Reddit, the popular online platform founded in 2005, has filed for an initial public offering (IPO) and plans to list on the New York Stock Exchange under the ticker symbol “RDDT.” This will be the first major social media IPO since 2019. Reddit is currently majority owned by publisher Advance Publications, with Chinese tech giant Tencent and OpenAI CEO Sam Altman also holding significant stakes.

In an unconventional move, Reddit plans to reserve some shares for its top content creators and moderators, based on their “karma” scores. This reflects Reddit’s community-driven ethos and desire to reward loyal users. However, it raises questions around equitable access for average retail investors.

With over 52 million daily active users, Reddit has grown into one of the world’s largest online communities. Its success has been built on a decentralized model where users create and manage individual forums called “subreddits.” This allows niche interests to flourish but also gives rise to controversial content.

Reddit came under fire during the 2021 GameStop trading frenzy, when its WallStreetBets forum helped drive a massive short squeeze. This demonstrated Reddit’s influence but also put the company under regulatory scrutiny. More recently, new monetization efforts like increased advertising and data licensing deals have sparked backlash among users.

The IPO comes amid a tech downturn that has battered advertising revenue. Reddit is not yet profitable, posting a $90 million net loss over the last three months of 2023. Going public will provide capital for growth but also increase pressure to boost monetization and content moderation.

Key challenges for Reddit’s leadership will be balancing community values with investors’ profit expectations. Allowing controversial content has been integral to Reddit’s appeal, but this could jeopardize advertising deals. The IPO is a milestone for Reddit, reflecting its cultural significance, but keeping its identity intact while becoming financially sustainable will be critical.

Overall, the offering is a test of whether an ad-based platform predicated on decentralized, user-generated content can thrive as a public company. Reddit’s IPO will be watched closely by tech investors and observers worldwide. Its success or failure could shape the future trajectory of social platforms.

The biotech sector is witnessing a dynamic start to the year 2024, with companies such as Alto Neuroscience (ANRO) and Fractyl Health (GUTS) surpassing expectations in their initial public offerings (IPOs).

Alto Neuroscience’s Upsized IPO

Alto Neuroscience today announced the pricing of its upsized IPO, offering 8,040,000 shares of common stock at $16.00 per share. The aggregate gross proceeds are estimated to be approximately $128.6 million. This figure exceeds Alto’s earlier projection of $89 million to $103 million, showcasing strong investor confidence. The shares, traded under the ticker symbol ANRO, are set to commence trading on the NYSE, with the offering expected to close on February 6.

The substantial funds raised will propel Alto’s research and development efforts, primarily supporting the advancement of its lead asset, ALTO-100. This oral small molecule inhibitor of BDNF is currently undergoing a Phase II study for major depressive disorder. Additionally, the IPO proceeds will contribute to the progress of Alto’s other depression asset, ALTO-300, and the Phase I PDE4 asset, ALTO-101, targeted at neurodegenerative and neuropsychiatric conditions.

Fractyl Health’s Successful Debut

In a parallel success story, Fractyl Health has announced the pricing of its IPO, offering 7,333,333 shares of common stock at $15.00 per share. The total gross proceeds amount to approximately $110.0 million, surpassing the initial expectation of $99 million. Fractyl Health, trading under the ticker symbol GUTS on the Nasdaq Global Market, is scheduled to debut on Friday, with the IPO closing on February 6.

The lead product candidate for Fractyl, named Revita, is an outpatient endoscopic procedural therapy utilizing hydrothermal ablation to remodel the dysfunctional duodenal lining and restore metabolic health. Revita is currently in a pivotal study for insulin-treated type 2 diabetes, with anticipated data release in the fourth quarter of 2024.

Mark your calendars! Don’t miss Noble Capital Markets’ Emerging Growth Virtual Healthcare Equity Conference on April 17-18. This exclusive virtual event connects investors with 50 leading public biotech, healthcare services, and medical device companies. Presenting company slots are available…Read More

Positive Industry Trends

Alto Neuroscience and Fractyl Health’s successful IPOs follow in the footsteps of CG Oncology, which recently announced an upsized IPO of $380 million, and ArriVent Biopharma, following suit with its own $175 million offering. These developments underscore the current investor enthusiasm and optimism surrounding biotech companies, indicating a positive trajectory for the sector in 2024.

The robust performance of Alto Neuroscience and Fractyl Health in the IPO market exemplifies the strong start for the biotech sector in 2024. These successful offerings not only provide these companies with the necessary capital for their innovative projects but also reflect a broader trend of confidence and interest from investors in the biotech industry. As the year progresses, these companies and their groundbreaking initiatives will undoubtedly be closely watched by industry insiders and investors alike.

The New Year has kicked off with a bang in biotech, as CG Oncology has completed the first initial public offering in the space for 2024. The cancer-focused biotech raised a whopping $380 million in its IPO on the Nasdaq, sailing past its initial target range of $181 million.

CG Oncology priced its shares at $19 apiece, above the $16-18 range it had set ahead of the IPO. The impressive deal is being viewed by many analysts and investors as a positive indicator that the biotech IPO market is rebounding in 2024 after a relatively slow 2023.

The robust demand for CG Oncology stock reflects renewed optimism and openness to investing in early-stage biotech companies, especially those with innovative science and strong leadership teams.

CG Oncology is developing a novel oncolytic virus therapy known as cretostimogene grenadenorepvec for the treatment of non-muscle invasive bladder cancer. Oncolytic viruses represent an exciting new approach in cancer treatment, wherein specially engineered viruses are able to infect and destroy cancer cells directly while also stimulating anti-tumor immune responses.

Cretostimogene grenadenorepvec is an adenovirus that has been engineered to replicate selectively in bladder cancer cells and stimulate the immune system by expressing granulocyte-macrophage colony-stimulating factor (GM-CSF). Early stage clinical data have shown promising signs of efficacy.

The company plans to use the IPO proceeds to fund a Phase 3 clinical trial of its lead candidate as well as earlier stage pipeline programs. Success in the Phase 3 study could support regulatory approval and commercialization.

CG Oncology was founded in 2018 by a veteran team of biotech entrepreneurs and scientists. The company pursued a pre-IPO crossover financing round in 2022, enabling it to build momentum heading into its public debut.

The IPO success places CG Oncology in a strong position to advance its pipeline. With the influx of capital, the company will be able to aggressively pursue its clinical development plans without relying heavily on external partners.

Moreover, the validation and visibility provided by being a public company can potentially help CG Oncology forge productive collaborations and access additional funding in the future.

Looking ahead, the positive investor response to CG Oncology seems likely to pave the way for more biotech IPOs in 2024. A robust IPO market provides fuel for innovation and discoveries that can transform patient lives.

The biotech sector sputtered in 2022, with only around 20 IPOs completed versus more than 50 in 2021. However, sentiment appears to be shifting, perhaps signaling sunnier days ahead.

In addition to favorable market conditions, biotech companies pursuing IPOs seem to be taking valuable lessons from 2022 by tightening focus on fundamentals like drug efficacy and visibility on clinical milestones.

Other than CG Oncology, a host of biotechs have already filed with SEC intentions to go public in 2024, spanning exciting areas like gene therapy, neurology, and synthetic biology.

With fresh capital and investor enthusiasm, the next generation of biotech companies can pursue ambitious goals to develop innovative medicines. More early-stage companies may also gain the funding needed to initiate or advance clinical trials.

CG Oncology’s big IPO pop reflects the right combination of cutting-edge science, unmet medical need, and strong leadership. This formula will likely be replicated by other emerging biotech stars in the making.

In all, the successful CG Oncology IPO kicks off 2024 as a promising year for biotech funding, innovation, and progress against once intractable diseases. Investors and industry observers will be tracking the IPO market closely through the year for signs of sustained momentum. If the appetite for compelling biotech stories persists, it could drive a much-needed renaissance helping to unlock new medical frontiers.

Mark your calendars! Don’t miss Noble Capital Markets’ Emerging Growth Virtual Healthcare Equity Conference April 17-18. This exclusive virtual event connects investors with 50 leading public biotech, healthcare services, and medical device companies. Presenting company slots are available.

Chinese fast fashion juggernaut Shein has filed confidentially for an initial public offering in the U.S., positioning itself to become one of the most highly-anticipated public debuts. As Shein aims to expand its global empire and enormous valuation, the company will need to convince investors it can overcome mounting controversies.

Currently privately held with an estimated $66 billion valuation, Shein is seeking to capitalize on surging investor appetite for ecommerce platforms. By targeting Gen Z and millennial shoppers with on-trend fast fashion at rock-bottom prices, Shein has experienced explosive growth. The company could start trading publicly in the U.S. as early as 2024 if it gains regulatory approval.

Shein Hopes to Captivate Ecommerce Investors

As a digital-only retailer with minimal storefronts, Shein epitomizes many of today’s leading ecommerce firms. With targeted influencer marketing and constantly updated inventory, Shein has won over young consumers across the globe. Revenues reached nearly $16 billion in 2021, making Shein one of the largest fashion retailers based on sales.

This rapid ascent has drawn comparisons to platforms like Pinduoduo and Meituan in China. Shein hopes investors will value it similarly and overlook the controversies it has battled along the way. Skeptics, however, point to lingering risks that could limit Shein’s appeal.

Mounting Concerns Create Obstacles for Shein’s IPO

While Shein has taken steps to revamp public perception, the company faces no shortage of detractors. Lawmakers across the political spectrum have raised alarms over Shein’s supply chain and environmental harms.

Accused of using labor from China’s Xinjiang region linked to human rights abuses, Shein must convince regulators it complies with ethical sourcing standards. The shadowy leadership of founder and CEO Sky Xu also clashes with typical corporate governance. As other Chinese firms face heightened scrutiny and even delisting threats in the U.S., Shein’s close China ties could hamper its reception.

Alongside these issues, fast fashion business models face growing backlash for fueling waste and pollution. Though unlikely to vanish overnight, changing consumer preferences add uncertainty to the sector’s outlook.

Betting on Shein’s Growth Trajectory While risks abound, Shein’s blockbuster financials may simply be too impressive for investors to ignore. Early in its life as a public firm, revenue expansion and user growth will remain the key metrics to watch.

As a veteran of the ultra-fast fashion space, Shein has proven adept at riding waves of consumer demand. The recent downturn for stocks like Farfetch and Revolve point to lingering appetite for digital fashion platforms. Though controversies cast a shadow, for risk-tolerant investors, getting in early with Shein could bring substantial rewards.

Shein, the Chinese fast fashion juggernaut, is aiming to achieve a massive $80-90 billion valuation in its eventual US stock market debut according to sources familiar with the company’s IPO plans.

The online fashion retailer has quickly become one of the largest in the world on the back of its ultra-fast production cycles and rock bottom pricing. Shein boasts a selection of over 5,000 fashion items with over 1,000 new products added daily. This rapid launch cadence along with AI-driven fashion designs and targeted social media marketing have supercharged Shein’s popularity among Gen Z consumers.

Shein’s meteoric rise has made it one of the most valuable private companies in the world. The company hit a $100 billion valuation in its last funding round in 2021. However, subsequent secondary market trades of Shein shares revealed erosion in its value, with estimates between $50-60 billion earlier this year.

The firm is looking to capitalize on the growth in online shopping with its planned US stock exchange listing. Shein is aiming to raise around $2 billion from public market investors as it continues its quest for global fashion industry dominance.

Shein has not officially confirmed its IPO plans yet, but is said to be targeting the second half of 2023 for its market debut. The timing remains in flux given the recent stock market volatility and economic uncertainty.

Unlike most ecommerce firms, Shein has claimed profitability since its inception. The company boasts strong margins partly derived from minimal advertising spend. Shein instead relies extensively on social media influencers and word-of-mouth among its primarily Gen Z fanbase.

The Chinese company does not disclose its financials publicly, but reportedly generated over $16 billion in sales in 2021. It has also expanded aggressively in Europe, the US and other international markets. Shein’s app was the second most downloaded shopping app globally on iOS last year after Amazon.

However, Shein faces controversies around alleged labor rights violations, plagiarized designs, and environmental concerns related to its fast fashion model. Critics also argue the opacity around its operations and finances warrant closer regulatory scrutiny especially as it plans to go public.

Shein’s US IPO will be a key test of investor appetite for cash-burning technology unicorns in the current market. Chinese companies listing in the US also face tighter regulations now. A number of them have opted instead for Hong Kong and domestic China exchanges more recently.

Nonetheless, the online fashion giant has its sights set firmly on tapping into public markets to fuel its next wave of worldwide expansion. Shein aims to leverage its digital-first model and supply chain agility to continue eating market share from struggling traditional retailers.

If Shein manages to pull off a $90 billion IPO, it would rank as one of the largest US listings ever for a foreign company. The blockbuster offering could set the stage for Shein to disrupt the global fashion hierarchy dominated by H&M, Zara and other legacy incumbents.

Cargo Therapeutics is gearing up for an initial public offering (IPO) that could be one of the biggest biotech listings in 2023. The cancer-focused gene therapy startup aims to raise around $300 million through the sale of 18.75 million shares priced between $15 to $17.

If successful, it would be a rare bright spot in an otherwise dreary IPO market for life science companies this year. Cargo’s offering comes at a time when biotech IPOs have slowed to a trickle amid volatile market conditions.

The company is developing CRG-022, an experimental CD22 CAR-T therapy for certain blood cancers. Cargo’s candidate takes a patient’s own T-cells and engineers them to target and kill cancerous B-cells expressing the CD22 antigen.

Cargo hopes CRG-022 can benefit patients with large B-cell lymphoma who have failed previous CD19 CAR-T treatment. It initiated a potentially pivotal Phase 2 trial for this population in September. Data from the study could support regulatory approval in 2025.

Beyond blood cancers, Cargo intends to study CRG-022 in solid tumors expressing CD22. This includes some forms of breast, lung, colorectal and liver cancers. The company believes its therapy may demonstrate activity in a wider range of advanced cancers than existing CAR-Ts.

Proceeds from the IPO will help fund Cargo’s clinical programs and earlier R&D. According to its SEC filing, the company had $42.4 million in cash at the end of June 2022 but accumulated losses exceeding $77 million. The capital infusion will provide runway through the expected interim Phase 2 data readout.

Cargo’s offering will be a key test of investor appetite for preclinical biotech IPOs. These platform companies developing multiple experimental drugs based on a core technology have fallen out of favor recently.

However, Cargo could attract more interest with CRG-022 already in mid-stage testing and potential for near-term commercialization. The FDA has approved several CAR-T cell therapies over the past five years, providing a regulatory pathway for followers like Cargo.

Companies pursuing IPOs have been forced to scale back valuations and offering sizes. Those that do list are often trading below issue price. So far in 2022, only around 15 biotechs have braved public markets compared to 60+ in recent years.

Yet some experts believe companies with innovative therapies and strong data can still obtain IPO financing. Cargo will provide a barometer of latent investor demand for biotech offerings amid the downturn.

A successful IPO could potentially reinvigorate biotech’s depressed financing environment. It may encourage other firms contemplating IPOs to move forward with planned deals.

Conversely, a lackluster response would signal biotech IPOs remain out-of-favor for now. This could lead companies to instead pursue private financing to advance programs and extend runways.

In any case, Cargo’s listing will generate insight into the health of biotech capital markets. The deal’s performance could significantly influence investment decisions and sentiment around the battered sector heading into 2023.

All eyes will be on whether one of biotech’s most promising young companies can buck the prevailing IPO trends. Cargo’s offering will help determine if the window for issuance might finally be opening back up.

Legendary German footwear company Birkenstock priced its highly anticipated initial public offering at $46 per share on Tuesday, at the lower end of its projected range of $44 to $49 per share.

The conservative pricing comes as investors are displaying caution towards new public offerings in the face of market volatility. At $46 per share, Birkenstock would raise approximately $1.5 billion in proceeds and gain a valuation of $8.6 billion.

The sandal maker is slated to begin trading Wednesday on the New York Stock Exchange under the ticker symbol “BIRK.”

Birkenstock is going public at an intriguing moment for the footwear industry, as major players like Nike and Adidas adapt their offerings to capitalize on surging demand for comfortable, casual styles that became popular during the pandemic.

As a storied brand known for its sandals and clogs, Birkenstock is uniquely positioned to ride this trend. However, questions remain about the nearly 250-year old company’s growth trajectory and valuation.

Built on Heritage, Positioned for Growth

Dating back to 1774, Birkenstock has a long legacy as a comfort-focused footwear brand, securing devotees across the decades with its contoured footbeds and versatile sandal styles. The company lays claim to inventing the original cork footbed.

In recent years, Birkenstock has experienced a resurgence in popularity, spearheaded by its iconic Boston clogs. Younger consumers are discovering the brand, enticed by its commitment to quality, comfort and sustainability.

This has fueled strong financials, with Birkenstock generating 1.2 billion euros in revenue in its latest fiscal year, representing a CAGR of 17% over the last decade. Its sales are split nearly evenly between Europe and the Americas.

To stoke further growth, Birkenstock plans to expand its digital presence, having already grown e-commerce sales to just under 20% of total revenue. It will also continue broadening its product portfolio into areas like athletic leisure.

Reasons for Caution Among Investors

However, Birkenstock also holds substantial debt of around 1 billion euros, sparking questions about its financial profile.

Additionally, the company conceded in its prospectus that it has “identified material weaknesses in our internal control over financial reporting” – never reassuring words for potential investors.

Some analysts argue that Birkenstock’s projected valuation range of up to $5 billion was simply too optimistic, given the market environment. The tepid pricing indicates investors are unwilling to take an exuberant bet on the storied brand.

Many also point to the fiercely competitive footwear arena, where Birkenstock must compete with a range of established casual brands and new direct-to-consumer upstarts. While Birkenstock enjoys enviable brand cachet, it may lack the scale and resources of giants like Nike and Adidas.

The Road Ahead

While Birkenstock took a conservative approach with its IPO pricing, the offering will still generate a substantial cash infusion to fuel the company’s expansion.

The true test will be whether Birkenstock can sustain momentum among younger demographics while defending its turf against deep-pocketed rivals. Its ultimate post-IPO performance will be determined by strategic decisions in areas like brand positioning, product innovation, and digital sales.

But with almost 250 years of history behind it, few companies can claim a legacy comparable to Birkenstock’s. This pedigree provides confidence that the brand has staying power, whatever public market challenges may arise. For long-term investors, Birkenstock remains a compelling story combining heritage and growth.

Shares of marketing software firm Klaviyo jumped 23% in their trading debut Wednesday on the New York Stock Exchange. The successful initial public offering provides investors a rare opportunity to buy into a high-growth U.S. tech startup following a nearly two-year IPO drought.

Klaviyo priced its shares at $30 each, raising $345 million and valuing the company at over $9 billion on a fully diluted basis. The listing comes just a day after grocery delivery service Instacart went public on the Nasdaq after cutting its valuation target. Investor appetite for unprofitable technology names has waned in recent years amid rising interest rates.

But demand for Klaviyo shares was strong right out of the gate. For investors, IPOs provide a chance to gain exposure to emerging, innovative companies before they are available on public markets. Companies utilize IPOs to raise cash for growth and operating expenses.

Klaviyo reported revenue jumped 51% last quarter to $165 million, as its marketing automation software is now used by over 130,000 customers. The company swung to a $11 million profit last quarter after losing money a year earlier.

This transition to profitability is an attractive quality for investors who have soured on money-losing technology firms in the current environment. One major backer providing strong IPO demand is e-commerce platform Shopify, which owns around 11% of Klaviyo’s shares.

Klaviyo gets approximately 78% of its annual recurring revenue from customers who also use Shopify, indicating close ties between the two tech firms. Shopify invested $100 million into Klaviyo last year.

The marketing software provider enables companies to store customer data and build profiles to target marketing campaigns across email, text messaging, social media, and other channels. It initially focused on e-commerce companies but is now seeing growing traction in other sectors like restaurants, travel, and entertainment.

Tech IPOs ground to a halt in 2022, as surging inflation led the Federal Reserve to aggressively raise interest rates, sparking volatility and a flight from risk assets. Klaviyo is the first notable U.S. venture-backed software IPO since HashiCorp and Samsara debuted in December 2021.

The offering provides investors hungry for exposure to high-growth tech the chance to buy into a next-generation software vendor. U.S. tech IPOs slowed to their lowest level in over a decade last year. If strong demand for Klaviyo shares continues, it could open the door for more tech IPOs in 2023.

Companies that only recently considered going public may once again pursue IPOs after Klaviyo’s success. The IPO window for unprofitable tech names appeared shut, but Klaviyo’s ability to raise over $340 million shows investors still have appetite for rapidly growing software vendors.

Looking ahead, the pipeline for tech IPOs includes names like Reddit, Databricks and Discord. But many may delay plans or explore direct listings to avoid leaving money on the table like Instacart. If markets grow choppy again, Klaviyo’s offering window could close as quickly as it opened.

For now, its strong first day of trading is a boon for both the company and tech investors. Early buyers are already sitting on sizable gains from an asset class that struggled last year. If the tech IPO market thaws, it would provide investors access to the high-growth innovators driving the future.

Instacart experienced a red-hot debut on the public markets as shares soared 40% in its first day of trading. The grocery delivery pioneer opened at $42 per share on the Nasdaq exchange, well above its IPO price of $30.

The opening trade valued Instacart at nearly $14 billion, up from the $10 billion valuation set by its IPO pricing on Monday. Demand from investors seeking exposure to the future of grocery commerce drove the shares sharply higher out of the gate.

Trading volume was heavy early on, with over 18 million shares changing hands in the first 30 minutes. The stock traded as high as $47.57 at its peak, showcasing strong appetite for the newly minted public company.

Instacart (CART) raised $420 million through the IPO by selling 14.1 million shares, representing just 8% of its total outstanding shares. Existing shareholders also sold 7.9 million shares in the offering for liquidity.

The blockbuster debut delivered significant returns for IPO participants during a volatile time for tech stocks. But Instacart’s valuation remains below the $39 billion mark it reached at the height of pandemic demand in 2021, reflecting more measured recent tech valuations.

Still, the strong first day pop is a promising sign for Instacart as it embarks on the public market journey. The company priced its offering conservatively to allow room for an impressive inaugural rally.

The offering adds Instacart to the ranks of publicly traded ecommerce innovators disrupting traditional retail models. It joins the likes of DoorDash, Uber, and Amazon in leveraging technology to unlock the potential of online grocery delivery.

Instacart is at the forefront of transforming the $1 trillion grocery industry through its on-demand digital marketplace. Its platform connects customers with personal shoppers who handle orders from partner grocers and deliver items in as fast as an hour.

Founded in 2012 by an Amazon veteran, Instacart was early to recognize the coming wave of grocery ecommerce. The company scaled rapidly when the pandemic accelerated adoption of online ordering and delivery.

Instacart seized its first-mover advantage to emerge as a leader in the space. It has partnered with prominent national, regional, and local grocers to build a retail network covering over 85% of U.S. households.

The company aligned with shifting consumer preferences for convenience and digital experiences. Busy lifestyles and smartphone ubiquity make grocery delivery a killer app of modern ecommerce.

Instacart smartly invested to expand services like fast unstaffed delivery and self-service pickup. Its Instacart Ads platform also lets brands promote products through sponsored listings.

The company rapidly grew revenue to over $7 billion in 2021 during the pandemic-driven surge. More recently it has focused on boosting profitability as demand normalizes post-Covid.

Instacart generated $14 billion in gross merchandise volume in 2021. Its net revenue neared $2 billion, doubling from 2020. But losses have narrowed dramatically since the company turned EBITDA positive last year.

As the first major tech IPO of 2023, Instacart’s trading provides a blueprint for startups and venture investors awaiting public debuts this year. The initial reception indicates persistent investor appetite for innovative tech names with strong growth narratives.

The blockbuster debut opens an exciting new chapter for Instacart and the future of digital grocery. Its first trading day validated Instacart’s pioneering business model and resilient growth prospects.

Calidi Biotherapeutics has completed its merger with special purpose acquisition company First Light Acquisition Group (FLAG), debuting as a publicly traded cancer immunotherapy company. The combined entity, now named Calidi Biotherapeutics, Inc., will commence trading on the NYSE American under ticker symbols “CLDI” and “CLDI WS” on September 13.

The merger provides Calidi with gross proceeds of approximately $28 million before expenses and debt repayments. This consists of $25 million raised in a concurrent private offering, $1 million in cash from FLAG’s trust, and $2 million in PIPE and non-redemption agreements.

Founded in 2014, Calidi is developing first-in-class immunotherapies using allogeneic stem cells to deliver targeted cancer treatments. The SPAC deal enables the company to continue advancing its pipeline as a publicly listed firm.

Calidi’s lead candidates CLD-101 and CLD-201 leverage proprietary platforms called NeuroNova and SuperNova. Both utilize allogeneic stem cells loaded with oncolytic viruses that directly infect and kill tumor cells.

CLD-101, which employs neural stem cells, is currently in a Phase 1 trial for recurrent high-grade glioma brain tumors. Interim data is expected in 2024. CLD-201 uses mesenchymal stem cells to treat advanced solid tumors, with a Phase 1/2 study slated for 2024.

According to Calidi CEO Allan Camaisa, the IPO “will allow us to push the boundaries of cell-based virotherapies and continue to research novel ways to eradicate cancer.”

SPACs have become an increasingly popular alternative to traditional IPOs in the biotech sector. Also known as “blank check companies”, SPACs raise capital through an IPO and then merge with a private entity to take it public. This allows the operating company to avoid some of the uncertainty associated with a traditional public debut.

First Light Acquisition Group, led by CEO Tom Vecchiolla, raised $172.5 million in its own IPO in May 2021. The team then sought a merger target that could benefit from the injection of public capital. They ultimately settled on clinical-stage Calidi and its novel immunotherapy approach.

In addition to the SPAC proceeds, Calidi has secured a $10 million forward purchase agreement from several institutional investors. It also intends to execute a $50 million purchase agreement with Lincoln Park Capital Fund.

Between its strengthened balance sheet and non-dilutive financing options, Calidi believes it now has the runway to advance its programs into 2025 without need for further equity funding.

According to Vecchiolla, “We are excited to see Calidi continue to grow as they transition into a public company and look forward to their clinical pursuit of new treatment options for patients everywhere in need.”

The merger completes Calidi’s transformation into a publicly traded company. With shares soon to start trading on the NYSE American under ticker “CLDI”, the company is poised to continue developing its promising immunotherapy candidates for cancer patients in need of new treatment options.

Online grocery delivery firm Instacart is gearing up to go public and has set the terms for its initial public offering (IPO). In a regulatory filing on Monday, Instacart outlined plans to raise around $616 million through the offering of 22 million shares priced between $26 and $28 each.

The IPO would give Instacart a fully diluted valuation of up to $9.3 billion. This is below earlier estimates of a $40 billion valuation, indicating moderating growth expectations. Nonetheless, the offering could still mark one of the largest public listings this year amid a freeze on IPOs over the past year due to market volatility.

Founded in 2012, San Francisco-based Instacart has established itself as a leading online grocery platform in the U.S. It partners with grocers and retailers to deliver items to customers’ doors in as little as an hour. Instacart competes in a crowded space against entrenched firms like Walmart and Amazon as well as delivery apps like DoorDash and GoPuff.

Take a moment to look at 1-800 Flowers.com, a leading e-commerce business platform that delivers gifts designed to help inspire customers to give more, connect more, and build more relationships.

Instacart plans to sell 14.1 million newly issued shares in the IPO, with the remainder offered by existing shareholders. Multiple prominent investors have committed to buying shares in the offering, including PepsiCo, which is investing $175 million, and Norges Bank Investment Management, Norway’s sovereign wealth fund.

Proceeds from the IPO will provide funding for Instacart to invest in areas like technology, fulfillment, and advertising as it aims to turn a profit. The company posted revenues of $1.8 billion in 2020 but has yet to become profitable.

The upcoming listing will test investor appetite for high-growth tech IPOs after a yearlong freeze. Instacart’s debut performance will depend on prevailing market sentiment closer to its trading date. But a successful IPO could boost Instacart’s brand and validate its status as a leading next-generation grocery platform.

The Current Environment for IPOs is Best in Over 15 Months

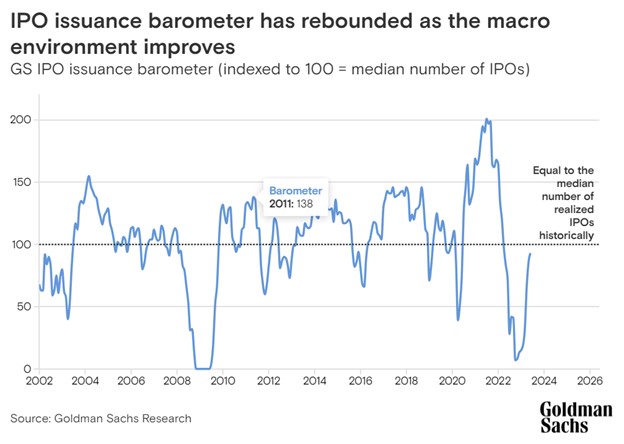

Does the elevated reading of the Consumer Confidence report, along with the extended period of low market volatility, and belief the Federal Reserve is near the end of the tightening cycle, set the climate for more companies going public? Goldman Sachs Research just released readings of its IPO Issuance Barometer. This measures the environment for initial public offerings (IPOs) using many different metrics. There is only one out of more than a dozen factors which does not support the expectation that the IPO climate is improving for companies.

As stock market prices stabilize and corporate executives grow more confident, the economic conditions in the United States are becoming more favorable for IPOs according to Goldman Sachs Research.

The GS IPO Issuance Barometer has risen to 93, a level consistent with steady IPO activity. After hitting a low point of 7 in September 2022, the Issuance Barometer is now at its highest level since March 2022. A reading of 100 represents the historical average number of IPOs realized in a given month.

The measure takes into account several factors including the S&P 500 drawdown (the difference between the index’s current value and its 52-week high), CEO confidence levels, the ISM Manufacturing Index, the six-month change in two-year Treasury note yields, and the S&P 500’s trailing enterprise value/sales ratio.

The most impactful contributor behind the improvement in the IPO Barometer has been the stabilization of stock market prices. Chief U.S. Equity Strategist at GS Research, David Kostin notes in the report that the S&P 500, which represents U.S. stocks, has remained relatively stable due to indications of resilient economic growth and the expected end of interest rate hikes by the Federal Reserve. Kostin also highlights that the drawdown in the S&P 500 has been the most significant factor influencing IPO activity. The largest decline from peak to trough this year was 8%, compared to an average of 13% since 1928. In the second quarter, the maximum drawdown has been only 3%. Additionally, market volatility has decreased, as indicated by the VIX, which measures the implied volatility of the S&P 500, dropping below 15, its lowest level since before the pandemic.

Although the S&P 500 has reached a new 52-week high, it is still 10% below its all-time high in January 2022.

The other components in Goldman’s IPO gauge that have also made large contributions to its current reading include improvements in CEO confidence, despite the fact that the median professional forecaster gives a 65% probability of a recession in the next 12 months. Short-term Treasury yields seem to have reached their peak, suggesting that the Federal Reserve’s tightening cycle is nearing its end. Also positive for companies deciding if now is a good time to go public is that stock valuation multiples remain high compared to historical levels. The only variable in the barometer that has not improved since September 2022 is the ISM Manufacturing Index.

Although the positive macroeconomic conditions have yet to translate into increased IPO activity, follow-on stock offerings, which occur after a company has gone public, have shown greater resilience. This year, there have been eight U.S. IPOs exceeding $25 million in size, excluding special purpose acquisition companies (SPACs) and spin-offs. These deals have raised a total of $2.4 billion in gross proceeds, compared to $3.8 billion for the entirety of 2022.

Forecasts from Goldman Sachs’ economists indicate a 25% chance of a recession in the next 12 months, but they suggest that the environment for IPOs could further improve in the second half of the year. Additionally, analysts at Goldman Sachs Research have recently increased their year-end price target for the S&P 500 to 4500, representing approximately a 2.5% increase from the current level.

If the U.S. economy experiences a “soft landing” characterized by stable equity prices and interest rates, modestly improving CEO confidence, an uptick in the ISM Manufacturing Index, and flat valuation multiples, the IPO Issuance Barometer could reach 119 (compared to 93 as of May 31). This would indicate an even more supportive environment for IPO activity according the research.

What Else?

After having an empty IPO calendar last week, six deals are scheduled this week. Four of them exceed $100 million. According to Renaissance Capital, a provider of IPO ETFs, there have been 46 U.S. deals so far in 2023. This is a 21% increase over the same period last year, and 89 deals have been filed which is a 16% increase.

Also likely to get the attention of management teams sitting on the fence determining if the timing is right, are returns. According to Renaissance, the ETF ticker symbol IPO, which invests in initial offerings, is up 26% so far this year. The S&P 500 is up only 13%.

The amount of investment in initial public offerings (IPOs) during March-April has jumped from January-February levels. Globally, the pick-up in IPOs is linked to the uptick in stock prices, which has allowed companies to tap into investor appetite for newer listings. A sizeable percentage of the offerings are in Asia, but Europe and the U.S. have experienced a surge as well. Activity during the first two months of 2023 had ground to a halt; new data compiled by Bloomberg demonstrates a much faster trend.

To date, there has been $25 billion worth of IPOs worldwide in March and April; this is nearly twice the amount transacted during the prior two months of the year. Companies headquartered from Hong Kong to Milan have put up their “Going Public” signs up as market volatility declined. The uptick in IPOs in Asia substantially moved the needle as non-U.S. exchanges accounted for nearly 80% of new share sales during April.

The uptick in Europe can’t be ignored either; European listings are higher by a wide margin compared to earlier in the year. The activity in the U.S. is not as robust but also noteworthy, as concern about a recession had been creating caution among potential U.S. issuers.

In a quote published by Bloomberg News, Jason Manketo global co-head of the law firm Linklaters’ equities practice said, “We are beginning to see green shoots of activity with companies restarting processes that were on hold, but there is still a fair degree of uncertainty in the market.” Mankel added, “The buy side is keen to see results for a couple of quarters before committing to an IPO. This means the potential pipeline of some 2023 deals has been moved out to 2024.”

Leaders

Statistically, Asia is where a great deal of the action is in the world today. But the activity is different, perhaps more appealing, than last year. In 2022 the vast majority of large deals were concentrated in mainland China; over the past two months, issuance is coming from a broader representation of Asia.

“The IPO market is coming back gradually and slowly. It is not 100% back yet, but there are signs of life and renewed vigor,” said James Wang, co-head of equity capital markets at Goldman Sachs Group Inc. in Asia ex-Japan.

A couple of nickel producers from Indonesia surged as they went public. And in Japan, as part of the country’s largest IPO since 2018, Rakuten Bank Ltd. soared after it raised 83.3 billion yen ($623 million). And KKR & Co.-backed Chinese liquor company ZJLD Group Inc. as recently as April 20th, priced Hong Kong’s largest offering in 2023.

Europe Wakes Up

Europe’s IPO market had been dragging, with activity in 2023 down about 12% from the same period last year as Russia’s invasion of Ukraine brought new listings to a screeching halt.

Also weighing on the market, poor IPO returns have been a deterrent for investors. Portfolio managers had been in the drivers seat insisting on bargains for less proven companies. In March the sudden meltdown of financial firm Credit Suisse, ignited a global market rout, this added to investor worries about interest rates and inflation; the event also made it less attractive for companies to try and attract a favorable price.

But there are growing signs of fear lifting. Most notably, Lottomatica SpA, the Italian gambling company backed by Apollo Global Management Inc., opened the books last week for a €600 million ($657 million) IPO, becoming the third large firm to tap European exchanges this year. Additionally, German web-hosting company Ionos SE and electric motor component maker EuroGroup Laminations SpA have managed to raise more than $400 million in the region, though both stocks have struggled after debuting.

U.S. Uptick

While IPO activity in the U.S. is not as robust, there has been a huge uptick as well. The IPO calendar for U.S. exchanges shows 20 priced deals totalling $751.5 billion, and 29 new filings. This is an acceleration after only $4.1 billion had been raised for companies listing on U.S. exchanges during the first two months of 2023.

Take Away

Globally companies are finding it more worthwhile to tap capital from the equity markets via IPO. While the most growth is greater Asia, Europe and the U.S. see a significant uptick as well. Whether this trend continues and represents, a buying opportunity seems to hinge on recession concerns. Many forecasters are now calling for a much more mild recession than previously expected.