Middle market companies often sit in a unique sweet spot: large enough to scale and access capital markets, yet small enough to maintain agility and entrepreneurial drive. For investors looking beyond the mega-cap names, these companies can offer strong growth potential and underappreciated value. However, one area where their size shows is in their vulnerability to policy shocks—particularly tariffs.

With the recent news of proposed pharmaceutical import tariffs as high as 200%, there is renewed focus on how U.S. trade and economic policy can affect publicly traded middle market firms. While much of the attention gravitates toward household names in the S&P 500, it is often middle market companies that feel the effects of these shocks most acutely—both in risk and in opportunity.

Why Middle Market Companies Are More Sensitive to Policy Changes

Unlike large-cap multinational corporations, which tend to have well-diversified supply chains and extensive legal and lobbying infrastructure, many mid-sized public companies operate with leaner operations and more concentrated supplier networks. A sudden 25% or 200% tariff on an input or finished product can dramatically alter their cost structure or compress margins.

For example, a middle market pharmaceutical manufacturer importing active ingredients from Asia might not have the domestic sourcing flexibility or pricing power of a top-tier player. Similarly, industrial firms relying on imported steel or semiconductors could find themselves needing to adjust production timelines or renegotiate customer contracts quickly.

Navigating Through the Volatility

Yet these challenges often breed innovation. One strength of middle market firms is their ability to pivot faster than larger peers. When tariffs shift the economics of a product line, smaller public companies often respond with strategic sourcing, nearshoring, or product reengineering at speeds larger bureaucracies struggle to match.

Investors should pay close attention to management’s ability to communicate and execute these adjustments. Companies that respond proactively to tariffs may emerge stronger, with improved operational resilience and competitive differentiation.

A Hidden Advantage: Domestic Focus

Interestingly, many middle market stocks have a geographic advantage when it comes to tariffs. Firms that focus primarily on domestic customers or rely on U.S.-based production may see relatively limited impact from import duties. In fact, some could benefit as competitors with overseas exposure face higher costs or delays.

This potential insulation is particularly relevant in sectors like building materials, specialty manufacturing, and consumer services—all areas where middle market companies often shine.

Long-Term Opportunities for Investors

For long-term investors, the key is to identify which middle market companies are not just reacting, but adapting and innovating in the face of policy changes. These firms may offer compelling upside potential when the dust settles.

Policy shocks like tariffs are not going away. But they don’t necessarily have to derail performance. In many cases, they can highlight hidden strengths—operational flexibility, strategic focus, and leadership that can thrive in uncertainty.

In an era of shifting policy, these resilient middle market growth stocks can be some of the most rewarding investments in the public markets.

This Sunday, over 100 million viewers will tune in to the Super Bowl, the biggest single sporting event of the year. The Super Bowl is about more than just football – it’s a cultural phenomenon that offers some interesting parallels to the world of investing. Here are a few key lessons investors can take away from the gridiron action.

Do Your Research

Top NFL teams like the Chiefs and 49ers do endless hours of film study, analyzing their opponents’ strengths and weaknesses. Similarly, successful investors research companies thoroughly before buying shares. They dig into financial statements, study industry trends and competitive dynamics, and evaluate leadership. Just as teams dissect game tape, investors need to do their homework before putting money on the line.

Stick to Your Game Plan

NFL teams map out detailed game plans listing the plays and strategies they will employ against a given opponent. But when things go awry during a game, emotions can take over and teams may abandon their plan. Investors face the same challenge. When market volatility spikes, it’s easy to panic and stray from your investment strategy. But patience and trusting your game plan, like asset allocation and time horizons, tends to pay off in the long run.

Remember Past Performance Doesn’t Guarantee Future Success

The 49ers and Chiefs have been among the hottest teams this season. But past performance doesn’t guarantee victory in the Super Bowl. Likewise, investors should be wary of stocks that have recently soared. Valuations may already price in expected growth. And markets humbles previous high flyers all the time. Picking stocks based on long-term fundamentals rather than short-term momentum is the better bet.

Expect the Unexpected

From major injuries to fluke plays, the Super Bowl often hinges on unpredictable events. Investing also involves constant surprises that can disrupt even the most ironclad strategies. Political turmoil, natural disasters, new technologies – the market is always full of unknown unknowns. Having flexibility to adapt to unforeseen events helps minimize damage and take advantage of mispriced assets when volatility strikes.

Patience Is a Virtue

Building a championship roster takes years. Teams must strategically draft prospects, develop their skills, and assemble complementary pieces patiently over time. Becoming a successful investor also requires long-term commitment. There are few get-rich quick schemes that work. Compounding modest gains over decades through steady contributions is the surest path to building wealth. Keep your eyes on the long-term prize.

Minimize Costs and Taxes

NFL teams structure contracts and manage salary caps astutely to get the most bang for their buck. As an investor, costs and taxes also directly impact your net returns. Minimizing investment fees, trading commissions, and avoiding short-term capital gains taxes helps grow your portfolio. Every basis point counts.

Diversify Your Holdings

Smart NFL general managers build depth at every position. If injuries arise, the next player up can step in seamlessly. Similarly, investors should diversify across asset classes, sectors, geographies, and risk levels. If certain segments of the market decline, gains in other areas can offset the losses. Spreading your investments helps smooth out volatility.

Stay Disciplined and Stick to Your Strategy

The bright lights of the Super Bowl can cause teams to get away from their identity. The same thing happens to investors during periods of market turmoil. It’s crucial to stay disciplined, avoid emotional decisions, and stick to your long-term strategy even as others lose their nerve. Composure under pressure leads to victory.

Just as fans love dissecting every nuance of the big game, studying the market from all angles is key for investment success. Enjoy the Super Bowl, but also reflect on the winning lessons it provides for building wealth. Your portfolio will thank you.

The investing world lost a titan this week with the death of Charlie Munger at age 99. As vice chairman of Berkshire Hathaway and close confidante of Warren Buffett for over 60 years, Munger played an integral role expanding Berkshire into the mammoth conglomerate it is today, valued over $700 billion. But beyond his partnership with Buffett, Munger made lasting impacts as a business leader, architect, philanthropist and teacher.

Born in Omaha, Nebraska in 1924, Munger served in World War II before earning his law degree from Harvard and embarking on dual careers in law and business. He founded the California-based investment firm Wheeler, Munger & Company which focused on real estate and traded stocks. By the 1970s, Munger had amassed ample wealth to retire early and pursue other passions.

Fatefully, a shared investing philosophy brought Munger together with Buffett years prior, though the two operated their own separate enterprises. When Buffett took control of struggling textile manufacturer Berkshire Hathaway in the 1960s, he tapped Munger to help redirect the company towards the insurance and investment vehicles that became its core business.

With Buffett as Chairman and CEO and Munger as Vice Chairman, the duo refined their strategy of identifying “wonderful companies at fair prices” and letting their investments compound over long periods. Their disciplined approach to capital allocation, thorough due diligence and patience in holding winners drove Berkshire’s stock price from around $300 per share when Munger joined to over $400,000 per share five decades later.

Beyond remarkable returns, Munger spearheaded Berkshire’s evolution from a holding company into the massive conglomerate it has become, owning outright brands like GEICO, Duracell and Dairy Queen and holding large stakes in public companies like Coca-Cola and Apple. Munger encouraged Buffett to open Berkshire’s wallet for large acquisitions when an attractive deal surfaced.

Investing principles etched in stone While Buffett attracted fame as the public face of Berkshire Hathaway, insiders knew Munger as an equal investing and decision-making force. The Berkshire Vice Chairman preached avoiding unnecessary complexity and instead focusing on business sustainability and management integrity.

“All intelligent investing is value investing – acquiring more than you are paying for,” Munger once said succinctly. He codified principles of patience, discipline and thoroughness that became central tenets of value investing doctrine studied by generations of students and money managers alike.

Munger himself authored multiple books and papers studied religiously in business schools and investment programs. Generations of proteges like Mohnish Pabrai and Guy Spier view Munger as a personal mentor despite limited direct interactions, such was the influence of his published wit and wisdom.

Architect, donor, teacher

Beyond the investing arena, Munger left his mark on educational institutions and fields as diverse as architecture and medicine. Though lacking formal credentials, the businessman designed multiple buildings on college campuses, forging his vision upon schools like Stanford and the University of Michigan through large-scale donations.

Even in his late 90s, Munger energetically dispensed advice as he engaged audiences at Berkshire’s famous shareholder meetings with his trademark wit. He urged individuals to expand their multidisciplinary knowledge and maintain ethical decision-making standards throughout their careers.

In interviews, Munger revealed how his own perseverance powered through major adversity, from the death of his young son to blindness in one eye. While Munger formally steps away from the investing stage he commanded alongside Warren Buffett for nearly sixty years, his insights and values will continue molding new generations of business leaders for decades to come. The legacy left behind ensures Charlie Munger’s status as an investing icon remains etched in stone.

Small cap stocks are an often overlooked opportunity for regular investors. While most focus their attention on big household names like Apple and Microsoft, small caps can provide key benefits to your portfolio. In this article, we’ll look at what makes small cap stocks different, reasons to consider investing in them, and how best to include them in your overall investing strategy.

What are Small Cap Stocks?

Small cap simply refers to small capitalization companies. They have a total market value or capitalization that is relatively small. In the U.S. stock market, small caps are generally defined as companies with a market cap between $300 million to $2 billion. Meanwhile, large cap stocks are the big boys like Walmart with market caps over $10 billion.

The most obvious trait of small caps is that they are younger, newer companies. Think of spunky young upstarts versus mature bluechip firms. Many small caps are still working to find their footing and carve out their niche, whereas large caps dominate established sectors.

This gives small caps more room for rapid growth, but also higher risk. Their smaller size means limited resources, unproven track records, and uncertainty around whether they will achieve scale. Volatility comes with the territory.

But with greater risk can also come greater reward if you pick the right small caps. For investors, this asset class offers plenty of overlooked potential.

So why should investors even bother with small caps? A few good reasons:

Growth Potential

The biggest appeal of small caps is their high growth potential. While large established companies have already reached maturity, small caps are still in their early stages where rapid expansion is possible. Getting in early on promising small cap stocks can lead to massive returns over time.

For example, buying shares of a company like Etsy or Shopify in their early days as small caps could have generated 10x or even 100x returns for patient investors as those companies grew to multi-billion dollar valuations. The chance to identify and own the next Apple or Amazon while their market cap is just a few hundred million dollars is an enormous opportunity.

Of course, investing in any small cap is high risk and many will not succeed. But a diversified portfolio of thoughtfully selected small caps tilted towards sectors with strong tailwinds can unlock tremendous growth. Taking some calculated risks while sticking to sound fundamentals is key.

Diversification

Owning small caps is a great way to diversify a portfolio heavy on mature large cap stocks. Because small caps operate in different niches and have unique risk factors, their stock prices behave differently than large caps. This means including small caps can actually lower overall portfolio risk and volatility.

Small caps also shine at different points of the economic cycle than large caps. When growth is sluggish, investors tend to favor large caps for their stability. But in periods of economic expansion and bull markets, small caps tend to deliver stronger returns. This cyclicality means pairing both provides more balanced exposure across market environments.

And importantly, the returns of small caps have low correlation to large caps. This low correlation is a crucial benefit, since it smooths out portfolio performance over time. For example, when large cap stocks are declining, small caps may be stable or even rising. This illustrates why allocating 20-30% of a portfolio to high-quality small caps can improve overall diversification.

Innovation Appeal

Another major reason to invest in small caps is the innovation factor. Small companies are often pioneers in developing cutting-edge technologies, medicines, software platforms and other game-changing solutions. Unlike large caps, small caps have agility and risk tolerance to focus intensely on bringing new ideas to market.

For example, most breakthrough biotech and pharma firms start out as small caps, racing to get FDA approval for their patented drugs. Software firms disrupting industries also tend to be younger and more nimble. And emerging sectors like green energy and electric vehicles are being driven by upstart small cap companies.

Getting in early with innovative small caps developing disruptive technologies provides exposure to future trends that large caps simply don’t offer. It allows investors to tap into new niches before they become mainstream. And investing alongside visionary founders and entrepreneurs in new fields generates exciting upside.

Of course, betting on unproven technologies and markets comes with risk. But a basket approach of diversifying across several promising small caps in high-potential areas prudently taps into this appeal. Backing innovation via calculated small cap investments generates asymmetric reward versus risk.

Investing Strategies with Small Caps

The most popular approach is investing in small cap mutual funds or ETFs. This provides instant diversification across dozens or hundreds of small cap stocks. Low cost index funds like the Vanguard Small-Cap ETF are a great starting point because they track the overall small cap market at low cost. Actively managed small cap funds aim to outperform by utilizing research and stock picking. Either method offers a simple way to add small cap exposure.

For a more active approach, investors can hand pick individual small cap stocks. This requires rigorous research to identify quality companies within attractive niches that have strong leadership, a durable competitive advantage, and metrics pointing to high growth potential.

Since small caps carry more risk, it’s crucial to diversify and size positions appropriately when buying individual stocks. Use them to complement a core portfolio of sturdy large caps. Blending individual stock picks with a small cap index core allows concentrating assets in your highest conviction ideas. Overweighting small caps beyond 20-30% of your total portfolio exposure adds undue risk.

While small caps demand more research and carry greater risk, they can supercharge portfolio returns. Blending small caps strategically with large caps allows investors to capitalize on this untapped potential while minimizing the downside.

Deciding if Buy and Hold or Trading is Best for You?

New investors today have powerful tools that may exceed what was available even at institutions just a decade ago. This provides a leg-up on those of us who had to cover high trading fees, buy and sell, before we made a dime. Then, there is today’s information availability. Stock prices were printed in the morning from the day before close; that is how investors were updated. Then there is all the other up-to-the-minute information from your broker and company data and research from platforms like Channelchek and others.

This can be both helpful and overwhelming to a new investor deciding where to focus and what type of investment style suits them.

The least expensive discount brokers, when I bought my very first hundred shares cost $100 in and $100 out ($200 round trip). So exceeding two dollars per share on each round lot (orders not in lots of 100 cost more) was necessary to break even. Between this and the non-current price information, a buy-and-hold position was the only position that made much sense.

Now, transacting is just point-and-shoot. Even bid versus ask spreads are minuscule. This makes it more practical for an investor to decide not to ride out a perceived slide even if they have confidence that it will reverse later. Instead, with the ability to unload before an expected trouble spot develops, an investor that waits instead, may become angry with themselves that they held and their account value has declined.

Today’s set of circumstances has a lot more investors acting like traders and trying to time the market. The tolerance for seeing a holding is up, say 6% over a period of time, only to be down 2% over a longer period, then up 7% down the road is much more rare. Newer investors don’t have as much price swing tolerance, they want to take a profit before the market drops. Some then expect as much as a 20% dip that they can buy back into.

Of course, hitting the near tops and low points to maximize profit is unlikely. And trying to do it usually leads to frustration from missed opportunity when it doesn’t then move in the direction that would benefit the trader.

So is it prudent to try to time price moves up and down and trade the shares, to take advantage of so much information? Or, should they do research, find companies they expect will do well, and then look for a good entry point, not even thinking about an exit unless it begins to behave outside of expectations?

This is particularly relevant in a year where the market is up above average, which means if it gravitates back to its mean average annual return, the overall market will end the year lower than it is now.

There is no one simple answer, but a practical approach is to have core holdings to take the long ride with, and then view other stocks separately that maybe move a little faster, up and down, that are for timing moves. This leads to diversification in holding periods. But, in order to work, one has to not forget or give up on the individual strategies of the two investment styles that are to be thought of separately, perhaps even in two different accounts.

But when does one sell from the buy-and-hold portion, is there a trigger? And what is the trigger with the assets in the trading portion?

The same idea could apply to both sets of assets. Set the parameters for every trade and stick to them. Take a profit or a loss when the parameter is met, regardless of what you may feel at that time. Good decisions and “if-this, then-that” thinking is best when not in the heat of battle. Plan your trade and trade your plan regardless. In some cases it may have worked out better if you had acted differently than planned, but if it is based on realistic expectations or probabilities, then chances are, over the years it will reap greater rewards.

This ongoing reassessment, regardless of expected holding time, has the investor set levels, both above and below a stock’s current price, that, when struck causes the investor to evaluate. That evaluation may simply be asking oneself has anything changed since I set this parameter? If not, act. It may also be asking oneself, is this the best use of my capital right now, or is there a better place that I believe has the potential to outperform the current holding?

Take Away

An investment portfolio plan with meaningful rules to follow helps reduce the anxiety of investing. Whether 90% is earmarked buy-and-hold, or 90% is to achieve short-term gains and avoid big drawdowns, the trades must be managed to a pre-thought-out sensible plan. The expectation then is that none of the positions will work out perfectly timed, but as a whole, over a long enough period, the investor will be better off than if they had no guidelines or fewer boundaries.

Avoiding a Hurricane May Mean Adjusting Your Portfolio

Like most people that live in Florida, I usually first learn of approaching hurricanes from concerned family members up North. My reaction is probably different than others. My first thoughts on rare news events is to ask myself, “is this bullish or bearish?” When it comes to hurricanes, there is an answer – like most events that impact stocks, the answer is, “it depends.” Getting out of the way of a hurricane could also mean a slight adjustment to holdings.

I will mention that the toll on life and property of natural disasters, or any travesty, is not lost on me. But as investors, we must control the risks that we can and look for the rainbow in situations we have no control over.

Economic Damage

Dubravko Lakos-Bujas, JP Morgan’s head of U.S. equity and quantitative strategy, shared insights on the economic impact of hurricanes a couple of years before hurricane Ian struck Naples Florida. But the value of the information has not changed. “Major U.S. hurricane landfalls have had less significant impact on aggregate market performance (~2% decline) given the subsequent pick-up in disaster-induced public and private spending,” Mr. Lakos-Bujas said. “The most significant impact on equity performance is seen at the stock and sub-industry level.”

Money May Grow on Trees

Does your portfolio contain Orange Growers? Gulf Coast REITS? Companies that operate in the affected area of the storm see a loss in production as they close up and, at the same time, a jump in costs as they make repairs. These stocks are most likely to underperform. For those companies in the repair business, for example, lumber and roofing supplies, they could generate business whether a storm actually makes landfall or not. The rebuilding effort will cost insurance companies with a concentration of insured properties in the path of a storm.

Lakos-Bujas warned, “The underperformance should be concentrated in insurance (i.e. property loss coverage), and companies with Hotels, Restaurants, Leisure, & Airlines (i.e. based on occupancy/traffic, rising commodity costs), Telecom and Cable (i.e. capital expenditure tied to repair and potentially lower revenue per unit), and Industrials (i.e. rising input costs, disruption in production and transportation) depending on geographic footprint.”

Solutions tend to gravitate toward problems, even if those problems include damage and destruction. This is a good thing, it is capitalism working in a way that helps others. This help is profitable and could make some sectors outperformers. “The largest outperformers include industries tied to replacing and/or repairing existing capital stock (i.e. Energy Equipment & Services, Communication Equipment, Autos), transportation and logistics (i.e. Distribution, Air Freight, Trading Companies), and construction (Basic Materials and Engineering),” Lakos-Bujas’ said.

The analysis of the JP Morgan equity strategist is based on a study of 31 hurricanes between 1965 and 2014, which had a combined cost of $520 billion. Two o the large storms, Irma and Harvey, represent a high percentage of the total cost.

“Based on current unofficial damage estimates for hurricanes Harvey and Irma, losses this year are expected to exceed 50% of combined costs over the last 50 years,” he said. “These outsized losses could currently drive more pronounced moves at the stock and sub-industry levels than historically.”

So, a person may live across the country or around the globe from the storm and still feel an impact. For historical context, the S&P 500 (^GSPC) has seen an average decline of 2% in the week following a hurricane’s passing.

Rebuilding Benefits Stockholdings Differently

Much of the backstop in the economy and the markets is based on the idea that rebuilding after a storm is stimulative. Households and businesses suddenly jam work that needed to be done into a short time span and spend much more on what could’ve been routine maintenance. Economists say that the near-term impact on GDP is a net positive once the hurricanes pass. A lasting positive impact occurs if a natural disaster brings about rebuilding that improves on the existing structures or facilities instead of just restoring them to their previous state.”

One caveat is that labor markets have been tight. Most other years, roofers and builders flocked to the highest bidders and the flow of money helped speed the rebuilding process. If there are currently not sufficient human resources, this will push costs up more than they otherwise would have. Unfortunately, there continue to be reports of labor shortages in many industries, including construction. Fox Business News reported on August 28, 2023, “America’s shortage of skilled workers is impacting the ability of businesses in the construction and manufacturing industries to staff their businesses and complete jobs on time.” This situation could certainly slow any needed rebuild.

As wildfires in Hawaii have shown us, funds for rebuilding efforts are further complicated by politics. Three of the Floridian candidates for president, including the governor, are from a party that is not in power

Take Away

Opportunity comes in all forms. This includes opportunity to avoid a dip in some of your holdings, and an opportunity to capitalize on increased company profits this includes disasters of all types. Weather events can impact stock performance of individual companies and industry subsets. At roughly a negative 2% average, the overall market could impact investors over the following 30 days at a rate that feels like normal monthly swings.

As a positive thought, after the storm clears, come join Channelchek, Noble Capital Markets and an expected 150 public companies companies all converging on South Florida in early December for NobleCon19, the investment conference where you’ll discover actionable investment ideas inspired directly from company management. Learn more here.

Need-to-Know for Those Starting to Dip Their Dough into the Stock Market

Maybe you’ve saved a little and know you ought to invest, or maybe school is finally out and you have time and a few dollars to build your future, but you don’t think you know enough about the world of stock market investing. It’s easy to feel overwhelmed by the abundance of information? It’s a big decision with many mysteries and unknowns for both newcomers, and veterans. This article aims to remove much of the mystery for new investors so you can be more confident in building a portfolio that can enhance your life plans.

Whether you become interested in small-cap stocks, growth stocks, or even IPOs, understanding key concepts such as valuing a stock, risk tolerance, investment goals, investment style, risk management, and portfolio strategy is crucial. Let’s dive in!

Set Investment Goals

Clearly defining your investment goals is essential so you can make decisions after comparing them to those goals. Are you investing for retirement, saving for a down payment on a house, or aiming for short-term gains? Your goals will influence the investment strategies you use. For example, if you’re investing for retirement and have decades of working years left, it may mean to buy and mostly hold for a long period stocks that have more potential given a long time horizon. This wouldn’t totally exclude mature companies with large market capitalizations but may include far more small and microcap opportunities than someone that is just a few years from retirement. If you are closer to retirement and don’t have as long for the growth to play out, the strategy may be to invest in large companies with stable dividends. If they throw off enough income, then an allocation of more speculative growth opportunities may make sense. This portfolio portion can allow for further growth.

Define Your Risk Tolerance

Before swimming in the deep end of investing, it’s important to assess your risk tolerance. Ask yourself how comfortable you are with potential fluctuations in stock prices. Small-cap stocks and microcaps, which represent companies with smaller market value, often offer greater growth potential, but they also come with increased volatility. Growth stocks, however, are known for their potential high returns over time, of course this could come with the cost of more volatility (sharp price moves) than established “blue-chip” stocks. Knowing your risk tolerance, or uneasiness with losing, or riding out drawdowns, versus gaining more than the potential loss (risk/reward tolerance) will help you make investment decisions aligned with your comfort level.

Determine Your Investment Style

After assessing your risk tolerance and setting goals, determine your investment style. Some investors prefer a more hands-on approach, engaging in frequent trading and closely monitoring stock market trends and evaluating stocks through websites like Channelchek. Others may prefer a more passive approach, investing in broad-based index funds or exchange-traded funds (ETFs) that provide diversification across various stocks. Understanding your investment style will help shape your overall investment strategy.

Minimizing Risk

Investing inherently involves risk, but there are strategies to help minimize potential losses. One approach is to conduct thorough research on companies you’re considering for investment. This includes analyzing company-sponsored research, equity research reports, and equity analysis provided by reputable sources. Understanding the financial health, competitive advantages, and growth prospects of a company can help you make informed investment decisions.

Developing an Investment Portfolio Strategy

Diversification is considered key when it comes to building an investment portfolio. Investing in a variety of stocks across different sectors and market capitalizations, including small-cap stocks and growth stocks, can help spread risk and potentially increase returns. Consider allocating a portion of your portfolio to IPOs if you have a higher risk appetite. However, it’s important to exercise caution as IPOs can be volatile shortly after their public debut.

Stay Informed

Keeping up with investment news is vital for any investor. Stay updated on market trends, company announcements, and economic indicators that may impact the stock market. Many financial news outlets provide lists of “stocks to watch” or provide insights into market trends. Regularly reviewing investment news and equity research can help you stay informed, make timely investment decisions, and expose you to opportunities you may not have discovered otherwise.

Take Away

Knowing it is time to start building an investment portfolio is a good first step. Now may be the when you should implement, especially if you have a long road ahead of you and financial security is important. It will require careful consideration of your risk tolerance, investment goals, investment style, risk management techniques, and portfolio strategy. Be prepared to conduct research, analyze equity reports, and stay informed about market developments. Investing is ordinarily long-term, patience, discipline, and a well-structured portfolio are key to achieving your financial objectives.

Image: Statue of Liberty Torch, Circa 1882 – Ron Cogswell (Flickr)

Current Technology May Be Leading the Next Shift in Stock Market Investing

Investor exposure to the stock market has grown and evolved through different iterations over the years. There is no reason to believe that it isn’t evolving still. The main drivers of change have been the cost of ownership, technology, and convenience, which are related to the other two drivers. There seems to be a new transformation that has been happening over the past few years. And with each change, there will be those that benefit and those that fall short. So it’s important for an investor to be aware of changes that may be taking place around them.

Recent History

Your grandfather probably didn’t own stocks. If he did, he bought shares in companies his broker researched, and he then speculated they would out-earn alternative uses of his capital – this was expensive. Mutual funds later grew in popularity as computer power expanded, and an increased number of investors flocked to these managed funds – the price of entry was less than buying individual stocks. Charles Schwab and other discount brokers sprang up – they offered lower commissions than traditional brokers. Mutual funds were able to further reduce fees charged by offering easier to manage indexed funds or funds linked to a market index like the Dow 30 or S&P 500. Indexed exchange-traded funds (ETF) took the indexed fund idea one step further – they have a much lower cost of entry than either mutual funds or even discount brokerage accounts. An added benefit to indexed ETFs is they can be traded at intraday prices and provide tax benefits.

Just as Schwab ushered in an era of low-commission trades, Robinhood busted the doors open to no-commission trades, and most large online brokers followed. This change allows for almost imperceptible costs in most stock market transactions. It also changed the concept of a round-lot, or transacting in increments of 100 shares. In fact, the most popular brokers all offer fractional share ownership now.

Are Index ETFs Becoming Dinosaurs?

Funds made sense for those seeking diversification of holdings, it used to take a large sum of money to do that; investors with a $10,000 account or more can easily achieve acceptable diversification with odd-lots and fractional shares ability.

Today investors can create their own index-like “fund,” or as they called it in your grandparent’s day, “portfolio management.”

One big advantage to creating your own portfolio, even if you rely heavily on stocks from a specific index to choose from, is that you can adapt it more toward your sector or company expectations. Indexed funds are stuck with their index holdings, they have no ability to change. One may increase or decrease risk by leaving out stocks or even whole industry groups. Also, it can be managed with greater tax efficiency than an index fund tailored to your situation.

There is also the DIY thrill that one gets from creating anything themselves rather than to just buying one off the shelf. There have been a number of renowned investors like Peter Lynch and Michael Burry warning that indexed funds no longer provide expected diversification and that many of the stocks are valued higher because so many dollars are on “auto-invest” into indexes that the bad has been pushed up with the good.

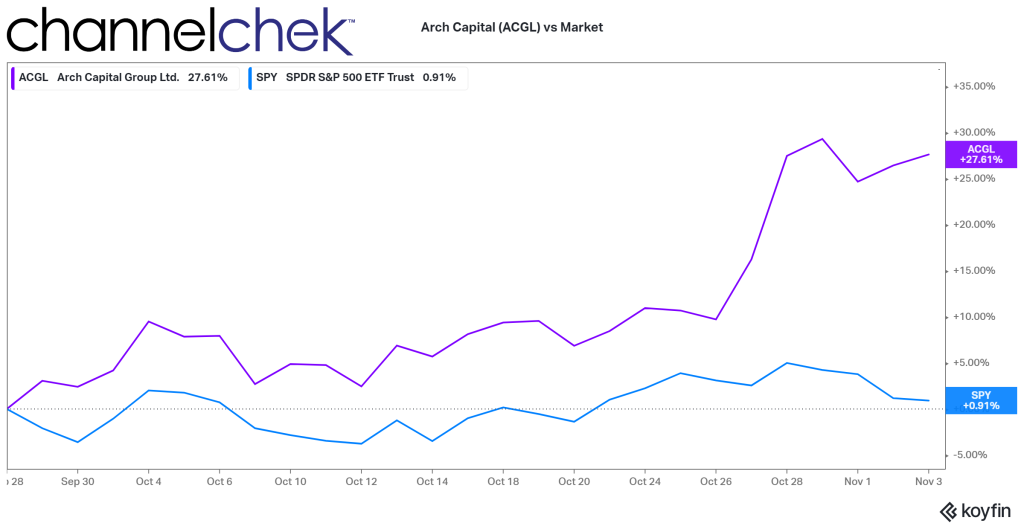

An example of what added demand does to the valuation of a company when being added to an index can be seen over the last month when it became clear that Twitter would be leaving an empty slot that would be filled by Arch Capital (ACGL). The added demand for ACGL pushed up the value by an estimated 25%. Was it undervalued before (when stand-alone), or is it over-valued now? Some stocks that are getting more attention because they are in an index could, as Michael Burry warned, be in bubble territory.

The more you do to ensure your portfolio weightings mimic an index, the closer your performance is likely to be to that index. You may want to limit your holdings to names that are actually in the index and shift the weightings for return enhancement. Another concern often cited with indexes is the way that they weight holdings; you may choose to weight your portfolio using the market capitalization of each company to own the same percentage of the company’s value or use another method like pure cost measures or cost per P/E.

Picking Stocks

While studies suggest that market diversification can be achieved by owning as few as five stocks and doesn’t improve much after 30 holdings, the more you own, providing they aren’t overweighted in a sector, it stands to reason the more diversification protection you can achieve.

As a DIY, self-directed investor, it makes sense not to chase after whatever YouTube influencer, loud-mouthed-TV analyst, or Stocktwit tells you. This is your baby, and the results, good or bad, are yours. Do what you can to make informed decisions, even if some turn out unexpected. The benefit of this is you can lean away from stocks that are still in indexes that don’t have good future prospects and lean into more companies that do.

I’m hearing from more of my self-directed investor friends and investment advisors that more people are looking to own companies that have non-financial objectives they, as an investor, support. And for some of them, there is no standard ESG framework that they support. They have decided, because they do care, to do more portfolio management with individual stocks than before. This is so they can individually look under the hood at employee policies, or environmental stature, etc. While ESG funds exist, the investor or client of the investment advisor would prefer not to own anything they oppose if they can avoid it. What better way than being able to say no to $XYZ company because they do this, this, and this that is against my own fabric?

Channelchek is a great resource for any percentage of your personally managed fund that includes stocks in the small-cap or microcap categories. These stocks could add a bit more potential for return but could also change your risk characteristics. Sign-up to get research from FINRA-licensed analysts.

Take Away

Stock investing has evolved and become more inclusive. But the future may be more like the past, with individuals creating portfolios of stocks for themselves. You don’t have to be rich anymore to buy stocks, and you don’t have to own a fund to get affordable diversification on nearly any size account. There’s a trend toward building one’s own personalized, diversified, low-transaction portfolio. Channelchek is helping investors find possible fits with its free research platform.

Robinhood’s Latest Step Could Increase the Influence of its Customers

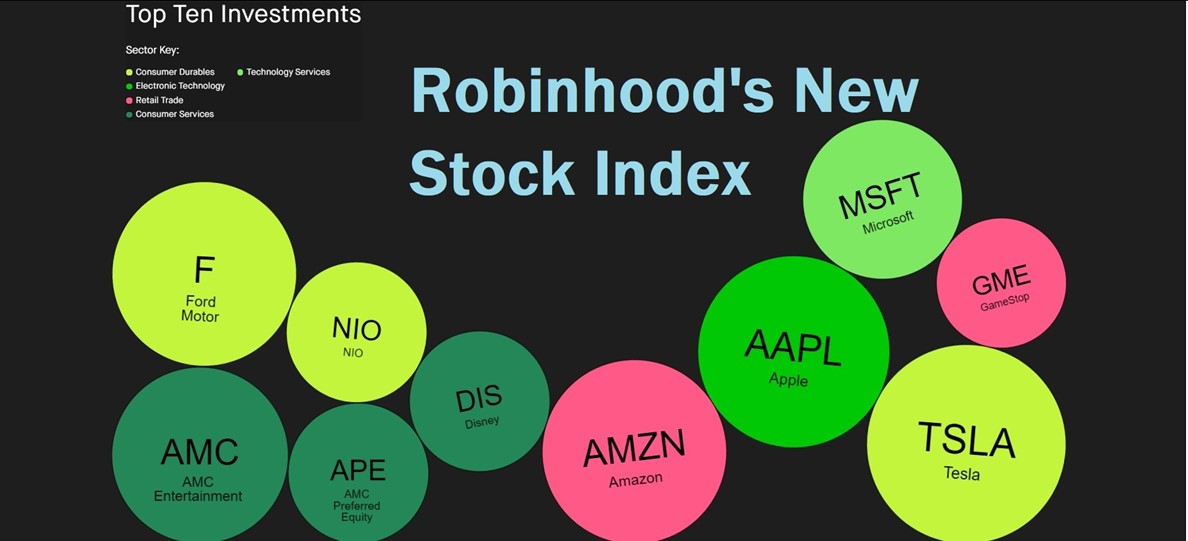

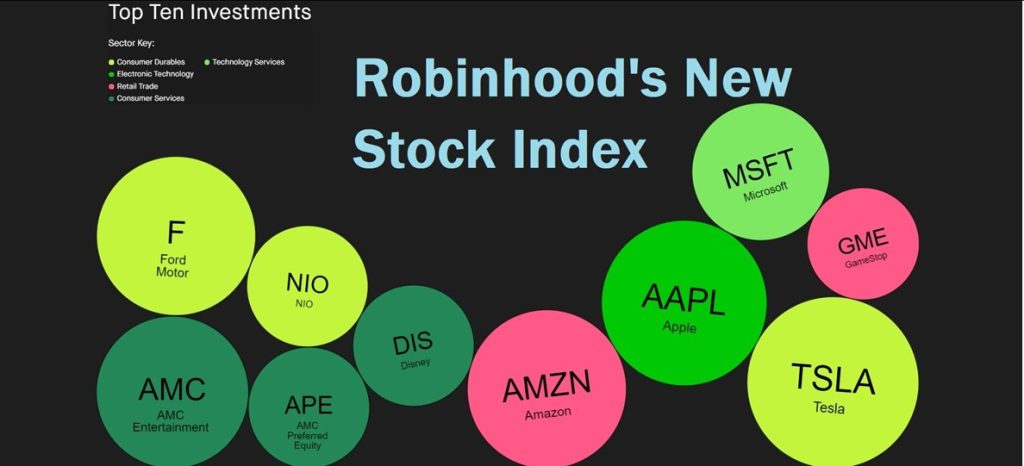

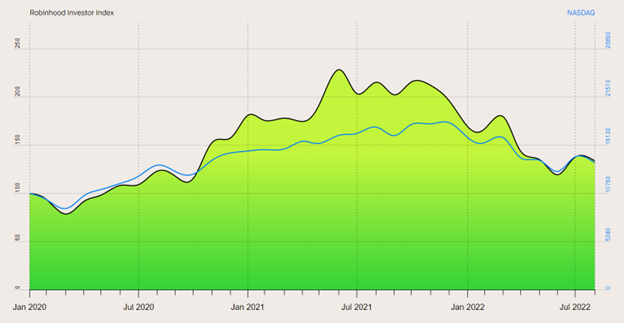

Robinhood made an exciting announcement at the close of business last week that went largely unnoticed. It is creating an index consisting of the most held stocks by its customers. For Robinhood ($HOOD) users and everyone else, this unique index will be useful intelligence to help serve as a barometer as to what top stocks users of the brokerage app are adding and which they are paring down. The Robinhood Investor Index will be based on the top 100 most owned stocks and is unique in how it is configured and weighted.

About the Index

The Robinhood Investor Index presents an aggregate view of its customers’ top 100 most owned investments (does not account for shorts) and tracks the performance of those investments. Unlike the S&P 500 or Nasdaq 100, the index isn’t weighted by the size of the company but instead by the “conviction” of the 20+ million investors using the app.

Robinhood will take a monthly snapshot of holdings of each ticker and look at the percentage each comprises of each customer portfolio. They’ll ensure that all customers are equally included by averaging the conviction for each investment across all customers. In this way, whether clients have $500 or $500,000 in their account, it is the weighting per account percentage, not shares or dollar value.

Robinhood plans to update the index once a month and will share the valuable insights reflecting where its customers are allocating their assets in the index. Robinhood says its data tells them that customers invest in the companies they’re passionate about, and the Robinhood Investor Index aims to make this known.

The index weights are re-calculated at the beginning of each new month, using data from the last trading day of the previous month. These monthly updates are expected to be published on a dedicated site within five trading days after the first trading day of each month. The index inception date for performance measurement is January 2020.

Performance

Robinhood says its customers tend to invest in what they know, entertainment, technology, and non-obscure staples in most of their lives.

For comparison, below is a look back to the beginning of 2020 (index inception date) comparing the Nasdaq 100 (NDX) in blue to the Robinhood Investor Index (RII) in green. Robinhood has shared that the evolution of its customer’s portfolios have shown an increased conviction to growth in electric vehicles with Tesla at the top, and growth in Ford and NIO, which has moved these holdings up the ranking system. Entertainment is also well represented, with Disney and AMC consistently among the top stocks. The sector representation, is diversified, also spanning financial services, energy and healthcare.

Overall, the RII leans towards large cap stocks with 75% in large-cap, 16% in midcap and 9% in small-cap.

The Nasdaq Composite Index is a market capitalization-weighted index of more than 3,600 stocks listed on the Nasdaq stock exchange. The index is constructed on a modified capitalization methodology. This modified method uses individual weights of included companies according to their market capitalization. Similar methods are used for other often quoted market indices. The holdings captured in the Robinhood index are directly invested in by its users and weighted in the proportion weighted in each of the user accounts.

The sectors are defined using the FactSet Revere Business and Industry Classification System (RBICS). Sectors may be excluded if they are not among the holdings with the highest conviction.

Market capitalization evaluation is broken into three categories, large-cap (greater than $10 billion), midcap (between $2 and $10 billion), and small-cap (between $300 million and $2 billion). The RII does not include securities considered microcap (below $300 million).

Take Away

This new index could be of interest to financial professionals and other traders that monitor the activities of retail investors as a factor behind stock-market moves. The average age of Robinhood account holders is 32, this demographic has become an increasingly powerful driver of movement and it will be worth monitoring its trends.

Channelchek reports on index changes that we believe impact our readers. The Robinhood Investor Index, now in its infancy, will certainly be reported on in its early stages.

Sign-up for Channelchek news and research free to your inbox each day.

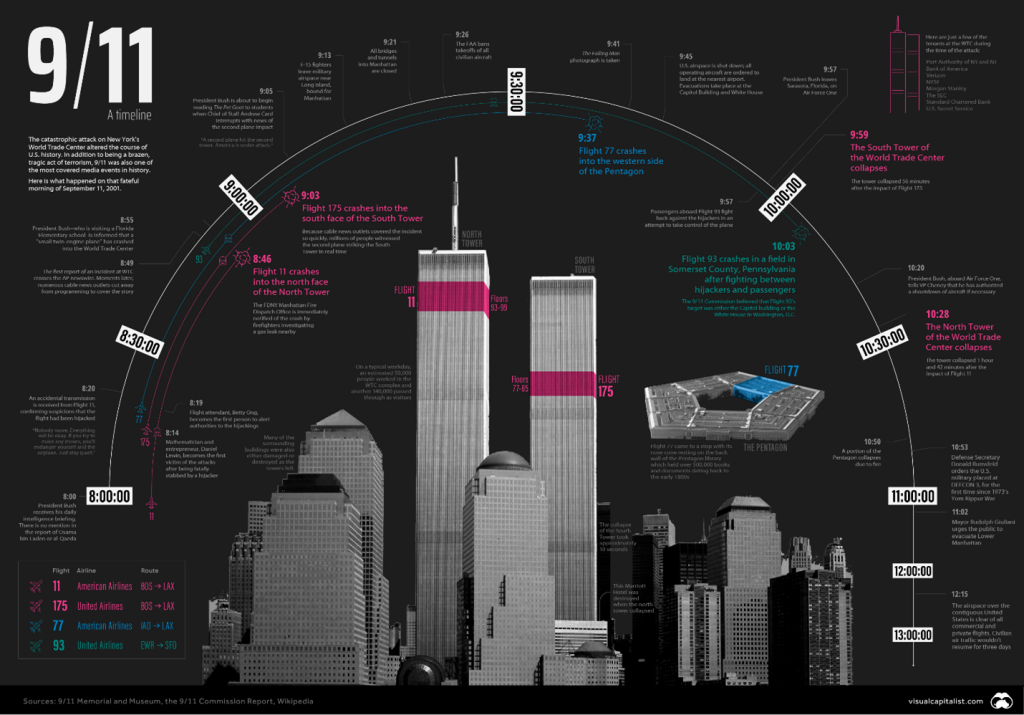

September 11, a Retrospective Account of Investment Fallout and Recovery

I wasn’t in New York City on September 11, 2001. Just prior to 911, I had taken a position as CIO for a major Wall Street firm headquartered in lower Manhattan; however, the trading floor I was responsible for was about 50 miles east of ground zero. I took the position outside NYC to be closer to my home and family – the benefit of my decision became apparent all at once, at 8:45 am that Tuesday morning, then reinforced 18 minutes later.

Twenty-one years have passed since then, the children of the deceased are now adults, and financial activity is spread much further than one small area in lower Manhattan. Although much has changed, it’s important to look back and recognize how the investment markets handle devastation and, at the same time, recognize how humans here and around the world will band together when others need help.

The opening bells at the New York Stock Exchange (NYSE) and Nasdaq were silent at 9:30 that morning. They remained silent until September 17, as traders and investors feared what their positions would be worth upon the reopening of the financial markets after the longest close on record.

Once reopened, the Dow Jones fell 7.1% or 684 points, setting a record at the time for the highest one-day loss in the exchange’s history. By Friday, the NYSE had experienced the greatest one-week decline in its history. The Dow 30 was down more than 14%, the S&P 500 plunged 11.6%, and the Nasdaq dropped 16%. In all, about $1.4 trillion in wealth disappeared during the five trading days. Since then, this record has only been surpassed once at the early stages of the pandemic.

In hindsight, the industries most negatively impacted make sense. Airlines and the insurance sectors lost tremendous value. A flight to quality made gold popular as the price per ounce leaped 6% to $287.

Gas and oil prices quickly rose as fears that oil imports from the Middle East would be slowed or stopped altogether. Those fears lasted about a week; then, after no new attacks and a clearer understanding of the intentions of government officials, index levels returned to near their pre-911 levels.

The sectors that experienced major gains after the attacks include technology companies and certainly defense and weapons contractors. Investors anticipated a huge increase in government borrowing and spending as the country prepared to root out terror around the world. Stock prices also spiked for communications and pharmaceutical companies.

On the U.S. options exchanges, volatility in the markets caused put and call volume to increase. Put options, designed to allow an investor to profit if a specific stock declines in price, were purchased in large numbers on airline, banking, and publicly traded insurance companies. Call options, designed to allow an investor to profit from stocks that go up in price, were purchased on defense and military-related companies. Short-term profits were made by investors who were quick to execute.

The terrorism of September 11 will, doubtless, have significant effects on the U.S. economy over the short term. An enormous effort will be required on the part of many to cope with the human and physical destruction. But as we struggle to make sense of our profound loss and its immediate consequences for the economy, we must not lose sight of our longer-run prospects, which have not been significantly diminished by these terrible events. – Fed Chairman Alan Greenspan, September 20, 2001

Since September 11

Over the following 21 years, the major U.S. stock exchanges have taken steps to make physical disruption of trading more difficult. This includes dramatically increasing the percentage of trading that is electronic. While this has made the U.S. markets less vulnerable to physical attacks, it is feared that there is increased potential for cyberattacks. “As we have digitized our lives, which has generally been a great blessing, we have sown the seeds for even greater destruction in terms of the ability to hack into our systems,” said former Securities and Exchange Commission Chairman Harvey Pitt, who led the agency on Sept. 11, 2001. “That is today’s equivalent of a 9/11 attack. There is a potential ‘black swan’ event every single day.”

Major Market Indices Since September 11, 2001 (Source: Koyfin)

The investment markets have enjoyed above-average upward movement, despite the negative short-term impact of the black swan event. In the nearly 20 years since Sept. 11, the S&P 500, Nasdaq 100, and Russell 2000 Small-Cap index has risen more than four-fold. The bond market has also been strong (persistent low rates) despite increased borrowing to fund defense operations to finance America’s 911 response.

The U.S. economy itself has had long periods of expansion since 2021, even with the mortgage market crisis from December 2007 to June 2009, and the economic challenges from the response to the COVID-19 pandemic.

The costs, however, are likely to continue to be borne by taxpayers for generations. Interest-related costs alone on debt which financed military operations, including the long Afghanistan war, which was resolved last year when the U.S. withdrew after 20 years, and the protracted conflict in Iraq from 2003 to 2011, are high. The economic drag of these costs, while not fully measurable, are real.

The U.S. government financed the wars with debt, not taxes. Interest rates have been low, but taxpayers have already helped pay approximately $1 trillion in interest costs on the debt incurred to finance the two wars. These interest costs are expected to balloon to $2 trillion by 2030 and to $6.5 trillion by 2050 (according to the Watson Institute at Brown University). This places upward pressure on interest rates and places downward pressure on economic activity. One reason is that taxes used to fund interest costs take money from the economy without providing any stimulus or new material benefit.

Off Wall Street

September 11 radically changed the national mood and political environment. Polls and surveys taken just before the 911 attacks found Americans growing less certain about the direction of the country as a recession began to weigh down the ability to be optimistic. A full 44 percent of the country thought it was headed in on the wrong direction, according to the August 29-30, 2001 New Models survey.

Logic might suggest that after a successful attack, people’s attitudes toward the direction of the country would trend toward a worse future. Reporters, politicians, and spokespeople all predicted a terrible economic shock; their forecast seemed supported by the first week’s plunge in markets. But the events of that day seemed to give citizens purpose. In fact, statistics that indicated the “direction of the country” showed that optimism surged. An October 25-28 CBS/NY Times survey reported that people felt the country was headed in the right direction by a two-to-one margin. A sense of pride in who we are as a country and as individuals overcame negative economic news in an unprecedented way.

Take Away

It has been over two decades since what many of us think of as recent. The truth is, children born on September 11, 2021 or before are now of drinking age. But history can prepare us for new events. The market’s first reaction to tragic news is always down; when proven temporary, bargain hunters come in, then the market has always resumed its historical growth trend upward.

The markets now trade more digitally with almost no need for runners in lower Manhattan and far less open-outcry and paper jockeying by masses of people working for companies in one small section of Manhattan island. But the new threats are also real, a cyber attack on electronic records or transactions could be devastating in its own way.

Challenges even those caused by tragedy provide opportunity and even purpose. September 11, and its aftermath are proof of this.