Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Macro Headwinds. While macro headwinds remain in the B2B and B2C segments, green shoots are appearing, with new B2B contracts and an expanding pipeline of new business opportunities. Over at retail, the Company has seen improved traction with targeted profitable sales campaigns and value added promotions.

Playing to its Strengths. Project “Optimize for Growth” and the B2B focus plays into ODP’s core strengths, such as robust supply chain assets, distribution capabilities, and an expansive B2B customer base. We believe these moves position ODP to unlock sustainable growth and long-term success.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

New partnership reaffirms ODP Business Solutions’ commitment to the hospitality industry and adjacent categories, fostering a refined guest experience

BOCA RATON, Fla.–(BUSINESS WIRE)–Mar. 3, 2025– ODP Business Solutions, a leading supplier of workplace solutions and services and a division of The ODP Corporation (NASDAQ: ODP), announced today a strategic distribution partnership with Hunter Amenities. ODP Business Solutions will distribute Hunter’s wide range of hotel and guest amenities to hospitality partners, including liquid beauty products, soaps, dry goods and more, all uniquely bundled to accommodate the needs of every client and guest.

“Our partnership with Hunter Amenities demonstrates our commitment to continuing to expand our presence and product offerings in the hospitality industry and other adjacent sectors,” said David Centrella, EVP and president of ODP Business Solutions. “Distributing Hunter Amenities’ premium products further positions ODP Business Solutions to serve as a key-supplier for in-room needs.”

Hunter Amenities is an award-winning global manufacturing company that has been a pioneer in the personal care and hospitality industry for more than four decades. Renowned for its world-class manufacturing facilities that combine artisanal traditions with cutting-edge innovation, the company partners with some of the world’s most prestigious hospitality and retail brands. Hunter Amenities now provides its rich portfolio of high-end personal care products through ODP Business Solutions’ vast network of solutions and service, advancing how the hospitality industry can bring a luxurious, elevated experience to their guests.

“Partnering with ODP Business Solutions as a distribution partner is a natural fit for our company. Their best-in-class distribution capabilities and remarkably agile team give us complete confidence, which is why we’ve gone all in—rolling out our full portfolio within their expansive customer network. This collaboration is a true win-win for both organizations and a game-changer for the entire hospitality industry,” said John Hunter, founder of Hunter Amenities.

Hunter’s extensive product portfolio includes curated shampoo, conditioner, body wash, lotion, and hand wash, along with VIP indulgences such as lip balm, hand cream, eye cream, sleep balm, facial mist, and pillow mist—crafted for discerning travelers who expect nothing but the best.

“Introducing Hunter Amenities to our hospitality distribution services will provide our customers the opportunity to enhance each guest’s stay with custom, high-end offerings that pair seamlessly with ODP Business Solutions’ unparalleled service,” said Nisha Brown, vice president of marketing & product management at ODP Business Solutions. “Hunter is a globally recognized luxury brand that aligns perfectly with our commitment to quality and innovation. We look forward to continuing our growth in the hospitality market and beyond, offering tailored solutions that meet the evolving needs of our clients.”

ODP Business Solutions also delivers high-quality solutions in categories that include technology, professional cleaning and furniture, while expanding into new verticals to better serve the needs of its customers. This partnership announcement follows ODP Business Solutions recent milestone contract with a leading hospitality management company.

To learn more about ODP Business Solutions, visit odpbusiness.com.

About ODP Business Solutions:

ODP Business Solutions is a trusted partner with more than 30 years of experience working with businesses to adapt to the ever-changing world of work. From technology transformation, sustainability, innovative workspace design, cleaning and breakroom, and everything in between, ODP Business Solutions has the integrated products and services businesses need. Powered by a collaborative team of experienced business consultants, world-class logistics and trusted brand names, ODP Business Solutions advances how the working world gets work done. For more information on ODP Business Solutions, visit odpbusiness.com.

ODP Business Solutions is a division of The ODP Corporation (NASDAQ: ODP). ODP and ODP Business Solutions are trademarks of ODP Business Solutions, LLC. Any other product or company names mentioned herein are the trademarks of their respective owners.

About Hunter Amenities:

Since 1981, Hunter Amenities has become one of the world’s largest manufacturers and leading formulators of superior personal care guest amenities, servicing hospitality customers in over 100 countries. Our products range from a prominent selection of licensed, internationally recognized designer and cosmetic brands to distinctive luxurious spa hotel amenities and retail collections.

The ODP Corporation (NASDAQ:ODP) is a leading provider of products and services through an integrated business-to-business (B2B) distribution platform and omnichannel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, online presence and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; and Veyer, LLC, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

This communication may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements or disclosures may discuss goals, intentions and expectations as to future trends, plans, events, results of operations, cash flow or financial condition, or state other information relating to, among other things, The ODP Corporation (“the Company”), based on current beliefs and assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “expectations”, “outlook,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “propose” “aim” or other similar words, phrases or expressions, or other variations of such words. These forward-looking statements are subject to various risks and uncertainties, many of which are outside of the Company’s control. There can be no assurances that the Company will realize these expectations or that these beliefs will prove correct, and therefore investors and stakeholders should not place undue reliance on such statements.

Investors and shareholders should carefully consider the foregoing factors and the other risks and uncertainties described in the Company’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K filed with the U.S. Securities and Exchange Commission. The Company does not assume any obligation to update or revise any forward-looking statements.

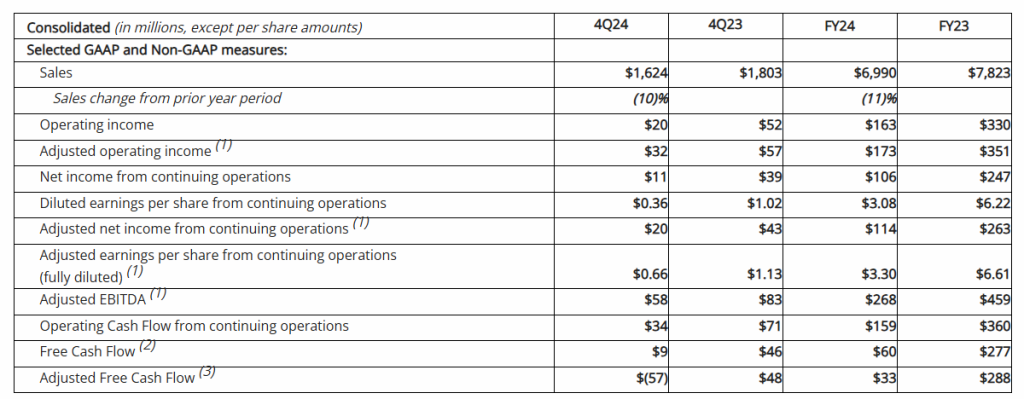

Fourth Quarter Revenue of $1.6 Billion with GAAP EPS of $0.36; Adjusted EPS of $0.66

Announced Milestone Agreement with Leading Hospitality Management Company Becoming Key Supplier and Distribution Partner — A Key Step in Expanding Beyond Office Supplies

Launches “Optimize for Growth” Plan to Accelerate Revenue Growth in B2B Industry Segments

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 26, 2025– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the fourth quarter and full year ended December 28, 2024.

Fourth Quarter 2024 Summary(1)(3)

Total reported sales of $1.6 billion, down 10% versus the prior year period on a reported basis. The decrease in reported sales is largely related to lower sales in its Office Depot Division, primarily due to 47 fewer retail locations in service compared to the previous year and reduced retail and online consumer traffic, as well as lower sales in its ODP Business Solutions Division

GAAP operating income of $20 million and net income from continuing operations of $11 million, or $0.36 per diluted share, versus $52 million and $39 million, respectively, or $1.02 per diluted share, in the prior year period

Adjusted operating income of $32 million, compared to $57 million in the fourth quarter of 2023; adjusted EBITDA of $58 million, compared to $83 million in the fourth quarter of 2023

Adjusted net income from continuing operations of $20 million, or adjusted diluted earnings per share from continuing operations of $0.66, versus $43 million or $1.13, respectively, in the prior year period

Operating cash flow from continuing operations of $34 million and adjusted free cash flow of $(57) million, versus $71 million and $48 million, respectively, in the prior year period

Repurchased 1.4 million shares at a cost of $43 million in the fourth quarter of 2024

$644 million of total available liquidity including $166 million in cash and cash equivalents at quarter end

Full Year 2024 Summary

Total reported sales of $7.0 billion, versus $7.8 billion in the prior year

GAAP operating income of $163 million and net income from continuing operations of $106 million, or $3.08 per diluted share, versus $330 million and net income from continuing operations of $247 million, or $6.22 per diluted share, respectively, in the prior year

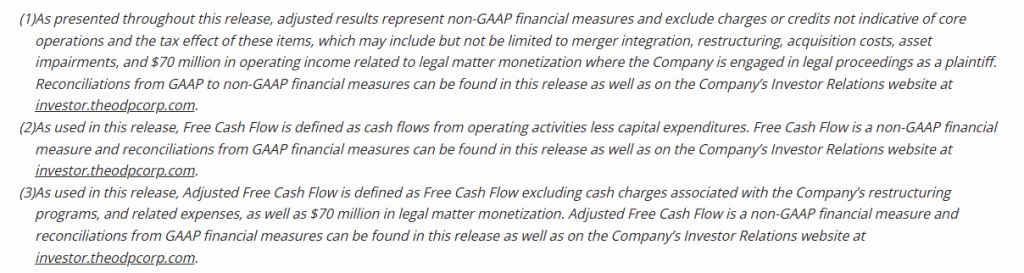

Adjusted operating income of $173 million, compared to $351 million in 2023; adjusted EBITDA of $268 million, compared to $459 million in 2023. Adjusted operating income in 2024 excludes $70 million of income related to legal matter monetization where the Company is engaged in legal proceedings as a plaintiff

Adjusted net income from continuing operations of $114 million, or adjusted diluted earnings per share from continuing operations of $3.30, versus $263 million or $6.61, respectively, in the prior year. Adjusted net income from continuing operations in 2024 excludes $70 million of income or $51 million of income, net of tax related to legal matter monetization where the Company is engaged in legal proceedings as a plaintiff

Operating cash flow from continuing operations of $159 million and adjusted free cash flow of $33 million, versus $360 million and $288 million, respectively in the prior year

Repurchased 8 million shares for $300 million in 2024

“We made significant progress in our B2B pivot during the year, strengthening ODP’s position to drive sustainable profitable growth in the future,” said Gerry Smith, chief executive officer of The ODP Corporation. “Our core strengths in supply chain, procurement, and distribution have continued to provide a meaningful competitive advantage, resulting in recent major new business wins across both our traditional market segments and in new higher-growth industry sectors. Building on our recent success and our core competencies, we are intensifying our focus on the growing potential within the B2B marketplace.”

“We’re now positioned to pursue growth in a new industry segment, recently signing a transformative contract with a major hotel management company that establishes ODP as a preferred supplier in the expanding $16 billion hospitality industry. This landmark agreement is a key step in expanding beyond office supplies and represents a true inflection point in our business, enabling us to strategically expand into growing industry segments where our core competencies resonate. When combined with adjacent industry segments, this represents a compelling $60 billion market opportunity for ODP to showcase its next-day delivery capabilities, exceptional customer service, and extensive national supply chain network to a growing customer base,” Smith continued.

“Our recent progress has the potential to reshape our business trajectory in the future after what has been a challenging period for our industry,” said Smith. “While we achieved our revised guidance for the year, our performance in 2024 was impacted by weak macroeconomic trends, subdued business and consumer activity, and effects from severe weather in the second half of the year. However, we remain competitively strong and, in addition to the landmark hospitality agreement, we continue to secure major new business wins, including signing one of the largest multi-year B2B contracts in our history and successfully launching strategic warehousing and fulfillment services to support one of the world’s leading social media-driven e-commerce platforms.”

“Building on these accomplishments, we are announcing our ‘Optimize for Growth’ plan,” Smith continued. “This plan capitalizes on our core strengths—including a robust B2B infrastructure, supply chain assets, strong distribution network, and loyal customer base—to expand and accelerate growth in the B2B distribution and 3PL market segments while reducing our retail exposure and associated obligations. Supporting our strategy, we are realigning our organization, refining product assortments, and reallocating capital to prioritize growth in the B2B marketplace. At the same time, we will suspend growth investments in our retail segment and continue to optimize our store footprint to better align with our long-term strategy. That said, we remain committed to supporting and providing an exceptional service experience at our active retail locations.”

“As we look ahead to 2025, our strategic priority remains centered on capturing the numerous opportunities in the B2B marketplace and pursuing growth in new industry segments. Although transformational progress takes time to fully materialize and macroeconomic conditions continue to present near-term challenges, we are confident in the strength of our strategy and steadfast in our commitment to delivering sustained, long-term value for our shareholders. We look forward to providing updates on our progress and offering deeper insights into our long-term growth plans in the quarters ahead,” Smith concluded.

Consolidated Results

Reported (GAAP) Results

Total reported sales for the fourth quarter of 2024 were $1.6 billion, a decrease of 10% compared with the same period last year, driven primarily by lower sales in both its consumer and business-to-business (B2B) divisions. Lower sales in its consumer division, Office Depot, was primarily due to lower retail and online consumer traffic and lower average order volumes, as well as 47 fewer stores in service compared to last year related to planned store closures. Sales at ODP Business Solutions Division were lower compared to last year, largely driven by macroeconomic factors causing reduced spending among business customers and fewer transactions. Meanwhile, Veyer continued to provide strong logistics support for the ODP Business Solutions and Office Depot Divisions on lower internal sales volume, and continued to execute across its growth strategy, delivering supply chain and procurement solutions to third-party customers and driving increases in external revenue.

The Company reported GAAP operating income of $20 million in the fourth quarter of 2024, down compared to GAAP operating income of $52 million in the prior year period. Operating results in the fourth quarter of 2024 included $12 million of charges primarily related to non-cash asset impairments of operating lease right-of-use (ROU) assets associated with the Company’s retail store locations. Net income from continuing operations was $11 million, or $0.36 per diluted share in the fourth quarter of 2024, down compared to net income from continuing operations of $39 million, or $1.02 per diluted share in the fourth quarter of 2023.

Adjusted (non-GAAP) Results(1)

Adjusted results for the fourth quarter of 2024 exclude charges and credits totaling $12 million as described above and the associated tax impacts.

Fourth quarter 2024 adjusted EBITDA was $58 million compared to $83 million in the prior year period. This included depreciation and amortization of $24 million in both the fourth quarter of 2024 and 2023

Fourth quarter 2024 adjusted operating income was $32 million, down compared to $57 million in the fourth quarter of 2023

Fourth quarter 2024 adjusted net income from continuing operations was $20 million, or $0.66 per diluted share, compared to $43 million, or $1.13 per diluted share, in the fourth quarter of 2023, a decrease of 42% on a per share basis

Division Results

ODP Business Solutions Division

Leading B2B distribution solutions provider serving small, medium and enterprise level companies with an annual trailing-twelve-month revenue of $3.6 billion.

Reported sales were $827 million in the fourth quarter of 2024, down 9% compared to the same period last year. The decrease in sales was related primarily to weaker macroeconomic conditions, a more cautious business spending environment, lower sales conversion, fewer customers, and the foreign exchange impact from a weaker Canadian dollar

Total adjacency category sales, including cleaning and breakroom, furniture, technology, and copy and print, were 44% of total ODP Business Solutions’ sales, flat with the prior year

Executed initiatives to convert strong pipeline of potential new business and implemented several initiatives to regain top-line traction, including progress on initiating service for one of the largest contracts in Company history, potentially generating up to $1.5 billion in revenue over a 10-year period

Remained competitively strong and made significant progress on establishing presence in new industry segments. Signed milestone agreement with leading hospitality management company becoming a key supplier and distribution partner, positioning ODP to expand in the growing $16 billion hospitality marketplace

Expected revenue generation from recent new business wins expected to ramp up in future quarters

Operating income was $25 million in the fourth quarter of 2024, down compared to $34 million in the same period last year on a reported basis. As a percentage of sales, operating income margin was 3%, down 70 basis points compared to the same period last year

Office Depot Division

Leading provider of retail consumer and small business products and services distributed via Office Depot and OfficeMax retail locations and eCommerce presence.

Reported sales were $784 million in the fourth quarter of 2024, down 13% compared to the prior year. Lower sales were partially driven by 47 fewer retail locations in service associated with planned store closures, as well as lower demand relative to last year in major product categories, lower average order volume, and lower online sales. The Company closed 16 retail stores in the quarter and had 869 stores at quarter end. Sales were down 8% on a comparable store basis

Store and online traffic were lower year over year due to macroeconomic factors causing weak consumer activity as well as the lingering effect of severe weather in major markets where we operate

Operating income was $30 million in the fourth quarter of 2024, compared to operating income of $43 million during the same period last year on a reported basis, driven primarily by the flow through impact from lower sales. As a percentage of sales, operating income was 4%, down 100 basis points compared to the same period last year

Veyer Division

Nationwide supply chain, distribution, procurement and global sourcing operation supporting Office Depot and ODP Business Solutions, as well as third-party customers. Veyer’s assets and capabilities include 8 million square feet of infrastructure through a network of distribution centers, cross-docks, and other facilities throughout the United States; a global sourcing presence in Asia; a large private fleet of vehicles; and business next-day delivery capabilities to 98.5% of US population.

In the fourth quarter of 2024, Veyer provided support for its internal customers, ODP Business Solutions and Office Depot, as well as its third-party customers, generating reported sales of $1.1 billion

Reported operating loss was $2 million in the fourth quarter of 2024, compared to operating income of $3 million in the prior year period driven by the flow through impact of lower sales to internal customers partially offset by services to third-party customers

Launched supply chain services for one of the world’s largest social media-focused e-commerce companies to deliver warehousing and fulfillment services for their online sales

In the fourth quarter of 2024, sales generated from third-party customers increased by 150% compared to the same period last year, resulting in sales of $20 million. EBITDA generated from third-party customers was $1 million in the quarter, lower compared to EBITDA of $3 million in the prior year period, driven largely by Veyer’s investment in resources to support the launch of services for new customer additions

Share Repurchases in 2024

During fiscal year 2024, the Company continued to execute under its previously announced $1 billion share repurchase authorization valid through March 31, 2027. During the fourth quarter of 2024, the Company repurchased approximately 1.4 million shares at a cost of $43 million.

“Throughout the year, we invested in our business while returning $300 million to shareholders through share repurchases in 2024,” said Adam Haggard, senior vice president and co-chief financial officer of The ODP Corporation. “Looking ahead to 2025, we plan to prioritize capital allocation toward our core business over share repurchases, focusing on high-return B2B growth opportunities that we believe will drive sustainable, long-term value for our shareholders.”

The number of shares to be repurchased under the authorization in the future and the timing of such transactions will depend on a variety of factors, including market conditions, regulatory requirements, and other corporate considerations. The share repurchase authorization could be suspended or discontinued at any time as determined by the Board of Directors.

Balance Sheet and Cash Flow

As of December 28, 2024, ODP had total available liquidity of approximately $644 million, consisting of $166 million in cash and cash equivalents and $478 million of available credit under the Fourth Amended Credit Agreement. Total debt was $279 million.

For the fourth quarter of 2024, cash provided by operating activities of continuing operations was $34 million, which included $70 million related to legal matter monetization where the Company is engaged in legal proceedings as a plaintiff, partially offset by $4 million in restructuring spend. This compared to cash provided by operating activities of continuing operations of $71 million in the fourth quarter of the prior year, which included $2 million in restructuring spend. The year-over-year change in operating cash flow is primarily related to lower sales and the timing of investments in working capital related to new business wins.

Capital expenditures were $25 million in both the fourth quarter of 2024 and 2023, reflecting continued growth investments in the Company’s digital transformation, distribution network, and eCommerce capabilities. Adjusted Free Cash Flow(3) was $(57) million in the fourth quarter of 2024, compared to $48 million in the prior year period.

Milestone Agreement with Premier Hospitality Company

Subsequent to the quarter end, the Company announced a major milestone agreement in its B2B evolution as its subsidiary, ODP Business Solutions, entered into a key new partnership with one of the world’s largest hotel management organizations becoming a preferred provider for Operating Supplies & Equipment (“OS&E”). Through this agreement, ODP Business Solutions will become a distribution partner to reliably support the recurring in-room hotel supply needs necessary to run operations, reset rooms between guests, and exceed their customers’ expectations. This product expansion and strategic partnership reflects ODP Business Solutions’ continued evolution beyond office supplies and highlights the Company’s ability to leverage its capabilities and offerings to elevate the experience to businesses in the hospitality, healthcare and adjacent sectors.

“Optimize for Growth” B2B Revenue Acceleration Plan

After a comprehensive review of its business units and in light of recent new business successes, including its recent entry into the hospitality industry, the Company announced its “Optimize for Growth” restructuring plan. This initiative focuses on capitalizing on ODP’s core strengths — including its supply chain and procurement expertise, robust distribution network, and strong B2B customer base — to accelerate growth in the B2B distribution and third-party logistics (3PL) market segments, while reducing retail exposure and associated liabilities. The plan strategically realigns the Company’s organizational structure, product offerings, and go-to-market strategies to target high-growth opportunities in the B2B marketplace, while also expanding into new enterprise segments, including hospitality, healthcare, and adjacent sectors.

As part of the plan, ODP will prioritize investments in resources and infrastructure critical to its growth in the B2B sector, while reducing fixed costs associated with retail operations, including store and distribution center leases. Concurrently, the Company will suspend growth investments in its consumer and retail business as it continues to optimize its retail store footprint. Despite reduced retail growth investments, ODP remains firmly committed to supporting and providing an exceptional service experience at its active retail locations, ensuring that customers continue to receive the top-tier care they expect.

In connection with this plan, the Company expects to incur costs in the range of $185 million to $230 million, which we anticipate will generate approximately $380 million in EBITDA improvement and generate over $1.3 billion in total value over the multi-year life of the plan.

The ODP Corporation will webcast a call with financial analysts and investors on February 26, 2025, at 9:00 am Eastern Time, which will be accessible to the media and the general public. To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products, services, and technology solutions through an integrated business-to-business (B2B) distribution platform and omni-channel presence, which includes supply chain and distribution operations, dedicated sales professionals, online presence, and a network of Office Depot and OfficeMax retail stores. Through its operating companies ODP Business Solutions, LLC; Office Depot, LLC; and Veyer, LLC, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

This communication may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements or disclosures may discuss goals, intentions and expectations as to future trends, plans, events, results of operations, cash flow or financial condition, or state other information relating to, among other things, the Company, based on current beliefs and assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “expectations”, “outlook,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “propose” or other similar words, phrases or expressions, or other variations of such words. These forward-looking statements are subject to various risks and uncertainties, many of which are outside of the Company’s control. There can be no assurances that the Company will realize these expectations or that these beliefs will prove correct, and therefore investors and stakeholders should not place undue reliance on such statements. Factors that could cause actual results to differ materially from those in the forward-looking statements include, among other things, highly competitive office products market and failure to differentiate the Company from other office supply resellers or respond to decline in general office supplies sales or to shifting consumer demands; competitive pressures on the Company’s sales and pricing; the risk that the Company is unable to transform the business into a service-driven, B2B platform or that such a strategy will not result in the benefits anticipated; the risk that the Company will not be able to achieve the expected benefits of its strategic plans, including charges and benefits related to Project Core and the Optimize for Growth Restructuring Plan; the risk that the Company may not be able to realize the anticipated benefits of acquisitions due to unforeseen liabilities, future capital expenditures, expenses, indebtedness and the unanticipated loss of key customers or the inability to achieve expected revenues, synergies, cost savings or financial performance; the risk that the Company is unable to successfully maintain a relevant omni-channel experience for its customers; the risk that the Company is unable to execute the Maximize B2B Restructuring Plan successfully or that such plan will not result in the benefits anticipated; failure to effectively manage the Company’s real estate portfolio; loss of business with government entities, purchasing consortiums, and sole- or limited- source distribution arrangements; failure to attract and retain qualified personnel, including employees in stores, service centers, distribution centers, field and corporate offices and executive management, and the inability to keep supply of skills and resources in balance with customer demand; failure to execute effective advertising efforts and maintain the Company’s reputation and brand at a high level; disruptions in computer systems, including delivery of technology services; breach of information technology systems affecting reputation, business partner and customer relationships and operations and resulting in high costs and lost revenue; unanticipated downturns in business relationships with customers or terms with the suppliers, third-party vendors and business partners; disruption of global sourcing activities, evolving foreign trade policy (including tariffs imposed on certain foreign made goods); exclusive Office Depot branded products are subject to additional product, supply chain and legal risks; product safety and quality concerns of manufacturers’ branded products and services and Office Depot private branded products; covenants in the credit facility; general disruption in the credit markets; incurrence of significant impairment charges; retained responsibility for liabilities of acquired companies; fluctuation in quarterly operating results due to seasonality of the Company’s business; changes in tax laws in jurisdictions where the Company operates; increases in wage and benefit costs and changes in labor regulations; changes in the regulatory environment, legal compliance risks and violations of the U.S. Foreign Corrupt Practices Act and other worldwide anti-bribery laws; volatility in the Company’s common stock price; changes in or the elimination of the payment of cash dividends on Company common stock; macroeconomic conditions such as higher interest rates and future declines in business or consumer spending; increases in fuel and other commodity prices and the cost of material, energy and other production costs, or unexpected costs that cannot be recouped in product pricing; unexpected claims, charges, litigation, dispute resolutions or settlement expenses; catastrophic events, including the impact of weather events on the Company’s business; the discouragement of lawsuits by shareholders against the Company and its directors and officers as a result of the exclusive forum selection of the Court of Chancery, the federal district court for the District of Delaware or other Delaware state courts by the Company as the sole and exclusive forum for such lawsuits; and the impact of the COVID-19 pandemic on the Company’s business. The foregoing list of factors is not exhaustive. Investors and shareholders should carefully consider the foregoing factors and the other risks and uncertainties described in the Company’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K filed with the U.S. Securities and Exchange Commission. The Company does not assume any obligation to update or revise any forward-looking statements.

LOS ANGELES, Feb. 25, 2025 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 13 other restaurant concepts, today announced that the Company will host a conference call to review its fourth quarter and full year 2024 financial results on Thursday, February 27, 2025 at 4:30 PM ET. A press release with fourth quarter and full year 2024 financial results will be issued prior to the conference call that day.

The conference call can be accessed live over the phone by dialing 1-877-704-4453 from the U.S. or 1-201-389-0920 internationally. A replay will be available after the call until Thursday, March 20, 2025, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 13751410. Hosting the call will be Andy Wiederhorn, Chairman, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call will also be webcast live from the corporate website at www.fatbrands.com, under the “Investors” section. A replay of the webcast will be available through the corporate website shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

SKYX Advanced and Smart Plug & Play Technologies to be utilized in Cavco’s High-End Premium Manufactured Homes at the World Largest Builders’ Show IBS

Since its Inception Cavco Homes is Estimated to Have Sold Nearly 1 Million Homes and Close to 20,000 Homes Annually During the Past Years

As SKYX Continues to Increase its U.S. and Canada Market Penetration, its Technologies will be Used in Cavco’s High-End Homes including the New Leading Premium Homes Skye View and Bungalow Models, in Show Village during the International Builders’ Show in Las Vegas February 25-27, 2025

MIAMI, Feb. 24, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 97 issued and pending patents globally and over 60 lighting and home décor websites, announces it will collaborate with Cavco Industries, Inc., a U.S. leading prefabricated home manufacturer to utilize SKYX’s advanced and smart plug & play technologies in Cavco’s premium prefabricated homes during the International Builders’ Show (IBS). SKYX’s technologies will be used in Cavco’s high-end homes, including their new leading premium homes Skye View and Bungalow models, in Show Village during the International Builders’ Show place in Las Vegas from February 25-27, 2025.

SKYX’s advance and smart plug & play platform technologies makes homes and buildings become advanced, safe, and smart instantly while significantly saving time and cost as well as adding substantial value to developers and homeowners.

Cavco is a leading U.S. manufacturer of prefabricated homes. As a publicly traded company, it ranks among the largest producers of manufactured and modular homes in the nation, renowned for its high-quality, premium designs. Cavco specializes in designing and producing factory-built housing products, which are distributed through an extensive network of independent and company-owned retailers. Since its inception, it is estimated that Cavco has sold nearly one million homes, with recent annual sales approaching 20,000 units.

Tim Gage, National Vice President of Cavco’s Park Models, and Specialty Homes said, “We are excited to utilize SKYX’s game-changing safe plug and play technology in our Cavco Park Model prefabricated homes at the IBS Pro Builder Show Village. We welcome people to visit our premium homes including our Skye View and Bungalow models to see how we utilize SKYX’s technologies. I strongly believe that the SKYX technology can become the standard for new construction, as it provides, safety, time saving, and smart capabilities, while advancing and adding significant value to our homes.”

Rani Kohen, Founder/Inventor and Executive Chairman, of SKYX Platforms, said, “We are truly excited to collaborate with a U.S. leading premium prefabricated home manufacturer such as Cavco during the world’s largest building show, IBS. This is another step toward our goal of making homes and buildings become advanced, safe, and smart as the new standard. We look forward to continuing to demonstrate our advanced smart platform technology’s ability to make homes and buildings become smarter and safer instantly, while significantly advancing buildings and saving time and costs for developers.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

ACCO Brands Corporation is one of the world’s largest designers, marketers and manufacturers of branded academic, consumer and business products. Our widely recognized brands include AT-A-GLANCE®, Esselte®, Five Star®, GBC®, Kensington®, Leitz®, Mead®, PowerA®, Quartet®, Rapid®, Rexel®, Swingline®, Tilibra®, and many others. Our products are sold in more than 100 countries around the world. More information about ACCO Brands, the Home of Great Brands Built by Great People, can be found at www.accobrands.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q24. Fourth quarter sales and EPS were in line with expectations, excluding greater than anticipated foreign currency headwinds. ACCO experienced ongoing softer demand for certain office-related products and lower demand for back-to-school products in Brazil, partially offset by growth in the technology accessories categories. ACCO further increased its multi-year cost reduction program to $100 million of cumulative savings.

Details. Revenue of $448.1 million was down 8.3% y-o-y, with comp sales down 5.9% and adverse foreign exchange reducing sales by 2.4%. Adjusted operating income was $64.2 million versus $68.3 million last year. Adjusted net income was $37.5 million, and adjusted EPS was $0.39 for both 4Q24 and 4Q23.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The Three Projects Will Include an 80 Story High-Rise Building in the Miami Brickell District at 1040 South Miami Ave, Two Buildings in Clearwater Beach, and a Project in Jupiter Florida, Totaling Over 400 High-End Luxury Units

SKYX is Expected to Supply Forte Development with Over 12,000 Smart and Plug & Play Products Across Three Luxury Projects, Including Ceiling Outlet Receptacles, Lighting, Ceiling Fans, Recessed Lights, EXIT Signs, Emergency Lights, Downlights, and Indoor/Outdoor Wall Lights

SKYX’s Technologies Provide Opportunities for Recurring Revenues Through Upgrades, Interchangeability, Monitoring and Subscriptions and More

MIAMI, Feb. 20, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive smart platform technology company with more than 97 issued and pending patents globally and over 60 lighting and home décor websites, announces that it will start supplying its technologies to Forte Developments’ upcoming high-end luxury projects, including an 80-story building in Miami located at the Brickell district, two buildings in Clearwater Beach and a project in Jupiter, Florida.

Forte Developments is a leading high-end luxury condo and home development company. Forte’s developments include well-known luxury buildings in Palm Beach and Miami, Florida, as well as in The Hamptons, New York, among others.

During the course of the three projects, SKYX is expected to deliver over 12,000 of its products, representing a variety of its advanced and smart platform technology plug & play platform products. SKYX is expected to start supplying its products during the second half of 2025.

Marius Fortelni CEO and Founder of Forte Developments said: “We are excited to develop our ultra-high-end luxury upcoming projects utilizing SKYX’s game-changing advanced, smart, and safe plug and play technologies. I strongly believe that SKYX’s disruptive ceiling platform technologies will become the standard for new construction as they provide smart capabilities, safety and time savings, while adding significant value to our homes and buildings.” Link to Forte’s website here: https://fortedevelopmentus.com/

Rani Kohen, Founder/Inventor and Executive Chairman, of SKYX Platforms, said: “We are excited to work with a high-end condo developer such as Forte Developers. This is another step toward our goal of making homes and buildings become advanced, safe, and smart as the new standard. We look forward to continuing to demonstrate our advanced smart platform technology’s ability to make homes and buildings become smart and safe instantly, while significantly advancing buildings and saving time and cost to developers.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

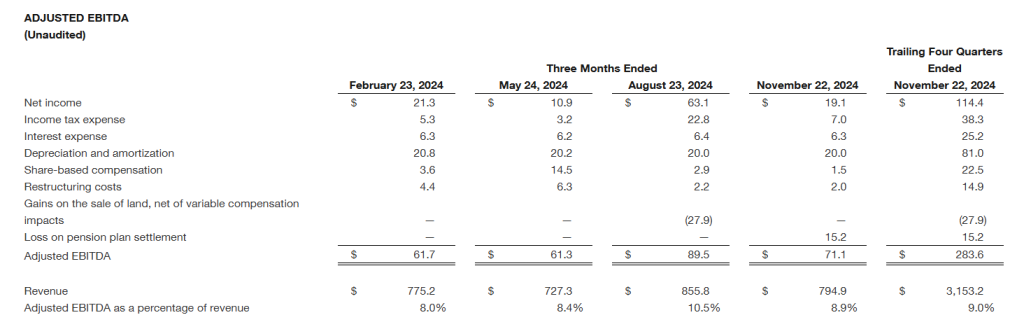

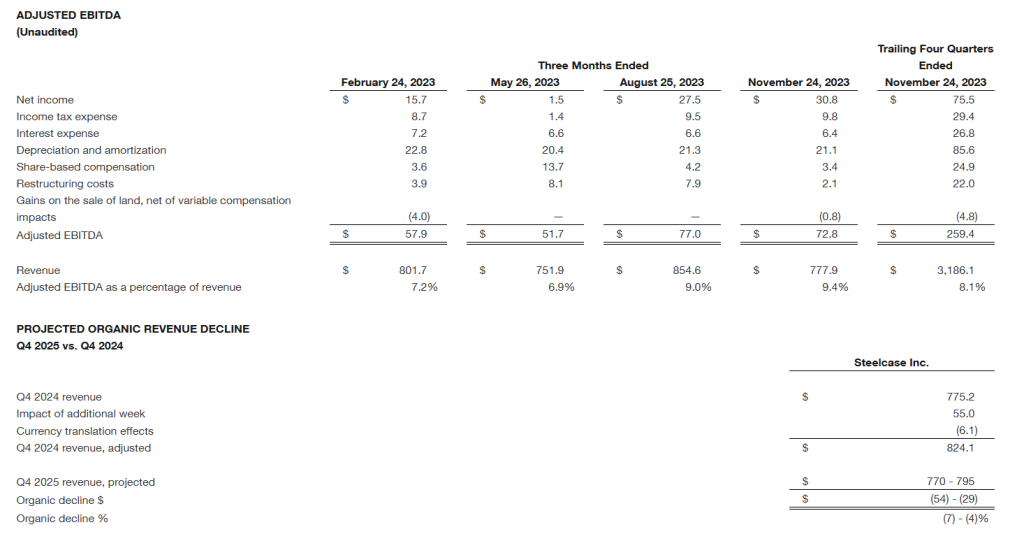

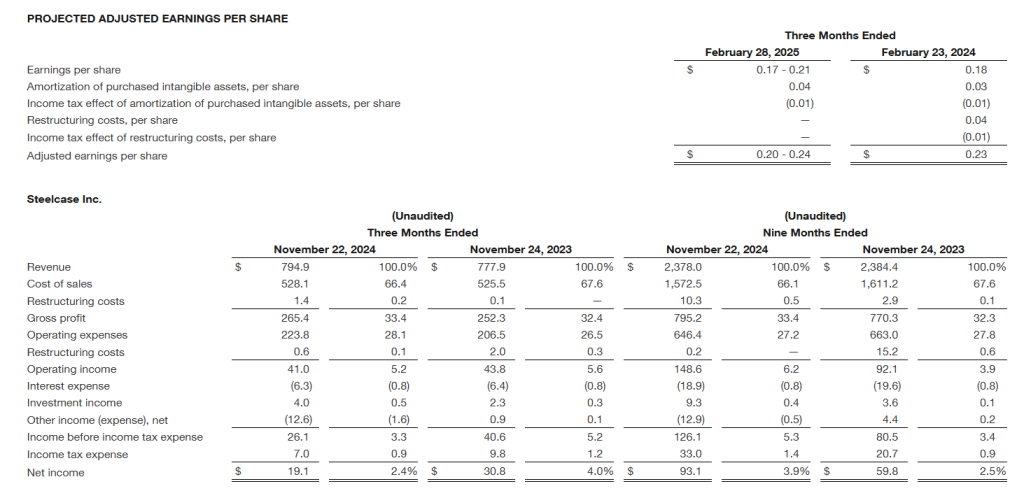

Revenue growth of 2% driven by 5% growth in the Americas

Gross margin improvement of100 basis points

Total liquidity strengthened by $152 million

Americas posted order growth of 2% compared to prior year

Outlook for fiscal 2025 adjusted earnings per share exceeds company targets

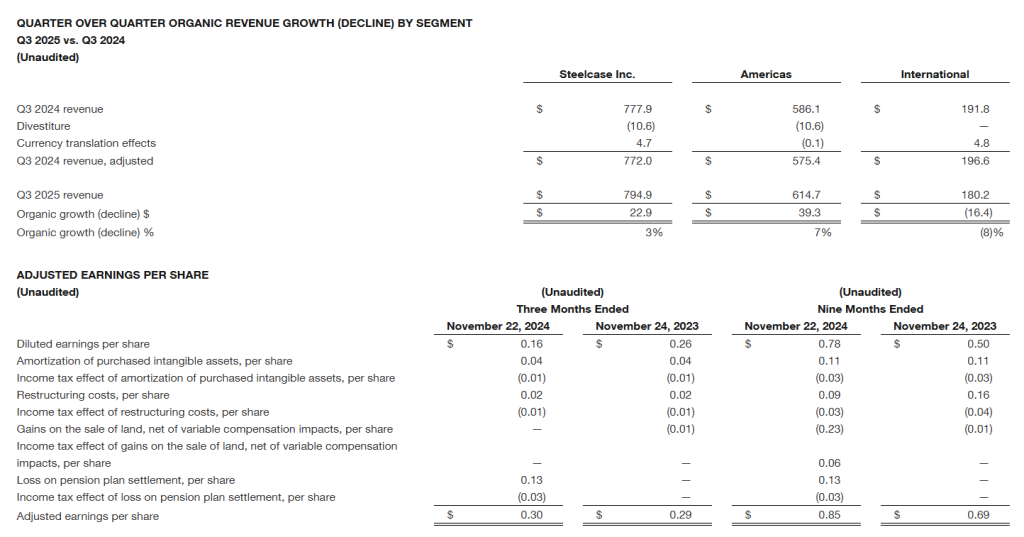

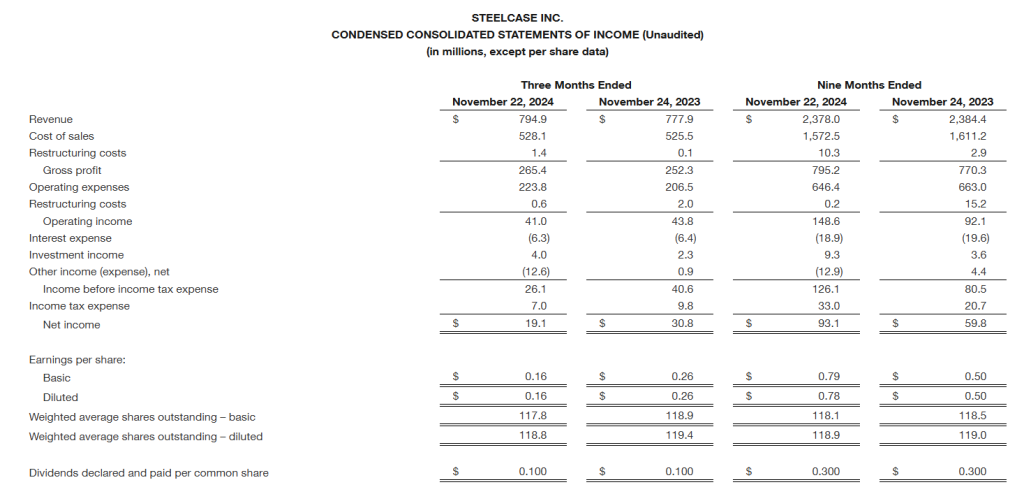

GRAND RAPIDS, Mich., Dec. 18, 2024 (GLOBE NEWSWIRE) — Steelcase Inc. (NYSE: SCS) today reported third quarter revenue of $794.9 million, net income of $19.1 million, or $0.16 per share, and adjusted earnings per share of $0.30. In the prior year, Steelcase reported revenue of $777.9 million and net income of $30.8 million, or $0.26 per share, and had adjusted earnings per share of $0.29.

Revenue and order growth (decline) compared to the prior year were as follows:

Revenue grew 2 percent in the third quarter compared to the prior year, with 5 percent growth in the Americas and a 6 percent decline in International. On an organic basis, revenue grew 3 percent, with 7 percent growth in the Americas and an 8 percent decline in International. The Americas growth benefited from a higher percentage of the beginning backlog shipping during the quarter compared to the prior year and included higher revenue from government, large corporate, healthcare and education customers, while the International decline was driven by most markets in Asia Pacific, except India, and France.

Orders (adjusted for the impact of a divestiture and currency translation effects) declined modestly in the third quarter compared to the prior year, and included 2 percent growth in the Americas and an 8 percent decline in International. The order growth in the Americas was driven by government customers. Orders from large corporate customers strengthened in the last month of the quarter, but modestly declined overall in the third quarter compared to the prior year. The order decline in International was driven by most markets in Asia Pacific and France, net of growth in Germany and some smaller markets in EMEA.

“Our Americas business posted 7% organic revenue growth this quarter driven by growth across many of our customer segments, and we delivered higher than expected adjusted earnings per share,” said Sara Armbruster, president and CEO. “As we continue to focus on serving our customers and supporting their workplace strategies, we posted another quarter of order growth in the Americas, and we are pleased with the improved trends we saw from our large corporate customers near the end of the quarter and into December.”

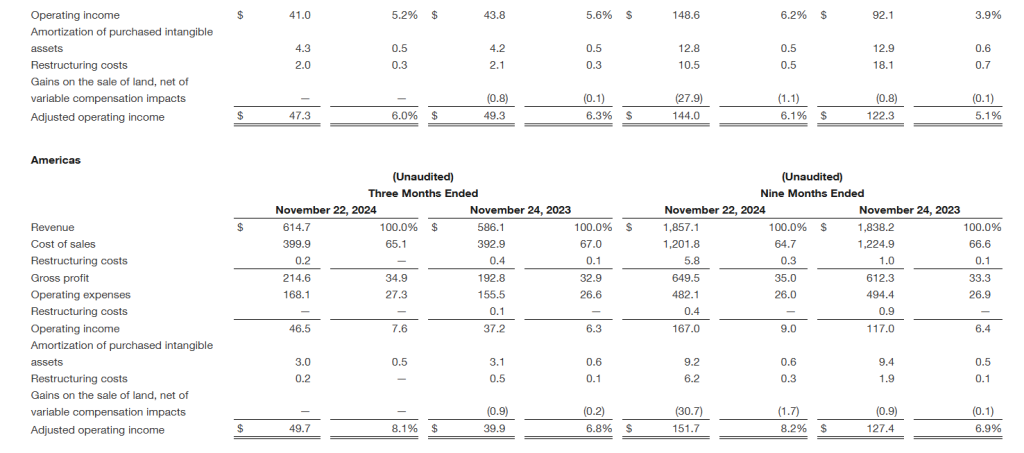

Operating income (loss) and adjusted operating income (loss) were as follows:

Operating income of $41.0 million in the third quarter represented a decrease of $2.8 million compared to the prior year. The prior year included a $9.5 million benefit from a decrease in the valuation of an acquisition earnout liability and $5.4 million of gains on the sale of fixed assets, including land, in the Americas. The current year included the benefits of higher revenue and gross margin in the Americas compared to the prior year. Adjusted operating income of $47.3 million in the third quarter represented a decrease of $2.0 million compared to the prior year.

“Our International results in the third quarter were below our expectations and were impacted by demand and some customer-driven shipment delays,” said Dave Sylvester, senior vice president and CFO. “We implemented additional restructuring actions and other cost reduction measures during the third quarter, which together are projected to drive approximately $5 million of annualized cost savings by the start of fiscal 2026. Also, we are encouraged by higher project activity levels from some of our global customers in our international markets and recent wins related to large opportunities with national accounts in France, Germany and the Middle East.”

Gross margin of 33.4 percent in the third quarter represented an improvement of 100 basis points compared to the prior year driven by the benefits of revenue growth in the Americas and cost reduction initiatives, including savings from our previously announced restructuring actions.

Operating expenses of $223.8 million in the third quarter represented an increase of $17.3 million compared to the prior year. The prior year included favorable impacts of a $9.5 million decrease in the valuation of an acquisition earnout liability and $5.4 million of gains on the sale of fixed assets, including land. The remaining increase was driven by $6.0 million of higher employee costs, partially offset by a $4.4 million decrease from a divestiture.

Other expense, net of $12.6 million in the third quarter included a $15.2 million non-cash charge related to the annuitization of a pension plan.

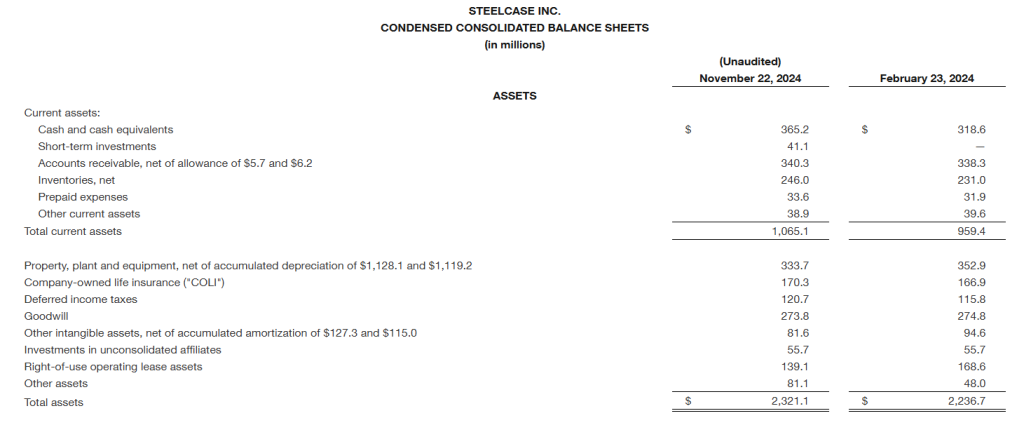

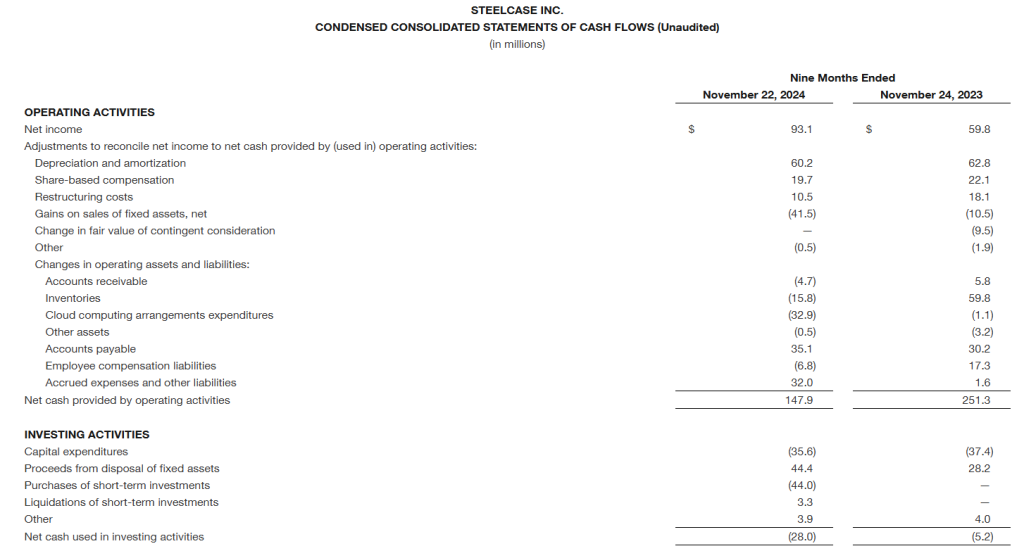

Total liquidity, which is comprised of cash and cash equivalents, short-term investments and the cash surrender value of company-owned life insurance, aggregated to $576.6 million at the end of the third quarter and represented an increase of $152.0 million compared to the prior year. Total debt was $446.9 million. Trailing four quarter adjusted EBITDA of $283.6 million (or 9.0 percent of revenue) represented an increase of 9 percent compared to the prior year.

The Board of Directors has declared a quarterly cash dividend of $0.10 per share, to be paid on or before January 13, 2025, to shareholders of record as of December 30, 2024.

Outlook

At the end of the third quarter, the company’s backlog was approximately $664 million, which was 5 percent lower than the prior year. Orders in the first three weeks of the fourth quarter grew 15 percent compared to the prior year and included a number of large projects scheduled to ship beyond the end of the quarter. The company expects fourth quarter fiscal 2025 revenue, which contains an additional week compared to the prior year, to be in the range of $770 to $795 million. The company reported revenue of $775.2 million in the fourth quarter of fiscal 2024. The projected revenue range translates to a decline of 1 percent to growth of 3 percent compared to the prior year, or a decline of 4 to 7 percent on an organic basis.

The company expects to report earnings per share of between $0.17 to $0.21 for the fourth quarter of fiscal 2025 and adjusted earnings per share of between $0.20 to $0.24. The company reported earnings per share of $0.18 and adjusted earnings per share of $0.23 in the fourth quarter of fiscal 2024.

The fourth quarter estimates include:

gross margin of approximately 33.5 percent,

projected operating expenses of between $230 to $235 million, which includes $4.3 million of amortization of purchased intangible assets,

projected interest expense, net of investment income and other income, net, of approximately $1 million and

a projected effective tax rate of approximately 27 percent.

“As work and work patterns continue to change, we remain focused on developing new solutions and evolving our capabilities to better serve our customers and dealers,” said Sara Armbruster. “Our teams have successfully driven higher levels of profitability all year and we are pleased that our fiscal 2025 adjusted earnings per share are projected to finish above our target.”

Business Segment Footnotes

The Americas segment serves customers in the U.S., Canada, the Caribbean Islands and Latin America with a comprehensive portfolio of furniture, architectural, textile and surface imaging products that are marketed to corporate, government, healthcare, education and retail customers primarily through the Steelcase, AMQ, Coalesse, Designtex, HALCON, Orangebox, Smith System and Viccarbe brands.

The International segment serves customers in EMEA and Asia Pacific with a comprehensive portfolio of furniture and architectural products that are marketed to corporate, government, healthcare, education and retail customers primarily through the Steelcase, Coalesse, Orangebox, Smith System and Viccarbe brands.

Webcast

Steelcase will discuss third quarter results and business outlook on a conference call at 8:30 a.m. Eastern time tomorrow. Listeners may access the conference call at http://ir.steelcase.com.

Non-GAAP Financial Measures

This earnings release contains certain non-GAAP financial measures. A “non-GAAP financial measure” is defined as a numerical measure of a company’s financial performance that excludes or includes amounts so as to be different than the most directly comparable measure calculated and presented in accordance with GAAP in the condensed consolidated statements of income, balance sheets or statements of cash flows of the company. The non-GAAP financial measures used are (1) organic revenue growth (decline), (2) adjusted operating income (loss), (3) adjusted earnings per share and (4) adjusted EBITDA. Pursuant to the requirements of Regulation G, the company has provided a reconciliation of each of the non-GAAP financial measures to the most directly comparable GAAP financial measure in the tables above. These measures are supplemental to, and should be used in conjunction with, the most comparable GAAP measures. Management uses these non-GAAP financial measures to monitor and evaluate financial results and trends.

Organic Revenue Growth (Decline)

The company defines organic revenue growth (decline) as revenue growth (decline) excluding the impact of acquisitions and divestitures and foreign currency translation effects. Organic revenue growth (decline) is calculated by adjusting prior year revenue to include revenues of acquired companies prior to the date of the company’s acquisition, to exclude revenues of divested companies and to use current year average exchange rates in the calculation of foreign-denominated revenue. The company believes organic revenue growth (decline) is a meaningful metric to investors as it provides a more consistent comparison of the company’s revenue to prior periods as well as to industry peers.

Adjusted Operating Income (Loss) and Adjusted Earnings Per Share

The company defines adjusted operating income (loss) as operating income (loss) excluding amortization of purchased intangible assets, restructuring costs (benefits) and gains (losses) on the sale of land, net of variable compensation impacts. The company defines adjusted earnings per share as earnings per share excluding amortization of purchased intangible assets, restructuring costs (benefits), gains (losses) on the sale of land, net of variable compensation impacts, and gains (losses) on pension plan settlements, and the related income tax effects of these items.

Amortization of purchased intangible assets: The company may record intangible assets (such as backlog, dealer relationships, trademarks, know-how and designs and proprietary technology) when it acquires companies. The company allocates the fair value of purchase consideration to net tangible and intangible assets acquired based on their estimated fair values. The fair value estimates for these intangible assets require management to make significant estimates and assumptions, which include the useful lives of intangible assets. The company believes that adjusting for amortization of purchased intangible assets provides a more consistent comparison of its operating performance to prior periods as well as to industry peers.

Restructuring costs (benefits): Restructuring costs (benefits) may be recorded as the company’s business strategies change or in response to changing market trends and economic conditions. The company believes that adjusting for restructuring costs (benefits), which are primarily associated with business exit and workforce reduction costs, provides a more consistent comparison of its operating performance to prior periods as well as to industry peers.

Gains (losses) on the sale of land, net of variable compensation impacts: We may sell land when conditions are favorable. Gains and losses on the sale of land may increase or decrease, respectively, our variable compensation expense. We believe adjusting for these items provides a more consistent comparison of our operating performance to prior periods as well as to industry peers. In Q2 2025, we began adjusting for these items, as we realized a significant gain on the sale of land during the quarter which had a significant impact on our variable compensation expense, and we have adjusted the prior periods presented for consistency and comparability.

Gains (losses) on pension plan settlements: We realize gains or losses previously reported as unrealized in Accumulated other comprehensive income (loss) in Other income (expense), net, in connection with pension plan settlements when all risks related to the benefit obligations to plan participants and plan assets are transferred. We believe adjusting for the gains or losses on pension plan settlements provides a more consistent comparison of our operating performance to prior periods as well as to industry peers.

Adjusted EBITDA

The company defines adjusted EBITDA as earnings before interest, taxes, depreciation and amortization (“EBITDA”) adjusted to exclude share-based compensation, restructuring costs (benefits), gains (losses) on the sale of land, net of variable compensation impacts, and gains (losses) on pension plan settlements. The company believes adjusted EBITDA provides investors with useful information regarding the operating profitability of the company as well as a useful comparison to other companies. EBITDA is a measurement commonly used in capital markets to value companies and is used by the company’s lenders and rating agencies to evaluate its performance. The company adjusts EBITDA for share-based compensation as it represents a significant non-cash item which impacts its earnings. The company also adjusts EBITDA for restructuring costs, gains (losses) on the sale of land, net of variable compensation impacts, and gains (losses) on pension plan settlements to provide a more consistent comparison of its earnings to prior periods as well as to industry peers.

Forward-looking Statements

From time to time, in written and oral statements, the company discusses its expectations regarding future events and its plans and objectives for future operations. These forward-looking statements discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition, or state other information relating to the company, based on current beliefs of management as well as assumptions made by, and information currently available to, the company. Forward-looking statements generally are accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “target” or other similar words, phrases or expressions. Although the company believes these forward-looking statements are reasonable, they are based upon a number of assumptions concerning future conditions, any or all of which may ultimately prove to be inaccurate. Forward-looking statements involve a number of risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements and vary from the company’s expectations because of factors such as, but not limited to, competitive and general economic conditions domestically and internationally; acts of terrorism, war, governmental action, natural disasters, pandemics and other Force Majeure events; cyberattacks; changes in the legal and regulatory environment; changes in raw material, commodity and other input costs; currency fluctuations; changes in customer demand; and the other risks and contingencies detailed in the company’s most recent Annual Report on Form 10-K and its other filings with the Securities and Exchange Commission. Steelcase undertakes no obligation to update, amend, or clarify forward-looking statements, whether as a result of new information, future events, or otherwise.

About Steelcase Inc.

Established in 1912, Steelcase is a global design, research and thought leader in the world of work. We help people do their best work by creating places that work better. Along with more than 30 creative and technology partner brands, we design and manufacture furnishings and solutions for the many places where work happens – including learning, health and work from home. Our solutions come to life through our community of expert Steelcase dealers in approximately 770 locations, as well as our online Steelcase store and other retail partners. Founded in Grand Rapids, Michigan, Steelcase is a publicly traded company with fiscal year 2024 revenue of $3.2 billion. With approximately 11,300 global employees and our dealer community, we come together for people and the planet – using our business to help the world work better.

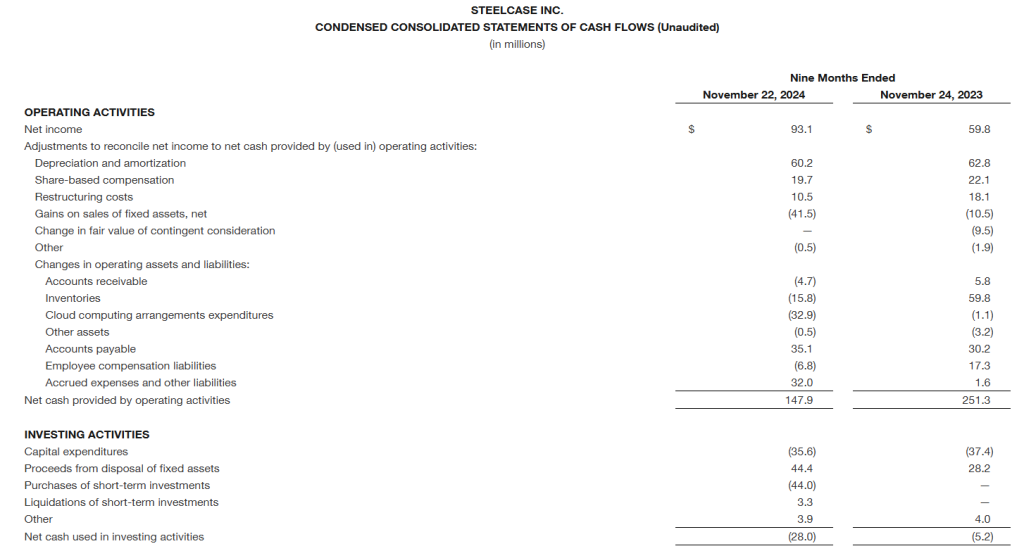

(1) These amounts include restricted cash of $7.3 and $6.8 as of February 23, 2024 and February 24, 2023, respectively.

(2) These amounts include restricted cash of $7.2 and $7.1 as of November 22, 2024 and November 24, 2023, respectively.

Restricted cash primarily represents funds held in escrow for potential future workers’ compensation and product liability claims. The restricted cash balance is included as part ofOther assetson the Condensed Consolidated Balance Sheets.

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on March 26, 2025 to stockholders of record as of the close of business on March 14, 2025.

“This is the Company’s 29th quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy, and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving an approximate 6% yield on their investment,” said Tom Tedford, President, and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn and play. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

NEW ALBANY, Ohio, Feb. 13, 2025 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI), a diversified industrial products and services company, is pleased to announce the appointment of Scott Reed as Chief Operating Officer, effective February 13, 2025. Mr. Reed comes to CVG with more than 30 years of diverse business and leadership experience in industrial and manufacturing organizations.

In his new role, Mr. Reed will oversee the global manufacturing and supply chain operations of the company, driving operational excellence and strengthening cross-functional alignment across planning and execution, ensuring that our operational processes are aligned with our strategic goals. He will report to James Ray, President and CEO of CVG, and serve on the executive leadership team.

“We are thrilled to welcome Scott to our executive leadership team,” said Mr. Ray. “His extensive background in operations and strategic leadership aligns perfectly with our mission to optimize our business operations and enhance our value proposition. We believe Scott’s vision and expertise will accelerate our growth and help us to deliver outstanding results.”

Before joining CVG, Mr. Reed served as President of Arrow Tru-Line Inc., the largest manufacturer and supplier of structural hardware components to the North American residential and commercial overhead garage door market. He also held operations leadership roles at Peterson Spring, Unique Fabricating, Inc., GT Technologies, Inc. and Lear Corporation. He is recognized for his ability to deliver year-over-year success in achieving operational, profit, and business growth objectives, as well as building, motivating, and leading culturally diverse worldwide operating teams.

“I am excited to join CVG and look forward to working with the team to drive continued operational excellence across our global operations footprint,” said Mr. Reed. “I am confident that together we will continue to strengthen the company’s position in the market and achieve success.”

Mr. Reed holds a bachelor’s degree in business administration from Cleary University.

As a material inducement to Mr. Reed joining the Company, the Compensation Committee of the Board of Directors approved the grant of the following inducement equity awards (collectively, the Inducement Awards), granted outside the Company’s stockholder-approved 2020 equity incentive plan: (i) 58,331 shares of time-vesting restricted stock, which will vest ratably on March 31, 2026, 2027 and 2028; and (ii) 87,497 performance shares, that will vest and be paid in cash if performance metrics are met, aligning the interests of Mr. Reed with the interests of the Company’s shareholders.

In addition to welcoming Mr. Reed, the Company is announcing the departure of Don Fishel, President, Trim Systems and Components, after 14 years with CVG. “We are grateful for Don’s leadership and contributions during his time at CVG,” said Mr. Ray. “He played an integral role in CVG’s growth and success, and we wish him well in his future endeavors. We are confident that the leadership team will continue to drive our company forward as we execute our vision and strategy.”

We expect to conduct a search for a new permanent leader for our Trim Systems and Components business. In the interim, Andy Cheung will oversee the Trim Systems and Components business, in addition to his current CFO responsibilities.

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about CVG and its products is available at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 12, 2025– The ODP Corporation (NASDAQ:ODP) (“ODP,” or the “Company”), a leading provider of products, services, and technology solutions to businesses and consumers, will announce fourth quarter and full year 2024 financial results before the market open on Wednesday, February 26th, 2025. The ODP Corporation will webcast a call with financial analysts and investors that day at 9:00 am Eastern Time which will be accessible to the media and the general public.

To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event. A copy of the earnings press release, supplemental financial disclosures and presentation will also be available on the website.

About The ODP Corporation The ODP Corporation (NASDAQ:ODP) is a leading provider of products and services through an integrated business-to-business (B2B) distribution platform and omnichannel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, online presence and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; and Veyer, LLC, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

ODP and ODP Business Solutions are trademarks of ODP Business Solutions, LLC. Office Depot is a trademark of The Office Club, LLC. OfficeMax is a trademark of OMX, Inc. Veyer is a trademark of Veyer, LLC. Grand&Toy is a trademark of Grand & Toy, LLC in Canada. Any other product or company names mentioned herein are the trademarks of their respective owners.

Key Points: – The Consumer Price Index (CPI) increased 3% year-over-year in January, exceeding expectations and accelerating from December’s 2.9%. – Rising energy costs and food prices, particularly eggs, contributed to the largest monthly headline increase since August 2023. – The Federal Reserve faces challenges in determining interest rate cuts, as inflation remains above its 2% target.

Newly released inflation data for January revealed that consumer prices rose at a faster-than-expected pace, complicating the Federal Reserve’s path forward. The Consumer Price Index (CPI) increased by 3% over the previous year, ticking up from December’s 2.9% annual gain. On a monthly basis, prices climbed 0.5%, marking the largest monthly increase since August 2023 and outpacing economists’ expectations of 0.3%.

Energy costs and persistent food inflation played a significant role in driving the index higher. Egg prices, in particular, surged by a staggering 15.2% in January—the largest monthly jump since June 2015—contributing to a 53% annual increase. Meanwhile, core inflation, which excludes volatile food and energy prices, rose 0.4% month-over-month, reversing December’s easing trend and posting the biggest monthly rise since April 2023.