf and Asia, offer potential opportunities amid shifting global supply chains.

The Middle East has largely avoided direct tariffs in the ongoing global trade war, but its economies remain vulnerable to broader economic shifts. With oil demand at risk, currency pressures mounting, and global trade flows changing, the region must navigate an increasingly uncertain landscape while also seizing new opportunities.

One of the most immediate concerns for the Middle East is oil. While a weaker U.S. dollar initially benefits oil-exporting nations by making crude cheaper for foreign buyers, tariffs and economic slowdowns could lead to lower global demand. Brent crude prices remain sensitive to global trade conditions, and a prolonged trade war could weigh on revenues for major producers like Saudi Arabia and the UAE. Despite efforts to diversify their economies, oil remains the backbone of many Gulf nations, making them particularly exposed to shifts in global demand.

Another challenge comes from currency pegs. Several Gulf states, including Saudi Arabia, the UAE, Qatar, Oman, and Bahrain, have their currencies tied to the U.S. dollar. As the dollar fluctuates in response to tariffs and economic policies, these countries face higher import costs. This could lead to inflationary pressures, especially in economies heavily reliant on imported goods. At the same time, countries with significant external debt, such as Lebanon, Jordan, and Egypt, could struggle with higher debt-servicing costs if the dollar strengthens further.

Trade tensions also pose risks to regional trade hubs like the UAE, which depend on global trade flows. As a logistics and financial center, Dubai has built its economy around international commerce, meaning a prolonged global slowdown could impact its growth. Economists warn that while Gulf economies have taken steps to diversify, the effects of reduced trade volumes could still be felt.

However, the situation is not entirely negative. The trade war has also encouraged the creation of new trade corridors, particularly between the Gulf and Asia. The GCC-Asia trade relationship has seen sustained growth, with increasing investment and business ties. China’s Belt and Road Initiative has already deepened economic connections, and as global supply chains shift, Middle Eastern economies could benefit from a larger role in these emerging trade networks.

Political factors could also play a role in shaping the region’s economic resilience. U.S. President Donald Trump has maintained strong ties with Gulf nations, particularly Saudi Arabia, and has shown an interest in keeping them aligned with U.S. economic and geopolitical priorities. This relationship may provide some buffer against trade war fallout, as evidenced by Jordan’s ability to secure exemptions from certain U.S. tariffs due to its strategic importance.

Looking ahead, Middle Eastern economies must continue to adapt to changing global conditions. Strengthening domestic demand, securing diversified trade partnerships, and managing currency risks will be key strategies for mitigating potential downturns. While challenges remain, opportunities exist for the region to carve out a more influential role in global trade as supply chains and economic alliances shift.

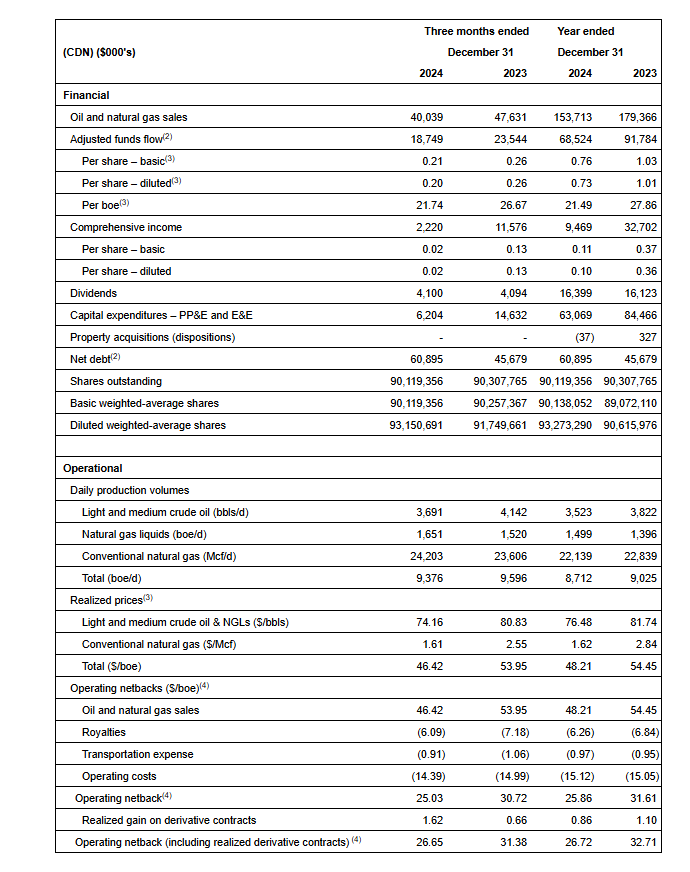

CALGARY, AB, March 14, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce its financial and operating results for the three and twelve months ended December 31, 2024, along with the results of its independent oil and gas reserves evaluation effective December 31, 2024 (the “Reserve Report”) prepared by Sproule Associates Limited (“Sproule”). InPlay’s audited annual financial statements and notes, and Management’s Discussion and Analysis (“MD&A”) for the year ended December 31, 2024 will be available at “www.sedarplus.ca” and the Company’s website at “www.inplayoil.com“. An updated presentation will be available after closing of the Pembina Cardium asset acquisition which is expected in April.

Message to Shareholders:

The upcoming year is set to be a transformational year for InPlay. We believe that the highly accretive acquisition of Pembina Cardium assets from Obsidian Energy Ltd. announced on February 19, 2025 will fundamentally shift the future of the Company. The acquired assets strategically complement InPlay’s existing holdings in the Pembina Cardium, an area where the Company has proven operational expertise. The acquisition will significantly expand our operational scale, with attributes including large oil in place, a higher oil weighting, strong netbacks, low decline rates and a robust inventory of high-quality drilling locations, enhancing our overall sustainability. This is expected to strengthen free adjusted funds flow (“FAFF”)(4) generation, allowing for debt reduction while supporting our shareholder return strategy, with over three times FAFF coverage of our existing base dividend (11.3%) expected for 2025. We are excited to begin operations of these newly acquired assets acquired in this synergistic acquisition and to demonstrate our expertise and ability to unlock the intrinsic value of our share price. We will remain committed to financial discipline maintaining our strong balance sheet, to ultimately generate shareholder value through FAFF growth and return of capital to shareholders.

The resumption of development of our Pembina Cardium Unit # (“PCU7”) asset was a key highlight in 2024. This area is our most prolific asset as it offers high production rates and lower declines. As a result of significantly improved capital costs, PCU7 yields the highest returns and strongest capital efficiencies in our current asset portfolio. Our 2024 development of PCU7 exceeded internal expectations. Operational enhancements since our last PCU7 drilling program in spring of 2022 resulted in costs 25% below budget. These new techniques can be leveraged across our Cardium asset base, including those acquired as part of the Pembina Cardium asset acquisition. Three additional 100% PCU7 extended reach horizontal (“ERH”) wells were drilled in the first quarter of 2025 and recently brought on production.

During 2024, InPlay remained focused on operational execution, disciplined capital allocation and prioritizing FAFF while preserving a strong balance sheet which resulted in adjusting our operational and capital activities accordingly. InPlay’s disciplined approach allowed the Company to capitalize on the transformational Pembina Cardium asset acquisition.

Following closing of the Pembina Cardium asset acquisition, InPlay will provide updated development plans and revised full-year 2025 guidance. The acquisition is currently expected to close in April 2025.

2024 was a year of disciplined execution, operational efficiency, and delivering shareholder returns. We remain focused on financial strength, sustainable production, and value creation for our shareholders. As we move into 2025, we believe the Pembina Cardium asset acquisition positions InPlay for significant growth and long-term success. On behalf of our employees, management team and Board of Directors, we would like to thank our shareholders for their support.

2024 Financial and Operating Results:

Achieved average annual production of 8,712 boe/d(1) (58% light crude oil and NGLs) with fourth quarter production average of 9,376 boe/d(1) (57% light crude oil and NGLs).

Generated adjusted funds flow (“AFF”)(2) of $68.5 million ($0.76 per basic share(3)) despite a 44% drop in AECO natural gas prices compared to 2023.

Distributed $16.4 million in dividends, equating to a 10.4% yield relative to year-end market capitalization. Since November 2022, total dividends distributed amounted to $39.2 million ($0.435 per share, including dividends declared to date in 2025).

Invested $63 million in development capital which was $2.5 million below the mid-range of our $64 – $67 million budget and 25% less than 2023. The majority of capital was spent on our drilling program, consisting of 12 (11.9) operated horizontal wells and three (0.65 net) non-operated horizontal wells, including strategic infrastructure projects, and an extensive downhole optimization program. $5.4 million was spent on the optimization program to replace plunger lifts with downhole pumps and lowering pumps in horizontal wells, helping to decrease our base decline rate to 26%.

Materially enhanced capital efficiencies through a 25% reduction in drilling and completion costs experienced in PCU7 as a result of operational enhancements on our four H2 2024 wells drilled in the area.

Exited 2024 at 0.8x net debt to earnings before interest, taxes and depletion (“EBITDA”)(4) which is among the lowest among industry peers.

Generated a strong operating income profit margin(4) of 54% and net income of $9.5 million ($0.11 per basic share, $0.10 per diluted share).

Renewed our $110 million revolving Senior Credit Facility, providing significant liquidity for tactical capital investment and strategic acquisitions.

Allocated $3.4 million to the successful abandonment of 40 wellbores, 37 pipelines and the reclamation of 25 wellsites.

2024 Financial & Operations Overview:

Our 2024 results reflect our disciplined capital allocation approach to maintain financial strength while delivering strong returns to shareholders. We executed our capital program under budget, generated meaningful adjusted funds flow and returned $16.4 million to shareholders. Production averaged 9,376 boe/d(1) (57% light crude oil & NGLs) in the fourth quarter of 2024.

InPlay’s capital program for 2024 consisted of $63.1 million of exploration and development capital. Efficient operational execution in 2024 led to capital expenditures coming in $2.5 million below the mid-point of our $64 – $67 million budget and approximately 25% less than 2023. The Company drilled, completed and brought on production two (1.9 net) ERH wells in Willesden Green, two (2.0 net) one-mile horizontal wells in Willesden Green, three (3.0 net) ERH wells in Pembina, four (4.0 net) PCU7 ERH wells, one (1.0 net) Belly River well, and three (0.65 net) non-operated Willesden Green ERH wells during 2024. This activity amounted to the drilling of 15 (12.6 net) wells. Additionally, the Company incurred drilling costs on one (1.0 net) Glauconite well where drilling challenges resulted in casing failure and led to the termination of drilling operations. In addition, $5.4 million was spent on the optimization of wells during 2024 to change plunger lifts to downhole pumps and lowering pumps in horizontal wells which has led to improved base decline rates. Going forward, InPlay’s improved decline rate results in reduced drilling capital required to maintain production and further enhancing our ability to generate FAFF.

Natural gas prices remained low in 2024 due to production growth in North America with higher than normal inventory levels in North America and Europe. This resulted in a 44% decrease in AECO pricing compared to already low prices in 2023. These lower prices resulted in a 11% decline in our realized boe sales price, which was partially offset by realized hedging gains.

Financial and Operating Results:

Operations Update:

InPlay’s capital program for 2025 is underway with three (3.0 net) ERH wells drilled in PCU7 recently coming on production and are in the early cleanup stage. These wells will offset the three well pad drilled in 2024 which has exceeded internal expectations. Despite the extreme cold temperatures in February, the costs for our first three wells of 2025 came in on time and on budget. Building on the success of our 2024 PCU7 development, we are excited to continue the focused development of this highly prolific area with an additional three net wells planned for the second half of 2025 included in our pre-acquisition 2025 budget. The majority of our remaining 2025 pre-acquisition capital program was scheduled for the second half of the year with minimal spending planned in the second quarter resulting in strong forecasted FAFF.

On March 4, 2025 the government of the United Stated announced tariffs on goods imported from Canada, including a 10% tariff on Canadian energy imports. The situation continues to be fluid and we believe the volatility surrounding these tariffs is already impacting valuations in the energy industry. We continue to monitor the impact of these tariffs on the Company and will make decisions keeping our strategy of disciplined capital allocation, financial flexibility and returns to shareholders at the forefront. InPlay’s financial hedges and a resulting weaker Canadian dollar are expected to mitigate the impact of these tariffs on the Company.

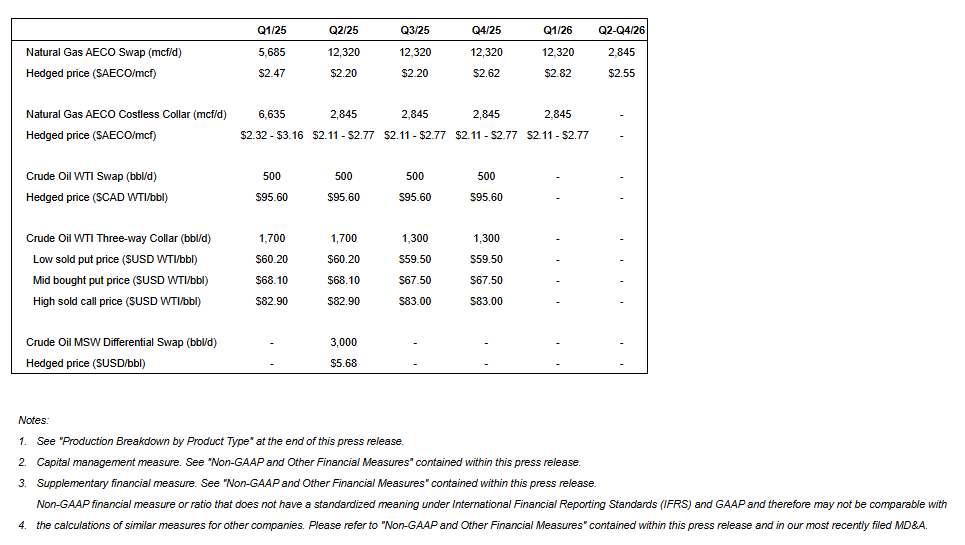

Hedging Update

The Company has reacted to commodity price volatility by securing commodity hedges extending through 2025 and into 2026. InPlay has hedged over 60% of pre-acquisition natural gas production and approximately 55% of pre-acquisition light crude oil production during 2025 at favorable pricing levels. Refer below for a summary of the Company’s commodity-based hedges.

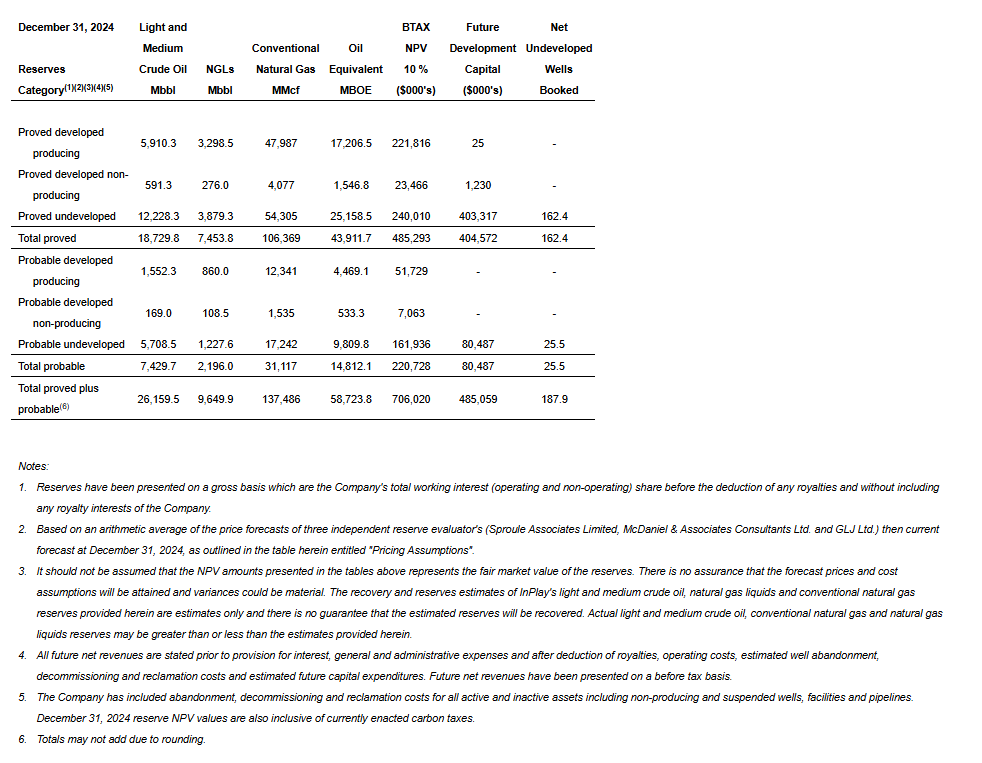

2024 Reserves Results(1):

An organic 2024 capital program without acquisition/disposition (“A&D”) activity resulted in:

Proved developed producing (“PDP”) reserves of 17,207 mboe (54% light and medium crude oil & NGLs)

Total proved (“TP”) reserves of 43,912 mboe (60% light and medium crude oil & NGLs)

Total proved plus probable (“TPP”) reserves of 58,724 mboe (61% light and medium crude oil & NGLs)

Reserves life index (“RLI”)(2) for PDP, TP and TPP of approximately 5.4 years, 13.8 years and 18.5 years, respectively highlights a sizable drilling inventory for long-term development potential.

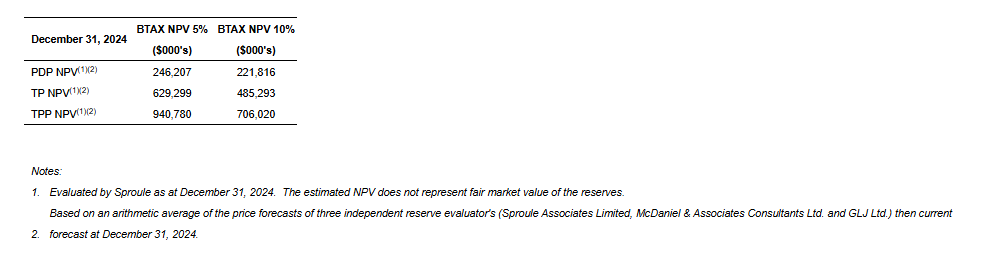

Achieved NPV BT10 reserve values(1) of:

PDP: $222 million

TP: $485 million

TPP: $706 million

Corporate Reserves Information:

The following summarizes certain information contained in the Reserve Report. The Reserve Report was prepared in accordance with the definitions, standards and procedures contained in the COGE Handbook and National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Additional reserve information as required under NI 51-101 will be included in the Company’s Annual Information Form (“AIF”) which will be filed on SEDAR+ by the end of March 2025.

Net Present Values of Reserves:

InPlay achieved strong before tax estimated net present values (“NPV”) of future net revenues associated with our 2024 year-end reserves discounted at 10% (“NPV BT10”), although impacted by weaker future commodity prices in comparison to December 31, 2023. Forecasted WTI and AECO prices used in the Reserve Report decreased by 5% and 30% in year one and 2% and 18% in year two, respectively, compared to 2023. The Company achieved NPV BT10 reserve values of $222 million (PDP), $485 million (TP) and $706 million (TPP) based on the three independent reserve evaluator average pricing, cost forecast and foreign exchange rates as at December 31, 2024 used in the Reserve Report.

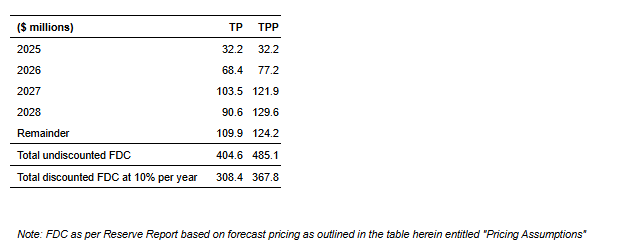

Future Development Costs (“FDCs”):

The following FDCs are included in the 2024 Reserve Report:

The $485 million of total FDC in the Reserve Report generates approximately $484 million in future net present value discounted at 10%.

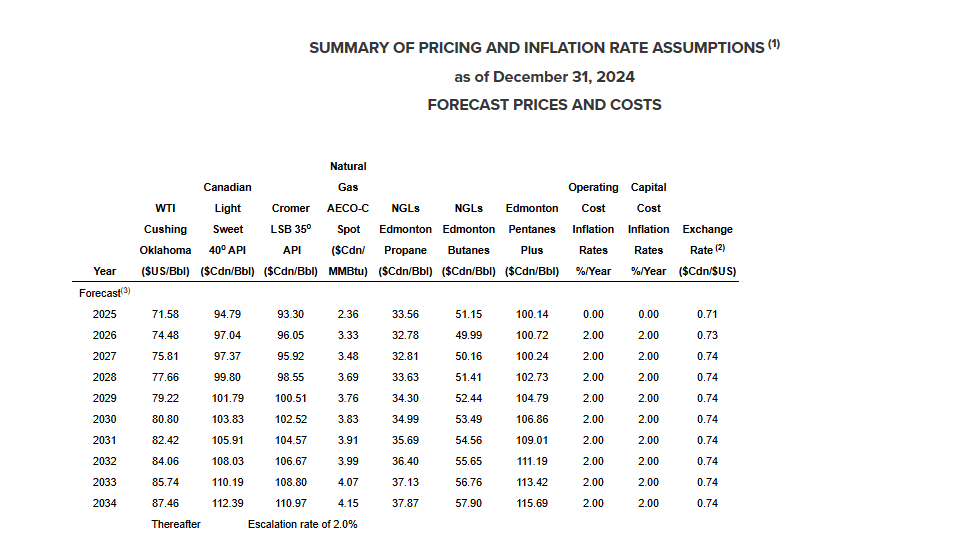

Pricing Assumptions:

The following tables set forth the benchmark reference prices, as at December 31, 2024, reflected in the Reserve Report. These price and cost assumptions were an arithmetic average of the price forecasts of three independent reserve evaluator’s (Sproule, McDaniel & Associates Consultants Ltd. and GLJ Ltd.) then current forecast and Sproule’s foreign exchange rate forecast at the effective date of the Reserve Report.

Forecasted WTI and AECO prices used in the Reserve Report decreased by 5% and 30% in year one and 2% and 18% in year two respectively compared to 2023.

InPlay also confirms that the management information circular (the “Circular”) and form of proxy with respect to the proposed Pembina Cardium asset acquisition and related matters have been mailed to the InPlay shareholders of record as of February 28, 2025. InPlay confirms that the Circular and form of proxy can be accessed and viewed on the Company’s website (www.inplayoil.com) or on the Company’s profile on SEDAR+ (www.sedarplus.ca).

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Throughout this document and other materials disclosed by the Company, InPlay uses certain measures to analyze financial performance, financial position and cash flow. These non-GAAP and other financial measures do not have any standardized meaning prescribed under GAAP and therefore may not be comparable to similar measures presented by other entities. The non-GAAP and other financial measures should not be considered alternatives to, or more meaningful than, financial measures that are determined in accordance with GAAP as indicators of the Company performance. Management believes that the presentation of these non-GAAP and other financial measures provides useful information to shareholders and investors in understanding and evaluating the Company’s ongoing operating performance, and the measures provide increased transparency and the ability to better analyze InPlay’s business performance against prior periods on a comparable basis.

Non-GAAP Financial Measures and Ratios

Included in this document are references to the terms “free adjusted funds flow”, “operating income”, “operating netback per boe”, “operating income profit margin” and “Net Debt to EBITDA”. Management believes these measures and ratios are helpful supplementary measures of financial and operating performance and provide users with similar, but potentially not comparable, information that is commonly used by other oil and natural gas companies. These terms do not have any standardized meaning prescribed by GAAP and should not be considered an alternative to, or more meaningful than “profit before taxes”, “profit and comprehensive income”, “adjusted funds flow”, “capital expenditures”, “net debt” or assets and liabilities as determined in accordance with GAAP as a measure of the Company’s performance and financial position.

Free Adjusted Funds Flow/FAFF per share

Management considers FAFF and FAFF per share important measures to identify the Company’s ability to improve its financial condition through debt repayment and its ability to provide returns to shareholders. FAFF should not be considered as an alternative to or more meaningful than AFF as determined in accordance with GAAP as an indicator of the Company’s performance. FAFF is calculated by the Company as AFF less exploration and development capital expenditures and property dispositions (acquisitions) and is a measure of the cashflow remaining after capital expenditures before corporate acquisitions that can be used for additional capital activity, corporate acquisitions, repayment of debt or decommissioning expenditures or potentially return of capital to shareholders. FAFF per share is calculated by the Company as FAFF divided by weighted average shares outstanding. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast FAFF.

Free Adjusted Funds Flow Yield

InPlay uses “free adjusted funds flow yield” as a key performance indicator. When presented on a corporate basis, free adjusted funds flow is calculated by the Company as free adjusted funds flow divided by the market capitalization of the Company. When presented on an asset basis for acquisition purposes, free adjusted funds flow is calculated by the Company as free adjusted funds flow divided by the operating income of the Acquired Assets. Management considers FAFF yield to be an important performance indicator as it demonstrates a Company or asset’s ability to generate cash to pay down debt and provide funds for potential distributions to shareholders. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast FAFF Yield.

Operating Income/Operating Netback per boe/Operating Income Profit Margin

InPlay uses “operating income”, “operating netback per boe” and “operating income profit margin” as key performance indicators. Operating income is calculated by the Company as oil and natural gas sales less royalties, operating expenses and transportation expenses and is a measure of the profitability of operations before administrative, share-based compensation, financing and other non-cash items. Management considers operating income an important measure to evaluate its operational performance as it demonstrates its field level profitability. Operating income should not be considered as an alternative to or more meaningful than net income as determined in accordance with GAAP as an indicator of the Company’s performance. Operating netback per boe is calculated by the Company as operating income divided by average production for the respective period. Management considers operating netback per boe an important measure to evaluate its operational performance as it demonstrates its field level profitability per unit of production. Operating income profit margin is calculated by the Company as operating income as a percentage of oil and natural gas sales. Management considers operating income profit margin an important measure to evaluate its operational performance as it demonstrates how efficiently the Company generates field level profits from its sales revenue. Refer below for a calculation of operating income, operating netback per boe and operating income profit margin. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast operating income, operating netback per boe and operating income profit margin.

(thousands of dollars)

Three Months EndedDecember 31

Year EndedDecember 31

2024

2023

2024

2023

Revenue

40,039

47,631

153,713

179,366

Royalties

(5,253)

(6,339)

(19,964)

(22,516)

Operating expenses

(12,413)

(13,233)

(48,198)

(49,576)

Transportation expenses

(786)

(940)

(3,083)

(3,130)

Operating income

21,587

27,119

82,468

104,144

Sales volume (Mboe)

862.6

882.8

3,188.5

3,294.1

Per boe

Revenue

46.42

53.95

48.21

54.45

Royalties

(6.09)

(7.18)

(6.26)

(6.84)

Operating expenses

(14.39)

(14.99)

(15.12)

(15.05)

Transportation expenses

(0.91)

(1.06)

(0.97)

(0.95)

Operating netback per boe

25.03

30.72

25.86

31.61

Operating income profit margin

54 %

57 %

54 %

58 %

Net Debt to EBITDA

Management considers Net Debt to EBITDA an important measure as it is a key metric to identify the Company’s ability to fund financing expenses, net debt reductions and other obligations. EBITDA is calculated by the Company as adjusted funds flow before interest expense. When this measure is presented quarterly, EBITDA is annualized by multiplying by four. When this measure is presented on a trailing twelve month basis, EBITDA for the twelve months preceding the net debt date is used in the calculation. This measure is consistent with the EBITDA formula prescribed under the Company’s Senior Credit Facility. Net Debt to EBITDA is calculated as Net Debt divided by EBITDA. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast Net Debt to EBITDA.

Capital Management Measures

Adjusted Funds Flow

Management considers adjusted funds flow to be an important measure of InPlay’s ability to generate the funds necessary to finance capital expenditures. Adjusted funds flow is a GAAP measure and is disclosed in the notes to the Company’s financial statements for the year ended December 31, 2024. All references to adjusted funds flow throughout this document are calculated as funds flow adjusting for decommissioning expenditures. Decommissioning expenditures are adjusted from funds flow as they are incurred on a discretionary and irregular basis and are primarily incurred on previous operating assets. The Company also presents adjusted funds flow per share whereby per share amounts are calculated using weighted average shares outstanding consistent with the calculation of profit per common share.

Net Debt

Net debt is a GAAP measure and is disclosed in the notes to the Company’s financial statements for the year ended December 31, 2024. The Company closely monitors its capital structure with the goal of maintaining a strong balance sheet to fund the future growth of the Company. The Company monitors net debt as part of its capital structure. The Company uses net debt (bank debt plus accounts payable and accrued liabilities less accounts receivables and accrued receivables, prepaid expenses and deposits and inventory) as an alternative measure of outstanding debt. Management considers net debt an important measure to assist in assessing the liquidity of the Company.

Free Funds Flow

Management considers free funds flow to be an important measure of InPlay’s ability to generate the funds necessary after capital expenditures and decommissioning expenditures to improve its financial condition through debt repayment and its ability to provide returns to shareholders. Free funds flow is comprised of GAAP measures disclosed in the notes to the Company’s financial statements for the year ended December 31, 2024. All references to free funds flow throughout this document are calculated as funds flow less exploration and development capital expenditures and property dispositions (acquisitions).

Supplementary Measures

“Average realized crude oil price” is comprised of crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil volumes. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized NGL price” is comprised of NGL commodity sales from production, as determined in accordance with IFRS, divided by the Company’s NGL volumes. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas volumes. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized commodity price” is comprised of commodity sales from production, as determined in accordance with IFRS, divided by the Company’s volumes. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Adjusted funds flow per weighted average basic share” is comprised of adjusted funds flow divided by the basic weighted average common shares.

“Adjusted funds flow per weighted average diluted share” is comprised of adjusted funds flow divided by the diluted weighted average common shares.

“Adjusted funds flow per boe” is comprised of adjusted funds flow divided by total production.

Forward-Looking Information and Statements

This document contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this document contains forward-looking information and statements pertaining to the following: the Company’s business strategy, milestones and objectives; the Company’s expectation that an updated presentation will be available after closing of the Pembina Cardium asset acquisition and the timing of such closing; the Company’s belief that the upcoming year will be transformational for InPlay; the Company’s beliefs and expectations regarding the Pembina Cardium asset acquisition, including that it will fundamentally shift the future of the Company, expand the Company’s operational scale, enhance the Company’s overall sustainability, and strengthen FAFF generation, enabling debt reduction and supporting the Company’s shareholder return strategy; the Company’s belief that the acquired assets will strategically complement InPlay’s existing holdings in the Pembina Cardium; the Company’s expectations regarding its expertise and ability to unlock the intrinsic value of its share price; the Company’s belief that it will remain committed to financial discipline maintaining its strong balance sheet, to ultimately generate shareholder value through FAFF growth and return of capital to shareholders; the Company’s belief that the operational enhancements to the drilling PCU7 program can be leveraged to the Company’s other Cardium assets, including those acquired as part of the Pembina Cardium asset acquisition; the Company’s expectation that it following closing of the Pembina Cardium asset acquisition, it will provide updated development plans and revised full-year 2025 guidance; expectations regarding the Company’s PCU7 asset; expectations regarding the Company’s 2025 capital program; the Company’s belief that it will monitor the impact of tariffs and will make decisions keeping the Company’s strategy of disciplined capital allocation, financial flexibility and returns to shareholders at the forefront; expectations regarding the Company’s hedges, including that its financial hedges and a resulting weaker Canadian dollar will mitigate the impact of tariffs on the Company; 2025 forecast production; 2025 guidance and 2025 pro-forma estimates related to the proposed Pembina asset acquisition based on the planned capital program and all associated underlying assumptions set forth in this document including, without limitation, forecasts of 2025 annual average production levels, adjusted funds flow, free adjusted funds flow, Net Debt/EBITDA ratio, operating income profit margin, net debt and Management’s belief that the Company can grow some or all of these attributes and specified measures; light crude oil and NGLs weighting estimates; expectations regarding future commodity prices; future oil and natural gas prices; future liquidity and financial capacity; future results from operations and operating metrics; future costs, expenses and royalty rates; future interest costs; the exchange rate between the $US and $Cdn; future development, exploration, acquisition, development and infrastructure activities and related capital expenditures, including InPlay’s planned 2025 capital program; the amount and timing of capital projects; and methods of funding our capital program.

The internal projections, expectations, or beliefs underlying our Board approved 2025 capital budget and associated guidance are subject to change in light of, among other factors, changes to U.S. economic, regulatory and/or trade policies (including tariffs), the impact of world events including the Russia/Ukraine conflict and war in the Middle East, ongoing results, prevailing economic circumstances, volatile commodity prices, and changes in industry conditions and regulations. InPlay’s 2025 financial outlook and revised guidance provides shareholders with relevant information on management’s expectations for results of operations, excluding any potential acquisitions or dispositions, for such time periods based upon the key assumptions outlined herein. Readers are cautioned that events or circumstances could cause capital plans and associated results to differ materially from those predicted and InPlay’s revised guidance for 2025 may not be appropriate for other purposes. Accordingly, undue reliance should not be placed on same.

Forward-looking statements or information are based on a number of material factors, expectations or assumptions of InPlay which have been used to develop such statements and information, but which may prove to be incorrect. Although InPlay believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because InPlay can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current U.S. economic, regulatory and/or trade policies; the impact of increasing competition; the general stability of the economic and political environment in which InPlay operates; the timely receipt of any required regulatory approvals; the ability of InPlay to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which InPlay has an interest in to operate the field in a safe, efficient and effective manner; the ability of InPlay to obtain debt financing on acceptable terms; the anticipated tax treatment of the monthly base dividend; that other than the tariffs that came into effect on March 4, 2025 (some of which were subsequently paused on March 6, 2025), neither the U.S. nor Canada (i) increases the rate or scope of such tariffs (if they come into effect in the future), or imposes new tariffs, on the import of goods from one country to the other, including on oil and natural gas, and/or (ii) imposes any other form of tax, restriction or prohibition on the import or export of products from one country to the other, including on oil and natural gas; the potential scope and duration of tariffs, export taxes, export restrictions or other trade actions; magnitude and duration of potential new or increased tariffs may be imposed on goods imported from Canada into the United States, which could adversely impact InPlay’s revenues; the potential for new and increased U.S. tariffs and protectionist trade measures on Canadian oil and gas imports; changes in political and economic conditions, including risks associated with tariffs, export taxes, export restrictions or other trade actions; impacts of any tariffs imposed on Canadian exports into the United States by the Trump administration and any retaliatory steps taken by the Canadian federal government; that InPlay’s results and operations could be adversely affected by economic or geopolitical developments, including protectionist trade policies such as tariffs, or other events; conditions in international markets, including social and political conditions, civil unrest, terrorist activity, governmental changes, restrictions on the ability to transfer capital across borders, tariffs and other protectionist measures; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and the ability of InPlay to secure adequate product transportation; future commodity prices; that various conditions to a shareholder return strategy can be satisfied; the ongoing impact of the Russia/Ukraine conflict and war in the Middle East; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which InPlay operates; and the ability of InPlay to successfully market its oil and natural gas products.

Without limitation of the foregoing, readers are cautioned that the Company’s future dividend payments to shareholders of the Company, if any, and the level thereof will be subject to the discretion of the Board of Directors of InPlay. The Company’s dividend policy and funds available for the payment of dividends, if any, from time to time, is dependent upon, among other things, levels of FAFF, leverage ratios, financial requirements for the Company’s operations and execution of its growth strategy, fluctuations in commodity prices and working capital, the timing and amount of capital expenditures, credit facility availability and limitations on distributions existing thereunder, and other factors beyond the Company’s control. Further, the ability of the Company to pay dividends will be subject to applicable laws, including satisfaction of solvency tests under the Business Corporations Act (Alberta), and satisfaction of certain applicable contractual restrictions contained in the agreements governing the Company’s outstanding indebtedness. Further, the actual amount, the declaration date, the record date and the payment date of any dividend are subject to the discretion of the InPlay Board of Directors. There can be no assurance that InPlay will pay dividends in the future.

The forward-looking information and statements included herein are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward-looking information or statements including, without limitation: changes in industry regulations and legislation (including, but not limited to, tax laws, royalties, and environmental regulations); the risk that the Pembina Cardium asset acquisition may not be completed on the anticipated terms or timing; risks related to an international trade war, including the risk that the U.S. government imposes additional tariffs on Canadian goods, including crude oil and natural gas, and that such tariffs (and/or the Canadian government’s response to such tariffs) adversely affect the demand and/or market price for InPlay’s products and/or otherwise adversely affects InPlay, or lead to the termination of InPlay’s financing arrangements for the Pembina Cardium asset acquisition, including specifically that the imposition of tariffs or similar measures in excess of 10% would be an adverse tariff event for the purposes of InPlay’s new credit facilities to be entered into in connection with the transaction and that the lenders thereunder may choose not to fund the transaction; the continuing impact of the Russia/Ukraine conflict and war in the Middle East; potential changes to U.S. economic, regulatory and/or trade policies as a result of a change in government; inflation and the risk of a global recession; changes in our planned 2025 capital program; changes in our approach to shareholder returns; changes in commodity prices and other assumptions outlined herein; the risk that dividend payments may be reduced, suspended or cancelled; the potential for variation in the quality of the reservoirs in which InPlay operates; changes in the demand for or supply of InPlay’s products; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans or strategies of InPlay or by third party operators of InPlay’s properties; changes in InPlay’s credit structure, increased debt levels or debt service requirements; inaccurate estimation of InPlay’s light crude oil and natural gas reserve and resource volumes; limited, unfavorable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time-to-time in InPlay’s continuous disclosure documents filed on SEDAR+ including InPlay’s Annual Information Form dated March 27, 2024 and the annual management’s discussion & analysis for the year ended December 31, 2024.

This document contains future-oriented financial information and financial outlook information (collectively, “FOFI”) about InPlay’s financial and leverage targets and objectives, potential dividends, and beliefs underlying our Board approved 2025 capital budget and associated guidance, all of which are subject to the same assumptions, risk factors, limitations, and qualifications as set forth in the above paragraphs. The actual results of operations of InPlay and the resulting financial results will likely vary from the amounts set forth in this document and such variation may be material. InPlay and its management believe that the FOFI has been prepared on a reasonable basis, reflecting management’s reasonable estimates and judgments. However, because this information is subjective and subject to numerous risks, it should not be relied on as necessarily indicative of future results. Except as required by applicable securities laws, InPlay undertakes no obligation to update such FOFI. FOFI contained in this document was made as of the date of this document and was provided for the purpose of providing further information about InPlay’s anticipated future business operations and strategy. Readers are cautioned that the FOFI contained in this document should not be used for purposes other than for which it is disclosed herein.

The forward-looking information and statements contained in this document speak only as of the date hereof and InPlay does not assume any obligation to publicly update or revise any of the included forward-looking statements or information, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

InPlay’s 2024 annual guidance and a comparison to 2024 actual results are outlined below.

GuidanceFY 2024(1)

ActualsFY 2024

Variance

Variance (%)

Production

Boe/d

8,700 – 8,750

8,712

–

–

Adjusted Funds Flow

$ millions

$68 – $70

$68.5

–

–

Capital Expenditures

$ millions

$63

$63

–

–

Free Adjusted Funds Flow

$ millions

$5 – $7

$5.5

–

–

Net Debt

$ millions

$59 – $61

$61

–

–

(1) As previously released February 4, 2025.

Risk Factors to FLI

Risk factors that could materially impact successful execution and actual results of the Company’s 2025 capital program and associated guidance and estimates include:

risks related to an international trade war, including the risk that the U.S. government imposes additional tariffs on Canadian goods, including crude oil and natural gas, and that such tariffs (and/or the Canadian government’s response to such tariffs) adversely affect the demand and/or market price for the Company’s products and/or otherwise adversely affects the Company;

volatility of petroleum and natural gas prices and inherent difficulty in the accuracy of predictions related thereto;

the extent of any unfavourable impacts of wildfires in the province of Alberta.

changes in Federal and Provincial regulations;

the Company’s ability to secure financing for the Board approved 2025 capital program and longer-term capital plans sourced from AFF, bank or other debt instruments, asset sales, equity issuance, infrastructure financing or some combination thereof; and

those additional risk factors set forth in the Company’s MD&A and most recent Annual Information Form filed on SEDAR+.

Key Budget and Underlying Material Assumptions to FLI

The key budget and underlying material assumptions used by the Company in the development of its 2025 guidance and 2025 pro-forma estimates(3) relating to the proposed acquisition of Pembina Cardium assets from Obsidian Energy Ltd. are as follows:

ActualsFY 2024

GuidanceFY 2024(1)

GuidanceFY 2025(1)

Pro-formaEstimateFY 2025(2)(3)(4)

WTI

US$/bbl

$75.72

$75.72

$72.00

$72.65

NGL Price

$/boe

$32.99

$32.90

35.40

48.65

AECO

$/GJ

$1.39

$1.39

$1.90

$1.85

Foreign Exchange Rate

CDN$/US$

0.73

0.73

0.70

0.70

MSW Differential

US$/bbl

$4.51

$4.50

$4.50

$4.75

Production

Boe/d

8,712

8,700 – 8,750

8,650 – 9,150

18,750

Revenue

$/boe

48.21

47.75 – 48.75

46.00 – 51.00

56.50 – 61.50

Royalties

$/boe

6.26

6.00 – 6.50

5.50 – 7.00

7.00 – 8.50

Operating Expenses

$/boe

15.12

14.50 – 15.50

13.00 – 15.00

16.00 – 18.00

Transportation

$/boe

0.97

0.90 – 1.05

0.90 – 1.15

0.90 – 1.15

Interest

$/boe

2.19

2.00 – 2.25

1.30 – 1.90

2.20 – 2.80

General and Administrative

$/boe

3.06

2.90 – 3.20

3.00 – 3.75

1.50 – 2.25

Hedging loss (gain)

$/boe

(0.86)

(0.75 – (1.00)

0.00 – 0.25

0.00 – 0.50

Decommissioning Expenditures

$ millions

$3.4

$3.2 – $3.4

$3.0 – $3.5

$6.0

Adjusted Funds Flow

$ millions

$68.5

$68 – $70

$69 – $75

$204

Dividends

$ millions

$16

$16

$16.5

$26

ActualsFY 2024

GuidanceFY 2024(1)

GuidanceFY 2025(1)

Pro-formaEstimateFY 2025(2)(3)(4)

Adjusted Funds Flow

$ millions

$68.5

$68 – $70

$69 – $75

$204

Capital Expenditures

$ millions

$63

$63

$41 – $44

$94

Free Adjusted Funds Flow

$ millions

$5.5

$5 – $7

$25 – $34

$104

Shares outstanding, end of year

# millions

90.1

90.1

90.4

158

Assumed share price

$/share

$1.73

$1.73

$1.65

1.55

Market capitalization

$ millions

$156

$156

$150

245

FAFF Yield

%

4 %

3% – 4%

17% – 23%

42 %

ActualsFY 2024

GuidanceFY 2024(1)

GuidanceFY 2025(1)

Pro-formaEstimateFY 2025(2)(3)(4)

Revenue

$/boe

48.21

47.75 – 48.75

46.00 – 51.00

56.50 – 61.50

Royalties

$/boe

6.26

6.00 – 6.50

5.50 – 7.00

7.00 – 8.50

Operating Expenses

$/boe

15.12

14.50 – 15.50

13.00 – 15.00

16.00 – 18.00

Transportation

$/boe

0.97

0.90 – 1.05

0.90 – 1.15

0.90 – 1.15

Operating Netback

$/boe

25.86

25.50 – 26.50

24.75 – 29.75

31.50 – 36.50

Operating Income Profit Margin

54 %

54 %

56 %

58 %

ActualsFY 2024

GuidanceFY 2024(1)

GuidanceFY 2025(1)

Pro-formaEstimateFY 2025(2)(3)(4)

Adjusted Funds Flow

$ millions

$68.5

$68 – $70

$69 – $75

$204

Interest

$/boe

2.19

2.00 – 2.25

1.30 – 1.90

2.20 – 2.80

EBITDA

$ millions

$76

$75 – $77

$74 – $80

$221

Net Debt

$ millions

$61

$59 – $61

$52 – $58

$203

Net Debt/EBITDA

0.8

0.8

0.6 – 0.8

0.9

(1)

As previously released February 4, 2025.

(2)

As previously released February 19, 2025.

(3)

InPlay’s pro-forma estimate for 2025 are preliminary in nature and do not reflect a Board approved capital expenditure budget. Following closing of the Pembina Cardium asset acquisition, InPlay will provide updated development plans and revised full-year 2025 guidance.

(4)

2025E pro forma estimates have been presented as though InPlay acquired the Acquired Assets at January 1, 2025 notwithstanding that income from January 1, 2025 to closing represents a purchase price adjustment and such production will not be directly attributed to InPlay.

See “Production Breakdown by Product Type” below

Quality and pipeline transmission adjustments may impact realized oil prices in addition to the MSW Differential provided above

Changes in working capital are not assumed to have a material impact between the years presented above.

Information Regarding Disclosure on Oil and Gas Reserves and Operational Information

Our oil and gas reserves statement for the year ended December 31, 2024, which will include complete disclosure of our oil and gas reserves and other oil and gas information in accordance with NI 51-101, will be contained within our Annual Information Form which will be available on our SEDAR profile at www.sedarplus.ca on or before March 31, 2025. The recovery and reserve estimates contained herein are estimates only and there is no guarantee that the estimated reserves will be recovered. In relation to the disclosure of estimates for individual properties, such estimates may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of aggregation. The Company’s belief that it will establish additional reserves over time with conversion of probable undeveloped reserves into proved reserves is a forward-looking statement and is based on certain assumptions and is subject to certain risks, as discussed above under the heading “Forward-Looking Information and Statements”.

This press release contains metrics commonly used in the oil and natural gas industry, such as “operating netbacks” and “reserve life index” or “RLI”. Each of these terms are calculated by InPlay as described within this press release. These terms do not have standardized meanings or standardized methods of calculation and therefore may not be comparable to similar measures presented by other companies, and therefore should not be used to make such comparisons. Such metrics have been included herein to provide readers with additional information to evaluate the Company’s performance, however such metrics should not be unduly relied upon.

Management uses these oil and gas metrics for its own performance measurements and to provide shareholders with measures to compare InPlay’s operations over time, however such measures are not reliable indicators of InPlay’s future performance and future performance may not be comparable to the performance in prior periods. Readers are cautioned that the information provided by these metrics, or that can be derived from the metrics presented in this press release, should not be relied upon for investment or other purposes, however such measures are not reliable indicators on InPlay’s future performance and future performance may not be comparable to the performance in prior periods.

References to light crude oil, NGLs or natural gas production in this press release refer to the light and medium crude oil, natural gas liquids and conventional natural gas product types, respectively, as defined in National Instrument 51-101, Standards of Disclosure for Oil and Gas Activities (“Nl 51-101“).

Production Breakdown by Product Type

Disclosure of production on a per boe basis in this document consists of the constituent product types as defined in NI 51–101 and their respective quantities disclosed in the table below:

Light and Medium Crude oil(bbls/d)

NGLs(boe/d)

Conventional Natural gas(Mcf/d)

Total(boe/d)

Q4 2023 Average Production

4,142

1,520

23,606

9,596

2023 Average Production

3,822

1,396

22,839

9,025

Q4 2024 Average Production

3,691

1,651

24,203

9,376

2024 Average Production

3,523

1,499

22,139

8,712

2024 Annual Guidance

3,535

1,495

22,170

8,725(1)

2025 Annual Guidance

3,425

1,510

23,790

8,900(2)

2025 Pro Forma Estimate

9,535

2,180

42,215

18,750

Notes:

1.

This reflects the mid-point of the Company’s 2024 production guidance range of 8,700 to 8,750 boe/d.

2.

This reflects the mid-point of the Company’s 2025 production guidance range of 8,650 to 9,150 boe/d.

3.

With respect to forward–looking production guidance, product type breakdown is based upon management’s expectations based on reasonable assumptions but are subject to variability based on actual well results.

BOE equivalent

Barrel of oil equivalents or BOEs may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different than the energy equivalency of 6:1, utilizing a 6:1 conversion basis may be misleading as an indication of value.

Initial Production Rates

References in this press release to IP rates, other short-term production rates or initial performance measures relating to new wells are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will commence production and decline thereafter and are not indicative of long-term performance or of ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Accordingly, the Company cautions that the test results should be considered to be preliminary.

Key Points: – U.S. Treasury yields declined slightly after lower-than-expected December producer price index (PPI) data. – Stock markets showed minimal movement as focus remained on upcoming consumer price index (CPI) data and policy uncertainty tied to President-elect Donald Trump. – Oil prices fell from recent highs, while the dollar index softened.

Treasury yields in the United States edged down on Tuesday following a report showing that producer prices increased just 0.2% month-on-month in December, underperforming the expected 0.3% rise. This marks a slowdown from November’s 0.4% gain. While the PPI data eased immediate inflation concerns, market attention remains fixed on the consumer price index (CPI) report due on Wednesday.

CPI figures are anticipated to reveal consistent monthly inflation at 0.3% for December, with an annual increase to 2.9%, up from 2.7% in November. Market sentiment has been shaped by fears of persistent inflation, amplified by uncertainty surrounding President-elect Trump’s proposed trade and tax policies. Speculation about tariffs ranging from 2% to 5% monthly has added to concerns about potential inflationary pressures.

Market Performance Stock market activity was muted as traders digested the PPI data. The Dow Jones Industrial Average added 0.10%, closing at 42,339.90, while the S&P 500 and Nasdaq Composite slipped 0.15% and 0.21%, respectively. The Russell 2000 index, a key indicator for smaller U.S. companies, has seen a decline of roughly 11% since its peak in November.

Internationally, MSCI’s global stock index inched up by 0.14%, while Europe’s STOXX 600 index dipped by 0.11%. With U.S. corporate earnings season kicking off, major banks are expected to report strong quarterly results, driven by increased dealmaking and trading activities.

Treasury Yields and Dollar Movement The yield on the 10-year Treasury note eased slightly to 4.790%, staying close to its recent 14-month high of 4.805%. Higher yields have weighed on equities, as they make bonds more attractive and raise borrowing costs for companies.

In currency markets, the dollar index fell by 0.1% to 109.31. The euro gained 0.46% to $1.0292, while the dollar strengthened against the yen, rising 0.25% to 157.87.

Oil and Asian Markets Oil prices retreated after reaching multi-month highs earlier this week. U.S. crude dropped 1.23% to $77.84 per barrel, while Brent crude declined 0.93% to $80.27 per barrel. In Asia, Japan’s Nikkei index fell 1.8%, dragged down by chip stocks and speculation about a potential interest rate hike by the Bank of Japan (BoJ). Deputy Governor Ryozo Himino hinted at a possible rate increase during the central bank’s next policy meeting on January 24, adding to market uncertainty.

With inflation and policy concerns dominating the narrative, investors are likely to remain cautious. The upcoming CPI data and the direction of Trump’s economic agenda are poised to play pivotal roles in shaping market sentiment in the coming weeks.

Key Points: – Ban protects 625 million acres of federal waters from new oil and gas development – Trump pledges reversal but faces legal hurdles without Congressional support – Decision impacts East, West coasts and parts of Alaska while preserving current operations

President Joe Biden has announced a sweeping ban on new offshore oil and gas development across vast stretches of U.S. coastlines, creating a potential environmental legacy that his successor may struggle to dismantle. The executive action, protecting 625 million acres of ocean, represents a significant move in Biden’s climate agenda just weeks before the presidential transition.

The ban covers federal waters off the East and West coasts, the eastern Gulf of Mexico, and portions of Alaska’s northern Bering Sea. While largely symbolic, as it doesn’t affect areas with active drilling operations, the decision aligns with Biden’s broader environmental goals, including his commitment to conserve 30% of U.S. lands and waters by 2030.

The timing of this decision carries particular significance, as President-elect Donald Trump has explicitly stated his intention to reverse the ban immediately upon taking office. However, legal precedent suggests this may be more challenging than anticipated. A 2019 court ruling established that while the 70-year-old Outer Continental Shelf Lands Act grants presidents the authority to withdraw areas from drilling, it doesn’t provide the power to reverse such withdrawals without Congressional action.

Industry impact appears limited, as only 15% of U.S. oil production comes from federal offshore acreage, primarily in the Gulf of Mexico. This share has been declining over the past decade as onshore drilling, particularly in Texas and New Mexico, has transformed the United States into the world’s leading oil and gas producer.

The American Petroleum Institute has criticized the decision, arguing it threatens energy security and urging policymakers to reverse what they term a “politically motivated decision.” Conversely, environmental groups like Oceana celebrate the move as a victory for coastal communities and marine ecosystems.

The ban’s geographical scope notably includes areas where Trump himself had previously prohibited drilling during his re-election campaign, including waters off Florida, Georgia, South Carolina, North Carolina, and Virginia. This overlap highlights the bipartisan nature of coastal protection concerns, as many Republican-led coastal states have historically opposed offshore drilling due to its potential impact on tourism.

Biden’s decision invokes the memory of the 2010 Deepwater Horizon disaster, arguing that the minimal drilling potential in the protected areas doesn’t justify the public health and economic risks associated with future leasing. The administration emphasizes that the ban aligns with both environmental protection goals and practical risk assessment.

Looking ahead, the ban’s durability will likely depend on Congressional willingness to intervene, as well as potential legal challenges. The decision adds another layer to the complex relationship between federal energy policy and environmental protection, setting up a significant early test for the incoming Trump administration’s energy agenda.

Key Points: – Brent crude oil prices are rising as markets speculate on a potential Israeli strike against Iran’s oil infrastructure, particularly Kharg Island, which handles 90% of Iran’s crude exports. – A worst-case scenario would involve disruption in the Strait of Hormuz, a critical passage for 20% of the world’s crude oil exports, which could cause a dramatic spike in oil prices. – While OPEC+ has enough spare capacity to offset supply disruptions from an Israeli strike, it may struggle if Iran retaliates, adding further uncertainty to the energy markets.

Brent crude oil extended its gains today, driven by rising fears that Israel could launch a retaliatory strike on Iran’s oil infrastructure following Tehran’s recent ballistic missile attack. Markets are increasingly concerned that such an attack could disrupt the flow of oil from one of the world’s most critical regions for crude exports.

Concerns Over Key Oil Choke Points

Israel’s retaliation, though not yet clearly defined, has analysts worried about the potential impact on Iran’s oil exports, especially if Israel targets Kharg Island, where 90% of Iran’s crude oil exports pass through. A strike there would have significant consequences on global oil supply, sending prices higher. However, the worst-case scenario would involve a strike on the Strait of Hormuz, through which 20% of the world’s crude oil flows, which would cause a dramatic spike in crude prices.

U.S. President Joe Biden has urged Israel to avoid targeting Iranian oil facilities, following his previous opposition to a strike on Iran’s nuclear sites.

Oil Prices Surge on Market Speculation

Brent crude prices surged last week, marking the steepest increase since early 2023. Activity in the options market has also shown increased demand for hedging against the risk of further gains, reflecting market fears of a supply disruption. Despite these gains, Brent crude is still trading below last year’s price of $88 per barrel, when the current conflict in the Middle East began.

OPEC+ Supply and Market Outlook

As OPEC+ prepares to raise production in December following years of output cuts, analysts believe the group has enough spare capacity to offset any supply disruptions caused by an Israeli attack on Iranian oil facilities. However, concerns linger that OPEC+ could face challenges if Iran retaliates, potentially leading to further volatility in oil markets.

While some analysts see an attack on Iranian oil infrastructure as a less likely response from Israel, the broader geopolitical tensions and risks of wider conflict are adding uncertainty to the energy markets.

Crude oil prices have spiked nearly 3% as geopolitical tensions in the Middle East escalate and Libya halts its oil production. This sudden surge has caught the attention of investors worldwide, potentially signaling a shift in the energy market landscape.

West Texas Intermediate (WTI) crude jumped to over $77 per barrel, while Brent crude, the international benchmark, surpassed $80 per barrel. This sharp increase comes after a weekend of heightened tensions in the Middle East and a significant disruption in Libyan oil production.

The catalyst for this price surge appears to be twofold. First, Israel’s recent airstrike against Hezbollah’s rocket launching stations in Lebanon has exacerbated fears of a broader conflict involving Iran. The potential for Iranian military response has raised concerns about possible disruptions to global oil movements, a factor that could significantly impact supply chains and pricing.

Adding fuel to the fire, Iran-backed Houthi rebels continue their attacks on vessels in the Red Sea, with a Greek oil tanker being the latest casualty. These ongoing hostilities pose a substantial threat to one of the world’s most crucial shipping routes, potentially disrupting oil transportation and further tightening supply.