Washington DC Law Firm that Won Operation Choke Hold Suit, Gives Congress Advice

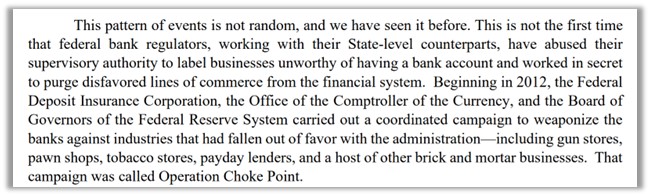

Are private digital assets, under unlawful attack by regulators? Sounds conspiratorial, but a D.C. law firm that successfully sued the FDIC, Federal Reserve, and Office of the Controller of the Currency (OCC), says they are doing just that. The firm Cooper & Kirk, won a large lawsuit dubbed against the agencies for their part in, “Operation Choke Point.” That was a decade ago, the law firm now claims they have uncovered a coordinated campaign by bank regulators to drive crypto out of the U.S. financial system.

The new “Operation Choke Point 2.0,” according to the firms website, “have published informal guidance documents that single out cryptocurrency and cryptocurrency customers as a risk to the banking system.” According to an informational paper published by the D.C. firm, “businesses in the cryptocurrency marketplace are losing their bank accounts, or their access to the ACH network, suddenly, and with no explanation from their bankers, the paper continued, “the owners and employees of cryptocurrency firms are even having their personal accounts closed without explanation.”

As an example of could be viewed as overstepping their charters, the firm pointed out that, “over the past two weeks, federal regulators have shut down a solvent bank that was known to be serving the crypto industry and, although it is required to resolve banks through the “least cost resolution” to the Deposit Insurance Fund, the FDIC chose to shutter rather than sell the part of the bank that serves digital asset customers, costing the Fund billions of dollars.” The overall theme of the 37 page paper is that the targeting of certain businesses is going on to force them out of existence.

What are Regulators Accused Of

Specifically the regulators are being accused of:

- Depriving businesses of their constitutional right to due process. This is a fifth amendment right that says that an entity tagging another with a derogatory label that causes injury (like lose bank accounts) The firm accuses that this is what the regulators have done by “labeling crypto a threat to the financial system.”

- Violating both the non-delegation and anticommandeering doctrine by, “depriving Americans of Key Structural constitutional protections against the arbitrary exercise of government power.”

- Refusing to perform their non-discretionary duties “when doing so will benefit the cryptocurrency industry.”

- Evading rules that require periods of notice and comment of the rulemaking requirements of the administrative procedure act. It claims circumventing this is, “undemocratic.”

- Acting in an arbitrary and capricious fashion by avoiding explaining underlying rules for their decisions. “It is difficult to imagine a more arbitrary and capricious agency action that simultaneously placing a solvent bank into receivership solely because it provided financial services to the cypto industry, while permitting insolvent institutions not tied to the crypto industry to continue operations.”

What is the Law Firms Stated Intent

Cooper and Kirk urge the U.S. Congress to perform its role and hold the agencies accountable. The firm urges the Congress to ask for all communications records related to these matters from the regulators.

The firm also would like for them to explain the basis for their conclusion that safety and soundness of the banking system requires the banking system be insulated from crypto. They would also like for it to be made clear to the agencies that the comment period of the Administrative procedure act is mandatory. It wanst an investigation into why Signature Bank was closed.

The last stated hope is fro Congress to investigate whether bank regulators are working to squelch innovation from the private sector in order to clear out competition for the benefit of existing regulated banks and a new federal crypto asset.

Take Away

Just like the first Operation Choke Point was targeting specific players, the new version does the same. The law firms stops short of any threats in their open paper, but it makes clear that the firm has solid experience achieving compliance if these maters.

https://www.cooperkirk.com/wp-content/uploads/2023/03/Operation-Choke-Point-2.0.pdf