How to Play and Win the Gift-Stealing Game Bad Santa, According to a Mathematician

Christmas comes but once a year – as do Christmas party games. With such little practice it’s hard to get good at any of them.

Let me help. I’m going to share with you some expert tips, tested through mathematical modelling, on how to win one of the most popular games: Bad Santa – also known as Dirty Santa, White Elephant, Grab Bag, Yankee Swap, Thieving Secret Santa, or simply “that present-stealing game”.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Joel Gilmore, Associate Professor, Griffith University.

This isn’t advice on being a bad sport. It’s about being a good Bad Santa – which is the name of the game. You might even come away with a good gift and bragging rights.

How Bad Santa Works

Bad Santa is a variation of the classic Kris Kringle (or Secret Santa) game, in which each guest receives an anonymous gift bought by another guest. Part of the fun (for others) is the unwrapping of silly and useless gifts, which is done one by one.

Bad Santa spices things up. All the gifts are pooled. Guests take turns to choose one to unwrap. Or they can choose to “steal” a gift already opened by someone else. The person losing their gift then gets the same choice: open a wrapped present or steal someone else’s.

It’s a good alternative to buying a gift for everyone, and a great way to ruin friendships.

The order of players is usually determined by drawing numbers from a hat. This is important, because you’ve probably already noted the disadvantage of going first and the benefit of going last. The right rules can mitigate this. There are at least a dozen different versions of this game published online, and some are much less fair than others.

How I Tested Bad Santa

The best way to test Bad Santa rule variations and playing strategies would be to observe games in real life – say, by attending 1,000 Christmas parties (funding bodies please call me).

I did the next best thing, deploying the same type of computer modelling (known as agent-based modelling) used to understand everything from bidding in electricity markets to how the human immune system works.

In my model there are 16 virtual guests and 16 gifts. Each has different present preferences, rating opened gifts on a scale of 1 to 10. They will steal a gift they rate better than a 5. To make it interesting, three gifts are rated highly by everyone and there are three no one really wants – probably a novelty mug or something.

After simulating 50,000 games with different rules, I’ve found a set of rules that seems the most fair, no matter what number you draw from the hat.

Choosing the Fairest Rules

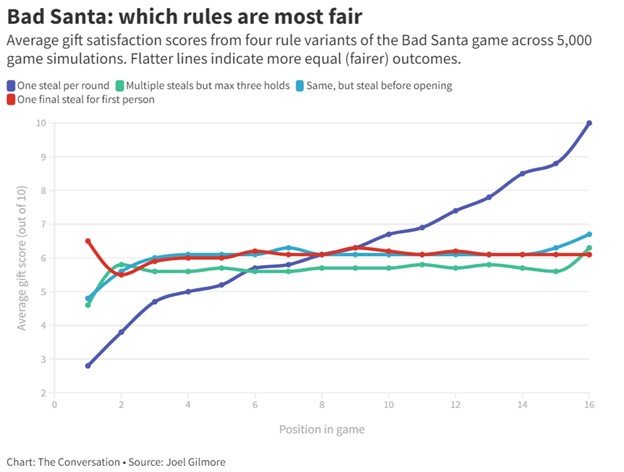

The following graph shows the results for four different game variations.

The higher the line, the greater the overall satisfaction. The flatter the lines, the fairer the result. (If gifts were chosen randomly with no stealing, every player’s average satisfaction score would be 5).

The most unfair result comes from the “dark blue rules”, which stipulate that any gift can only be stolen once in any round. This mean if you’re the last person, you’ve got the biggest choice and get to keep what you steal. If you go first, you’re bound to lose out.

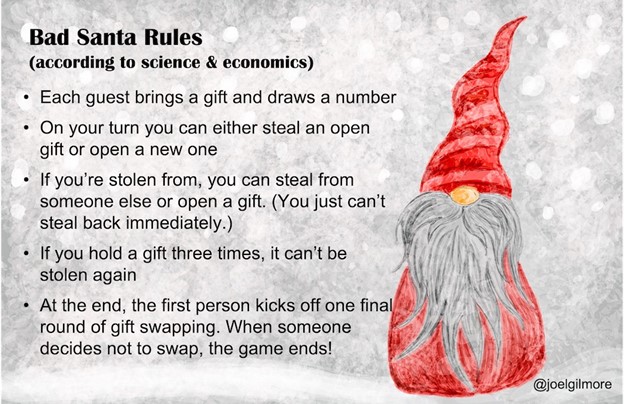

Fairest and Best Bad Santa Rules

The most fair outcomes come from the “red rules”:

- A gift can be stolen multiple times each turn. This keeps presents moving between guests, which adds to the fun.

- Once a person holds the same gift three times it becomes “locked”, and can no longer be stolen. This evens the game out a lot. Later players still see more gifts, but earlier players have more chance to lock the gift they want. It also ensures games don’t go on for hours.

- After the last player’s turn, there is one more round of stealing, starting with the very first player. This also gives them a chance to steal at least once – and a slight advantage. But overall, these rules provide the most even outcomes.

Like most games, the rules are’t perfect. But the maths shows they are better than the alternatives. If you want to test other scenarios using my model, you can download my source code here.

On your turn you can either steal an open gift or open a new one If you’re stolen from, you can steal from someone else or open a gift. If you hold a gift three times, it is locked. First person gets a final steal.

Three Tips on Game Strategy

The right rules help level the playing field. They don’t eliminate the need for strategic thinking to maximise your chance to get a gift you want.

As in real life, seemingly fair rules can be manipulated.

One thing you could do is team up with other players to manipulate the “three holds and locked” rule. To do this, you’ll need at least two co-conspirators.

Say your friends Donner and Blitzen have their preferred gifts, and now it’s your turn. You steal Blitzen’s gift. Blitzen in turn steals Donner’s, who steals yours, and so on. Donner and Blitzen end up holding their chosen gifts a second time, then a third. You helped them out, and then can choose another gift.

In competitive markets this type of co-operation is usually know as collusion – and it’s illegal. In sport, it would simply be called cheating. So I’m not saying you should do this; I am merely explaining how the strategy works. If you do this and end up on the naughty list, don’t blame me.

I haven’t yet tested rules variations in my model to see how this collusion can best be eliminated or minimised. Maybe by next Christmas. (Or maybe not – for me, cheating through maths is half the fun of the game.)

So let me leave you with two perfectly legitimate strategies.

First, and most obviously, you must steal gifts!

My modelling quantifies how necessary this is. I simulated a game in which four guests will never steal a gift. Those guests are 75% less satisfied with their final gifts than the players who do steal. They’re also much less fun at parties.