Motorsport Games, a Motorsport Network company, combines innovative and engaging video games with exciting esports competitions and content for racing fans and gamers around the globe. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”). Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 results disappoint. The company reported its first quarter results, which were disappointing, but not unexpected. With the lack of current franchise game releases, total company revenues declined 48% to $1.7 million. Given the continued investment in game development, EBITDA loss increased to $4.6 million, well above our $2.2 million loss estimate.

A tough situation. Management is trying to get to the finish line of launching new franchise motorsport games, which should provide a significant revenue lift and generate positive cash flow. The largest opportunity for that prospect would be in the second quarter 2024 when it launches its new IndyCar game.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q1 results. The company reported strong quarterly results. Revenue grew 87% from Q1 22 to $21.2 million, beating our estimate of $17.1 million by 24%. Additionally, Adj. EBITDA of $0.5 million surpassed our estimate of negative $0.2 million. The better than expected results were a product of strength in both Buy-side and Sell-side segments.

Buy-side excels. The company’s higher margin Buy-side segment reported revenue of $7.4 million, beating our estimate of $6.1 million by 22%. While Buy-side only comprises 35% of revenues, its margins are much higher than Sell-side and contributes to cash flow in a more meaningful way. Management attributed the success of its Buy-side segment to existing clients spending 20% to 30% more, and increasing is client base by 3%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile application. Codere currently operates in its core markets of Spain, Italy, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence in the region.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Beats Q1 expectations. The company reported strong Q1 results with net gaming revenue (NGR) of €39.5 million and an adj. EBITDA loss of €2.3 million, compared with our forecast of €33.5 million and a loss of €9.2 million, respectively. The company achieved the favorable results after lowering its marketing spend to streamline its path to profitability.

Performing well in Mexico. Despite lower marketing spend, net gaming revenue (NGR) in Mexico continued to grow in Q1. NGR of €17.6 million was up 75% while the adj. EBITDA loss of €2.0 million, compared with a €7.7 million loss in the prior year period. The strong results in Mexico were driven by a 42% increase in active users and higher spend per active user.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Beats Q1 estimates. The company reported another industry leading performance in the first quarter with revenues up 2.9% to $103.1 million, beating our $100.9 million estimate. We estimate that industry revenues likely will be down in the range of 3% to 5%. First quarter adj. EBITDA was $19.4 million, which beat our $17.9 million estimate.

Digital surpasses 50% of revenue. Digital revenue grew 8% in the quarter, accounting for 54% of total revenue. Impressively, Digital contributed 63% of total operating profit. The Digital revenue growth was fueled by the company’s Digital Advertising solutions business, which was up 15%, making up for the slight decline in Townsquare Interactive revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

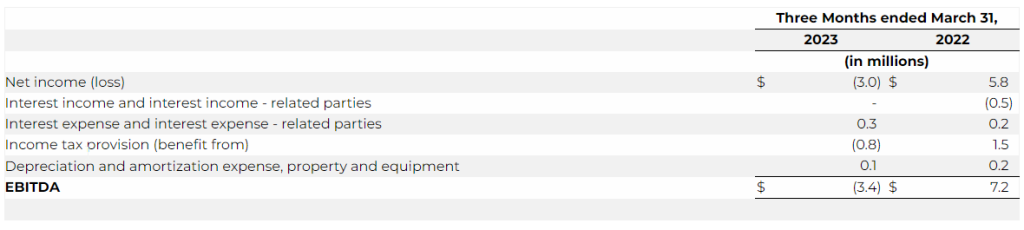

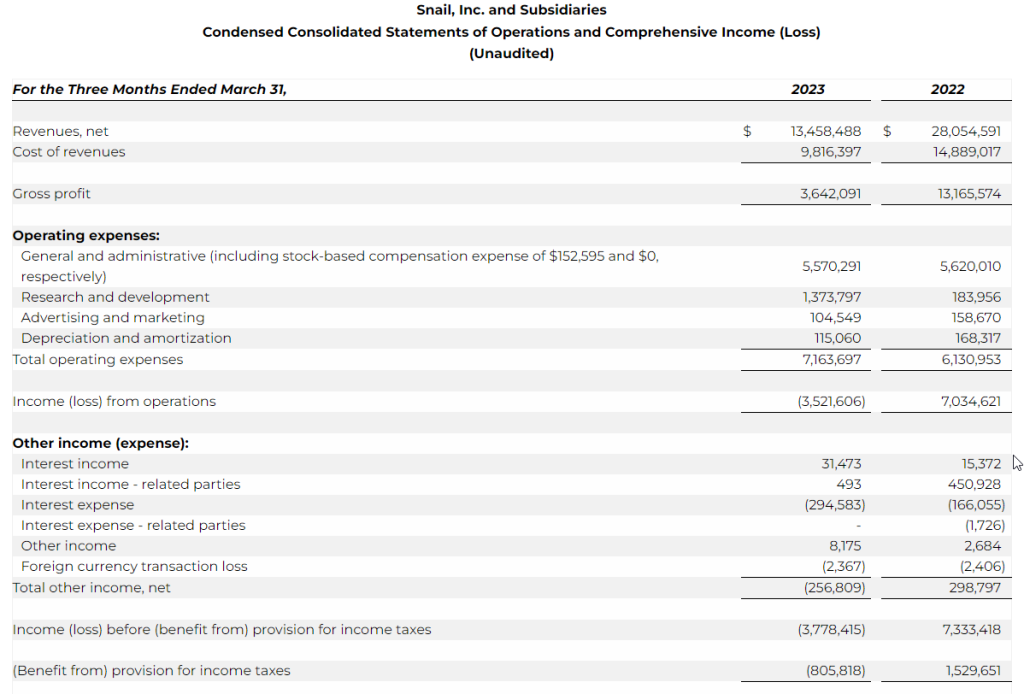

Q1 results. The company reported quarterly results largely in line with our expectations. Q1 revenue was $13.5 million and adj. EBITDA was a loss of $3.4 million, compared with our estimates of $12.5 million and a loss of $2.6 million, respectively.

ARK Remastered. The release of a remastered version of its popular game ARK is expected later this year. The game, which will be remastered using Unreal Engine 5, will be called ARK: Survival Ascended, and will include the entirety of ARK: Survival Evolved, including previously issued DLCs. Core fans appear excited about the upcoming release, which we believe could offer a favorable revenue boost during the lead up to the ARK 2 release in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CULVER CITY, Calif., May 10, 2023 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment, today announced financial results for the three months ended March 31, 2023.

Jim Tsai, Chief Executive Officer of Snail, commented: “We are thrilled by the ongoing engagement surrounding our ARK series. We have faced the challenging choice of postponing the release of ARK 2 until next year to ensure that we devote ample time to enhancing the game’s quality and providing an unparalleled gaming experience for our players.”

Tsai continued, “We have exciting plans to launch an expanded edition of the ARK series, which will undergo a remastering process using Unreal Engine 5. This remastered series will offer an extraordinary experience to both new and existing players, while also establishing a solid foundation for a successful launch of ARK 2.”

First Quarter 2023 and Subsequent Financial and Business Highlights

Revenue was $13.5 million for the three months ended March 31, 2023, compared to revenue of $28.1 million in the prior year period, representing a decrease of $14.6 million. The decrease in net revenues was due to a decrease in sales of ARK, attributable to a decrease in the average sales price per unit, and the recognition of additional revenue from deferred revenue and one-time payments related to contracts with certain platforms that did not repeat in the three months ended March 31, 2023. ARK sales decreased by $3.1 million, deferred revenue from contracts decreased by $2.5 million, and one-off contract payments decreased by $8.5 million. Sales of the Company’s smaller titles decreased by a collective $0.7 million. These decreases in the Company’s smaller titles were partially offset by $0.2 million in revenue related to West Hunt.

ARK: Survival Evolved. In the three months ended March 31, 2023, ARK: Survival Evolved averaged a total of 276,144 daily active users (“DAUs”) versus 257,168 DAUs in the prior year period.

ARK units sold increased for the first quarter 2023 compared to the same period last year; approximately 1.6 million vs. 1.2 million, respectively.

Through March 31, 2023, total playtime for the ARK franchise amounted to 3.2 billion hours.

The Company sold an additional 0.4 million units of its ARK franchise in the three-month period ended March 31, 2023, versus the prior year period, due to the increase in sales promotions offered by our platform partners during the period.

The Company expects to release ARK: Survival Ascended later this year. ARK: Survival Ascended is the entire base game of ARK: Survival Evolved, remastered with Unreal Engine 5 and expanded numerous times. It’ll feature The Island, Survival of the Fittest, and a collection of downloadable content (“DLC”) maps released over time.

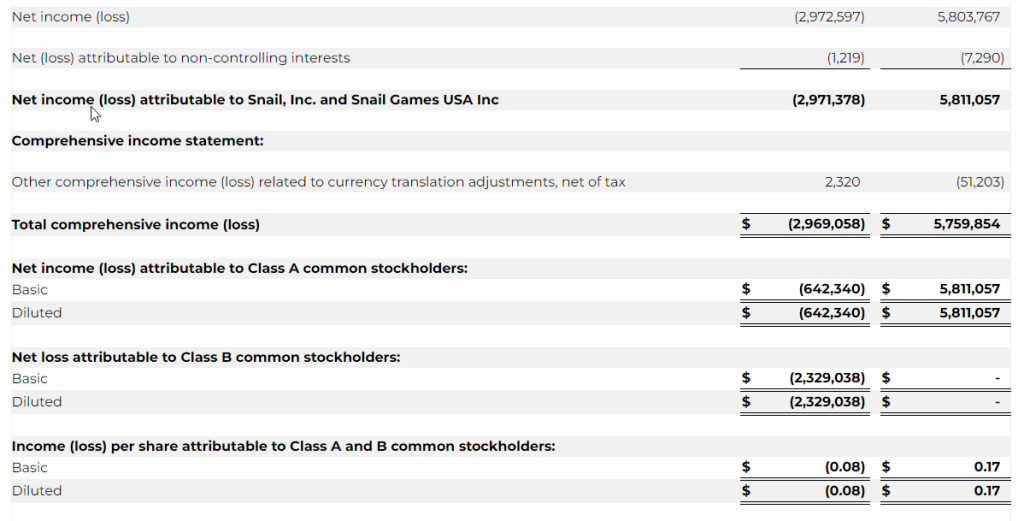

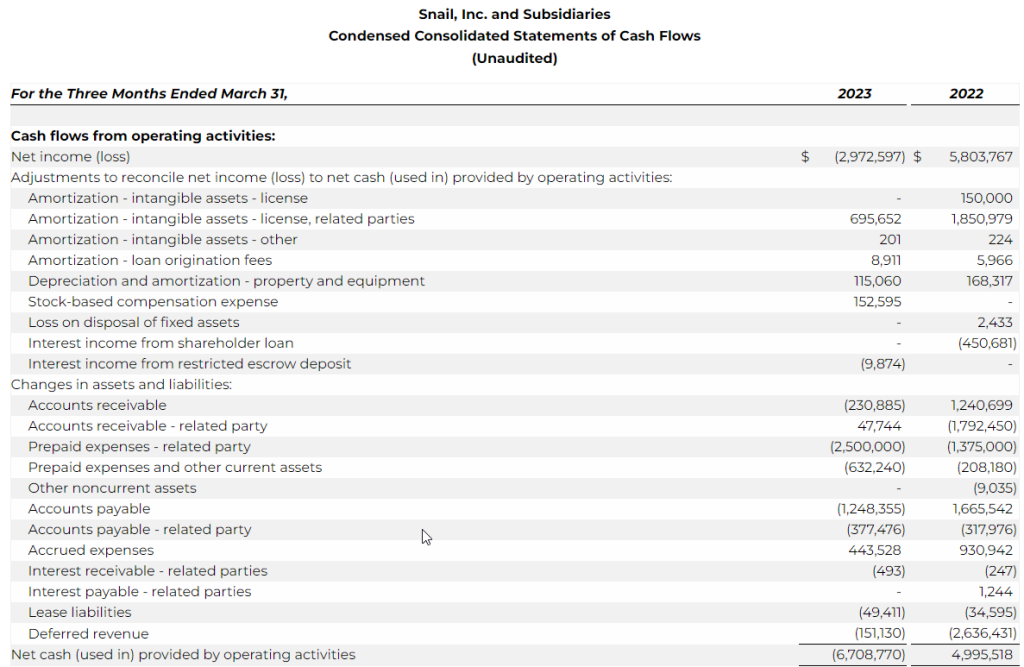

Net loss was $3.0 million for the three months ended March 31, 2023 as compared to a net income of $5.8 million for the three months ended March 31, 2022, representing a decrease of $8.8 million. The decrease was primarily due to a decrease in revenue of $14.6 million, an increase in research and development expense of $1.2 million, a net decrease in interest income – related parties of $0.5 million, an increase in interest expense of $0.1 million, offset by a decrease in royalties of $3.2 million, a decrease in license cost and license right amortization of $1.3 million, a decrease in merchant and engine fees of $0.5 million, and a decrease in the Company’s tax provision of $2.3 million.

Bookings for the three months ended March 31, 2023 were $13.3 million, a decrease of $12.2 million, or 47.6%, compared to the three months ended March 31, 2022. The decrease was primarily the result of decreased ARK revenues in 2023 due to the factors mentioned above.

Earnings before interest, taxes, depreciation and amortization (“EBITDA”) for the first quarter of 2023 was a loss of $3.4 million compared to a gain of $7.2 million in the prior year period.

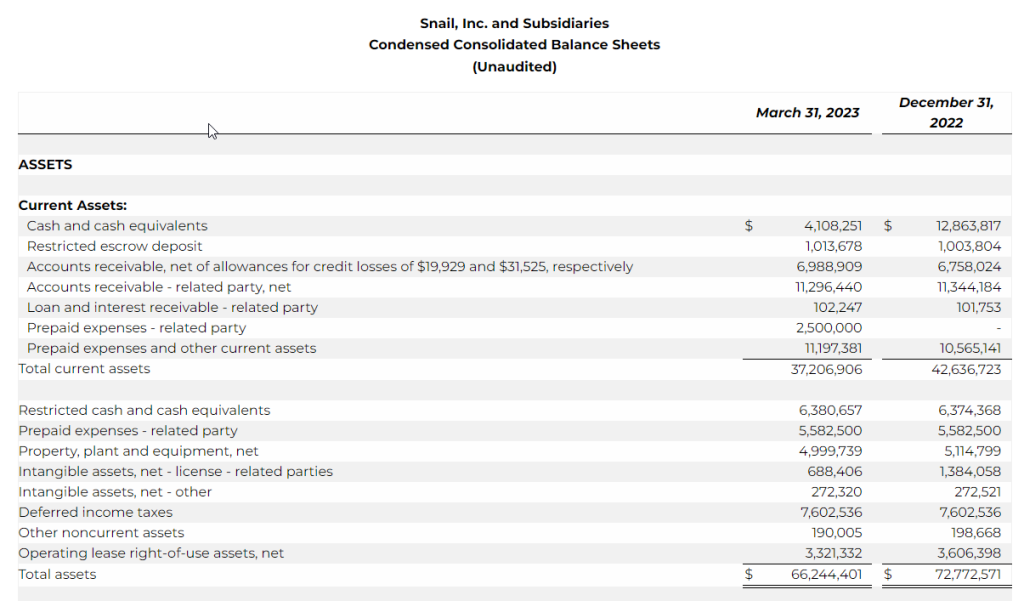

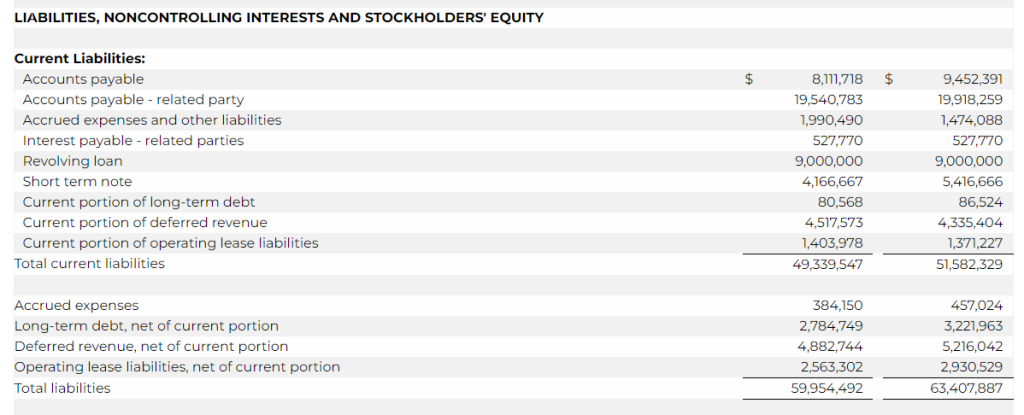

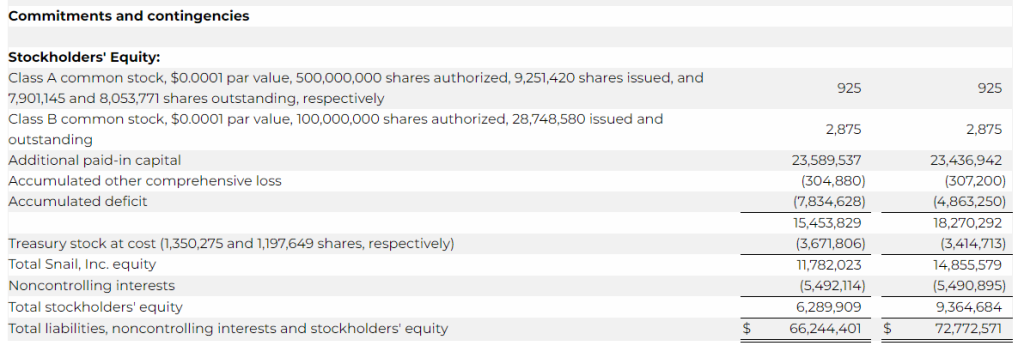

As of March 31, 2023, unrestricted cash was $4.1 million versus $12.9 million as of December 31, 2022.

Use of Non-GAAP Financial Measures

In addition to the financial results determined in accordance with U.S. generally accepted accounting principles, or GAAP, Snail believes Bookings and EBITDA, as non-GAAP measures, are useful in evaluating its operating performance. Bookings and EBITDA are non-GAAP financial measures that are presented as supplemental disclosures and should not be construed as alternatives to net income (loss) or revenue as indicators of operating performance, nor as alternatives to cash flow provided by operating activities as measures of liquidity, both as determined in accordance with GAAP. Snail supplementally presents Bookings and EBITDA because they are key operating measures used by management to assess financial performance. Bookings adjusts for the impact of deferrals and, Snail believes, provides a useful indicator of sales in a given period. EBITDA adjusts for items that Snail believes do not reflect the ongoing operating performance of its business, such as certain non-cash items, unusual or infrequent items or items that change from period to period without any material relevance to its operating performance. Management believes Bookings and EBITDA are useful to investors and analysts in highlighting trends in Snail’s operating performance, while other measures can differ significantly depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which Snail operates and capital investments.

Bookings is defined as the net amount of products and services sold digitally or physically in the period. Bookings is equal to revenues excluding the impact from deferrals. Below is a reconciliation of total net revenue to Bookings, the closest GAAP financial measure.

We define EBITDA as net income (loss) before (i) interest expense, (ii) interest income, (iii) income tax provision (benefit from) and (iv) depreciation and amortization expense. The following table provides a reconciliation from net income (loss) to EBITDA:

Webcast Details

The Company will host a webcast at 5:00 PM ET today to discuss the first quarter 2023 financial results. Participants may access the live webcast and replay on the Company’s investor relations website at https://investor.snail.com/. The earnings call may also be accessed by dialling 1 (877) 451-6152 from the United States, or by dialling 1 (201) 389-0879 internationally.

About Snail, Inc.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Forward-Looking Statements This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future results of Snail’s business, financial condition, results of operations, liquidity, plans and objectives. The statements Snail makes regarding the following matters are forward-looking by their nature: growth prospects and strategies; launching new games and additional functionality to games that are commercially successful; expectations regarding significant drivers of future growth; its ability to retain and increase its player base and develop new video games and enhance existing games; competition from companies in a number of industries, including other casual game developers and publishers and both large and small, public and private Internet companies; its ability to attract and retain a qualified management team and other team members while controlling its labor costs; its relationships with third-party platforms such as Xbox Live and Game Pass, PlayStation Network, Steam, Epic Games Store, My Nintendo Store, the Apple App Store, the Google Play Store and the Amazon Appstore; the size of addressable markets, market share and market trends; its ability to successfully enter new markets and manage international expansion; protecting and developing its brand and intellectual property portfolio; costs associated with defending intellectual property infringement and other claims; future business development, results of operations and financial condition; the ongoing conflict involving Russia and Ukraine on its business and the global economy generally; rulings by courts or other governmental authorities; the Share Repurchase Program, including expectations regarding the timing and manner of repurchases made under the program; its plans to pursue and successfully integrate strategic acquisitions; assumptions underlying any of the foregoing.

Further information on risks, uncertainties and other factors that could affect Snail’s financial results are included in its filings with the Securities and Exchange Commission (the “SEC”) from time to time, annual reports on Forms 10-K and quarterly reports on 10-Q filed, or to be filed, with the SEC. You should not rely on these forward-looking statements, as actual outcomes and results may differ materially from those expressed or implied in the forward-looking statements as a result of such risks and uncertainties. All forward-looking statements in this press release are based on management’s beliefs and assumptions and on information currently available to Snail, and Snail does not assume any obligation to update the forward-looking statements provided to reflect events that occur or circumstances that exist after the date on which they were made.

CULVER CITY, Calif., May 09, 2023 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL), a leading, global independent developer and publisher of interactive digital entertainment, announced today that it will report financial results for the first quarter ended March 31, 2023 on Wednesday, May 10, 2023, after the U.S. stock market closes. Management will host a conference call and webcast on the same day at 5:00 p.m. ET to discuss the results.

Participants may access the live webcast and replay on the Company’s investor relations website at https://investor.snail.com/. The earnings call may also be accessed by dialing 1 (877) 451-6152 from the United States, or by dialing 1 (201) 389-0879 internationally.

About Snail, Inc. Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs, and mobile devices.

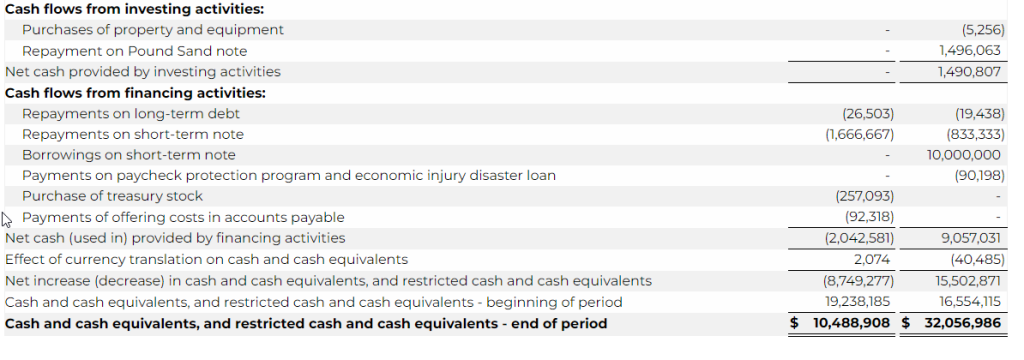

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (the “company”)(NASDAQ: SALM) released its results for the three months ended March 31, 2023.

First Quarter 2023 Results

For the three months ended March 31, 2023 compared to the three months ended March 31, 2022:

Consolidated

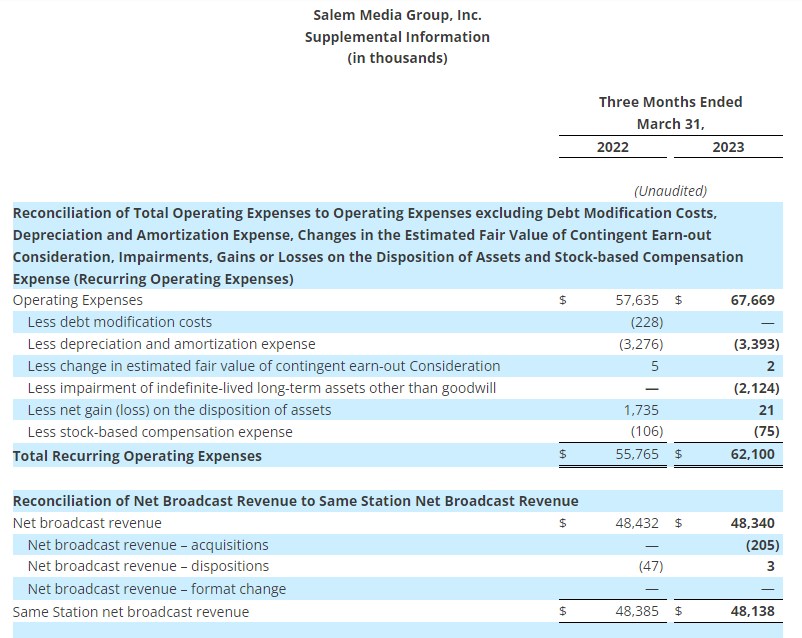

Total revenue increased 1.4% to $63.5 million from $62.6 million;

Total operating expenses increased 17.4% to $67.7 million from $57.6 million;

Operating expenses, excluding stock-based compensation expense, debt modification costs, gains and losses on the sale or disposition of assets, impairments, depreciation expense and amortization expense (1) increased 11.4% to $62.1 million from $55.8 million;

The company had an operating loss of $4.2 million as compared to operating income of $5.0 million;

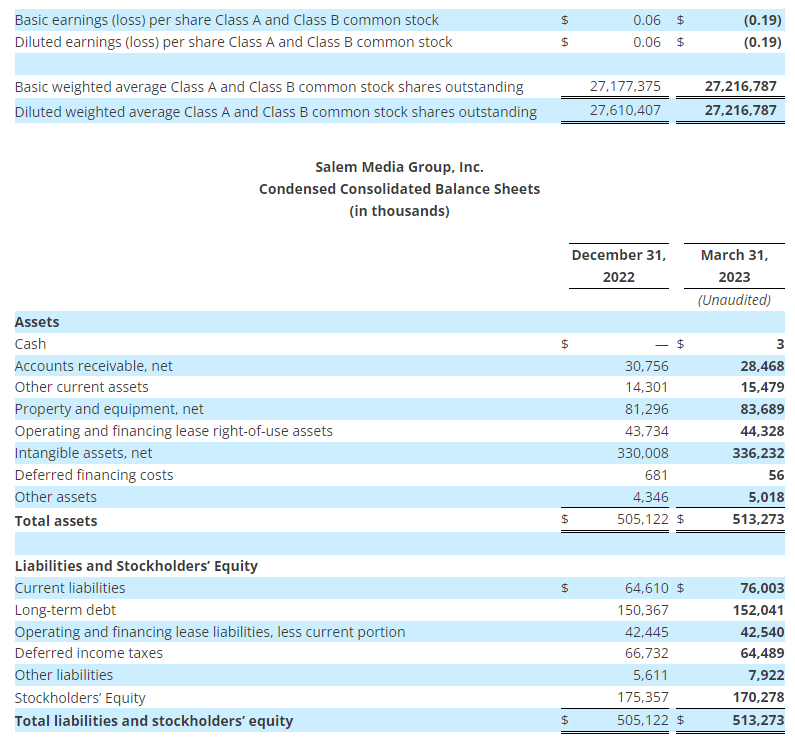

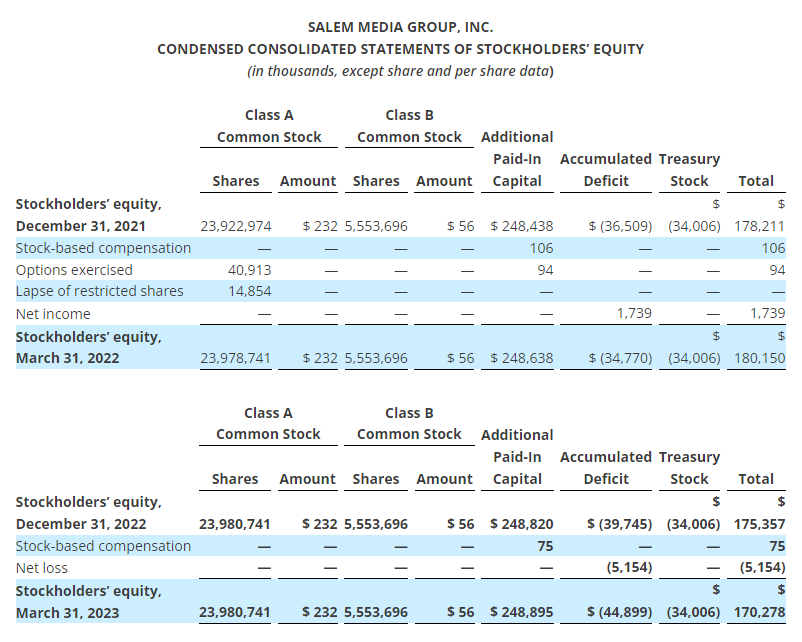

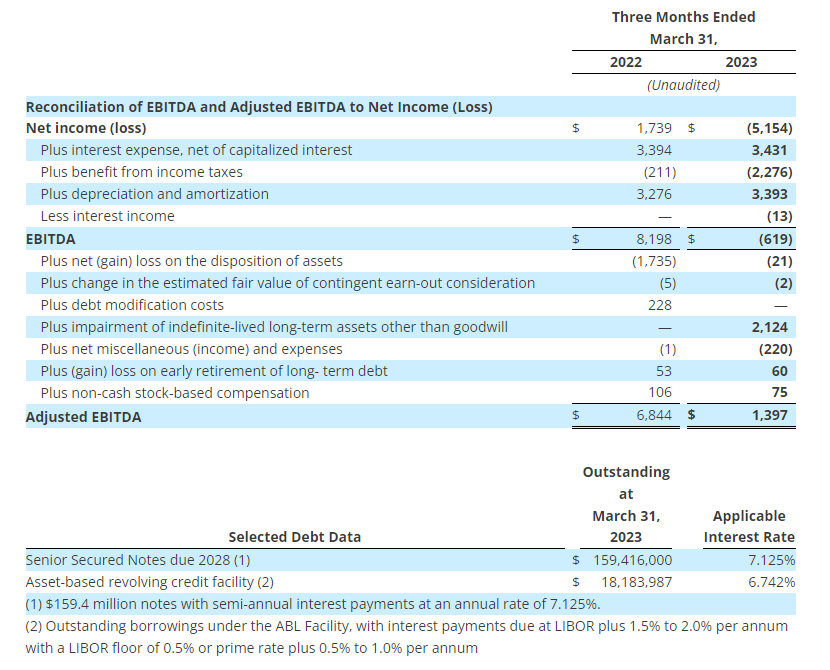

The company had a net loss of $5.2 million, or $0.19 net loss per share, compared to net income of $1.7 million, or $0.06 net income per diluted share;

EBITDA (1) decreased 107.6% to $(0.6) million from $8.2 million; and

Adjusted EBITDA (1) decreased 79.6% to $1.4 million from $6.8 million.

Broadcast

Net broadcast revenue decreased 0.2% to $48.3 million from $48.4 million;

Station Operating Income (“SOI”) (1) decreased 46.4% to $5.5 million from $10.3 million;

Same Station (1) net broadcast revenue decreased 0.5% to $48.1 million from $48.4 million; and

Same Station SOI (1) decreased 41.6% to $6.0 million from $10.3 million.

Digital Media

Digital media revenue increased 2.0% to $10.5 million from $10.3 million; and

Digital Media Operating Income (1) decreased 17.0% to $1.5 million from $1.8 million.

Publishing

Publishing revenue increased 19.7% to $4.6 million from $3.9 million; and

Publishing Operating Loss (1) increased 24.9% to $0.7 million from $0.6 million.

Included in the results for the three months ended March 31, 2023 are:

A $2.1 million ($1.6 million, net of tax, or $0.06 per share) impairment charge to the value of broadcast license related to the acquisition of radio station WMYM-AM in Miami, Florida;

A $0.1 million loss on the early retirement of long-term debt associated with the 2024 Notes; and

A $0.1 million non-cash compensation charge related to the expensing of stock options.

Included in the results for the three months ended March 31, 2022 are:

A $1.7 million ($1.3 million, net of tax, or $0.05 per diluted share) net gain on the disposition of assets related primarily to the gain on sale of land in Phoenix, Arizona offset by various fixed asset disposals; and

A $0.2 million ($0.2 million, net of tax, or $0.01 per share) charge for debt modification costs; and

A $0.1 million non-cash compensation charge ($0.1 million, net of tax) related to the expensing of stock options.

Per share numbers are calculated based on 27,216,787 diluted weighted average shares for the three months ended March 31, 2023, and 27,610,407 diluted weighted average shares for the three months ended March 31, 2022.

Balance Sheet

As of March 31, 2023, the company had $159.4 million outstanding on the 7.125% senior secured notes due 2028 (“2028 Notes”) and $18.2 million outstanding on the ABL facility.

Acquisitions and Divestitures

The following transactions were completed since January 1, 2023:

The company invested $1.5 million in a limited liability company that will own, distribute, and market a motion picture.

On March 24, 2023, the company closed on the acquisition of Digital Felt Productions and its digital content library for $25,000 in cash.

On February 1, 2023, the company acquired the George Gilder Report and other digital newsletters and related website assets. The company assumed the deferred subscription liabilities paying no cash at the time of closing. The purchase price is 25% of net revenue generated from sales of most Eagle Financial products during the next year to subscribers who are on George Gilder subscriber lists that are not already on Eagle Financial lists.

On January 10, 2023, the company closed on the acquisition of radio stations WWFE-AM, WRHC-AM and two FM translators in Miami, Florida for $3.0 million in cash. The Asset Purchase Agreement (“APA”) was amended for the company to acquire only the radio stations and translators for $3.0 million, a related party to acquire the land directly from the seller for $2.0 million, and the company to have an option to purchase the land from the related party pursuant to an option to purchase real estate agreement. The company’s executive officers, who have no relationship with the related party, began negotiations for the related party lease agreements and option agreements, subject to final approval by the company’s Audit Committee pursuant to its related party transaction policy. The option to purchase real estate agreement was approved by the company’s Audit Committee on March 1, 2023.

On January 6, 2023 the company closed on the acquisition of radio station WMYM-AM and an FM translator in Miami, Florida for $3.2 million in cash. The company began operating the radio station under a Time Brokerage Agreement (“TBA”) beginning on November 16, 2022. The APA was amended for the company to acquire only the radio station and translator for $3.2 million, a related party to acquire the land directly from the seller for $1.8 million, and the company to have an option to purchase the land from the related party pursuant to an option to purchase real estate agreement. The company’s executive officers, who have no relationship with the related party, began negotiations for the related party lease agreements and option agreements, subject to final approval by the company’s Audit Committee pursuant to its related party transaction policy. The option to purchase real estate agreement was approved by the company’s Audit Committee on March 1, 2023.

Pending transactions:

In June 2022 the company entered into agreements to sell radio stations KLFE-AM and KNTS-AM in Seattle, Washington for $0.7 million subject to approval of the Federal Communications Commission. Radio station KLFE-AM is being programmed under a TBA as of August 1, 2022.

Conference Call Information

The company will host a teleconference to discuss its results on May 9, 2023 at 4:00 p.m. Central Time. To access the teleconference, please dial (888) 770-7291, and then ask to be joined into the Salem Media Group First Quarter 2023 call or listen via the investor relations portion of the company’s website, located at investor.salemmedia.com. A replay of the teleconference will be available through May 23, 2023 and can be heard by dialing (800) 770-2030, passcode 2413416 or on the investor relations portion of the company’s website, located at investor.salemmedia.com.

Follow us on Twitter @SalemMediaGrp.

Second Quarter 2023 Outlook

For the second quarter of 2023, the company is projecting total revenue to decline between 5% and 7% from the second quarter 2022 total revenue of $68.7 million. The company is also projecting operating expenses before gains or losses on the sale or disposal of assets, stock-based compensation expense, legal settlement, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation expense and amortization expense (“Recurring Operating Expenses”) to increase between 3% and 6% compared to the second quarter of 2022 Recurring Operating Expenses of $60.0 million.

A reconciliation of Recurring Operating Expenses (a non-GAAP measure) to the most directly comparable GAAP measure is not available without unreasonable efforts on a forward-looking basis due to the potential high variability, complexity and low visibility with respect to the charges excluded from this non-GAAP financial measure, in particular, the change in the estimated fair value of earn-out consideration, impairments and gains or losses from the disposition of fixed assets. The company expects the variability of the above charges may have a significant, and potentially unpredictable, impact on its future GAAP financial results.

About Salem Media Group, Inc.

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Forward-Looking Statements

Statements used in this press release that relate to future plans, events, financial results, prospects or performance are forward-looking statements as defined under the Private Securities Litigation Reform Act of 1995. Actual results may differ materially from those anticipated as a result of certain risks and uncertainties, including but not limited to the ability of the company to close and integrate announced transactions, market acceptance of the company’s radio station formats, competition from new technologies, inflation and other adverse economic conditions, and other risks and uncertainties detailed from time to time in the company’s reports on Forms 10-K, 10-Q, 8-K and other filings filed with or furnished to the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The company undertakes no obligation to update or revise any forward-looking statements to reflect new information, changed circumstances or unanticipated events.

(1) Regulation G

Management uses certain non-GAAP financial measures defined below in communications with investors, analysts, rating agencies, banks and others to assist such parties in understanding the impact of various items on its financial statements. The company uses these non-GAAP financial measures to evaluate financial results, develop budgets, manage expenditures and as a measure of performance under compensation programs.

The company’s presentation of these non-GAAP financial measures should not be considered as a substitute for or superior to the most directly comparable financial measures as reported in accordance with GAAP.

Regulation G defines and prescribes the conditions under which certain non-GAAP financial information may be presented in this earnings release. The company closely monitors EBITDA, Adjusted EBITDA, Station Operating Income (“SOI”), Same Station net broadcast revenue, Same Station broadcast operating expenses, Same Station Operating Income, Digital Media Operating Income, Publishing Operating Loss, and operating expenses excluding gains or losses on the disposition of assets, stock-based compensation, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation and amortization, all of which are non-GAAP financial measures. The company believes that these non-GAAP financial measures provide useful information about its core operating results, and thus, are appropriate to enhance the overall understanding of its financial performance. These non-GAAP financial measures are intended to provide management and investors a more complete understanding of its underlying operational results, trends and performance.

The company defines Station Operating Income (“SOI”) as net broadcast revenue minus broadcast operating expenses. The company defines Digital Media Operating Income as net Digital Media Revenue minus Digital Media Operating Expenses. The company defines Publishing Operating Loss as net Publishing Revenue minus Publishing Operating Expenses. The company defines EBITDA as net income before interest, taxes, depreciation, and amortization. The company defines Adjusted EBITDA as EBITDA before gains or losses on the disposition of assets, before debt modification costs, before changes in the estimated fair value of contingent earn-out consideration, before impairments, before net miscellaneous income and expenses, before (gain) loss on early retirement of long-term debt and before non-cash compensation expense. SOI, Digital Media Operating Income, Publishing Operating Loss, EBITDA and Adjusted EBITDA are commonly used by the broadcast and media industry as important measures of performance and are used by investors and analysts who report on the industry to provide meaningful comparisons between broadcasters. SOI, Digital Media Operating Income, Publishing Operating Loss, EBITDA and Adjusted EBITDA are not measures of liquidity or of performance in accordance with GAAP and should be viewed as a supplement to and not a substitute for or superior to its results of operations and financial condition presented in accordance with GAAP. The company’s definitions of SOI, Digital Media Operating Income, Publishing Operating Loss, EBITDA and Adjusted EBITDA are not necessarily comparable to similarly titled measures reported by other companies.

The company defines Same Station net broadcast revenue as broadcast revenue from its radio stations and networks that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. The company defines Same Station broadcast operating expenses as broadcast operating expenses from its radio stations and networks that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. The company defines Same Station SOI as Same Station net broadcast revenue less Same Station broadcast operating expenses. Same Station operating results include those stations that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. Same Station operating results for a full calendar year are calculated as the sum of the Same Station operating results for each of the four quarters of that year. The company uses Same Station operating results, a non-GAAP financial measure, both in presenting its results to stockholders and the investment community, and in its internal evaluations and management of the business. The company believes that Same Station operating results provide a meaningful comparison of period over period performance of its core broadcast operations as this measure excludes the impact of new stations, the impact of stations the company no longer owns or operates, and the impact of stations operating under a new programming format. The company’s presentation of Same Station operating results is not intended to be considered in isolation or as a substitute for the financial information prepared and presented in accordance with GAAP. The company’s definition of Same Station operating results is not necessarily comparable to similarly titled measures reported by other companies.

For all non-GAAP financial measures, investors should consider the limitations associated with these metrics, including the potential lack of comparability of these measures from one company to another.

The Supplemental Information tables that follow the condensed consolidated financial statements provide reconciliations of the non-GAAP financial measures that the company uses in this earnings release to the most directly comparable measures calculated in accordance with GAAP. The company uses non-GAAP financial measures to evaluate financial performance, develop budgets, manage expenditures, and determine employee compensation. The company’s presentation of this additional information is not to be considered as a substitute for or superior to the directly comparable measures as reported in accordance with GAAP.

The company defines EBITDA (1) as net income before interest, taxes, depreciation, and amortization. The table below presents a reconciliation of EBITDA (1) to Net Income (Loss), the most directly comparable GAAP measure. EBITDA (1) is a non-GAAP financial performance measure that is not to be considered a substitute for or superior to the directly comparable measures reported in accordance with GAAP. The company defines Adjusted EBITDA (1) as EBITDA (1) before gains or losses on the disposition of assets,before debt modification costs, before changes in the estimated fair value of contingent earn-out consideration, before impairments, before net miscellaneous income and expenses, before (gain) loss on early retirement of long-term debt, and before non-cash compensation expense. The table below presents a reconciliation of Adjusted EBITDA (1) to Net Income (Loss), the most directly comparable GAAP measure. Adjusted EBITDA (1) is a non-GAAP financial performance measure that is not to be considered a substitute for or superior to the directly comparable measures reported in accordance with GAAP.

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In-line Q1 results. The company reported Q1 revenue of $63.5 million, beating our estimate of $62 million by 2.4%. Revenue in the quarter was driven by slightly better than expected broadcast and publishing revenues. Adj. EBITDA of $1.4 million was largely in line with our estimate of $1.7 million.

Sizeable cost reductions. The company eliminated $5 million in annualized costs in the first quarter. The savings were included in management issued guidance for Q2 and full year 2023, and are expected to have an equal impact in each quarter moving forward. We believe that the company is managing cash flow while investing in its Digital businesses and into Salem News.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Lee Enterprises, Incorporated provides local news, information, and advertising primarily in midsize markets in the United States. It publishes 49 daily newspapers, as well as offers 300 weekly newspapers and specialty publications in 23 states. The company also provides online advertising and services; and online infrastructure and online publishing services for approximately 1,500 daily and weekly newspapers and shoppers. In addition, it offers commercial printing services. The company has a strategic alliance with Yahoo!, Inc. to provide its classified employment advertising customer base the opportunity to post job listings and other employment products on Yahoo!�s HotJobs national platform. Lee Enterprises, Incorporated was founded in 1890 and is based in Davenport, Iowa.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Post quarterly review. The company delivered a solid fiscal second quarter in spite of heavy economic headwinds and secular pressure on its print legacy business. Notably, its Digital businesses performed well, and its digital subscriber growth continues to lead the industry. We believe that the company will be able to achieve its FY 2023 revenue and adj. EBITDA guidance given its attention to costs.

Reiterates guidance. Management reiterated its previously issued FY 2023 guidance of $270 to $285 million in digital revenues, $94 to $100 million in adj. EBITDA, 632,000 digital subscribers and cash costs in the range of $610 to $620 million. While management did not provide guidance for print revenues, we are flowing through Q2 operating results to our full year 2023 forecast.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gray Television is a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets in the United States. Our television stations serve 113 television markets that collectively reach approximately 36 percent of US television households. This portfolio includes 80 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station. We also own video program companies Raycom Sports, Tupelo Honey, PowerNation Studios and Third Rail Studios.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q1 results. The company reported quarterly revenue of $801 million, 2.9% better than our estimate of $778.5 million, and adj. EBITDA of $162 million, which was in line with our estimate. Results are illustrated in Figure #1 Q1 Results. While all business segments reported stronger than expected revenues, political revenues of $8 million was the biggest surprise versus our estimate of $2 million.

Favorable advertising momentum. In spite of the macroeconomic headwinds core advertising is pacing ahead of last year. We believe that a good portion of its positive advertising momentum is coming from revenue synergies. In addition, Auto advertising appears to be rebounding, pacing up double-digits. Looking ahead, the company is also likely to benefit from annual Net Retransmission revenue growth, when it renews 58% of its MVPD contracts later this year. Moreover, management expects Net Retransmission revenue growth to accelerate in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

MIAMI, May 08, 2023 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world, will report its financial results for the first fiscal quarter of 2023 on Thursday, May 11, 2023, after market close. Management will host a conference call and webcast on the same day at 6:00 p.m. ET to discuss the results.

Participants may access the live webcast on the Company’s investor relations website at https://ir.motorsportgames.com under “Events.” The call may also be accessed by dialing 1 (844) 826-3033 from the U.S., or by dialing 1 (412) 317-5185 internationally.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Gray Television is a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets in the United States. Our television stations serve 113 television markets that collectively reach approximately 36 percent of US television households. This portfolio includes 80 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station. We also own video program companies Raycom Sports, Tupelo Honey, PowerNation Studios and Third Rail Studios.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q1 results. The company reported quarterly revenue of $801 million, 2.9% better than our estimate of $778.5 million, and adj. EBITDA of $162 million, which was in line with our estimate. Results are illustrated in Figure #1 Q1 Results. While all business segments reported stronger than expected revenues, political revenues of $8 million was the biggest surprise versus our estimate of $2 million.

Favorable momentum. In spite of the macroeconomic headwinds, Q2 core advertising pacing is up a surprising 4%. We believe that a good portion of its positive advertising momentum is coming from revenue synergies. In addition, Auto advertising appears to be rebounding, pacing up double-digits. Looking ahead, the company is also likely to benefit from annual Net Retransmission revenue growth, when it renews the majority of its MVPD contracts later this year. Moreover, management expects Net Retransmission revenue growth to accelerate in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.