InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter financial results. InPlay Oil reported a first quarter net loss of C$2.9 million or C$0.18 per share compared to net income of C$1.7 million or C$0.02 per share during the prior year period. This was below our net income estimate of C$4.2 million or C$0.15 per share, primarily due to an unrealized loss on derivative contracts of C$4.6 million and higher-than-expected expenses. Moreover, commodity prices declined slightly during the first quarter, leading to lower revenues of C$38.4 million compared to our estimate of C$40.4 million.

Corporate 2025 guidance. The company generated quarterly production of 9,076 barrels of oil equivalent per day (boe/d), a 5% increase year-over-year and above our expectations of 8,800 boe/d. The company is raising its estimated field production expectations to 21,500 boe/d, a marked increase from 18,750 boe/d, and expects 2025 full year production to be in the range of 16,000 to 16,800 boe/d. Revenue guidance has been adjusted downward to C$46.75 to C$51.75 boe/d from C$56.50 to C$61.50 boe/d. Adjusted funds flow is expected to be between C$124 million and C$133 million, down from $204 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Share consolidation. As of April 21, 2025, InPlay Oil shares are trading on a post-consolidation basis, with 27,939,437 common shares outstanding. The terms of the share consolidation were one post-consolidation common share per six pre-consolidation common shares. Fractional shares resulting from the consolidation were rounded down to the nearest whole number.

Updating estimates and price target. We are updating our 2025 estimates to reflect fewer shares outstanding and lower crude oil price estimates. For 2025, we are lowering our oil and gas revenue and earnings per share estimates to C$318.7 million and C$1.34, from C$333.5 million and C$1.46, both adjusted for the share consolidation. Moreover, we have lowered our adjusted funds flow (AFF) to C$149.5 million from C$161.6 million. We are maintaining our production estimate of 18,750 barrels of oil equivalent per day (boe/d) post the Pembina acquisition, which averages 15,816 boe/d for the full-year 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transformative acquisition closed. InPlay Oil recently closed its acquisition of Cardium light oil focused assets in the Pembina area of Alberta from Obsidian Energy for net consideration of approximately $301 million. The transaction more than doubles InPlay’s total output to 18,750 barrels of oil equivalent per day (boe/d). The assets are 68% weighted in oil and natural gas liquids (NGLs) and have a low decline rate of 22%. Management expects greater production, a lower decline rate, and enhanced operational efficiency. Following the completion of the acquisition, InPlay had 167,636,627 shares issued and outstanding.

Share consolidation. Effective April 14, InPlay will implement a share consolidation based on one common share for six common shares. The consolidation was unanimously approved by the company’s board and by 96.56% of the votes cast during a special meeting of shareholders. Post-consolidation, InPlay will have approximately 27,939,438 common shares issued and outstanding. The shares are expected to begin trading on a post-consolidation basis two to three trading days following the effective date.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Reserve report. Hemisphere released results from its independent reserve evaluation as of December 31, 2024. Compared to the year-end 2023 reserve report, proved developed producing (PDP) reserves increased 13.1% to 9,302.2 thousand barrels of oil equivalents. The growth in PDP reserves replaced 186% of 2024 production. Hemisphere’s estimated 2024 capital expenditures of ~C$22 million funded PDP reserve growth, annual production growth of ~10%, additional infrastructure, and the testing of a new resource play in Saskatchewan with an enhanced oil recovery (EOR) polymer pilot project.

Outlook for 2025.Hemisphere expects 2025 capital expenditures of ~C$17 million which are expected to support ~15% growth in annual average production to 3,900 barrels of oil equivalent per day (boe/d) compared to 2024. Most of the capital will be allocated to drilling, optimization, and facility work, with ~10% allotted to exploration and land acquisition. The majority of the planned expenditures are scheduled for the third quarter of 2025, providing the company with the flexibility to adjust plans based on changes in commodity prices.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full-year 2024 financial results. InPlay Oil reported full-year net income and earnings per share of C$9.5 million and C$0.10, respectively, below our estimates of approximately C$11.4 million and C$0.12. The variance was primarily due to lower-than-expected natural gas revenue driven by weaker AECO pricing. Production for the year averaged 8,712 barrels of oil equivalent per day (boe/d) compared to 9,025 boe/d in 2023. Consequently, revenue decreased to C$153.7 million compared to C$179.4 million in 2023. Adjusted funds flow in 2024 was C$68.5 million, down from C$91.8 million in 2023.

Updated 2025 estimates. Please note that our revised estimates assume the closing of the pending Pembina acquisition on April 15th, 2025. For 2025, our oil and gas revenue estimate is C$333.5 million compared to our prior estimate of C$159.4 million. We have raised our 2025 AFF and EPS estimates to C$161.6 million and C$0.27, respectively, from C$71.7 million and C$0.14. We forecast net income of C$40.9 million, up from our previous estimate of C$13.2 million. Our 2025 estimates are based on an average annual production of 15,879 boe/d compared to our prior forecast of 8,901 boe/d.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transaction highlights. The acquisition appears to offer significant synergies and benefits to InPlay’s operations. InPlay’s production is expected to more than double to 18,750 boe/d from previous guidance of 8,650-9,150. Additionally, on a per share basis, 2025 adjusted funds flow (AFF) is expected to increase to C$204 million from previous guidance of C$69-75 million. Furthermore, the nature of the assets acquired is expected to enhance operational efficiencies to InPlay’s existing Pembina asset base by increasing the scale and contributing to lower decline, higher oil-weighting, and less capital-intensive production.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated 2024 guidance. Inplay Oil modestly lowered its 2024 production guidance to 8,700 to 8,750 boe/d from 8,700 to 9,000. Additionally, the company lowered its expectations for crude oil prices and slightly raised expense guidance. Due to these changes, the adjusted funds flow (AFF) is expected to range from C$68 million to C$70 million compared to prior guidance of C$70 million to C$73 million. Capital expenditures for 2024 are expected to come in at around C$63 million compared to original expectations of C$64-67 million. The savings are mainly due to cost efficiencies from the Pembina Cardium Unit #7 (PCU7) drilling program.

Outlook for 2025. Management has planned a capital-efficient program in 2025. The company expects to increase production by 2%, in the range of 8,650 to 9,150 boe/d, compared to 2024, while spending around C$20 million less. The total capital budget for 2025 is C$41 million to C$44 million and will primarily be directed toward the Pembina Cardium Unit #7 property. Management expects adjusted funds flow (AFF) to benefit from lower capital expenditures and anticipates 2025 AFF to be between C$69 million and C$75 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Outlook for 2025. Hemisphere Energy expects 2025 capital expenditures of approximately C$17 million which are expected to support ~15% growth in annual average production to 3,900 barrels of oil equivalent per day (boe/d) compared to 2024. Expenditures will be funded entirely from adjusted funds flow. Most of the capital will be allocated to drilling, optimization, and facility work, with approximately 10% allotted to exploration and land acquisition. Most planned expenditures are scheduled for the third quarter of 2025, providing the company with the flexibility to adjust plans based on changes in commodity prices.

Updating estimates. We have increased our 2024 adjusted funds flow (AFF) and EPS estimates to C$45.4 million and $0.32, respectively, from C$43.5 million and $0.31 to reflect modestly higher operating earnings. AFF and EPS in the fourth quarter are estimated to be C$10.0 million and $0.06, respectively. We have also increased our 2025 AFF and EPS estimates to C$50.6 million and $0.37, respectively, from C$38.0 million and $0.27 to reflect higher average annual production of 3,900 boe/d compared to our prior estimate of 3,625 boe/d. Additionally, we increased our WTI crude oil price assumption to US$72.00 per barrel versus our prior estimate of US$70.00.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – January 29, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide a corporate update, announce the declaration of a quarterly dividend payment to shareholders, and deliver guidance for 2025.

Corporate Update

In 2024, Hemisphere achieved annual production growth of 10%, executed a $22 million capital expenditure program, and increased its positive year-end working capital position. The Company also returned over $0.22/share ($21.2 million) to shareholders in the form of dividends ($15.7 million) and share buybacks ($5.5 million), which represents an annualized 11.9% yield to shareholders based on Hemisphere’s market capitalization at December 31, 2024.

Hemisphere’s 2024 capital expenditure program grew production, added required infrastructure, and commenced testing a new resource play with an enhanced oil recovery (“EOR”) polymer pilot project. These investments were funded entirely by cash flow from the Company’s long-life reserve base and ultra-low production decline rates in the Atlee Buffalo oil assets, and have set up Hemisphere for continued growth in 2025.

Based on field estimates, production over the past two months (December 1, 2024 – January 27, 2025) has averaged approximately 3,800 boe/d (99% heavy oil) as new Atlee Buffalo wells were brought online through the fourth quarter of last year. With the addition of a new treater late in the quarter and upcoming injector conversions, these and other wells are expected to continue to be optimized during the first quarter of 2025 in Hemisphere’s flagship EOR polymer flood projects.

Balance sheet strength in 2024 allowed Hemisphere to invest in its pilot EOR project in the Marsden area of western Saskatchewan. The Company drilled 5 wells (3 production wells and 2 injection wells) and built facilities required to produce oil and inject polymer back into a known accumulation of oil that had been previously produced with vertical wells and abandoned, with the plans of rebuilding reservoir pressure and increasing the recovery factor of the oil-in-place from the pool. First injection commenced late in the third quarter of 2024 and Hemisphere is anticipating to see potential EOR response in mid-to-late 2025.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on February 26, 2025 to shareholders of record as of the close of business on February 12, 2025. The dividend is designated as an eligible dividend for income tax purposes.

2025 Corporate Guidance

Hemisphere’s Board of Directors has approved a 2025 capital expenditure program of approximately $17 million, which is planned to be entirely funded by Hemisphere’s estimated 2025 adjusted funds flow1 (“AFF”) of $51 million and is anticipated to provide 15% annual production growth. The majority of capital will be allocated to drilling, optimization, and facility work, with approximately 10% allotted to exploration and land acquisition. Most of the planned capital expenditures are scheduled for the third quarter of 2025, providing Hemisphere with the flexibility to adjust plans subject to the commodity price environment.

After capital expenditures and asset retirement obligations (“ARO”), 2025 free funds flow1 (“FFF”) is estimated to be $34 million, of which approximately 30% is budgeted to be paid in quarterly base dividends as shown in the table below. The balance of cash will be used for discretionary purposes, which may include potential acceleration of other development or exploration projects, acquisitions, and additional return of capital to shareholders through Hemisphere’s normal course issuer bid (“NCIB”) program and/or special dividends. In 2024, two special dividends totaling $0.06/share ($5.7 million) were paid to shareholders in addition to Hemisphere’s base quarterly dividends of $0.10/share ($10 million), and share buybacks amounted to $0.06/share ($5.5 million), bringing total shareholder returns to $0.22/share ($21.2 million).

Management believes that the 2025 development plan provides stable production growth and consistent shareholder returns, with significant flexibility built in to allow for necessary adjustments based on changing political and commodity environments.

Highlights and assumptions of Hemisphere’s guidance at US$75/bbl WTI are as follows:

Average annual production of 3,900 boe/d (99% heavy oil), a 15% increase as compared to 2024

Average WTI price of US$75/bbl, with sensitivities shown at US$65/bbl and US$85/bbl

WCS differential of US$14.00/bbl and quality adjustment of $7.00/bbl

CAD/US FX of 1.43

Operating and transportation costs of $15.25/boe

Royalties and GORRs on gross revenue of 21% at US$75/bbl WTI, 19% at US$65/bbl WTI, and 23% at US$85/bbl WTI

Net G&A of $3.66/boe

Tax Costs of $8.10/boe at US$75/bbl WTI, $5.64/boe at US$65/bbl WTI, and $10.37/boe at US$85/bbl WTI

Notes: (1) AFF, Capital Expenditures, and FFF (including per share amounts) are non-IFRS financial measures that are forward looking and do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. AFF per basic share and FFF per basic share are non-IFRS financial ratios that are forward looking and do not have any standardized meaning under IFRS and therefore may not be comparable to similar ratios presented by other entities and include non-IFRS financial measure components of AFF and FFF. See “Non-IFRS Measures“. (2) See assumptions noted above within “2025 Corporate Guidance”. (3) Using a 2025 weighted average of 97.4 million basic shares issued and outstanding. (4) The amounts above do not include potential future purchases through the Company’s NCIB program or other discretionary uses of available funds.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as anticipate, continue, estimate, expect, forecast, may, will, project, could, plan, intend, should, believe, outlook, potential, target, and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements regarding the record date and payment date for Hemisphere’s quarterly dividend; expectations for the continued optimization of certain wells during the first quarter of 2025 in Hemisphere’s flagship EOR polymer flood projects; expectations on timing for potential EOR responses for activities in the Marsden area of western Saskatchewan; that Hemisphere’s 2025 capital budget is planned to be entirely funded by Hemisphere’s estimated 2025 AFF and is anticipated to provide 15% annual production growth, including that the majority of capital will be allocated to drilling, optimization, and facility work, with approximately 10% allotted to exploration and land acquisition, as well as expectations for the timing of such expenditures; Hemisphere’s anticipation that approximately 30% of estimated $34 million in free funds flow will be paid in quarterly dividends with the balance of cash being used for discretionary purposes; the expected manner in which the Company’s 2025 capital budget will be spent, including the timing of such expenditures and any discretionary amounts, which may include potential acceleration of other development or exploration projects, acquisitions, and return of capital to shareholders through Hemisphere’s NCIB program and/or dividends, and the anticipated effects thereof, including as set forth under “2025 Corporate Guidance” and the Company’s dividend policy and the other matters and guidance set forth under “2025 Corporate Guidance”; and management’s belief that the 2025 development plan provides stable production growth and consistent shareholder returns, with significant flexibility built in to allow for necessary adjustments based on changing political and commodity environments.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein (including the assumptions noted in respect of “2025 Corporate Guidance”), assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; continued trade-agreements remain in place and no trade related disputes will develop, including tariffs on Canadian energy production to the United States will be applicable, that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; inflationary pressure and related costs; that the Company’s dividend policy will remain the same and the Company will continue to be able to declare dividends; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the accuracy of the Company’s reservoir modelling; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; regulatory risks, including penalties or other remedial actions, the ability of the Company to maintain legal title to its properties; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; results of Hemisphere’s waterflood operations; the ability of Hemisphere to, pending future events, return capital to shareholders as a result of any required third party approvals; changes in budgets; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s most recent Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Forward Looking Financial Information

This news release may contain future oriented financial information (“FOFI”) within the meaning of applicable securities laws, including with respect to the Company’s anticipated 2025 Free Funds Flow, Capital Expenditures and Adjusted Funds Flow (including where applicable per share amounts). The FOFI has been prepared by management to provide an outlook of the Company’s activities and results. The FOFI has been prepared based on a number of assumptions including the assumptions discussed and disclosed above, including in relation to “2025 Corporate Guidance” above and “Forward Looking Statements” above and that the Company is cash taxable in 2025. Readers are cautioned that the assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be placed on FOFI. The Company’s actual results, performance or achievement could differ materially from those expressed in, or implied by, these FOFI, or if any of them do so, what benefits the Company will derive therefrom. The Company has included the FOFI in order to provide readers with a more complete perspective on the Company’s future operations and such information may not be appropriate for other purposes. The Company disclaims any intention or obligation to update or revise any FOFI statements, whether as a result of new information, future events or otherwise, except as required by law.

Non-IFRS and Other Measures

This news release contains terms that are non-IFRS measures or ratios that are forward looking and commonly used in the oil and gas industry which are not defined by or calculated in accordance with International Financial Reporting Standards (“IFRS”), such as: (i) adjusted funds flow (ii) adjusted funds flow per basic share; (iii) capital expenditures; (iv) free funds flow; and (v) free funds flow per basic share. These terms should not be considered an alternative to, or more meaningful than the comparable IFRS measures (as determined in accordance with IFRS) which in the case of funds flow is cash provided by operating activities, in the case of adjusted funds flow (and adjusted funds flow per share) is cash provided by operating activities and in the case of capital expenditures is cash flow used in investing activities. There is no IFRS measure that is reasonably comparable to free funds flow. These measures are commonly used in the oil and gas industry and by Hemisphere to provide shareholders and potential investors with additional information regarding: (i) in the case of adjusted funds flow and free funds flow, the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt.

Hemisphere’s determination of these measures may not be comparable to that reported by other companies. Adjusted funds flow is calculated as cash generated by operating activities, before changes in non-cash working capital and adjusted for any decommissioning expenditures; Adjusted funds flow per share is calculated using the outstanding basic shares of the company as footnoted in the 2024 Corporate Guidance table; Free Funds Flow is calculated as Adjusted Funds Flow less capital expenditures; and Free funds flow per share is calculated using the outstanding basic shares of the company as footnoted in the 2025 Corporate Guidance table. The Company has provided additional information on how these measures are calculated, including a reconciliation of such measures to their comparable IFRS measure, in the Management’s Discussion and Analysis for the year ended December 31, 2023 and the interim period ended September 30, 2024, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

In respect of any forward-looking non-IFRS measures, there is no significant difference between the non-GAAP financial measure that are forward-looking information and the equivalent historical non-GAAP financial measures.

In this news release, Hemisphere uses the term market capitalization at year-end. Hemisphere’s market capitalization was $178.2 million based on 97,389,735 shares outstanding and the Company’s closing price of $1.83 per share on December 31, 2024.

All amounts are expressed in Canadian dollars unless otherwise noted.

Oil and Gas Advisories

Any references in this news release to recent production rates (including as a result of recent waterflood activities) which may be considered to be initial rates and are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

Barrel

WTI

West Texas Intermediate

bbl/d

barrels per day

WCS

Western Canadian Select

$/bbl

dollar per barrel

US$

United States Dollar

boe

barrel of oil equivalent

boe/d

barrel of oil equivalent per day

IFRS

International Financial Reporting Standards

$/boe

dollar per barrel of oil equivalent

G&A

General and Administrative Costs

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Vancouver, British Columbia–(Newsfile Corp. – December 16, 2024) – Hemisphere Energy Corporation (TSXV: HME)(OTCQX: HMENF) (“Hemisphere” or the “Company”) announces that its Board of Directors has approved a new Restricted Share Unit (“RSU”) Plan and made certain amendments to its existing Stock Option Plan that are intended to comply with the provisions of TSXV Policy 4.4 – Security Based Compensation, as well as other housekeeping changes, both subject to shareholder approval at the next annual general meeting in May 2025. The Company’s Board of Directors has also approved grants of incentive RSUs and stock options.

Restricted Share Units

Under the new RSU Plan, RSUs may be granted to directors, employees, and contractors of the Company. The RSU Plan permits the Company to either redeem RSUs for cash or by issuance of Hemisphere’s common shares.

On December 13, 2024, the Company conditionally awarded 930,000 incentive RSUs to directors and officers of Hemisphere, all of which will vest one-third annually over a three-year period and will expire on December 15, 2027.

The RSU Plan and the grant of the above noted RSUs each remain subject to the requisite approval of the shareholders of the Company, in accordance with the rules of the TSX Venture Exchange. These matters, as well as matters relating to the amendments and renewal of the Company’s Stock Option Plan, are expected to be presented for approval at the Company’s next annual meeting of shareholders.

Stock Options

Additionally, in accordance with the Company’s Stock Option Plan, Hemisphere has granted 48,000 incentive stock options to its investor relations service provider on December 13, 2024 at an exercise price of $1.84 per share which will vest quarterly over 12 months and expire on December 13, 2029.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood EOR methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

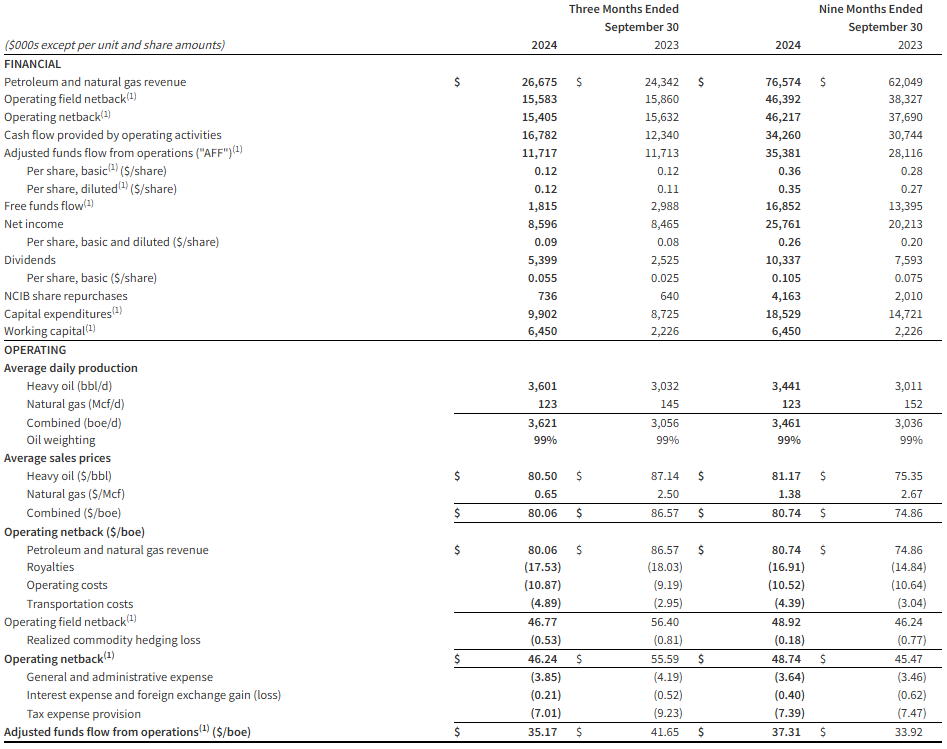

Third quarter financial results. Hemisphere Energy reported third-quarter net income of C$8.6 million or C$0.09 per share compared to C$8.5 million or C$0.08 per share during the third quarter of 2023. We had projected net income of C$8.4 million or C$0.08 per share. Year-over-year, oil and natural gas revenue increased 9.6% to C$26.7 million, driven by an 18.5% increase in average daily production to 3,621 barrels of oil equivalent (BOE) compared to 3,056 during the prior year period and our estimate of 3,600. The average sales price per BOE declined to C$80.06 compared to C$86.57 in the third quarter of 2023. Adjusted funds flow from operations amounted to C$11.7 million or C$0.12 per diluted share compared to C$11.7 million or C$0.11 per diluted share during the prior year period.

Updating estimates. While our 2024 EPS estimate is unchanged at C$0.31, we have modestly lowered our adjusted funds flow estimate to C$43.5 million from C$43.8 million. We lowered our full year average daily production expectations to 3,456 barrels of oil equivalent from 3,534 to reflect down time in the fourth quarter associated with vessel inspections and maintenance. While our 2025 average daily production estimate of 3,625 barrels of oil equivalent is unchanged, we lowered our 2025 AFF and EPS estimates to C$38.0 million and C$0.27 per share from C$42.6 million and C$0.32 to reflect lower crude oil prices.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – November 21, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the three and nine months ended September 30, 2024, declare a quarterly dividend payment to shareholders, and provide an operations update.

Q3 2024 Highlights

Achieved quarterly production of 3,621 boe/d (99% heavy oil), an 18% increase over the same quarter last year.

Attained quarterly revenue of $26.7 million, a 10% increase from the third quarter of 2023.

Delivered operating netback1 of $15.4 million or $46.24/boe for the quarter.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $11.7 million or $35.17/boe.

Executed a $9.9 million capital expenditure program to drill eight successful wells in Atlee Buffalo, Alberta and construct a new multi-well battery and polymer injection facility in Marsden, Saskatchewan.

Exited the third quarter with a positive working capital1 position of $6.5 million.

Paid a special dividend of $2.9 million ($0.03/share) to shareholders on July 26, 2024.

Paid a quarterly base dividend of $2.5 million ($0.025/share) to shareholders on September 13, 2024.

Announced a special dividend of $0.03/share to shareholders that was paid subsequent to the quarter on October 25, 2024.

Renewed the Company’s Normal Course Issuer Bid (“NCIB”).

Purchased and cancelled 756,400 shares under the Company’s NCIB.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditures, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited consolidated interim financial statements and related notes, and the Management’s Discussion and Analysis for the three and nine months ended September 30, 2024 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Financial and Operating Summary

Quarterly Dividend and Shareholder Return

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 27, 2024 to shareholders of record as of the close of business on December 13, 2024. The dividend is designated as an eligible dividend for income tax purposes.

A minimum of $21 million is anticipated to be returned to Hemisphere’s shareholders in 2024, inclusive of $9.8 million in quarterly base dividends, $5.9 million in two special dividends, and $5.3 million in NCIB share repurchases and cancellations. Based on the Company’s current market capitalization of $179 million (97.5 million shares issued and outstanding at market close price of $1.84 per share on November 20, 2024), this represents an annualized yield of 11.7% to Hemisphere’s shareholders.

Operations Update

Hemisphere’s polymer floods in Atlee Buffalo continue to perform well, with third quarter production up 18% from the same period of 2023. During the third quarter of 2024, Hemisphere drilled eight new horizontal wells into its Atlee Buffalo pools, of which three are in the F pool and five in the G pool. All but one of these wells were brought online subsequent to the end of the quarter, although at least two will ultimately be converted into injectors to continue to build reservoir pressure and sweep oil to producers in the pool.

The Company is currently adding another treater to its G pool battery to handle the additional volumes from these wells. At the same time, vessel inspection and overall maintenance is being completed across the G pool battery. Due to this downtime, management anticipates lower corporate production during the first half of the fourth quarter, with overall expectations for annual 2024 production to be in line with guidance.

In its Marsden, Saskatchewan property, Hemisphere continues to evaluate its new polymer pilot project and is awaiting source well regulatory approval in order to increase injection rates. At this time no significant production is budgeted from the area.

The Hemisphere team is currently working on development plans for next year and expects to release details on its 2025 guidance in January.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a quarterly dividend will be paid December 27, 2024 to shareholders of record as of the close of business on December 13, 2024; that a minimum of $21 million is anticipated to be returned to shareholders in 2024; that at least two of Hemisphere’s new wells will be converted into injectors; that management anticipates lower corporate production during the first half of the fourth quarter, with overall expectations for annual 2024 production to fall in line with guidance; and that Hemisphere expects to release details on its 2025 guidance in January.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the perspectivity of recently acquired properties and the timing and manner to explore and develop the same; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, free funds flow, capital expenditures, operating field netback, operating netback, and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered more meaningful than IFRS measures in evaluating the Company’s performance.

a)Adjusted funds flow from operations (“AFF”) (Non-IFRS Financial Measure and Ratio if calculated on a per share or boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter financial results. InPlay Oil generated third quarter net income of C$146 thousand or C$0.00 per share compared to C$9.2 million or C$0.08 per share during the prior year period. We had predicted net income in the amount of C$423 thousand or C$0.00 per share. Average quarterly production declined to 8,206 barrels of oil equivalents per day (boe/d) compared to 9,003 boe/d in the third quarter of 2023 and our estimate of 8,238 boe/d.

Corporate 2024 guidance. While InPlay has maintained its production guidance of 8,700 to 9,000 boe/d, commodity price expectations were lowered, and operating expenses are expected to be in the range of C$13.50 to C$15.50 per boe/d compared to prior guidance of C$13.00 to C$15.25 per boe/d. Capital expenditures are expected to total $63 million compared with prior guidance of C$64 million to C$67 million. Adjusted funds flow is expected to be in the range of C$70 million to C$73 million compared to previous expectations of C$80 million to C$85 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.