FOMC Now Contending With Banks and Sticky Inflation

The Federal Reserve is facing a rather sticky problem. Despite its best efforts over the past year, inflation is stubbornly refusing to head south with any urgency to a target of 2%.

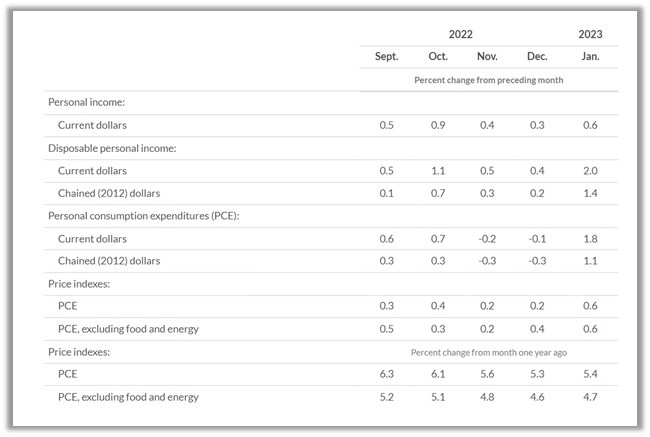

Rather, the inflation report released on March 14, 2023, shows consumer prices rose 0.4% in February, meaning the year-over-year increase is now at 6% – which is only a little lower than in January.

So, what do you do if you are a member of the rate-setting Federal Open Market Committee meeting March 21-22 to set the U.S. economy’s interest rates?

The inclination based on the Consumer Price Index data alone may be to go for broke and aggressively raise rates in a bid to tame the inflationary beast. But while the inflation report may be the last major data release before the rate-setting meeting, it is far from being the only information that central bankers will be chewing over.

Don’t let yourself be misled. Understand issues with help from experts

And economic news from elsewhere – along with jitters from a market already rather spooked by two recent bank failures – may steady the Fed’s hand. In short, monetary policymakers may opt to go with what the market has already seemingly factored in: an increase of 0.25-0.5 percentage point.

Here’s why.

While it is true that inflation is proving remarkably stubborn – and a robust March job report may have put further pressure on the Fed – digging into the latest CPI data shows some signs that inflation is beginning to wane.

Energy prices fell 0.6% in February, after increasing 0.2% the month before. This is a good indication that fuel prices are not out of control despite the twin pressures of extreme weather in the U.S. and the ongoing war in Ukraine. Food prices in February continued to climb, by 0.4% – but here, again, there were glimmers of good news in that meat, fish and egg prices had softened.

Although the latest consumer price report isn’t entirely what the Fed would have wanted to read – it does underline just how difficult the battle against inflation is – there doesn’t appear to be enough in it to warrant an aggressive hike in rates. Certainly it might be seen as risky to move to a benchmark higher than what the market has already factored in. So, I think a quarter point increase is the most likely scenario when Fed rate-setters meet later this month – but certainly no more than a half point hike at most.

This is especially true given that there are signs that the U.S. economy is softening. The latest Bureau of Labor Statistics’ Job Openings and Labor Turnover survey indicates that fewer businesses are looking as aggressively for labor as they once were. In addition, there have been some major rounds of layoffs in the tech sector. Housing has also slowed amid rising mortgage rates and falling prices. And then there was the collapse of Silicon Valley Bank and Signature Bank – caused in part by the Fed’s repeated hikes in its base rate.

This all points to “caution” being the watchword when it comes to the next interest rate decision. The market has priced in a moderate increase in the Fed’s benchmark rate; anything too aggressive has the potential to come as a shock and send stock markets tumbling.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Christopher Decker,Professor of Economics, University of Nebraska Omaha.

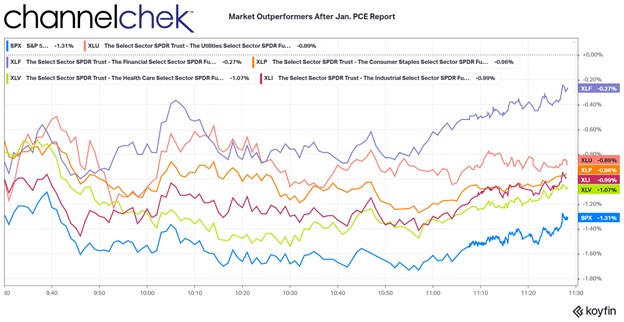

What Sectors Outperformed the Market after the PCE Inflation Shock?

When an investor inquires, “What stocks do well with high inflation?” they are often asking, “What sectors do well with rising interest rates?,” because inflation expectations often drive rate moves. The text book response usually given are: consumer staples, banks and financials, and commodities. The PCE indexes are considered the Fed’s preferred indicator of inflation trends. The PCE surprised markets on the high side when released on February 24th. What can investors now expect from higher-than-forecast inflation?

Rather than look at old information on what outperforms the overall market when inflation expectations rise, I thought it would be informative and more useful to see what is outperforming under current 2023 conditions and climate. The chart below and the remainder of this simple study is a snapshot three hours after the news settled in among investors (11:30am ET, February 24th).

There were five S&P sectors that outperformed the S&P 500 a few hours after the inflation number showed an almost across-the-board acceleration in price increases. At this point, the S&P 500 had already fallen 1.31%.

Beating the S&P larger index, but the worst of the five outperformers was Health Care (XLV). The Health sector is considered to be a necessity that consumers find a means to pay for regardless of cost. Within the sector there are companies providing goods and services that are more embraced by investors than others. Within the XLV, many stocks were green after the report.

Outperforming the Health Care sector were stocks making up the Industrial Sector (XLI). This includes large industrial manufacturers like John Deere, General Electric, and Caterpillar. Many of these companies have contracts well out into the future that assures business. What is not ordinarily assured is the cost of manufacturing which can go up with inflation. A number of the top holdings in XLI barely budged on the morning – GE was up .08%, Honeywell was down .18%, and UPS was down just .20%.

Almost even with the Industrial Sector was Consumer Staples (XLP). As with Health Care and to a lesser degree Industrials this sector is where money moves to during inflationary periods. Consumers may be postpone a new car purchase, but they’ll keep their buying habits unchanged for products produced by Colgate, Coca-Cola, Proctor and Gamble, or cigarette manufacturers.

Performing second best after the inflation numbers was the Utility sector (XLU). Again this follows the mindset that consumers can only cutback on water, electricity, and natural gas so much. It is more likely that cutbacks would come in other areas like entertainment, or technology. Technology was the worst performing sector.

The top performer, although still modestly negative, was the Financial sector. This includes insurance, banks and credit card companies, as well as investment firms. Banks, particularly those with a higher percentage of traditional banking business, benefit from a steepening yield curve. Banks use cash as their product line. They borrow short from customers, and lend longer term. As the yield curve steepens, their net income can be expected to rise. This may explain why two of the top three holdings were positive after the report, JP Morgan (JPM), and Wells Fargo (WFC). Brokerage firms also may benefit as accounts uninvested balances can be a source of revenue as financial firms earn interest on them. Rising rates means every balance they can earn on creates additional income.

Larger Index Observations

As indicated earlier, technology was the worst-performing sector. This causes the tech heavy Nasdaq to far underperform the other major indexes. The best performing a few hour after the open was the Dow Industrials, which is comprised of just 30 industrial stocks, many paying consistent dividends. The second best performer, beating both the Dow and S&P 500 was the Russell 2000 Small-Cap index. Small-cap stocks tend to be less affected when borrowing costs change, and tend to have more of their end customers located domestically. The U.S.-based customers is an advantage to smaller stocks when rising rates cause rising dollar values. A rising dollar makes goods or services from the U.S. more expensive overseas.

Take Away

The textbook reply to questions related to rising rates, inflation, and sector rotation in stocks held up after the surprise PCE index increase. Banks, and necessities like heat and consumer goods outperformed. Also small-cap stocks did not disappoint, they also held up better than the overall large cap universe.

One difficulty small and even microcap investors face is that information is less available on many of these companies. And there are a lot of them, including in the sectors that outperform with inflation. One easy way to find which smaller companies are rising to the top is Channelchek’s Market Movers tab. This can be viewed throughout the trading day by clicking here for the link.

Investors Receiving a 5% Yield are Losing to Inflation

The CPI inflation report and the Fed’s relentless increases in Fed funds levels have pushed the six-month US Treasury Bill (T-Bill) above 5%. This is the first time since 2007 that this low-risk investment has topped 5%. Last year on this date, the six-month T-Bill was 0.76%. While the stock market is concerned that higher borrowing costs will have the Fed’s intended effect of slowing demand, rates are reaching a point where another concern creeps in. The concern is will traditional stock investors lay back and be satisfied getting paid interest.

More likely, the high cash position represents “dry powder” waiting for an opportunity.

Short Term Rates

Money Market fund assets were $4.81 trillion for the week ended Wednesday, February 8, according to the Investment Company Institute. Just shy of the record MF balances reported in January. Higher than average cash levels have often been thought of as a bullish sign as it represents potential to drive stock prices up when flows toward equities increase.

This may be part of the situation as we come off a dismal 2022 for equities, but there is likely something else incentivizing the retreat to safety. The higher interest rates are in the short end of the curve, investors are getting paid to retreat. High-yielding cash equivalents with six-month T-Bills now at 5% (10-year Treasuries are only 3.75%) may be more than a parking place. It may represent an alternative investment with a much more assured return.

With inflation at 6.4%, the answer is no. But it is definitely preferable to seven of the periods on the 10-year chart above. And with January’s consumer price index (CPI) report revealing signs of sticky to reaccelerating inflation, the Federal Reserve is more likely to be hiking rates for longer than expected.

For investors looking to invest for longer periods, the stock market handily beats inflation. In other words, for the various time frames below, S&P 500 investors did not see their assets erode due to inflation.

Beating inflation is foundational to investing. Far exceeding it is the goal of many. Investors are not doing this choosing cash, in fact they are choosing to lose buying power rather than risk that the market doesn’t perform as it has historically.

Data released on Tuesday February 14 showed the inflation rate (CPI) slowed to 6.4% in January. The cost of goods and services rose 0.5% during the month. The half percentage is the largest one month erosion of purchasing power in three months.

Investors content with 4%-5% returns should consider that they are losing ground to persistent inflation.

Investors with a five-year time horizon or longer should weigh the risks of earning yields below the inflation rate to the ups and downs of stocks. In fact, as more do, the 4-5 trillion in cash can make or quite a bull market.

Is the Mismatch in Workers and Open Jobs Proving to Be Transitory?

Inflation has been the most bearish word for the stock and bond markets over the past year or more. Shortly after many of the supply chain issues cleared up, and the cargo ships were no longer stacked up outside of major ports, attracting scarce workers with higher pay became a growing cause of inflationary pressure. At the end of November 2022, Federal Reserve Chair Jerome Powell stated that “job openings exceed available workers by about 4 million.” That number has now grown to 4.7 million after the continued strengthening of the market for qualified labor.

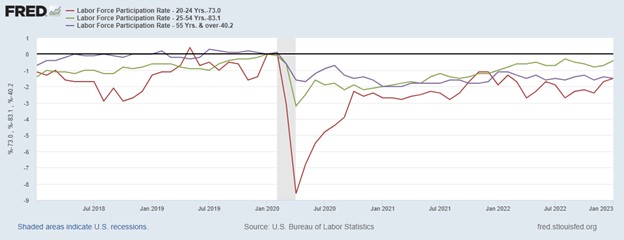

This mismatch, depicted in the Fed Data below, between available positions and workers to fill them, developed a more inflationary trend. The graph depicts the mismatch of labor supply and demand and the extent that it has worsened.

When the civilian labor force is greater than employment plus job openings, the economy has an immediate capacity to fill open positions. Currently, the employment level plus job openings are at 170.5 million, while the total labor force is at 165.8 million. Thus the 4.7 million quoted earlier. There are a whopping 4.7 million more jobs available compared to people available to fill them.

The civilian labor force, the amount of people working or looking for a job, is shown below in red; the current employment level plus the number of job openings is shown in blue.

The pandemic has been emphasized as a cause of this not-very-transitory labor shortage, but the trends in labor demand and labor supply in the graph above indicate that demand was already outpacing supply as the US entered 2018. This was two years before the novel coronavirus hit US shores. Back then the mismatch was about one million workers fewer than jobs available before the economic disruption.

As the US began to move toward business-as-usual, news and market analysts offered many explanations for the labor shortage. These included childcare problems, health concerns, minimum wage pushback, and even a wave of new retirees.

The visual below shows the change experienced in the labor force participation rate (LFPR) for specific age groups: 20 to 24 years old, 25 to 54 years old, and 55+ years old. By subtracting the most recent LFPR from that of January 2020 we get the percentage-point change in labor force participation relative to the month just before the pandemic began impacting businesses.

When the pandemic hit, the sharpest decline in the LFPR was for workers between the ages of 20 and 24. Their LFPR decreased from 73% to 64.4% in 4 months before increasing again. However, at the end of 2022, the LFPR for 20- to 24-year-olds still hadn’t fully recovered and remained 1.7 percentage points below its January 2020 value.

This overall pattern is similar but less extreme for the other age groups. Although no age group fully recovered by the end of 2022, the 25-54 group was closest, at 0.7 percentage points below its January 2002 level. There’s been speculation older workers retired early (and permanently) during the pandemic, and the 55+ group remained 1.4 percentage points below its January 2020 level as of December 2022, with no sign of further recovery.

The mechanisms that cause inflation are widely understood. If there is a shortage of goods because of the supply chain, sellers can ask more for the product. If the cost of producing goods or providing services increase, perhaps because of the cost of labor, the seller may try to pass those higher costs along. On the demand-pull side, if there is an abundance of currency, this increases demand for goods and services and is also inflationary.

While the Fed has been waging a fight against rising prices by removing liquidity and ratcheting up the cost of money (interest rates), the number of open jobs compared to the number of workers available to fill them has widened.

The Increasing Popularity of the PCE Inflation Gauge

US inflation, by a number of official measures, reached its highest level in 40 years last year. For a large percentage of investors and shoppers, this is their first experience of prices quickly rising. For decades, on many tech products, prices declined over time (while adding functionality). There are a number of different measures of inflation reported regularly – they impact us in different ways. Knowing the difference, whether you’re investing, planning a purchase, or expecting a cost of living (COLA) increase, is helpful. Below we go through the different measures so you understand the impact of say “headline CPI” versus “core PCE.”

According to James Bullard, the president and CEO of the Federal Reserve Bank of St. Louis, “measuring inflation is one of the most difficult issues studied by economists.”

By definition, inflation is the percentage change in overall prices in the economy over a specified period, commonly quoted as a year-over-year change. It’s much more than an increase in the prices of a few products. Given the inherent difficulties in following every price in the country, economists have created price indexes to approximate the overall price level.

PCE Inflation

Before the year 2000, the Federal Open Market Committee (FOMC) primarily focused on the Consumer Price Index (CPI) as its inflation gauge. We’ll explain CPI next, but for the Fed, when it now says it has a 2% inflation target, PCE is the data used.

Though the two indexes have a lot of overlap, there are reasons why the PCE is considered a better tool by policymakers.

The PCE price index, which rose 5.5% in November 2022 from a year earlier, is derived from a broader index of prices than the CPI’s more narrow set of goods and services. The argument as to why policymakers gave an edge in the late 1990s to make the change in 2000 is that a more comprehensive index (such as PCE) of prices provides a better way to gauge underlying inflationary pressures. Since the PCE includes more goods and services, the index’s weights for particular items will differ dramatically from those in the CPI. For example, housing has a weight of about 16% in the PCE price index versus 33% in the CPI. The varied items more accurately reflect actual costs to consumers since they may substitute one for another as prices of items change at different rates. This ability to substitute is a primary reason why PCE tends to print lower than headline CPI.

CPI Remains Important

The most widely cited measure of inflation is the headline Consumer Price Index (CPI), which is calculated by the Bureau of Labor Statistics (BLS). This index was created in 1919 as officials devised a way to measure rising consumer prices just after World War I.

The CPI, which rose 6.5% for all of 2022, measures the price changes for a basket of goods and services purchased by the typical urban consumer. The items in this basket are weighted by their relative importance in consumer expenditures. For example, housing—rent and other spending on shelter—accounts for 33% of the index, while medical care accounts for nearly 9%.

This index, like others, takes into account changing consumption. New items come in and old items leave. The example I like to use is that prohibition began in January 1920, just after CPI came into use. Alcohol was not part of the index back then, whereas it is today (5.78% increase in 2022), product adoption changes.

The CPI weights had been adjusted every two years using two years of consumer spending data. Starting in 2023, the BLS will update weights annually using one year of data.

Headline PCE Inflation versus Headline CPI Inflation

The increasing popularity of the PCE is because the index’s weights are updated monthly, versus annually for CPI (prior to 2023 updates were every two years). Thus, the PCE can quickly reflect the impact of new technology or an abrupt change in consumer spending patterns. For example, the onset of the coronavirus pandemic quickly shifted consumption from services like restaurants to services like communication technology. Since the headline PCE uses more timely, actual outlays, it provides the FOMC a more accurate consumer experience in terms of inflation.

The stated target by the FOMC is 2%, a level that policymakers judge to be consistent with achieving price stability and maximum employment. On average, inflation was hovering below this target before the pandemic’s economic ramifications (from 1995 through 2019 PCE average equaled 1.8%).

Other Inflation Measures

While the FOMC targets headline PCE inflation, policymakers also watch other measures to gauge inflationary pressures. The headline PCE measure can be quite volatile due to the effects of extreme price movements for certain products. To get a sense of where underlying inflation really is, economists often look at some summary measure of inflation that doesn’t include these volatile prices.

A so-called “core” index—whether it be PCE or CPI—excludes food and energy components. That has some simplicity around it, but it’s not satisfactory. There are better ways to analyze underlying inflation than to throw out certain goods and services, especially those that hit low- to moderate-income consumers the hardest when prices rise. And even if you exclude food and energy prices, the remaining part of the index is still affected by their volatility; restaurant prices would be a classic example.

More recently, other statistical ideas have been developed. One method looks at price change distribution for the entire range of goods and services.3

One commonly used measure of this type is the Dallas Fed trimmed-mean PCE inflation rate, which removes the upper tail (the largest price changes) and the lower tail (the smallest price changes) and then takes a weighted average of the price changes for the remaining components. This measure has been popular as a tool for examining trends and overall inflation as opposed to special factors that might be driving inflation. Of course, these types of measures4 tend to be more persistent and move more slowly than headline inflation measures.

Take Away

While market concerns over inflation for many years were low and most may have been more concerned about deflation, the current tight supply of goods and labor, coupled with the easiness of money, has ushered in a period where markets are likely to feel the impact of each inflation post.

Understanding the most watched inflation gauges will help sort out whether a trend or single post is likely to cause a change in course on interest rates. Or is it more likely a blip that will on average work its way out? The Fed is currently targeting a PCE inflation rate of 2%. The current pace is more than double this, but trending down after the Fed tightened in 2022 at a record pace. The Fed and the markets are now awaiting the impact of those cuts as there is a lag in applying the economic brakes (to lessen inflation) and when the economy has its biggest reaction to the Fed’s heavy pressure on the brake pedal.

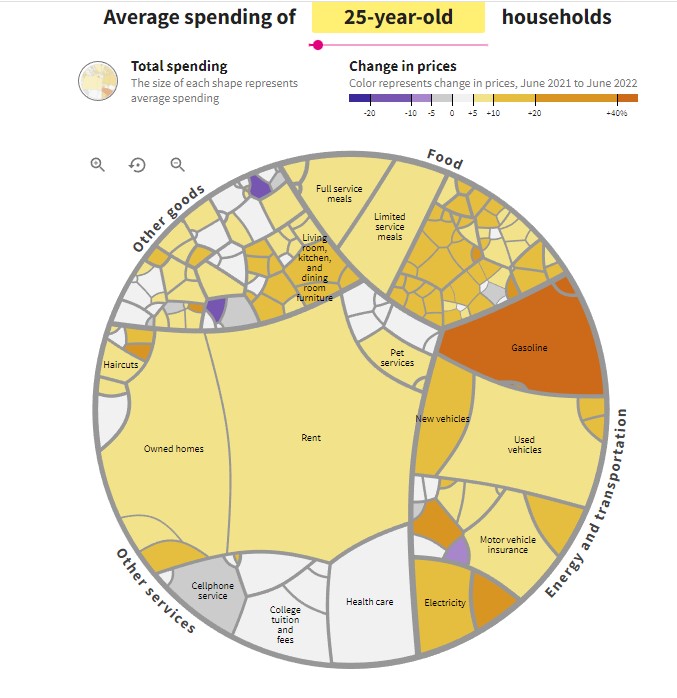

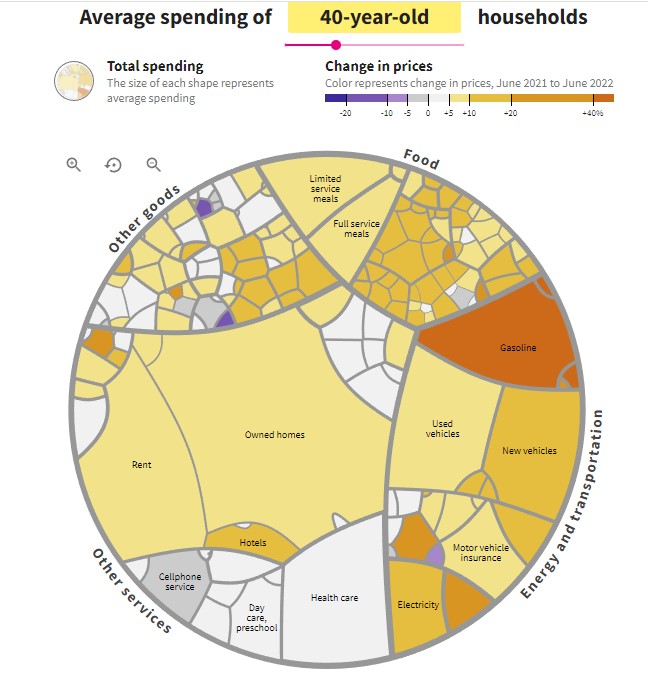

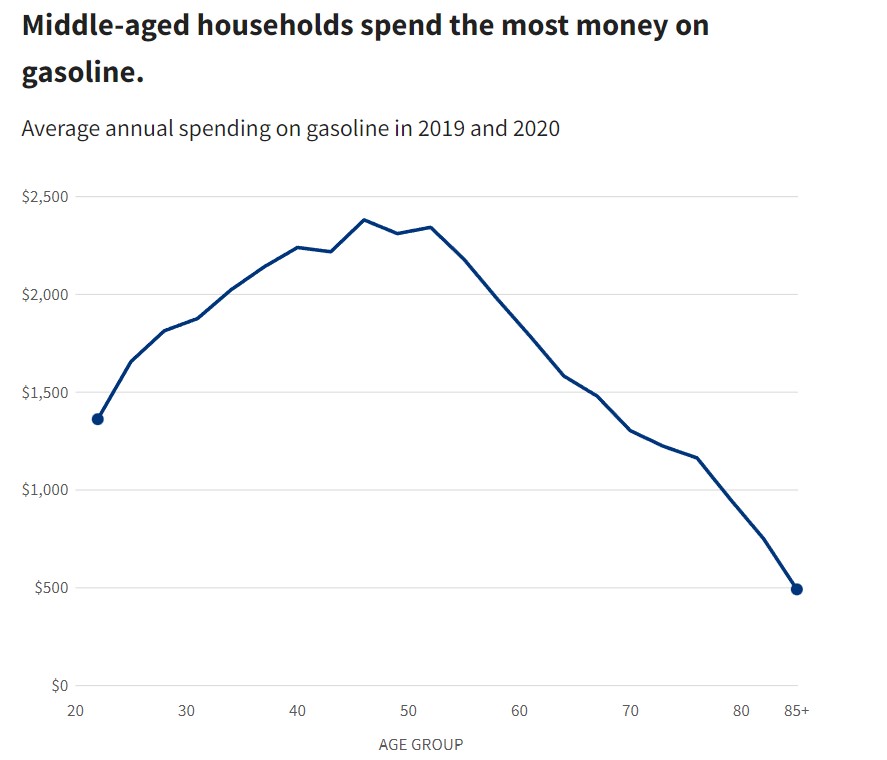

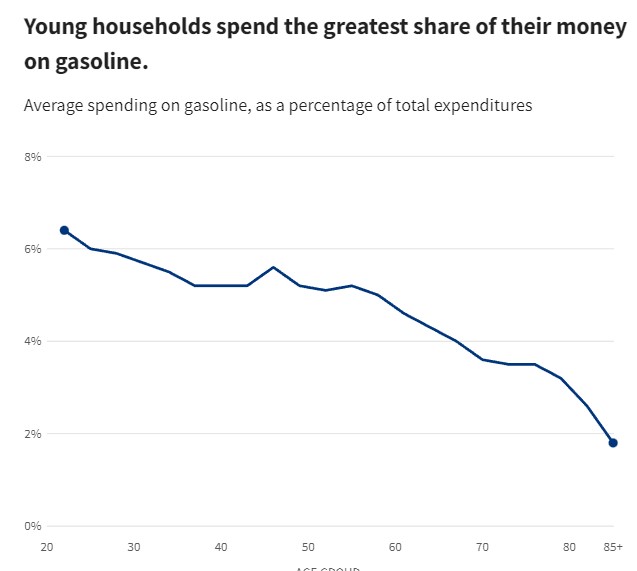

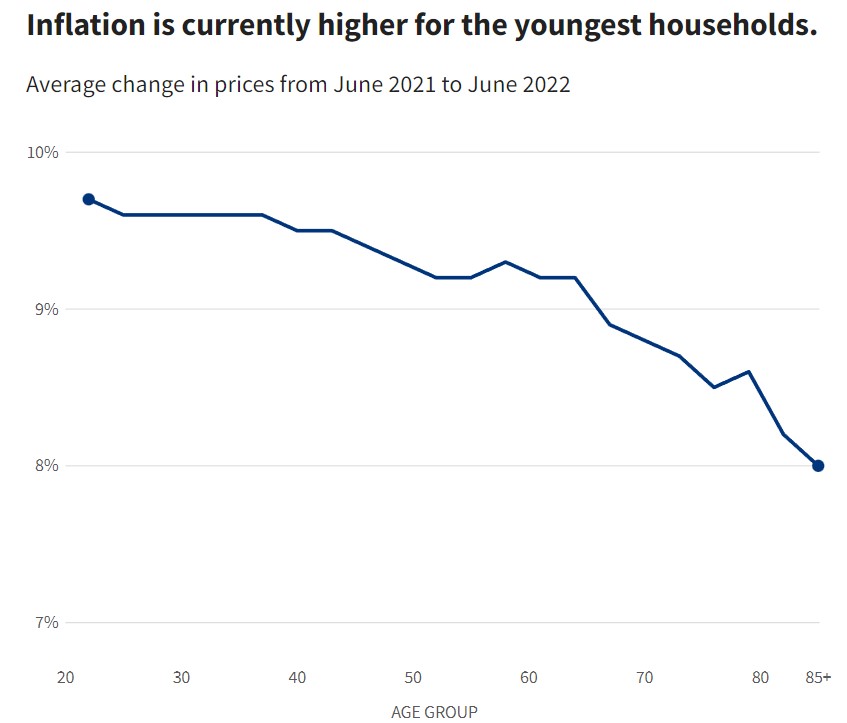

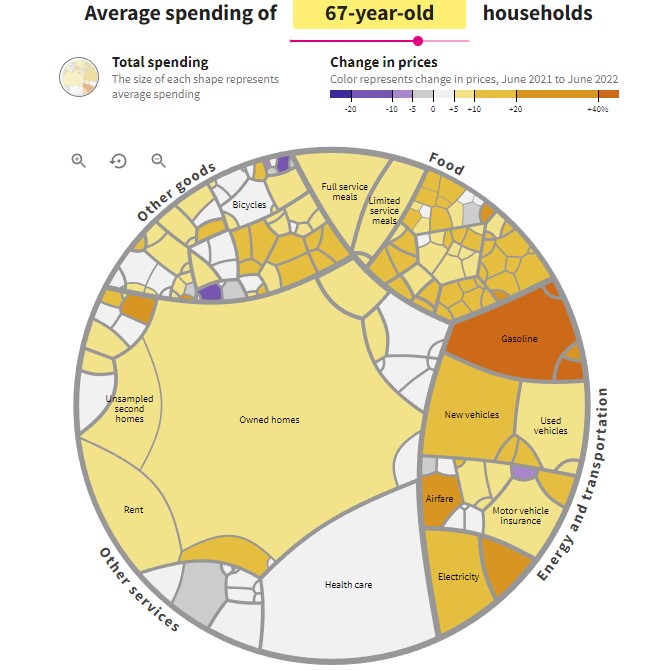

According to the Bureau of Labor Statistics, consumer prices rose 9.1% from June 2021 to June 2022, the highest rate since 1981. That figure is an average of price increases for bananas, electricity, haircuts, and more than 200 other categories of goods and services. But households in different age groups spend money differently, so inflation rates vary by age, too. The diagrams below show average spending for households at different ages, in the categories that make up the inflation index.

Young households spend more of their budgets on gasoline, where prices rose 60% in the last year. Gasoline has been the largest single-category driver of inflation since March 2021, accounting for nearly 25% of inflation by itself. Gas has had an outsized impact considering that the category is 4.8% of Consumer Price Index spending. (Gasoline prices began falling in mid-June.)

Taking an average of all categories, as the inflation index does, shows that inflation is currently highest for younger households. It is about 2 percentage points higher for households headed by 21-year-olds as it is for octogenarians who live at home. That has not been true for most of the last 40 years. Inflation rates calculated in this way were higher for older households as recently as early 2021, when medical care costs were rising faster than gasoline prices.

These estimates are imperfect. The Bureau of Labor Statistics notes in its estimate of inflation for elderly households that different age groups may buy different items within each category or buy them from different types of stores. They may also live in locations with costs of living so dissimilar that national changes in prices are not relevant. Over the past 12 months, inflation was 6.7% in the New York City metropolitan area and 12.3 in the Phoenix metropolitan area, due in part to different housing markets.

The above was adapted from USAFacts and is the intellectual property of USAFacts protected by copyrights and similar rights. USAFacts grants a license to use this Original Content under the Creative Commons Attribution-ShareAlike 4.0 (or higher) International Public License (the “CC BY-SA 4.0 License”).

Arguments Can be Made for Rates Being Too Low and for Rates Being Too High

The Federal Reserve has raised the Fed Funds rate from an average of 0.08% in January 2022 to its current 4.05%, and a likely adjustment to 4.25% to 4.50% tomorrow. Inflation, as measured by CPI and even the Fed’s favorite, the PCE deflator, has been showing a decreasing rise in prices. So investors within all affected markets are asking, how much more will the Fed raise rates? Ignoring any suggestion that “this time it’s different,” I looked at US interest rates and inflation going back to 1962 and may have found enough consistency and historical norms to help determine what to expect now and why.

Are Increases Nearing an End?

I’ll start with the conclusion. The data suggests that the movement of market rates depends on whether higher current inflation is being caused by temporary or long-lived factors. The 10-year Treasury Note market believes current inflation is mostly temporary. This is shown by its yield, having touched 4.25% in late October, and then falling. The ten-year is now near 3.50%, despite the 0.75% increase in overnight rates implemented on November 2. If the combined wisdom of the Treasury market is reliable, this suggests FOMC rate increases are nearing an end. Perhaps one more smaller hike and then a wait-and-see period. The Fed would then monitor prices while past increases work their way through the economy.

Powell’s Concerns

At his last address on November 30th, Fed Chair Jay Powell indicated he’d rather go too far (with tightening) and then reignite the economy rather than err on the side of not doing enough and having a bigger problem. The markets and the media largely ignored this, but it’s important to know what the Fed Chair believes is prescient and is sharing publicly. Powell also said, “Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level.” And then he said something very telling, Powell added, “It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.”

Market Thinks Inflation is Temporary

But, the markets are overjoyed by the last two months of inflation data. Despite what the nations top central banker is saying. Markets may be right, but if they are wrong (bond and stock markets) spotting it early can help stave off losses. If inflation, which is lower than it had been, but not historically low, proves more permanent, for example, if employers continue to have to bid up the price of workers, and demand for goods causes commodity prices to rise, then the Fed will have paused too early. This will lead to a more difficult challenge for the Fed as compared to tightening too much. The data used in this article are from the Federal Reserve Economic Data (FRED) maintained by the Federal Reserve Bank of St. Louis.

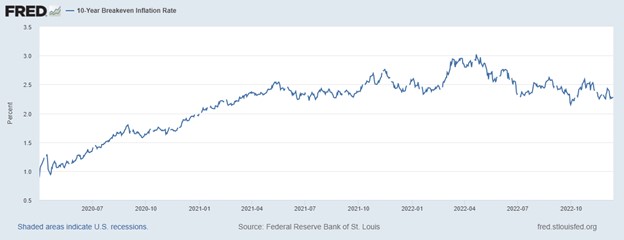

Actual and Expected Inflation

The St. Louis Federal Reserve publishes a market estimate of expected average inflation over the next ten years. It is derived from the 10-year Treasury constant maturity bond and 10-year Treasury inflation-indexed constant maturity bond. It was first published in 2003. Over 2003-2021, 10-year inflation expectation averaged 2.0%, the same as GDP deflator inflation. During the second quarter of 2022, the expected 10-year inflation was 2.7%, or less than 1.0 percentage point above its 2003-2021 average. In contrast, GDP deflator inflation was 7.6%. A significant wedge exists between current and expected inflation.

Source: St. Louis Fed

The breakeven inflation rate represents a measure of expected inflation derived from 10-Year Treasury Constant Maturity Securities (BC_10YEAR) and 10-Year Treasury Inflation-Indexed Constant Maturity Securities (TC_10YEAR). The latest value implies what market participants expect inflation to be in the next 10 years, on average.

Beginning with the end of the last recession on April 1, 2020, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

Take Away

The Market’s expectation of 10-year average inflation is dramatically different from current inflation, even at inflation’s new lower pace. This implies the market believes it to be temporary.

If the market’s expectation of inflation is accurate, there is an average difference between Fed Funds and the PCE deflator of 1.6% (since 1962). The last read on PCE was October 2022 at 6%. Reducing this by 1.6 would provide a Fed Funds level of 4.4%. This level is in line with historic averages and likely where we will be after the FOMC meeting wraps up on December 14. This comparatively high rate relative to where we began the year may be considered neutral.

Will the Fed stop at neutral? Are the markets right? Powell said he’d rather err on the side of going beyond what is needed, which suggests the Fed will continue some. As for the markets, being on the side of the markets is how you make money, but getting out before trouble arises is how you keep the money. Markets are not always accurate forecasters and since economic behavior and debt levels tend to adjust slowly, prudent portfolio management suggests it is wise to keep an eye out for today’s interest rates still being too low.

An Alternative View of Today’s Economy by Cathie Wood

Cathie Wood made the argument that investors comparing the current economic crosscurrents to the 1970s are developing forecasts based on the wrong data-set. Speaking at the Finimize Modern Investor Summit via video, the ARK Invest funds founder instead suggested the current economy and inputs are similar to a different period – she then made a case for her reasoning.

“If you go back to the 19-teens (1912-1922), then the period was very similar to the period we’re in today,” she said at the Investor Summit. That period featured a war, a pandemic (Spanish flu), and supply-chain problems. “It was the most prolific period for innovation in history,” she said, pointing to the disruptive impact of electricity, the telephone, and the car.

Wood explained that inflation went from 24% in June 1920 to -15% in June 2021. She made clear she isn’t forecasting deflation this severe; however, she is expecting year-over-year inflation to swing into negative territory, with prices going down. “What has happened during the last few years is going to flip, and we think that the market will flip back to a preference for growth stocks and our innovation strategy,” she said.

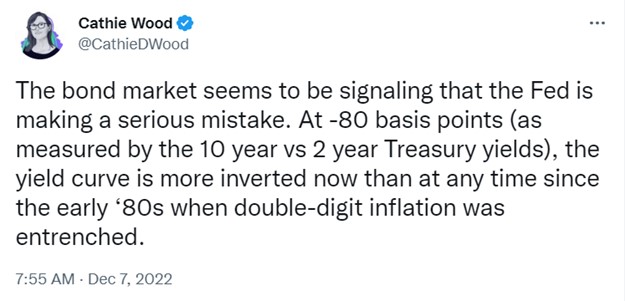

Wood also elaborated on a tweet she issued earlier about how deep the inversion was of the yield curve.

Twitter @CathieDWood

“That’s the bond market saying, ‘hello, Fed, are you watching?'” She said Federal Reserve Chair Jerome Powell is trying to be the reincarnation of Paul Volcker at a time when it’s not appropriate. “I think that’s a mistake because this is not a 15-year problem; it’s a 15-month one,” said Wood. She highlighted that commodity prices are tumbling, supply chains are improving, and companies are

Ark Invest funds have been positioned in a more concentrated waiting pattern while Wood waits for inflation dynamics to be supportive of innovation. She gave an example; the innovation fund, for instance, has been narrowed to 32 companies from 58, Wood said, as she highlighted that the firm has become less convinced China is supportive of innovation.

Take Away

It’s worth reviewing the differing opinions of several investors that have made above-average returns in their careers. While almost no one is always correct, there are many different right ways to make money in any market.

The Ark flagship fund is down 63% this year; in the past, Wood has indicated her funds’ time period to measure return is five years, not one. Perhaps investors with a longer holding period can garner useful ideas from her pounding the deflation drum, while investors with a shorter time horizon are concerned about inflation.

Why the Fed Needs to Gain Trust, Gain Momentum, and Gain More Yards

Monetary policy and its implementation is as much sport as science. Economics is actually a social science, so it relies on human behavior to mimic past behaviors as its prediction guide. But as in sports, victory is difficult if there is distrust in the coach that’s calling the shots (in this case Powell), or if there are people on your side that have reason to work against you, (an example would be Yellen). Consistency in blocking and tackling (doing the right thing) and not giving up, over time, wins games. Knowing what to expect from the opposing team (consumers) wins a healthy economy.

One repeated trait in monetary policy is that there is a lag between implementation (easing or tightening) and a change in economic conditions. It isn’t a short lag, and the impact varies. Since it could take more than a year for a policy change to begin to impact the economy, the Fed usually moves at a slow and measured pace in order to not overdo it.

The slow pace allows policymakers to observe the impact of their moves and change tactics (positions on the playing field) mid-game.

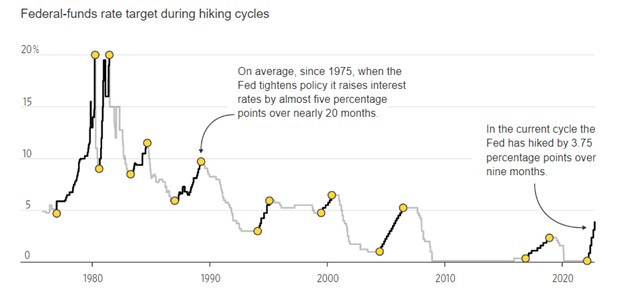

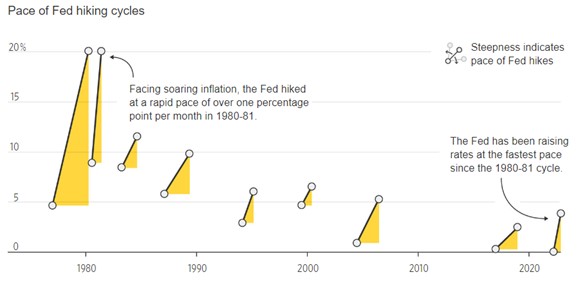

Federal-Funds Rate During Tightening Cycles

Note: From December 2008, midpoint of target range. December 2015 hike excluded from 2016-18 cycle

Source: Federal Reserve

Over the past nine months, we have been in a tightening cycle. During this period, the Fed has raised rates by 3.75%. On average (since 1975), when the Fed has tightened rates, they are notched up by 5.00% over 20 months.

The Fed’s current pace is faster than average. This is because inflation took them by surprise, and rose rapidly. Putting up a strong defense against inflation that has been rampant is necessary to not be shut out and allow the Fed to gain control over the outcome.

Because one has to be able to reflect back more than 40 years to have experienced the Fed raising rates this fast. Many have lost confidence in its ability, and are in their own way working against a winning outcome.

Pace of Fed Hiking Cycles

Note: From December 2008, the midpoint of target range

Source: Federal Reserve

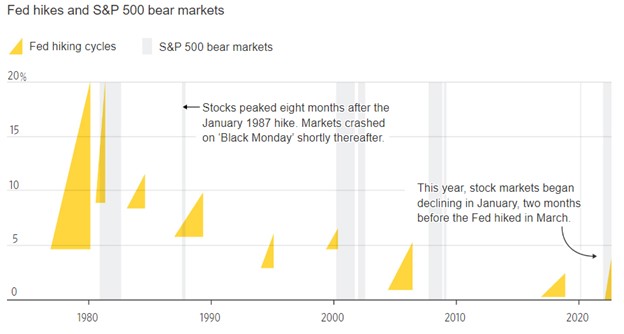

The stock and bond markets move in group anticipation of expected policy moves by the Fed. This has been more pronounced in recent years as the Fed has basically shared its expectations after each meeting, setting up for the next. Higher rates make bonds and bank deposits more attractive. Higher rates also weaken the economy and corporate profits, and that induces investors to move away from stocks and even real estate.

Bonds now offer the highest yields since 2007. The stock market may have anticipated what was to come as it peaked in early January of this year, more than two months before the Fed began hiking in March.

Fed Hikes and S&P 500 Bear Markets

Sources: Federal Reserve; Dow Jones Market Data

Sources: Federal Reserve; Dow Jones Market Data

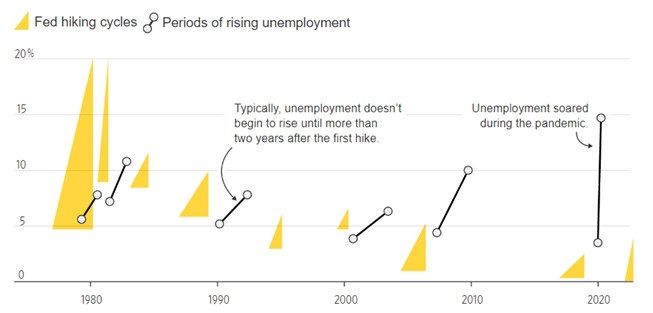

Employment

The Fed is concerned with a wage-price spiral feeding on itself. It likely won’t be satisfied that its tightening has been sufficient until it can be confident that it has avoided a wage-price storm on the economy.

Ideally, this would happen without unemployment rising. Soft landings took place in 1983-84 and 1994-95. But when inflation starts out too high, as it is now, unemployment usually rises notably, and a recession occurs.

Historically, this doesn’t happen until several years after the first increase. This time it is hoped it will be different, since the Fed is playing more aggressively.

Periods of Fed Hiking and Rising Unemployment

Note: The unemployment rate rose to 3.7% in October, up from the pandemic low of 3.5% a month earlier. Sources: Federal Reserve; Labor Department

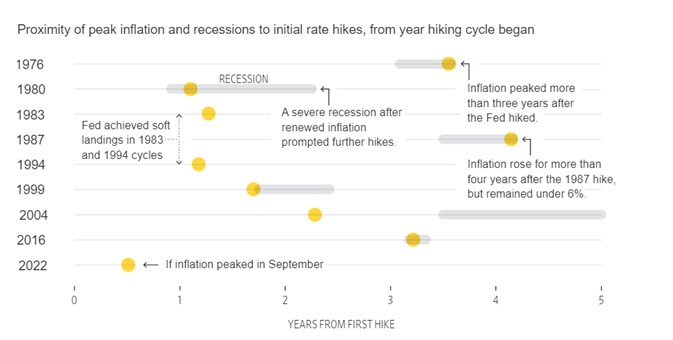

Inflation

Historically, inflation has only fallen to acceptable levels after unemployment has increased, and long after the first rate increase – the exact timing has varied. If the fall in core inflation (which excludes the volatile food and energy components) between September and October continues, and September proves to be the peak, the time between the first Fed increase and the high point of inflation will be one of the shortest of any Fed hiking cycle.

Often, the break in inflation has been accompanied by a recession. The economy receded in each of the first two quarters and then grew in the third. The changes in the inflation component in Gross Domestic Product may have borrowed from one quarter and have been additive to the next. The fourth quarter reading should help level the growth averages out to see if we were indeed in a shallow recession.

Proximity of Peak Inflation and Recessions to Initial Rate Hikes, from Year Hiking Cycle Began

Note: Inflation refers to core CPI.

Sources: Federal Reserve; Labor Department

Take Away

As in many team sports, once one side gets momentum, they are difficult to stop . The Fed needs to gain the trust of the individual players in the economy in order to be successful. Saying one thing, then doing another, would undermine this trust. So far, despite the Fed originally being wrong about inflation, the Fed has done what it has said it would do. Stock and bond markets, which are a considerable part of the economy, have been slow to understand the Fed’s resolve.

It has been implementing the balance sheet run-off plan and raising rates toward a level it believes would equate to a future 2% inflation rate. Like so many other things in the social sciences, widely held expectations of the future become self-fulfilling.

Philippe Petit walks Tightrope between buildings one and two of WTC, Manhattan, 1974 – Robert.Dearie (Flickr)

Analyst Team Point Out Asset Classes that Slingshotted in the 1970s

While the traditional fine print usually says, “past performance is no guarantee of future results,’ we all know trading decisions, whether the stocks are to be held for seconds, or decades, are based on probabilities. And market probabilities are rooted in past performance. What does past performance tell us about the chances that the markets can survive high inflation and low growth? Well, if the stagflation of the 70s repeats, there may be a small section of the markets to keep a solid footing.

Michael Hartnett is the chief investment strategist at Bank of America/Merrill Lynch. Hartnett sees in our current economy the ingredients in the macroeconomic picture that lead to the difficult economic combination of high inflation and low growth. His team, in their Flow Show note on Friday, wrote: “Inflation and stagnation was ‘unanticipated in 2022…hence $35 trillion collapse in asset valuations; but relative returns in 2022 have very much mirrored asset returns in 1973/74, and the 70s remain our asset allocation analog for 2020s.”

If the conditions of the 1970s are being mirrored and we are creating a foundation similar to 1973/74, Hartnett and team have a list of assets that could springboard off the stagflation cycle.

The assets with potential include taking long positions in small-caps, value, commodities, resources, volatility, and emerging markets. The group also highlights the short positions that worked well in the 1970s, the note indicates these are larger stocks, bonds, growth, and technology.

Why Small-Caps

As it applies to the smaller companies, the note points out that stagflation persisted through the late 1970s, but the inflation shock had ended by 1973/74, when the small-cap asset class “entered one of the great bull markets of all-time.” The Hartnett team sees small-caps set to keep outperforming in the “coming years of stagflation.”

The current year-to-date status has the Russell 2000 small-cap stock market index (measured by iShares ETF) down 19.8% in 2022. At the same time, the Dow Industrials are down 11%, S&P 500 lost 21%, and the Nasdaq Composite gave back 33%.

The current state of the Fed and Chairman Powell is they continue to be adamant about tightening, Powell said he’d prefer to overdo withdrawing stimulus than do too little. He also knows that until the market believes this, his tightening efforts will have a lower impact.

The BofA team isn’t helping market expectations as they noted, despite Powell’s clear signal that the Fed isn’t ready to declare even a slight victory from its raising rates; the analyst team says, don’t give up on that pivot.

After tightening interest rates through 1973/74 amid inflation and oil shocks, the central bank first cut in July 1975 as growth turned negative, Hartnett points out. A sustained pivot began in December of that year, and importantly, the unemployment rate surged from 5.6% and 6.6% that same month.

The “following 12 months, the S&P 500 rose 31%. The note suggests the lesson learned is that job losses when they occur, will be the catalyst for a 2023 pivot,” said Hartnett and the team.

We’re not there yet. Today’s economic release on jobs showed the U.S. added a stronger-than-expected 261,000 jobs during October. This is a slower pace than the prior month’s 315,000 job gains but still shows the Fed can comfortably notch rates up more and continue reducing its balance sheet.

Take Away

The team of analysts at BofA/Merrill Lynch, reporting to Michael Hartnett, drew conclusions from the stagflation and financial markets’ performance of the 1970s. They shared their thoughts in a research note with investors. Looking at past performance, their expectation is that the Fed will pivot away from aggressively raising rates when it begins to negatively impact job creation. At this point, many markets will have already reacted to inflation expectations and would then react to a more accommodative monetary policy.

The asset sectors to avoid or short are larger stocks, bonds, growth, and technology. The preferred sectors that, in past situations, have done well are small-caps, value, commodities, resources, volatility, and emerging markets.

Be sure to sign-up at no cost for small and microcap company research sent to you each day by Channelchek.

These Are the New Federal Tax Brackets and Standard Deductions For 2023

Now for the inflation good news. Thankfully, as it relates to federal income taxes, the IRS makes annual adjustments to certain tax provisions. Simply put, the higher the inflation, the more tax credit benefit, which includes tax credits and taxable wages adjusted downward. So, in addition to receiving much higher COLA increases on Social Security payments and earning an interest rate in excess of 9% on U.S. Savings Bonds, those making an income in 2023 are likely to see more take-home pay.

The IRS Numbers Are In

The IRS announced the 2023 inflation adjustments to the standard deduction and other tax provisions for the 2023 tax year. The adjustments affect 60 provisions in the tax code, and leave a few key provisions unchanged.

Highlights of Changes in Revenue Procedure 2021-38

The tax year 2023 adjustments described below generally apply to tax returns filed in 2024. A higher level of details about these annual adjustments can be found in IRS Revenue Procedure 2022-38PDF.

The standard deduction for married couples filing jointly for tax year 2023 rises to $27,700 up $1,800 from the prior year. For single taxpayers and married individuals filing separately, the standard deduction rises to $13,850 for 2023, up $900, and for heads of households, the standard deduction will be $20,800 for tax year 2023, up $1,400 from the amount for tax year 2022.

Marginal Rates: For tax year 2023, the top tax rate remains 37% for individual single taxpayers with incomes greater than $578,125 ($693,750 for married couples filing jointly).

The other rates are:

35% for incomes over $231,250 ($462,500 for married couples filing jointly);

32% for incomes over $182,100 ($364,200 for married couples filing jointly);

24% for incomes over $95,375 ($190,750 for married couples filing jointly);

22% for incomes over $44,725 ($89,450 for married couples filing jointly);

12% for incomes over $11,000 ($22,000 for married couples filing jointly).

The lowest rate is 10% for incomes of single individuals with incomes of $11,000 or less ($22,000 for married couples filing jointly).

The Alternative Minimum Tax exemption amount for tax year 2023 is $81,300 and begins to phase out at $578,150 ($126,500 for married couples filing jointly for whom the exemption begins to phase out at $1,156,300). The 2022 exemption amount was $75,900 and began to phase out at $539,900 ($118,100 for married couples filing jointly for whom the exemption began to phase out at $1,079,800).

The tax year 2023 maximum Earned Income Tax Credit amount is $7,430 for qualifying taxpayers who have three or more qualifying children, up from $6,935 for tax year 2022. The revenue procedure contains a table providing maximum EITC amount for other categories, income thresholds and phase-outs.

For 2023, the monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking increases to $300, up $20 from the limit for 2022.

For the taxable years beginning in 2023, the dollar limitation for employee salary reductions for contributions to health flexible spending arrangements increases to $3,050. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount is $610, an increase of $40 from taxable years beginning in 2022.

For tax year 2023, participants who have self-only coverage in a Medical Savings Account, the plan must have an annual deductible that is not less than $2,650, up $200 from tax year 2022; but not more than $3,950, an increase of $250 from tax year 2022. For self-only coverage, the maximum out-of-pocket expense amount is $5,300, up $350 from 2022. For tax year 2023, for family coverage, the annual deductible is not less than $5,300, up from $4,950 for 2022; however, the deductible cannot be more than $7,900, up $500 from the limit for tax year 2022. For family coverage, the out-of-pocket expense limit is $9,650 for tax year 2023, an increase of $600 from tax year 2022.

For tax year 2023, the foreign earned income exclusion is $120,000 up from $112,000 for tax year 2022.

Estates of decedents who die during 2023 have a basic exclusion amount of $12,920,000, up from a total of $12,060,000 for estates of decedents who died in 2022.

The annual exclusion for gifts increases to $17,000 for calendar year 2023, up from $16,000 for calendar year 2021.

The maximum credit allowed for adoptions for tax year 2023 is the amount of qualified adoption expenses up to $15,950, up from $14,890 for 2022.

Brand New for 2023

The Inflation Reduction Act extended some energy-related tax breaks and indexed for inflation the energy-efficient commercial buildings deduction beginning with the tax year 2023. For 2023, the applicable dollar value used to determine the maximum allowance of the deduction is $0.54 increased by $0.02 for each percentage point by which the total annual energy and power costs for the building are certified to be reduced by a percentage greater than 25 percent (but not above $1.07). The applicable dollar value used to determine the increased deduction amount for certain property is $2.68 increased (but not above $5.36) by $0.11 for each percentage point by which the total annual energy and power costs for the building are certified to be reduced by a percentage greater than 25 percent.

Items Unaffected by Inflation Indexing

By statute, these items that were indexed for inflation in the past are currently not adjusted.

The personal exemption for tax year 2023 remains at 0, as it was for 2022, this elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act.

For 2023, as in 2022, 2021, 2020, 2019 and 2018, there is no limitation on itemized deductions, as that limitation was eliminated by the Tax Cuts and Jobs Act.

The modified adjusted gross income amount used by joint filers to determine the reduction in the Lifetime Learning Credit provided in § 25A(d)(2) is not adjusted for inflation for taxable years beginning after December 31, 2020. The Lifetime Learning Credit is phased out for taxpayers with modified adjusted gross income in excess of $80,000 ($160,000 for joint returns).

What Else is Impacted

The maximum contribution amount for a 401(k) or similar workplace retirement plan is governed by yet another formula that uses September inflation data. It is estimated that the contribution limit will increase to $22,500 in 2023 from $20,500 this year and the catch-contribution amount for those age 50 or more will rise from $6,500 to at least $7,500.

The child tax credit under current law is $2,000 per child is not adjusted for inflation. But the additional child tax credit, which is refundable and available even to taxpayers that have no tax liability, is adjusted for inflation. It is expected to increase from $1,500 to $1,600 in 2023.

For those that look forward to capping out payments to Social Security, there is bad news. This has also increased. According to the 2022 Social Security Trustees Report, the wage base tax rate is projected to increase 5.5% from $147,000 to $155,100 in 2023.

Costs are rising, but so are deductions. It’s improbable that the reduced taxes will offset skyrocketing inflation, but at least there is one financial category that is helped by the increases.

Soaring Inflation Prompts Biggest Social Security Cost-Of-Living Boost Since 1981 – 6 Questions Answered

Social Security is set to boost the benefits it provides retirees by 8.7%, the biggest cost-of-living adjustment since 1981. It comes as sky-high inflation continues to eat into incomes and savings.

The changes are set to take effect in January 2023 and were announced following the release of the September 2022 consumer price index report, which showed inflation climbing more than expected during the month, by 0.4%.

The automatic adjustment will surely come as a relief to tens of millions of retirees and those who receive supplemental security income who may be struggling to afford basic necessities as inflation has accelerated throughout 2022. But an annual adjustment wasn’t always the case – and other government benefits and programs deal with inflation differently.

John Diamond, who directs the Center for Public Finance at Rice’s Baker Institute, explains the history of the Social Security cost-of-living, or COLA, increase, what other benefits are adjusted for inflation and why the government makes these changes.

1. How fast is the cost of living rising?

The latest data, for September, shows average consumer prices are up 8.2% from a year earlier. The monthly gain of 0.4% was double what economists surveyed by Reuters had expected.

More troubling, so-called core inflation – which excludes volatile food and energy prices – gained even more in September, ticking up by 0.6%. Core inflation is a measure that’s closely watched by the Federal Reserve, as it helps show how pervasive and persistent inflation has become in the economy.

2. How are Social Security benefits adjusted for inflation?

Automatic adjustments to Social Security benefits began in 1975 after President Richard Nixon signed the 1972 Social Security amendments into law.

Before 1975, Congress had to act each year to increase benefits to offset the effects of inflation. But this was an inefficient system, as politics would often be injected into a simple economic decision. Under this system, an increase in benefits could be too small or too large, or could fail to happen at all if one party blocked the change entirely.

Not to mention that with the baby boomers – those born from 1946 to 1964 – entering the labor force it was already clear that Social Security would face long-term funding issues in the future, and so putting the program on autopilot reduced the political risk faced by politicians.

Since then, benefits have climbed automatically by the average increase in consumer prices during the third quarter of a given year from the same period 12 months earlier. This is based on a version of the consumer price index meant to estimate price changes for working people and has been rising slightly faster than the overall pace of inflation.

While helpful, these inflation adjustments are backward-looking and imperfect. For example, 2022 Social Security benefits increased by 5.9% from the previous year, even though inflation throughout this year has been significantly higher – which means the higher benefits weren’t covering the higher cost of living. Thus, the 2023 increase in benefits primarily offsets what was lost over the previous year.

A white hand holds a card reading social security

Millions of retirees and other will soon see a big jump in their Social Security benefits. AP Photo/Jenny Kane

3. Are the benefits taxable?

A growing portion of Social Security benefits are taxed in the same way as ordinary income, except at different threshold with various caps and percentages. Only 8% of benefits were subject to taxation in 1984, but that’s climbed to almost 50% in recent years. That percentage will likely continue to increase as the taxable thresholds are not adjusted for inflation.

For example, if an individual filer’s income, including benefits, is below US$25,000, none of that is taxed. But up to 50% of a person’s benefits may be taxed at incomes of $25,000 to $34,000. After that, up to 85% of their benefits may be taxed.

Such a big increase in Social Security benefits likely means some people who paid no tax will now have to pay some, while others will see larger increases in their tax liability.

4. Why does the government adjust benefits for inflation?

Rapid gains of inflation, like the kind the U.S. and many other countries are currently experiencing, can have significant impacts on the finances of households and businesses.

For example, it might mean seniors cutting back on heating or food. Government policies generally try to account for this to reduce the negative impacts that rising prices can have on those with limited or fixed resources.

In addition, reducing the impacts of price changes creates a more efficient and fair allocation of resources and reduces the arbitrary outcomes that would otherwise occur.

5. What other government programs typically get a COLA?

Other government programs and benefits also increase to account for inflation.

The U.S. Department of Agriculture estimates the cost of its Thrifty Food Plan each June and adjusts Supplemental Nutrition Assistance Program or SNAP benefits – formerly known as food stamps – in October of each year. Beginning in October 2022, food stamp benefits rose by 12.5%, which helps make up for the largest increases in food prices since the 1970s.

In addition, the federal poverty level is adjusted for changes in the consumer price index annually by the Department of Health and Human Services, an adjustment that affects a number of government-provided benefits, such as housing benefits, health insurance and others, including SNAP benefits.

6. Does the tax system also adjust for inflation?

While some aspects of the tax code adjust for inflation, others do not.

For example, income tax bracket thresholds, the size of the standard deduction, alternative minimum tax parameters and estate tax provisions all increase annually for inflation. That means come tax filing season next year, U.S. tax filers will likely see big changes in all these items.

But examples of provisions that are not adjusted for inflation include the maximum value of the child tax credit and the $10,000 cap on the deduction of state and local taxes. In addition, the threshold that determines who is liable for the net investment income tax – the additional 3.8% tax on investment and passive income for taxpayers above a certain income level – doesn’t adjust, which means each year more individuals are subject to it.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of John W. Diamond, Director of the Center for Public Finance at the Baker Institute, Rice University.

The Connection Between Producer Price (PPI) and Consumer Price (CPI) Inflation

Does a higher PPI mean a higher CPI? A newly released report shows U.S. suppliers raised prices by 0.4% in September from August, when the Producer Price Index report had shown a 0.2% drop. The inflation measure that has impacted the stock market most severely this year is the Consumer Price Index. The two Bureau of Labor Statistics (BLS) releases are related but not directly correlated and are often used to measure different things by economists and those in industry.

The PPI rose 8.5% in September from a year before, down from its 8.7% annual increase in August and 11.3% in June. – BLS

How CPI and PPI are Different

The PPI for personal consumption includes all marketable production sold by U.S.-domiciled businesses for personal consumption. The majority of the products sold by domestic producers come from non-governmental sectors. However, government produces some marketable output that is under the PPI umbrella. In contrast to the PPI’s components, CPI includes goods and services provided by businesses or governments when direct costs to the consumer are levied.

The most heavily weighted item in CPI is rent. It’s weighted at 24% of the index. What the BLS calls owners’ equivalent rent is the implied rent occupants would have to pay if they were renting their homes. This is how the Bureau of Labor Statistics captures the cost of housing for owner-occupied and rented housing. This heavily weighted component is not in PPI – obviously, owners’ equivalent rent is not a domestically produced output.

The PPI for personal consumption and the CPI also differ in their treatment of imports. The CPI includes, within its basket, goods and services purchased by domestic consumers and therefore includes imports. The PPI, in contrast, does not include imports because imports are, by definition, not produced by domestic firms.

How PPI Impacts CPI

The PPI trends often work their way into consumer price movements, but not at a one-to-one basis or even a standard delayed interval. The demand component of consumer’s impact, what the consumers are willing to consume at certain price levels, is at play with what is charged for goods at the retail level. So even if the cost to manufacture goods has risen, passing the cost on is not always possible without hurting sales. At some level of price increases, demand decreases. This is different for each type of product. For instance, food, medical care, and housing may not be impacted as much as recreation, clothing, and other items which are easier to put off or do without.

Companies are trying to manage higher costs without alienating consumers who are weary of price increases. So far in the 2022 U.S. economy, consumer spending has remained strong despite the rate of CPI, but economists worry that we’re approaching a tipping point.

The Fed has raised the benchmark federal funds rate at its last three meetings by 0.75 percentage points, it now sits in the range of 3% and 3.25%. Officials have indicated they are prepared to raise rates over the course of their final two gatherings this year to around 4.25%.

Today, with consumer inflation running at a four-decade high and savings measurements trending lower, consumers are expected to begin to change buying habits. This overall is bad for business and the economy, which is why the Federal Reserve is expected to continue its fight against price increases, despite their lack of popularity with the financial markets.

“Monetary policy will be restrictive for some time to ensure that inflation moves back” Fed Vice Chair Lael Brainard (October 10).

Prices have begun to fall for some goods and services, including commodities, freight shipping, and housing. Those declines have led some Fed watchers to warn that the central bank risks tightening financial conditions too much.

Take Away

Increases in producer prices are passed to consumers when they can be. However, there is only so much a consumer is willing to pay for a purchase they can put off or substitute for something cheaper. This has ramifications for investors.

Companies where demand will wain when prices rise, may find earnings weaken; these could include producers of discretionary goods. Stocks that are shares of consumer staple companies may not feel the brunt of consumer pushback; those that produce more cost-effective brands, including white label providers, may outshine their brand name competitors if consumers increase their substituting for lower priced alternatives. Health care is one area where demand changes little as prices change at the producer or consumer level.