Enbridge Inc.’s agreement to acquire three natural gas utilities from Dominion Energy for $14 billion presents opportunities for smaller companies in the sector.

The Canadian pipeline giant will dramatically expand its regulated gas distribution business in the U.S. through the purchase of Questar Gas, East Ohio Gas and Public Service Company of North Carolina.

But the deal also creates an opening for nimble smaller utilities to grow amidst consolidation. Regulators may require certain assets to be divested as conditions for merger approval.

Smaller players could potentially gain customers, infrastructure and new geographies by acquiring these divested assets. Companies in the energy sector may be well positioned.

The agreement comes as Dominion reviews its business mix. Other major utilities are also rationalizing assets, setting the stage for smaller competitors.

Small operators boast strong community ties and localized expertise. They have advantages in customer service and responsiveness.

While lacking scale, these firms can thrive by focusing resources on targeted markets and infrastructure modernization. Many also offer renewable natural gas and other next-gen offerings.

Pennsylvania instrumentation company AMETEK (NYSE: AME) is expanding its testing and measurement capabilities with the acquisition of United Electronic Industries.

Massachusetts-based UEI is a leader in data acquisition and control solutions for aerospace, defense, energy and semiconductor sectors. Its products enable customers to build robust systems for simulation, monitoring and automated testing.

AMETEK CEO David Zapico expressed excitement about bringing UEI’s innovative solutions into the company’s Power Systems and Instruments division. He said the $35 million deal broadens AMETEK’s presence in attractive markets that complement existing strengths.

UEI will join AMETEK’s Electronic Instruments Group, known for analytical, calibration and display instruments. The acquisition aligns with AMETEK’s growth strategy of targeting niche segments and making strategic buys.

Headquartered near Philadelphia, AMETEK has annual sales over $6 billion globally. The 90-year-old firm focuses on cash flow and capital deployment to drive double-digit earnings growth.

Take a moment to learn about Kratos Defense & Security Solutions, a company that specializes in satellite communications, missile defense, and hypersonic systems.

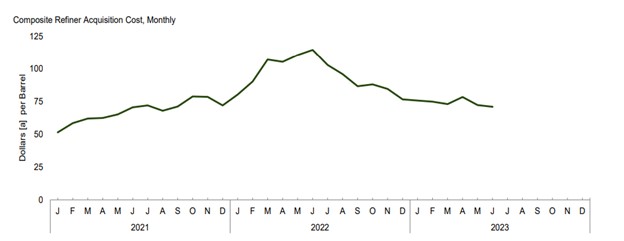

Oil prices are near flat on the month but have recently been rising. Meanwhile, the energy sector itself, relative to the overall market, is outperforming in a way that is getting attention as we move to September. Are the drivers of performance solidly in place to keep crude oil prices strong? Will the energy sector continue to benefit from factors impacting oil? We lay out factors impacting future price movements below.

Credit for the recent strength in oil has been given in part to the Saudi Arabian production cuts that began in July when the Saudi’s voluntarily lowered production by one million barrels a day starting in July. This quickly strengthened prices, which then fell off as concerns over China’s weakening economy, and global economies in general, grew. China is the world’s second-largest consumer of crude oil.

The U.S. has seen strong economic reports recently. The market is still reacting poorly to “good” news. This reaction also played into the direction of stocks and commodity prices. U.S. economic activity readings raised expectations for further monetary policy tightening by the Federal Reserve. The idea of heightened activity lifted U.S. Treasury yields and, along with them, the U.S. dollar. During the last week in August, weaker U.S. labor data served to ease some of the rise in yields.

Adding to the strength, this week, the Energy Information Administration (EIA) on Wednesday reported that U.S. commercial crude inventories fell by 10.6 million barrels for the week ending Aug. 25. That was the third straight weekly decline reported by the agency and the largest since the week ended July 28. U.S. commercial crude inventories have fallen by almost 34 million barrels over the past five weeks.

Inventories are now only 1.1% higher than the same week last year, even with over 100 million barrels having been released from the U.S. Strategic Petroleum Reserve during the 12 months.

A reversal to the upside after crude fell last week below support at $78 a barrel also coincided with the formation of what technicians refer to as a golden cross, this is when the 50-day moving average crosses above the 200-day moving average from below. This got the attention of commodity traders.

Source: EIA

Overall, the price paid per barrel of oil has been range-bound through 2023. The extended production cuts by Saudi Arabia and Russia were largely offset by fears about China’s economy flailing; it had been expected it would rebound strongly after pandemic lockdowns were lifted. Oil consumption did not rise as expected.

Source: EIA

There is also increasing indications the United States is relaxing sanctions on crude exports from Iran and Venezuela to keep prices from rising too much and in exchange for diplomatic objectives. The U.S. is the number one oil consumer.

Given still low inventories and a need to replenish the U.S. Strategic Oil Reserves there are market participants that remain bullish on oil prices and the energy sector. There are others that are more cautious, despite Saudi production cuts, as the chart above indicates, consumption recently fell below the level of production.

Take Away

Oil prices have been in a tight range all year. Better stock market performance from energy producers has in part been because of easing of rules concerning fossil fuels, and headway made on green energy projects. Consumption will increase and fall based on economic activity. Where the U.S. economy and global economy are headed is faced with more cross-currents than usual. Added supply to the U.S. may come from countries we don’t currently trade with. Those spigots can not be turned on quickly. This leaves oil and energy with a current trend upward but challenges down the road.

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURE™ and VPURE+™ products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Largo announced that its Board has initiated a review and evaluation of strategic alternatives for Largo Clean Energy. LCE represents Largo’s interest in energy storage investments including the Vanadium Redox Flow Battery (VRFB). VRFBs have the potential to store energy at the utility grid level for longer periods that lithium batteries. LCE was formed in 2020 with the acquisition of assets and patents owned by VionX Energy for $3.862 million. The division has completed a 3 MWH test project in Massachusetts and is near completion of a 6.1 MWH battery for Enel Green Power in Spain. Strategic alternatives for LCE could include the sale, merger, or other financial arrangements with other parties interested in vanadium batteries.

Would Largo consider selling LCE outright? Largo has a unique corporate structure that includes mining (Largo Production), LCE, and its investment in publicly-traded vanadium units (Large Physical Vanadium). Through its involvement in all three units, it hopes to promote the development of VRFBs. Increased adoption of VRFBs would greatly enhance the demand for vanadium. We believe Largo remains committed to promoting VRFBs but would be willing to sell LCE, or a partial interest in LCE, if it were to find a partner sharing an equal commitment.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

TORONTO–(BUSINESS WIRE)– Largo Inc. (“Largo” or the “Company”) (TSX: LGO) (NASDAQ: LGO) today announces that its Board of Directors (the “Board”) has initiated a review and evaluation of strategic alternatives with the intent to unlock and fully maximize the value of Largo Clean Energy Corp. (“LCE”).

The comprehensive review and evaluation process will include consideration of a full range of strategic, business, and financial alternatives, including, but not limited to, evaluating and completing financing transactions at the LCE subsidiary level, mergers and acquisitions of LCE with other battery companies and partnership opportunities with well-established energy system producers who are interested in entering the vanadium battery sector with the unique elements that Largo offers to this industry.

Daniel Tellechea, Interim CEO and Director of Largo commented: “Largo is commencing a comprehensive and thorough review of strategic alternatives to accelerate and enhance the distinctive value proposition LCE presents for vanadium batteries and the long duration energy storage sector. We believe several strategic opportunities exist in the market today that would benefit from LCE’s unique characteristics, and a formal process for comparing these alternatives is expected to deliver maximum value for all shareholders in a timely manner. These characteristics include: i) LCE’s access to the innovative Largo Physical Vanadium Corp. (“LPV”) (TSXV:VAND, OTCQX:VANAF) structure, which is expected to significantly reduce vanadium battery costs for customers, ii) LCE’s U.S.-based manufacturing capabilities, which may be eligible for significant fiscal incentives, grants and benefits, and iii) LCE’s patented vanadium flow battery stack technology and electrolyte purification technology.”

He continued: “We believe the strategic review process announced today could also accelerate the prospects for deployment of vanadium units owned by LPV in batteries, which we consider provides a major improvement in the cost-competitiveness of LCE against other battery technologies and other vanadium flow battery competitors. With the start of this process underway, the Company also remains committed to delivering on its set targets for the year in a safe and responsible manner.”

There can be no assurance that this process will result in any specific strategic plan or financial transaction and the Company does not plan to provide updates on the status of the review unless there are material developments to report.

Gallatin Capital LLC (“Gallatin”) is advising on securities transactions and Castle Grove Capital, LLC (“Castle Grove Capital”) is providing consulting services in support of the strategic review and evaluation process. Inquiries regarding the process may be directed to Myron Manternach, a registered representative of Gallatin and the President of Castle Grove Capital.

About Largo

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURE™ and VPURE+™ products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing an ilmenite concentrate plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business to support a low carbon future.

Largo’s common shares trade on the Nasdaq Stock Market and on the Toronto Stock Exchange under the symbol “LGO”. For more information on the Company, please visit www.largoinc.com.

Cautionary Statement on Forward-looking Information:

This press release contains forward-looking information under applicable securities legislation, (“forward-looking information”). Forward‐looking information in this press release includes, but is not limited to, statements with respect to LCE’s strategic review, the expectation that the strategic review will deliver maximum value for all shareholders, the timeliness of the strategic review, access to LPV’s structure, the ability to reduce vanadium battery costs for customers, eligibility for fiscal incentives, grants and benefits, the deployment of vanadium units and other benefits that may arise from the strategic review and/or LPV. Forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. All information contained in this news release, other than statements of current and historical fact, is forward looking information.

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking information, including but not limited to those risks described in the annual information form of Largo and in its public documents filed on www.sedarplus.caand www.sec.govfrom time to time. Such risks and uncertainties include, without limitation: the ability to obtain, in a timely manner, all necessary regulatory, stock exchange, shareholder and other third-party approvals to consummate any transactions contemplated by the strategic review; the risk of any disruptions to the Company’s business and operations; competition; conflict in eastern Europe; changes in interest rates, inflation, foreign exchange rates, and the other risks involved in the mining and long-term battery storage industries and capital markets. Forward-looking information are based on the opinions and estimates of management as of the date such statements are made. Although management of Largo has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on Forward-looking information. Largo does not undertake to update any forward-looking information, except in accordance with applicable securities laws. Readers should also review the risks and uncertainties sections of Largo’s annual and interim MD&A which also apply.

Trademarks are owned by Largo Inc.

For further information, please contact:

Investor Relations Alex Guthrie Senior Manager, External Relations +1.416.861.9778 aguthrie@largoinc.com

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production was a bit light, but new wells are coming. Production was flat in the June quarter versus last year and down 9% versus the previous quarter. Results were modestly below our expectations. Management indicated that it pushed drilling (and thus well completion) into the third quarter. Hemisphere remains on track to drill ten wells this year. The company reports that production is back up over 3,000 boe/d in August and appears heading towards a good jump in production in the December quarter when wells are completed.

Lower-than-expected production had an adverse affect on bottom-line financial results. With lower-than-expected production’ revenues, operating income, adjusted fund flow, and net income were all a few C$ million lower than projected in our models. Realized prices were in line with expectations as were operating costs and netbacks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Permex reported a loss of $0.74 per share as drilling delays put the company behind our original production schedule. Permex reported $157,019 in revenues for the fiscal third quarter ended June 30, 2023, a 43% decline from third quarter revenues last year. Permex receives sales from ownership interest in 78 wells in the Permian Basin as well as royalty interests in 73 wells. It completed its first well in the Breedlove Field (a transformative acquisition) in January and is working to turn the well into a horizontal well. We had hoped the well would be producing and Permex would have started on a second well by now.

The extension and repricing of a warrant program and subsequent exercises resulted in 273,410 addition shares and generated $688,092 in net proceeds. The number of fully diluted shares including warrants is now more than 3 million versus basic shares of less than 2 million. The proceeds, along with a $847,000 positive change in working capital, helped offset a $865,000 net loss in operating cash. Permex’s cash position at the end of the quarter was $764,386, not enough to drill a well. The balance sheet remains debt free. Management shelved plans for an equity offering and uplisting. Liquidity remains an issue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A combination of negative events led to a 7.6% year over year and 6.1% quarter over quarter decline in production. Management estimates that the events reduced production by 1,350 boe/day. The decline was larger than expected and led to management taking down 2023 production guidance to 9,100-9,500 boe/day from 9,500-10,000 boe/day. The production decline is unfortunate but should be viewed as temporary.

New wells coming on should boost production. Six wells have recently, or are about to, come on line. Initial well production is impressive. In addition, six new wells are planned for the rest of 2023. Management believes processing constraints should ease in the third quarter. Higher production, combined with easing processing constraints should help boost cash flow and earnings.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURE™ and VPURE+™ products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Quarterly results were below expectations as a decline in vanadium prices and lower sales led to decreased revenues. The company is working hard to return mining activity to normal levels while at the same time reducing costs. Largo had been making strides toward achieving both goals, even if the financial numbers do not demonstrate the improvement due to the decline in vanadium prices. Largo sold less than it produced reversing a trend in the first quarter, as expected.

Vanadium prices declined 19% to $8.46/lb. Largo received a premium to benchmark prices during the quarter that it did not receive in the first quarter. We believe improving premiums reflect additional drilling in the first half of the year that allowed the company to blend vanadium concentrations and achieve a higher-premium product. Vanadium prices continued to sink during the quarter and were $7.98/lb. on June 30, 2023. Management indicates that vanadium prices have stabilized since the end of June and showed some signs of improving.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Alvopetro reported financial results for the quarter ended June 30, 2023 that were above our expectations. Results reflect a decline in production volume which had been preannounced through monthly production releases and thus expected. Realized gas prices were above expectations. Favorable results also reflect a decline in royalty rates. Royalty rates for natural gas production are based on Henry Hub natural gas prices, not realized gas sales prices. Henry Hub prices have been weak relative to realized gas prices resulting in a lower rate per boe produced.

Alvopetro is taking steps to replace production. The decline in production began in April and reflect higher nominations claimed by Alvopetro’s partner in the Cabure Field. Higher partner nominations will mean Alvopetro will own more of future production when prices are expected to be higher. Meanwhile, Alvopetro has accelerated drilling in fields in which it has a 100% ownership. We believe production from these wells will replace the production decline and even has the potential to double production levels in the next four years using internally generated cash.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

All dollar amounts expressed are in thousands of U.S. dollars unless otherwise indicated.

Q2 2023 and Other Highlights

Revenues of $53.1 million vs. revenues of $84.8 million Q2 2022; Revenues per pound of V2O5 sold1 of $9.42 vs. $11.69 per pound sold in Q2 2022, mainly driven by a sharp decrease in V2O5 prices during the quarter, which was partially offset by an increase in the Company’s high purity vanadium sales

Operating costs of $43.0 million vs. $50.7 million in Q2 2022; Cash operating costs excluding royalties per pound1 of V2O5 equivalent sold of $5.18 vs. $4.23 in Q2 2022

Net loss of $6.0 million vs. net income of $18.0 million in Q2 2022; Basic loss per share of $0.09

Cash provided before working capital items of $3.8 million vs. $25.4 million in Q2 2022; Cash provided by operating activities of $18.1 million vs. $2.9 million in Q2 2022

Cash balance of $64.0 million, net working capital2 surplus of $103.1 million and debt of $65.0 million exiting Q2 2023

V2O5 production 2,639 tonnes (5.8 million lbs3) vs. 3,084 tonnes in Q2 2022 and 2,111 tonnes in Q1 2023; V2O5 equivalent sales of 2,557 tonnes vs. 3,291 tonnes in Q2 2022

Commissioning of the Company’s ilmenite concentration plant has commenced and is expected to be completed in Q3 2023, at which point a gradual ramp-up of ilmenite production in Q4 2023; Ilmenite concentrate will become a by-product of the Company’s vanadium operations in Brazil

Hot commissioning of Largo Clean Energy’s (“LCE”) 6.1 megawatt-hour (“MWh”) Enel Green Power España (“EGPE”) vanadium redox flow battery (“VRFB”) deployment remains ongoing, with provisional acceptance by EGPE expected in Q3 2023

The Company published its 2022 Sustainability Reportentitled: “Building a low-carbon future together” highlighting the development and improvement of its ongoing sustainability programs

Q2 2023 results conference call: Thursday, August 10th at 1:00 p.m. ET

Vanadium Market Update4

The average benchmark price per lb of V2O5 in Europe was $8.46 in Q2 2023, a 19% decrease from the average of $10.39 seen in Q1 2023 and a 24% decrease from the average of $11.08 seen in Q2 2022; The average benchmark price per kg of ferrovanadium in Europe was $33.47 in Q2 2023, a 15% decrease from the average of $39.46 seen in Q1 2023 and a 24% decrease from the average of $43.83 seen in Q2 2022

Lower vanadium prices can be attributed to weaker demand in the Chinese construction market; however, these prices been partially offset by higher VRFB deployments in China and increased aerospace demand

The average European benchmark V2O5 price at June 30, 2023 was approximately $7.98 per lb, compared with approximately $10.13 per lb at March 31, 2023 and $9.15 per lb at June 30, 2022

According to Vanitec, demand in energy storage applications has increased by 141% from Q1 2022 to Q1 2023

TORONTO–(BUSINESS WIRE)– Largo Inc. (“Largo” or the “Company“) (TSX: LGO) (NASDAQ: LGO) today released financial and operating results for the three and six months ended June 30, 2023. The Company reported revenues of $53.1 million from vanadium pentoxide (“V2O5”) equivalent sales of 2,557 tonnes.

Daniel Tellechea, Interim CEO and Director of Largo, stated: “A sharp decrease in V2O5 prices combined with lower sales in Q2 2023 impacted the Company’s financial performance for the quarter. Higher production at the end of the second quarter is positively impacting in-transit inventory and should support higher availability and sales in the coming months. Our primary focus continues to be on delivering production and sales targets safely, optimizing our mine plan, as well as implementing additional cost reduction measures at both the mine site and at LCE to support profit margins going forward. The Company is beginning to see a reduction in key consumable costs at its mine site and has implemented a cost reduction plan at LCE.”

He continued: “Chinese and European steel sector spot demand for vanadium was weaker in Q2 2023, however, strong demand from the aerospace industry offset this during the quarter. Importantly, recent estimates indicate that energy storage demand is expected to increase significantly in the future, driven primarily by new VRFB deployments to 2030, with a CAGR of 14%8.”

Financial Results

(thousands of U.S. dollars, except for basic earnings (loss) per share and diluted earnings (loss) per share)

Three months ended

Six months ended

June 30, 2023

June 30, 2022

June 30, 2023

June 30, 2022

Revenues

53,110

84,804

110,531

127,492

Operating costs

(43,029)

(50,704)

(88,960)

(79,662)

Direct mine and production costs

(24,976)

(23,905)

(53,395)

(41,465)

Net income (loss) before tax

(4,647)

22,409

(3,932)

23,223

Income tax recovery (expense)

295

(7,115)

(38)

(7,717)

Deferred income tax (expense) recovery

(1,614)

2,671

(3,203)

505

Net income (loss)

(5,966)

17,965

(7,173)

16,011

Basic earnings (loss) per share

(0.09)

0.28

(0.11)

0.25

Diluted earnings (loss) per share

(0.09)

0.28

(0.11)

0.25

Cash provided before non-cash working capital items

3,841

25,400

11,991

31,151

Net cash provided by (used in) operating activities

18,057

2,902

23,010

(1,148)

Net cash (used in) provided by financing activities

(1,756)

(15,679)

23,549

(15,294)

Net cash used in investing activities

(14,283)

(11,383)

(37,689)

(15,651)

Net change in cash

2,405

(25,516)

9,509

(30,912)

As at

June 30, 2023

December 31, 2022

Cash

63,980

54,471

Debt

65,000

40,000

Working capital2

103,147

115,171

Maracás Menchen Mine Operational and Sales Results

Q2 2023

Q2 2022

Total Ore Mined (tonnes)

489,892

378,273

Ore Grade Mined – Effective Grade5 (%)

0.86

1.18

Total Mined – Dry Basis (tonnes)

3,671,842

2,503,696

Concentrate Produced (tonnes)

99,083

124,317

Grade of Concentrate (%)

3.34

3.28

Global Recovery6 (%)

81.0

81.8

V2O5 Produced (Flake + Powder) (tonnes)

2,639

3,084

High purity V2O5 equivalent produced (tonnes)

983

587

V2O5 produced (equivalent pounds3 )

5,817,992

6,799,048

V2O5 Equivalent Sold (tonnes)

2,557

3,291

Produced V2O5 equivalent sold (tonnes)

2,268

2,783

Purchased V2O5 equivalent sold (tonnes)

289

508

Cash Operating Costs Excluding Royalties per pound ($/lb)1

5.18

4.23

Revenues per pound sold ($/lb)1

9.42

11.69

Q2 2023 Financial Highlights

The Company recognized revenues of $53.1 million from sales of 2,557 tonnes of V2O5 equivalent (Q2 2022 – 2,849 tonnes) in Q2 2023. This represents a 37% decrease in revenues over Q2 2022 ($84.8 million) mainly due to lower sales and vanadium prices for the quarter. Reconciliation of the Company’s revenues per pound sold1 and total quantities sold of each product are provided in the “Non-GAAP7 Measures” section of this press release.

Operating costs of $43.0 million (Q2 2022 – $50.7 million) include direct mine and production costs of $25.0 million (Q2 2022 – $23.9 million), conversion costs of $2.2 million (Q2 2022 – $2.3 million), product acquisition costs of $3.8 million (Q2 2022 – $9.6 million), royalties of $2.5 million (Q2 2022 – $3.7 million), distribution costs of $2.5 million (Q2 2022 – $2.9 million), inventory write-down of $0.7 million (Q2 2022 – $2.3 million), depreciation and amortization of $6.2 million (Q2 2022 – $5.5 million) and iron ore costs of $0.2 million (Q2 2022 – $0.2 million). The increase in direct mine and production costs is attributable to an increase in total ore mined and the move to a new mining contractor in Q3 2022. Higher mining costs, the change in production levels across the period and the ramp up following the challenges experienced in the prior quarter negatively impacted costs. In addition, as compared with Q2 2022, the Company continued to experience elevated costs in critical consumables. The Company is actively working to manage its usage of these consumables and is also starting to see a softening in consumable prices.

Cash operating costs excluding royalties1 per pound sold were $5.18 per lb, compared with $4.23 for Q2 2022. The increase seen in Q2 2023 compared with Q2 2022 is largely due to the reasons noted above.

Professional, consulting and management fees of $5.8 million decreased from Q2 2022 by 9%. The decrease was mainly due to lower expenses incurred in the mine properties segment in Q2 2023 over Q2 2022, which is primarily attributable to additional compensation costs incurred in Q2 2022.

Other general and administrative expenses of $3.3 million decreased from Q2 2022 by 35% (or $1.8 million), which is primarily attributable to the increase in legal provisions recognized in Q2 2022 in the mine properties segment.

Finance costs of $2.0 million in Q2 2023 increased by $1.7 million from Q2 2022, which is primarily attributable to interest on the increased debt level in Q2 2023 as compared with Q2 2022, as well as a write-down of vanadium assets of $0.2 million.

Exploration and evaluation costs of $1.3 million in Q2 2023 increased by $1.1 million from Q2 2022. This was driven by infill drilling and geological model work at the Maracás Menchen Mine and diamond drilling at Campo Alegre de Lourdes.

Following the completion of its short-term infill drilling program in the Campbell Pit, the resulting geological model update and the decision to prioritize operating flexibility in the near-term mine planning, the Company has decided to accelerate its pre-stripping mining rates. Accordingly, it has revised its guidance for capitalized waste stripping costs for 2023. Expenditures of $11.7 million were capitalized during the six months ended June 30, 2023, and the Company now plans to incur approximately $15.0 million in the remainder of 2023. The Company believes that increased operating flexibility at its open pit mine will, amongst other things, assist in preventing weather related disruptions at the mine.

Cash provided by operating activities continues to be impacted by expenditures at LCE, with a net loss of $5.3 million recognized in Q2 2023 (Q2 2022 – $5.4 million).

Additional Corporate Updates

Production: V2O5 production in April, May and June 2023 was 676 tonnes, 945 tonnes and 1,018 tonnes, respectively, for a total of 2,639 tonnes of V2O5 produced in Q2 2023.

The Company completed its 2023 infill drilling campaign, which resulted in a further refinement of the Company’s short-term mining model. The Company achieved a normalized production level in June following the completion of upgrades to the crushing circuit and an improvement in mining performance as compared with Q1 2023. These upgrades are expected to reduce operational maintenance costs and provide more flexibility in the blending of ores to stabilize V2O5 production.

In Q2 2023, the Company produced 983 V2O5 equivalent tonnes of high purity products, including 706 tonnes of high purity V2O5 and 277 tonnes of high purity vanadium trioxide (“V2O3“). This represented 37% of the Company’s total quarterly production.

The global recovery6 achieved in Q2 2023 was 81.0%, a decrease of 1.0% from the 81.8% achieved in Q2 2022 and 2.4% lower than the 83.0% achieved in Q1 2023. The global recovery6 in April, May and June 2023 was 81.3%, 80.4%, 81.3%, respectively.

The total material moved in the mine in June was a record 1,349,405 tonnes of waste and 108,104 tonnes of ore (dry basis). In Q2 2023, 489,892 tonnes of ore were mined with an effective grade5 of 0.86% of V2O5. The ore mined in Q2 2023 was 30% higher than in Q2 2022. The Company produced 99,083 tonnes of concentrate with an effective grade5 of 3.34%.

Subsequent to Q2 2023, production in July 2023 was 644 tonnes of V2O5 equivalent as a result of process restrictions following the accident in July at its chemical plant. However, the Company accumulated intermediate stocks of vanadium material that is expected to be processed in August, offsetting a portion of weaker July V2O5 output.

Sales: In Q2 2023, the Company sold 2,557 tonnes of V2O5 equivalent (Q2 2022 – 3,291 tonnes), including 289 tonnes of purchased products (Q2 2022 – 508 tonnes). Produced V2O5 equivalent sold decreased, with 2,268 tonnes sold in Q2 2023, as compared with 2,783 tonnes in Q2 2022. The Company delivered both standard grade and high purity V2O5, as well as vanadium trioxide (“V2O3”) and ferrovanadium (“FeV”) to customers globally. Subsequent to Q2 2023, sales in July 2023 were 860 tonnes of V2O5 equivalent.

Largo Clean Energy: During Q2 2023, LCE continued to make progress on the delivery of the EGPE contract, which remains a priority focus. LCE finalized the pumping of electrolyte for EGPE’s VCHARGE VRFB deployment and completed cold commissioning of the system in June. The battery system was also successfully interconnected with the grid and the system inverter was successfully utilized to form the chemistry. The battery is currently performing charge-discharge cycles as part of the ongoing hot commissioning phase, which is anticipated to be completed in Q3 2023, along with provisional acceptance of the system by EGPE.

During Q2 2023, Mr. Francesco D’Alessio was appointed as President of LCE. The Company continues to evaluate all strategic options for LCE in order to fully maximize its unique value proposition in the energy storage sector. This includes but is not limited to the potential strengthening and formalization of existing industry and commercial relationships, developing additional collaborative partnerships, evaluating alternative deployment strategies, and performing a comprehensive review of cost reduction measures.

In accordance with this strategic evaluation, LCE has implemented a cost reduction plan and expects to realize savings of approximately 50% in its expenditures at LCE going forward.

Ilmenite Plant: Construction of the ilmenite concentration plant was completed in Q2 2023. Commissioning of this new facility has commenced and is expected to be completed in Q3 2023. A gradual ramp-up of ilmenite concentrate production will occur in Q4 2023.

Exploration: During Q2 2023, the Company completed approximately 5,000 metres of reverse circulation (“RC”) infill drilling in the Campbell Pit and 3,500 metres of diamond drilling in the near mine deep drilling program. The Campbell Pit geological model was updated in Q2 2023 and delivered to the mine planning team. This model will continue to be updated quarterly and will assist with mine planning activities going forward.

Largo Physical Vanadium Corp. (“LPV”): LPV continued its acquisition of vanadium assets, with $1.5 million spent during Q2 2023. LPV has deployed over 90% of its capital and is focussed on marketing and strategic initiatives to establish its business model.

Q2 2023 Webcast and Conference Call Information

The Company will host a webcast and conference call on Thursday, August 10th at 1:00 p.m. ET, to discuss its second quarter 2023 results and progress.

Webcast and Conference Call Details:

Details of the webcast and conference call are listed below:

To view press releases or any additional financial information, please visit the Investor Resources section of the Company’s website at: www.largoinc.com/English/investor-resources

A playback recording will be available on the Company’s website for a period of 60-days following the conference call.

The information provided within this release should be read in conjunction with Largo’s unaudited condensed interim consolidated financial statements for the three and six months ended June 30, 2023 and 2022, and its management’s discussion and analysis for the three and six months ended June 30, 2023, which are available on our website at www.largoinc.com or on the Company’s respective profiles at www.sedar.com and www.sec.gov.

About Largo

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURETM and VPURE+TM products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) vanadium production from its operations in Brazil and 2.) energy storage business in the U.S. to support a low carbon future through its clean energy division.

Largo’s common shares trade on the Nasdaq Stock Market and on the Toronto Stock Exchange under the symbol “LGO”. For more information, please visit www.largoinc.com.

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable Canadian and United States securities legislation. Forward‐looking information in this press release includes, but is not limited to, statements with respect to the timing and amount of estimated future production and sales; the future price of commodities; costs of future activities and operations, including, without limitation, the effect of inflation and exchange rates; the effect of unforeseen equipment maintenance or repairs on production; timing and cost related to the commissioning and ramp-up of the ilmenite plan, ilmenite production; the ability to sell ilmenite, V2O5 or other vanadium commodities on a profitable basis, the ability to produce high purity V2O5 and V2O3 according to customer specifications; the extent of capital and operating expenditures; the improvements to mine planning based on the results of drilling campaigns; the affect of the re-assay program results on measured and indicated resource estimates. Forward‐looking information in this press release also includes, but is not limited to, statements with respect to our ability to build, finance and successfully operate a VRFB business, the projected timing and cost of the completion of the EGPE project; our ability to protect and develop our technology, our ability to maintain our IP, the competitiveness of our product in an evolving market, our ability to market, sell and deliver our VCHARGE batteries on specification and at a competitive price, our ability to successfully deploy our VCHARGE batteries in foreign jurisdictions, the affect of the workforce reduction on operating costs, our ability to secure the required resources to build and deploy our VCHARGE batteries, and the adoption of VRFB technology generally in the market.

The following are some of the assumptions upon which forward-looking information is based: that general business and economic conditions will not change in a material adverse manner; demand for, and stable or improving price of V2O5, other vanadium products, ilmenite and titanium dioxide pigment; receipt of regulatory and governmental approvals, permits and renewals in a timely manner; that the Company will not experience any material accident, labour dispute or failure of plant or equipment or other material disruption in the Company’s operations at the Maracás Menchen Mine or relating to Largo Clean Energy, specially in respect of the installation and commissioning of the EGPE project; the availability of financing for operations and development; the availability of funding for future capital expenditures; the ability to replace current funding on terms satisfactory to the Company; the ability to mitigate the impact of heavy rainfall; the reliability of production, including, without limitation, access to massive ore, the Company’s ability to procure equipment, services and operating supplies in sufficient quantities and on a timely basis; that the estimates of the resources and reserves at the Maracás Menchen Mine are within reasonable bounds of accuracy (including with respect to size, grade and recovery and the operational and price assumptions on which such estimates are based); the accuracy of the Company’s mine plan at the Maracás Menchen Mine, the competitiveness of the Company’s VRFB technology; the ability to obtain funding through government grants and awards for the Green Energy sector, the accuracy of cost estimates and assumptions on future variations of VCHARGE battery system design, that the Company’s current plans for ilmenite and VRFBs can be achieved; the Company’s “two-pillar” business strategy will be successful; the Company’s sales and trading arrangements will not be affected by the evolving sanctions against Russia; and the Company’s ability to attract and retain skilled personnel and directors; the ability of management to execute strategic goals.

Forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. All information contained in this news release, other than statements of current and historical fact, is forward looking information. Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Largo or Largo Clean Energy to be materially different from those expressed or implied by such forward-looking statements, including but not limited to those risks described in the annual information form of Largo and in its public documents filed on www.sedar.com and available on www.sec.gov from time to time. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made. Although management of Largo has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Largo does not undertake to update any forward-looking statements, except in accordance with applicable securities laws. Readers should also review the risks and uncertainties sections of Largo’s annual and interim MD&As which also apply.

Trademarks are owned by Largo Inc.

Q2 2023 Net Income Reconciliation

Q2 2023

Total V2O5 equivalent sold

000s lbs

5,637

A

Tonnesi

2,557

Produced V2O5 equivalent sold

000s lbs

5,000

B

Tonnesi

2,268

Revenues per pound sold

$/lb

$

9.42

C

Cash operating costs per pound

$/lb

$

5.67

D

Conversion of tonnes to pounds, 1 tonne = 2,204.62 pounds or lbs.

Q2 2023

Revenues

$

53,110

A x C 2,557 tonnes of V2O5 equivalent sold (Q2 2022 – 3,291 tonnes), with revenues per pound sold of $9.42 (Q2 2022 – $11.69)

Cash operating costs

(28,365)

B x D Global recovery of 81.0% (Q2 2022 – 81.8%), impact of increased mining costs and cost increases for critical consumables

Other operating costs

Conversion costs (costs incurred in converting V2O5 to FeV that are recognized on the sale of FeV)

(2,220)

Note 19 579 tonnes of FeV sold

Product acquisition costs (costs incurred in purchasing products from 3rd parties that are recognized on the sale of those products)

(3,753)

Note 19 289 tonnes of V2O5 equivalent of purchased products sold, compared with 508 tonnes in Q2 2022 with a cost of $9,568

Distribution costs

(2,525)

Note 19

Depreciation

(6,202)

Note 19

Inventory write-down

(683)

Note 19 Attributable to purchased FeV and V2O5 inventory

Increase in legal provisions

(230)

See “other general and administrative expenses” section on page 5

Iron ore costs

(220)

Note 19

(15,833)

Commercial & Corporate costs

Professional, consulting and management fees

(2,453)

Note 15 (Sales & trading plus Corporate)

Other general and administrative expenses

(1,332)

Share-based payments

(413)

(4,198)

Largo Clean Energy

(5,236)

Note 15 (excluding finance costs and foreign exchange) 2023 guidance between $13,500 and $14,500

Largo Physical Vanadium

(332)

Note 15 (excluding finance costs and foreign exchange)

Titanium project

(174)

Note 15 – “other”

Foreign exchange loss

(817)

Finance costs

(1,981)

Interest income

480

Exploration and evaluation costs

(1,301)

Net income before tax

(4,647)

Income tax expense

295

Deferred income tax expense

(1,614)

Net income (loss)

$

(5,966)

Note references in the table above refer to the note disclosures contained in the Q2 2023 unaudited condensed interim consolidated financial statements.

Non-GAAP Measures

The Company uses certain non-GAAP measures in its press release, which are described in the following section. Non-GAAP financial measures and non-GAAP ratios are not standardized financial measures under IFRS, the Company’s GAAP, and might not be comparable to similar financial measures disclosed by other issuers. These measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Revenues Per Pound

The Company’s press release refers to revenues per pound sold, V2O5 revenues per pound of V2O5 sold and FeV revenues per kg of FeV sold, which are non-GAAP financial measures that are used to provide investors with information about a key measure used by management to monitor performance of the Company.

These measures, along with cash operating costs, are considered to be key indicators of the Company’s ability to generate operating earnings and cash flow from its Maracás Menchen Mine and sales activities. These measures differ from measures determined in accordance with IFRS, and are not necessarily indicative of net earnings or cash flow from operating activities as determined under IFRS.

The following table provides a reconciliation of revenues per pound sold, V2O5 revenues per pound of V2O5 sold and FeV revenues per kg of FeV sold to revenues and the revenue information presented in note 18 as per the Q2 2022 unaudited condensed interim consolidated financial statements.

Three months ended

Six months ended

June 30, 2023

June 30, 2022

June 30, 2023

June 30, 2022

Revenues – V2O5 producedi

$

30,558

$

45,976

$

65,084

$

67,790

V2O5 sold – produced (000s lb)

3,083

4,385

6,881

7,079

V2O5 revenues per pound of V2O5 sold – produced ($/lb)

$

9.91

$

10.48

$

9.46

$

9.58

Revenues – V2O5 purchasedi

$

2,937

$

1,143

$

5,465

$

1,529

V2O5 sold – purchased (000s lb)

396

88

705

132

V2O5 revenues per pound of V2O5 sold – purchased ($/lb)

$

7.42

$

12.99

$

7.75

$

11.58

Revenues – V2O5i

$

33,495

$

47,119

$

70,549

$

69,319

V2O5 sold (000s lb)

3,479

4,473

7,586

7,211

V2O5 revenues per pound of V2O5 sold ($/lb)

$

9.63

$

10.53

$

9.30

$

9.61

Revenues – V2O3i

$

2,358

$

47,119

$

3,841

$

69,319

V2O3 sold (000s lb)

177

–

311

–

V2O3 revenues per pound of V2O3 sold ($/lb)

$

13.32

$

–

$

12.35

$

–

Revenues – FeV producedi

$

17,230

$

22,883

$

34,658

$

41,911

FeV sold – produced (000s kg)

579

550

1,147

1,182

FeV revenues per kg of FeV sold – produced ($/kg)

$

29.76

$

41.61

$

30.22

$

35.46

Revenues – FeV purchasedi

$

27

$

14,802

$

328

$

16,262

FeV sold – purchased (000s kg)

1

317

11

357

FeV revenues per kg of FeV sold – purchased ($/kg)

$

27.00

$

46.69

$

29.82

$

45.55

Revenues – FeVi

$

17,256

$

37,685

$

34,986

$

58,173

FeV sold (000s kg)

580

867

1,158

1,539

FeV revenues per kg of FeV sold ($/kg)

$

29.75

$

43.47

$

30.21

$

37.80

Revenuesi

$

53,110

$

84,804

$

110,531

$

127,492

V2O5 equivalent sold (000s lb)

5,637

7,255

11,918

12,176

Revenues per pound sold ($/lb)

$

9.42

$

11.69

$

9.27

$

10.47

As per note 18 in the Company’s Q2 2023 unaudited condensed interim consolidated financial statements.

Cash Operating Costs and Cash Operating Costs Excluding Royalties

The Company’s press release refers to cash operating costs per pound and cash operating costs excluding royalties per pound, which are non-GAAP ratios based on cash operating costs and cash operating costs excluding royalties, which are non-GAAP financial measures, in order to provide investors with information about a key measure used by management to monitor performance. This information is used to assess how well the Maracás Menchen Mine is performing compared to plan and prior periods, and also to assess its overall effectiveness and efficiency.

Cash operating costs includes mine site operating costs such as mining costs, plant and maintenance costs, sustainability costs, mine and plant administration costs, royalties and sales, general and administrative costs (all for the Mine properties segment), but excludes depreciation and amortization, share-based payments, foreign exchange gains or losses, commissions, reclamation, capital expenditures and exploration and evaluation costs. Operating costs not attributable to the Mine properties segment are also excluded, including conversion costs, product acquisition costs, distribution costs and inventory write-downs.

Cash operating costs excluding royalties is calculated as cash operating costs less royalties.

Cash operating costs per pound and cash operating costs excluding royalties per pound are obtained by dividing cash operating costs and cash operating costs excluding royalties, respectively, by the pounds of vanadium equivalent sold that were produced by the Maracás Menchen Mine.

Cash operating costs, cash operating costs excluding royalties, cash operating costs per pound and cash operating costs excluding royalties per pound, along with revenues, are considered to be key indicators of the Company’s ability to generate operating earnings and cash flow from its Maracás Menchen Mine. These measures differ from measures determined in accordance with IFRS, and are not necessarily indicative of net earnings or cash flow from operating activities as determined under IFRS.

The following table provides a reconciliation of cash operating costs and cash operating costs excluding royalties, cash operating costs per pound and cash operating costs excluding royalties per pound for the Maracás Menchen Mine to operating costs as per the Q2 2022 unaudited condensed interim consolidated financial statements.

Three months ended

Six months ended

June 30, 2023

June 30, 2022

June 30, 2023

June 30, 2022

Operating costsi

$

43,029

$

50,704

$

88,960

$

79,662

Professional, consulting and management feesii

624

1,567

1,468

2,603

Other general and administrative expensesiii

315

209

624

476

Less: iron ore costsi

(220)

(222)

(493)

(437)

Less: conversion costsi

(2,220)

(2,337)

(4,138)

(4,184)

Less: product acquisition costsi

(3,753)

(9,568)

(7,931)

(11,118)

Less: distribution costsi

(2,525)

(2,851)

(3,972)

(4,306)

Less: inventory write-down

(683)

(2,285)

(683)

(2,285)

Less: depreciation and amortization expense1

(6,202)

(5,507)

(13,453)

(9,812)

Cash operating costs

28,365

29,710

60,382

50,599

Less: royaltiesi

(2,450)

(3,742)

(4,895)

(5,768)

Cash operating costs excluding royalties

25,915

25,968

55,487

44,831

Produced V2O5 sold (000s lb)

5,000

6,135

10,741

10,882

Cash operating costs per pound ($/lb)

$

5.67

$

4.84

$

5.62

$

4.65

Cash operating costs excluding royalties per pound ($/lb)

$

5.18

$

4.23

$

5.17

$

4.12

As per note 19 in the Company’s Q2 2023 unaudited condensed interim consolidated financial statements.

As per the Mine properties segment in note 15 in the Company’s Q2 2023 unaudited condensed interim consolidated financial statements.

As per the Mine properties segment in note 15, less the increase in legal provisions of $0.2 million (Q2 2023) and $0.3 million (for the six months ended June 30, 2023) as noted in the “other general and administrative expenses” section on page 6 of the Company’s Q2 2023 Management Discussion and Analysis.

______________________________________ 1Revenues per pound sold and cash operating costs are non-GAAP financial measures, and cash operating costs per pound and cash operating costs excluding royalties per pound are non-GAAP ratios with no standard meaning under IFRS, and may not be comparable to similar financial measures disclosed by other issuers. Refer to the “Non-GAAP Measures” section of this press release. 2Defined as current assets less current liabilities per the consolidated statements of financial position. 3Conversion of tonnes to pounds, 1 tonne = 2,204.62 pounds or lbs. 4Fastmarkets Metal Bulletin. 5Effective grade represents the percentage of magnetic material mined multiplied by the percentage of V2O5 in the magnetic concentrate. 6Global recovery is the product of crushing recovery, milling recovery, kiln recovery, leaching recovery and chemical plant recovery. 7GAAP – Generally Accepted Accounting Principles 8RBC Capital Markets Vanadium Outlook (2023)

For further information, please contact: Investor Relations Alex Guthrie Senior Manager, External Relations +1.416.861.9778 aguthrie@largoinc.com

CALGARY, AB, Aug. 9, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) is pleased to announce financial results for the three and six months ended June 30, 2023 and an operational update.

All references herein to $ refer to United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

President & CEO, Corey C. Ruttan commented:

“We continue to post strong results, generating an operating netback of $69.61 per boe and $11 million in funds flow from operations, highlighting the strong profitability of our operations. Our 2023 capital program is focused on adding 100% interest production from our Murucututu natural gas project and our Bom Lugar oil field. We have had exciting early results with the stimulation of our 197(1) Murucututu well and drilling our first oil development well at Bom Lugar.”

Operational Update

Drilling operations continue on the 183-A3 well on our Murucututu natural gas field. The well was spud on July 11th and is targeting shallower exploration potential in the Caruaçu Formation and the Gomo member of the Candeias Formation. We expect drilling to be completed later this quarter. We also expect to complete our recently drilled Bom Lugar well (BL-06) and have the well on production in the third quarter.

Our natural gas price under our long-term gas sales agreement with Bahiagás was adjusted effective August 1st to BRL1.99/m3 or $13.25/Mcf, based on our average heat content to date, the July 31, 2023 BRL/USD foreign exchange rate of 4.74 and enhanced sales tax credits applicable in 2023. This new gas price is effective for all of our natural gas sales from both our Caburé and Murucututu fields as of August 1, 2023.

Financial and Operating Highlights – Second Quarter of 2023

Average daily sales decreased to 1,975 boepd (-29% from Q1 2023 and -16% from Q2 2022) due mainly to reduced production from our Caburé natural gas field as a result of higher nominated volumes from our partner.

Our average realized natural gas price increased to $12.86/Mcf, an 8% increase from Q2 2022 with the 3% increase in our contracted natural gas price and enhanced sales tax credits available in 2023. Compared to Q1 2023, our realized sales price increased 7% due mainly to the appreciation of the BRL to the USD in Q2. With the higher natural gas price, our overall realized price per boe increased to $77.41 (+6% from Q1 2023 and +5% from Q2 2022), despite lower Brent pricing on condensate sales.

Our natural gas, condensate and oil revenue was $13.9 million in Q2 2023, a decrease of $1.9 million compared to Q2 2022 (-12%) due to a 16% decrease in production partially offset by the increase in realized sales prices per boe.

Our operating netback improved to $69.61 per boe (+$3.00 per boe from Q1 2023 and +$5.65 per boe from Q2 2022) with a higher realized sales price and lower royalties, partially offset by the impact of fixed operating costs with lower sales volumes.

We generated funds flows from operations of $11.0 million ($0.30 per basic share and $0.29 per diluted share), a decrease of $1.4 million compared to Q2 2022 and $3.9 million compared to Q1 2023.

We reported net income of $9.9 million in Q2 2023, an increase of $3.2 million (+49%) compared to Q2 2022.

Capital expenditures totaled $8.5 million, including drilling cost for our BL-06 well on our Bom Lugar field, stimulation costs for our 197(1) well on our Murucututu field, and long-lead purchases for future capital projects.

Our working capital surplus was $18.1 million as of June 30, 2023, a decrease of $2.8 million from March 31, 2023, and an improvement of $3.4 million from December 31, 2022.

The following table provides a summary of Alvopetro’s financial and operating results for three and six months ended June 30, 2023 and June 30, 2022. The consolidated financial statements with the Management’s Discussion and Analysis (“MD&A”) are available on our website at www.alvopetro.com and will be available on the SEDAR+ website at www.sedarplus.ca.

As at and Three Months EndedJune 30,

As at and Six Months EndedJune 30,

2023

2022

Change

2023

2022

Change (%)

Financial

($000s, except where noted)

Natural gas, oil and condensate sales

13,914

15,787

(12)

32,074

29,759

8

Net income

9,852

6,631

49

22,054

17,746

24

Per share – basic ($)(1)

0.27

0.20

35

0.60

0.52

15

Per share – diluted ($)(1)

0.26

0.18

44

0.59

0.49

20

Cash flows from operating activities

13,473

12,997

4

27,329

21,330

28

Per share – basic ($)(1)

0.37

0.38

(3)

0.75

0.63

19

Per share – diluted ($)(1)

0.36

0.35

3

0.73

0.59

24

Funds flow from operations (2)

11,047

12,434

(11)

26,019

23,338

11

Per share – basic ($)(1)

0.30

0.37

(19)

0.71

0.69

3

Per share – diluted ($)(1)

0.29

0.34

(15)

0.69

0.64

8

Dividends declared

5,109

2,728

87

10,213

5,444

88

Per share(1)

0.14

0.08

75

0.28

0.16

75

Capital expenditures

8,521

6,338

34

11,812

10,138

17

Cash and cash equivalents

25,598

13,672

87

25,598

13,672

87

Net working capital surplus(2)

18,084

11,641

55

18,084

11,641

55

Working capital, net of debt(2)

18,084

9,096

99

18,084

9,096

99

Weighted average shares outstanding

Basic (000s)(1)

36,697

33,973

8

36,627

33,941

8

Diluted (000s)(1)

37,755

36,637

3

37,657

36,426

3

Operations

Natural gas, NGLs and crude oil sales:

Natural gas (Mcfpd)

11,269

13,546

(17)

13,520

13,940

(3)

NGLs – condensate (bopd)

92

97

(5)

111

98

13

Oil (bopd)

5

5

–

5

8

(38)

Total (boepd)

1,975

2,359

(16)

2,369

2,429

(2)

Average realized prices(2):

Natural gas ($/Mcf)

12.86

11.90

8

12.40

10.94

13

NGLs – condensate ($/bbl)

83.35

121.93

(32)

83.79

114.11

(27)

Oil ($/bbl)

63.93

94.47

(32)

68.00

83.90

(19)

Total ($/boe)

77.41

73.54

5

74.80

67.68

11

Operating netback ($/boe)(2)

Realized sales price

77.41

73.54

5

74.80

67.68

11

Royalties

(1.97)

(5.35)

(63)

(2.18)

(4.84)

(55)

Production expenses

(5.83)

(4.23)

38

(4.75)

(4.00)

19

Operating netback

69.61

63.96

9

67.87

58.84

15

Operating netback margin(2)

90 %

87 %

3

91 %

87 %

5

Notes:

(1) Per share amounts are based on weighted average shares outstanding other than dividends per share, which is based on the number of common shares outstanding at each dividend record date. The weighted average number of diluted common shares outstanding in the computation of funds flow from operations and cash flows from operating activities per share is the same as for net income per share.

(2) See “Non-GAAP and Other Financial Measures” section within this news release.

Q2 2023 Results Webcast

Alvopetro will host a live webcast to discuss our Q2 2023 financial results at 9:00 am Mountain time on Thursday August 10, 2023. Details for joining the event are as follows:

The webcast will include a question and answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to socialmedia@alvopetro.com.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé and Murucututu natural gas fields and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Abbreviations:

$000s

=

thousands of U.S. dollars

bbls

=

barrels

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

BRL

=

Brazilian Real

CAD

=

Canadian dollars

m3

=

cubic metre

Mcf

=

thousand cubic feet

Mcfpd

=

thousand cubic feet per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

NGLs

=

natural gas liquids

Q1 2023

=

three months ended March 31, 2023

Q2 2022

=

three months ended June 30, 2022

Q2 2023

=

three months ended June 30, 2023

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this report should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s MD&A which may be accessed through the SEDAR+ website at www.sedarplus.ca.

Non-GAAP Financial Measures

Operating netback

Operating netback is calculated as natural gas, oil and condensate revenues less royalties and production expenses. This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR+ website at www.sedarplus.ca. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations.

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback divided by total sales volumes (barrels of oil equivalent). This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR+ website at www.sedarplus.ca. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe).

Operating netback margin

Operating netback margin is calculated as operating netback per boe divided by the realized sales price per boe. Operating netback margin is a measure of the profitability per boe relative to natural gas, oil and condensate sales revenues per boe and is calculated as follows:

Three Months EndedJune 30,

Six Months EndedJune 30,

2023

2022

2023

2022

Operating netback – $ per boe

69.61

63.96

67.87

58.84

Average realized price – $ per boe

77.41

73.54

74.80

67.68

Operating netback margin

90 %

87 %

91 %

87 %

Funds Flow from Operations Per Share

Funds flow from operations per share is a non-GAAP ratio that includes all cash generated from operating activities and is calculated before changes in non-cash working capital, divided by the weighted the weighted average shares outstanding for the respective period. For the periods reported in this news release the cash flows from operating activities per share and funds flow from operations per share is as follows:

Three Months EndedJune 30,

Six Months EndedJune 30,

$ per share

2023

2022

2023

2022

Per basic share:

Cash flows from operating activities

0.37

0.38

0.75

0.63

Funds flow from operations

0.30

0.37

0.71

0.69

Per diluted share:

Cash flows from operating activities

0.36

0.35

0.73

0.59

Funds flow from operations

0.29

0.34

0.69

0.64

Capital Management Measures

Funds Flow from Operations

Funds flow from operations is a non-GAAP capital management measure that includes all cash generated from operating activities and is calculated before changes in non-cash working capital. The most comparable GAAP measure to funds flow from operations is cash flows from operating activities. Management considers funds flow from operations important as it helps evaluate financial performance and demonstrates the Company’s ability to generate sufficient cash to fund future growth opportunities. Funds flow from operations should not be considered an alternative to, or more meaningful than, cash flows from operating activities however management finds that the impact of working capital items on the cash flows reduces the comparability of the metric from period to period. A reconciliation of funds flow from operations to cash flows from operating activities is as follows:

Three Months EndedJune 30,

Six Months EndedJune 30,

2023

2022

2023

2022

Cash flows from operating activities

13,473

12,997

27,329

21,330

(Deduct) add back changes in non-cash working capital