DALLAS, Oct. 18, 2022 (GLOBE NEWSWIRE) — Permex Petroleum Corporation (CSE: OIL) (OTCQB: OILCF) (FSE: 75P) (“Permex” or the “Company“), a junior oil and gas company, will be participating in The ThinkEquity Conference, which will take place on October 26, 2022 at The Mandarin Oriental Hotel in New York.

Mehran Ehsan, President and CEO, will be presenting at 12:00 PM ET on October 26th. Interested parties can register to attend here. Members of the Permex Petroleum Corporation management will also be holding one-on-one investor meetings throughout the day.

About Permex Petroleum Corporation

Permex Petroleum is a uniquely positioned junior Oil & Gas company with assets and operations across the Permian Basin of West Texas and the Delaware Sub-Basin of New Mexico. The company focuses on combining its low-cost development of Held by Production assets (“HBP”) for sustainable growth with its current and future Blue-Sky projects for scale growth. The company through its wholly owned subsidiary Permex Petroleum US Corporation is a licensed operator in both states; and owns and operates on Private, State and Federal land.

About The ThinkEquity Conference

The ThinkEquity Conference will gather industry insiders, investors and leading executives from around the world on October 26th in New York. Attendees can expect a full day of company presentations, panel discussions, one-on-one investor meetings and more.

Featured sectors include AI/Big data technology, Biotechnology, EV/EV Infrastructure, Metals & Mining and Oil & Gas.

To register to attend The ThinkEquity Conference, please follow this link.

CONTACT INFORMATION Permex Petroleum Corporation Mehran Ehsan President, Chief Executive Officer & Director 469-804-1306

Greg Montgomery CFO, Corporate Secretary & Director 469-804-1306

Or for Investor Relations, please contact: Dave Gentry RedChip Companies Inc. +1-800-RED-CHIP (733-2447) Or +1 407-491-4498 OILCF@redchip.com

CAUTIONARY DISCLAIMER STATEMENT:

The Canadian Securities Exchange has neither approved nor disapproved the contents of this press release.

Forward-Looking Statements

This news release includes certain statements and information that may constitute forward-looking information within the meaning of applicable Canadian securities laws. Forward-looking statements relate to future events or future performance and reflect the expectations or beliefs of management of the Company regarding future events. Generally, forward-looking statements and information can be identified by the use of forward-looking terminology such as “intends”, “expects” or “anticipates”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “should”, “would” or will “potentially” or “likely” occur. This information and these statements, referred to herein as “forward‐looking statements”, are not historical facts, are made as of the date of this news release and include without limitation, statements regarding Permex’s expectations of entering into a growth phase in relation to its business and drilling programs; the market opportunity in the oil and gas industry; Permex’s future plans to bring additional shut-in wells online, and the deployment of the Company’s capital.

In addition, forward-looking statements or information are based on a number of material factors, expectations or assumptions of Permex which have been used to develop such statements and information but which may prove to be incorrect. Although Permex believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because Permex can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: that Permex will continue to conduct its operations in a manner consistent with past operations; continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Permex’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Permex’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Permex operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Permex to obtain qualified staff, equipment and services in a timely and cost efficient manner; the ability of Permex to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Permex operates; and the ability of Permex to successfully market its oil and natural gas products.

Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements and information. Readers are cautioned that reliance on such information may not be appropriate for other purposes. The Company does not undertake to update any forward-looking statement, forward-looking information or financial outlook that are incorporated by reference herein, except in accordance with applicable securities laws. We seek safe harbor.

CALGARY, Alberta, Oct. 13, 2022 (GLOBE NEWSWIRE) — InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) today announced that the Toronto Stock Exchange (“TSX“) has accepted InPlay’s notice of intention to commence a normal course issuer bid (the “NCIB“).

Under the NCIB, InPlay may purchase for cancellation, from time to time, as InPlay considers advisable, up to a maximum of 6,467,875 common shares of InPlay (“Common Shares“), which represents 10% of the Company’s public float of 64,678,759 Common Shares as at October 7, 2022. As of the same date, InPlay had 87,150,301 Common Shares issued and outstanding. Purchases of Common Shares may be made on the open market through the facilities of the TSX and through other alternative Canadian trading platforms at the prevailing market price at the time of such transaction. The actual number of Common Shares that may be purchased for cancellation and the timing of any such purchases will be determined by InPlay, subject to a maximum daily purchase limitation of 112,558 Common Shares which equates to 25% of InPlay’s average daily trading volume of 450,234 Common Shares for the six months ended September 30, 2022. InPlay may make one block purchase per calendar week which exceeds the daily repurchase restrictions. Any Common Shares that are purchased by InPlay under the NCIB will be cancelled.

The NCIB will commence on October 17, 2022 and will terminate on October 16, 2023 or such earlier time as the NCIB is completed or terminated at the option of InPlay.

InPlay believes that implementing the NCIB is a prudent step in this volatile energy market environment, when at times, the prevailing market price does not reflect the underlying value of its Common Shares. The timely repurchase of the Company’s Common Shares for cancellation represents confidence in the long term prospects and sustainability of its business model. This reduction in share count adds per share value to InPlay’s shareholders and adds another tool to management’s disciplined capital allocation strategy.

About InPlay Oil Corp.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The Company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The Common Shares on the Toronto Stock Exchange under the symbol IPO and the OTCQX under the symbol IPOOF.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

This news release contains certain statements that may constitute forward-looking information within the meaning of applicable securities laws. This information includes, but is not limited to InPlay’s intentions with respect to the NCIB and purchases thereunder and the effects of repurchases under the NCIB. Although InPlay believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because InPlay can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions by their very nature they involve inherent risks and uncertainties. Actual results could defer materially from those currently anticipated due to a number of factors and risks. Certain of these risks are set out in more detail in InPlay’s Annual Information Form which has been filed on SEDAR and can be accessed at www.sedar.com.

The forward-looking statements contained in this press release are made as of the date hereof and InPlay undertakes no obligation to update publically or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

ENGLEWOOD, Colo., Oct. 12, 2022 (GLOBE NEWSWIRE) — Gevo, Inc. (NASDAQ: GEVO) announced today that it will host a conference call on Tuesday, November 8, 2022, at 4:30 p.m. EST (2:30 p.m. MST) to report its financial results for the third quarter ended September 30, 2022 and provide an update on recent corporate highlights.

A webcast replay will be available two hours after the conference call ends on November 8, 2022. The archived webcast will be available in the Investor Relations section of Gevo’s website at www.gevo.com.

About Gevo Inc.

Gevo’s mission is to transform renewable energy and carbon into energy-dense liquid hydrocarbons. These liquid hydrocarbons can be used for drop-in transportation fuels such as gasoline, jet fuel, and diesel fuel, that when burned have potential to yield net-zero greenhouse gas emissions when measured across the full lifecycle of the products. Gevo uses low-carbon renewable resource-based carbohydrates as raw materials and is in an advanced state of developing renewable electricity and renewable natural gas for use in production processes, resulting in low-carbon fuels with substantially reduced carbon intensity (the level of greenhouse gas emissions compared to standard petroleum fossil-based fuels across their lifecycle). Gevo’s products perform as well or better than traditional fossil-based fuels in infrastructure and engines, but with substantially reduced greenhouse gas emissions. In addition to addressing the problems of fuels, Gevo’s technology also enables certain plastics, such as polyester, to be made with more sustainable ingredients. Gevo’s ability to penetrate the growing low-carbon fuels market depends on the price of oil and the value of abating carbon emissions that would otherwise increase greenhouse gas emissions. Gevo believes that it possesses the technology and know-how to convert various carbohydrate feedstocks through a fermentation process into alcohols and then transform the alcohols into renewable fuels and materials, through a combination of its own technology, know-how, engineering, and licensing of technology and engineering from Axens North America, Inc., which yields the potential to generate project and corporate returns that justify the build-out of a multi-billion-dollar business.

Gevo believes that Argonne National Laboratory GREET model is the best available standard of scientific based measurement for life cycle inventory or LCI.

Company Contact: John Richardson (Director of Investor Relations) Gevo, Inc. Tel: +1 720-360-7794 E-mail: IR@gevo.com

ENGLEWOOD, Colo., Oct. 10, 2022 (GLOBE NEWSWIRE) — Gevo, Inc. (NASDAQ: GEVO) (“Gevo” or the “Company”), a renewable fuels company focused on the production of sustainable aviation fuel (“SAF”), today provides an update on the Company and projects currently in process.

Market Development Gevo now has approximately 375 million gallons per year (“MGPY”) of predominantly take-or-pay, financeable SAF and hydrocarbon fuel supply agreements, which are expected to support project debt financing. This level of demand would require multiple plants to be built over the next four years to satisfy those agreements. Based on current market projections and certain assumptions, collectively, these agreements represent approximately $2.3 billion in expected annual sales. Offtake partners include: Trafigura, Kolmar, Delta Airlines, American Airlines, Alaska Airlines, Finnair, Japan Airlines, British Airways, Aer Lingus, and SAS.

Inflation Reduction Act The Inflation Reduction Act (“IRA”) which was signed into law in August of this year is helpful to many companies in the renewable energy industry and is a positive signal for SAF specifically. The first phase of this two-phased approach to encouraging investment in the SAF industry creates a SAF blenders tax credit for the 2023-2024 period with a value potential of $1.25 per gallon. In the second two-year phase, 2025-2027, it created a Clean Fuel Production Credit (“CFPC”) that has a credit of $1.75 per gallon for domestically produced, net-zero carbon intensity (“CI”) score SAF. The value of both credits is based on the CI score of the fuel produced and requires a minimum 50% reduction in greenhouse gas (“GHG”) emissions. Gevo, like other net-zero businesses, is expected to benefit from such a program because of the expected low CI score of Gevo products.

Net-Zero 1 Status Following the recent groundbreaking ceremony in Lake Preston, South Dakota, the Net-Zero 1 (“NZ1”) project is on schedule with initial volumes of SAF expected to be delivered in 2025. NZ1 is expected to produce approximately 55 MGPY of SAF, or 62 MGPY of total hydrocarbon volumes, which would satisfy part of the ~375 MGPY of financeable SAF and hydrocarbon supply agreements that are currently in place.

The transition to an ethanol-to-SAF design from Gevo’s original isobutanol-to-SAF and isooctane design continues to yield improved output expectations as pre-project planning has been completed through phase 2 of front-end loading work (“FEL-2”). The results of this work, combined with support from the CFPC, have led to the forecast Project EBITDA1 for NZ1 to be in the range of $300-$325 million per year, a 56% increase at the mid-point from the prior estimate of $200 million per year. The total installed cost for NZ1, including the capital required for the alcohol-to-jet fuel plant as well as any site development costs, is currently forecasted to be approximately $850 million, a 33% increase from the prior estimate of $640 million. This increase is primarily due to increased steel, equipment, and supply chain costs related to the inflationary environment.

Progress on Key NZ1 Development Milestones Through year-end 2022:

√ Close the purchase of the land for NZ1 in Lake Preston, South Dakota √ Execute development agreements for:

√ Wind energy – Wastewater (design no longer requires) √ Green hydrogen

• Select engineering, procurement, and construction (“EPC”) contractor • Select fabricator for hydrocarbon plant modules • Substantial Completion of Front End Engineering Design √ Break ground and begin site preparation at Lake Preston

Through first-half 2023:

• Close the construction financing, including non-recourse debt • Order long lead equipment

Throughout the remainder of 2022 and 2023, Gevo expects to update stockholders about certain key milestones related to the development, financing, and construction of NZ1 as well as subsequent Net-Zero plants. Updates to those milestones will be found in the Company’s press releases and investor presentations in the Investor Relations section of Gevo’s website.

Additional Plant Sites Gevo continues to make steady progress on securing future SAF production locations beyond NZ1. These future sites must offer an appealing mix of attributes that enable the Company to produce low-cost fuels with the lowest carbon footprint possible. Gevo’s preferred list of partners and locations with decarbonization in mind are continuously being refined and the Company is engaged in preliminary feasibility and development discussions with several of them, including ADM.

RNG Project Status Gevo’s renewable natural gas (“RNG”) project in Northwest Iowa (the “RNG Project”) continues to ramp up its production. The Company recently received notice from the federal Renewable Fuel Standard (“RFS”) that the RNG produced qualifies for Renewable Identification Numbers (“RINs”). Gevo will begin to recognize revenue for RNG sales in the third quarter of 2022; however, initial revenue will be limited to the value of the commodity, exclusive of environmental credits and will represent a partial quarter. Some sales revenue from environmental attributes are expected in the fourth quarter of 2022; however, the full extent of the available credits will begin contributing to revenue in 2023 due to timing of the approval and documentation process for the Low Carbon Fuel Standard (“LCFS”) credits.

The RNG Project is expected to generate Project EBITDA1 in the range of $16-$22 million per year beginning in 2023, depending on a variety of assumptions, including the value of credits under the federal RFS and the LCFS in California.

Verity Tracking & U.S. Department of Agriculture Grant Gevo is proud to have been tentatively awarded up to $30 million by the U.S. Department of Agriculture to advance its Climate-Smart Farm-to-Flight initiative. This award and program are expected to be finalized in the coming months.

Gevo will be working with its strong team of partners in the Lake Preston, South Dakota area to lower the Company’s carbon footprint throughout the SAF business system as well as within other projects in Gevo’s portfolio of projects. Gevo plans to deliver a high-quality carbon accounting system that will help reward growers who adopt farming methods that reduce greenhouse GHG emissions. This accounting system will focus on the importance of immutable tracking and tracing of carbon-intensity scores that begins at the farm level and follows the molecules through the production of SAF and finally to its ultimate use in a jet engine. Gevo plans to accomplish these goals through further development and implementation of Verity Tracking, which is a blockchain-enabled solutions platform for carbon tracking throughout an entire business system.

Chevron Conversations between Chevron and Gevo continue as we each evaluate how best to structure our relationship going forward. Chevron and the Company have mutually agreed upon an extension to the letter of intent between the parties that allows these discussions and negotiations to continue.

Management Comment Dr. Patrick Gruber, CEO of Gevo commented, “With the bulk of the engineering and design work for Gevo’s NZ1 project in South Dakota nearing completion and our RNG project in Iowa up and running, a portion of our team can shift their focus to the development and planning for projects beyond NZ1. We now have approximately 375 MGPY of commercial offtake commitments. Our team will take all that we have learned, and continue to learn, from the design and construction process for NZ1 and leverage that growing knowledge base as we plan and design each subsequent plant. Gevo has developed an outstanding set of partners with the capability to help execute our plans. We are excited to get on with building out capacity and getting product to the market at commercial scale. NZ1 is going to demonstrate how a commercial scale SAF plant can achieve net-zero greenhouse gas emissions.” Dr. Gruber continued, “The passage of the Inflation Reduction Act is a game changer and is expected to reward companies like ours that drive to net-zero emissions.”

Upcoming Investor Conferences Presentations provided in conjunction with these events will be available on Gevo’s website at www.gevo.com in the Investor Relations section on the morning of the respective presentation. Members of Gevo’s senior management will participate in the following hosted investor events:

Capital One Investor Conference – December 6, 2022, in Houston, TX

About Gevo Inc.

Gevo’s mission is to transform renewable energy and carbon into energy-dense liquid hydrocarbons. These liquid hydrocarbons can be used for drop-in transportation fuels such as gasoline, jet fuel, and diesel fuel, that when burned have potential to yield net-zero greenhouse gas emissions when measured across the full lifecycle of the products. Gevo uses low-carbon renewable resource-based carbohydrates as raw materials and is in an advanced state of developing renewable electricity and renewable natural gas for use in production processes, resulting in low-carbon fuels with substantially reduced carbon intensity (the level of greenhouse gas emissions compared to standard petroleum fossil-based fuels across their lifecycle). Gevo’s products perform as well or better than traditional fossil-based fuels in infrastructure and engines, but with substantially reduced greenhouse gas emissions. In addition to addressing the problems of fuels, Gevo’s technology also enables certain plastics, such as polyester, to be made with more sustainable ingredients. Gevo’s ability to penetrate the growing low-carbon fuels market depends on the price of oil and the value of abating carbon emissions that would otherwise increase greenhouse gas emissions. Gevo believes that it possesses the technology and know-how to convert various carbohydrate feedstocks through a fermentation process into alcohols and then transform the alcohols into renewable fuels and materials, through a combination of its own technology, know-how, engineering, and licensing of technology and engineering from Axens North America, Inc., which yields the potential to generate project and corporate returns that justify the build-out of a multi-billion-dollar business.

Gevo believes that Argonne National Laboratory GREET model is the best available standard of scientific based measurement for life cycle inventory or LCI.

Important Cautions Regarding Forward Looking Statements

Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements relate to a variety of matters, including, without limitation, Gevo’s NZ1 project, including the timing of NZ1, the total installed capital estimate for NZ1, the financial projections in this press release, the RNG Project, Gevo’s business development activities, Gevo’s ability to successfully develop, construct and finance its projects, whether Gevo’s supply agreements are financeable, Gevo’s ability to achieve cash flow from its planned projects, Chevron and whether Gevo and Chevron will enter into binding, definitive agreements, and other statements that are not purely statements of historical fact. These forward-looking statements are made based on the current beliefs, expectations and assumptions of the management of Gevo and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Gevo undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Gevo believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Gevo in general, see the risk disclosures in the Annual Report on Form 10-K of Gevo for the year ended December 31, 2021, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the U.S. Securities and Exchange Commission by Gevo.

Company Contact: John Richardson (Director of Investor Relations) Gevo, Inc. Tel: 720-360-7794 E-mail: IR@gevo.com

_________________________________ 1 Project EBITDA is a non-GAAP financial measure that we define as total operating revenues less total operating expenses for the project.

The Organization of Petroleum Exporting Countries (OPEC) and the extended Russia-led allies )making it OPEC+) just agreed to slash two million barrels a day from the global petroleum markets. This is likely to nudge the cost of energy up around the globe. Oil and gas had been trending down in the U.S. in part the result of President Biden’s authorized release of one million barrels a day into the market from the U.S. Strategic Petroleum Reserve back in March.

The move by OPEC+, which counteracts efforts in the U.S. to bring prices down, should have the effect of pushing up global energy prices and benefiting oil-exporting countries such as Russia increase revenue per barrel.

The Russian-Ukraine war has had an impact on crude prices since Russia is a major exporter of the commodity. Prices in the futures market have been falling since June, and are currently near their pre-war levels. The softening in the market price may not be a function of supply, writes Michael Heim, CFA, Senior Research Analyst, at Noble Capital Markets, in his quarterly Energy Industry Report. Heim says they believe, “…recent weakness largely reflects demand concerns and foreign currency changes but is not a condition of oversupply.” Explaining the connection between dollar strength and oil, Heim added, “Historically, oil prices are lower when the dollar is stronger. This is because most oil suppliers, including international suppliers, demand payments in dollars.”

WTI prices peaked at $120 per barrel in the first week of June. According to Heim, since the peak, they have come down as a “response to signs of a global economic slowdown as governments raise interest rates to fight inflation.” Oil on the futures market is down nearly 50% from its 2022 peak.

Oil Prices and Politics

OPEC+ has said they are seeking to prevent price swings rather than to target a particular oil price. Benchmark Brent crude is trading at $92 per barrel after the announcement. “The decision is technical, not political,” United Arab Emirates Energy Minister Suhail al-Mazroui told reporters ahead of the meeting.

The actions announced by OPEC+ may cause the NOPEC Bill (No Oil Producing and Exporting Cartels) that passed the Senate Judiciary Committee back in May to resurface and gain traction. The bipartisan NOPEC bill would change U.S. antitrust law to revoke the sovereign immunity that has long protected OPEC and its national oil companies from lawsuits. Under the Bill, the U.S. attorney general would have the ability to sue the oil cartel or its members, in federal court.

The West has accused Russia of weaponizing energy and orchestrating a crisis in Europe that could trigger rationing power this winter with the potential for gas shortages. This has become a hot issue with humanitarian implications that may help the West paint cartel members in a less than flattering or even adversarial light. While the West is busy accusing Russia of using energy exports in inappropriate ways, Moscow has accused the U.S. and it allies of weaponizing the dollar and financial systems such as SWIFT in retaliation for Russia sending troops into Ukraine in February. SWIFT is a method the U.S. Treasury uses to sanction international suppliers of Russian companies.

While Saudi Arabia has not condemned Moscow’s actions in Ukraine, U.S. officials have said part of the reason Washington wants lower oil prices is to deprive Moscow of oil revenue.

Take Away

Oil will continue to be an interesting sector. The variables impacting price, which have an impact on the broader energy sector include a slowing global economy, ability, and willingness for countries such as the U.S. to tap oil reserves, length of time the Russia and Ukraine war is prolonged, rigs put online, OPEC’s ability to produce at levels targeted, and dollar strength which increases energy costs for those whose native currency is weaker than U.S. petrodollars.

Subscribe to Channelchek and receive emails each day on many industries, including oil and natural gas, as well as in-depth analysis of small-cap energy opportunities.

CALGARY, AB, Oct. 4, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF). We are pleased to announce drilling results from our 182-C2 well. We completed drilling the 182-C2 well to a total measured depth (“MD”) of 3,185 metres on our 100% owned and operated Block 182 in the Recôncavo basin.

Based on open-hole wireline logs, at 2,607 metres total vertical depth (“TVD”), the well encountered 10.9 metres of potential net hydrocarbon pay in the Agua Grande Formation, with an average porosity of 8.9% and average water saturation of 25.1%, using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off.

The 182-C2 well also encountered a 223.7-metre-thick section in the Sergi Formation with 121.3 metres of sand estimated above 6% porosity in the sand-dominated interval between 2,704.1 and 2,927.8 metres TVD. Caliper logs indicate that a significant amount of the wellbore in the Sergi interval contains washouts from drilling and is out of gauge, making open-hole log analysis challenging. As such, hydrocarbon potential in the Sergi will be validated through formation testing.

Based on these drilling results, we plan to case the well and undertake a multi-zone testing program of the 182-C2 well. This testing will assess the extent, if any, of commercial hydrocarbons associated with the well, the productive capability of the well and will help define the field development plan.

Operational Update

On our Murucututu project, we are completing the commissioning of our 183-1 field production facility and expect to have commercial natural gas and condensate sales from the 183-1 well this month.

We are completing service rig inspection and acceptance testing and expect to commence a multizone production test of our 183-B1 well later this week.

September Sales Volumes

September sales volumes averaged 2,686 boepd, including natural gas sales of 15.4 MMcfpd and associated natural gas liquids sales from condensate of 124 bopd, based on field estimates. Our sales volumes averaged 2,642 boepd in the third quarter of 2022, an increase of 12% from the second quarter of 2022.

Corporate Presentation

Alvopetro’s updated corporate presentation is available on our website at:

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Abbreviations:boepd = barrels of oil equivalent (“boe”) per daybopd = barrels of oil and/or natural gas liquids (condensate) per dayMBOE = thousands of barrels of oil equivalentMMcf = million cubic feetMMcfpd = million cubic feet per day

BOE Disclosure. The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Testing and Well Results. Data obtained from the 182-C2 well identified in this press release, including hydrocarbon shows, open-hole logging, net pay and porosities, should be considered to be preliminary until testing, detailed analysis and interpretation has been completed. Hydrocarbon shows can be seen during the drilling of a well in numerous circumstances and do not necessarily indicate a commercial discovery or the presence of commercial hydrocarbons in a well. There is no representation by Alvopetro that the data relating to the 182-C2 well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Cautionary statements regarding the filing of a Notice of Discovery. We have submitted a Notice of Discovery of Hydrocarbons to the Agência Nacional do Petróleo, Gás Natural e Biocombustíveis (the “ANP”) with respect to the 182-C2 well. All operators in Brazil are required to inform the ANP, through the filing of a Notice of Discovery, of potential hydrocarbon discoveries. A Notice of Discovery is required to be filed with the ANP based on hydrocarbon indications in cuttings, mud logging or by gas detector, in combination with wire-line logging. Based on the results of open-hole logs, we have filed a Notice of Discovery relating to our 182-C2 well. These routine notifications to the ANP are not necessarily indicative of commercial hydrocarbons, potential production, recovery or reserves.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning potential hydrocarbon pay in the 183-C2 well, anticipated production commencement on our Murucututu project, exploration and development prospects of Alvopetro and the expected timing of certain of Alvopetro’s testing and operational activities. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning testing results of the 183-B1 well and the 182-C2 well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

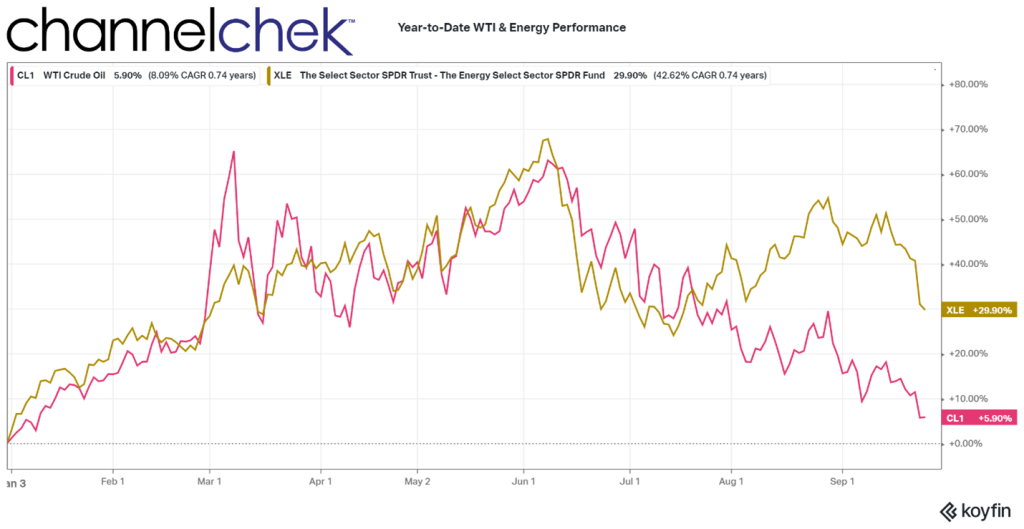

Energy stocks, as measured by the XLE Energy Index, were essentially flat during the third quarter rising 0.1%. The performance was impressive given overall market weakness. The S&P Composite Index declined 5.0% during the quarter. What makes the performance even more impressive is the fact that spot oil prices declined 25% during the quarter. We believe energy stocks remain an attractive investment and are an important part of a diversified investment portfolio.

WTI prices peaked at $120 per barrel in the first week of June. Since then, prices have declined in response to signs of a global economic slowdown. Near month oil future contracts are now below $80 per barrel. We believe recent weakness largely reflects demand concerns and foreign currency changes but is not a condition of oversupply. The domestic rig count remains at less than half peak levels. What’s more, rig count has leveled off in recent months in response to the decline in oil prices.

Production has risen to 90% of peak, but it has been done by harvesting the low-hanging fruit. When oil prices began falling early in 2020, there was an increase in Drilled Uncompleted (DUC) wells. When prices rose, drillers focused on completing DUCs. With the number of DUCs having fallen in half, future supply increases will be more difficult. If demand does not decrease in reaction to a slowing economy, domestic production may be hard pressed to meet demand. If worries about a recession are overblown and demand increases, there’s a good chance oil prices will be back at a price of $120 or even higher.

Energy industry fundamentals remain strong. The recent drop in oil prices does not concern us as long-term prices are still above the levels assumed in our financial and valuation models. Energy company cash flow generation is high, and companies are facing the envious position of trying to decide what to do with the cash. Debt levels have been pared down and managements are reluctant to initiate/raise dividends in case the industry goes into a down cycle forcing them to reverse course. Share repurchase remains a viable option especially if energy stocks continue to be weak alongside the overall market.

Energy Stocks

Energy stocks, as measured by the XLE Energy Index, were essentially flat during the third quarter rising 0.1%. The performance was impressive given overall market weakness. The S&P Composite Index declined 5.0% during the quarter. What makes the performance even more impressive is the fact that spot oil prices declined 25% during the quarter. We believe energy stocks remain an attractive investment and are an important part of a diversified investment portfolio.

Oil Prices

Oil prices rose steadily over a two-year period beginning the spring of 2020. WTI prices peaked at $120 per barrel in the first week of June. Since then, prices have declined in response to signs of a global economic slowdown as governments raise interest rates to fight inflation. Near month oil future contracts are now below $80 per barrel.

Figure #1

We believe recent weakness largely reflects demand concerns and foreign currency changes but is not a condition of oversupply. Historically, oil prices are lower when the dollar is stronger. This is because most oil suppliers, including international suppliers, demand payments in dollars.

The domestic rig count remains at less than half peak levels. According to Baker Hughes, there were 764 active rigs as of September 23, 2022, as compared to 1600 in 2015. What’s more, rig count has leveled off in recent months in response to the decline in oil prices.

Figure #2

Rig count is one way to forecast future supply. While only half the peak number of rigs are active, that does not mean that production is half of peak levels. In fact, as the chart below shows, domestic daily production surpassed 2015 peak rig production levels in 2018. Production declined sharply when oil prices fell in 2020 but have recovered to a point where production has reached 90% of peak production. The increased production demonstrates an improved productivity per well as drillers better tailor drilling techniques to individual formations.

Figure #3

But before we chalk up increased production to improved technology, let’s look at one more chart. The chart below shows the number of drilled but uncompleted (DUC) wells against active rigs. The chart shows that the number of uncompleted wells has declined sharply the last two years as the active rig count has grown. When oil prices began falling early in 2020, drillers continued drilling but often did not complete the wells. This led to a large increase in the number of DUC wells. When prices started rising in the summer of 2020, drilling returned. However, drilling was largely focused on completing or reworking wells.

Figure #4

The implication of a declining DUC count is that the industry is running out of low hanging fruit. Future drilling will need to focus on wells that are likely to have a lower production rate per rig than what we have witnessed recently. Declining production could exasperate already low inventory levels (see chart below). Thus, if demand does not decrease in reaction to a slowing economy, domestic production may be hard pressed to meet demand. If worries about a recession are overblown and demand increases, there’s a good chance oil prices will be back at a price of $120 or even higher.

Figure #5

Natural Gas Prices

Natural gas prices tend to track oil prices but with a few distinctions. Natural gas demand and supply is less global than oil. Imports (and now exports) of liquefied natural gas represent a small portion of domestic supply and demand. Secondly, natural gas is used primarily for space heating. That means demand is more seasonal. It also means demand can be affected by weather conditions. On the other hand, natural gas demand is less affected by general economic conditions than oil. As the chart below shows, natural gas prices do not seem to be affected by recession concerns as compared to oil prices.—-

Figure #6

Source: Natural Gas Intelligence

Summer is usually a quiet time for natural gas prices. Wells are producing more gas than is demanded, and gas is put in inventory. As is the case with oil, inventory levels are running below historical averages as we approach the point of withdrawing from inventory. This bodes well for natural gas prices remaining at current historical high levels and perhaps even rising higher.———- page break ———-

Figure #7

Outlook

Energy industry fundamentals remain strong. The recent drop in oil prices does not concern us as long-term prices are still above the levels assumed in our financial and valuation models. Energy company cash flow generation is high, and companies are facing the envious position of trying to decide what to do with the cash. Debt levels have been pared down and managements are reluctant to initiate/raise dividends in case the industry goes into a down cycle forcing them to reverse course. Share repurchase remains a viable option especially if energy stocks continue to be weak alongside the overall market.

We also believe the case for smaller cap energy stocks is strong. Major oil companies are facing increasing pressure to focus on renewable energy. While the majors are increasing drilling, they are doing so in a controlled manner as they also invest in green energy. Smaller cap energy companies are less tethered and often able to acquire and exploit properties being ignored by the majors. If our belief that a world-wide recession is already factored into energy prices is correct, small cap energy companies will be in the best position to take advantage of any price increase.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Russia’s Energy War: Putin’s Unpredictable Actions and Looming Sanctions Could Further Disrupt Oil and Gas Markets

Russia’s effort to conscript 300,000 reservists to counter Ukraine’s military advances in Kharkiv has drawn a lot of attention from military and political analysts. But there’s also a potential energy angle. Energy conflicts between Russia and Europe are escalating and likely could worsen as winter approaches.

One might assume that energy workers, who provide fuel and export revenue that Russia desperately needs, are too valuable to the war effort to be conscripted. So far, banking and information technology workers have received an official nod to stay in their jobs.

The situation for oil and gas workers is murkier, including swirling bits of Russian media disinformation about whether the sector will or won’t be targeted for mobilization. Either way, I expect Russia’s oil and gas operations to be destabilized by the next phase of the war.

The explosions in September 2022 that damaged the Nord Stream 1 and 2 gas pipelines from Russia to Europe, and that may have been sabotage, are just the latest developments in this complex and unstable arena. As an analyst of global energy policy, I expect that more energy cutoffs could be in the cards – either directly ordered by the Kremlin to escalate economic pressure on European governments or as a result of new sabotage, or even because shortages of specialized equipment and trained Russian manpower lead to accidents or stoppages.

Dwindling Natural Gas Flows

Russia has significantly reduced natural gas shipments to Europe in an effort to pressure European nations who are siding with Ukraine. In May 2022, the state-owned energy company Gazprom closed a key pipeline that runs through Belarus and Poland.

In June, the company reduced shipments to Germany via the Nord Stream 1 pipeline, which has a capacity of 170 million cubic meters per day, to only 40 million cubic meters per day. A few months later, Gazprom announced that Nord Stream 1 needed repairs and shut it down completely. Now U.S. and European leaders charge that Russia deliberately damaged the pipeline to further disrupt European energy supplies. The timing of the pipeline explosion coincided with the start up of a major new natural gas pipeline from Norway to Poland.

Russia has very limited alternative export infrastructure that can move Siberian natural gas to other customers, like China, so most of the gas it would normally be selling to Europe cannot be shifted to other markets. Natural gas wells in Siberia may need to be taken out of production, or shut in, in energy-speak, which could free up workers for conscription.

Restricting Russian Oil Profits

Russia’s call-up of reservists also includes workers from companies specifically focused on oil. This has led some seasoned analysts to question whether supply disruptions might spread to oil, either by accident or on purpose.

One potential trigger is the Dec. 5, 2022, deadline for the start of phase six of European Union energy sanctions against Russia. Confusion about the package of restrictions and how they will relate to a cap on what buyers will pay for Russian crude oil has muted market volatility so far. But when the measures go into effect, they could initiate a new spike in oil prices.

Under this sanctions package, Europe will completely stop buying seaborne Russian crude oil. This step isn’t as damaging as it sounds, since many buyers in Europe have already shifted to alternative oil sources.

Before Russia invaded Ukraine, it exported roughly 1.4 million barrels per day of crude oil to Europe by sea, divided between Black Sea and Baltic routes. In recent months, European purchases have fallen below 1 million barrels per day. But Russia has actually been able to increase total flows from Black Sea and Baltic ports by redirecting crude oil exports to China, India and Turkey.

Russia has limited access to tankers, insurance and other services associated with moving oil by ship. Until recently, it acquired such services mainly from Europe. The change means that customers like China, India and Turkey have to transfer some of their purchases of Russian oil at sea from Russian-owned or chartered ships to ships sailing under other nations’ flags, whose services might not be covered by the European bans. This process is common and not always illegal, but often is used to evade sanctions by obscuring where shipments from Russia are ending up.

To compensate for this costly process, Russia is discounting its exports by US$40 per barrel. Observers generally assume that whatever Russian crude oil European buyers relinquish this winter will gradually find alternative outlets.

Where is Russian Oil Going?

The U.S. and its European allies aim to discourage this increased outflow of Russian crude by further limiting Moscow’s access to maritime services, such as tanker chartering, insurance and pilots licensed and trained to handle oil tankers, for any crude oil exports to third parties outside of the G-7 who pay rates above the U.S.-EU price cap. In my view, it will be relatively easy to game this policy and obscure how much Russia’s customers are paying.

On Sept. 9, 2022, the U.S. Treasury Department’s Office of Foreign Assets Control issued new guidance for the Dec. 5 sanctions regime. The policy aims to limit the revenue Russia can earn from its oil while keeping it flowing. It requires that unless buyers of Russian oil can certify that oil cargoes were bought for reduced prices, they will be barred from obtaining European maritime services.

However, this new strategy seems to be failing even before it begins. Denmark is still making Danish pilots available to move tankers through its precarious straits, which are a vital conduit for shipments of Russian crude and refined products. Russia has also found oil tankers that aren’t subject to European oversight to move over a third of the volume that it needs transported, and it will likely obtain more.

Traders have been getting around these sorts of oil sanctions for decades. Tricks of the trade include blending banned oil into other kinds of oil, turning off ship transponders to avoid detection of ship-to-ship transfers, falsifying documentation and delivering oil into and then later out of major storage hubs in remote parts of the globe. This explains why markets have been sanguine about the looming European sanctions deadline.

One Fuel at a Time

But Russian President Vladimir Putin may have other ideas. Putin has already threatened a larger oil cutoff if the G-7 tries to impose its price cap, warning that Europe will be “as frozen as a wolf’s tail,” referencing a Russian fairy tale.

U.S. officials are counting on the idea that Russia won’t want to damage its oil fields by turning off the taps, which in some cases might create long-term field pressurization problems. In my view, this is poor logic for multiple reasons, including Putin’s proclivity to sacrifice Russia’s economic future for geopolitical goals.

Russia managed to easily throttle back oil production when the COVID-19 pandemic destroyed world oil demand temporarily in 2020, and cutoffs of Russian natural gas exports to Europe have already greatly compromised Gazprom’s commercial future. Such actions show that commercial considerations are not a high priority in the Kremlin’s calculus.

How much oil would come off the market if Putin escalates his energy war? It’s an open question. Global oil demand has fallen sharply in recent months amid high prices and recessionary pressures. The potential loss of 1 million barrels per day of Russian crude oil shipments to Europe is unlikely to jack the price of oil back up the way it did initially in February 2022, when demand was still robust.

Speculators are betting that Putin will want to keep oil flowing to everyone else. China’s Russian crude imports surged as high as 2 million barrels per day following the Ukraine invasion, and India and Turkey are buying significant quantities.

Refined products like diesel fuel are due for further EU sanctions in February 2023. Russia supplies close to 40% of Europe’s diesel fuel at present, so that remains a significant economic lever.

The EU appears to know it must kick dependence on Russian energy completely, but its protected, one-product-at-a-time approach keeps Putin potentially in the driver’s seat. In the U.S., local diesel fuel prices are highly influenced by competition for seaborne cargoes from European buyers. So U.S. East Coast importers could also be in for a bumpy winter.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Amy Myers Jaffe, Research professor, Fletcher School of Law and Diplomacy, Tufts University.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production surpassing expectations. InPlay announced production levels of 9,600 boe/d, a significant increase over 2022-2Q average of 9,063 BOE/d. Management now believes 2022 production will be at the upper half of a previously stated range of 9,150-9,400 BOE/d. so we are raising our production forecast to 9,400 BOE/d. In addition, two other wells will be brought to production in the next few days leading us to believe production will continue to grow into the fourth quarter.

Drilling success leads to more activity. The company is adding two Extended Reach Horizontal (ERH) wells in 2022. We suspect InPlay may be drilling ERH wells to forego building infrastructure. In addition to drilling longer well spurs, management announced that it is planning to move part of its 2023 drilling program into late 2022. InPlay is adding two horizontal wells in the Belly River where it has not drilled since 2016. Management believes utilizing the success it has found in the Cardium play (Pembina and Willesden Green) will translate into the Belly River.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, Alberta, Sept. 28, 2022 (GLOBE NEWSWIRE) — InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce an operations update and a long-term forecast through 2025.

Operations Update

InPlay is currently producing at record production levels of 9,600 boe/d(2) (57% light oil and NGLs) based on field estimates. In Willesden Green, three (2.9 net) Extended Reach Horizontal (“ERH”) wells were brought on production approximately ten days ago and an additional two (1.9 net) ERH wells will be brought on production in the next few days. These wells are currently in the early clean-up stage and should achieve peak production over the next 30 to 60 days. The Company’s current plans from our original capital program is to drill one (0.95 net) additional two-mile well in Willesden Green.

Given the strong operational results in 2022 to date, InPlay expects to be in the upper half of our full year 2022 production guidance which equates to 9,150 to 9,400 boe/d(2). This forecast is estimated to deliver production growth of 28% to 31% on a per share basis (83% to 92% on a debt adjusted per share basis (1)) which is expected to be top-tier amongst light oil peers.

InPlay has elected to drill additional extended reach wells in 2022 (and fewer one-mile wells) than originally planned, including two two-mile ERH wells which achieved exceptional efficient drill times. The Company is also expecting increased industry activity levels in the first quarter of 2023. With our strong balance sheet, InPlay plans to take advantage of utilizing our preferred contractors and is now tactically planning to start 2023 expenditures in late 2022 by initiating preliminary construction work and adding two horizontal (2.0 net) Belly River light oil wells to the 2022 capital program. These wells are expected to be brought on production late in the fourth quarter positioning the Company for significant production increases in 2023. The Belly River is a producing play which we have not drilled in since 2016 and plans are to utilize the technologies and expertise developed in our Cardium play over the years. These wells have a high light oil weighting (approximately 90% – 95% light oil) that receives a premium to our benchmark Mixed Sweet Blend (“MSW”) pricing. The Company also plans to invest in environmental initiatives by constructing a third vapour recovery unit for additional emission conservation. As a result, the Board of Directors have approved an increased 2022 development capital budget of $70 to $72 million.

Outlook and Long-Term Forecast (3)

InPlay is continuously evaluating market conditions including current recession concerns in order to maximize shareholder returns. Even with the current volatility, commodity prices continue to remain historically strong in part due to the weak Canadian dollar, resulting in high rates of return on capital investment and short payout periods. It is InPlay’s belief that long-term commodity pricing will remain strong due to the lack of industry wide capital spending over recent years, restrictive government regulations and mandates and unstable global geopolitics leading to a multi-year bull cycle in crude oil prices. The Company is continuing to rapidly pay down debt and is in the best operational and financial position in our history while remaining focused on our disciplined strategy.

InPlay is pleased to provide a forecast to the end of 2025. The Company’s strategy is to continue to provide top-tier light-oil weighted growth, maintaining a strong financial position while providing significant FAFF and sustainable returns to shareholders. Our strategy is to provide organic production growth in a range of 6% – 10%. At a WTI price of US $80/bbl or better, we target 10% production growth and with WTI pricing of approximately US $60/bbl, production growth of 6% is targeted. This is demonstrated in our forecast to 2025 which would provide a meaningful return to shareholders.

The table below outlines the highlights of the four year forecast based on the following WTI pricing scenarios:

2022

2023

2024

2025

WTI (US$/bbl)

93.25

75.00

70.00

65.00

Production (boe/d)(2)

9,150 – 9,400

9,900 – 10,400

10,650 – 11,200

11,300 – 11,900

Capital ($ millions)

70 – 72

69 – 71

75 – 77

80 – 82

Net wells

17.5

17.5 – 18.5

18.5 – 19.5

21.0 – 22.0

DAPPS Growth (%)(1) *

83 – 92

46 – 59

40 – 45

30 – 35

AFF ($ millions)(4)

139 – 143

134 – 140

136 – 142

133 – 139

FAFF ($ millions)(1)

67 – 73

63 – 71

59 – 67

51 – 59

Working Capital (Net Debt) at Year-end ($ millions)(4)

(12) – (16)

43 – 50

97 – 103

141 – 147

Annual Net Debt / EBITDA(1)

0.1 – 0.2

(0.3) – (0.4)

(0.7) – (0.8)

(1.0) – (1.1)

EV / DAAFF(1)*

1.5 – 1.6

1.2 – 1.3

0.8 – 0.9

0.5 – 0.6

* Assumes a $2.50 share price

This forecast shows the high quality deliverability and return of our assets evidencing the sustainability of the Company with increasing positive working capital and minimal leverage.

Return of Shareholder Capital

InPlay’s trailing 12 month net debt to earnings before interest, taxes and depletion (“EBITDA”) ratio was less than 0.5 times at the end of the second quarter and is forecast to be 0.1 – 0.2 times at the end of 2022. With this threshold achieved, in addition to the continued generation of FAFF, elimination of debt and generation of positive working capital forecasted through to 2025, the Company is committed towards providing a return of capital to shareholders. The Company believes that our share price is currently significantly undervalued and the prudent first step in enhancing returns to shareholders is a share buyback program which the Company’s Board of Director’s has approved for implementation and will be subject to regulatory approval. With this in place the Company will be able to acquire common shares at opportunistic times and share prices.

As outlined above in the long term forecast, the Company is forecasting to generate material FAFF resulting in a growing positive working capital balance through to 2025. Our strategy for the accumulating additional FAFF is to provide returns to shareholders through potential share buybacks, dividends, increased tactical capital investment and accretive strategic acquisitions.

Given the significant volatility in both commodity prices and market conditions experienced in recent weeks, the Company and its Board of Directors will continue to monitor and evaluate the timing and implementation of additional returns to shareholders.

The Company has been disciplined in maintaining operational flexibility by quickly adapting to changing market conditions and commodity price fluctuations in making business decisions. This same prudent approach is currently being followed. Management would like to thank our employees, board members, lenders and shareholders for their support and we look forward to continuing our journey of deleveraging and delivering strong returns to shareholders in a sustainable, prudent and responsible manner.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release.

See “Production Breakdown by Product Type” at the end of this press release.

See “Reader Advisories – Forward Looking Information and Statements” for full details and key budget and underlying assumptions related to our 2022 capital program and associated guidance and long-term forecast.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

Reader Advisories

Non-GAAP and Other Financial Measures

Throughout this press release and other materials disclosed by the Company, InPlay uses certain measures to analyze financial performance, financial position and cash flow. These non-GAAP and other financial measures do not have any standardized meaning prescribed under GAAP and therefore may not be comparable to similar measures presented by other entities. The non-GAAP and other financial measures should not be considered alternatives to, or more meaningful than, financial measures that are determined in accordance with GAAP as indicators of the Company performance. Management believes that the presentation of these non-GAAP and other financial measures provides useful information to shareholders and investors in understanding and evaluating the Company’s ongoing operating performance, and the measures provide increased transparency and the ability to better analyze InPlay’s business performance against prior periods on a comparable basis.

Non-GAAP Financial Measures and Ratios

Included in this document are references to the terms “free adjusted funds flow (“FAFF”)”, “Net Debt to EBITDA”, “Production per debt adjusted share (“DAPPS”)” and “EV / DAAFF”. Management believes these measures and ratios are helpful supplementary measures of financial and operating performance and provide users with similar, but potentially not comparable, information that is commonly used by other oil and natural gas companies. These terms do not have any standardized meaning prescribed by GAAP and should not be considered an alternative to, or more meaningful than “profit (loss) before taxes”, “profit (loss) and comprehensive income (loss)”, “adjusted funds flow”, “capital expenditures”, “corporate acquisitions, net of cash acquired”, “working capital (net debt)”, “weighted average number of common shares (basic)” or assets and liabilities as determined in accordance with GAAP as a measure of the Company’s performance and financial position.

Free Adjusted Funds Flow (“FAFF”)

Management considers FAFF per share important measures to identify the Company’s ability to improve its financial condition through debt repayment, which has become more important recently with the introduction of second lien lenders, on an absolute and weighted average per share basis. FAFF should not be considered as an alternative to or more meaningful than AFF as determined in accordance with GAAP as an indicator of the Company’s performance. FAFF is calculated by the Company as AFF less exploration and development capital expenditures and property dispositions (acquisitions) and is a measure of the cashflow remaining after capital expenditures before corporate acquisitions that can be used for additional capital activity, corporate acquisitions, and repayment of debt or decommissioning expenditures or potentially return of capital to shareholders. FAFF per share is calculated by the Company as FAFF divided by weighted average outstanding shares. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast FAFF.

Net Debt to EBITDA

Management considers Net Debt to EBITDA an important measure as it is a key metric to identify the Company’s ability to fund financing expenses, net debt reductions and other obligations. EBITDA is calculated by the Company as adjusted funds flow before interest expense. When this measure is presented quarterly, EBITDA is annualized by multiplying by four. When this measure is presented on a trailing twelve month basis, EBITDA for the twelve months preceding the Net Debt date is used in the calculation. This measure is consistent with the EBITDA formula prescribed under the Company’s Senior Credit Facility. Net Debt to EBITDA is calculated as Net Debt divided by EBITDA. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast Net Debt to EBITDA.

Production per Debt Adjusted Share

InPlay uses “Production per debt adjusted share” as a key performance indicator. Debt adjusted shares should not be considered as an alternative to or more meaningful than common shares as determined in accordance with GAAP as an indicator of the Company’s performance. Debt adjusted shares is a non-GAAP measure used in the calculation of Production per debt adjusted share and is calculated by the Company as common shares outstanding plus the change in working capital (net debt) divided by the Company’s current trading price on the TSX, converting working capital (net debt) to equity. Debt adjusted shares should not be considered as an alternative to or more meaningful than weighted average number of common shares (basic) as determined in accordance with GAAP as an indicator of the Company’s performance. Management considers Debt adjusted share is a key performance indicator as it adjusts for the effects of capital structure in relation to the Company’s peers. Production per debt adjusted share is calculated by the Company as production divided by debt adjusted shares. Management considers Production per debt adjusted share is a key performance indicator as it adjusts for the effects of changes in annual production in relation to the Company’s capital structure. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast production per debt adjusted share.

EV / DAAFF

InPlay uses “enterprise value to debt adjusted AFF” or “EV/DAAFF” as a key performance indicator. EV/DAAFF is calculated by the Company as enterprise value divided by debt adjusted AFF for the relevant period. Debt adjusted AFF (“DAAFF”) is calculated by the Company as adjusted funds flow plus financing costs. Enterprise value is a capital management measures that is used in the calculation of EV/DAAFF. Enterprise value is calculated as the Company’s market capitalization plus working capital (net debt). Management considers enterprise value a key performance indicator as it identifies the total capital structure of the Company. Management considers EV/DAAFF a key performance indicator as it is a key metric used to evaluate the sustainability of the Company relative to other companies while incorporating the impact of differing capital structures. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast EV/DAAFF.

Capital Management Measures

Adjusted Funds Flow