Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating estimates. We increased our 2024 adjusted funds flow (AFF) and earnings per share (EPS) estimates to C$44.3 million and C$0.34 from C$40.9 million and C$0.30. Our revisions are driven by higher crude oil price assumptions and a redistribution of quarterly production estimates. While we have assumed higher oil prices in the second and third quarters, our model assumes prices weaken in the fourth quarter. We increased our 2025 AFF and EPS estimates to C$41.1 million and C$0.30, respectively, from C$31.4 million and C$0.21 based on higher production volume and crude oil price assumptions. We think our 2025 estimates could be conservative if the company can increase annual production within its targeted range of 10% to 20%.

Normal course issuer bid (NCIB). Hemisphere renewed its NCIB to purchase up to 8,255,766 common shares, representing ~10% of the current public float, for cancellation. The NCIB commenced on July 14 and will terminate on July 13, 2025. Under its previous NCIB, which authorized the repurchase of 8,670,636 shares and terminated July on 13, the company purchased 4,074,400 shares on the open market at a weighted average price of C$1.425. Shares are generally purchased opportunistically during periods of weakness.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – July 11, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that the TSX Venture Exchange (the “TSXV”) has accepted the Company’s Notice of Intention to renew of its Normal Course Issuer Bid (the “NCIB”) to purchase for cancellation, from time to time, as Hemisphere considers advisable, up to 8,255,766 common shares (“Common Shares”) of the Company, representing approximately 10% of the current public float of the Common Shares.

Purchases of Common Shares will be made on the open market through the facilities of the TSXV. For any Common Shares purchased, Hemisphere will pay the prevailing market price of the Common Shares. The actual number of Common Shares that may be purchased for cancellation and the timing of any such purchases will be determined by the Company and dependent on market conditions.

The Company is commencing the NCIB because it believes that, from time to time, the market price of its Common Shares may not properly reflect the underlying, intrinsic value of the Company, and that, at such times, the purchase of Common Shares for cancellation will increase the proportionate interest of, and be advantageous to, all remaining shareholders.

The NCIB will commence on July 14, 2024 and will terminate on July 13, 2025 or at such earlier time as the NCIB is completed or terminated at the option of Hemisphere. The Company has retained Canaccord Genuity Corp. as its broker to conduct the NCIB on its behalf.

Under the Company’s previous notice of intention to conduct a normal course issuer bid, the Company sought and received approval of the TSXV to purchase 8,670,636 Common Shares for the period from July 14, 2023 to July 13, 2024. During that period, the Company purchased 4,074,400 Common Shares on the open market at a weighted-average price of $1.425 per Common Share.

About Hemisphere Energy Corporation

Hemisphere is a dividend paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Note Regarding Forward-Looking Statements and Other Advisories

This document contains forward-looking information. This information relates to future events and the Company’s future performance. All information and statements contained herein that are not clearly historical in nature constitute forward-looking information, and the words “may”, “will”, “should”, “could”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “propose”, “predict”, “potential”, “continue”, “aim”, or the negative of these terms or other comparable terminology are generally intended to identify forward-looking information. Such information represents the Company’s internal projections, estimates, expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. This information involves known or unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking information. Hemisphere believes that the expectations reflected in this forward-looking information are reasonable; however, undue reliance should not be placed on this forward-looking information, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. This press release contains forward-looking information concerning, among other things, the anticipated advantages of the NCIB to Hemisphere’s shareholders and the Company’s business strategy, the price to be paid by Hemisphere for purchases of Common Shares under the NCIB and Hemisphere’s plans for maximizing value per share growth with the sustainable development of its high netback high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. The reader is cautioned that such information, although considered reasonable by the Company, may prove to be incorrect. A number of risks and other factors could cause actual results to differ materially from those expressed in the forward-looking information contained in this document including, but not limited to, the risk that the anticipated benefits of the NCIB may not be achieved and the risk that the Company may not be able to successfully execute its business strategy or growth plans. Readers are cautioned that the foregoing list of factors is not exhaustive. Although the forward-looking statements contained in this document are based upon assumptions which management of Hemisphere believes to be reasonable, Hemisphere cannot assure investors that actual results will be consistent with these forward-looking statements. With respect to forward-looking statements contained in this document, Hemisphere has made assumptions regarding, among other things, the ability of Hemisphere to fund purchases of Common Shares under the NCIB and its business strategy. These forward-looking statements are made as of the date of this document and Hemisphere disclaims any intent or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or results or otherwise, other than as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Special dividend. Excluding special dividends, Hemisphere Energy pays a base dividend of C$0.025 per share per quarter, or C$0.10 per share on an annual basis. Hemisphere Energy recently declared a special dividend of C$0.03 per common share. The special dividend will be paid on July 26 to shareholders of record on July 12. In May, the company’s board of directors approved a quarterly cash dividend of C$0.025 per share that will be paid on June 28 to shareholders of record on June 20.

Return of capital to shareholders. To date in 2024, Hemisphere has committed to returning C$10.7 million to shareholders, including shares repurchased and canceled under the company’s normal course bid, quarterly dividend payments in February and June, and the special dividend payment in July. Returns of capital are funded entirely with free cash flow supported by ultra-low decline rates, low operating expenses, low capital-intensive assets, long life reserves and minimal decommissioning liabilities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – June 4, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that its board of directors has approved the declaration of a special dividend to shareholders.

Given the strong financial position and performance outlook of the Company, Hemisphere is pleased to announce that its board of directors has approved the declaration of a special dividend of C$0.03 per common share. The special dividend is part of Hemisphere’s comprehensive shareholder return model, and will be paid on July 26, 2024 to shareholders of record on July 12, 2024. This special dividend is designated as an eligible dividend for Canadian income tax purposes. It is in addition to the Company’s quarterly base dividend of C$0.025 per common share announced on May 29, 2024, and is in accordance with the Company’s dividend policy.

Hemisphere has committed to shareholder returns of $10.7 million thus far in 2024, including shares repurchased and cancelled under the Company’s normal course issuer bid, two quarterly dividend payments in February and June, and the special dividend payment in July. This return of capital is funded entirely by the Company’s free cash flow and is made possible by its high-margin enhanced oil recovery (“EOR”) assets, ultra-low production decline, and healthy balance sheet.

Subsequent to Hemisphere’s last news release, the Company has now brought online all three producers in its new Marsden, Saskatchewan development play. The purpose of primary production at these wells prior to polymer flood start-up is to gather fluid samples, pressure data, and other relevant reservoir data that will assist in EOR project planning. Construction of Hemisphere’s multi-well battery is currently underway, with anticipated polymer skid delivery and EOR project start-up in the third quarter.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood EOR methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a quarterly dividend will be paid in June 2024; that a special dividend will be paid to shareholders on July 26, 2024 to shareholders of record on July 12, 2024; and the timing of Hemisphere’s anticipated polymer skid delivery and EOR project start-up in the third quarter.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the timing for payment of the special dividend; no delays in the anticipated timing for delivery of the polymer skid and EOR project; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in project timelines and workstreams; changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Hemisphere Energy reported production results, pricing, and costs in line with expectations. The company remains on track to meet or beat management guidance. With production and oil prices rising, we expect cash flow and earnings to improve in upcoming quarters.

The company is actively drilling, including in a new area. Hemisphere drilled five wells during the quarter which should lead to production growth. Current production has already reached peak levels. The recently acquired property Marsden play represents a step out of current production and could be an important area for future growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – May 30, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) announces the results of its Annual General and Special Meeting of Shareholders that was held today.

Annual General and Special Meeting of Shareholders (“AGSM”)

A total of 46,475,140 common shares were voted, representing 47.45% of total shares issued and outstanding as at the April 11, 2024 record date of the AGSM.

Shareholders voted in favour of all items put forward by the Company’s Board of Directors and management, including:

Fixed the number of directors of the Company at six (6);

Elected the following directors of the Company for the ensuing year: Charles O’Sullivan, Don Simmons, Frank Borowicz, Bruce McIntyre, Gregg Vernon, and Richard Wyman;

Appointed KPMG LLP as auditors of the Company for the ensuing year at a remuneration to be fixed by the Board of Directors; and

Passed an ordinary resolution approving the renewal of the Company’s Stock Option Plan.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Vancouver, British Columbia–(Newsfile Corp. – May 29, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the first quarter ended March 31, 2024, declares a quarterly dividend payment to shareholders, renews credit facility, and provides operations update.

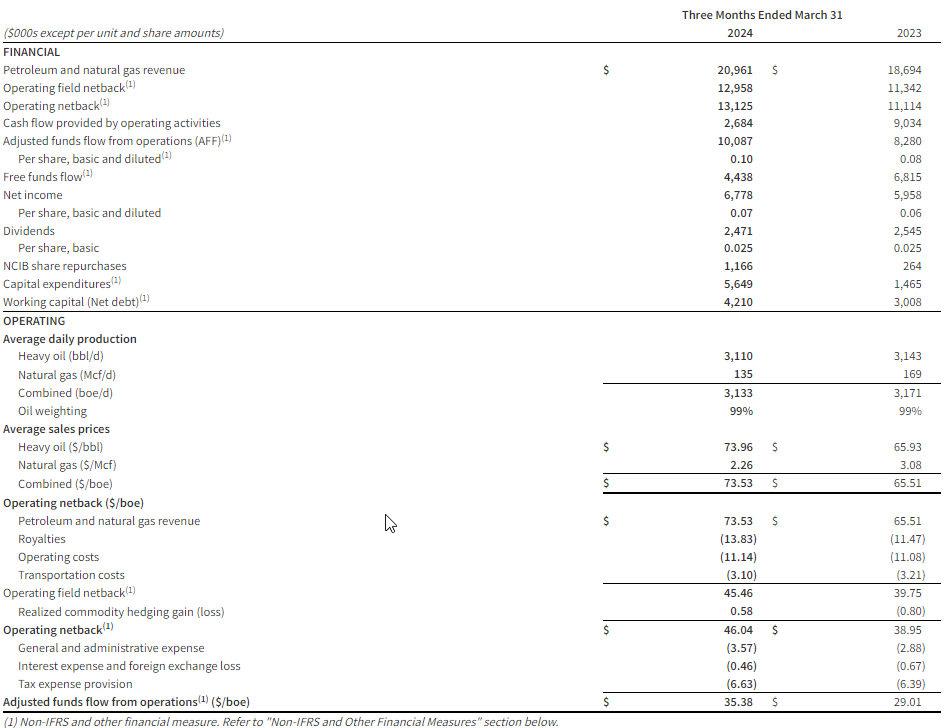

Q1 2024 Highlights

Produced a quarterly average of 3,133 boe/d (99% heavy oil), including significant downtime in January and early February due to extreme cold weather.

Attained quarterly revenue of $21.0 million.

Maintained low operating and transportation costs of $14.24/boe despite reduced quarterly production.

Delivered an operating netback1 of $13.1 million, or $46.04/boe.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $10.1 million, or $35.38/boe.

Achieved free funds flow1 of $4.4 million, or $0.04 per share.

Executed a $5.6 million capital expenditure1 program, including drilling five horizontal wells (three producers, two injectors) in the Company’s new Marsden, Saskatchewan oil play.

Received Enhanced Oil Recovery (“EOR”) project approval from the Ministry of Energy and Resources for a pilot polymer flood in Marsden.

Distributed $2.5 million, or $0.025 per share, in dividends to shareholders during the quarter.

Purchased and cancelled 869,100 shares for $1.2 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Exited the first quarter with positive working capital1 of $4.2 million, compared to $3.0 million at the end of March 2023.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditure, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited consolidated interim financial statements and related notes, and the Management’s Discussion and Analysis for the three months ended March 31, 2024 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Financial and Operating Summary

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on June 28, 2024 to shareholders of record as of the close of business on June 20, 2024. The dividend is designated as an eligible dividend for income tax purposes.

Credit Facility

The Company has completed its annual bank review and renewed its $35.0 million two-year extendible credit facility, with the next annual review date set for May 31, 2025.

Operations Update

Hemisphere’s Atlee Buffalo polymer injection projects both continue to perform well, contributing to slight overall corporate production growth. Current production is approximately 3,500 boe/d (99% heavy oil, field estimates between April 1 – May 25, 2024), 3% higher than the fourth quarter of 2023 despite no new wells having been brought online since last September.

In the first quarter of 2024, the Company received EOR project approval from the Ministry of Energy and Resources for a polymer flood pilot in its recently acquired Marsden acreage in Saskatchewan. Subsequently, Hemisphere executed a $5.6 million capital expenditure program, which included drilling five Marsden wells (three producers and two injectors). The Company has recently brought one well on primary production to a single well battery in order to gather initial test data required for EOR project planning. Hemisphere expects to commission a new polymer injection skid and oil treating battery for its Marsden project during the third quarter.

Preparation is also underway for the remainder of Hemisphere’s 2024 capital expenditure program, which includes up to nine new wells in the Atlee Buffalo area being drilled and brought on production to existing facilities later this summer.

Annual General and Special Meeting of Shareholders

Hemisphere’s Annual General and Special Meeting of Shareholders will be held at 10:00 am (Pacific Daylight Time) on May 30, 2024 in the Walker Room of the Terminal City Club located at 837 West Hastings Street, Vancouver, British Columbia.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that the Company expects to commission a new polymer injection skid and oil treating battery for its Saskatchewan production during the third quarter; the timing and execution of Hemisphere’s 2024 capital expenditure program, which includes up to nine new wells in the Atlee Buffalo area being drilled and brought on production to existing facilities later this summer; and that a dividend will be paid June 28, 2024 to shareholders of record as of the close of business on June 20, 2024.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the length of time that oil and gas operations will be impaired by the outbreak of Covid-19; the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, free funds flow, capital expenditures, operating field netback, operating netback, and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered more meaningful than IFRS measures in evaluating the Company’s performance.

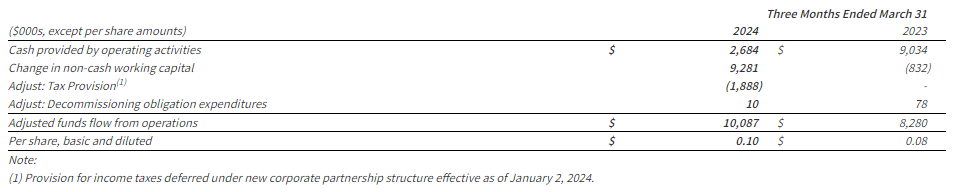

a)Adjusted funds flow from operations (“AFF”) (Non-IFRS Financial Measure and Ratio if calculated on a per share or boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

A reconciliation of AFF to cash provided by operating activities is presented as follows:

b)Free funds flow (“FFF”) (Non-IFRS Financial Measure): Calculated by taking adjusted funds flow and subtracting capital expenditures, excluding acquisitions and dispositions. Management believes that free funds flow provides a useful measure to determine Hemisphere’s ability to improve returns and to manage the long-term value of the business.

c)Capital Expenditures (Non-IFRS Financial Measure): Management uses the term “capital expenditures” as a measure of capital investment in exploration and production assets, and such spending is compared to the Company’s annual budgeted capital expenditures. The most directly comparable IFRS measure for capital expenditures is cash flow used in investing activities. A summary of the reconciliation of cash flow used in investing activities to capital expenditures is set forth below:

d)Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): A benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses, and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e)Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): calculated as the operating field netback plus the Company’s realized gain (loss) on derivative financial instruments on an absolute and per barrel of oil equivalent basis.

f)Working Capital/Net debt (Non-IFRS Financial Measure): Closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working capital/Net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding derivative financial instruments, decommissioning obligations, lease liabilities, and tax provisions, and including any bank debt. There is no IFRS measure that is reasonably comparable to working capital/net debt.

The following table outlines the Company calculation of working capital/net debt:

g)Supplementary Financial Measures and Non-IFRS Ratios

“Adjusted Funds Flow from operations per basic share” is comprised of funds from operations divided by basic weighted average common shares. “Adjusted Funds Flow from operations per diluted share” is comprised of funds from operations divided by diluted weighted average common shares. “Annual Free Funds Flow” is comprised of free funds flow from the current three-month period multiplied by four. “Operating expense per boe” is comprised of operating expense, as determined in accordance with IFRS, divided by the Company’s total production. “Realized heavy oil price” is comprised of heavy crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. “Realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. “Realized combined price” is comprised of total commodity sales from production, as determined in accordance with IFRS, divided by the Company’s total production. “Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the Company’s total production. “Transportation costs per boe” is comprised of transportation expense, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2023 and the interim period ended March 31, 2024, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

Any references in this news release to initial production rates (including as a result of recent water or polymer flood activities) are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

Barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

IFRS

International Financial Reporting Standards

boe/d

barrel of oil equivalent per day

$/boe

dollar per barrel of oil equivalent

US$

United States Dollar

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results were in line with expectations absent charge. Income, cash flow and earnings for the 2023-4Q and 2023 year would have been in line with expectations absent a $4.2 million nonrecurring charge to write down non-core assets.

Quarter production rose 16% year over year due to an active fall drilling program. The increase was expected. Extreme weather hurt production in the first few months of 2024 (2024-1Q production was announced below that in our models) but has risen to all-time high levels recently. We have lowered our 2024-1Q production estimate but raised our estimate for the remaining quarter’s of 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – April 18, 2024) – Hemisphere Energy Corporation (TSXV: HME)(OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the fourth quarter and year ended December 31, 2023.

2023 Highlights

Increased fourth quarter production by 16% to a record of 3,386 boe/d (99% heavy oil), and annual production by 11% to 3,125 boe/d (99% heavy oil), as compared to 2022.

Achieved annual revenue of $84.5 million, with adjusted funds flow from operations (“AFF”)(1) of $39.4 million.

Invested $16.9 million to drill eight successful Atlee Buffalo wells, one unsuccessful exploration well, upgrade facilities, purchase land and seismic, and pre-purchase materials for the 2024 development program.

Generated $22.5 million of free funds flow (“FFF”)(1).

Distributed $10.1 million in quarterly dividends to shareholders.

Distributed $3.0 million in special dividends to shareholders.

Purchased and cancelled 3.2 million shares at an average price of $1.28 per share under the Company’s normal course issuer bid (“NCIB”), returning $4.1 million to shareholders.

Exited the year with a positive working capital(1) position of $3.6 million compared to a net debt(1) position of $0.8 million at December 31, 2022.

Increased Proved Developed Producing (PDP) NPV10 BT reserve value by 9% to $248 million and maintained reserve volumes at 8.2 MMboe (99.6% heavy oil).

Increased Proved (1P) NPV10 BT reserve value by 5% to $325 million and maintained reserve volumes at 12.1 MMboe (99.4% heavy oil).

Increased Proved plus Probable (2P) NPV10 BT reserve value by 5% to $416 million and maintained reserve volumes at 16.3 MMboe (99.4% heavy oil).

Note: (1)Non-IFRS financial measure that is not a standardized financial measure under International Financial Reporting Standards (“IFRS”) and may not be comparable to similar financial measures disclosed by other issuers. Refer to “Non-IFRS and Other Financial Measures” section below.

Financial and Operating Summary

Selected financial and operational highlights should be read in conjunction with Hemisphere’s audited annual financial statements and related Management’s Discussion and Analysis for the year ended December 31, 2023. These reports, including the Company’s Annual Information Form for the year ended December 31, 2023, are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Three Months Ended December 31

Years Ended December 31

($000s except per unit and share amounts)

2023

2022

2023

2022

FINANCIAL

Petroleum and natural gas revenue

$

22,423

$

19,564

$

84,472

$

96,699

Operating field netback(1)

13,517

10,926

51,843

58,270

Operating netback(1)

14,428

11,396

52,118

51,995

Cash provided by operating activities

13,496

8,995

44,241

45,091

Adjusted funds flow from operations (AFF)(1)

11,295

11,011

39,411

46,686

Per share, basic(1)

0.11

0.11

0.39

0.47

Per share, diluted(1)

0.11

0.11

0.39

0.46

Free funds flow (FFF)(1)

9,144

4,921

22,539

28,420

Net income

3,981

3,253

24,195

21,317

Per share, basic

0.04

0.03

0.24

0.21

Per share, diluted

0.04

0.03

0.24

0.21

Dividends

5,489

2,560

13,083

7,683

Per share, basic

0.025

0.025

0.130

0.075

NCIB share repurchases

2,085

1,694

4,095

3,387

Capital expenditures (1)

2,151

6,090

16,872

18,266

Working capital (Net debt)(1)

3,589

(766

)

3,589

(766

)

OPERATING

Average daily production

Heavy oil (bbl/d)

3,364

2,884

3,100

2,801

Natural gas (Mcf/d)

132

138

147

158

Combined (boe/d)

3,386

2,907

3,125

2,828

Oil weighting

99%

99%

99%

99%

Average sales prices

Heavy oil ($/bbl)

$

72.36

$

73.52

$

74.53

$

94.29

Natural gas ($/Mcf)

2.19

4.76

2.56

5.03

Combined ($/boe)

$

71.97

$

73.16

$

74.07

$

93.69

Operating netback ($/boe)

Petroleum and natural gas revenue

$

71.97

$

73.16

$

74.07

$

93.69

Royalties

(14.07

)

(16.50

)

(14.71

)

(23.71

)

Operating costs

(11.49

)

(13.16

)

(10.87

)

(11.09

)

Transportation costs

(3.03

)

(2.64

)

(3.03

)

(2.43

)

Operating field netback(1)

43.38

40.86

45.46

56.46

Realized commodity hedging gain (loss)

2.92

1.76

0.24

(6.08

)

Operating netback(1)

$

46.30

$

42.62

$

45.70

$

50.38

General and administrative expense

(5.63

)

(4.92

)

(4.05

)

(3.94

)

Interest expense and foreign exchange (loss)

(0.44

)

(0.70

)

(0.58

)

(1.00

)

Current tax expense

(3.98

)

4.18

(6.51

)

(0.21

)

Adjusted funds flow from operations(1) ($/boe)

$

36.25

$

41.18

$

34.56

$

45.23

Note: (1)Non-IFRS financial measure that is not a standardized financial measure under IFRS Accounting Standards (“IFRS”) and may not be comparable to similar financial measures disclosed by other issuers. Refer to “Non-IFRS and Other Financial Measures” section of the MD&A.

COMMON SHARES

April 17, 2024

December 31, 2023

December 31, 2022

Common shares issued and outstanding

97,951,239

99,340,339

101,978,939

Stock options

7,563,000

7,563,000

6,075,000

Total fully diluted shares outstanding

105,514,239

106,903,339

108,053,939

Operations Update and Outlook

2023 was another rewarding year for Hemisphere, resulting in production growth of 11%, significant shareholder returns of $0.17 per share paid in dividends and NCIB purchases (representing a FFF payout ratio(2) of 76%), and the transformation from a net debt to a cash position.

Additionally, Hemisphere purchased mineral rights in a Saskatchewan oil resource play during the year, and kicked off the first quarter of 2024 by successfully drilling a 5-well pad (3 producers and 2 injectors) into the pool. The Company anticipates bringing the wells on production in the third quarter of the year, after commissioning a new polymer flood facility and oil treating battery in the area. The remainder of Hemisphere’s 2024 capital development program will be spent in its core Atlee Buffalo property later this summer.

Following significant downtime due to extreme cold weather in January and early February, Hemisphere’s corporate production during the latter half of the quarter has reached all-time highs of over 3,500 boe/d (February 15 – March 31, 2024 field estimates, 99% heavy oil), bringing average first quarter production to 3,135 boe/d.

Pricing outlook for heavy oil is bullish across the industry with the Trans Mountain pipeline anticipated to commence operations in May. With this additional egress capacity, WCS differential forecasts for the year have narrowed substantially. Combined with strong WTI pricing and a weak Canadian dollar, Hemisphere is optimistic about the year ahead as it tests its new Saskatchewan play while continuing to deliver top-tier free funds flow yields to its shareholders from ultra-low decline, high-value reserves in Atlee Buffalo.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Note: (2) Non-IFRS Financial Ratio that is not a standardized financial measure under IFRS and may not be comparable to similar ratios disclosed by other issuers. Free funds flow, a non-IFRS financial measure, is used as a component of the non-IFRS ratio. The ratio is calculated as dividends of $13.1 million plus NCIB of $4.1 million divided by FFF of $22.5 million, equals a FFF payout ratio of 76% to shareholders.

Forward-looking Statements

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements regarding Hemisphere’s expectations that it will bring wells in Saskatchewan on production in the third quarter of the year, after commissioning a new polymer flood facility and oil treating battery in the area; that the remainder of Hemisphere’s 2024 capital development program will be spent in its core Atlee Buffalo property later this summer; outlook for heavy oil and commencement of operations for the Trans Mountain pipeline; anticipated WCS differential forecasts for the year and Hemisphere’s outlook for the year. In addition, statements relating to “reserves” are deemed to be forward-looking statements as they involve the implied assessment, based on certain estimates and assumptions, that the reserves described exist in the quantities predicted or estimated and can be profitably produced in the future.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; timing of operations for the Trans Mountain pipeline; completion of commissioning a new polymer flood facility and oil treating battery in in its Saskatchewan operating area in the manner (and on the timing) currently expected; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, free funds flow, operating field netback and operating netback, capital expenditures and net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered to be more meaningful than IFRS measures in evaluating the Company’s performance.

a) Adjusted funds flow from operations (“AFF”) (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures, and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

A reconciliation of AFF to cash provided by operating activities is presented as follows:

Three Months Ended December 31

Years Ended December 31

($000s, except per share amounts)

2023

2022

2023

2022

Cash provided by operating activities

$

13,496

$

8,995

$

44,240

$

45,091

Change in non-cash working capital

(2,259

)

1,447

(5,266

)

911

Adjust: Decommissioning obligation expenditures

58

569

437

684

Adjusted funds flow from operations

$

11,295

$

11,011

$

39,411

$

46,686

Per share, basic

$

0.11

$

0.11

$

0.39

$

0.47

Per share, diluted

$

0.11

$

0.11

$

0.39

$

0.46

b)Free funds flow (“FFF”) (Non-IFRS Financial Measures): Is calculated by taking adjusted funds flow and subtracting capital expenditures, excluding acquisitions and dispositions. Management believes that free funds flow provides a useful measure to determine Hemisphere’s ability to improve returns and to manage the long-term value of the business.

Three Months Ended December 31

Years Ended December 31

($000s, except per share amounts)

2023

2022

2023

2022

Adjusted funds flow

$

11,295

$

11,011

$

39,411

$

46,686

Capital expenditures

(2,151

)

(6,090

)

(16,872

)

(18,266

)

Free funds flow

$

9,144

$

4,921

$

22,539

$

28,420

Per share, basic

$

0.09

$

0.05

$

0.22

$

0.29

Per share, diluted

$

0.09

$

0.05

$

0.22

$

0.28

c) Capital Expenditures (Non-IFRS Financial Measure): Management uses the term “capital expenditures” as a measure of capital investment in exploration and production assets, and such spending is compared to the Company’s annual budgeted capital expenditures. The most directly comparable IFRS measure for capital expenditures is cash flow used in investing activities. A summary of the reconciliation of cash flow used in investing activities to capital expenditures is set forth below:

Three Months Ended December 31

Years Ended December 31

($000s)

2023

2022

2023

2022

Cash used in investing activities

$

3,745

$

4,680

$

19,456

$

18,847

Change in non-cash working capital

(1,594

)

1,410

(2,584

)

(581

)

Capital expenditures

$

2,151

$

6,090

$

16,872

$

18,266

d) Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): Is a benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e) Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): Is calculated as the operating field netback plus the Company’s realized commodity hedging gain (loss) on an absolute and per barrel of oil equivalent basis.

f) Net debt (Non-IFRS Financial Measure): Is closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding the fair value of financial instruments, lease and warrant liabilities, and including the bank debt. There is no IFRS measure that is reasonably comparable to net debt.

The following table outlines the Company calculation of net debt:

As at December 31

2023

2022

Current assets(1)

$

14,110

$

5,825

Current liabilities(1)

(10,521

)

(6,591

)

Working capital / (Net debt)

$

3,589

$

(765

)

Note: (1)Excluding fair value of financial instruments, and lease and decommissioning obligations.

g)Supplementary Financial Measures and Ratios

“Adjusted Funds Flow from operations per basic share” is comprised of funds from operations divided by basic weighted average common shares. “Adjusted Funds Flow from operations per diluted share” is comprised of funds from operations divided by diluted weighted average common shares. “Operating expense per boe” is comprised of operating expense, as determined in accordance with IFRS, divided by the Company’s total production. “Free Funds Flow Payout Ratio” is a non-IFRS financial ratio comprised of dividends declared during the year plus NCIB expenditures during the year divided by free funds flow (a non-IFRS financial measure) for the applicable year. “Realized heavy oil price” is comprised of heavy crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. “Realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. “Realized combined price” is comprised of total commodity sales from production, as determined in accordance with IFRS, divided by the Company’s total production. “Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the Company’s total production. “Transportation costs per boe” is comprised of transportation expense, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2023, which is available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

All estimated reserve volumes and the estimated net present values of the future net revenues of such reserve estimates included in this news release are as attributed by McDaniel Associates & Consultants Ltd., the Company’s independent reserve evaluators in its report as at December 31, 2023 and prepared in accordance with the COGE Handbook and National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

It should not be assumed that the net present value of the estimated net revenues of the reserves presented in this news release represent the fair market value of the reserves. There is no assurance that the forecast prices and costs assumptions upon which such estimates are made will be attained and variances could be material. The reserve estimates of Hemisphere’s crude oil, natural gas liquids and natural gas reserves and any estimated recovery factors provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual crude oil, natural gas and natural gas liquids reserves may be greater than or less than the estimates provided herein.

Definitions and Abbreviations

bbl

barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

NGL

natural gas liquids

boe/d

barrel of oil equivalent per day

NPV10 BT

Net Present Value discounted at 10%, before tax

$/boe

dollar per barrel of oil equivalent

IFRS

International Financial Reporting Standards

Mboe

thousand barrels of oil equivalent

WCS

Western Canadian Select

MMboe

million barrels of oil equivalent

US$

United States Dollar

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Hemisphere announced an independent evaluation of its reserves highlighting a 5% increase in NPV10 value for proved reserves. The estimated value for total proved reserves (PR) when discounted back at a 10% rate was $325 million ($3.27 per share) versus $308 million in the reserve from last year. The increase reflects higher West Canada Select oil prices in future years with the completion of the Trans Mountain Pipeline running from Alberta to the Pacific Coast. The value of proved developed producing (PDP) reserves rose 9% as the company was active drilling in 2023 and moving reserves into the PDP category.

The company was able to replace reserves reduced by production through drilling and acquisition. Hemisphere produced 1.1 mmboe in 2023 and added 1.0 mmboe of reserves through the drillbit or from acquisition. As a result, proved reserves were 12.1 mmboe in the most recent report versus 12.2 mmboe last year. The company spent $16 million to drill eight wells in addition to purchasing land and seismic. Just two years ago, capital expenditures were only $8 million. Finding, Development and Acquisition costs per proved reserve added in 2023 were $14.82/boe, an attractive price given current oil prices.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – March 12, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce highlights from its independent reserves evaluation (the “Reserve Report”), prepared by McDaniel & Associates Consultants Ltd. (“McDaniel”) and effective as at December 31, 2023.

In 2023, Hemisphere invested $16 million to drill eight successful Atlee Buffalo wells, upgrade facilities in Atlee Buffalo, purchase land and seismic, and pre-purchase some of the materials for its 2024 development program. With the Company’s capital additions, corporate production in 2023 increased by more than 10% year-over-year, to 3,124 boe/d (99% heavy oil). Production is currently trending over 3,450 boe/d (99% heavy oil, based on field estimates between February 10 – March 10, 2024), after significant downtime experienced in January and early February due to extreme cold weather and equipment failure.

During the year, Hemisphere also distributed $13.1 million in base and special dividends, purchased 3.2 million shares under its normal course issuer bid (“NCIB”) for a total price of $4.0 million (at an average price of $1.25/share), and exited the year in a cash position with working capital1 of over $3 million.

The Company’s continued success in the development of its enhanced oil recovery projects was recognized again by McDaniel in the Reserve Report. In the Proved Developed Producing (“PDP”) category, Hemisphere replaced 104% of 2023 production and increased reserve value by 9% to $248 million NPV10 BT. Hemisphere also grew Proved (“1P”) reserve value to $325 million NPV10 BT and Proved plus Probable (“2P”) reserve value to $416 million NPV10 BT.

The Company’s new Saskatchewan lands currently account for only 5% of 1P and 7% of 2P reserves, while making up only 3% of 1P and 5% of 2P NPV10 BT valuations of Hemisphere’s reserves. Significant reserve upside remains on Hemisphere lands if the play proves successful over the course of 2024 and beyond.

Consistent with McDaniel’s 2022 year-end evaluation, the Reserve Report incorporates full corporate abandonment, decommissioning, and reclamation costs (“ADR”) in the PDP category. Hemisphere has always been cautious of acquiring additional wellbore and facility liabilities. A direct result of this strategy is that Hemisphere’s reserves retain more comparative value per barrel than companies with additional ADR liabilities that must be deducted from their base valuations. Management estimates that total undiscounted and uninflated existing ADR is $8.3 million ($2.3 million NPV10 BT, with costs inflated at 2%/yr), which includes all ADR associated with both active and inactive wells, pipelines, and facilities regardless of whether such wells, pipelines, and facilities had any attributed reserves. Based on public information, Hemisphere stands out among its industry peers as being within the top 8% of Alberta oil and gas operators for its industry-leading liability management ratio (“LMR”) of 17, resulting in Hemisphere having less than 1% of its PDP net present value impaired by ADR.

Hemisphere’s low decline, long life, and high value reserves are a sign of the tremendous resource the Company has been developing over the past number of years. These valuable assets are the backbone of Hemisphere and are expected to generate significant free cash flow as they continue to grow with planned additional development and optimization of enhanced oil recovery techniques.

2023 Reserve Highlights

Proved Developed Producing (“PDP”) Reserves

NPV10 BT of $248 million, an increase of 9% over year-end 2022 and equivalent to $2.49 per basic share.

Replaced 104% of 2023 production through organic development.

Maintained reserve volumes year-over-year at 8.2 MMboe (99.6% heavy crude oil).

Achieved a 2-year FD&A cost of $9.30/boe (including changes in future development capital (“FDC”)) for a recycle ratio of 5.4.

RLI of 7.2 years based on 2023 production.

Proved (“1P”) Reserves

NPV10 BT of $325 million, an increase of 5% over year-end 2022 and equivalent to $3.27 per basic share.

Replaced 90% of 2023 production through organic development.

Maintained reserve volumes year-over-year at 12.1 MMboe (99.4% heavy crude oil).

Achieved a 2-year FD&A cost of $14.82/boe (including changes in FDC) for a recycle ratio of 3.4.

RLI of 10.6 years based on 2023 production.

NAV of $3.18 per fully diluted share based on Reserve Report pricing assumptions.

NAV of $3.28 and $4.27 per fully diluted share based on Reserve Report run internally at McDaniel’s pricing sensitivities of US$80 and US$100 WTI flat pricing.

Proved plus Probable (“2P”) Reserves

NPV10 BT of $416 million, an increase of 5% over year-end 2022 and equivalent to $4.19 per basic share.

Replaced 125% of 2023 production through organic development.

Maintained reserve volumes at 16.3 MMboe (99.4% heavy crude oil).

Achieved a 2-year FD&A cost of $14.91/boe (including changes in FDC) for a recycle ratio of 3.4.

RLI of 14.3 years based on 2023 production.

NAV of $4.03 per fully diluted share based on Reserve Report pricing assumptions.

NAV of $4.12 and $5.36 per fully diluted share based on Reserve Report run internally at McDaniel’s pricing sensitivities of US$80 and US$100 WTI flat pricing.

2023 Independent Qualified Reserve Evaluation

The reserves data set forth below is based upon an independent reserves evaluation prepared by McDaniel dated March 11, 2024 with an effective date of December 31, 2023, and is in accordance with definitions, standards, and procedures contained within COGEH and National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Additional reserve information as required under NI 51-101 will be included in Hemisphere’s Annual Information Form which will be filed on SEDAR+ on or before April 30, 2024. Due to rounding, certain totals in the columns may not add in the following tables. All dollar values are in Canadian dollars, unless otherwise noted.

Pricing Assumptions

McDaniel’s independent evaluation was based on the average of the published price forecasts for McDaniel, GLJ Petroleum Consultants Ltd., and Sproule Associates Ltd. (the “3-Consultant Average Price Forecast”) at January 1, 2024, with the following table detailing pricing and foreign exchange rate assumptions. Hemisphere’s corporate production historically averages a discount of approximately $4.50 to WCS pricing. When compared to last year’s 3-Consultant Average Price Forecast dated January 1, 2023, the current WCS pricing outlook is down approximately 1% in 2024, and up 1% thereafter over the next 15-year period. The 2024 3-Consultant Average Price Forecast uses a 5-year 2024-28 WTI price of US$76.33/bbl and WCS price of Cdn$81.11/bbl.

3-Consultant Average Price Forecast January 1, 2023

3-Consultant Average Price Forecast January 1, 2024

WTI Crude Oil ($US/bbl)

Edmonton Light Crude Oil ($Cdn/bbl)

Western Canadian Select WCS Crude Oil ($Cdn/bbl)

AECO Spot Price ($Cdn/MM Btu)

Inflation (%)

US/Cdn Exchange Rate ($US/$Cdn)

WTI Crude Oil ($US/bbl)

Western Canadian Select WCS Crude Oil ($Cdn/bbl)

Edmonton Light Crude Oil ($Cdn/bbl)

AECO Spot Price ($Cdn/MM Btu)

Inflation (%)

US/Cdn Exchange Rate ($US/$Cdn)

2024

78.50

97.74

77.75

4.40

2.3

0.765

2024

73.67

92.91

76.74

2.20

0

0.745

2025

76.95

95.27

77.55

4.21

2

0.768

2025

74.98

95.04

79.77

3.37

2

0.765

2026

77.61

95.58

80.07

4.27

2

0.772

2026

76.14

96.07

81.12

4.05

2

0.768

2027

79.16

97.07

81.89

4.34

2

0.775

2027

77.66

97.99

82.88

4.13

2

0.772

2028

80.74

99.01

84.02

4.43

2

0.775

2028

79.22

99.95

85.04

4.21

2

0.775

2029

82.36

100.99

85.73

4.51

2

0.775

2029

80.80

101.94

86.74

4.30

2

0.775

2030

84.00

103.01

87.44

4.60

2

0.775

2030

82.42

103.98

88.47

4.38

2

0.775

2031

85.69

105.07

89.20

4.69

2

0.775

2031

84.06

106.06

90.24

4.47

2

0.775

2032

87.40

106.69

91.11

4.79

2

0.775

2032

85.74

108.18

92.04

4.56

2

0.775

2033

89.15

108.83

92.93

4.88

2

0.775

2033

87.46

110.35

93.89

4.65

2

0.775

2034

90.93

111.00

94.79

4.98

2

0.775

2034

89.21

112.56

95.77

4.74

2

0.775

2035

92.75

113.22

96.69

5.08

2

0.775

2035

90.99

114.81

97.68

4.84

2

0.775

2036

94.61

115.49

98.62

5.18

2

0.775

2036

92.81

117.10

99.64

4.94

2

0.775

2037

96.50

117.80

100.59

5.29

2

0.775

2037

94.67

119.45

101.63

5.03

2

0.775

2038

98.43

120.16

102.60

5.40

2.00

0.78

2038

96.56

121.83

103.66

5.14

2.00

0.78

Summary of Reserves(1)

Heavy Oil

Conventional Natural Gas

Total

Reserves Category

(Mbbl)

(MMcf)

(Mboe)

Proved

Developed Producing

8,196

173

8,225

Developed Non-Producing

34

7

35

Undeveloped

3,756

250

3,798

Total Proved

11,987

429

12,058

Probable

4,231

188

4,262

Total Proved plus Probable

16,217

617

16,320

Note:

(1)Reserves are presented as “gross reserves” which are the Company’s working interest reserves before royalty deductions and without including any royalty interests.

Summary of Net Present Value of Future Net Revenue, Before Tax (“NPV BT”) (1)(2)

NPV BT (M$, except per share amount)

Discounted at (% per Year)

Reserves Category

0%

5%

10%