Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fostering advanced exploration technologies. Comstock is collaborating with its strategic investee Quantum Generative Materials (GenMat) to develop and expand the next generation geostatistical digital model of its most strategic mining development areas, including the November launch of a space-based hyperspectral imager that will extract relevant chemical and physical information for high precision mineral prospecting. The goal is to incorporate innovative technology within its exploration activities to increase mineral resources to two million gold equivalent ounces.

Successful launch of satellite and imager. GENMAT-1 was launched via Maverick Space Systems aboard a SpaceX Falcon 9 Transporter rocket from Vandenberg Space Force Base in Lompoc, California on November 11. At an altitude of 500 kilometers, the satellite will continuously capture and transmit hyperspectral image data of minerals and surface matter. The initial mission is to capture hyperspectral data of the Comstock Lode.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Refining estimates. We have increased our 2023 EBITDA and EPU estimates to $4.96 and $975.2 million from $966.2 million and $4.89. We decided to increase our total coal sales estimates which are now at the midpoint of guidance instead of at the low end. We also modestly increased our coal sales price per ton estimate to $65.15 from $65.00 but still within the guidance range of $64.50 to $66.00. We have lowered our 2024 EBITDA and EPU estimates to $998.1 million and $5.05 from $1.0 billion and $5.15 based on modestly lower commodity prices.

Why the revisions? Alliance has committed and priced 35.0 million tons in 2023, including 29.7 million tons in the domestic market and 5.3 million tonnes in export markets. While a portion of higher priced export volumes could be deferred into 2024, we think our previous estimate was too conservative. As part of our review, we also adjusted quarterly and full year 2024 estimates and refined both years’ estimates associated with equity method investments.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Oklahoma City-based Mach Natural Resources LP announced Monday that it has agreed to acquire oil and gas assets in Oklahoma’s Anadarko Basin from Paloma Partners IV, LLC for $815 million. The deal marks a significant expansion for Mach as it looks to increase production and proved reserves.

The acquisition includes approximately 62,000 net acres concentrated in the core counties of Canadian and Grady, along with recent production of around 32,000 barrels of oil equivalent per day. Mach cited substantial proved developed producing (PDP) reserves of 75 million barrels of oil equivalent and over a decade’s worth of drilling inventory supporting the transaction.

Mach was attracted to the assets’ high margin oil production and potential for further development. The company said the purchase advances its strategy of focusing on distributions, disciplined acquisitions, maintaining low leverage, and keeping the reinvestment rate under 50%. According to Mach, the deal is accretive to cash available for distribution and cash distribution per unit.

The properties change hands with one rig currently running in Grady County and plans for 6 more wells to be completed before the expected December 29 closing. Post-acquisition, Mach intends to add another rig, continuing its measured approach to capital spending.

The purchase price reflects discounted PDP value, presenting an opportunity for Mach to boost near-term cash flow. At the same time, the company is bringing aboard de-risked SCOOP/STACK drilling locations that can fuel longer-term growth.

To finance the $815 million transaction, Mach has lined up committed debt financing led by Chambers Energy Management and EOC Partners. The senior secured term loan will provide $825 million at the closing date. Mach stated that its leverage ratio will remain below 1.0x debt to EBITDA after absorbing the new debt.

Mach’s Chief Executive Officer commented, “This transaction creates significant value for our unitholders and represents an important step in executing our strategic vision. We look forward to developing these high-quality assets and welcoming a talented local team to the Mach family.”

The seller, Paloma Partners IV, is backed by private equity firms EnCap Investments and its affiliates. Paloma amassed the properties in 2017 and 2018 when SCOOP/STACK deal activity was high. Its divestiture to Mach comes amidst a cooling of M&A in the play.

Mach was founded in 2021 with an emphasis on shareholder returns and steady growth in Oklahoma’s Anadarko Basin. The company currently runs a two-rig development program on its legacy acreage position.

The Anadarko Basin has seen resurgent activity as producers apply drilling and completion technology to unlock the potential of the SCOOP and STACK plays. Operators continue to drive down costs and improve productivity in the prolific geological formations.

Mach’s new Grady County acreage provides exposure to the volatile oil window of the SCOOP Woodford condensate play. Well results in the area have benefited from longer laterals, increased sand loadings, and optimized well spacing.

Canadian County offers additional Woodford potential plus stacked pays in the Meramec, Osage and Oswego horizons. Together, these reservoirs offer a mix of liquids-rich gas and high-margin oil for Mach’s operated portfolio.

With its firm financial footing and expanded operational scale, Mach appears positioned for further consolidation in the Anadarko Basin. The company now controls over 150,000 net acres in the region. Its proven strategy may attract additional sellers seeking to divest non-core acreage and realize value from their own holdings.

Mach can leverage its expanded position and technical expertise to exploit not only the SCOOP and STACK but also emerging zones like the Osage and Cottage Grove. The company anticipates its enlarged inventory will support steady production growth and consistent cash returns in the years ahead.

Monday’s major acquisition cements Mach Natural Resource’s status as a premier independent operator in the Anadarko Basin. The company seems intent on delivering on its promises of accretive growth, high cash margins, and peer-leading capital discipline. For Mach, size and scale will likely prove critical in generating free cash flow and distributions in a commodity price environment with little room for error.

Haynes International, Inc. is a leading developer, manufacturer and marketer of technologically advanced, nickel and cobalt-based high-performance alloys, primarily for use in the aerospace, industrial gas turbine and chemical processing industries.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating estimates. We have trimmed our fiscal year 2023 EBITDA and EPS estimates to $80.6 million and $3.22 from $81.2 million and $3.25 per share. Our estimates reflect lower gross margins during the September quarter due to the negative impact of raw material fluctuations. Our September EBITDA and EPS estimates were lowered to $23.2 million and $0.97 from $23.7 million and $1.00. We are making no changes to our 2024 estimates and expect Haynes to provide guidance for fiscal 2024 when it reports results for fiscal year 2023. We still expect the September quarter will be Haynes’ strongest of the fiscal year in terms of volumes shipped, net revenues, and earnings.

Strong order backlog. Orders during the June quarter resulted in a record backlog of $468.1 million and represented a 4.8% increase compared to the prior quarter and a 38.4% increase on a year-over-year basis. Backlog pounds increased 3.2% during the third quarter to approximately 14.6 million pounds and increased 20.7% compared to the prior year period driven by strong demand in the aerospace and industrial gas turbine markets. In our view, the strong order book is indicative of the company’s strong competitive position and favorable outlook.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURE™ and VPURE+™ products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Volumes are down due to an accident and technical delays. However, management reports improved October results. Vanadium prices remain an issue, but the decline shows signs of abating. Management reports that input costs such as sodium carbonate are beginning to ease and that the company is actively working to lower costs at the mine and at Largo Clean Energy (LCE).

Financial results remain depressed. The company has made several investments to improve operations including completing an infill drilling program. Completion of Largo’s Ilmenite plant and an initial shipment should not only improve profitability but also diversify sales. The company’s cash position remains adequate at $39.6 million to fund future operations. We would note that Largo’s debt position increased by $50 million year over year but was unchanged from June 30, 2023 levels.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Newrange is focused on district-scale exploration for precious metals in the prolific Red Lake District of northwestern Ontario. The past-producing high-grade Argosy Gold Mine is open to depth, while the adjacent North Birch Project offers additional blue-sky potential. Focused on developing shareholder value through exploration and development of key projects, the Company is committed to building sustainable value for all stakeholders. Further information can be found on our website at www.newrangegold.com .

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transaction to form Pinnacle Silver & Gold Corp. In May,Newrange executed a binding Scheme Implementation Deed (SID)to acquire 100% of Mithril Resources Limited (ASX: MTH) in a reverse takeover (RTO). Pending approval by the TSX Venture Exchange, the resulting company will be named Pinnacle Silver & Gold Corp. and will be listed on the TSX Venture exchange under the symbol “PINN.” During their respective special meetings, Newrange and Mithril shareholders approved the merger between Newrange and Mithril to form Pinnacle Silver & Gold Corporation. Assuming that all requirements are satisfied, the transaction could close in late November or early December.

Key conditions remain. Although both sets of shareholders have approved the transaction, several requirements remain outstanding. These include: 1) the Federal Court of Australia must approve the transaction, 2) an Independent Expert must affirm that in the absence of a superior offer, the share and option schemes are in the best interests of Mithril shareholders and option holders, 3) completion of Newrange Gold’s concurrent financing, 4) Newrange Gold receiving unconditional approval to re-list on the TSX Venture Exchange, and 5) satisfaction or waiver of any remaining conditions prior to the Court hearing.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

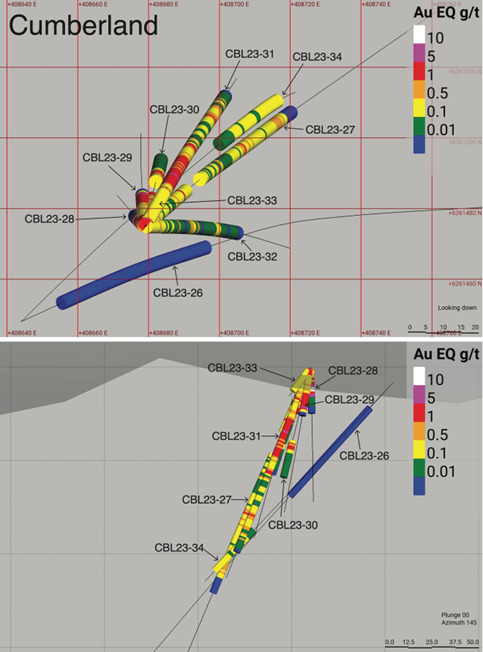

Productive drill season. Eskay Mining had a productive 2023 diamond drill and exploration season at its 100% controlled Consolidated Eskay Gold Project. The roughly 6,000 meter drill program centered on seven targets: 1) Cumberland, 2) Scarlet Knob-Bruce Glacier, 3) Tarn Lake, 4) Hexagon-Mercury, 5) Maroon Cliffs, 6) Storie Creek, and 7) TV South. While the company confirmed new precious metal rich volcanogenic massive sulfide (VMS) discoveries, the most significant outcome, in our view, is that the program highlighted the significant exploration potential in the areas between the Cumberland target and the TV-Jeff complex. Tied for second are results from Scarlet Knob and Tarn Lake.

Encouraging results at Cumberland. Cumberland is ~6 kilometers south of the TV deposit and is similarly situated along the east side of the Eskay anticline. Nine holes were completed at the Cumberland target. Several returned promising assays, including Hole CBL23-28 which returned 3.02 grams of gold per tonne, 68.66 grams of silver per tonne, 0.24% copper, 0.74% lead, and 4.86% zinc, or 6.28 grams of gold equivalent, over 15 meters.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In a bold move to combat surging fuel prices and rampant inflation, President Biden is unleashing a flood of black gold onto the markets. The White House is planning to tap a massive 180 million barrels of crude oil from the nation’s Strategic Petroleum Reserve (SPR) – the biggest withdrawal in the reserve’s history.

The news sent oil prices tumbling 5% in early trading as speculators reacted to the supply boost. But will the SPR floodgates really succeed in taming the oil price beast that has economists worried about recession?

The sheer size of the release, equivalent to two full days of global oil consumption, grabbed headlines. Set to be gradually emptied over several months, Biden’s SPR unleashing is meant to act like a shot of bear tranquilizer for the raging oil market.

Ever since Russia’s invasion of Ukraine, reduced supply from the world’s No. 2 exporter combined with surging demand has driven prices to their highest levels since 2008. Brent crude already flirted with a mind-boggling $140 per barrel in March. Even after the SPR news-driven dip, benchmark oil remains stubbornly high at around $105.

For Biden, doling out the emergency crude is a midterm elections Hail Mary pass. Painfully high gas prices have contributed to the president’s dismal approval ratings. Tapping the SPR to lower fuel costs may be his best bet to avoid Democrats enduring a disastrous drubbing by the Republicans in November.

Beyond politics, uncorking America’s oil reserves also sends an important message to the market. It signals the Administration’s determination to fight an inflation rate that keeps printing four-decade highs. Few things impact inflation expectations like changes in oil prices. A meaningful drop could help tamp down the runaway price increases eroding consumer confidence.

But will the effort succeed or will it flounder like past attempts? With global crude inventories at historic lows, many analysts see the SPR release as a mere band-aid solution. It provides some short-term relief but doesn’t fix the supply and demand imbalance.

Goldman Sachs estimates the 180 million barrel slug will help rebalance markets this year. But it warned the move doesn’t resolve the structural deficit caused by excluding Russian exports.

Previous SPR releases also failed to produce lasting effects. Oil prices quickly rebounded after 60 million barrels were tapped in November 2021 and another 30 million in March 2022.

This time, the White House is also counting on allies for help. The International Energy Agency meets soon to potentially coordinate a collective release from its members’ reserves.

But Biden’s SPR gambit already seems at odds with other moves meant to restrict oil supply and fight climate change. Canceling the Keystone XL pipeline permit and banning new federal drilling auctions counterproductively worsened the supply crunch. A of couple million extra daily barrels from those sources would have eased pressure on prices.

The Administration now finds itself trying to fix with one hand problems partly created by the other. That internal tension undermines the large SPR release’s credibility.

Traders also scoffed when OPEC refused to boost production more than a token amount after the U.S. lobbied for extra output. With the cartel and allies like Russia benefitting handsomely from $100+ oil, they have little incentive to pump much more.

Meanwhile, risks of a demand-killing recession loom if the Fed’s inflation fight requires jumbo interest rate hikes. And Covid lockdowns in China already hurt oil demand in the world’s largest importer.

So while Biden’s SPR flow should offer some near-term relief at the pump, it may not move the needle much for long. Markets fear what happens if 180 million barrels merely postpones the supply day of reckoning rather than preventing it.

With inventories low, spare capacity shrinking, geopolitical unrest continuing, and ESG considerations constraining investment, oil looks poised to remain highly volatile. While the SPR release was historic in size, it likely won’t fully tranquilize the energy markets.

Drill intercepts of 6.28 gpt AuEq over 15.00m, 2.96 gpt AuEq over 22.52m, 2.00 gpt AuEq over 61.23m and 1.39 gpt AuEq over 45.67m encountered at Cumberland

Rock chip samples of 37.23, 23.34, 20.34 and 20.23 gpt AuEq from Scarlet Knob

TORONTO, ON / ACCESSWIRE / November 2, 2023 / Eskay Mining Corp. (“Eskay” or the “Company”) (TSXV:ESK)(OTCQX:ESKYF)(Frankfurt:KN7)(WKN:A0YDPM) is pleased to announce it has received very encouraging assay results from its 2023 diamond drill and exploration campaign at its 100% controlled Consolidated Eskay Gold Project in the Golden Triangle of British Columbia. Precious metal-rich volcanogenic massive sulfide (“VMS”) deposits are the focus of Eskay’s exploration.

Cumberland VMS Discovery

Nine short diamond core holes were completed at the Cumberland Showing in 2023 (Figure 2), several of which encountered very promising precious and base metal-rich stockwork and massive mineralization. Notable results include:

3.02 gpt Au, 68.66 gpt Ag, 0.24% Cu, 0.73% Pb and 4.86% Zn (6.28 gpt AuEq) over 15.00m including 8.48 gpt Au, 103.27 gpt Ag, 0.23% Cu, 1.08% Pb and 4.16% Zn (12.02 gpt AuEq) over 3.41m in hole CBL23-28.

1.21 gpt Au, 29.22 gpt Ag, 0.12% Cu, 0.32% Pb and 2.94% Zn (2.96 gpt AuEq) over 22.52m including 3.45 gpt Au, 108.21 gpt Ag, 0.65% Cu, 0.54% Pb and 19.40% Zn (13.24 gpt AuEq) over 1.75m in hole CBL23-29.

0.68 gpt Au, 15.72 gpt Ag, 0.07% Cu, 0.27% Pb and 0.90% Zn (1.39 gpt AuEq) over 45.67m in hole CBL23-30.

0.95 gpt Au, 29.04 gpt Ag, 0.07% Cu, 0.29% Pb and 1.31% Zn (2.00 gpt AuEq) over 61.23m including 1.57 gpt Au, 58.80 gpt Ag, 0.16% Cu, 0.60% Pb and 3.13% Zn (3.91 gpt AuEq) over 20.08m in hole CBL23-31.

Cumberland lies approximately 6km due south of the TV deposit and is similarly situated along the east side of the Eskay anticline. Eskay’s geologic team thinks this discovery opens up considerable exploration potential in areas between Cumberland and the TV-Jeff VMS complex (Figures 3 and 4). It is notable that mineralization at Cumberland displays very high base metals, an indicator of high formational fluid temperatures, a potential sign that this area lies in proximity to a major feeder vent or vents.

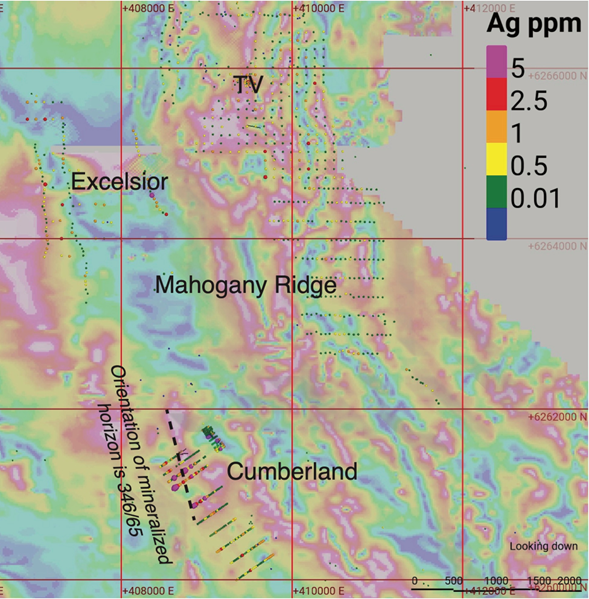

Based upon data from this limited first phase drill program, the Cumberland VMS deposit is interpreted to be tabular with a N-S orientation and a near vertical dip, perhaps slightly overturned. It remains open along strike and at depth. A review of historic soil data (Figures 3 and 4) from areas up to 1.5 km south of Cumberland indicates a broad area of strongly anomalous geochemistry, especially elevated silver values, confirming a likely extension of mineralization in this direction. Eskay’s geologic team observed significant outcropping sulfide mineralization while conducting traverses in this region south of Cumberland.

While prospecting late in the season, a notable area of outcropping sulfide mineralization was observed approximately 2.5 km to the northeast of Cumberland and is potentially part of the same VMS system. This area has been named Mahogany Ridge. Historic rock chip sample data from the broader Cumberland trend includes samples grading 25.0, and 27.9 gpt Au.

Given the strong drill and rock chip sample results from the Cumberland-Mahogany Ridge area, Eskay Mining views this discovery as a high priority exploration target. Compelling evidence is emerging that the corridor starting at TV-Jeff in the north through Mahogany Ridge and Cumberland and continuing a further 1.5km south of Cumberland is highly prospective for further precious metal-rich VMS discoveries. Eskay Mining thinks this corridor requires urgent follow up work including drilling in 2024.

“Cumberland is shaping up to be a very compelling and unique target”, commented John DeDecker, Eskay’s VP of Exploration. “Intense polymetallic sulfide mineralization ranges from stockwork-style, to massive seafloor-hosted mineralization. The seafloor-hosted mineralization is associated with barite breccia, and is capped by a non-mineralized and highly magnetic pillow basalt. Drilling and field investigations have defined the orientation of the mineralized seafloor horizon, and have shown that Ag anomalies in historic soil samples, and a pronounced magnetic anomaly evident in the 2021 EM survey lie along the trend of mineralization extending at least 300 m south of Cumberland. Our team looks forward to investigating this area further in 2024. The confirmation of another mineralized seafloor horizon at Scarlet Knob, and extensive disseminated Au mineralization at Tarn Lake opens these areas up to targeted exploration in 2024.”

Summary of significant results from nine core holes completed at the Cumberland Showing in 2023:

Hole

From (m)

To (m)

Length (m)

Au (gpt)

Ag (gpt)

Cu (%)

Pb (%)

Zn (%)

Au Eq (gpt)

CBL23-26

NSV

CBL23-27

1.26

8.15

6.89

0.58

16.93

–

–

–

0.79

22.57

25.76

3.19

0.33

12.50

–

0.25

0.34

0.70

30.50

35.39

4.89

0.43

11.80

–

0.10

0.61

0.85

71.83

92.65

20.82

0.28

1.11

0.06

0.08

2.00

1.16

includes

73.63

76.71

3.08

0.17

6.62

0.08

0.04

2.80

1.44

includes

84.90

85.90

1.00

1.78

23.00

0.35

0.25

11.85

7.13

103.98

121.03

17.05

0.34

10.12

–

–

–

0.47

CBL23-28

1.29

16.29

15.00

3.02

68.66

0.24

0.73

4.86

6.28

includes

5.68

16.29

10.61

4.11

92.84

0.30

0.92

6.33

8.39

includes

9.86

13.27

3.41

8.48

103.27

0.23

1.08

4.16

12.02

CBL23-29

1.69

24.21

22.52

1.21

29.22

0.12

0.32

2.94

2.96

includes

1.69

4.79

3.10

2.90

14.18

0.06

0.29

0.49

3.44

and

14.94

24.21

9.27

1.70

53.89

0.23

0.51

0.62

3.07

includes

22.46

24.21

1.75

3.45

108.21

0.65

0.54

19.40

13.24

CBL23-30

0.89

46.56

45.67

0.68

15.72

0.07

0.27

0.90

1.39

includes

0.89

2.79

1.90

2.72

5.03

0.02

1.46

0.19

3.37

and

17.12

46.56

29.44

0.84

21.40

0.11

0.38

1.56

1.97

CBL23-31

1.22

62.45

61.23

0.95

29.04

0.07

0.29

1.31

2.00

includes

1.22

2.22

1.00

9.84

6.78

0.02

0.15

0.06

10.02

and

30.20

50.28

20.08

1.57

58.80

0.16

0.60

3.13

3.91

includes

30.20

35.20

5.00

1.36

57.82

0.48

0.43

8.75

6.18

and

36.20

38.25

2.05

4.64

155.07

0.07

1.16

1.34

7.57

85.00

95.00

10.00

0.48

13.07

–

0.08

0.17

0.74

CBL23-32

NSV

CBL23-33

NSV

CBL23-34

114.28

117.28

3.00

0.20

7.42

–

0.09

1.38

0.85

127.61

136.65

9.04

0.14

3.42

–

0.02

1.01

0.58

NSV = No Significant Values; AuEq values have been calculated using a Ag-to-Au ratio of 80:1, Cu-to-Au ratio of 8,100:1, Pb-to-Au ratio of 29,800:1 and Zn-to-Au ratio of 26,050:1 for this news release.

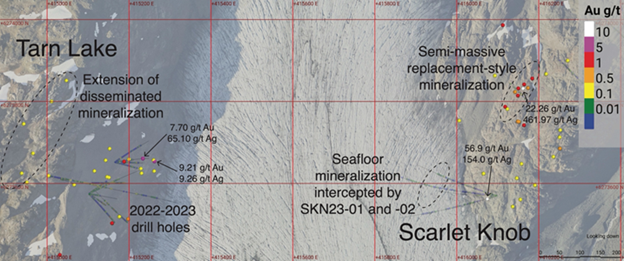

Scarlet Knob-Bruce Glacier Discovery

Near the end of the exploration season at a time of maximum snowmelt, Eskay Mining’s exploration team found outcrops of metal-rich VMS mineralization immediately adjacent to the eastern margin of Bruce Glacier. This area is called Scarlet Knob and is located in the northeastern part of the Consolidated Eskay Gold Project approximately 7km southeast of the Eskay Creek mine. Four rock chip samples collected from a 100 m long, 5 m wide sulfide replacement body (Figures 6 and 7) returned very strong precious and base metal values as presented below:

Sample

Au (gpt)

Ag (gpt)

Cu (%)

Pb (%)

Zn (%)

Au Eq (gpt)

1001A

11.71

199.03

0.33

7.77

8.16

20.34

1001B

22.26

461.97

0.22

14.57

10.50

37.23

1001C

10.04

169.50

0.16

12.00

10.02

20.23

1001D

14.80

160.82

0.16

9.53

8.18

23.34

Although this outcropping sulfide body is small, it appears to occur at or near the paleo-sea floor interface, a stratigraphic position conducive for hosting a deposit like that at the nearby Eskay Creek mine. Given the very strong precious metal values from these samples, Eskay mining’s geologic team takes a strong view that this occurrence suggests a bigger system may be present in this area.

Early in the drill season, four core holes were drilled in an area approximately 200 m south of this high-grade discovery. These holes were drilled based upon a conceptual view formed by Eskay Mining’s geologic team that the paleo-seafloor position, possibly mineralized, should be hiding under Bruce Glacier. All four of these drill holes indeed pierced the contact between volcanic rocks and sea floor mudstone, and two of these holes encountered highly elevated precious and base metal values as seen in the table below:

Hole

From (m)

To (m)

Length (m)

Au (gpt)

Ag (gpt)

Cu (%)

Pb (%)

Zn (%)

Au Eq (gpt)

SKN23-01

172.92

174.10

1.18

0.24

46.90

–

1.93

1.19

1.93

255.32

257.51

2.19

0.40

49.66

–

0.45

0.47

1.35

SKN23-02

188.81

191.43

2.62

0.52

33.75

–

0.62

1.63

1.78

SKN23-03

NSV

SKN23-04

NSV

Although these intercepts are not long, the strong precious and base metal contents encountered in these holes are considered the sort of values that might occur proximal to a much stronger VMS system. Combined with the latter surface discovery of high-grade precious and base metal mineralization discussed above, this lends further strong evidence for a larger VMS system in this area. Eskay Mining’s geologic team takes the view that more exploration including core drilling is warranted at Scarlet Knob in 2024.

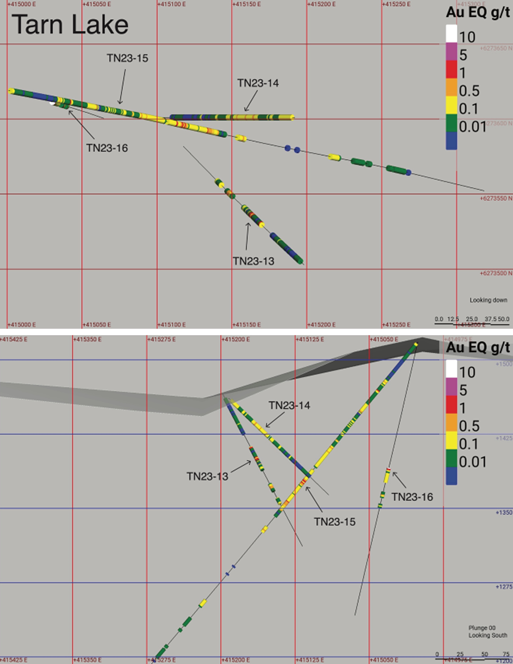

Tarn Lake

Four diamond drill holes were completed at Tarn Lake during the 2023 drill campaign (Figure 5) to follow up on encouraging drill results from this area in 2022. While all four holes encountered short to moderate length intervals of mineralization, two holes, TN23-14 and TN23-16 encountered short high-grade intervals, 4.84 gpt Au and 8.14 gpt Ag (4.94 gpt AuEq) over 2.00m in TN23-14 and 7.83 gpt Au and 6.96 gpt Ag (7.92 gpt AuEq) over 2.45m in TN23-16. These can be seen in the table below:

Hole

From (m)

To (m)

Length (m)

Au (gpt)

Ag (gpt)

Cu (%)

Pb (%)

Zn (%)

Au Eq (gpt)

TN23-13

34.00

37.69

3.69

0.48

2.69

–

–

–

0.51

43.50

48.50

5.00

0.37

4.44

–

–

–

0.43

TN23-14

66.39

67.80

1.41

3.33

0.84

–

–

–

3.34

78.40

84.40

6.00

2.07

4.82

–

–

–

2.13

includes

80.40

82.40

2.00

4.84

8.14

–

–

–

4.94

114.81

117.90

3.09

0.59

4.70

–

–

–

0.65

TN23-15

51.00

54.02

3.02

0.43

3.08

–

–

–

0.47

63.15

65.28

2.13

0.83

1.95

–

–

–

0.85

136.80

153.70

16.90

0.31

6.40

–

–

–

0.39

175.90

187.50

11.60

0.82

5.88

–

–

–

0.89

208.30

215.82

7.52

0.75

8.00

–

–

–

0.85

244.93

250.30

5.37

0.46

2.04

–

–

–

0.49

TN23-16

130.44

132.89

2.45

7.83

6.96

–

–

–

7.92

includes

130.44

131.39

0.95

12.40

10.00

–

–

–

12.53

Given the most promising results from Tarn Lake to date come from feeder zone type mineralization perhaps occurring deep in a VMS system, Eskay Mining’s geologic team is considering where the upper part of this system, including the favorable paleo-sea floor position, might lie. Rock chip sampling conducted in 2023 shows that disseminated Au mineralization extends approximately 100 m to the west of and over 200 m to the north of the drill holes at Tarn Lake (Figure 6). More field work and follow up drilling will be needed to ascertain if the better part of this system is present in the Tarn Lake area.

Other Targets

Targeting at Hexagon-Mercury (Figure 1), situated on the western flank of the Eskay Anticline approximately 9 km south of Eskay Creek mine, was driven by geophysical anomalies interpreted by Riaz Mirza of Simcoe Geoscience. One of two drill holes completed at the target yielded an intercept of over 100 m of appreciable stockwork sulfide mineralization hosted by volcanic rock thought to be part of the lower Hazelton Group. While no appreciable precious metals were encountered, moderately elevated pathfinder elements are present. Further work is needed in this location to refine future targets.

Two holes tested the Maroon Cliffs target (Figure 1) situated in the far northeast corner of the Consolidated Eskay Gold Project. Similar to Hexagon-Mercury, targeting at Maroon Cliffs was driven by geophysics. Neither hole encountered appreciable precious metal mineralization, and only weak pathfinder geochemistry. The magnetic expression that defined this target is believed to be driven by a package of conglomerate rock with magnetite-bearing clasts observed in core.

One hole was completed at Storie Creek, a target situated just 3.5 km SSE of the Eskay Creek mine. Prior to drilling, Eskay Mining’s geologic team formed the view that favorable Hazelton Group host rocks dip westward under the drill site thus making an intriguing blind target. Drilling determined that an east dipping reverse fault underlies Storie Creek. Therefore, any prospective Hazelton Group rocks will only lie to the east of Storie Creek. Consideration is being given to what further exploration might be done in the area.

Drill hole data from 2023 program:

Hole ID

Easting (m)

Northing (m)

Elevation (m)

Azimuth

Dip

Total Depth (m)

CBL23-26

408644

6261448

367

65

45

210

CBL23-27

408679

6261475

375

40

65

258

CBL23-28

408679

6261475

375

330

80

78

CBL23-29

408679

6261475

375

354

70

81

CBL23-30

408679

6261475

375

10

70

62

CBL23-31

408679

6261475

375

25

65

122

CBL23-32

408679

6261475

375

85

65

95

CBL23-33

408679

6261475

375

30

50

16.5

CBL23-34

408644

6261448

367

45

45

142

TV23-124

409628

6265299

963

283

55

299

TN23-13

415192

6273601

1461

270

44

141.2

TN23-14

415198

6273503

1465

305

55

190.4

TN23-15

415001

6273619

1518

100

50

463.2

TN23-16

415001

6273619

1518

100

75

284

SKN23-01

416097

6273570

1465

270

45

339

SKN23-02

416097

6273570

1465

295

45

289

SKN23-03

416097

6273570

1465

255

45

296

SKN23-04

416097

6273570

1465

275

65

307

MC23-02

421550

6280156

917

180

45

248

MC23-01

423441

6279855

917

180

45

260

HM23-02

408901

6270942

541

245

45

255

HM23-01

408473

6272255

831

245

45

276

SC23-01

411834

6273639

399

130

50

810

SC23-02

413145

6275147

559

130

50

151

QA/QC, Methodology Statement:

Halved HQ drill core samples are submitted to ALS Geochemistry in Terrace, British Columbia for preparation and analysis. ALS is accredited to the ISO/IEC 17025 standard for gold assays. All analytical methods include quality control standards inserted at set frequencies. The entire sample interval is crushed and homogenized, 250 g of the homogenized sample is pulped. All samples were analyzed for gold, silver, mercury, and a suite of 48 major and trace elements. Analysis for gold is by fire assay fusion followed by Inductively Coupled Plasma Atomic Emission Spectroscopy (ICP-AES) on 30 g of pulp. Analysis for silver is by fire assay and gravimetric analysis on 30 g of pulp. Mercury is analyzed using the trace Hg Inductively Coupled Plasma Mass Spectroscopy (ICP-MS) method. All other major and trace elements are analyzed by four-acid digestion followed by ICP-MS.

The assay results for rock chip samples reported for Scarlet Knob were obtained from Skeena Resources field assay laboratory. The entire sample is crushed and homogenized, and 100g of the homogenized sample is pulped. All samples were analyzed for gold, silver, arsenic, copper, lead, and zinc. Duplicates of these samples were sent to ALS Geochemistry in Terrace, British Columbia for certified analyses. Certified assay results for the Scarlet Knob rock chip samples are pending.

Historical rock chip and soil sample data is sourced from Assessment Reports AR17205 and AR22231. Eskay Mining is unable to fully verify this data, and it should be treated as such by the reader.

Mineralization at the TV and Jeff deposits displays similar characteristics and mineralogy to the Eskay Creek deposit and therefore for Au eq, and Au:Ag, a ratio of 78:1 is used and Au eq and Ag eq values are deemed to be reasonable based on assumed gold recovery (84.2%) and silver recovery (87.3%) as reported in the Eskay Creek Project NI 43-101 Technical Report and Prefeasibility Study, British Columbia, Canada, Effective Date: 22 July, 2021, Prepared for: Skeena Resources Ltd., Prepared by: Absence Engineering Canada Inc.

True widths of reported intercepts are not fully understood at this time. More drilling is required to ascertain true widths at these newly identified mineralized areas.

Dr. Quinton Hennigh, P. Geo., a Director of the Company and its technical adviser, a qualified person as defined by National Instrument 43-101, has reviewed and approved the technical contents of this news release.

About Eskay Mining Corp:

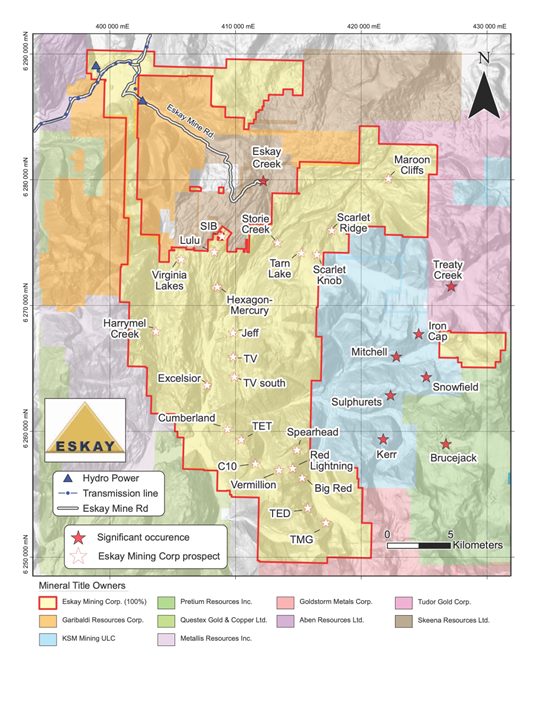

Eskay Mining Corp (TSX-V:ESK) is a TSX Venture Exchange listed company, headquartered in Toronto, Ontario. Eskay is an exploration company focused on the exploration and development of precious and base metals along the Eskay rift in a highly prolific region of northwest British Columbia known as the “Golden Triangle,” 70km northwest of Stewart, BC. The Company currently holds mineral tenures in this area comprised of 177 claims (52,600 hectares).

All material information on the Company may be found on its website at www.eskaymining.com and on SEDAR at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements: This Press Release contains forward-looking statements that involve risks and uncertainties, which may cause actual results to differ materially from the statements made. When used in this document, the words “may”, “would”, “could”, “will”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “expect” and similar expressions are intended to identify forward-looking statements. Such statements reflect our current views with respect to future events and are subject to risks and uncertainties. Many factors could cause our actual results to differ materially from the statements made, including those factors discussed in filings made by us with the Canadian securities regulatory authorities. Should one or more of these risks and uncertainties, such as actual results of current exploration programs, the general risks associated with the mining industry, the price of gold and other metals, currency and interest rate fluctuations, increased competition and general economic and market factors, occur or should assumptions underlying the forward looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, or expected. We do not intend and do not assume any obligation to update these forward-looking statements, except as required by law. Shareholders are cautioned not to put undue reliance on such forward-looking statements.

(Figure 1. Plan view of Eskay Mining’s land holdings at Consolidate Eskay Gold Project.)

(Figure 2. Plan view (top) and section looking southeast (bottom) showing assay results in Au equivalent for 2023 drill holes at Cumberland.)

(Figure 3. Map of the Cumberland prospect showing Ag values in soil samples and Au in rock chip samples reported in assessment reports 17205 and 22231. The Ag anomaly immediately south of Cumberland lies along the trend of mineralization as determined by drilling and field work in 2023.)

(Figure 4. Magnetic map of the Cumberland-Excelsior-Mahogany Ridge-TV area showing soil sample results from the 2021-2022 exploration programs and historic sampling programs reported in assessment reports 17205, and 22231. There are pronounced magnetic and Ag soil anomalies along trend from mineralization at the Cumberland prospect. This area will be a focus of exploration activities in 2024.)

(Figure 5. Plan view (top) and section looking southeast (bottom) showing assay results in Au equivalent for 2023 drill holes at Tarn Lake.)

(Figure 6. Map of the Bruce Glacier area showing the drill traces at Tarn Lake and Scarlet Knob, and Au assay results for rock chip samples collected during the 2021-2023 exploration programs. An approximately 100 m long and 5 m wide trend of semi-massive replacement-style polymetallic sulfide mineralization at Scarlet Knob yielded several Au- and Ag-bearing samples. Sampling at Tarn Lake shows that disseminated Au mineralization extends at least 100 m west of and 200 m north of 2022-2023 drilling. Both of these areas remain high-priority targets for exploration in 2024.)

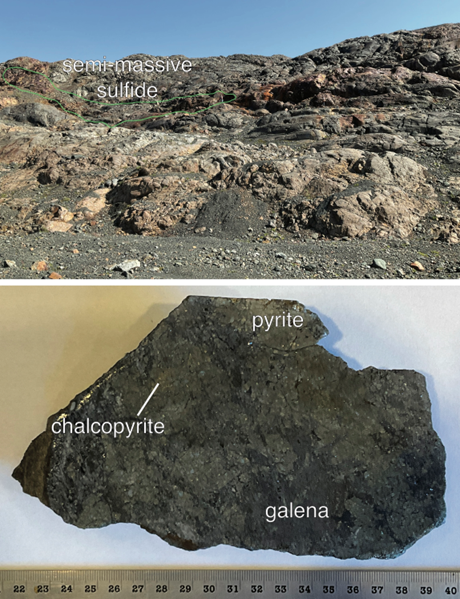

(Figure 7. Top: The trend of semi-massive sulfide mineralization that was sampled at Scarlet Knob, with geologist for scale. Bottom: Photograph of sample 1001B showing massive polymetallic sulfide mineralization. This zone is associated with an andesite dike, with the most intense mineralization associated with sulfide replacement of volcaniclastic debris flow breccia surrounding the dike. The presence of replacement-style mineralization indicates a stratigraphic position within 200 m of the paleoseafloor. The confirmation of a paleoseafloor horizon in the 2023 drill holes at Scarlet Knob, raises the possibility that the VMS system that produced the replacement-style mineralization shown above may have fed seafloor vents. Investigation of this possibility will be an objective of the 2024 exploration program.)

VANCOUVER, BC, Oct. 30, 2023 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company“) (TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce that it has filed the detailed Technical Report (the “Technical Report“) of its updated Mineral Resource Estimate (“2023 MRE“) for its 100% owned Wicheeda Rare Earth Element (REE) deposit located in British Columbia, Canada. The Technical Report is dated October 27, 2023, effective August 28, 2023, is entitled “Technical Report on the Wicheeda Property, British Columbia, Canada”, and was prepared by APEX Geoscience Ltd.

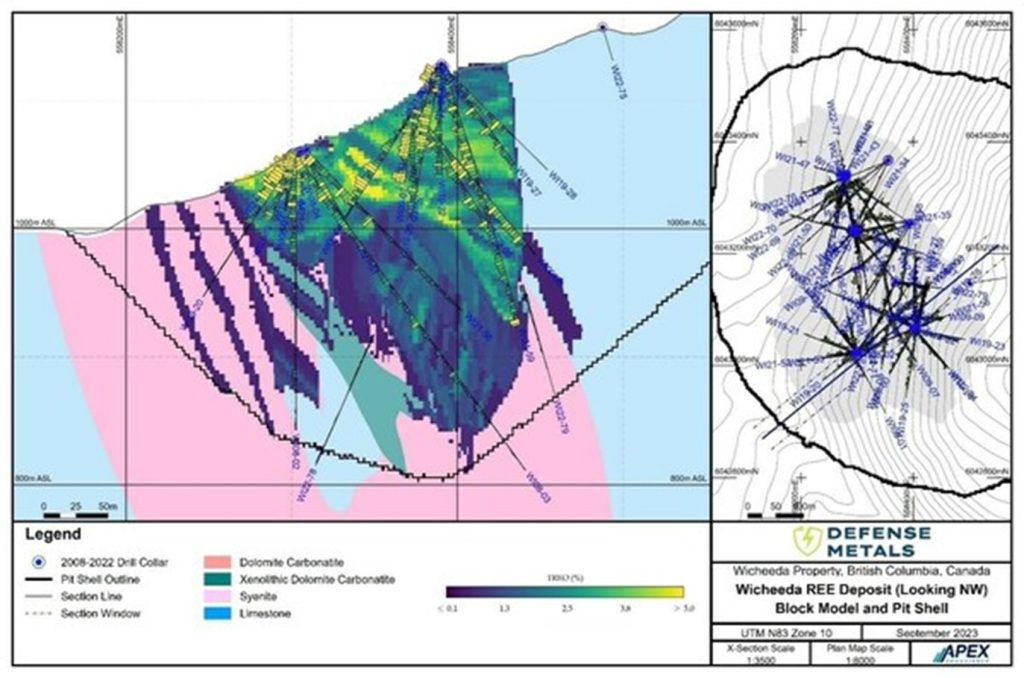

Figure 1: Cross Section of the Wicheeda RE Deposits 2023 MRE (CNW Group/Defense Metals Corp.)

The results of the updated 2023 MRE were previously disclosed in summary form in the Company’s news release dated September 12, 2023. The Technical Report was prepared in accordance with the Canadian Securities Administrators’ National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101“) and is available for review under the Company’s profile on SEDAR+ at www.sedarplus.ca and on the Company’s website at www.defensemetals.com. Readers are encouraged to read the Technical Report in its entirety, including all qualifications, assumptions, and exclusions.

Highlights of the 2023 Wicheeda REE Deposit Mineral Resource Estimate

The 2023 MRE comprises a:

6.4 million tonne Measured Mineral Resource, averaging 2.86% Total Rare Earth Oxide (TREO1);

a 27.8 million tonne Indicated Mineral Resource, averaging 1.84 % TREO;

and an 11.1 million tonne Inferred Mineral Resource, averaging 1.02% TREO, all reported at a cut-off grade of 0.5% TREO within a conceptual open pit shell (Figure 1);

Total Measured and Indicated (M+I) Mineral Resources of 34.2 million tonnes, averaging 2.02% TREO, is a significant upgrade representing a conversion of 101% of the 2021 MRE comprising some indicated and mostly inferred resources (see Defense Metals’ news release of November 24, 2021) to M+I on a contained metal basis;

Measured and Indicated resources are inclusive of 17.8 million tonnes of dolomite carbonatite, averaging 2.92% TREO;

The 2023 MRE represents a 17% increase in TREO on a contained metal basis, or 31% tonnage increase, in comparison to the prior 2021 MRE.

The 2023 MRE is based on an updated geological model that incorporates an additional 10,350 metres of drillhole data, from 45 holes drilled by Defense Metals during 2021 and 2022.

___________________________ 1 TREO % is the sum of CeO2, La2O3, Nd2O3, Pr6O11, Sm2O3, Eu2O3, Gd2O3, Tb4O7, Dy2O3 and Ho2O3 %.

Defense Metals to Attend New Orleans Investment Conference

Defense Metals also announces that it will be attending in the New Orleans Investment Conference in New Orleans, U.S., from November 1-4, 2023.

For additional information on the conference please visit the following link:

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (B.C.), Principal and Consultant of APEX Geoscience Ltd. of Edmonton, Alberta, who is a director of Defense Metals and a “Qualified Person” as defined in NI 43-101.

About the Wicheeda REE Property

Defense Metals 100% owned, 6,759-hectare (~16,702-acre) Wicheeda Project is located approximately 80 km northeast of the city of Prince George, British Columbia; population 77,000. The Wicheeda REE Project is readily accessible by all-weather gravel roads and is near infrastructure, including hydro power transmission lines and gas pipelines. The nearby Canadian National Railway and major highways allow easy access to the port facilities at Prince Rupert, the closest major North American port to Asia.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the development of its 100% owned Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades on the TSX Venture Exchange under the symbol “DEFN”, in the United States, trading symbol “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Defense Metals is a proud member of Discovery Group. For more information please visit: http://www.discoverygroup.ca/

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

The Company previously completed a preliminary economic assessment NI 43-101 technical report on January 6, 2022, effective November 21, 2021 (“PEA”), however, given the exploration work completed since and the new mineral resource estimate of August 28, 2023 and included in the Technical Report, the Company does not consider the PEA current and therefore the Wicheeda REE Project is no longer considered an “advanced property” as that term is defined under applicable securities laws.

This news release contains “forward‐looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, the Technical Report and the 2023 MRE, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, accuracy of assay results, performance of available laboratory and other related services, future operating costs, interpretation of geological and metallurgical data, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration and metallurgical results, risks related to the inherent uncertainty of exploration, metallurgy and development and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR+ at www.sedarplus.ca. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological, metallurgical and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 and other viruses and diseases on the business of the Company, the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward‐looking statements or forward‐looking information, except as required by law.

Newrange is focused on district-scale exploration for precious metals in the prolific Red Lake District of northwestern Ontario. The past-producing high-grade Argosy Gold Mine is open to depth, while the adjacent North Birch Project offers additional blue-sky potential. Focused on developing shareholder value through exploration and development of key projects, the Company is committed to building sustainable value for all stakeholders. Further information can be found on our website at www.newrangegold.com .

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transaction wins shareholder approval. In May,Newrange executed a binding Scheme Implementation Deed (SID) to acquire 100% of Mithril Resources Limited (ASX: MTH) in a reverse takeover (RTO). Pending approval by the TSX Venture Exchange, the resulting company will be named Pinnacle Silver & Gold Corp. and will be listed on the TSX Venture exchange under the symbol “PINN.” During their respective special meetings, Newrange and Mithril shareholders approved the merger between Newrange and Mithril to form Pinnacle Silver & Gold Corporation. Assuming that all requirements are satisfied, the transaction is expected to close in mid-November.

Key conditions remain. Although both sets of shareholders have approved the transaction, several requirements remain outstanding. These include: 1) the Federal Court of Australia must approve the transaction at a hearing scheduled for November 6, 2) an Independent Expert must affirm that in the absence of a superior offer, the share and option schemes are in the best interests of Mithril shareholders and option holders, 3) completion of Newrange Gold’s concurrent financing, 4) Newrange Gold receiving unconditional approval to re-list on the TSX Venture Exchange, and 5) satisfaction or waiver of any remaining conditions prior to the Court Hearing.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

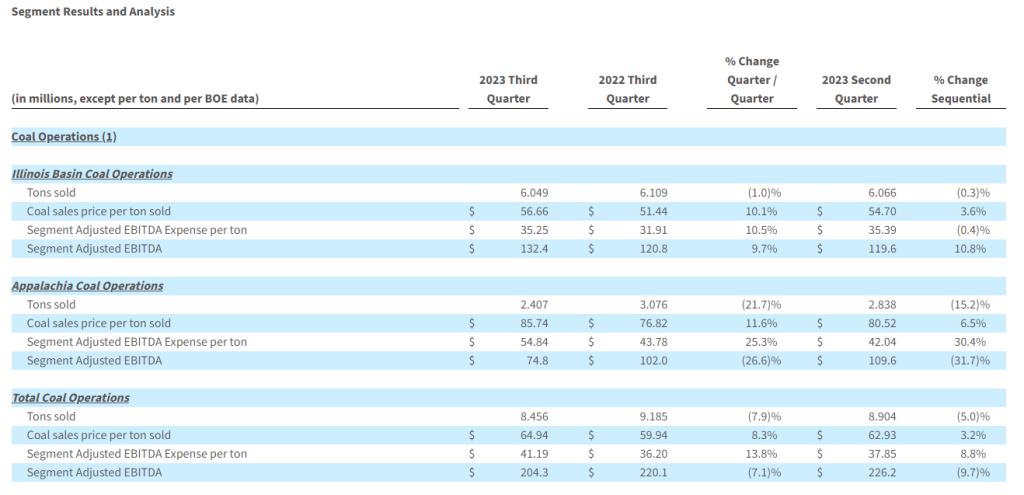

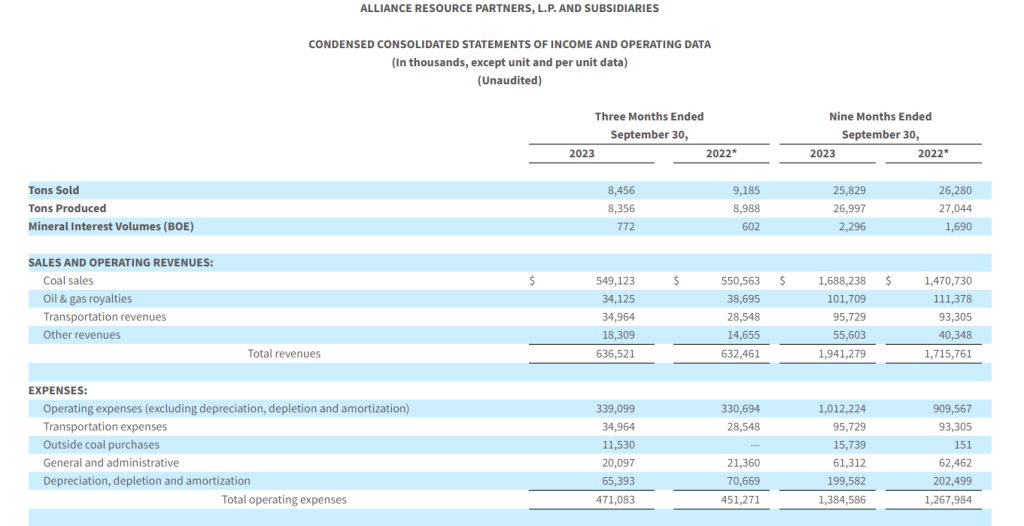

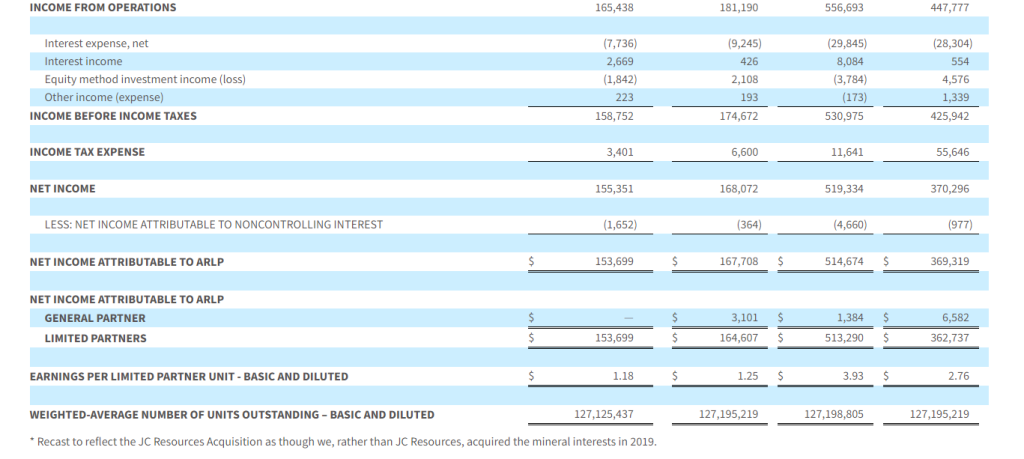

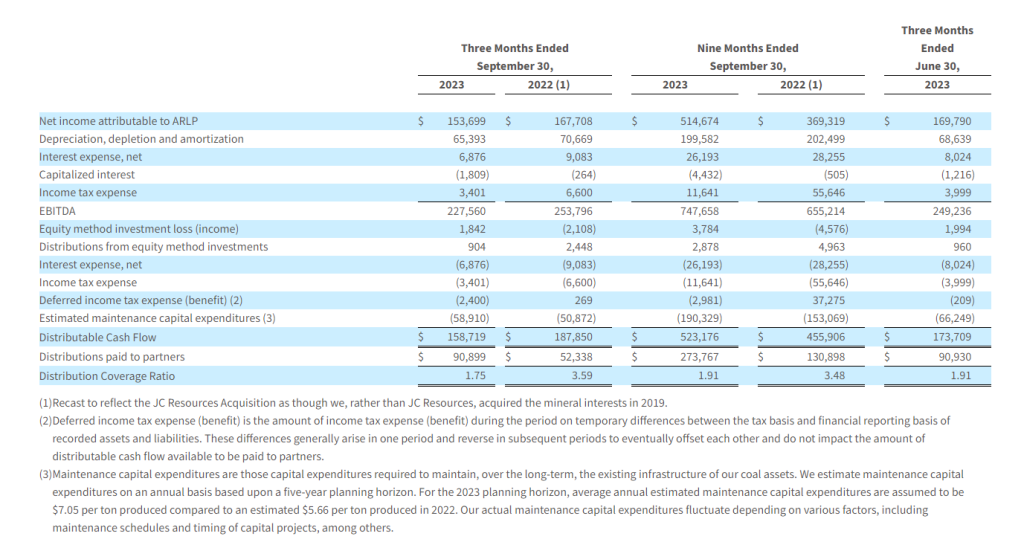

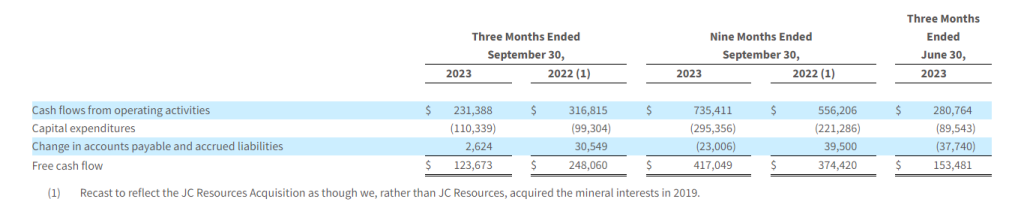

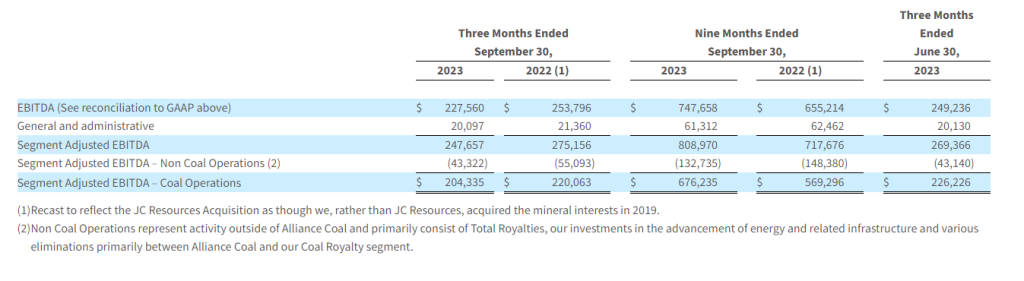

Third quarter financial results. Alliance reported third quarter EBITDA and earnings per unit (EPU) of $227.6 million and $1.18, respectively, compared to $253.8 million and $1.25 during the prior year period. We had forecast EBITDA and EPU of $240.3 million and $1.20. Revenue increased 0.6% to $636.5 million, while income from operations declined 8.7% to $165.4 million. The company generated free cash flow of $123.7 million and distributable cash flow provided quarterly cash distribution coverage of 1.75x. Third quarter financial results were negatively impacted by lower coal sales volumes and higher costs at its coal operations in Appalachia.

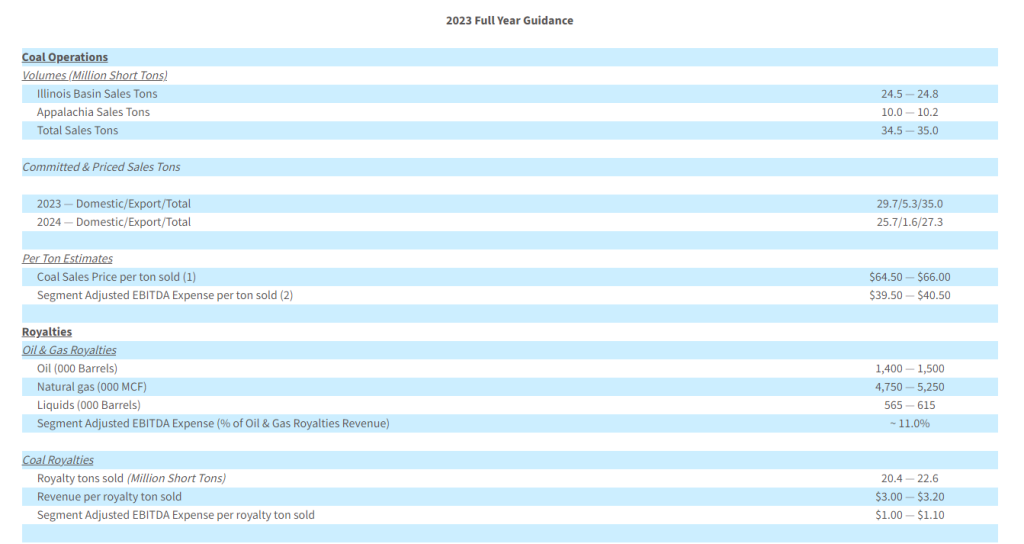

Refined management guidance. Alliance provided updated guidance for the remainder of the year which we have incorporated into our estimates as detailed in the body of this note. Total coal sales are expected to be in the range of 34.5 million to 35.0 million tons compared to previous expectations of 35.5 million to 36.0 million tons, while the coal sales price per ton is expected to be in the range of $64.50 to $66.00 compared to previous guidance of $65.00 to $66.00. Segmented adjusted EBITDA expense per ton sold is expected to be $39.50 to $40.50 compared to previous guidance of $38.00 to $41.00.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

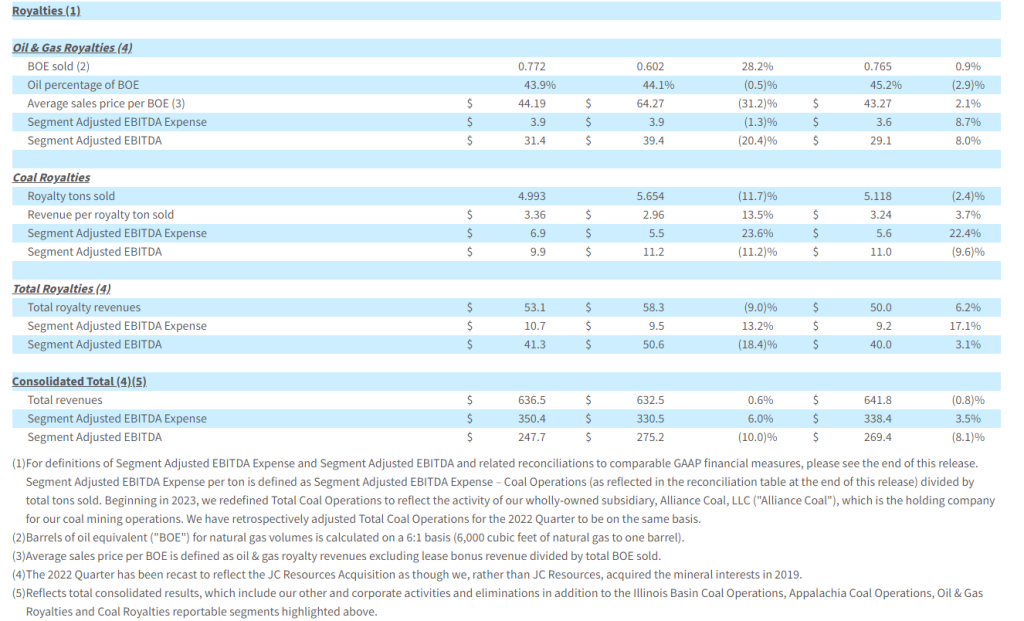

Coal sales price realizations of $64.94 per ton sold, up 8.3% year-over-year

Record oil & gas royalty volumes of 772 MBOE sold, up 28.2% year-over-year

Completed two strategic new ventures investments, totaling approximately $50.0 million

Declares a quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized, up 40.0% year-over-year

Reduced outstanding senior notes by $54.6 million during the 2023 Quarter, resulting in total and net leverage ratio of 0.36 times and 0.17 times, respectively

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter ended September 30, 2023 (the “2023 Quarter”). Total revenues in the 2023 Quarter increased slightly to $636.5 million compared to $632.5 million for the quarter ended September 30, 2022 (the “2022 Quarter”) primarily as a result of higher transportation and other revenues, partially offset by lower oil & gas royalties. Net income for the 2023 Quarter was $153.7 million, or $1.18 per basic and diluted limited partner unit, compared to $167.7 million, or $1.25 per basic and diluted limited partner unit, for the 2022 Quarter as a result of increased total operating expenses, partially offset by higher interest income and lower income tax expense. EBITDA for the 2023 Quarter was $227.6 million compared to $253.8 million in the 2022 Quarter. (Unless otherwise noted, all references in the text of this release to “net income” refer to “net income attributable to ARLP.”)

Compared to the quarter ended June 30, 2023 (the “Sequential Quarter”), total revenues in the 2023 Quarter decreased 0.8% primarily as a result of lower coal sales volumes of 8.5 million tons sold compared to 8.9 million tons sold in the Sequential Quarter, partially offset by higher average coal sales prices, which increased 3.2% to $64.94 per ton sold in the 2023 Quarter. Lower revenues and higher total operating expenses contributed to a reduction in net income and EBITDA of 9.5% and 8.7%, respectively, compared to the Sequential Quarter. (For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.)

Financial and operating results for the nine months ended September 30, 2023 (the “2023 Period”) increased compared to the nine months ended September 30, 2022 (the “2022 Period”). Coal sales prices and coal sales revenues during the 2023 Period were higher by 16.8% and 14.8%, respectively, compared to the 2022 Period. Increased revenues and lower income tax expense were partially offset by higher total operating expenses in the 2023 Period, which resulted in higher net income and EBITDA by 39.4% and 14.1%, respectively, both as compared to the 2022 Period.

CEO Commentary

“Our well-contracted coal order book enabled us to navigate an otherwise challenging operating environment during the 2023 Quarter,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Our coal segment achieved higher realized pricing per ton sold relative to both the 2022 and Sequential Quarters, a theme that continues to favorably impact year-to-date results, particularly with regards to EBITDA and net income. However, we faced some difficult mining conditions in Appalachia at all three mines during the 2023 Quarter, which resulted in higher operating costs and fewer tons produced versus previous expectations.”

Mr. Craft added, “Our Oil & Gas Royalties segment reported continued growth resulting in record production volumes, underscoring the success of recent acquisitions in core parts of the prolific Permian Basin. Although average realized pricing per BOE during the 2023 Quarter was lower compared to near record levels in the 2022 Quarter, our royalty portfolio is well-positioned to provide significant cash flow via hedge-free exposure to commodity price and cost-free organic growth.”

Mr. Craft concluded, “We are excited to announce direct investments in Ascend Elements and Infinitum during the 2023 Quarter. These companies are led by proven management teams and possess innovative, commercial technologies that, in our view, will reshape their respective industries. Beyond our direct investments, we are actively engaged in discussions with both companies to explore additional strategic opportunities intended to unlock value and growth for our unitholders.”

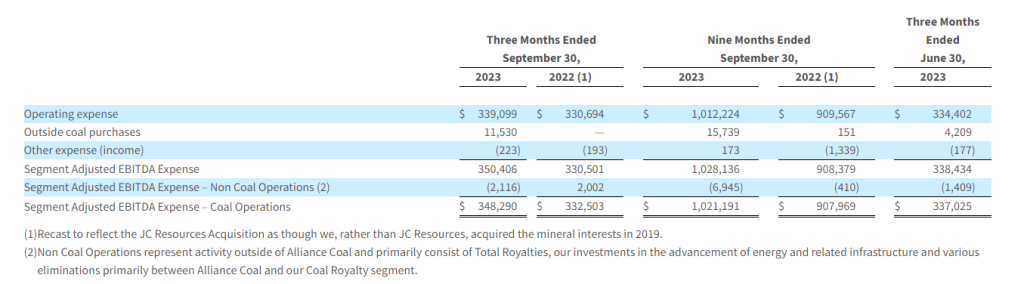

Coal Operations

ARLP’s coal sales prices per ton increased in all regions compared to both the 2022 and Sequential Quarters. Improved domestic pricing, partially offset by lower export price realizations, drove coal sales prices higher by 10.1% and 3.6% in the Illinois Basin and 11.6% and 6.5% in Appalachia as compared to the 2022 and Sequential Quarters, respectively. Tons sold decreased by 21.7% and 15.2% in Appalachia compared to the 2022 and Sequential Quarters, respectively, due to reduced volumes across the region caused by lock outages, customer plant maintenance, reduced operating units at MC Mining, and unique geologic conditions that delayed development of a new district at our Mettiki longwall operation. ARLP ended the 2023 Quarter with total coal inventory of 1.8 million tons, representing an increase of 0.5 million tons compared to the end of the 2022 Quarter and comparable to the end of the Sequential Quarter.

Segment Adjusted EBITDA Expense per ton for the 2023 Quarter increased by 10.5% in the Illinois Basin compared to the 2022 Quarter, resulting from increased sales-related expenses due to higher price realizations and higher labor-related, roof support and maintenance costs due to days lost by a sizable roof fall in July and a longwall move in August at our Hamilton mine. Segment Adjusted EBITDA Expense per ton in Appalachia increased by 25.3% and 30.4% compared to the 2022 and Sequential Quarters, respectively, due primarily to lower production volumes, purchased coal and increased labor-related, roof support, maintenance and selling expenses per ton.

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased to $31.4 million in the 2023 Quarter compared to $39.4 million in the 2022 Quarter. The decrease was directly connected to lower price realizations, which decreased by 31.2%, partially offset by record oil & gas volumes, which increased 28.2% to 772 MBOE sold in the 2023 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA increased by 8.0% due to higher prices and volumes. Higher volumes during the 2023 Quarter resulted from increased drilling and completion activities on our interests and the acquisition of additional oil & gas mineral interests.

Segment Adjusted EBITDA for the Coal Royalties segment was $9.9 million for the 2023 Quarter, representing a decrease of $1.3 million and $1.1 million compared to the 2022 and Sequential Quarters, respectively, as a result of lower royalty tons sold and increased selling expenses, partially offset by higher average royalty rates per ton received from the Partnership’s mining subsidiaries.

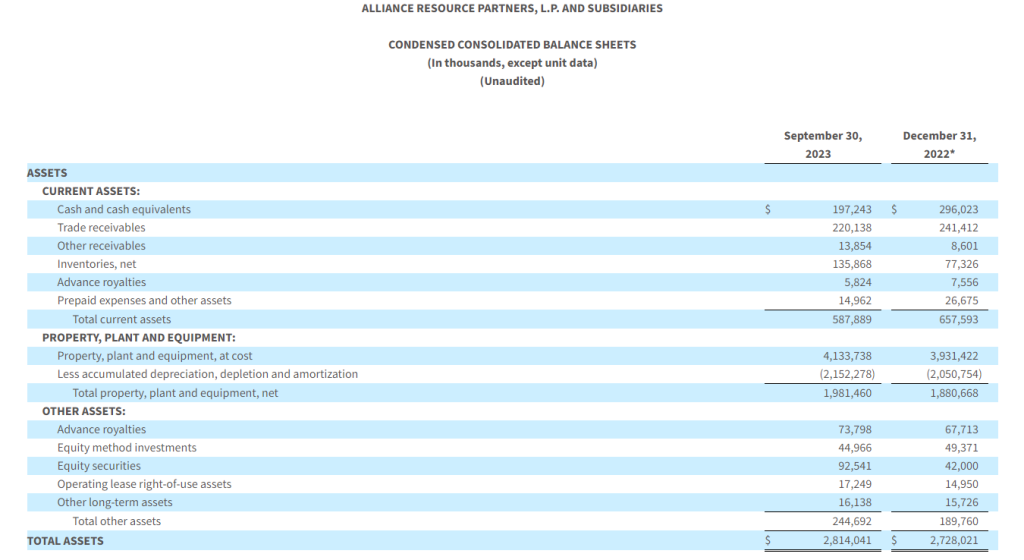

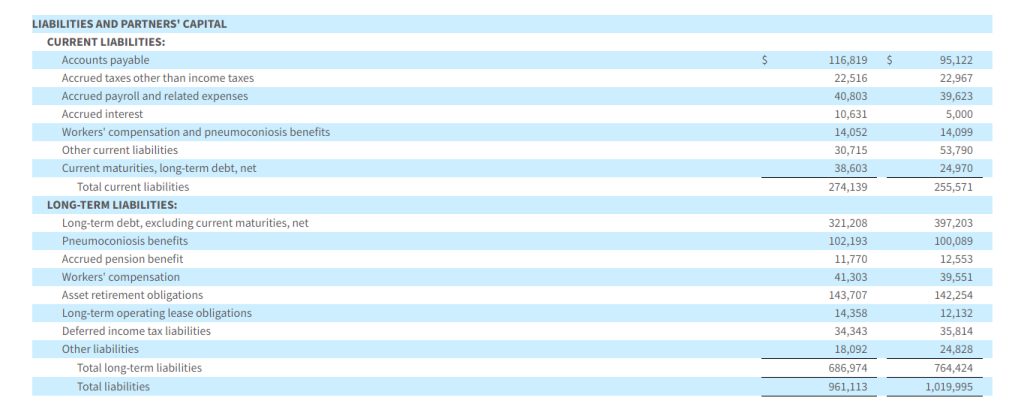

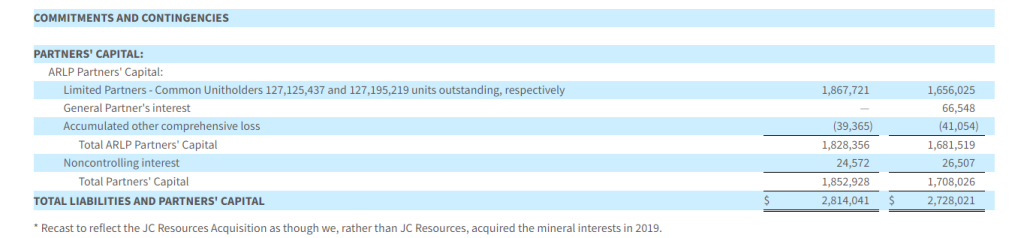

Balance Sheet and Liquidity

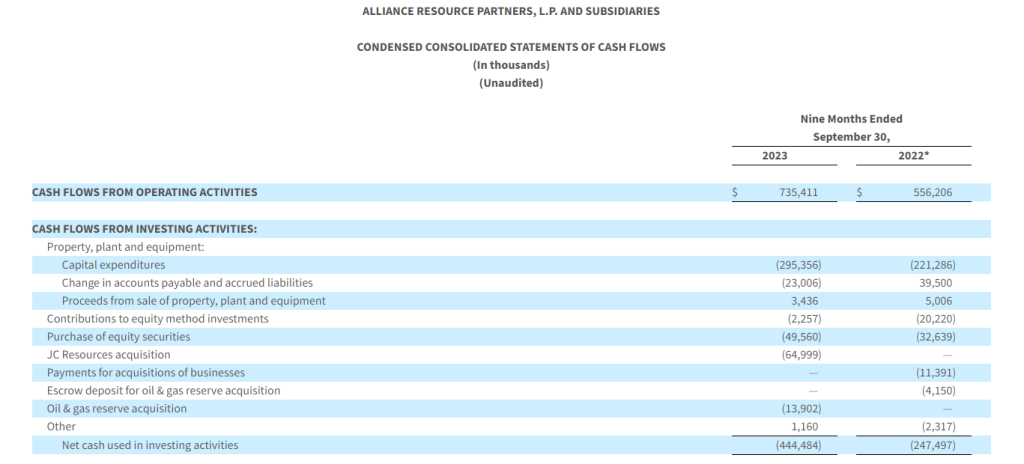

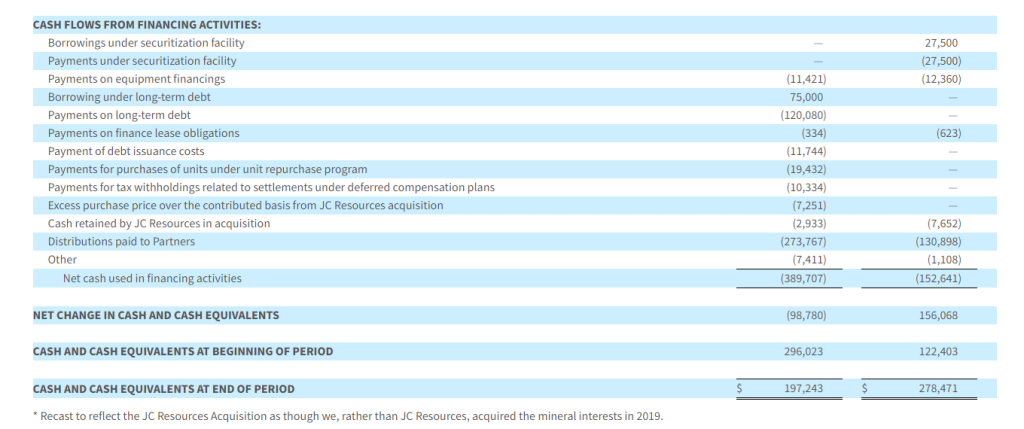

As of September 30, 2023, total debt and finance leases outstanding were $371.0 million, including $284.6 million in ARLP’s 2025 senior notes. During the 2023 Quarter, ARLP redeemed $50.0 million and repurchased $4.6 million of its senior notes due May 1, 2025. The Partnership’s total and net leverage ratio was 0.36 times and 0.17 times, respectively, as of September 30, 2023. ARLP ended the 2023 Quarter with total liquidity of $629.5 million, which included $197.2 million of cash and cash equivalents and $432.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

Distributions

On October 25, 2023, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2023 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on November 14, 2023, to all unitholders of record as of the close of trading on November 7, 2023. The announced distribution represents a 40.0% increase over the cash distribution of $0.50 per unit for the 2022 Quarter and is consistent with the Sequential Quarter cash distribution.

Strategic Investments

During the 2023 Quarter, ARLP invested approximately $50 million in two companies that align with the Partnership’s strategy to allocate a portion of excess cash flows into high-growth businesses where ARLP can leverage its core competencies to generate meaningful, risk-adjusted returns.

Ascend Elements, Inc. (“Ascend Elements”)

As previously announced, on September 6, 2023, ARLP invested $25 million in Ascend Elements, a U.S.-based manufacturer and recycler of sustainable, engineered battery materials for electric vehicles, as part of its $460 million Series D funding round. This capital, combined with $480 million in total grants awarded by the Department of Energy, will advance construction of North America’s first commercial-scale manufacturing facility, located near Hopkinsville, Kentucky, producing cathode materials for electric vehicle batteries.

In close proximity to ARLP’s western Kentucky mining operations, when complete, the 1-million-square-foot manufacturing facility will produce enough cathode materials for 750,000 electric vehicles per year. ARLP intends to explore other strategic opportunities with Ascend Elements to expand investment in the battery recycling industry and leverage our unique operational expertise, geographic footprint, and strategic relationships in Kentucky and the surrounding battery-belt states to drive value creation for both companies.

Infinitum

During the 2023 Quarter, ARLP invested an additional $24.6 million in Infinitum, a Texas-based developer and manufacturer of high-efficiency electric motors, as part of their ongoing Series E equity raise. The incremental amount brings ARLP’s total investment in the company to approximately $67 million. Infinitum believes that its patented air core motors offer superior performance in half the weight and size, at a fraction of the carbon footprint of traditional motors, making them pound for pound the most efficient in the world.

In addition to the investment, ARLP’s wholly-owned subsidiary Matrix Design Group LLC (“Matrix“) and Infinitum are actively evaluating opportunities to combine Matrix’s underground mining expertise with Infinitum’s technology to deliver much needed innovation to the growing global mining industry by improving the safety, efficiency, and performance of certain mining machinery.

Outlook

“As we assess current market conditions, we have elected to slightly adjust our full year 2023 guidance for coal sales volumes and pricing, which will be highly dependent on logistics during the fourth quarter,” commented Mr. Craft. “We expect Appalachia operating expense per ton sold to be 8-10% higher during the fourth quarter of 2023 as development for the new district at Mettiki is not expected to be complete until late November 2023 and Tunnel Ridge has a normally scheduled longwall move. The new longwall district at Mettiki allows us to develop longer panels that will increase production and reduce unit costs in 2024.”

Mr. Craft closed, “As we look beyond 2023, we are encouraged by improving fundamentals for coal export demand based on recent trends in international benchmark pricing and emerging opportunities we see in the market. On the domestic front, we hold firm in our conviction that the reliability of our product is highly valued by our customers and the long-term potential for higher natural gas prices and growth in electric demand will sustain our projections for coal demand and lead to a slowing in the pre-mature closure of coal-fired power plants in the eastern U.S.”

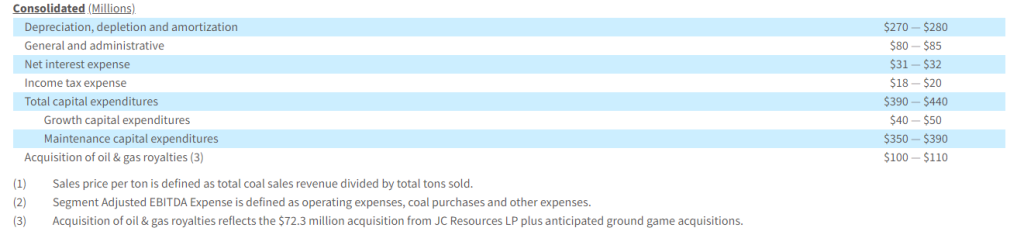

ARLP is providing the following updated guidance for the 2023 full year:

Conference Call

A conference call regarding ARLP’s 2023 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13741573.

Concurrent with this announcement, we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

***

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.