Research News and Market Data on GLDD

Feb 18, 2025

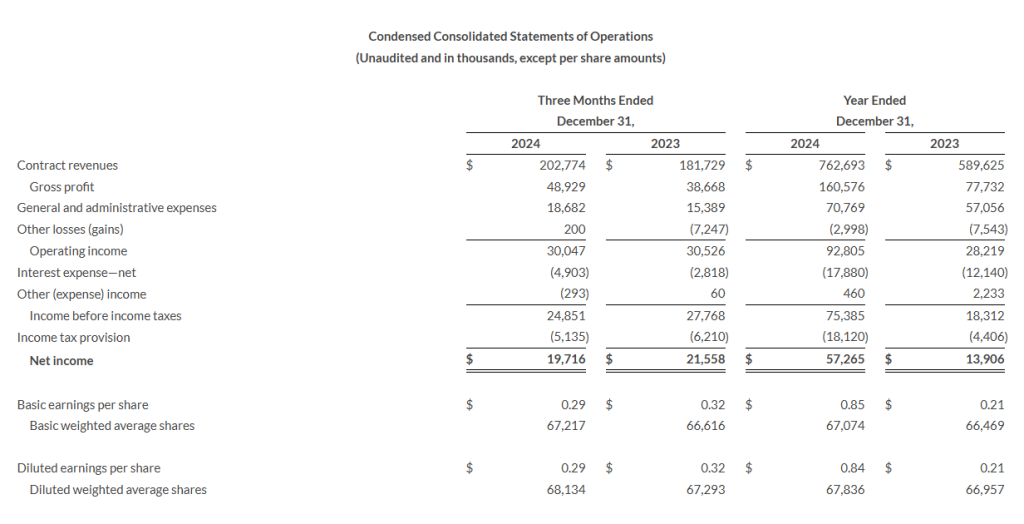

Fourth quarter net income of $19.7 million

Fourth quarter Adjusted EBITDA of $40.2 million

Full year net income of $57.3 million

Full year Adjusted EBITDA of $136.0 million

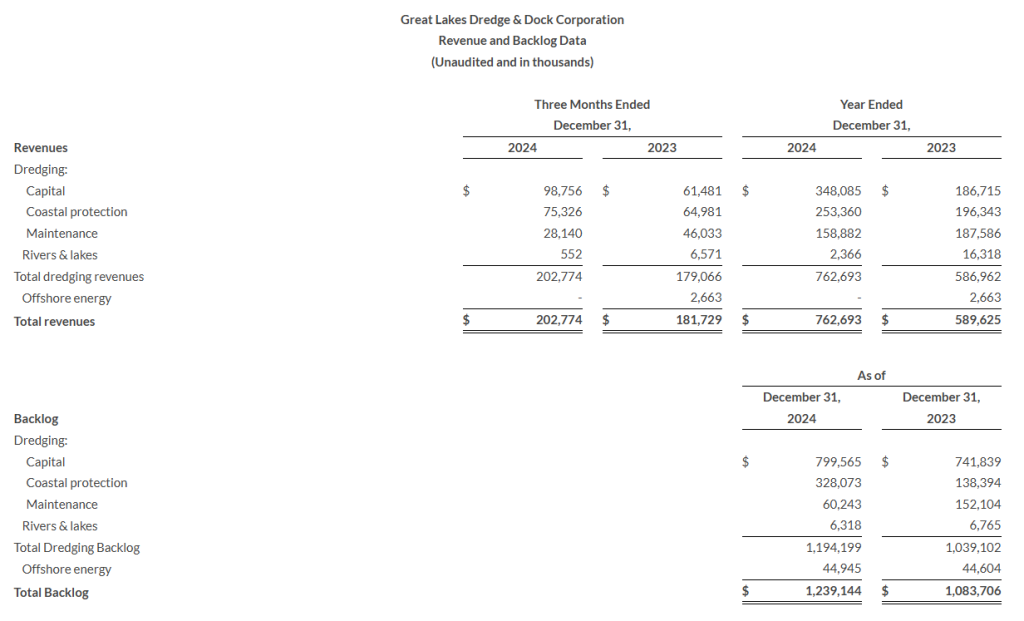

Dredging backlog of $1.2 billion at December 31, 2024

HOUSTON, Feb. 18, 2025 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) (Nasdaq: GLDD), the largest provider of dredging services in the United States, today reported financial results for the fourth quarter and year ended December 31, 2024.

Fourth Quarter 2024 Highlights

- Revenue was $202.8 million

- Total operating income was $30.0 million

- Net income was $19.7 million

- Adjusted EBITDA was $40.2 million

Full Year 2024 Highlights

- Revenue was $762.7 million

- Total operating income was $92.8 million

- Net income was $57.3 million

- Adjusted EBITDA was $136.0 million

Management Commentary

Lasse Petterson, President and Chief Executive Officer, commented, “Great Lakes had an outstanding 2024, with strong project performance and exceptional financial results. We capped off the year with another strong quarter and ended 2024 with revenue of $762.7 million, net income of $57.3 million, and Adjusted EBITDA of $136.0 million, the latter two metrics being the second-highest in Great Lakes’ history. The bid market for 2024 hit a historic level of $2.9 billion of which Great Lakes won 33%. This further added to our substantial dredging backlog which as of the end of 2024 stood at $1.2 billion, with an additional $282.1 million in low bids and options pending award, providing expected revenue visibility well into 2026. At the end of the year, capital and coastal protection projects accounted for 94% of our backlog, which typically yield higher margins. The largest capital project bid in the year was the Sabine-Neches Contract 6 Deepening project, won by Great Lakes, with awarded base and open options totaling $235 million.

Also included in our backlog are two Liquified Natural Gas (“LNG”) projects that were awarded in 2023, the Port Arthur LNG Phase 1 project and the Brownsville Ship Channel project for Next Decade Corporation’s Rio Grande LNG project, which is the largest project undertaken in Great Lakes’ history. Dredging began on both capital projects in the third quarter of 2024. We continue to tender bids on several pending LNG projects in an effort to diversify and expand our client base.

We remain steadfast in our commitment to executing a long-term strategy that maximizes growth opportunities for the Company. The Acadia, the first U.S.-flagged Jones Act compliant subsea rock installation (“SRI”) vessel, is currently under construction and has secured offshore wind rock placement contracts for Equinor’s Empire Wind 1 and Ørsted’s Sunrise Wind projects to protect foundations and cables. In addition, during the fourth quarter, we signed a vessel reservation agreement for the Acadia for another wind project in the United States. All three of these projects are fully permitted and we believe will not be directly impacted by the President’s Executive Order pausing issuance of new offshore wind leases and permits.

The Acadia is also well suited for work outside of U.S. offshore wind and over the past year we have been broadening our target markets for the Acadia to include international offshore wind projects, as well as protecting critical subsea infrastructure such as oil and gas pipelines and telecommunication and power cables. These additional markets pave the way for the rebranding of our offshore wind division to Offshore Energy.

In the second quarter, Great Lakes entered into a $150 million second-lien credit agreement which provides Great Lakes with additional liquidity which we expect will help us complete our new build program. In the third quarter, S&P Global Ratings upgraded Great Lakes’ credit rating to “B-” from “CCC+”, which further demonstrates the improvements we have made this past year to our balance sheet, cash flows and overall performance.

The Company had an exceptional 2024, and with our enhanced fleet, strong project performance, sustainable cost savings initiatives and strategic growth initiatives, we believe we are well prepared for the future.”

Operational Update

Fourth Quarter 2024

- Revenue was $202.8 million, an increase of $21.1 million from the fourth quarter of 2023. The higher revenue in the fourth quarter of 2024 was due primarily to higher capital and coastal protection project revenues, offset partially by a decrease in rivers and lakes and maintenance project revenue.

- Gross profit was $48.9 million, an improvement of $10.2 million compared to the gross profit from the fourth quarter of 2023. Gross margin percentage increased to 24.1% in the fourth quarter of 2024 from 21.3% in the fourth quarter of 2023 due to improved project performance and higher capital and coastal protection revenue in the current year quarter.

- Operating income was $30.0 million, which is slightly down compared to operating income of $30.5 million in the prior year fourth quarter. The year over year decrease is primarily due to a $7.4 million gain from a terminated offshore wind contract in the fourth quarter of 2023 and higher incentive pay in the current year quarter as a result of improved operational performance. These were mostly offset by the $10.2 million improvement in gross profit in the current year quarter.

- Net income for the quarter was $19.7 million, which is a $1.9 million decrease compared to net income of $21.6 million in the prior year fourth quarter. The decrease is mostly driven by an increase in net interest expense partially offset by a decrease in income tax provision.

Full Year 2024

- Revenue was $762.7 million, an increase of $173.1 million from 2023. The higher revenue in 2024 was due primarily to higher capital and coastal protection project revenues, offset partially by a decrease in rivers and lakes and maintenance project revenue.

- Gross profit for the full year 2024 was $160.6 million, an improvement of $82.9 million compared to the prior year’s gross profit. Gross margin percentage increased to 21.1% for the full year 2024 from 13.2% for the full year 2023 partially due to improved project performance and more capital and coastal protection revenue, which typically yield higher margins.

- Operating income for the full year 2024 was $92.8 million, which is a $64.6 million improvement from the prior year. The year-over-year increase is primarily a result of the $82.9 million increase in gross profit, which was partially offset by a $7.4 million gain from the terminated offshore wind contract in 2023 and by higher general and administrative expenses in the current year primarily due to higher incentive pay as a result of improved operational performance this year.

- Net income for the full year 2024 was $57.3 million, which is a $43.4 million improvement compared to $13.9 million for the full year 2023. This increase is primarily a result of the improved operating income, partially offset by an increase in net interest expense and income tax provision.

Balance Sheet, Dredging Backlog & Capital Expenditures

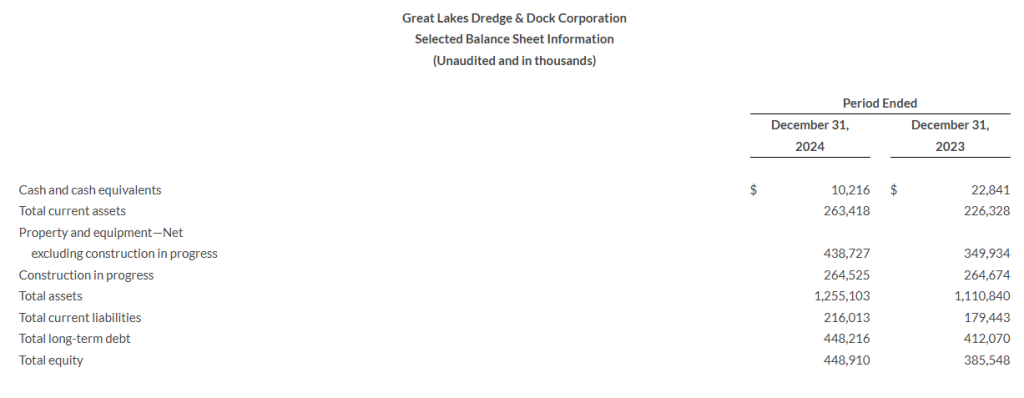

- At December 31, 2024, the Company had $10.2 million in cash and cash equivalents and total long-term debt of $448.2 million including $35 million outstanding against our $300 million revolver.

- At December 31, 2024, the Company had $1.2 billion in dredging backlog as compared to $1.04 billion at December 31, 2023. Dredging backlog does not include approximately $282.1 million of low bids and options pending award and approximately $44.9 million of performance obligations and $12.7 million in options pending award related to offshore energy.

- Total capital expenditures for 2024 were $135.7 million compared to $144.8 million for 2023. The 2024 capital expenditures included $72.7 million for the construction of the subsea rock installation vessel, the Acadia, $41.0 million for the Amelia Island, $5.4 million for the completion of the Galveston Island, and $16.6 million for maintenance and growth.

Market Update

We continue to see strong support from the Administration for the dredging industry. The 2024 Energy and Water Appropriations Bill provided a record $8.7 billion to the U.S. Army Corps of Engineers (the “Corps”). Additionally, the 2023 Disaster Relief Supplemental Appropriations Act allocated $1.5 billion for infrastructure repairs and beach renourishment projects. The year ended with a record bid market of $2.9 billion, which included a robust beach renourishment market and 13 capital projects.

The 2025 Corps’ budget is expected to be another record appropriation. On June 28, 2024, the U.S. House of Representatives Energy and Water Appropriations Subcommittee passed their 2025 Appropriations Bill providing the Corps with a budget of $9.96 billion, which is $2.7 billion above the President’s Budget request. The bill includes $5.7 billion for Operations and Maintenance projects, of which $3.1 billion is from the Harbor Maintenance Trust Fund. On August 1, 2024, the Senate Appropriations Committee approved its draft of the 2025 Energy and Water spending bill which provides $10.3 billion in total funding for the Corps. On December 20, 2024, U.S. Congress approved a continuing resolution through March 14, 2025, for the Corps’ Fiscal 2025 budget.

The Water Resources Development Act (“WRDA”) is renewed every two years and authorizes funding for Corps’ projects related to flood protection, dredging, and ecosystem restoration. WRDA 2022 included funding for deepening New York and New Jersey shipping channels to 55 feet and the Coastal Texas Protection and Restoration Program, which aims to protect the Texas Gulf Coast from hurricanes. On January 4, 2025, President Biden signed WRDA 2024 into law which includes several capital projects and projects designed to enhance flood protection, improve coastal resilience, and support ecosystem restoration.

We continue to be confident about our growth and diversification plans via our subsea rock installation initiative. As stated previously, we are broadening our targeted SRI markets to include oil and gas pipeline and telecommunications cable protection, and international offshore wind.

We continue to pursue SRI vessel projects with work planned for 2026 and beyond. Included in the subsea rock installation opportunities are global offshore wind projects. The latest BloombergNEF offshore wind market outlook shows global offshore wind expected to grow tenfold by 2040 with a forecast exceeding 700GW. In addition, market expectations for telecommunication and oil and gas scour protection projects globally are estimated on average to require approximately 2,000 SRI vessel days annually. We believe there is an undersupply of rock placement vessels and we are pursuing opportunities in all the above mentioned markets which are expected to provide the Acadia with work planned for 2026 and beyond.

Conference Call Information

The Company will conduct a quarterly conference call, which will be held on Tuesday, February 18, 2025, at 9:00 a.m. C.S.T (10:00 a.m. E.S.T.). Investors and analysts are encouraged to pre-register for the conference call by using the link below. Participants who pre-register will be given a unique PIN to gain immediate access to the call. Pre-registration may be completed at any time up to the call start time.

To pre-register, go to https://register.vevent.com/register/BI3ee71908023c466fb83abf345f36e0ca

The live call and replay can also be heard at https://edge.media-server.com/mmc/p/oqt4ireo or on the Company’s website, www.gldd.com, under Events on the Investor Relations page. A copy of the press release will be available on the Company’s website.

Use of Non-GAAP measures

Adjusted EBITDA, as provided herein, represents net income from continuing operations, adjusted for net interest expense, income taxes, depreciation and amortization expense, debt extinguishment, accelerated maintenance expense for new international deployments, goodwill or asset impairments and gains on bargain purchase acquisitions. Adjusted EBITDA is not a measure derived in accordance with GAAP. The Company presents Adjusted EBITDA as an additional measure by which to evaluate the Company’s operating trends. The Company believes that Adjusted EBITDA is a measure frequently used to evaluate performance of companies with substantial leverage and that the Company’s primary stakeholders (i.e., its stockholders, bondholders and banks) use Adjusted EBITDA to evaluate the Company’s period to period performance. Additionally, management believes that Adjusted EBITDA provides a transparent measure of the Company’s recurring operating performance and allows management and investors to readily view operating trends, perform analytical comparisons and identify strategies to improve operating performance. For this reason, the Company uses a measure based upon Adjusted EBITDA to assess performance for purposes of determining compensation under the Company’s incentive plan. Adjusted EBITDA should not be considered an alternative to, or more meaningful than, amounts determined in accordance with GAAP including: (a) operating income as an indicator of operating performance or (b) cash flows from operations as a measure of liquidity. As such, the Company’s use of Adjusted EBITDA, instead of a GAAP measure, has limitations as an analytical tool, including the inability to determine profitability or liquidity due to the exclusion of accelerated maintenance expense for new international deployments, goodwill or asset impairments, gains on bargain purchase acquisitions, net interest and income tax expense and the associated significant cash requirements and the exclusion of depreciation and amortization, which represent significant and unavoidable operating costs given the level of indebtedness and capital expenditures needed to maintain the Company’s business. For these reasons, the Company uses operating income to measure the Company’s operating performance and uses Adjusted EBITDA only as a supplement. Adjusted EBITDA is reconciled to net income in the table of financial results. For further explanation, please refer to the Company’s SEC filings.

The Company

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States, which is complemented with a long history of performing significant international projects. In addition, Great Lakes is fully engaged in expanding its core business into the offshore energy industry. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 135-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Cautionary Note Regarding Forward-Looking Statements

Certain statements in this press release may constitute “forward-looking” statements, as defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (the “SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Great Lakes and its subsidiaries, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Statements that are not historical fact are forward-looking statements. Forward-looking statements can be identified by, among other things, the use of forward-looking language, such as the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “may,” “would,” “could,” “should,” “seeks,” “are optimistic,” “commitment to” or “scheduled to,” or other similar words, or the negative of these terms or other variations are being made pursuant to the Exchange Act and the PSLRA with the intention of obtaining of these terms or comparable language, or by discussion of strategy or intentions. These cautionary statements have the benefit of the “safe harbor” provisions of such laws. Great Lakes cautions investors that any forward-looking statements made by Great Lakes are not guarantees or indicative of future performance. Important assumptions and other important factors that could cause actual results to differ materially from those forward-looking statements with respect to Great Lakes include, but are not limited to: a reduction in government funding for dredging and other contracts, or government cancellation of such contracts, or the inability of the Corps to let bids to market; our ability to qualify as an eligible bidder under government contract criteria and to compete successfully against other qualified bidders in order to obtain government dredging and other contracts; our business and operating results could be adversely affected by the political environment and governmental fiscal and monetary policies; cost over-runs, operating cost inflation and potential claims for liquidated damages, particularly with respect to our fixed cost contracts; the timing of our performance on contracts and new contracts being awarded to us; significant liabilities that could be imposed were we to fail to comply with government contracting regulations; project delays related to the increasingly negative impacts of climate change or other unusual, non-historical weather patterns; costs necessary to operate and maintain our existing vessels and the construction of new vessels; equipment or mechanical failures; pandemic, epidemic or outbreak of an infectious disease; disruptions to our supply chain for procurement of new vessel build materials or maintenance on our existing vessels; capital and operational costs due to environmental regulations; market and regulatory responses to climate change, including proposed regulations concerning emissions reporting and future emissions reduction goals; contract penalties for any projects that are completed late; force majeure events, including natural disasters, war and terrorists’ actions; changes in the amount of our estimated backlog; significant negative changes attributable to large, single customer contracts; our ability to obtain financing for the construction of new vessels, including our new offshore energy vessel; our ability to secure contracts to utilize our new offshore energy vessel; unforeseen delays and cost overruns related to the construction of our new vessels; any failure to comply with the Jones Act provisions on coastwise trade, or if those provisions were modified or repealed; our ability to comply with anti-discrimination laws, including those pertaining to diversity, equity and inclusion programs; fluctuations in fuel prices, particularly given our dependence on petroleum-based products; impacts of nationwide inflation on procurement of new build and vessel maintenance materials; our ability to obtain bonding or letters of credit and risks associated with draws by the surety on outstanding bonds or calls by the beneficiary on outstanding letters of credit; acquisition integration and consolidation, including transaction expenses, unexpected liabilities and operational challenges and risks; divestitures and discontinued operations, including retained liabilities from businesses that we sell or discontinue; potential penalties and reputational damage as a result of legal and regulatory proceedings; any liabilities imposed on us for the obligations of joint ventures, partners and subcontractors; increased costs of certain material used in our operations due to newly imposed tariffs; unionized labor force work stoppages; any liabilities for job-related claims under federal law, which does not provide for the liability limitations typically present under state law; operational hazards, including any liabilities or losses relating to personal or property damage resulting from our operations; our substantial amount of indebtedness, which makes us more vulnerable to adverse economic and competitive conditions; restrictions on the operation of our business imposed by financing terms and covenants; impacts of adverse capital and credit market conditions on our ability to meet liquidity needs and access capital; limitations on our hedging strategy imposed by statutory and regulatory requirements for derivative transactions; foreign exchange risks, in particular, as it relates to the new offshore energy vessel build; losses attributable to our investments in privately financed projects; restrictions on foreign ownership of our common stock; restrictions imposed by Delaware law and our charter on takeover transactions that stockholders may consider to be favorable; restrictions on our ability to declare dividends imposed by our financing agreements or Delaware law; significant fluctuations in the market price of our common stock, which may make it difficult for holders to resell our common stock when they want or at prices that they find attractive; changes in previously recorded net revenue and profit as a result of the significant estimates made in connection with our methods of accounting for recognized revenue; maintaining an adequate level of insurance coverage; our ability to find, attract and retain key personnel and skilled labor; disruptions, failures, data corruptions, cyber-based attacks or security breaches of the information technology systems on which we rely to conduct our business; and impairments of our goodwill or other intangible assets. For additional information on these and other risks and uncertainties, please see Item 1A. “Risk Factors” of Great Lakes’ Annual Report on our most recent Form 10-K, Item 1A. “Risk Factors” of Great Lakes’ Quarterly Report on Form 10-Q, and in other securities filings by Great Lakes with the SEC.

Although Great Lakes believes that its plans, intentions and expectations reflected in or suggested by such forward looking statements are reasonable, actual results could differ materially from a projection or assumption in any forward-looking statements. Great Lakes’ future financial condition and results of operations, as well as any forward-looking statements, are subject to change and inherent risks and uncertainties. The forward-looking statements contained in this press release are made only as of the date hereof and Great Lakes does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

For further information contact:

Tina Baginskis

Director, Investor Relations

630-574-3024