Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Senior Vice President – Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Battery recycling facility sale. Comstock’s LINICO subsidiary recently entered into amended and restated agreements to sell its battery recycling facility in the Tahoe Reno Industrial Center to American Battery Technology Corporation (OTCQX: ABML) for $27 million. Of the purchase price, $1.5 million will be held in escrow for up to 18 months. LINICO had leased the facility with an option to purchase for $15.25 million, of which $3.25 million was paid. The transaction contemplates Comstock would buy out the lease prior to closing the transaction in the second quarter.

Sale results in net cash inflows. On March 1, Comstock received $6 million from the sale of equipment associated with the agreement. On April 6, the company received $5 million in cash and 10 million restricted shares of American Battery Technology Corporation stock with the guarantee that Comstock will receive additional cash and/or shares if the proceeds for the shares are less than $6.6 million. Comstock will receive an additional $10 million in cash on or before April 21. We have updated our financial model to reflect expected cash flows, including an estimated net accounting gain of ~$5 million on the income statement in the second quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Vice President – Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

The Lost Cities project. Aurania’s Lost Cities project is in the Cordillera de Cutucu range of Ecuador which represents the relatively unexplored extension of a rich mineral belt that is believed to run through the Cordillera del Condor range to the south; an area that has been more widely explored and the source of several major gold and copper discoveries. The project is comprised of 42 mineral exploration concessions encompassing 207,764 hectares in southeastern Ecuador and would be difficult to replicate. To date, Aurania’s exploration and drilling activities have underscored its rich mineral potential for epithermal gold-silver, copper porphyries, sedimentary-hosted copper-silver, and carbonate-replacement silver-zinc-lead-barite.

Private placement financing. In March, Aurania closed the first tranche of its private placement of up to 10,869,565 units for gross proceeds of up to C$5,000,000 with the right to increase the size of the initial offering by up to 25%. A total of 7,801,145 units were sold in the first tranche at a price of C$0.46 per unit for gross proceeds of C$3,588,526.70. Proceeds funded annual concession fees to renew the Lost Cities project mineral concessions. We expect Aurania to close the second and final tranche shortly.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

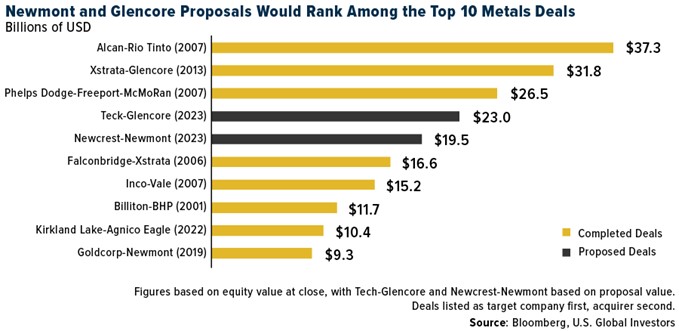

Is This The Start Of A New Golden Age Of Gold Mining Deals?

We may be about to enter a new golden age of gold mining deals as explorers and producers seek to capitalize on higher metal prices and gain exposure to other key minerals, including copper, at a time when consolidation in the gold industry vastly trails that of other metals.

Last week, major U.S. gold producer Newmont raised its bid for Australian rival Newcrest Mining to $19.5 billion after its earlier bid of $17 billion was rejected. Due diligence is expected to take around four weeks, and if Newcrest’s board and shareholders accept the offer, the acquisition would represent one of the top 10 biggest metal deals ever and the single biggest gold mining takeover, nearly twice the value of last year’s merger between Kirkland Lake and Agnico Eagle.

(A note about the chart above: Just today, Teck Resources rejected Glencore’s $23 billion takeover bid, calling it “opportunistic and unrealistic.” Vancouver-based Teck says it will proceed with plans to spin off its steelmaking coal business, creating two new companies: Teck Metals and Elk Valley Resources. This separation “creates a significantly greater spectrum of opportunities to maximize value for Teck shareholders” compared to an acquisition by Glencore, says Teck’s Board of Directors Chair Sheila Murray.)

This article was republished with permission from Frank Talk, a CEO Blog by Frank Holmes

Time will tell if Newcrest approves of Newmont’s offer, but I believe this could be the start of a much-needed consolidation cycle in the gold industry, one that could potentially benefit shareholders.

Gold Is One Of The Most Fragmented Gold Mining Industries

Back in 2019, many analysts and market participants—myself included—heralded Newmont and Goldcorp’s $9.3 billion merger as the beginning of a new era of gold consolidation, and I believe the Newmont-Newcrest deal could serve as a (delayed) continuation of the trend.

The truth is that, compared to other important metals, gold is sorely in need of consolidation. The chart below, courtesy of metals and mining consultancy firm CRU Group, shows the global share of output from each metal’s top 10 producers. Gold is at the bottom, with its top 10 producers responsible for only 28% of global output. By comparison, the top 10 iron ore producers generate nearly 70% of the world’s supply.

Higher gold prices in recent years have not resulted in significantly increased exploration spending. In lieu of that, companies can expand and create shareholder value through mergers and acquisitions (M&A), which allow miners to “increase their production share, replenish depleting gold reserves and… lower production costs through relatively less risk,” writes CRU analysts.

Copper To Face Ongoing Supply Deficits

M&A can also result in metal diversification—one of Newmont’s stated goals in acquiring Newcrest. Copper currently accounts for roughly 25% of Newcrest’s total net revenue, and the company hopes to increase it to 50% of revenue by the end of the decade. As one of the key minerals in the global transition to renewable energy, copper is poised to surge in price in the coming years as demand far outpaces supply.

In fact, copper mining deals exceeded gold mining deals in total value last year, according to a new report by S&P Global. M&A work among copper companies in 2022 totaled more than $14 billion in value, a 103% jump over the previous year, while the combined value of gold deals stood at $9.8 billion, a 48% decrease from 2021.

US Global Investors Disclaimer

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. Free cash flow (FCF) represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2021): Torex Gold Resources Inc., Centerra Gold Inc., Gran Colombia Gold Corp., Dundee Precious Metals Inc., Pretium Resources Inc., Endeavour Mining PLC, Barrick Gold Corp., Eldorado Gold Corp., SSR Mining Inc., Silver Lake Resources Ltd., Karora Resources Inc.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Toronto, Ontario, April 13, 2023 – Aurania Resources Ltd. (TSXV: ARU; OTCQB: AUIAF; Frankfurt: 20Q) (“Aurania” or the “Company”) is pleased to announce its proposed 2023 exploration activities.

As the concessions for its mineral properties in Ecuador are fully renewed and in good standing for another year after payment of all concession fees in March, the Company is able to develop the 2023 exploration programs.

Aurania attended the Prospector’s and Developer’s Association of Canada meeting (PDAC) in Toronto the first week of March, and we were delighted by the interest shown by several Major companies in our Ecuador asset. As a result of follow-up meetings there are now several companies in our data room. The primary interest has been in our porphyry copper and sediment-hosted copper-silver prospects.

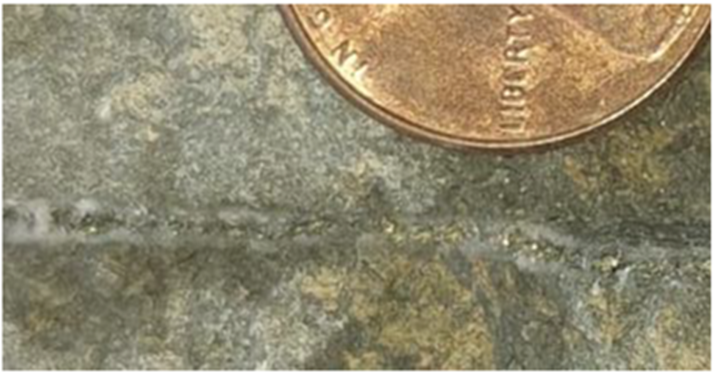

To date, approximately 45% of the Awacha Porphyry Target has been covered by “Anaconda-style Mapping”. This is an intensive mapping technique that was originally developed by the famous Anaconda Copper Company, and has been taught to the Aurania geological staff by consultant Dr. Steve Garwin. This target is approximately 11 km x 5 km in size and was discovered by stream sediment sampling which showed elevated copper and molybdenum in the vicinity of two strong airborne magnetic anomalies. This size is significantly larger than any copper porphyry known and so our working hypothesis is that it is a cluster of porphyries, and similar to the Warintza cluster to the south of our concessions. Intrusive rock types from gabbro to diorite to monzonite and syenite have been mapped. Many of these intrusives show secondary biotite (potassic) alteration and fine quartz veins containing molybdenite or a centre line of chalcopyrite. These so called distinctive “B veins” are classic evidence of mineralized porphyry systems. An independent explanation of B veins can be found at: https://www.youtube.com/watch?v=gL0WzJ70z3s

Figure 1: Quartz vein with centre line of chalcopyrite, covellite and pyrite. US cent for scale.

Most of the Awacha area is covered by a unit of black shale which obscures the geology except where streams have cut down through the sediments and exposed the porphyry. The area is also covered by thick jungle. Nevertheless, Terraspec Mineral Spectrometer analysis of soils in the southern half of the anomaly indicates chlorite, kaolinite, white micas, dickite and pyrophyllite which are compatible with porphyry-style alteration. The last two minerals are typically found in the upper part of porphyry systems.

Copper soil anomalies are patchy, which is in keeping with soil results seen near outcropping sediment hosted copper elsewhere on the property. It would seem that copper is easily flushed away from surface soils by the significant rainfall in the area. Molybdenum however, which is essentially insoluble and immobile presents a much more coherent group of anomalies. Half of the Awacha target is still to be sampled for soils.

The reinterpretation of the surficial geology and structure in the areas of outcropping sediment-hosted copper-silver and zinc-lead-silver has generated a large number of compelling drill targets (see press release dated October 17, 2022). This copper-silver-zinc system across the concessions is 38 kilometres in lngth and is open to the north over an additional 15 kilometres. We believe this is perhaps one of the best areas of the property to find an economic ore deposit, considering the numerous high assays already yielded to date. A few areas are highlighted for follow-up, but we concede that a comprehensive programme here is more appropriate for a Major mining company partner.

The Tatasham epithermal gold/porphyry copper target is compelling due to the presence of what are believed to be pipe breccias. The area is, however, in steep terrain and the geology is mostly covered by post-mineral sedimentary cover and does not outcrop. Soil samples along the ridgeline above the previous porphyry drilling campaign yielded anomalous antimony, which is a pathfinder element in gold systems. An additional soil survey is required at Tatasham to extend the antimony anomaly that is still open to the north. Intensive mapping and prospecting are required. The discovery of the epithermal system at Tatasham was unexpected, in our pursuit of a copper porphyry target indicated by geophysics. That porphyry target is still valid, but it may lie at considerable depth, or it may lie laterally.

Over the next six months it is intended to finish the Anaconda mapping on Awacha, and bring it to drill readiness. At the same time, Tatasham will be re-examined in the belief that the antimony anomaly in soils may be due to a subcropping mineralized system. The Fruta del Norte gold deposit was discovered by drilling a geochemical anomaly of antimony, arsenic and mercury which had virtually no gold on surface. Aurania is currently investigating the feasibility of conducting an Induced Polarization (IP) geophysical survey at Tatasham and Awacha.

The proposed exploration programmes are dependent on raising further funding. The proceeds of the current private placement (as announced on March 13, 2023 and March 23, 2023) to date, have been applied to concession fees and general and administrative expenses.

Qualified Person

The geological information contained in this news release has been verified and approved by Aurania’s VP Exploration, Mr. Jean-Paul Pallier, MSc. Mr. Pallier is a designated EurGeol by the European Federation of Geologists and a Qualified Person as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and copper in South America. Its flagship asset, The Lost Cities – Cutucu Project, is located in the Jurassic Metallogenic Belt in the eastern foothills of the Andes mountain range of southeastern Ecuador.

Information on Aurania and technical reports are available at www.aurania.com and www.sedar.com, as well as on Facebook at https://www.facebook.com/auranialtd/, Twitter at https://twitter.com/auranialtd, and LinkedIn at https://www.linkedin.com/company/aurania-resources-ltd-.

For further information, please contact:

Carolyn Muir

VP Corporate Development & Investor Relations Aurania Resources Ltd.

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes Aurania’s objectives, goals or future plans, statements, exploration results, potential mineralization, the corporation’s portfolio, treasury, management team and enhanced capital markets profile, the estimation of mineral resources, exploration, timing of the commencement of operations, the Company’s teams being on track ahead of any drill program, the commencement of any drill program and estimates of market conditions. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that, there will be no material adverse change in metal prices, all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things, the ability to anticipate and counteract the effects of COVID-19 pandemic on the business of the Company, including without limitation the effects of COVID-19 on the capital markets, commodity prices supply chain disruptions, restrictions on labour and workplace attendance and local and international travel; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals and copper; and. those risks set out in the Company’s public documents filed on SEDAR. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Vice President – Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase I testing completed. Phase I testing of Defense Metals’ fully integrated pilot plant at SGS Lakefield was successfully completed. During five days of operation, the plant ran continuously over a total run time of 110 hours. The goal of the Phase I program was to test the hydrometallurgical process and identify any changes that might be required prior to a longer test program. Defense Metals and SGS Lakefield confirmed the viability of the process, optimized certain design parameters, and identified areas that will be improved ahead of the Phase II pilot plant run scheduled for late April.

Proving the process works. The pilot plant is being configured to produce a high purity rare earth precipitate suitable as feed stock for a rare earths element (REE) separation plant. The objective of the pilot plant is to demonstrate, at a larger scale, the processing of Wicheeda flotation concentrate to produce rare earths using the acid bake hydrometallurgy process and to collect data for a preliminary feasibility study which is expected to be completed in the first quarter of 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VANCOUVER, BC, April 12, 2023 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company“) (TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce that the Phase I of its hydrometallurgical pilot plant at SGS Lakefield has been successfully completed.

John Goode, Consulting Metallurgist to Defense Metals and who attended the pilot plant, commented:

“This first fully integrated pilot plant demonstration of the proposed Wicheeda hydrometallurgical process delivered exactly what was required of it. We have confirmed the general workability of the process, optimized certain design parameters, and identified areas that will be improved ahead of the Phase II pilot plant. The SGS Lakefield team did an excellent job of construction and operation of the circuit, and their efforts are much appreciated.”

The main objective of Phase I of the pilot plant was to test the flowsheet for operability and identify any changes that might be required before a longer test campaign. During the five days of continuous operation, the parameters for the various unit operations were varied slightly to allow optimization of the circuit ahead of the Phase II pilot plant run scheduled for late-April 2023.

Assays are still being received and evaluation of the results has not yet been finalized. However, to date it can be reported that the extraction of Pr (praseodymium) and Nd (neodymium) from the acid bake calcine was in excess of 90%, the impurity removal circuits were very efficient, and reagent regeneration and water recirculation were effective. Minor changes will be made to the circuit ahead of Phase II and an alternative product precipitant will be used.

Methodology

The fully integrated Pilot Plant included sulphuric acid baking, water leaching, three stages of impurity removal, rare earth precipitation, magnesia regeneration and recycling, and process water recycle. The plant ran continuously and without interruption for 24 h/day over a total run time of 110 hours. Operations were handled by a total of ten SGS technicians and metallurgists on each of two shifts managed by senior day-shift staff.

Qualified Person

The scientific and technical information contained in this news release, as it relates to the metallurgical aspects of the Wicheeda Rare-Earth Project, has been reviewed and approved by John Goode, P. Eng., who is a Qualified Person as defined by National Instrument 43-101 and who has provided the technical information relating to metallurgy in this news release.

About the Wicheeda REE Property

Defense Metals 100% owned, 4,262-hectare (~10,532-acre) Wicheeda Light REE property is located approximately 80 km northeast of the city of Prince George, British Columbia; population 77,000. The Wicheeda REE Project is readily accessible by all-weather gravel roads and is near infrastructure, including hydro power transmission lines and gas pipelines. The nearby Canadian National Railway and major highways allow easy access to the port facilities at Prince Rupert, the closest major North American port to Asia.

The 2021 Wicheeda REE Project Preliminary Economic Assessment technical report (“PEA”) outlined a robust after-tax net present value (NPV@8%) of $517 million and an 18% IRR1. This PEA contemplated an open pit mining operation with a 1.75:1 (waste:mill feed) strip ratio providing a 1.8 Mtpa (“million tonnes per year”) mill throughput producing an average of 25,423 tonnes REO annually over a 16 year mine life. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Light Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Defense Metals is a proud member of Discovery Group. For more information please visit: http://www.discoverygroup.ca/

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, the expected benefits and outcomes of the hydrometallurgical pilot plant, the expected completion of the hydrometallurgical pilot plant and the expected timelines, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration and metallurgical results, risks related to the inherent uncertainty of exploration and development and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological, metallurgical and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

____________________________

1 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Endeavour Silver is a mid-tier precious metals mining company that operates two high-grade, underground, silver-gold mines in Mexico. Endeavour is currently advancing the Terronera mine project towards a development decision, pending financing and final permits and exploring its portfolio of exploration and development projects in Mexico, Chile and the United States to facilitate its goal to become a premier senior silver producer. Our philosophy of corporate social integrity creates value for all stakeholders.

Mark Reichman, Senior Vice President – Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production modestly ahead of our expectations. First quarter 2023silver and gold production amounted to 1,623,545 ounces and 9,342 ounces, respectively, or 2,370,905 ounces on a silver equivalent basis. Silver and gold ounces sold amounted to 1,667,408 ounces and 9,126 ounces, respectively. At quarter-end, Endeavour held 435,722 ounces of silver and 1,263 ounces of gold bullion inventory and 35,347 ounces of silver and 503 ounces of gold in concentrate inventory.

Updating estimates. Endeavour’s 2023 production guidance calls for silver production in the range of 5.7 million to 6.3 million ounces and gold production of 36,000 to 40,000 ounces. We forecast silver and gold production of 6.2 million ounces and 37,633 ounces, respectively. While our revenue and EBITDA estimates increased modestly to $212.1 million and $59.5 million, respectively from $210.8 million and $59.0 million, our quarterly and full earnings per share estimates are unchanged. The increase in our revenue estimate is largely due to higher commodity price assumptions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Vice President – Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Expectations for 2023. In February, Coeur provided 2023 gold and silver production guidance of 320.0 to 370.0 thousand ounces and 10.0 to 12.0 million ounces, respectively. Production is weighted toward the second half of the year due to the impact of the Rochester expansion and higher gold production at Wharf. Operationally, we expect the third quarter to be the company’s strongest based on the Rochester mine’s production profile.

Updating estimates. We have lowered our 2023 EBITDA and EPS estimates to $132.7 million and $(0.23) from $158.1 million and $0.00. We have refined our quarterly production estimates and also raised our cost estimates. We note that the company’s guidance on taxes could result in variances to our EPS estimates. While the company expects first quarter cash taxes in the range of $14 to $18 million, we note that cash taxes paid and recorded income tax expense may differ. We have also adjusted our EBITDA estimate to reflect certain items such as inventory adjustments.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VIRGINIA CITY, NEVADA,April 11, 2023 – Comstock Inc. (NYSE: LODE) (“Comstock” and the “Company”) today announced the board of directors of Comstock Inc. nominated and appointed Dr. Güez Salinas, as a new independent director to the Company’s Board of Directors and appointed Mr. Walter “Del” Marting as the Chairman of the Company’s Audit and Finance Committee. The Company also announced the resignation of Mr. Judd Merrill as a director of the company, all effective as of April 5, 2023.

Dr. Salinas has over 30 years of professional experience in the areas of engineering, strategy, finance, corporate management, and business development, with a primary focus on cyber-security and artificial intelligence policy and is currently an international cyber security expert at the Pacific Council on International Policy. Dr. Salinas has also been advising Quantum Generative Materials LLC (“GenMat”) on strategy and commercialization.

Dr. Salinas also founded and serves as the Director Emeritus of The Polymathic Academy for the Teaching of the Humanities & Sciences (“The PATH”) where he mentors and develops students’ multidisciplinary entrepreneurial pursuits. He also co-founded and serves as the Executive Director for The Law Enforcement Work Inquiry System (“LEWIS”), where, in partnership with Microsoft Corporation, serves as a touchpoint between peace officers and the community. Dr. Salinas, a U.S. Marine, also held positions in banking and private equity.

“We are honored to welcome Dr. Salinas and his perspective on the commercialization and rapidly growing positive impacts of generative artificial intelligence, and the security thereof, on our markets and society overall,” stated Mr. Corrado De Gasperis, Comstock’s executive chairman and chief executive officer. “His direct work with GenMat has forged an alignment and productivity that complements the current competencies of our Board.”

Mr. Marting was elected to the board of directors of Comstock in April of 2018. He is the Founder and Managing Member of CereCare, LLC, D/B/A Brain Health Restoration since March 2017, a firm focused on providing breakthrough rehabilitation treatment for individuals, including numerous veterans, suffering from brain disease, traumatic brain injury and related substance use disorders, most commonly alcoholism and opioid addictions.

Mr. Marting is also a deeply experienced mining, financial, capital markets, transactional and corporate governance executive. Mr. Marting graduated from Yale University in 1969, with a BA in English and holds an MBA from Harvard Business School. Mr. Marting is a Navy veteran, including service with US Navy SEAL Team Two.

“Del’s experience and counsel has been invaluable over the past five years, including his long tenure as a member of our Audit Committee, which he will now lead,” continued Mr. Corrado De Gasperis, Comstock’s executive chairman and chief executive officer. “We are sorry to see Judd step down and could not be more appreciative of his contributions and leadership on our board. I consider him one of the most reliable, professional, trustworthy and productive professionals I have ever worked with. We wish him nothing but success in his future endeavors.”

About Comstock

Comstock (NYSE: LODE) commercializes innovative technologies that contribute to global decarbonization by efficiently converting under-utilized natural resources, primarily, woody biomass into net zero renewable fuels, end of life metal extraction, and generative AI-enabled advanced materials synthesis and mineral discovery.

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future industry market conditions; future explorations or acquisitions; future changes in our exploration activities; future prices and sales of, and demand for, our products; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; and future working capital, costs, revenues, business opportunities, debt levels, cash flows, margins, taxes, earnings and growth. These statements are based on assumptions and assessments made by our management considering their experience and their perception of historical and current trends, current conditions, possible future developments, and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; ability to achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology, quantum computing and advanced materials development, and development of cellulosic technology in bio-fuels and related carbon-based material production; ability to successfully identify, finance, complete and integrate acquisitions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether because of new information, future events, or otherwise.

Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Contact information:

Comstock Inc. P.O. Box 1118 Virginia City, NV 89440 www.comstock.inc

Investor Relations RB Milestone Group Tel (203) 487-2759 [email protected]

Zach Spencer Director of External Relations Tel (775) 847-5272 Ext.151 [email protected]

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Telbel drilling results are pending. The goal of exploration and drilling along the past-producing Eagle-Telbel mine trend is to define high-grade zones of gold mineralization and additional mineral resources to complement the established resource at Douay. Maple Gold has completed more than 21,500 meters of drilling across the four-kilometer Eagle-Telbel Mine trend, with 14,720 meters at Maple’s 100%-owned Eagle mine property and more than 7,000 meters of joint venture drilling at the Telbel Mine area of the Joutel Project, which is held by a 50/50 joint venture between Maple and Agnico Eagle Mines Limited. Assay results associated with the drilling at Telbel are pending.

Last of the 2022 Eagle results released. Maple recently released remaining assay results from ~20% of the 14,720 meters of drilling at Eagle. To date, the company’s drilling at Eagle has confirmed that gold mineralization is not limited to the Eagle-Telbel Mine Horizon, a narrow stratigraphic interval, but instead covers a significantly broader stratigraphic interval of over 100 meters straddling the Harricana Deformation Zone. Drill core observations support Maple Gold’s concept of a significant structural component to gold mineralization in the form of an orogenic gold overprint.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – April 6, 2023) – Maple Gold Mines Ltd. (TSXV: MGM) (OTCQB: MGMLF) (FSE: M3G) (“Maple Gold” or the “Company“) is pleased to report results from the final 20% of assays that were received from the previously completed 14,720 metres (“m”) of drilling at the 100%-controlled Eagle Mine Property (“Eagle”). The Company is also pleased to report that more than 7,000 m have now been completed (6,000 m planned) at the Telbel Mine area of the Joutel Project, which is held by a 50/50 joint venture (the “JV”) between the Company and Agnico Eagle Gold Mines Limited.

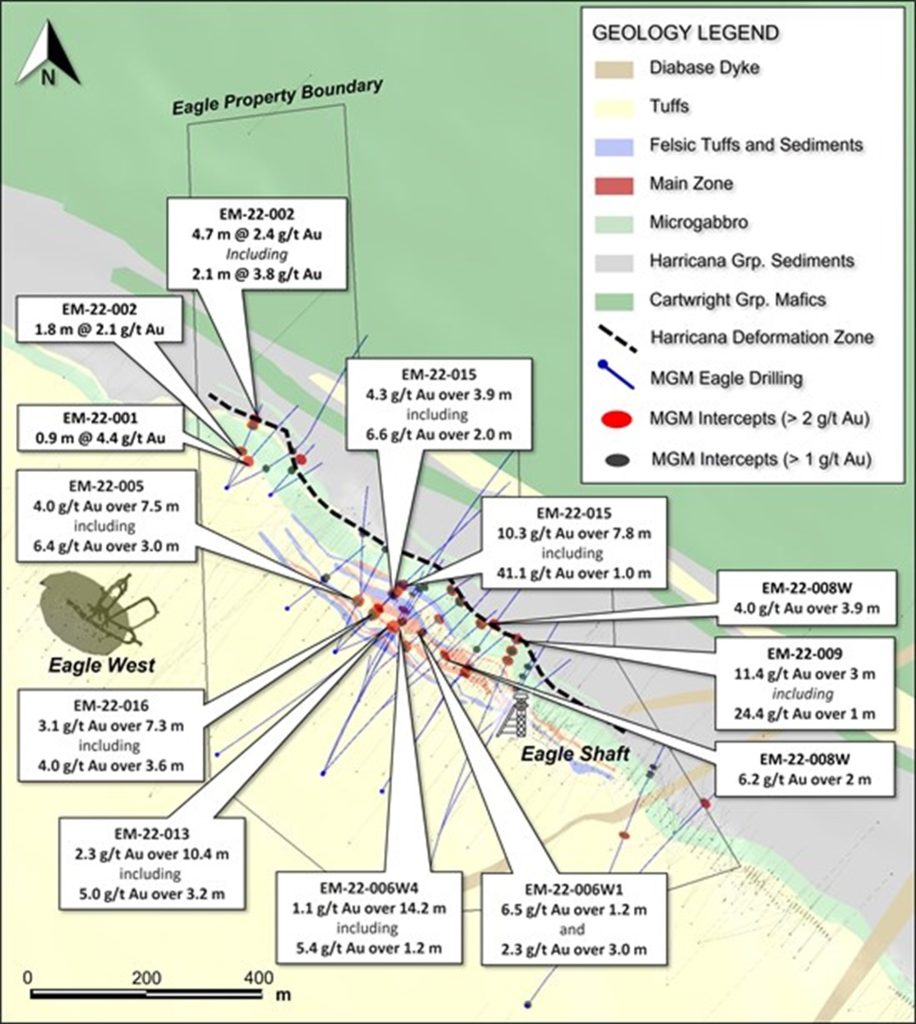

The final batch of assays received from completed drilling at Eagle correspond to approximately 3,000 m of the 14,720 m drilled to-date. The results continue to demonstrate continuity of mineralization and the potential significance of the multiple horizons/splays to the northwest of the former Eagle mine. Highlights include (see Table 1 and Figure 1 for highlighted results from all Maple Gold drilling at Eagle to-date):

EM-22-008W intersected 6.2 grams per tonne (“g/t”) gold (“Au”) over 2.0 m in the South Mine Horizon (“SMH”) and 4.2 g/t Au over 3.9 m in sediments further downhole.

EM-22-006W1 intersected multiple intercepts including 6.5 g/t Au over 1.2 m and 2.0 g/t Au over 3.0 m in the SMH and 2.3 g/t Au over 3.0 m at the microgabbro/Harricana sediment contact further downhole.

EM-22-006W4 intersected 4.0 g/t Au over 0.7 m within a broader 1.1 g/t Au over 14.2 m intercept within the SMH.

EM-22-017A intersected 2.9 g/t Au over 2.0 m and additional lower grade over broader near-surface intervals (1.0 g/t Au over 15.5 m from 93 m downhole).

“We have come along way since first consolidating the Joutel ground into our JV property package,” stated Matthew Hornor, CEO of Maple Gold. “All of our exploration and drilling work along the past-producing Eagle-Telbel mine trend is designed with the aim of defining high-grade zones of gold mineralization and additional mineral resources to complement the established potentially bulk-mineable resource present at Douay. Our first year of drilling at Eagle has more than covered our exploration spending commitments to earn a 100% interest and we are now in position to finalize our compilation and model updates to support focused follow-up drilling in areas we believe have the most promise to deliver additional high-quality ounces.”

Overview Summary and Key Takeaways from Drilling at Eagle

The Eagle-Telbel Mine trend produced 1.1 Moz at 6.5 g/t Au from 1974 – 1993, during a period when the price of gold averaged approximately $350 per ounce. During the first year of the JV (2021), all historical mining, stope and drilling data was digitized to underpin a new 3D geological model. The Company signed an option agreement to acquire a 100% interest in the Eagle Mine Property (see press release July 19, 2021) and has since completed more than 21,500 m of drilling across the 4 km long Eagle-Telbel Mine trend, with 14,720 m at Eagle (see Figure 1) and more than 7,000 m (assays pending) of JV drilling at Telbel.

The Company’s drilling to-date at Eagle has served to confirm that gold mineralization is not limited to a narrow stratigraphic interval (Eagle-Telbel Mine Horizon) but instead covers a significantly broader stratigraphic interval of over 100 m straddling the Harricana Deformation Zone. Drill core observations also support the Company’s concept of a significant structural component to gold mineralization in the form of an orogenic gold overprint.

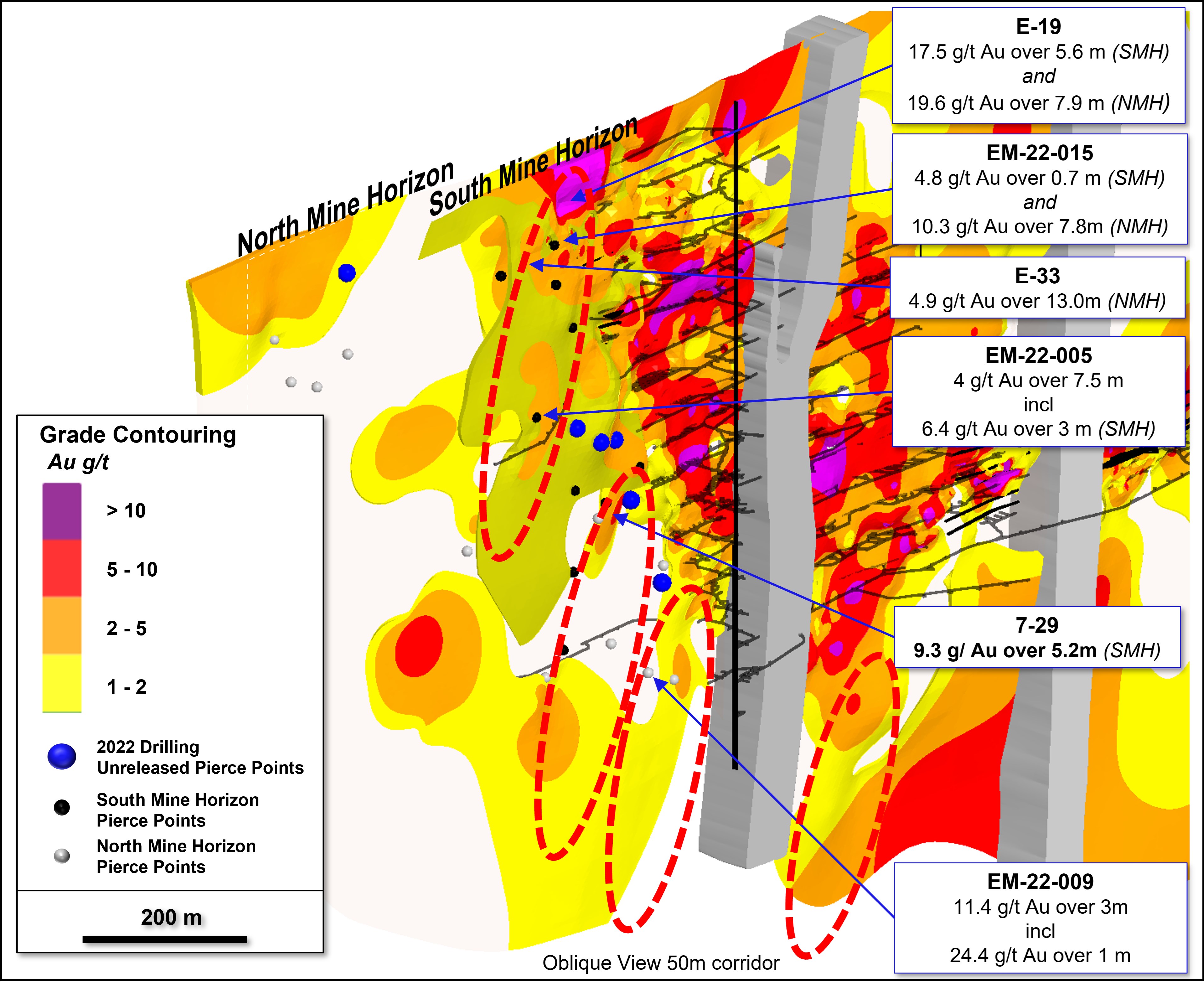

Figure 1: Plan view map showing drilling to-date at Eagle with highlighted intercepts.

Several highlights from the Company’s first year of drilling at Eagle are summarized below (see Figure 1 above for locations):

EM-22-005: 4.0 g/t Au over 7.5 m, including 6.4 g/t Au over 3.0 m

EM-22-009: 11.4 g/t Au over 3 m, including 24.4 g/t Au over 1 m

EM-22-013: 2.3 g/t Au over 10.4 m, including 5.0 g/t Au over 3.2 m

EM-22-015: 10.3 g/t Au over 7.8 m, including 41.1 g/t Au over 1.0 m

EM-22-015: 4.3 g/t Au over 3.9 m, including 7.4 g/t Au over 1.5 m

EM-22-016: 3.1 g/t Au over 7.3 m, including 4.0 g/t Au over 3.6 m

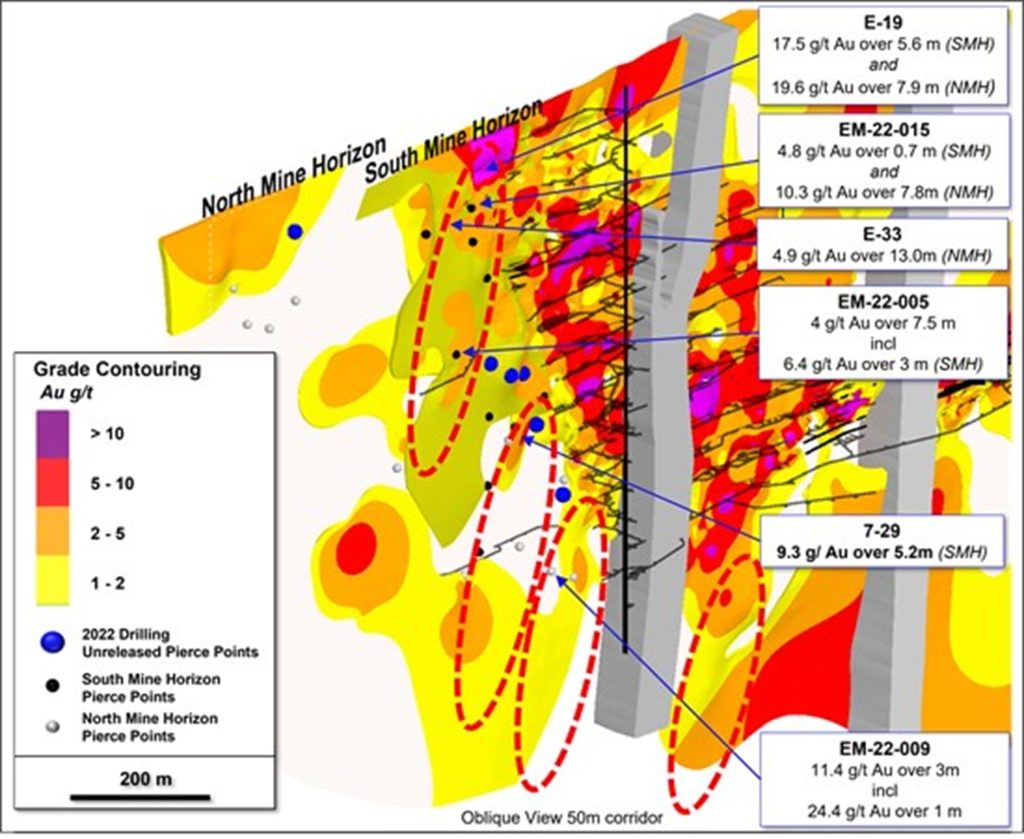

When combining the Company’s drilling results and observations with notable historical results and new geophysical data, several priority target areas emerge along the SMH and North Mine Horizon (“NMH”); including multiple cross-plunging target concepts that will form part of the focus for the Company’s next phase of drilling (~5,000 m). The Company has initiated target definition and permitting work for a planned summer 2023 follow-up program at Eagle (see press release March 16, 2023) and priority follow-up targets will also be defined at Telbel once assay results have been received and interpreted from the first phase of deep drilling.

Figure 2: Oblique view showing SMH and NMH trends with grade contouring and highlighted pierce points with corresponding intercepts and target areas.

Table 2: Highlighted Assay Results from Maple Gold Drilling at Eagle to-date

Hole

UTME

UTMN

Azimuth

Plunge

Length (m)

From

To

Interval

Au g/t

EM-22-001

690565

5486334

40.6

-66.8

356.6

132.0

134.6

2.6

1.7

including

133.7

134.6

0.9

4.4

EM-22-002

690565

5486334

22.0

-52.4

243

183.2

185.0

1.8

2.1

EM-22-002

200.4

205.0

4.7

2.4

including

200.4

202.4

2.1

3.8

EM-22-003

690642

5486322

59.1

-70.5

288

Narrow intercepts <1 g/t Au

EM-22-004

690673

5486120

49.9

-56.0

288

139.0

141.0

2.0

1.2

EM-22-005

690758

5486043

22.6

-75.7

714

346.0

360.0

14.0

2.2

including

346.0

353.5

7.5

4.0

including

350.0

353.0

3.0

6.4

EM-22-006

690737

5485828

25.9

-63.2

777.75

539.3

543.0

3.7

1.3

EM-22-007

690736

5485826

23.9

-73.2

985

877.0

878.0

1.0

2.0

EM-22-009

690921

5485639

17.5

71.4

1009

920.4

921.0

0.6

10.8

EM-22-009

951.0

956.0

5.0

1.6

EM-22-009

984.0

993.0

9.0

4.0

EM-22-009

990.0

993.0

3.0

11.4

EM-22-009

991.0

993.0

2.0

15.5

including

992.0

993.0

1.0

24.4

EM-22-010

690841

5485795

32.5

-71.4

570

539.5

540.0

0.5

14.0

EM-22-010

543.0

544.0

1.0

8.3

EM-22-010W

690841

5485795

34.1

-61.2

932

921.0

922.0

1.0

3.7

EM-22-011

690547

5485859

56.7

-62

924

858.3

859.0

0.7

3.2

EM-22-012

691098.7

5485413

35.3

-78.6

1284

1232.2

1234.3

2.1

2.0

EM-22-013

690757.5

5486043

63.8

-69.8

327

257.0

267.4

10.4

2.3

including

257.0

260.2

3.2

5.0

EM-22-014

690565

5486334

64.5

-67.9

646

231.0

231.7

0.7

4.6

EM-22-015

690757.5

5486043

45

-50.1

408

142.5

148.6

6.1

1.6

EM-22-015

164.9

165.5

0.7

4.8

EM-22-015

217.1

221.0

3.9

4.3

including

218.5

220.0

1.5

7.4

EM-22-015

228.0

235.8

7.8

10.3

including

228.5

232.8

4.3

15.9

including

230.0

231.0

1.0

41.1

EM-22-015

246.7

248.4

1.7

4.3

including

247.5

248.4

0.9

7.1

EM-22-015

252.2

255.0

2.8

1.8

EM-22-016

690757.8

5486043

45.1

-62.6

297

193.0

206.2

13.2

2.2

including

193.0

200.3

7.3

3.1

including

196.0

199.6

3.6

4.0

EM-22-016

202.0

206.2

4.2

1.7

EM-22-017A

690643

5486322

41.3

-55.76

201

93.5

109.0

15.5

1.0

including

97.0

103.0

6.0

1.4

EM-22-017A

137.0

144.0

7.0

1.4

including

141.0

143.0

2.0

2.9

EM-22-005W

690795

5486136

2.2

-65.5

364

364.3

365.8

1.5

1.3

624.0

625.0

1.0

1.2

EM-22-006W1

690736.7

5485828

29.5

-57

435.2

476.0

479.0

3.0

2.0

EM-22-006W1

482.8

484.0

1.2

6.5

EM-22-006W1

652.0

655.0

3.0

2.3

including

653.5

654.1

0.6

6.6

EM-22-009W2A

690921

5485639

21.4

-65.9

634

828.0

830.0

2.0

1.4

EM-22-010W1

690841

5485795

30.8

-62

361

583.5

584.0

0.5

1.5

EM-22-008W

690737

5485828

45.6

-58.1

377

527.0

529.0

2.0

6.2

EM-22-008W

630.1

634.0

3.9

4.2

including

631.0

632.5

1.5

6.8

EM-23-006W4

690737

5485828

24.5

-39.4

236

472.0

486.2

14.2

1.1

including

472.0

477.4

5.4

1.4

including

481.6

482.3

0.7

4.0

EM-23-006W4

521.0

523.6

2.6

1.9

EM-22-012W

691098.7

5485413

20

-45.6

524.7

1095.3

1097.4

2.1

1.2

Notes: Drill holes EM-22-006W, EM-22-006X, EM-22-008 and EM-22-009W1 returned no significant assays. Drill hole EM-22-017 was lost at 51 m. True widths estimated at 40% to 70% of downhole width depending on the hole inclination.

Qualified Person

The scientific and technical data contained in this press release was reviewed and prepared under the supervision of Fred Speidel, M. Sc., P. Geo., Vice-President Exploration of Maple Gold. Mr. Speidel is a Qualified Person under National Instrument 43-101 Standards of Disclosure for Mineral Projects. Mr. Speidel has verified the data related to the exploration information disclosed in this press release through his direct participation in the work.

Quality Assurance (QA) and Quality Control (QC)

The Company implements strict Quality Assurance (“QA”) and Quality Control (“QC”) protocols at Eagle covering the planning and placing of drill holes in the field; drilling and retrieving the NQ-sized drill core; drill hole surveying; core transport; core logging by qualified personnel; sampling and bagging of core for analysis; transport of core from site to the Val d’Or, Québec AGAT laboratory; sample preparation for assaying; and analysis, recording and final statistical vetting of results. Check assays for gold are being done on a sample subset at ALS’ laboratory in Val d’Or. For a complete description of protocols, please visit the Company’s QA/QC webpage at www.maplegoldmines.com.

About Maple Gold

Maple Gold Mines Ltd. is a Canadian advanced exploration company in a 50/50 joint venture with Agnico Eagle Mines Limited to jointly advance the district-scale Douay and Joutel gold projects located in Québec’s prolific Abitibi Greenstone Gold Belt. The projects benefit from exceptional infrastructure access and boast ~400 km2 of highly prospective ground including an established gold resource at Douay (SLR 2022) that holds significant expansion potential as well as the past-producing Eagle, Telbel and Eagle West mines at Joutel. In addition, the Company holds an exclusive option to acquire 100% of the Eagle Mine Property.

The district-scale property package also hosts a significant number of regional exploration targets along a 55 km strike length of the Casa Berardi Deformation Zone that have yet to be tested through drilling, making the project ripe for new gold and polymetallic discoveries. The Company is well capitalized and is currently focused on carrying out exploration and drill programs to grow resources and make new discoveries to establish an exciting new gold district in the heart of the Abitibi. For more information, please visit www.maplegoldmines.com.

ON BEHALF OF MAPLE GOLD MINES LTD.

“Matthew Hornor”

B. Matthew Hornor, President & CEO

For Further Information Please Contact:

Mr. Joness Lang Executive Vice-President Cell: 778.686.6836 Email: [email protected]

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS PRESS RELEASE.

Forward Looking Statements:

This press release contains “forward-looking information” and “forward-looking statements” (collectively referred to as “forward-looking statements”) within the meaning of applicable Canadian securities legislation in Canada, including statements about exploration work and results from current and future work programs. Forward-looking statements are based on assumptions, uncertainties and management’s best estimate of future events. Actual events or results could differ materially from the Company’s expectations and projections. Investors are cautioned that forward-looking statements involve risks and uncertainties. Accordingly, readers should not place undue reliance on forward-looking statements. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to Maple Gold Mines Ltd.’s filings with Canadian securities regulators available on www.sedar.com or the Company’s website at www.maplegoldmines.com. The Company does not intend, and expressly disclaims any intention or obligation to, update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Collaboration with Invest Alberta. LithiumBank executed a Memorandum of Understanding with Invest Alberta Corporation (IAC) to support the development of a lithium production facility at the company’s Boardwalk brine project. Established as a crown corporation of the Government of Alberta, Invest Alberta promotes Alberta as an investment destination of choice to investors in Canada and internationally. LithiumBank’s commercial lithium production facility in northern Alberta could factor importantly in Alberta becoming a destination for critical mineral resource development and as a partner in the electrification supply chain.

Why is this collaboration important? With teams in Calgary and Edmonton along with 11 international locations, IAC connects industry, government partners, and economic development organizations and provides services to facilitate investment in Alberta. The organization will support LithiumBank by promoting the Boardwalk project domestically and internationally, facilitate relationships with key stakeholders and senior government officials, and bolster LithiumBank’s relationships with post-secondary institutions to create a qualified talent pipeline in support of the project.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

TORONTO, April 04, 2023 (GLOBE NEWSWIRE) — Labrador Gold Corp. (TSX.V:LAB | OTCQX:NKOSF | FNR: 2N6) (“LabGold” or the “Company”) is pleased to announce results of its annual general meeting of shareholders held in Toronto on April 3, 2023.

At the meeting shareholders re-elected five current directors, being Roger Moss, James Borland, Trevor Boyd, Leonidas Karabelas and Kai Hoffmann and approved the re-appointment of DeVisser Gray LLP, of Vancouver, British Columbia, as auditors of the Corporation. Shareholders also ratified the 2021 Stock Option Plan and approved the Corporation’s new 2023 Stock Option Plan which supercedes and replaces the 2021 Stock Option Plan.

Following the shareholder meeting the Board of Directors reconstituted its Audit Committee and also reappointed officers for the ensuing year as follows:

President and CEO: Roger Moss

Chief Financial Officer: Eric Myung

Corporate Secretary: William Johnstone

The Company also announces that in accordance with its Stock Option Plan, it has granted officers, directors, consultants and employees an aggregate of 3,100,000 incentive stock options exercisable until April 3, 2028 at $0.23 per share. The options will vest according to the following schedule, 20% on August 3, 2023, 20% on October 3, 2023, 20% on April 3, 2024, 20% on October 3, 2024 and 20% on April 3,2025.

About Labrador Gold Labrador Gold is a Canadian based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada.

Labrador Gold’s flagship property is the 100% owned Kingsway project in the Gander area of Newfoundland. The three licenses comprising the Kingsway project cover approximately 12km of the Appleton Fault Zone which is associated with gold occurrences in the region, including those of New Found Gold immediately to the south of Kingsway. Infrastructure in the area is excellent located just 18km from the town of Gander with road access to the project, nearby electricity and abundant local water. LabGold is drilling a projected 100,000 metres targeting high-grade epizonal gold mineralization along the Appleton Fault Zone with encouraging results to date. The Company has approximately $16 million in working capital and is well funded to carry out the planned program.

The Hopedale property covers much of the Florence Lake greenstone belt that stretches over 60 km. The belt is typical of greenstone belts around the world but has been underexplored by comparison. Work to date by Labrador Gold show gold anomalies in rocks, soils and lake sediments over a 3 kilometre section of the northern portion of the Florence Lake greenstone belt in the vicinity of the known Thurber Dog gold showing where grab samples assayed up to 7.8g/t gold. In addition, anomalous gold in soil and lake sediment samples occur over approximately 40 km along the southern section of the greenstone belt (see news release dated January 25 th 2018 for more details). Labrador Gold now controls approximately 40km strike length of the Florence Lake Greenstone Belt.

The Company has 170,009,979 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release .

Forward-Looking Statements: This news release contains forward-looking statements that involve risks and uncertainties, which may cause actual results to differ materially from the statements made. When used in this document, the words “may”, “would”, “could”, “will”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “expect” and similar expressions are intended to identify forward-looking statements. Such statements reflect our current views with respect to future events and are subject to risks and uncertainties. Many factors could cause our actual results to differ materially from the statements made, including those factors discussed in filings made by us with the Canadian securities regulatory authorities. Should one or more of these risks and uncertainties, such as actual results of current exploration programs, the general risks associated with the mining industry, the price of gold and other metals, currency and interest rate fluctuations, increased competition and general economic and market factors, occur or should assumptions underlying the forward looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, or expected. We do not intend and do not assume any obligation to update these forward-looking statements, except as required by law. Shareholders are cautioned not to put undue reliance on such forward-looking statements .

{kind=link}

{kind=link}