ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

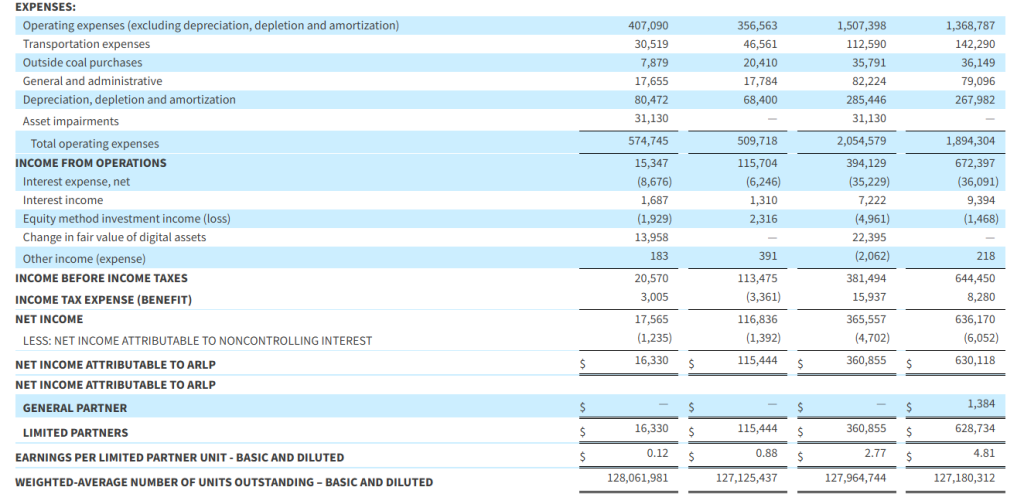

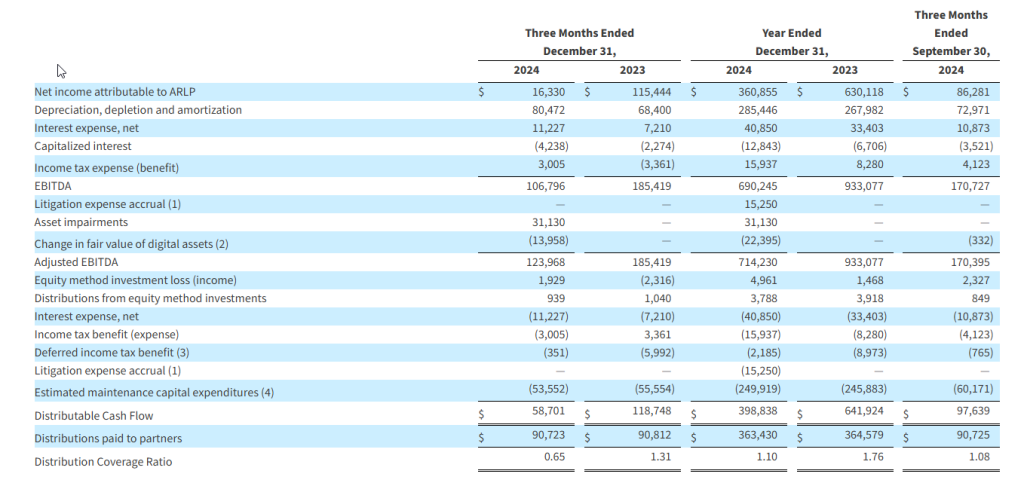

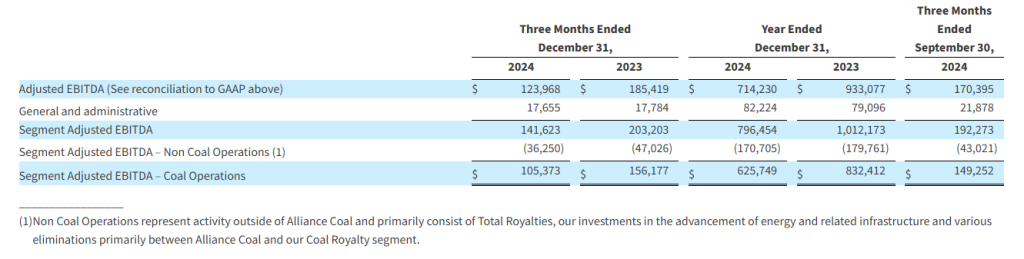

Full year and fourth quarter 2024 financial results. On a full year basis, Alliance generated 2024 adjusted EBITDA of $714.2 million and earnings per unit (EPU) of $2.77, respectively, compared to $933.1 million and $4.81 in 2023. Fourth quarter adjusted EBITDA was $124.0 million, and EPU amounted to $0.12, respectively, compared to $185.4 million and $0.88 during the prior year period. Fourth quarter and full year results were impacted by lower coal volumes, operational challenges within ARLP’s coal operations in Appalachia, and a $30.1 million non-cash asset impairment charge which had a negative impact of ~$0.24 per unit.

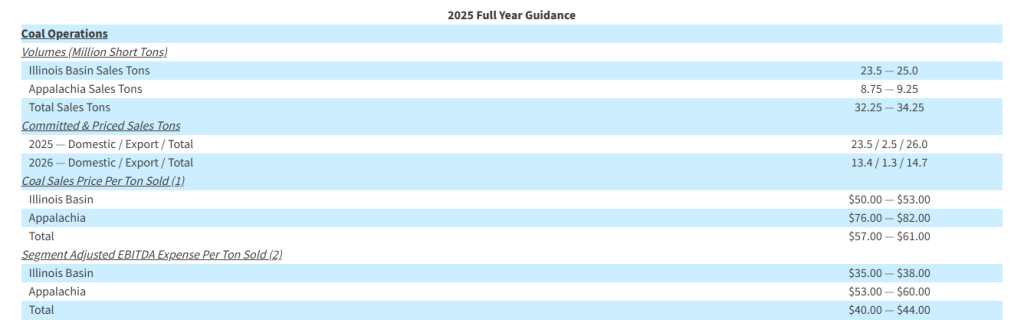

Management guidance for 2025. Coal sales are expected to be in the range of 32.25 million to 34.25 million tons, while the sales price of coal per ton is expected to be in the range of $57.00 to $61.00. Segmented adjusted EBITDA expense per ton sold is expected to be $40.00 to $44.00. The company has committed and priced 26.0 million tons of its 2025 sales volume, including 23.5 million for the domestic market and 2.5 million tons for the export market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

February 4, 2025 – Vancouver, Canada – Century Lithium Corp. (TSXV:LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (“Century Lithium” or “the Company”) is pleased to provide an update on its wholly owned Angel Island project near Silver Peak, Nevada, USA and associated Lithium Extraction Facility (“Pilot Plant”) in Amargosa Valley Nevada. The Company has completed the successful implementation of process improvements at its Pilot Plant. These changes were developed in collaboration with Amalgamated Research, LLC (“ARi”) of Twin Falls, Idaho, a research and development company specializing in industrial implementation of process technologies. Century Lithium is now shifting the focus at its Pilot Plant from research and development to demonstration.

“The initial results from ARi are very encouraging, indicating greater efficiency can be achieved that could result in positive reductions in the estimated capital and operating costs at Angel Island,” said Century Lithium President and CEO, Bill Willoughby. “Century Lithium remains committed to delivering value to our shareholders through Angel Island, one of the few advanced lithium projects in the United States. We are optimistic about the long-term fundamentals of the lithium market and the strategic importance of Angel Island to the future mineral supply in the United States.”

Project Update

The processing testing program (“Program”) implemented ARi’s proprietary adsorption-based technology for Direct Lithium Extraction (“DLE”) and was accomplished in conjunction with ARi’s Twin Falls testing facilities and Century Lithium’s Pilot Plant. The results of the Program are positive and further validate the efficiency of Century Lithium’s extraction technology. The Program augmented Century Lithium’s DLE system with the addition of ARi equipment and expertise. Early results indicate Century Lithium can eliminate the recycle loops within its DLE and lithium carbonate areas, while increasing eluate grades. The Company believes this will result in a substantial reduction in estimated capital and operating costs at Angel Island.

The decision to shift the focus at the Pilot Plant to demonstration mode is two-fold; it will allow the Company to focus on providing dedicated testing to prospective strategic partners or potential end-users and reduce the ongoing operating costs of the Pilot Plant. Current Pilot Plant operations will continue to convert a backlog of lithium solutions, which were made prior to the commissioning of the on-site lithium carbonate process at the Pilot Plant, into battery-grade lithium carbonate.

Moving Forward

The Company recently announced a non-binding Memorandum of Understanding (“MOU”) with Orica Specialty Mining Chemicals (see news release). The non-binding MOU outlines the intent of Century Lithium and Orica to formalize a multiyear offtake agreement for Orica to purchase sodium hydroxide from Angel Island. The favorable outlook for the sodium hydroxide by-product contributes significantly to Century Lithium’s low-cost lithium carbonate production model.

Ongoing engineering is focused on mining, and the leaching, filtration, DLE, and lithium carbonate processing areas. The Company continues to compile all data generated at the Pilot Plant. The data will be used in engineering models and to run analytical tests on full-scale construction designs focused on further reducing the estimated capital and operating costs for producing lithium carbonate at Angel Island.

Century Lithium remains focused on seeking strategic partnerships with potential end-users and market participants interested in securing a domestic supply of battery-grade lithium carbonate. The Company continues to move forward with permitting work to ensure that our future operations at Angel Island will align with both regulatory requirements and Century Lithium’s environmental and social stewardship goals.

Qualified Person

Todd Fayram, MMSA-QP and Senior Vice President, Metallurgy of Century Lithium is the qualified person as defined by National Instrument 43-101 and has approved the technical information in this release.

ABOUT Ari

Amalgamated Research LLC (ARi) is a supplier of chromatography, adsorption, and ion exchange technology and equipment specialized in commercializing innovative technology at large industrial scale. ARi has developed a cost-effective and streamlined solution for adsorption-based direct lithium extraction that maximizes plant profitability while minimizing upfront capital cost. ARi’s patented fluid distribution and mixing technology de-risks scale-up allowing separation processes to be reliably scaled from pilot plant data up to industrial vessels exceeding 20-ft in diameter, with no degradation in equipment performance. ARi provides a full spectrum of customer support services, from proof of concept through to industrial-scale installation. Comprehensive analytical services and a wide range of pilot equipment are available on-site to support process development and scale-up. Please visit arifractal.net for more information.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced stage lithium company, focused on developing its wholly owned Angel Island project in Esmeralda County, Nevada, which hosts one of the largest sedimentary lithium deposits in the United States. The Company has utilized its patent-pending process for chloride leaching combined with direct lithium extraction to make high purity lithium carbonate product samples from Angel Island lithium-bearing claystone on-site at its Pilot Plant in Amargosa Valley, Nevada.

Angel Island is one of the few advanced lithium projects in development in the United States to provide an end-to-end process to produce battery quality lithium carbonate for the growing electric vehicle and battery storage market. Angel Island is currently in the permitting stage for a three-phase feasibility-level production plan expected to yield an average of 34,000 tonnes per year of lithium carbonate over a 40-year mine-life.

Century Lithium trades on both the TSX Venture Exchange under the symbol “LCE” and the OTCQX under the symbol “CYDVF”; and on the Frankfurt Stock Exchange under the symbol “C1Z”.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.

These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein. These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.com. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

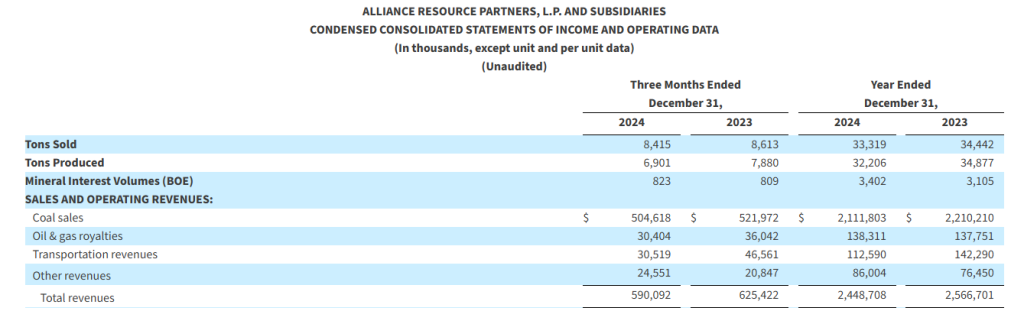

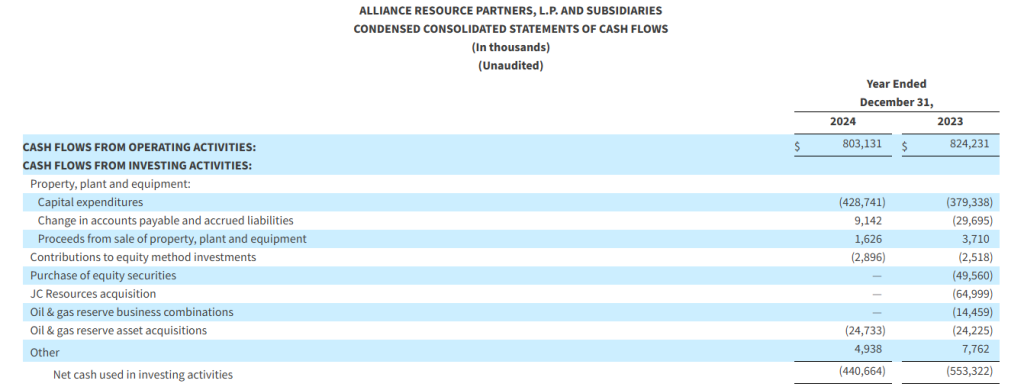

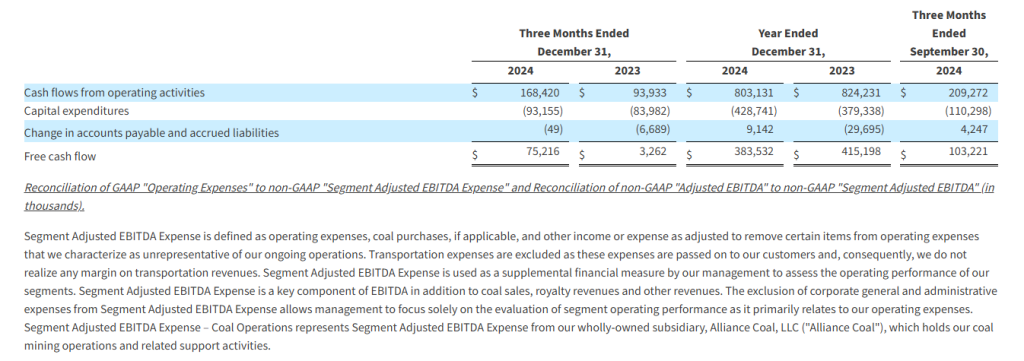

Full year 2024 total revenue of $2.4 billion, net income of $360.9 million, and Adjusted EBITDA of $714.2 million

Record full year 2024 oil & gas royalty volumes of 3.4 million BOE, up 9.6% year-over-year

Fourth quarter 2024 total revenue of $590.1 million, net income of $16.3 million, and Adjusted EBITDA of $124.0 million

Completed $9.6 million in oil & gas mineral interest acquisitions during fourth quarter

In January 2025, declared quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter and full year ended December 31, 2024 (the “2024 Quarter” and “2024 Full Year”). This release includes comparisons of results to the quarter and year ended December 31, 2023 (the “2023 Quarter” and “2023 Full Year”, respectively), as well as the quarter ended September 30, 2024 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of Adjusted EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.

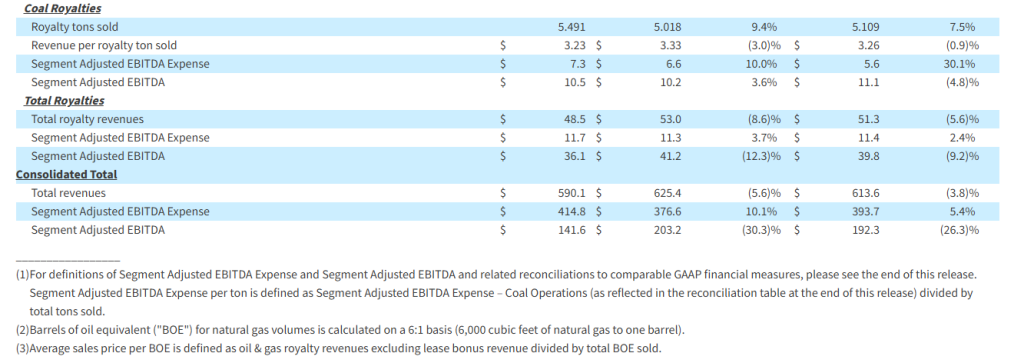

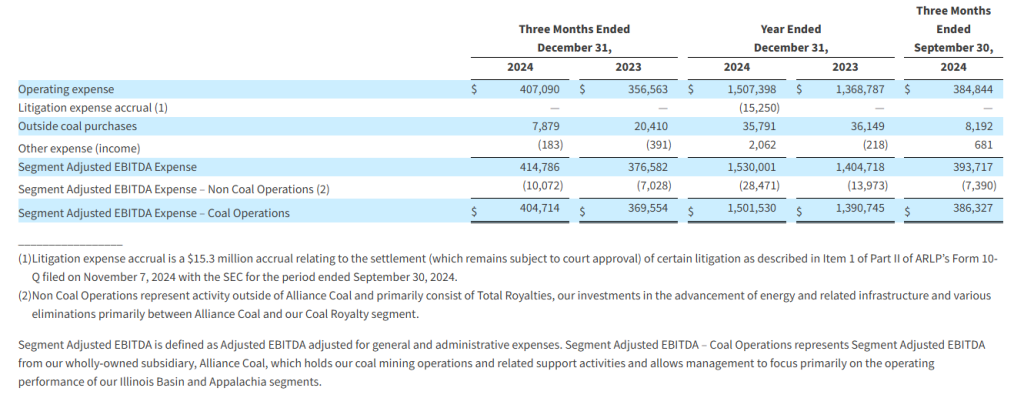

Total revenues in the 2024 Quarter decreased 5.6% to $590.1 million compared to $625.4 million for the 2023 Quarter primarily as a result of reduced coal sales volumes, which declined 2.3%, and lower transportation revenues. Net income for the 2024 Quarter was $16.3 million, or $0.12 per basic and diluted limited partner unit, compared to $115.4 million, or $0.88 per basic and diluted limited partner unit, for the 2023 Quarter as a result of lower revenues, higher per ton operating expenses, which include $13.1 million of non-cash accruals for certain long-term liabilities, and $31.1 million of non-cash impairment charges in the 2024 Quarter due to market uncertainty at our MC Mining operation, partially offset by a $14.0 million increase in the fair value of our digital assets. Adjusted EBITDA for the 2024 Quarter was $124.0 million compared to $185.4 million in the 2023 Quarter.

Total revenues in the 2024 Quarter decreased 3.8% compared to $613.6 million in the Sequential Quarter primarily as a result of reduced coal sales prices, which declined 5.7% due in part to lower export price realizations. Net income for the 2024 Quarter decreased by 81.1% compared to the Sequential Quarter as a result of lower revenues and higher non-cash accruals relating to certain long-term liabilities and impairment charges in the 2024 Quarter, partially offset by an increase in the fair value of our digital assets. Adjusted EBITDA for the 2024 Quarter decreased 27.2% compared to the Sequential Quarter, as a result of higher non-cash accruals for certain long-term liabilities in the Illinois Basin, higher expenses related to the continuation of challenging geological conditions at our Tunnel Ridge and MC Mining operations in Appalachia, and lower revenue per ton for spot coal sold and per BOE in the Royalties segment.

Total revenues decreased 4.6% to $2.45 billion for the 2024 Full Year compared to $2.57 billion for the 2023 Full Year primarily due to lower coal sales volume, partially offset by higher other revenues. Net income for the 2024 Full Year was $360.9 million, or $2.77 per basic and diluted limited partner unit, compared to $630.1 million, or $4.81 per basic and diluted limited partner unit, for the 2023 Full Year as a result of lower revenues, increased operating expenses and non-cash impairment charges, partially offset by a $22.4 million increase in the fair value of our digital assets. Adjusted EBITDA for the 2024 Full Year was $714.2 million compared to $933.1 million in the 2023 Full Year.

CEO Commentary

“Due to the continued strength of our coal contracts, our average coal sales price per ton for the 2024 Full Year of $63.38 came close to the record level achieved in the 2023 Full Year of $64.17. However, lower sales volumes, higher operating costs and several non-cash accruals caused 2024 Full Year financial results to fall short of last year’s record revenues and net income,” said Joseph W. Craft III, Chairman, President and CEO. “The cold winter weather at the start of this year has driven higher natural gas prices and increased coal consumption in the eastern United States, helping reduce inventories. We are seeing customer solicitations for both near-term and long-term supply contracts, and if the colder weather continues to be above normal, we are hopeful we can reach our goal to ship 30 million tons to the domestic market in 2025.”

Mr. Craft continued, “Having substantially completed major infrastructure projects at Tunnel Ridge, Hamilton, Warrior, and River View in 2024, we expect to see improved costs and productivity along with reduced capital spending this year. Additionally, the combination of cold winter weather and new LNG export terminal capacity should support strong domestic natural gas prices in 2025, benefiting both our Coal and Royalties segments.”

Mr. Craft concluded, “The increase in forecasted electricity demand, particularly from data centers and growth in AI, is highlighting the inadequacy of current resource plans without extended use of fossil fuel plants. These market realities, coupled with what we expect to be a more favorable regulatory environment, are laying the foundation for Alliance to continue serving as a cornerstone of the country’s reliable electricity infrastructure for years to come. We look forward to what we can achieve in 2025.”

Coal Operations

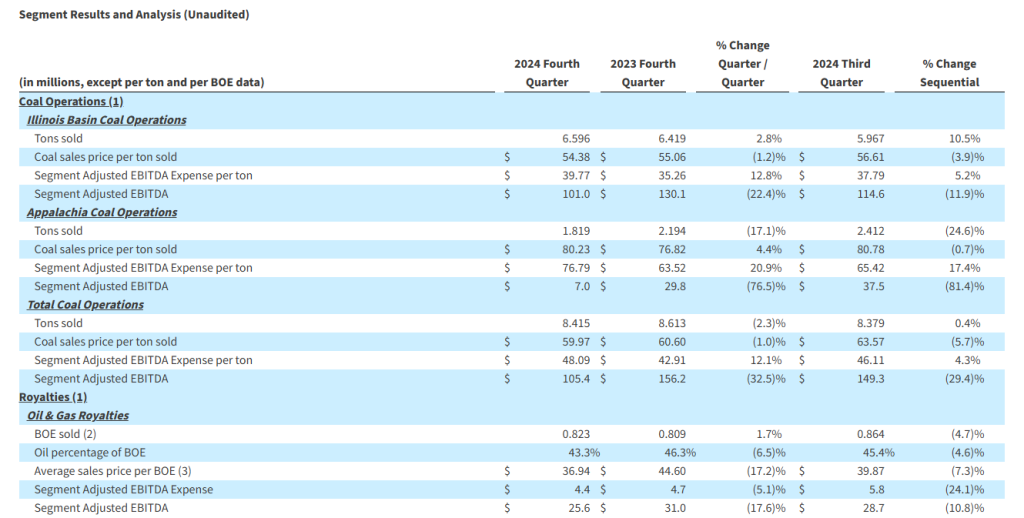

Total coal sales volumes for the 2024 Quarter decreased 2.3% compared to the 2023 Quarter while remaining relatively consistent compared to the Sequential Quarter. In Appalachia, tons sold decreased by 17.1% and 24.6% in the 2024 Quarter compared to the 2023 Quarter and Sequential Quarter, respectively, primarily as a result of lower production levels which reduced domestic sales volumes from our Tunnel Ridge operation. Partially offsetting these decreases, tons sold increased by 2.8% and 10.5% in the Illinois Basin compared to the 2023 Quarter and Sequential Quarter, respectively, due to improved sales performance from our River View, Hamilton, and Gibson South mines. Coal sales price per ton increased by 4.4% in Appalachia compared to the 2023 Quarter as a result of higher domestic price realizations at our Tunnel Ridge mine. In the Illinois Basin, coal sales prices decreased by 3.9% in the 2024 Quarter compared to the Sequential Quarter primarily due to reduced domestic price realizations from our Hamilton operation. ARLP ended the 2024 Quarter with total coal inventory of 0.6 million tons, representing decreases of 0.7 million tons and 1.4 million tons compared to the end of the 2023 Quarter and Sequential Quarter, respectively.

Segment Adjusted EBITDA Expense per ton for the 2024 Quarter increased by 12.8% and 5.2% in the Illinois Basin compared to the 2023 Quarter and Sequential Quarter, respectively, due primarily to reduced production, higher labor costs and lower recoveries at several mines in the region as well as an $11.0 million non-cash deferred purchase price adjustment recorded in the 2024 Quarter related to the 2015 acquisition of our Hamilton mine. In Appalachia, Segment Adjusted EBITDA Expense per ton for the 2024 Quarter increased by 20.9% and 17.4% compared to the 2023 Quarter and Sequential Quarter, respectively, due to lower recoveries across the region as well as challenging mining conditions which reduced production and led to higher materials and supplies and maintenance costs at our Tunnel Ridge operation.

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased to $25.6 million in the 2024 Quarter compared to $31.0 million and $28.7 million in the 2023 Quarter and Sequential Quarter, respectively, due primarily to lower average sales price per BOE, which decreased 17.2% and 7.3%, respectively, partially offset by decreased expenses. A reduction in oil & gas volumes compared to the Sequential Quarter also contributed to the sequential decrease.

Segment Adjusted EBITDA for the Coal Royalties segment increased 3.6% to $10.5 million for the 2024 Quarter compared to $10.2 million for the 2023 Quarter as a result of higher royalty tons sold, which increased 9.4%, partially offset by increased selling expenses and lower average royalty rates per ton received from the Partnership’s mining subsidiaries. Compared to the Sequential Quarter, Segment Adjusted EBITDA decreased 4.8% due to higher selling expenses, partially offset by increased sales volumes.

Balance Sheet and Liquidity

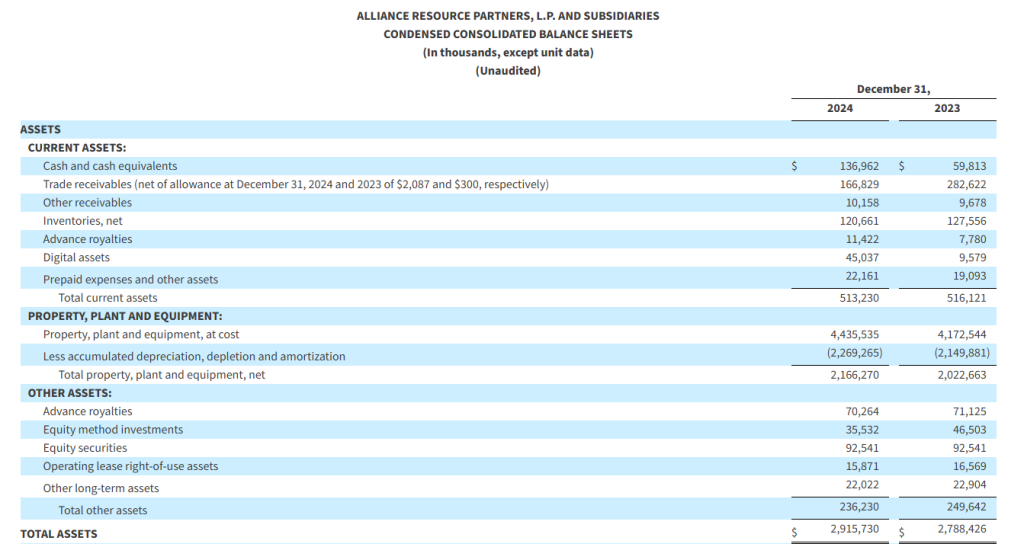

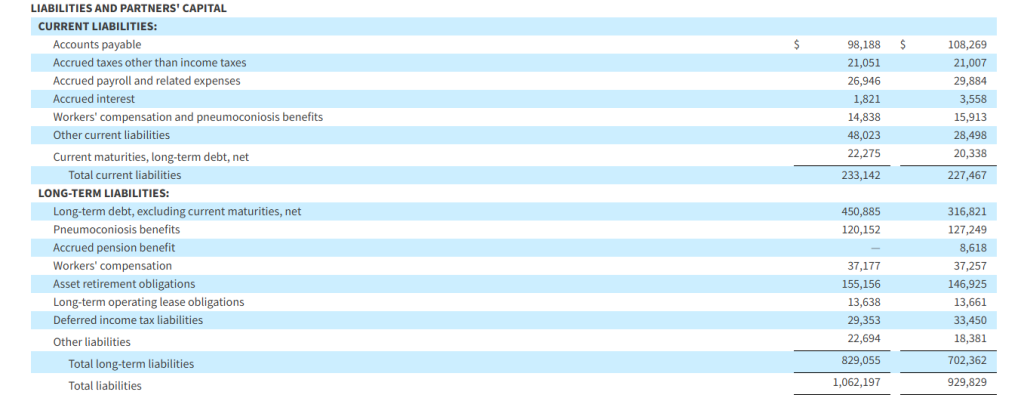

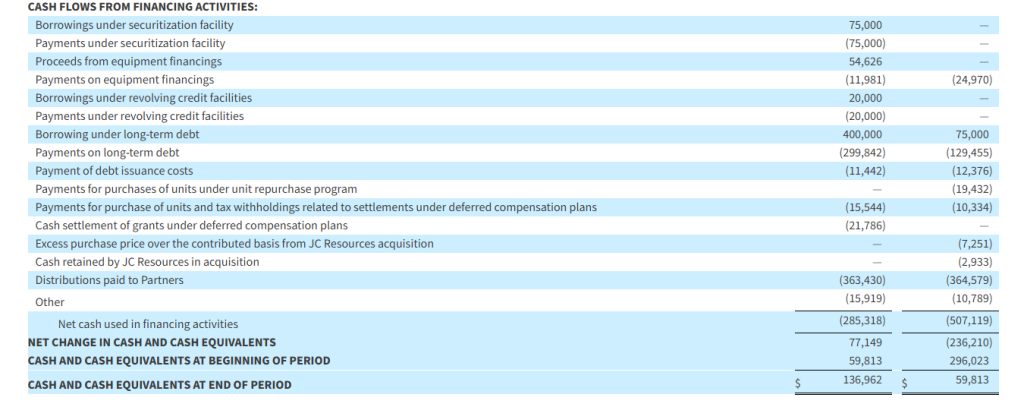

As of December 31, 2024, total debt and finance leases outstanding were $490.8 million, including $400 million in recently issued Senior Notes due 2029. The Partnership’s total and net leverage ratios were 0.69 times and 0.50 times debt to trailing twelve months Adjusted EBITDA, respectively, as of December 31, 2024. ARLP ended the 2024 Quarter with total liquidity of $593.9 million, which included $137.0 million of cash and cash equivalents and $456.9 million of borrowings available under its revolving credit and accounts receivable securitization facilities. ARLP also held 482 bitcoins valued at $45.0 million as of December 31, 2024.

Distributions

On January 28, 2025, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2024 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on February 14, 2025, to all unitholders of record as of the close of trading on February 7, 2025. The announced distribution is consistent with the cash distributions for the 2023 Quarter and Sequential Quarter.

Outlook

“For 2025, we expect improved coal production costs to counterbalance lower market prices, keeping Coal segment margins near 2024 Full Year levels,” commented Mr. Craft. “In the Oil & Gas Royalty business, we achieved record production volumes for the 2024 Full Year despite only making modest additions to our overall acreage position. We continue to favor the cash flow generation profile and ability to self-fund growth in the Oil & Gas Royalties segment, and therefore, will actively pursue growth in this segment in 2025.”

Mr. Craft concluded, “Looking forward, we anticipate a more supportive regulatory environment from the new administration that will help address the growing need for affordable, reliable baseload power without prematurely retiring critical generation sources. As the realities of physics meet the needs of the grid, we believe previously announced retirements will be delayed and our products will remain a cornerstone of energy security in some of the strongest industrial growth areas of the country for years to come.”

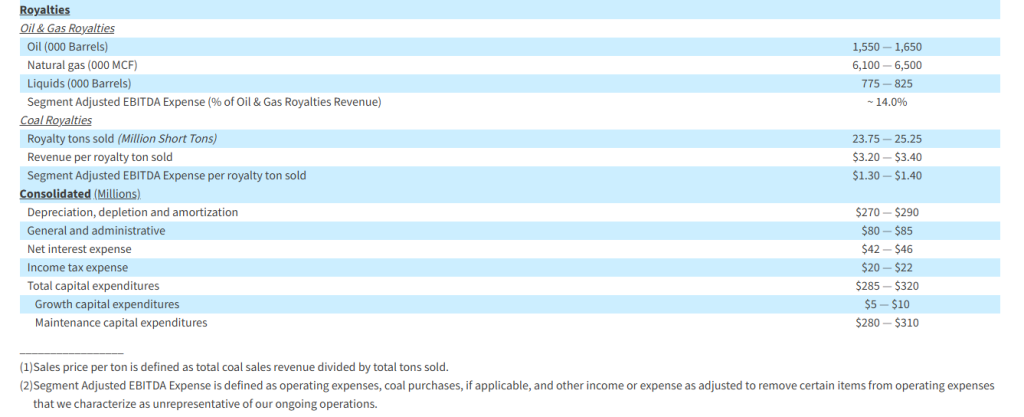

ARLP is providing the following guidance for the full year ending December 31, 2025 (the “2025 Full Year”):

Conference Call

A conference call regarding ARLP’s 2024 Quarter and Full Year financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13750955.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the second largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase or maintain unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, infrastructure projects at our existing properties, growth in domestic electricity demand, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; our ability to provide fuel for growth in domestic energy demand, should it materialize; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine and the Israel-Gaza conflict; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers and operators, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by the operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of and investments into the infrastructure of our operations and properties, including the timing of such investments coming online; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, and the results of central bank policy actions, including interest rates, bank failures, and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, such as the Environmental Protection Agency’s recently promulgated emissions regulations for coal-fired power plants, and state legislation seeking to impose liability on a wide range of energy companies under greenhouse gas “superfund” laws, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2023, filed on February 23, 2024, and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2024, June 30, 2024 and September 30, 2024, filed on May 9, 2024, August 7, 2024 and November 7, 2024, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of Non-GAAP Financial Measures (Unaudited)

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA,” “Adjusted EBITDA,” “Distribution Coverage Ratio” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization and Adjusted EBITDA is EBITDA adjusted for certain items that we characterize as unrepresentative of our ongoing operations. Distributable cash flow (“DCF”) is defined as Adjusted EBITDA excluding equity method investment earnings, interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures and adding distributions from equity method investments and litigation expense accrual. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, Adjusted EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, Adjusted EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, Adjusted EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e., public reporting versus computation under financing agreements).

Investor Relations Contact Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Agreement with SACL. Comstock Fuels executed definitive agreements with SACL Pte. Limited (SACL), a Singapore-based renewable fuel project developer with plans to develop renewable energy projects in Australia, New Zealand, Vietnam, Cambodia, and Malaysia. SACL has been granted a master non-exclusive license to Comstock Fuel’s intellectual property to develop, finance, build, and manage renewable fuel production facilities. The agreement provides exclusive rights to market projects subject to SACL’s satisfaction of certain milestones, including completion of engineering and financing for SACL’s first licensed facility in 2025 followed by commissioning and production in 2027.

Favorable terms. Comstock will contribute site-specific technology rights in exchange for a 20% equity stake in each refinery and provide engineering support in exchange for 3% of each facility’s capital and construction costs. This will increase to 6% for facilities with a capacity of 250,000 metric tons per year (MTPY) or more. Additionally, an upfront payment of $2.5 million will be required upon the execution of a site license agreement. Comstock Fuels will receive a royalty fee equal to 3% of the total sales from licensed products produced by each facility, which will rise to 6% for facilities with a capacity of 250,000 metric tons per year or greater.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Gold hits record $2,817/oz amid dollar weakness and trade policy concerns – Trump’s proposed tariffs spark renewed interest in safe-haven assets – Federal Reserve adopts cautious stance on rate cuts amid policy uncertainty

Gold prices reached an unprecedented peak of $2,817 per ounce, marking a 1.4% surge amid growing economic uncertainties and a weakening dollar. The precious metal’s rally reflects mounting investor concerns over President Trump’s proposed tariff measures and their potential impact on global trade relations.

The rally comes as traders digest Trump’s latest announcement of potential 25% tariffs on Mexico and Canada, along with hints of broader levies that could exceed previous Treasury estimates. This policy uncertainty, coupled with a softer dollar following the European Central Bank’s rate decision, has intensified the appeal of gold as a safe-haven asset.

The Federal Reserve’s recent “wait-and-see” stance, articulated by Chair Jerome Powell during the year’s first FOMC meeting, has added another layer of complexity to the market dynamics. While holding interest rates steady, the Fed expressed caution about rushing into rate cuts, particularly given the uncertain impact of the new administration’s economic policies.

Market strategists, including Phil Streible of Blue Line Futures, point to growing concerns about stagflation – a combination of rising inflation and declining growth – as a key driver behind gold’s attractiveness. The precious metal historically performs well in such economic conditions, making it an increasingly appealing hedge for investors.

The rally has sparked a notable shift in precious metals markets, with U.S. prices for both gold and silver commanding premiums over international benchmarks. Dealers and traders are accelerating efforts to secure inventory ahead of potential tariff implementation, further driving up domestic prices.

Beyond immediate trade concerns, the precious metal’s appeal is bolstered by persistent worries over growing U.S. debt levels. Many analysts anticipate continued strength in gold prices throughout 2025, supported by central banks’ efforts to diversify reserves and reduce dollar dependency.

The latest surge represents a significant milestone in gold’s historical trajectory, surpassing the previous record set in October. This breakthrough is particularly notable as it comes during a period of relative economic strength, suggesting that investors are increasingly viewing gold as both a hedge against uncertainty and a strategic asset class in diversified portfolios.

The current gold market dynamics echo historical patterns of price appreciation during periods of significant policy shifts and economic uncertainty. Historical data shows that gold has typically performed strongly during periods of trade tensions and currency fluctuations, with the metal gaining an average of 15% during similar periods of policy uncertainty in the past two decades

Market watchers are particularly focused on the Saturday deadline for Mexican and Canadian tariffs, which could trigger further volatility in precious metals markets and potentially drive gold to new records as investors seek safety amid economic policy shifts.

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) today announced that the Board of Directors of ARLP’s general partner approved a cash distribution to its unitholders for the quarter ended December 31, 2024 (the “2024 Quarter”).

ARLP unitholders of record as of the close of trading on February 7, 2025 will receive a cash distribution for the 2024 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on February 14, 2025. The announced distribution is consistent with the cash distributions of $0.70 per unit for the quarters ended December 31, 2023 and September 30, 2024.

As previously announced, ARLP will report financial results for the 2024 Quarter before the market opens on Monday, February 3, 2025 and Alliance management will discuss these results during a conference call beginning at 10:00 a.m. Eastern that same day.

To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13750955.

Concurrent with this announcement we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the second largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

Investor Relations Contact

Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

Key Points: – $1.275B deal creates $3.8B energy giant with doubled production – Shifts from gas-heavy to balanced oil/gas portfolio – 3.3x EBITDA price with $345M cash flow; EIG takes 20% stake

Diversified Energy (NYSE:DEC) made waves in the energy sector Monday with its $1.275 billion acquisition of Maverick Natural Resources, a move that signals a major shift in domestic energy production strategy and could spark further consolidation in the industry.

The deal, which combines two major players in the U.S. energy market, is set to nearly double Diversified’s revenue and significantly boost its free cash flow, according to company statements. Market observers note this could mark the beginning of a new wave of consolidation in the domestic energy sector, as companies seek to build scale and efficiency in an increasingly competitive market.

“This acquisition expands our unique and highly focused energy production company with a complementary portfolio of attractive, high-quality assets,” said Rusty Hutson, Jr., CEO of Diversified. The combined company will boast an enterprise value of approximately $3.8 billion and operate across five distinct regions, with production reaching approximately 1,200 MMcfe/d.

What’s catching investors’ attention is the deal’s attractive valuation at roughly 3.3 times LTM EBITDA, suggesting Diversified may have found value in a market where quality assets often command premium multiples. The transaction structure, including the assumption of $700 million in Maverick debt and the issuance of 21.2 million new shares, appears designed to maintain financial flexibility while expanding the company’s operational footprint.

Perhaps most significantly, the merger dramatically shifts Diversified’s production mix. While the company has historically been heavily weighted toward natural gas with about 85% of production, Maverick brings a more balanced portfolio with 55% liquids production. This diversification could prove crucial in navigating volatile energy markets.

The deal also marks a strategic entry into the coveted Permian Basin, while strengthening Diversified’s position in the Western Anadarko Basin. Industry analysts suggest this multi-basin exposure could provide valuable operational flexibility and help mitigate regional production risks.

EIG, a major energy-focused investor, will emerge as a significant stakeholder, owning approximately 20% of the outstanding shares post-merger. This backing from a sophisticated institutional investor may provide additional validation for Diversified’s growth strategy.

Looking ahead, the combined company is positioned to benefit from substantial operational synergies and improved market presence. With a projected free cash flow of $345 million, the merged entity should have ample resources to fund both growth initiatives and shareholder returns.

The transaction, expected to close in the first half of 2025, still requires shareholder approval and regulatory clearance. However, with unanimous board approval and strong strategic rationale, the deal appears well-positioned to move forward.

For investors watching the energy sector, this merger could signal a broader trend toward consolidation as companies seek to build scale and improve operational efficiency in an evolving market landscape. The success of this integration could set a template for future deals in the domestic energy sector.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase I Drilling at Douay. Maple Gold Mines commenced a Phase I diamond drilling program at the Douay Gold project that is expected to last three to four months. The company’s drilling program will entail a minimum of 10,000 meters of diamond drilling, with ~70% dedicated to de-risking and expanding the Douay mineral resource and 30% for testing new regional geological and geophysical targets. At the Douay gold project, the goal is to expand and upgrade the current three-million-ounce gold resource to five million ounces. The first phase will target shallow portions of the Douay system at a vertical depth of less than 500 meters, while the second phase will test vertical depths greater than 500 meters.

Drilling at Joutel is planned in 2H 2025. An additional 3,000 meters of diamond drilling is planned at Joutel in the second half of 2025 to extend the known high-grade gold mineralization along the past-producing Eagle-Telbel mine trend.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – January 22, 2025) – Maple Gold Mines Ltd. (TSXV: MGM) (OTCQB: MGMLF) (FSE: M3G) (“Maple Gold” or the “Company“) is pleased to provide an exploration update and 2025 outlook for its 100%-owned Douay Gold Project (“Douay“) and Joutel Gold Project (“Joutel“) (together, “Douay/Joutel” or the “Property“) located along the Casa Berardi-Douay Gold Trend in Québec, Canada (see Figures 1 and 2).

A 10,000-metre (“m“) Phase I diamond drilling program (the “Program“) has now commenced at Douay with an expected duration of three to four months. The location of the Douay mineralized zones and primary targets are shown in Figures 3 and 4. Key objectives of the Program include:

Targeting poorly drilled areas within Inferred Resources for conversion to Indicated Resources within the pit-constrained and underground resource domains;

Step-out drilling along strike, down-dip, and down-plunge to expand Inferred Resources

Step-out drilling from zones of high-grade gold mineralization within the underground Inferred Resources to demonstrate lateral and vertical continuity;

Targeting areas between modeled mineralized zones with geological continuity; and

Testing new targets developed during the compilation exercise of geological, geochemical and geophysical data.

Concurrent development initiatives are anticipated throughout 2025 to advance and de-risk the Douay deposit, including a review of the current Douay mineral resource estimate (“MRE“) and an evaluation of potential scenarios to optimize higher grade mineral resources that could be accessible via underground mining methods. An additional 3,000 m of diamond drilling is planned at Joutel in H2 2025 to extend the known high-grade gold mineralization along the past-producing Eagle-Telbel mine trend.

“We are excited to be drilling again at Douay with refocused attention on the higher-grade core of the deposit and its possible extensions both within and beyond our current drill pattern up to 500 m vertical depth,” stated Kiran Patankar, President and CEO. “Maple Gold’s technical team has accomplished a monumental task in compiling over 50 years of exploration data to generate new geological/structural/geochemical 3D models that have vastly improved our drill targeting. This work highlights the excellent exploration potential of Douay/Joutel, the importance of its location along the deep-seated Casa Berardi break, and the opportunity for the Property to host multiple gold deposits within a variety of geological settings. Our focus in 2025 will be executing a comprehensive exploration and development program that is aimed at delivering shareholder value through the drill bit and via project de-risking, while maintaining strict cost discipline across the Company.”

A total exploration budget of approximately $6.3 million has been established for 2025, including permitting, drilling, assaying, personnel, camp and site support costs. The 2025 work program will be fully funded from Maple Gold’s existing treasury.

Program Details

The Company is currently planning a minimum of 10,000 m of diamond drilling at Douay in 2025. Phase I drilling has now commenced with an expected duration of approximately three to four months (see Figures 3 and 4). The breakdown of the drilling metreage will be approximately: 70% dedicated to de-risking and expanding the Douay MRE through strategic infill and step-out holes (along strike and at depth); and 30% for the testing of new regional geological and geophysical targets along strike from the Douay MRE and north into the Taibi Group sediments along favourable structural breaks and lithologic contacts. The Company plans to complete infill drilling throughout the Douay MRE to convert Inferred Resources to Indicated Resources, potentially add new Inferred Resources within poorly drilled 100-200 m gaps between modeled mineral domains and target the down-plunge extensions of higher-grade zones outside the Douay MRE.

The Company plans to utilize all available data from its year-long data compilation exercise to initially target the shallow portions of the Douay mineralizing system (<500 m vertical depth) to fully understand the geometry of the known zones and outline key plunge directions (Phase I on Figure 4) before systematically stepping down-plunge and at depth (>500 m vertical depth) during a proposed second drilling phase (Phase II on Figure 4). This will allow the Company to control exploration risk and maximize exploration success.

The initial focus of Phase I drilling will be on the central portions of the Douay MRE targeting higher grade areas within the Porphyry Zone (comprised of West/Central/East portions), which is hosted within the Douay Intrusive Complex and includes some of the highest-grade assays returned on the Property (up to 2,888 grams/tonne (“g/t”) of gold (“Au”) over 0.5 m in historical drill hole DO-05-04). Other targets include: the 531 Zone which is hosted within mafic volcanic and folded interflow sedimentary rocks and includes one of highest-grade gold intersections reported by the Company in drill hole DO-21-310 which returned 8.8 g/t Au over 28.5 m, including 12.7 g/t Au over 10.0 m and 31.1 g/t Au over 0.5 m (see Company news release dated September 9, 2021); and the Main Zone which lies along the northern edge of the Douay Deformation Zone (“DDZ“) with gold mineralization hosted along the sheared graphitic contact between the Taibi Group volcaniclastic and sedimentary rocks to the north and Cartwright Hills Group mafic volcanic rocks to the south. Taibi Group sediments represent a promising new target area for the Company with the potential for sediment-hosted gold deposits along a major lithotectonic boundary similar to the Casa Berardi and Canadian Malartic deposits.

Douay/Joutel Exploration Update

Since the completion of its last drilling campaign in Spring 2023, the Company has focused on streamlining onsite operations, standardizing procedures, enhancing efficiencies, centralizing data management, optimizing workflow, and reducing overhead site costs. This effort has led to increased productivity from a revamped technical team that has reviewed historical drill core, compiled and digitized data, distinguished new geological and structural controls on gold mineralization, and developed vectors for targeting gold mineralization in the next phases of drilling.

Key tasks completed by the Maple Gold technical team include: re-logging of historical diamond drill core (>20,000 m); re-interpretation and preparation of drill hole cross-sections and level plans for all mineralized zones; updating and creating new robust 3D geological and structural models in Leapfrog software; updating of the Property-wide drill hole and geochemical databases with previously unincorporated historical data; layering of geological, structural, geochemical and geophysical data sets to generate new targets; and use of expert geochemical consultants to process multi-element assay data to identify potential pathfinder elements and ‘hot’ spots.

Key findings from the year-long data review and compilation exercise include:

The Casa Berardi Deformation Zone (the “CBDZ“) widens around Douay/Joutel resulting in complex zones along the DDZ of brittle and ductile deformation, subsidiary splays, NNE cross-faulting, and potential dextral rotation around the Douay Intrusive Complex resulting in Delta-type pressure shadows and possible structural traps for gold (see Figure 2).

A variety of host domains and rock types are favourable for gold mineralization including the Douay Alkaline Intrusion, Taibi Group sediments (including iron formations), Cartwright Hills Group basalts (including Fe-Rich tholeiitic komatiites), Temiskaming-style conglomerates, and structural breaks associated with major lithotectonic (volcanic-sedimentary) contacts.

Multiple styles and generations of mineralization are present at Douay/Joutel including Intrusion-Related Gold Systems (“IRGS“), multi-phase breccias, late orogenic gold, and synvolcanic-exhalative gold (Eagle-Telbel).

Gold mineralization is commonly associated with broad zones of albitization, Fe-carbonatization, silicification, hematization, fenitization, biotitization, and pyritization and alteration can be used as a key vector for gold mineralization.

The twelve (12) main mineralized zones all display a strong plunge geometry to the higher-grade gold mineralization, which varies from shallow to steep, and from southeast to southwest, possibly related to an earlier folding event. There also appears be a periodicity to the mineralized zones within the DDZ spaced 500 m to 1,000 m apart (see Figure 3).

There has been very limited drilling below 500 m vertical depth in comparison to other gold deposits in the Abitibi (East Gouldie/Odyssey, LaRonde) (see Figure 4).

Planned Douay Development Initiatives

The Company plans to review the current Douay MRE for the Project which currently contains both pit-constrained and underground Inferred and Indicated mineral resources to optimize higher grade resources that could be accessible via an underground mining scenario. Initial focus would include the Douay West zone which currently hosts Indicated mineral resources totaling 4.2 million tonnes (“Mt“) grading 2.13 g/t Au (containing 286,000 ounces of Au) and Inferred mineral resources totaling 3.7 Mt grading 1.39 g/t Au (containing 169,000 ounces of Au)1. Douay West also includes existing surface infrastructure constructed in 1995 including a headframe and mine hoist.

Figure 1: Location of the Douay/Joutel (Eagle-Telbel) Property in the Abitibi Sub-Province, Québec

Figure 4: Composite longitudinal section showing location of Douay Mineralized Zones and 2025 Target Areas (in red) (note: comparison to other deposits for reference purposes only)

2024 Exploration Work Completed at Joutel and Morris VMS Project

In Q2 2024, the Company completed a 525 line-km airborne drone-magnetic geophysical survey over a detailed grid on the western portion of the Joutel gold project to assist in the development of new drill targets along the western strike extent of the Eagle-Telbel stratigraphy.

In Q3 2024, the Company completed a lithogeochemical sampling program over its Morris volcanogenic massive sulphide (“VMS“) project, located 29 km east of Matagami, Québec. The program focused on the felsic volcanic rocks of the key Watson Lake formation which is present on the Morris project and is known to host the major VMS deposits within the Matagami mining camp. The Summer 2024 sampling program highlighted several areas of highly altered rhyolite, and the Company is developing plans for follow-up work in 2025.

Qualified Person

Ian Cunningham-Dunlop, P.Eng., Vice President, Technical Services of Maple Gold and a qualified person (“QP“) as defined by Canadian National Instrument 43-101, has reviewed and approved the scientific and technical information related to exploration and Mineral Resource matters contained in this news release.

About the Douay/Joutel Gold Project

The Douay/Joutel Gold Project is located adjacent to Highway 109 in the heart of the Abitibi greenstone belt, Canada’s premier gold mining jurisdiction (see Figure 1). This large, 100%-owned land package includes the multi-million ounce2 Douay Gold Project and the past-producing, high-grade Joutel Gold Mine Complex3. The Property contains ~400 km2 of highly prospective geology (see Figure 2) within the influence of the major gold-bearing CDBZ. Gold mines in the immediate region include the Casa Berardi Gold Mine operated by Hecla Mining Company and the Detour Lake Gold Mine operated by Agnico Eagle Mines Ltd. (see Figure 1).

About Maple Gold

Maple Gold Mines Ltd. is a Canadian advanced exploration company focused on advancing its 100%-owned, district-scale Douay and Joutel gold projects located in Québec’s prolific Abitibi Greenstone Gold Belt. The Douay/Joutel projects benefit from exceptional infrastructure access and boast ~400 km2 of highly prospective ground including an established gold mineral resource at Douay with significant expansion potential as well as the past-producing Telbel and Eagle West mines at Joutel. In addition, the Company holds an exclusive option to acquire 100% of the Eagle Mine Property, a key part of the historical Joutel Mining Complex.

Maple Gold’s property package also hosts a significant number of regional exploration targets along a 55-km strike length of the Casa Berardi Deformation Zone that have yet to be tested through drilling, making the property ripe for new gold and polymetallic discoveries. The Company is currently focused on carrying out exploration and drill programs to grow mineral resources and make new discoveries to establish an exciting new gold district in the heart of the Abitibi. For more information, please visit www.maplegoldmines.com.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS PRESS RELEASE.

Forward-Looking Statements and Cautionary Notes:

This news release contains “forward-looking information” and “forward-looking statements” (collectively referred to as “forward-looking statements”) within the meaning of applicable Canadian securities legislation in Canada. Forward-looking statements are statements that are not historical facts; they are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “aims,” “potential,” “goal,” “objective,”, “strategy”, “prospective,” and similar expressions, or that events or conditions “will,” “would,” “may,” “can,” “could” or “should” occur, or are those statements, which, by their nature, refer to future events. Forward-looking statements in this news release include, but are not limited to, statements about the resource expansion and discovery potential across the Company’s gold projects, and its intention to pursue such potential, and the Company’s exploration work and results from current and future work programs. Although the Company believes that forward-looking statements in this news release are reasonable, it can give no assurance that such expectations will prove to be correct, as forward-looking statements are based on assumptions, uncertainties and management’s best estimate of future events on the date the statements are made and involve a number of risks and uncertainties. Consequently, actual events or results could differ materially from the Company’s expectations and projections, and readers are cautioned not to place undue reliance on forward-looking statements. For a more detailed discussion of additional risks and other factors that could cause actual results to differ materially from those expressed or implied by forward-looking statements in this news release, please refer to the Company’s filings with Canadian securities regulators available on the System for Electronic Document Analysis and Retrieval Plus (SEDAR+) at www.sedarplus.ca or the Company’s website at www.maplegoldmines.com. Except to the extent required by applicable securities laws and/or the policies of the TSX Venture Exchange, the Company undertakes no obligation to, and expressly disclaims any intention to, update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

________________________ 1 For additional details, see the technical report for the Douay gold project entitled “Technical Report on the Douay and Joutel Projects Northwestern Québec, Canada Report for NI 43-101” prepared by SLR Consulting (Canada) Ltd. with an effective date of March 17, 2022, and dated April 29, 2022. 2 The Douay Project contains Indicated Mineral Resources estimated at 10 million tonnes at a grade of 1.59 g/t Au (containing 511,000 ounces of gold), and Inferred Mineral Resources estimated at 76.7 million tonnes at a grade of 1.02 g/t Au (containing 2,527,000 ounces of gold). See the technical report for the Douay Gold Project entitled “Technical Report on the Douay and Joutel Projects Northwestern Québec, Canada Report for NI 43-101″ prepared by SLR Consulting (Canada) Ltd. with an effective date of March 17, 2022, and dated April 29, 2022. 3 The Eagle, Eagle West and Telbel Gold Mines at Joutel were in production from 1974 to 1993 and produced 1.1 million ounces of gold at an average grade of 6.5 g/t Au (Agnico Eagle Mines Ltd. website)

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Agreement with Hexas Biomass. Comstock Fuels executed an agreement with Hexas Biomass Inc. to acquire an exclusive worldwide license to Hexas’ intellectual properties in liquid fuels applications, subject to certain pre-existing agreements and relationships. Moreover, Hexas will provide development services in connection with Comstock Fuels’ site development and innovation activities. Comstock Fuels will invest $500,000 in Hexas to be paid in four tranches on January 15, January 31, February 28, and March 31, 2025.

High yield energy crops. Hexas has developed a portfolio of proprietary intellectual properties supporting the propagation, production, harvesting, and processing of purpose-grown energy crops with yields exceeding 25 to 30 dry metric tons per acre per year, or about 4 to 7 times the yields of traditional forestry species.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Paving the way for an off-take agreement. Century Lithium recently executed a non-binding memorandum of understanding (MOU) to formalize a multi-year off-take agreement with Orica Specialty Chemicals to purchase sodium hydroxide from Century Lithium’s wholly owned Angel Island project. Orica is a leading mining and infrastructure solutions provider, the largest producer of sodium cyanide, and a supplier of specialty mining chemicals to Nevada’s mining industry.

Initial term of five years. The contemplated off-take agreement will have an initial term of five years and a right of first offer for an additional five years. It would account for a large portion of the surplus sodium hydroxide produced during the early years of the Angel Island project’s operation. A definitive agreement will contain pricing terms.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

January 21, 2025 – Vancouver, Canada – Century Lithium Corp. (TSXV:LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (Century Lithium) is pleased to announce it signed a non-binding memorandum of understanding (MOU) with Orica Specialty Mining Chemicals (Orica) on January 16, 2025. The non-binding MOU outlines the intent of Century Lithium and Orica to formalize a multiyear offtake agreement for Orica to purchase sodium hydroxide (NaOH) from Century Lithium’s wholly owned Angel Island project near Silver Peak, Nevada. Orica is one of the world’s leading mining and infrastructure solutions providers, and a major US manufacturer and supplier of specialty mining chemicals to Nevada’s mining industry.

“The non-binding MOU with Orica marks a key milestone for Angel Island,” said Century Lithium President and CEO, Bill Willoughby. “The MOU outlines the first expected agreement of its kind for the project and involves a large portion of the surplus sodium hydroxide anticipated during the early years of operation. We are excited to work with Orica and have their support at this stage of development at Angel Island.”

Orica President Specialty Mining Chemicals Andrew Stewart said: “This collaboration signifies our commitment to strengthening and unlocking Nevada’s manufacturing and mining sectors. By securing a reliable source of sodium hydroxide from Angel Island, we strengthen the local supply chain and reinforce our dedication to innovative US manufacturing solutions for our customers in North America.”

Century Lithium patent-pending process for extracting lithium from the claystone at Angel Island combines chloride leaching with direct lithium extraction and uses salt, in the form of solid sodium chloride or saline brine, to make the reagents for leaching and pH control. In addition to lithium, the process produces surplus sodium hydroxide, the sales of which are anticipated to underpin low operating costs for Angel Island’s primary product, lithium carbonate.

Highlights of MOU

Century Lithium to intends to provide Orica membrane-grade sodium hydroxide (NaOH)

Initial 5-year term, right of first offer for an additional 5 years

Pricing to be determined by definitive agreement

Orica – Century Lithium relationship will strengthen the U.S. supply chain, reducing reliance on imports of NaOH to the western U.S. and supporting Nevada’s mining industry

ABOUT ORICA

Orica (ASX: ORI) is one of the world’s leading mining and infrastructure solutions providers. From the production and supply of explosives, blasting systems, specialty mining chemicals and geotechnical monitoring to our cutting-edge digital solutions and comprehensive range of services, we sustainably mobilize the earth’s resources.

Operating for more than 150 years, today our 14,000+ global workforce supports customers across surface and underground mines, quarry, construction, and oil and gas operations.

With a sodium cyanide manufacturing plants located in Winnemucca, Nevada and Alvin Texas, Orica is now the world’s largest producer of sodium cyanide and supplier to the Nevada mining industry, a leader in U.S. gold production. Find out more about Orica: www.orica.com

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced stage lithium company, focused on developing its wholly-owned Angel Island project in Esmeralda County, Nevada, which hosts one of the largest sedimentary lithium deposits in the United States. The Company has utilized its patent-pending process for chloride leaching combined with direct lithium extraction to make high purity lithium carbonate product samples from Angel Island lithium-bearing claystone on-site at its Pilot Plant in Amargosa Valley, Nevada.

Angel Island is one of the few advanced lithium projects in development in the United States to provide an end-to-end process to produce battery quality lithium carbonate for the growing electric vehicle and battery storage market. Angel Island is currently in the permitting stage for a three-phase feasibility-level production plan expected to yield an average of 34,000 tonnes per year of lithium carbonate over a 40-year mine-life.

Century Lithium trades on both the TSX Venture Exchange under the symbol “LCE” and the OTCQX under the symbol “CYDVF”; and on the Frankfurt Stock Exchange under the symbol “C1Z”. To learn more, please visit: centurylithium.com

ON BEHALF OF CENTURY LITHIUM CORP. WILLIAM WILLOUGHBY, PhD., PE President & Chief Executive Officer

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.

These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.com. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Special meeting of stockholders. Comstock will host a virtual special meeting of stockholders on February 14 at 9:00 a.m. PT. Stockholders of record, as of January 2, are asked to vote to authorize a reverse stock split of the company’s issued and outstanding common stock at a ratio ranging from one-for-five to one-for-twenty, with the timing and ratio to be determined by the Board. There will be no reduction or change to Comstock’s 245,000,000 authorized share count. The primary goal of the reverse split is to increase the number of shares available for issuance should the company need to raise additional capital.