Shares of Virgin Galactic Holdings Inc. (SPCE) surged over 30% on Thursday after the company unveiled plans to reduce costs and temporarily pause spaceflight operations. The stock jumped from $1.56 to over $2 as investors reacted positively to Virgin Galactic’s aim to conserve cash while developing its next generation of spaceships.

Virgin Galactic announced it will wind down flights of its existing VSS Unity spacecraft in mid-2024. The company will then focus resources on finalizing assembly of its new Delta class spaceship line.

The Delta class ships represent the future of Virgin Galactic’s space tourism business. Pausing VSS Unity flights will allow engineers to concentrate on getting the Delta fleet ready to fly tourists on suborbital trips to the edge of space.

Cutting Costs to Fund New Spaceships

To finance the spaceship transition, Virgin Galactic is cutting costs substantially. This week the company laid off around 18% of its workforce, about 185 employees. The reductions will generate $25 million in annual cost savings.

The job cuts come as Virgin looks to trim expenses and streamline operations during the fleet transition. Management aims to direct as much capital as possible toward completing work on the Delta class vessels.

Virgin Galactic also announced it will reduce the flight rate of its current VSS Unity ship. Since June, VSS Unity has been flying commercial tourist missions roughly once per month. Going forward it will shift to quarterly flights before fully standing down in 2024.

Fewer VSS Unity flights will conserve rocket fuel and other operating costs. These savings can be redirected to accelerate progress on the new generation Delta ships.

VSS Unity Flights Winding Down

VSS Unity began commercial service in July 2021 and has completed five revenue-generating passenger flights so far. It will continue making quarterly trips to the fringes of space until its retirement in mid-2024.

So far this year VSS Unity flew its first fully private astronaut mission in June. This was followed by its first Italian researcher flight in September. Both missions generated crucial revenue for Virgin Galactic.

But VSS Unity is only capable of flying four passengers to space on each trip. The Delta class spacecraft will increase that capacity to six passengers. This 50% bump is critical to ramping up Virgin’s space tourism business.

The company is aiming to begin Delta test flights from its New Mexico spaceport in 2025. With a smoother flight profile and more spacious cabin, the Delta promises a superior overall experience compared to VSS Unity.

Stock Surges on Cash Conservation Plan

Virgin Galactic’s shares have suffered in 2022, falling over 50% year-to-date before Thursday’s 30% pop. The market responded favorably to management’s decisive actions to reinforce its financial position.

The workforce reductions and spaceflight pause will slow Virgin’s cash burn rate while buying time to ready the Delta fleet. With its existing cash balance, the company has ample runway to execute the transition.

Pausing VSS Unity flights will allow Virgin to upgrade ground infrastructure at its spaceport to support Delta operations. By winding down one program and preparing for the next, Virgin Galactic hopes to hit the ground running once the Delta ships are flight ready.

If executed successfully, the cost cutting and spaceflight hiatus could put Virgin in position to ramp up flights profitably after the Delta class ships come online. With improved ships unlocking expanded market opportunities, Virgin Galactic aims to soar both literally and financially over the long term.

Healthcare investor favorite Apollo Medical Holdings (NASDAQ: AMEH) is expanding its presence in value-based care arrangements through the acquisition of Community Family Care (CFC), a large independent physician association based in Los Angeles. The all-cash deal worth up to $202 million reflects ApolloMed’s strategy of targeting risk-bearing providers as a high-growth segment of the health biotech sector.

CFC manages care for over 200,000 members via its network of more than 350 primary care physicians and 500 specialists. The group has a strong presence in Medicaid, with a Restricted Knox Keene (RKK) license enabling it to take on full risk for this population in California. CFC also serves Medicare and commercial members under value-based contracts that incentivize providers to control costs and improve health outcomes.

For ApolloMed, acquiring CFC significantly boosts its portfolio of managed lives, particularly under global capitation arrangements that cover total cost of care. Additionally, CFC’s long track record of profitability in Medicaid provides ApolloMed with demonstrated capabilities to take on risk successfully in a population that is often challenging for providers.

The deal exemplifies a unique competitive edge for ApolloMed – its end-to-end platform spanning technology, management services, and risk contracting. CFC has utilized ApolloMed’s care enablement tools since 2020, allowing it to perform well under value-based care. Now, full acquisition enables tight integration and aligned incentives as CFC transitions to an ApolloMed care partner responsible for total cost and outcomes.

For 2023, CFC is expected to generate $190 million in revenue with $25 million in adjusted EBITDA, an impressive 13% margin for a risk-bearing provider group. ApolloMed has agreed to an acquisition price of up to $202 million, including $152 million in cash, $20 million in ApolloMed stock, and $30 million in potential milestone payments. The deal is anticipated to close in Q1 2024 after clearing regulatory reviews.

Rapid Growth in Value-Based Care

The acquisition comes at a time of rapid expansion in value-based care, where providers take on financial accountability for cost and quality of healthcare for a population of patients. Government and commercial payers are pushing providers into these arrangements to incentivize focus on preventative care and eliminating wasteful spending.

Analysts size the global market for value-based care at $3.1 billion by 2030, reflecting a blistering compound annual growth rate of 21.7% from 2022. In the United States, value-based care penetration is expected to reach 65% of healthcare payments by 2025.

ApolloMed is positioned at the forefront of this transformation with its integrated platform and focus on enabling providers, such as CFC, to take on risk successfully. The CFC deal adds a sizable value-based care presence to ApolloMed’s portfolio, demonstrating the appetite to aggressively scale its model with like-minded partners.

Targeting High-Growth Segments

The CFC acquisition also highlights ApolloMed’s focus on areas of healthcare with strong secular tailwinds: government programs and risk-based arrangements.

Medicaid represents a massive $650 billion total addressable market, and ApolloMed is specifically targeting expansion in California, which has among the most progressive Medicaid programs in supporting coordinated care models. CFC’s strong capabilities in the Medicaid population will be a key strategic asset.

Likewise, ApolloMed’s thesis of investing behind risk-bearing providers is underscored by CFC’s demonstrated ability to generate double-digit margins while managing patients under capitated contracts. As fee-for-service reimbursement models decline, providers capable of taking on risk will be increasingly valuable.

Wall Street’s View

ApolloMed has been a darling of growth investors, with shares up 270% over the past five years. Revenue and EBITDA have compounded annually at 50% and 90%, respectively, as the company scales its platform.

The market continues to reward this rapid expansion, with ApolloMed trading at a premium valuation of 50x P/E. Bulls believe the company’s strategy and competitive moats position it for continued acceleration as value-based care proliferates.

Meanwhile, bears argue that ApolloMed’s nosebleed valuation leaves little room for error. There are also concerns around rising fragmentation in California’s Medicaid market challenging operators.

However, with impressive unit economics and strong execution thus far, ApolloMed has many convinced it can maintain momentum. The CFC deal offers further validation of the company’s model and market opportunity. Investors will be watching closely for successful integration and financial accretion.

If ApolloMed can effectively leverage CFC to penetrate Medicaid and value-based arrangements more deeply, the deal may be looked back upon as an inflection point in the company’s growth story. At minimum, it provides another data point for ApolloMed’s ability to execute on acquisitions rapidly expanding its national footprint – a core piece of the bull thesis.

BigBear.ai, a provider of AI-powered business intelligence solutions, has announced the acquisition of Pangiam, a leader in facial recognition and biometrics, for approximately $70 million in an all-stock deal. The acquisition represents a major strategic move by BigBear.ai to expand its capabilities and leadership in vision artificial intelligence (AI).

Vision AI refers to AI systems that can perceive, understand and interact with the visual world. It includes capabilities like image and video analysis, facial recognition, and other computer vision applications. Vision AI is considered one of the most promising and rapidly growing AI segments.

With the acquisition, BigBear.ai makes a big bet on vision AI and aims to create one of the industry’s most comprehensive vision AI portfolios. Pangiam’s facial recognition and biometrics technologies will complement BigBear.ai’s existing computer vision capabilities.

Major Boost to Government Business

A key rationale and benefit of the deal is expanding BigBear.ai’s business with U.S. government defense and intelligence agencies. The company currently serves 20 government customers with its predictive analytics solutions. Adding Pangiam’s technology and expertise will open significant new opportunities.

Pangiam brings an impressive customer base that includes the Department of Homeland Security, U.S. Customs and Border Protection, and major international airports. Its vision AI analytics help these customers streamline operations and enhance security.

According to Mandy Long, BigBear.ai CEO, the combined entity will be able to “pursue larger customer opportunities” in the government sector. Leveraging Pangiam’s portfolio is expected to result in larger contracts for expanded vision AI services.

CombiningComplementary Vision AI Technologies

Technologically, the acquisition enables BigBear.ai to provide comprehensive vision AI solutions. Pangiam’s strength lies in near-field applications like facial recognition and biometrics. BigBear.ai has capabilities in far-field vision AI that analyzes wider environments.

Together, the combined portfolio covers the full spectrum of vision AI’s possibilities. BigBear.ai notes this full stack capability will be unique in the industry, giving the company an edge over other players.

The vision AI integration also unlocks new potential for BigBear.ai’s existing government customers. Its current predictive analytics solutions can be augmented with Pangiam’s facial recognition and biometrics tools. This builds on the company’s strategy to cross-sell new capabilities to established customers.

Long describes the alignment of Pangiam and BigBear.ai’s vision AI prowess as a key factor that will “vault solutions currently available in market.” The combined innovation assets create opportunities to push vision AI technology forward and build next-generation solutions.

Fast-Growing Market Opportunities

The acquisition comes as vision AI represents a $20 billion market opportunity predicted to grow at over 20% CAGR through 2030. It is one of the most dynamic segments within the booming AI industry.

With Pangiam under its wing, BigBear.ai is making a major play for leadership in this high-potential space. The new capabilities and customer reach significantly expand its addressable market in areas like government, airports, identity verification, and border security.

BigBear.ai also gains vital talent and IP to enhance its vision AI research and development efforts. This will help fuel its ability to bring new innovations to customers seeking advanced vision AI systems.

In a statement, BigBear.ai CEO Mandy Long called the merger a “holy grail” deal that delivers full spectrum vision AI capabilities spanning near and far field environments. It positions the newly combined company to capitalize on surging market demand from government and commercial sectors.

The proposed $70 million acquisition shows BigBear.ai is putting its money where its mouth is in terms of dominating the up-and-coming vision AI arena. With Pangiam’s tech and talent on board, BigBear.ai aims to aggressively pursue larger opportunities and cement its status as an industry frontrunner.

Low-Cost Business Model and Disciplined Capital Allocation Drive Solid Operating Performance and Strong EPS Growth

Third Quarter Revenue of $2 Billion with GAAP EPS of $1.79; Adjusted EPS of $1.88

GAAP Operating Income of $91 Million; GAAP Net Income of $70 Million; Adjusted EBITDA of $125 Million

Repurchased $32 Million of Shares in the Third Quarter of 2023

Updates Full-Year 2023 Guidance

BOCA RATON, Fla.–(BUSINESS WIRE)–Nov. 8, 2023– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the third quarter ended September 30, 2023.

Consolidated (in millions, except per share amounts)

3Q23

3Q22

YTD23

YTD22

Selected GAAP and Non-GAAP measures:

Sales

$2,009

$2,172

$6,025

$6,385

Sales change from prior year period

(8)%

(6)%

Operating income

$91

$84

$232

$188

Adjusted operating income (1)

$95

$95

$247

$238

Net income from continuing operations

$70

$67

$176

$142

Diluted earnings per share from continuing operations

$1.79

$1.36

$4.38

$2.84

Adjusted net income from continuing operations (1)

$73

$73

$187

$177

Adjusted earnings per share from continuing operations (fully diluted) (1)

$1.88

$1.48

$4.66

$3.54

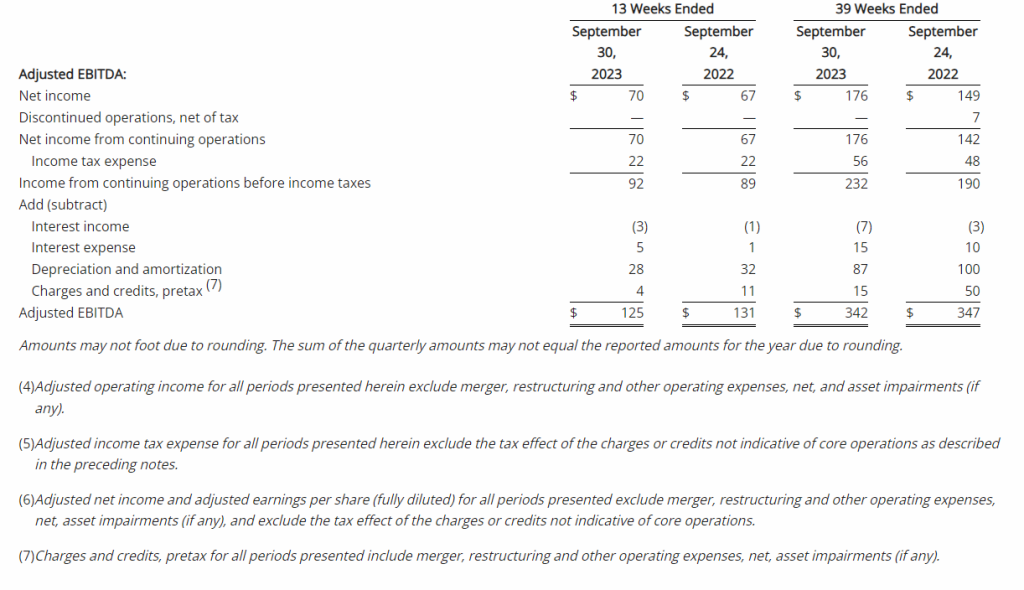

Adjusted EBITDA (1)

$125

$131

$342

$347

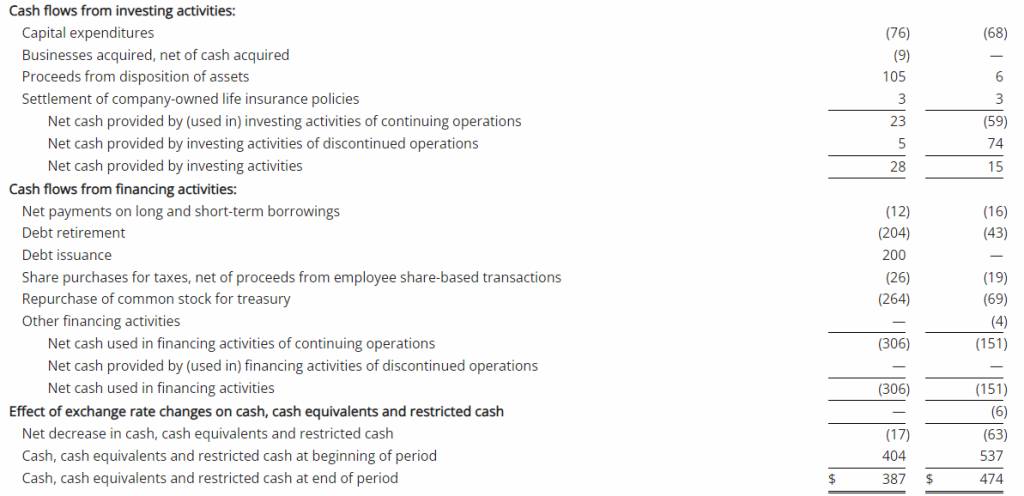

Operating Cash Flow from continuing operations

$112

$163

$261

$79

Free Cash Flow (2)

$86

$138

$183

$11

Adjusted Free Cash Flow (3)

$89

$160

$192

$54

Third Quarter 2023 Summary(1)(2)(3)

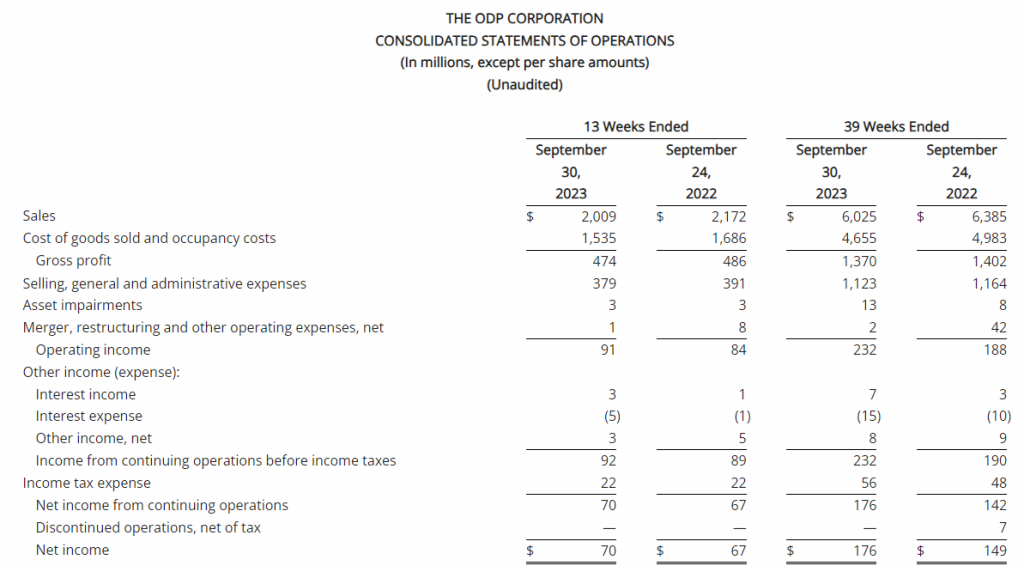

Total reported sales of $2.0 billion, down 8% versus the prior year, primarily due to lower sales in its Office Depot consumer division, largely driven by 71 fewer retail locations in service compared to the prior year, as well as lower retail and online consumer traffic and transactions

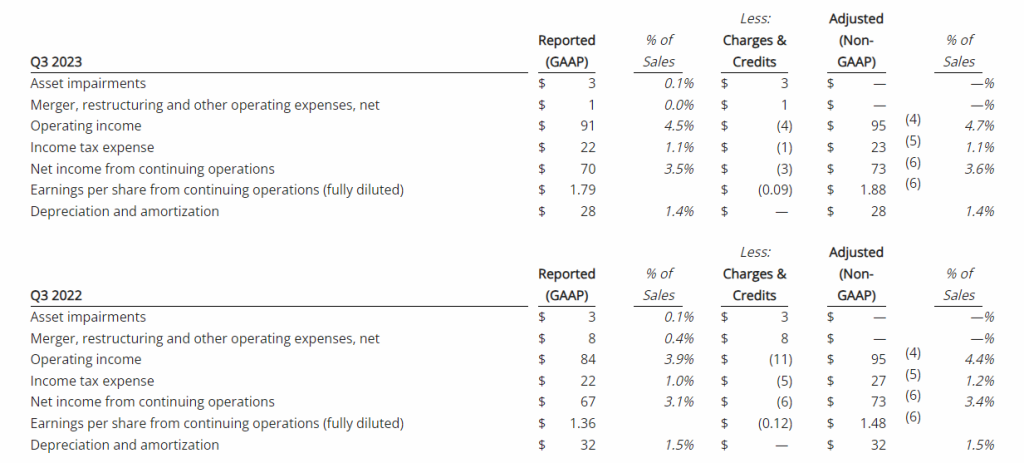

GAAP operating income of $91 million and net income from continuing operations of $70 million, or $1.79 per diluted share, versus $84 million and $67 million, respectively, or $1.36 per diluted share, in the prior year

Adjusted operating income of $95 million, flat compared to the third quarter of 2022; adjusted EBITDA of $125 million, compared to $131 million in the third quarter of 2022

Adjusted net income from continuing operations of $73 million, or adjusted diluted earnings per share from continuing operations of $1.88, versus $73 million or $1.48, respectively, in the prior year

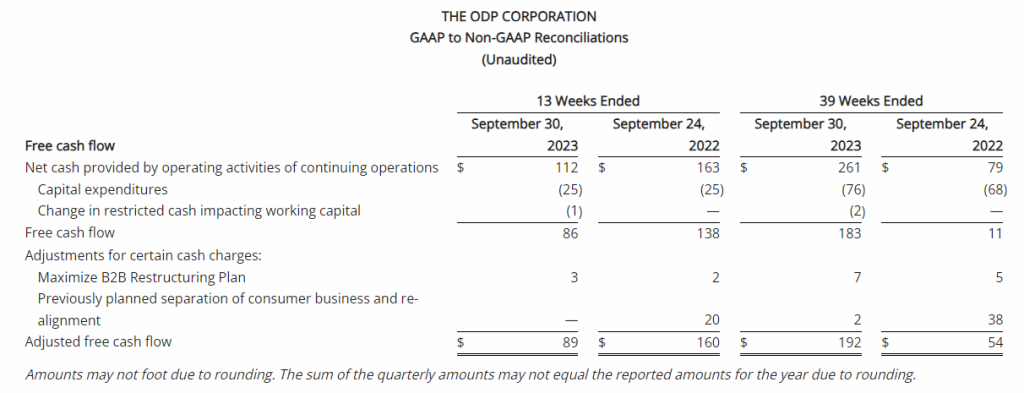

Operating cash flow from continuing operations of $112 million and adjusted free cash flow of $89 million, versus $163 million and $160 million, respectively, in the prior year

Repurchased 659 thousand shares at a cost of $32 million in the third quarter of 2023

$1.2 billion of total available liquidity including $384 million in cash and cash equivalents at quarter end

“I am extremely impressed seeing the day-to-day commitment and exceptional execution from our team as I fulfill Chief Executive Officer Gerry Smith’s responsibilities while he is on medical leave,” said Joseph Vassalluzzo, ODP’s chairman of the board. “In the quarter, our team delivered strong operating income and earnings per share results against a challenging economic backdrop, reflecting our unwavering commitment to operational excellence and to our low-cost business model approach.

“We continue to make progress across our four business units as we execute our three horizons strategy. This included expanding margins at ODP Business Solutions, new product testing and category expansion at Office Depot, securing new third-party customers at Veyer while remaining on track to more than double third-party EBITDA this year, and enhancing our platform and customer engagement at Varis.

“Our shareholder value creation formula, which integrates operational excellence with a shareholder-focused capital allocation plan, including the repurchase of approximately $32 million of shares during the quarter, contributed to a meaningful year-over-year increase in adjusted earnings per share for the third quarter and revised upward EPS guidance for the full year,” Vassalluzzo added.

“As we look ahead, we anticipate the macroeconomic environment to remain challenging throughout the remainder of the year. However, we are confident in our position of strength and will continue to focus on driving value for shareholders through our low-cost business model, leveraging our multiple routes to market, and continuing with our disciplined capital allocation,” Vassalluzzo concluded.

Consolidated Results

Reported (GAAP) Results

Total reported sales for the third quarter of 2023 were $2 billion, a decrease of 8% compared with the same period last year. This was driven primarily by lower sales in its consumer division, Office Depot, primarily due to 71 fewer stores in service compared to last year related to planned store closures, as well as lower retail and online consumer traffic. Sales at ODP Business Solutions Division were down slightly compared to last year, largely driven by slower return to office trends and lower sales of technology products. Meanwhile, Veyer provided strong logistics support for the ODP Business Solutions and Office Depot Divisions, and continued to capture additional demand for its supply chain and procurement solutions among other third-party customers.

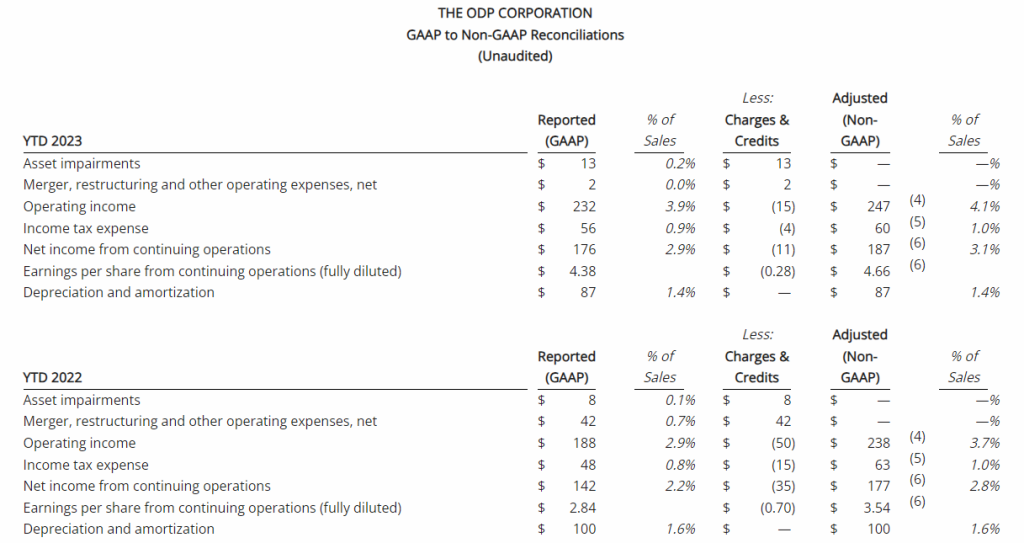

The Company reported operating income of $91 million in the third quarter of 2023, up 8% compared to operating income of $84 million in the prior year period. Operating results in the third quarter of 2023 included $4 million of charges. These charges consisted primarily of $3 million associated with non-cash asset impairments largely related to the operating lease right-of-use (ROU) assets associated with the Company’s retail store locations. Net income from continuing operations was $70 million, or $1.79 per diluted share in the third quarter of 2023, up from $67 million, or $1.36 per diluted share in the third quarter of 2022.

Adjusted (non-GAAP) Results(1)

Adjusted results for the third quarter of 2023 exclude charges and credits totaling $4 million as described above and the associated tax impacts.

Third quarter of 2023 adjusted EBITDA was $125 million compared to $131 million in the prior year period. This included depreciation and amortization of $28 million and $32 million in the third quarters of 2023 and 2022, respectively

Third quarter of 2023 adjusted operating income was $95 million, flat compared to the third quarter of 2022

Third quarter of 2023 adjusted net income from continuing operations was $73 million, or $1.88 per diluted share, compared to $73 million, or $1.48 per diluted share, in the third quarter of 2022, an increase of 27% on a per share basis

Division Results

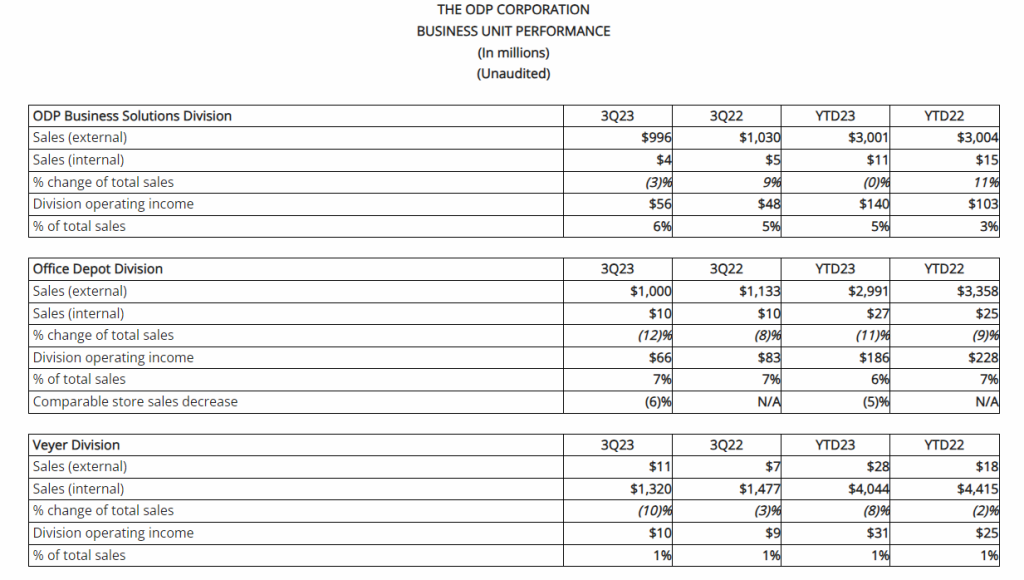

ODP Business Solutions Division

Leading B2B distribution solutions provider serving small, medium and enterprise level companies with an annual trailing-twelve-month revenue in excess of $4 billion

Reported sales were $1.0 billion in the third quarter of 2023, down approximately 3% compared to the same period last year primarily related to lower sales of technology products and weaker macroeconomic conditions

Stronger sales in cleaning and breakroom supplies were more than offset by lower sales of technology and core supplies

Total adjacency category sales, including cleaning and breakroom, furniture, technology, and copy and print, were 44% of total ODP Business Solutions’ sales

Continued strong pipeline and net new business customer additions

Operating income was $56 million in the third quarter of 2023, up 17% over the same period last year, related primarily to higher gross margins. As a percentage of sales, operating income margin was 6%, up 90 basis points compared to the same period last year

Office Depot Division

Leading provider of retail consumer and small business products and services distributed via Office Depot and OfficeMax retail locations and an award-winning eCommerce presence

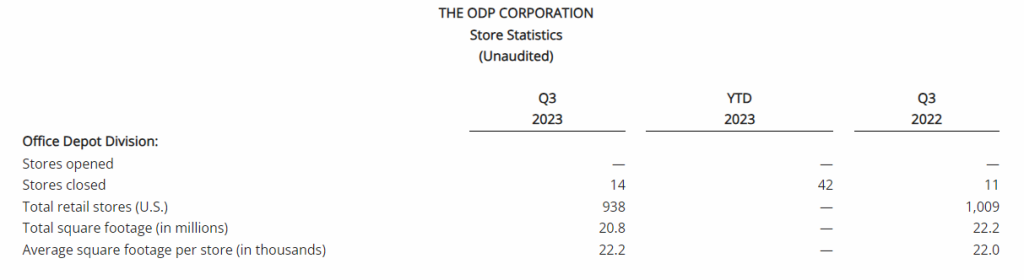

Reported sales were $1.0 billion in the third quarter of 2023, down 12% compared to the prior year period partially due to 71 fewer retail outlets in service associated with planned store closures, as well as lower demand relative to last year in certain product categories, softer back-to-school seasonal demand, and lower online sales. The Company closed 14 retail stores in the quarter and had 938 stores at quarter end. Sales were down approximately 6% on a comparable store basis

Stronger sales of copy and print services were more than offset by lower sales in supplies, technology, and other categories

Store and online traffic were lower year over year due to a greater percentage of customers having returned to the office post pandemic, as well as weaker macroeconomic activity

Operating income was $66 million in the third quarter of 2023, compared to operating income of $83 million during the same period last year, driven primarily by the flow through impact from lower sales. As a percentage of sales, operating income was 7%, flat compared to the same period last year.

Veyer Division

Veyer is a supply chain, distribution, procurement and global sourcing operation with over 35 years of experience and proven leadership, supporting Office Depot and ODP Business Solutions, as well as third-party customers. Veyer’s assets and capabilities include 8 million square feet of infrastructure through a nationwide network of distribution centers, cross-docks, and other facilities throughout the United States; a global sourcing presence in Asia; a large private fleet of vehicles; and next-day delivery to 98.5% of US population

In the third quarter of 2023, Veyer provided strong support for its internal customers, ODP Business Solutions and Office Depot, as well as for its third-party customers, generating sales of $1.3 billion

Operating income was $10 million in the third quarter of 2023, up from $9 million in the prior year period related to the favorable impacts of higher sales to external third parties and lower product costing

In the quarter relative to last year, sales and EBITDA generated from third party customers was up 57% and 119% respectively, resulting in sales of approximately $11 million and EBITDA of $3 million in the quarter

Varis Division

Varis is a tech-enabled B2B indirect procurement marketplace launched in the fourth quarter of 2022, which provides buyers and suppliers a seamless way to transact through the platform’s consumer-like buying experience and advanced spend management tools

Successfully launched the platform in the fourth quarter of 2022; adding and on-boarding new customers, incorporating feedback, and adding new features and capabilities to the platform

Varis generated revenues in the third quarter of 2023 of $2 million, flat compared to the third quarter of 2022

Operating loss was $17 million, flat compared to the third quarter of 2022, as the division continued to enhance its platform and onboard new customers

Share Repurchases

The Company continued to execute under its previously announced $1 billion share repurchase authorization, available through year-end 2025. During the third quarter of 2023, the Company repurchased 659 thousand shares at a cost of $32 million. Since the inception of the authorization beginning in November 2022, the Company has repurchased 9 million shares for approximately $420 million.

The number of shares to be repurchased in the future and the timing of such transactions will depend on a variety of factors, including market conditions, regulatory requirements, and other corporate considerations. The current authorization could be suspended or discontinued at any time as determined by the Board of Directors.

Balance Sheet and Cash Flow

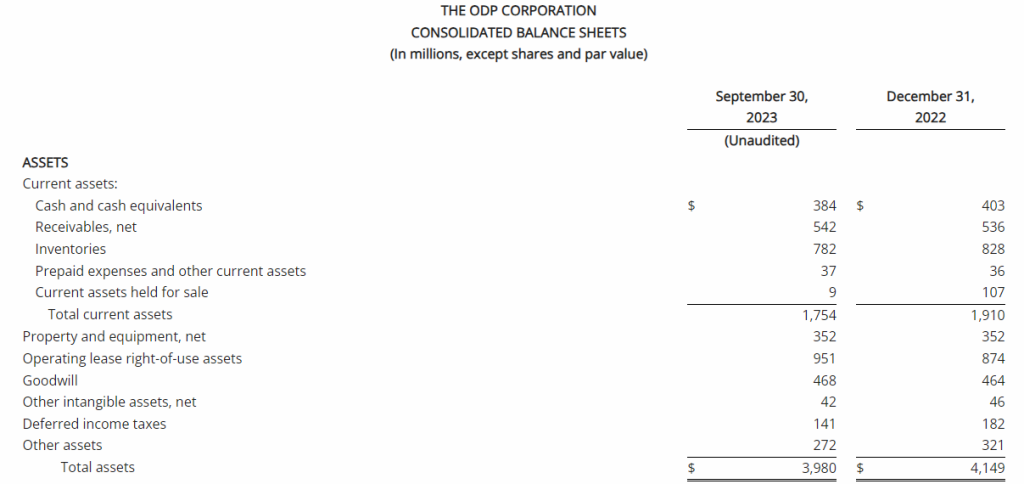

As of September 30, 2023, ODP had total available liquidity of approximately $1.2 billion, consisting of $384 million in cash and cash equivalents and $771 million of available credit under the Third Amended Credit Agreement. Total debt was $173 million.

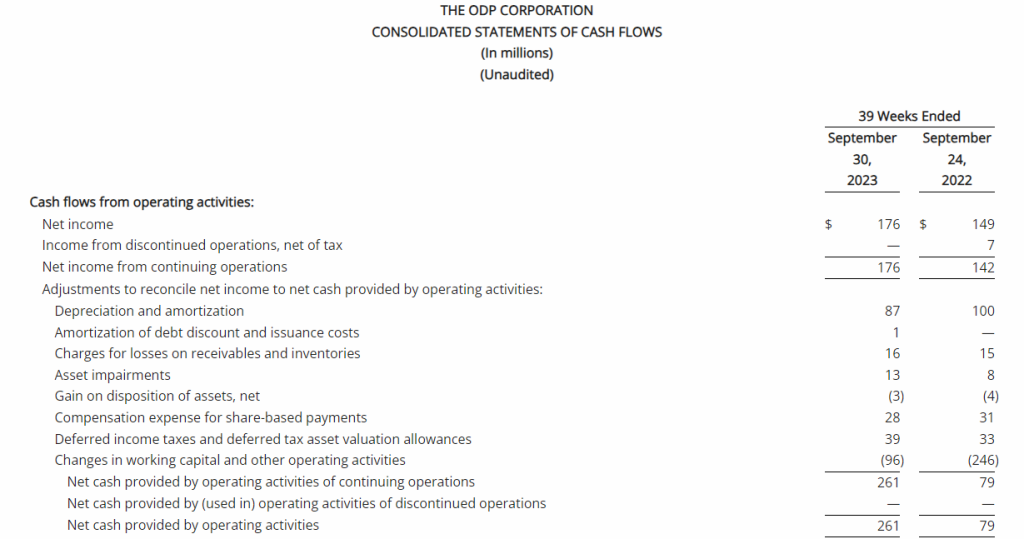

For the third quarter of 2023, cash generated by operating activities of continuing operations was $112 million, which included $3 million in restructuring and other spend, compared to cash provided by operating activities of continuing operations of $163 million in the third quarter of the prior year, which included $22 million in restructuring and other spend. The year-over-year change in operating cash flow is largely related to the timing of certain working capital items.

Capital expenditures in the third quarter of 2023 and 2022 were $25 million, reflecting continued growth investments in the Company’s digital transformation, distribution network, and eCommerce capabilities. Adjusted Free Cash Flow(3) was $89 million in the third quarter of 2023, compared to $160 million in the prior year period.

“I would like to recognize our entire team for their commitment and dedication in managing inventory and working capital, which has resulted in another quarter of strong cash flow generation,” said Anthony Scaglione, executive vice president and chief financial officer of The ODP Corporation. “As we work to close out the year, we maintain our disciplined approach, focusing on managing costs, maximizing cash flow, and executing our capital allocation plan,” Scaglione added.

Updated 2023 Expectations

“Our team’s unwavering commitment to delivering value is evident in our compelling customer proposition, strong free cash flow generation, and strategic capital allocation for the benefit of our shareholders,” highlighted Vassalluzzo. “While we acknowledge the influence of the challenging macroeconomic environment on consumer and business activity, we remain steadfast in our dedication to driving long-term value within our business through effective execution of our three horizons strategy.”

The Company’s full year guidance for 2023 included in this release includes non-GAAP measures, such as Adjusted EBITDA, Adjusted Operating Income, Adjusted Earnings per Share and Adjusted Free Cash Flow. These measures exclude charges or credits not indicative of core operations, which may include but not be limited to merger integration expenses, restructuring charges, acquisition-related costs, executive transition costs, asset impairments and other significant items that currently cannot be predicted without unreasonable efforts. The exact amount of these charges or credits are not currently determinable but may be significant. Accordingly, the Company is unable to provide equivalent GAAP measures or reconciliations from GAAP to non-GAAP for these financial measures without unreasonable effort.

The Company is updating its full year guidance for 2023 as follows:

Previous 2023 Guidance

Updated 2023 Guidance

Sales

Approximately $8 billion

Revised to $7.8 – $7.9 billion

Adjusted EBITDA

$400 – $430 million

Affirmed

Adjusted Operating Income

$270 – $300 million

Revised to $280 – $310 million

Adjusted Earnings per Share(*)

$5.00 – $5.30 per share

Revised to $5.30 – $5.60 per share

Adjusted Free Cash Flow(**)

$200 – $230 million

Affirmed

Capital Expenditures

$100 – $120 million

Affirmed

*Adjusted Earnings per Share (EPS) guidance for 2023 includes tax benefits related to R&D and employee-related tax credits and includes expected impact from share repurchases

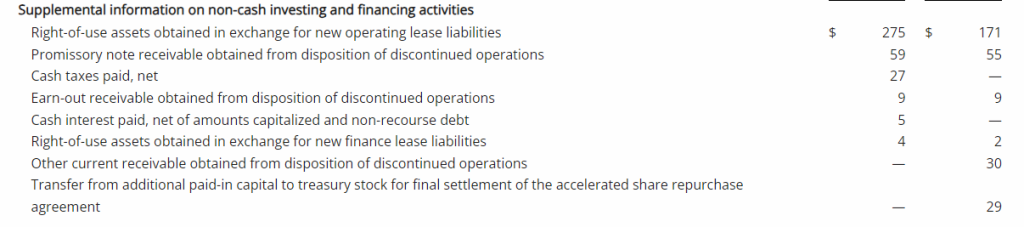

**Adjusted Free Cash Flow is defined as cash flows from operating activities less capital expenditures excluding cash charges associated with the Company’s Maximize B2B Restructuring and expenses incurred in connection with our previously planned separation of the consumer business and re-alignment

“Our year-to-date performance speaks to the resilience of our team and the strength of our low-cost business model and capital allocation approach,” said Scaglione. “While the weaker macroeconomic conditions have impacted the level of consumer and business activity creating top-line headwinds, our continued focus on operational excellence has us well positioned to continue driving strong operating results as we close out the year. Our updated guidance assumes a consistent overall macroeconomic environment and reflects our year-to-date revenue trends, while increasing our outlook for adjusted operating income and adjusted EPS.

Our increased adjusted EPS outlook also assumes a lower full-year effective tax rate driven by the execution of certain tax credits, lower than anticipated interest expense associated with projected intra-quarter ABL borrowings, and the impact from our continued share buyback activity,” Scaglione added.

The ODP Corporation will webcast a call with financial analysts and investors on November 8, 2023, at 9:00 am Eastern Time, which will be accessible to the media and the general public. To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event.

(1)

As presented throughout this release, adjusted results represent non-GAAP financial measures and exclude charges or credits not indicative of core operations and the tax effect of these items, which may include but not be limited to merger integration, restructuring, acquisition costs, and asset impairments. Reconciliations from GAAP to non-GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(2)

As used in this release, Free Cash Flow is defined as cash flows from operating activities less capital expenditures. Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(3)

As used in this release, Adjusted Free Cash Flow is defined as Free Cash Flow excluding cash charges associated with the Company’s Maximize B2B Restructuring, and expenses incurred in connection with our previously planned separation of the consumer business and re-alignment. Adjusted Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products, services, and technology solutions through an integrated business-to-business (B2B) distribution platform and omni-channel presence, which includes supply chain and distribution operations, dedicated sales professionals, a B2B digital procurement solution, online presence, and a network of Office Depot and OfficeMax retail stores. Through its operating companies ODP Business Solutions, LLC; Office Depot, LLC; Veyer, LLC; and Varis, Inc, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

This communication may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements or disclosures may discuss goals, intentions and expectations as to future trends, plans, events, results of operations, cash flow or financial condition, the potential impacts on our business due to the unknown severity and duration of the COVID-19 pandemic, or state other information relating to, among other things, the Company, based on current beliefs and assumptions made by, and information currently available to, management. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “expectations”, “outlook,” “intend,” “may,” “possible,” “potential,” “predict,” “project,” “propose” or other similar words, phrases or expressions, or other variations of such words. These forward-looking statements are subject to various risks and uncertainties, many of which are outside of the Company’s control. There can be no assurances that the Company will realize these expectations or that these beliefs will prove correct, and therefore investors and stakeholders should not place undue reliance on such statements.

Factors that could cause actual results to differ materially from those in the forward-looking statements include, among other things, highly competitive office products market and failure to differentiate the Company from other office supply resellers or respond to decline in general office supplies sales or to shifting consumer demands; competitive pressures on the Company’s sales and pricing; the risk that the Company is unable to transform the business into a service-driven, B2B platform that such a strategy will not result in the benefits anticipated; the risk that the Company will not be able to achieve the expected benefits of its strategic plans, including its strategic shift to maintain all of its businesses under common ownership; the risk that the Company may not be able to realize the anticipated benefits of acquisitions due to unforeseen liabilities, future capital expenditures, expenses, indebtedness and the unanticipated loss of key customers or the inability to achieve expected revenues, synergies, cost savings or financial performance; the risk that the Company is unable to successfully maintain a relevant omni-channel experience for its customers; the risk that the Company is unable to execute the Maximize B2B Restructuring Plan successfully or that such plan will not result in the benefits anticipated; failure to effectively manage the Company’s real estate portfolio; loss of business with government entities, purchasing consortiums, and sole- or limited-source distribution arrangements; failure to attract and retain qualified personnel, including employees in stores, service centers, distribution centers, field and corporate offices and executive management, and the inability to keep supply of skills and resources in balance with customer demand; failure to execute effective advertising efforts and maintain the Company’s reputation and brand at a high level; disruptions in computer systems, including delivery of technology services; breach of information technology systems affecting reputation, business partner and customer relationships and operations and resulting in high costs and lost revenue; unanticipated downturns in business relationships with customers or terms with the suppliers, third-party vendors and business partners; disruption of global sourcing activities, evolving foreign trade policy (including tariffs imposed on certain foreign made goods); exclusive Office Depot branded products are subject to additional product, supply chain and legal risks; product safety and quality concerns of manufacturers’ branded products and services and Office Depot private branded products; covenants in the credit facility; general disruption in the credit markets; incurrence of significant impairment charges; retained responsibility for liabilities of acquired companies; fluctuation in quarterly operating results due to seasonality of the Company’s business; changes in tax laws in jurisdictions where the Company operates; increases in wage and benefit costs and changes in labor regulations; changes in the regulatory environment, legal compliance risks and violations of the U.S. Foreign Corrupt Practices Act and other worldwide anti-bribery laws; volatility in the Company’s common stock price; changes in or the elimination of the payment of cash dividends on Company common stock; macroeconomic conditions such as higher interest rates and future declines in business or consumer spending; increases in fuel and other commodity prices and the cost of material, energy and other production costs, or unexpected costs that cannot be recouped in product pricing; unexpected claims, charges, litigation, dispute resolutions or settlement expenses; catastrophic events, including the impact of weather events on the Company’s business; the discouragement of lawsuits by shareholders against the Company and its directors and officers as a result of the exclusive forum selection of the Court of Chancery, the federal district court for the District of Delaware or other Delaware state courts by the Company as the sole and exclusive forum for such lawsuits; and the impact of the COVID-19 pandemic on the Company’s business. The foregoing list of factors is not exhaustive. Investors and shareholders should carefully consider the foregoing factors and the other risks and uncertainties described in the Company’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K filed with the U.S. Securities and Exchange Commission. The Company does not assume any obligation to update or revise any forward-looking statements.

ATLANTA, November 8, 2023 — Gray Television, Inc. (“Gray”) (NYSE: GTN) announced today that its Board of Directors has authorized a quarterly cash dividend of $0.08 per share of its common stock and Class A common stock. The dividend is payable on December 29, 2023, to shareholders of record at the close of business on December 15, 2023.

About Gray Television:

We are a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets. Our television stations serve 113 television markets that collectively reach approximately 36 percent of US television households. This portfolio includes 80 markets with the top-rated television station and 102 markets with the first and/or second highest rated television station in 2022. We also own video program companies Raycom Sports, Tupelo Media Group, and PowerNation Studios, as well as the studio production facilities Assembly Atlanta and Third Rail Studios. We own a majority interest in Swirl Films. For more information, please visit www.gray.tv.

Forward-Looking Statements:

This press release contains certain forward-looking statements that are based largely on Gray’s current expectations and reflect various estimates and assumptions by Gray. These statements are statements other than those of historical fact and may be identified by words such as “estimates”, “expect,” “anticipate,” “will,” “implied,” “assume” and similar expressions. Forward-looking statements are subject to certain risks, trends and uncertainties that could cause actual results and achievements to differ materially from those expressed in such forward-looking statements. Such risks, trends and uncertainties, which in some instances are beyond Gray’s control include Gray’s inability to provide expected future payment of dividends, and other future events. Gray is subject to additional risks and uncertainties described in Gray’s quarterly and annual reports filed with the Securities and Exchange Commission from time to time, including in the “Risk Factors,” and management’s discussion and analysis of financial condition and results of operations sections contained therein, which reports are made publicly available via its website, www.gray.tv. Any forward-looking statements in this communication should be evaluated in light of these important risk factors. This press release reflects management’s views as of the date hereof. Except to the extent required by applicable law, Gray undertakes no obligation to update or revise any information contained in this communication beyond the date hereof, whether as a result of new information, future events or otherwise.

# # #

Gray Contacts:

www.gray.tv.

Jim Ryan, Executive Vice President and Chief Financial Officer, (404) 504-9828

Kevin P. Latek, Executive Vice President, Chief Legal and Development Officer, (404) 266-8333

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 103 facilities totaling approximately 83,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q23 Results. Revenue for the quarter came in at $602.8 million, compared to $616.7 million a year ago. Adjusted EBITDA totaled $118.7 million, EPS was $0.16, and adjusted EPS $0.19. In the year ago period, GEO reported $136.2 million, $0.26, and $0.33, respectively. We had forecast $595 million, $125.6 million, $0.21, and $0.21, respectively.

Overcoming ISAP. Population declines under the ISAP program continue to be a headwind, with segment revenue $42.6 million y-o-y. Secure Services revenue was off modestly, while Reentry Services, Managed Only, and Non-residential Services all saw nice increases in revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Approval. Yesterday, MustGrow announced the Company received Health Canada’s Pest Management Regulatory Agency (PMRA) approval to commence large-scale field trials via NexusBioAg’s 2024 BioAdvantage Trials Program (BAT Program). The program will focus on the Company’s TerraMG mustard-derived soil biopesticide technology for use in Canadian canola and pulse crop markets.

NexusBioAg BAT Program. The BAT Program is an industry leading field trialing program with an established process to gather data from large field scale trials across Canada. NexusBioAg, a partner of MustGrow and the operator of the program, validates product efficacy and establishes the product value and opportunity. Through the BAT Program, NexusBioAg farm customers will have access to MustGrow’s mustard plant-based product.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results. Great Lakes reported total revenue of $117.2 million, a decrease from $158.4 million the prior year and below our estimate of $137 million. Gross margin was 7.7% compared to 2.4%, but lower than our projection of 8.8%. Net loss was at $6.2 million, or $0.09 per diluted share compared to $9.9 million last year, or $0.15. We projected a net loss of $6 million, or $0.09 per share. Adjusted EBTIDA totaled $5.3 million versus $1.3 million in the previous year.

Backlog. Great Lakes ended the quarter record backlog of $1.03 billion, up from $327.1 million at 1Q23, not including approximately $50.0 million of performance obligations related to offshore wind contracts. In addition, the Company ended the quarter with $225 million in low bids and options pending award. Significantly, 71% of backlog was capital projects work, which will help drive margins higher going forward.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FY Q1 results. The company reported Q1 revenue of $227.4 million, 4.7% below our estimate of $238.5 million. The modest revenue miss was attributed to experimenting with various mid-week promotional pricing, which did not go well, before pivoting to a more cost effective pricing strategy. Adj. EBITDA in Q1 was $52.1 million, approximately 16% below our estimate of $62 million. While operating results were a tad softer, management gained valuable knowledge about its customer base.

2024 Outlook. Management views fiscal 2024 as a year of investment for more robust top and bottom line growth in fiscal 2025. Notably, for full fiscal year 2024, the company has allocated roughly $160 million for acquisitions, $40 million for new builds, and $75 million for conversions. In our view, the aggressive expansion efforts should help the company continue its impressive revenue growth trajectory.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mortgage rates took a steep dive last week in the biggest one-week drop since September 2021. The average 30-year fixed mortgage rate decreased to 7.61% from 7.86% the week prior, according to the Mortgage Bankers Association (MBA).

This plunge in rates over the course of just one week sparked a 2.5% increase in total mortgage loan application volume. It was the first uptick in demand after four straight weeks of declines.

The drop in mortgage rates was driven by positive economic news. The Federal Reserve struck a dovish tone signaling slower future rate hikes. This was followed by monthly jobs data that came in under expectations pointing to cooling inflation.

What does the rate plunge mean for mortgage borrowers? Here are the key takeaways:

Refinancing Demand Rises But Still Lags 2021

The dip in rates led to a 2% bump in refinance application volume last week. This marks a turnaround after refinancing demand fell to a 22-year low in October when rates topped 7%.

But refinancing is still 7% lower than the same week last year. In 2021, rates hovered near 3%, fueling a refinancing boom. Today, most homeowners already refinanced at those historically low rates.

For context, 63% of mortgage borrowers are paying rates under 4%, according to Black Knight data. There is little incentive for these borrowers to refinance at today’s higher rates.

The bottom line is that lower rates are inviting more refinancing but volumes are still a fraction of the 2021 frenzy. Only borrowers with rates well above 7% stand to meaningfully benefit from a refi now.

Homebuying Demand Rebounds But Remains Suppressed

The positive rate movement also drove a 3% weekly gain in purchase mortgage applications. This suggests some home buyers are jumping at the chance to lock lower rates.

But purchase demand remains sharply lower than last year, down 20% from the same week in 2021. Sky high home prices are outweighing the lure of lower rates for many prospective buyers.

The median home sales price in September was $384,800, up 8.4% from 2021 according to the National Association of Realtors. Price gains are outpacing the rate relief.

The optimism was cemented on November 4 when the October jobs report showed the labor market is starting to cool. Employers added 261,000 jobs last month, below estimates of 300,000.

Slower job growth reduces inflation pressures, reinforcing the case for the Fed to temper rate hikes. This positive news for the economy caused mortgage rates to unravel.

What’s Ahead for Mortgage Rates?

Mortgage rates started this week slightly higher but remain volatile. The MBA noted there are fewer major economic events on the calendar this week that could substantially sway rates.

But Fed speakers may still influence rate expectations. Any renewed hawkish signals could nudge rates higher again. Rates are also very sensitive to inflation data hints.

For now, the overall trend for mortgage rates is bouncing within a range but remains comparatively high historically. Barring an unforeseen shock, major swings in either direction appear unlikely in the near term.

BY THE COMTECH EDITORIAL TEAM – NOV 7, 2023 | 3 MIN READ

TORRANCE, Calif. & MELVILLE, N.Y. — Nov. 7, 2023 — Stellant Systems, Inc. (Stellant) and Comtech (NASDAQ: CMTL), both global technology leaders, announced today that the companies have closed, effective November 7, 2023, on the previously announced sale of Comtech’s Power Systems Technology (PST) product line. Stellant is a portfolio company of Arlington Capital Partners, a Washington D.C.-area private equity firm with extensive experience investing in regulated industries.

Net cash proceeds received at closing by Comtech approximated $32.5 million and were used in part by Comtech to pay down outstanding debt on its existing Credit Facility. In connection with the consummation of the closing of the transaction, Comtech entered into a Third Amended and Restated Credit Agreement with its existing lenders and a Second Amended and Restated Certificate of Designations with its existing Series A convertible preferred shareholders, who both consented to the transaction. Comtech will provide financial and other information concerning the impact of the PST transaction during its next regularly scheduled quarterly earnings conference call to review the results of its fiscal quarter ended October 31, 2023, the exact date and time of which will be announced in advance.

About Stellant Systems, Inc.

Stellant Systems is a premier manufacturer of critical spectrum and RF power amplification systems to the space, defense, medical, science and industrial markets for both domestic and international customers. Stellant has three domestic manufacturing facilities and nearly 1,000 employees. For more information, visit www.Stellantsystems.com.

About Comtech

Comtech Telecommunications Corp. is a leading global technology company providing terrestrial and wireless network solutions, next-generation 9-1-1 emergency services, satellite and space communications technologies, and cloud native capabilities to commercial and government customers around the world. Our unique culture of innovation and employee empowerment unleashes a relentless passion for customer success. With multiple facilities located in technology corridors throughout the United States and around the world, Comtech leverages our global presence, technology leadership, and decades of experience to create the world’s most innovative communications solutions.For more information, please visit www.comtech.com.

About Arlington Capital Partners

Arlington Capital Partners is a Washington, DC-based private equity firm that has managed approximately $7 billion in capital commitments. Arlington is focused on middle market investment opportunities in growth industries including government services and technology, aerospace & defense, healthcare, and business services and software. The firm’s professionals and network have a unique combination of operating and private equity experience that enable Arlington to be a value-added investor. Arlington invests in companies in partnership with high quality management teams that are motivated to establish and/or advance their company’s position as leading competitors in their field. For more information, visit Arlington Capital’s website at arlingtoncap.com and follow Arlington on LinkedIn.

Forward-Looking Statements

Certain information in this press release contains forward-looking statements. Forward-looking statements can be identified by words such as: “will,” “intend,” “expect,” and similar references to future periods. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements about the consummation of the transaction and the anticipated benefits thereof. All such forward-looking statements are based upon current plans, estimates, expectations and ambitions that are subject to risks, uncertainties and assumptions, many of which are beyond the control of Stellant and Comtech, that could cause actual results to differ materially from those expressed in such forward-looking statements. Important risk factors that may cause such a difference include, but are not limited to: anticipated tax treatment, unforeseen liabilities, the possibility that any of the anticipated benefits of the transaction will not be realized or will not be realized within the expected time period, and other factors as described in Comtech’s filings with the Securities and Exchange Commission, including those under the heading “Risk Factors” in Comtech’s most recent Annual Report on Form 10-K. Stellant and Comtech do not intend to update or revise publicly any forward-looking statements, whether because of new information, future events, or otherwise, except as required by law.

PRINCETON, N.J., Nov. 07, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB) (PDS Biotech or the Company), a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer immunotherapies and infectious disease vaccines based on the Company’s proprietary T cell activating platforms, today announced that the Company will release financial results for the third quarter of 2023 on Tuesday, November 14, 2023, before the market opens. Following the release, management will host a conference call to review the financial results and provide a business update.

Tuesday, November 14, 2023, 8:00 AM ET Domestic: 877-407-3088 International: 201-389-0927 Conference ID: 13741454

After the live webcast, the event will be archived on PDS Biotech’s website for six months.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune® T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce and shrink tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials and will be advancing into a Phase 3 clinical trial in combination with KEYTRUDA® for the treatment of recurrent/metastatic HPV16-positive head and neck cancer in 2023. Our Infectimune® based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune® based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the other risks, uncertainties, and other factors described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in the documents we file with the U.S. Securities and Exchange Commission. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® and Infectimune® are registered trademarks of PDS Biotechnology Corporation. KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

Substantial THIO program progress including unprecedented disease control rate (DCR) of 100% in second-line non-small cell lung cancer (NSCLC)

Key THIO findings in gliomas, pediatric brain cancer, and second generation THIO-derived cancer therapies

Strong pace of enrollment in THIO-101 Phase 2 trial exceeds average enrollment pace in similar NSCLC trials

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA” or the “Company”), a clinical-stage biopharmaceutical company developing telomere-targeting immunotherapies for cancer, today reported financial results for the third quarter ended September 30, 2023 and key operational updates.

“Our successful and productive third quarter was punctuated by the outstanding data on our lead asset THIO that we recently revealed, and an accelerating pace of enrollment in our THIO-101 Phase 2 trial,” said Vlad Vitoc, M.D., MAIA’s Chairman and Chief Executive Officer. “We are expanding our trial in Europe, and with the FDA’s recent clearance for THIO studies in the U.S. as part of THIO-101, we have reached an essential milestone in the clinical development of THIO. Preliminary efficacy data from the trial is excellent and includes an unprecedented disease control rate (DCR) of 100% in second-line NSCLC treatment, far surpassing the standard of care DCR of 53-64%. We achieved the pre-determined statistical requirements to proceed to the next stage of the trial earlier than expected, and we look forward to sharing our continuing progress in the coming months and into 2024.”

Third Quarter Business Highlights and Recent Developments

THIO Program

Announced 100% Disease Control in Second-Line Non-Small Cell Lung Cancer Demonstrating Impressive Positive Preliminary Efficacy Data: 100% preliminary DCR was observed in second-line and 88% in third-line, in highly difficult-to-treat patients who already progressed through previous lines of treatment. DCRs across all dose levels met the pre-determined statistical requirements earlier than expected to proceed to next stage of the THIO-101 Phase 2 trial.

Highly Potent Anticancer Activity in Gliomas: MAIA’slead asset THIO showed highly potent anticancer activity in models of glioma, an aggressive type of brain tumor that originates from glial cells and is among the most difficult-to-treat cancers. As a monotherapy, THIO demonstrated efficacy in multiple glioma cell lines that had acquired resistance to the current state-of-the-art care temozolomide (TMZ).

THIO as Potential Therapy for Pediatric Brain Cancer: Study data showed THIO’s potent anticancer activity in diffuse intrinsic pontine glioma (DIPG), one of the most aggressive tumors affecting the central nervous system in children. The treatment resulted in noticeably increased tumor sensitivity to immune or ionizing radiation therapies.

Higher Anticancer Potency of Next Generation THIO Conjugates: Positive Investigational New Drug-enabling study data on telomere-targeting agents derived from lipid-modified THIO molecules warrant further in vivo in-depth investigation of THIO-like agents as second generation cancer therapies.

THIO-101 Phase 2 Clinical Trial

U.S. FDA Clearance of THIO IND Application: TheU.S. Food and Drug Administration (FDA) cleared an Investigational New Drug (IND) application enabling THIO to be evaluated in the U.S. as part of THIO-101, the Company’s ongoing global phase 2 clinical study in patients with advanced non-small cell lung cancer (NSCLC). THIO is being tested in sequential combination with a checkpoint inhibitor (CPI) to evaluate anti-tumor activity and immune response in NSCLC patients.

Strong Pace of Enrollment in THIO-101: 49 patients have been dosed to date at a pace of enrollment that is currently exceeding the average enrollment pace in similar NSCLC trials. Out of the 49 patients dosed, 37 have already completed at least one post baseline assessment.

Continuing Positive Preliminary Survival Data: The first 2 subjects dosed on trial (both receiving 3rd line of treatment) reported long term survival of 14.6 and 12.5 months, respectively, at the latest post baseline assessment with no new anti-cancer treatment initiated. Follow up was ongoing for the first subject at the time of data cut-off.

Third Quarter 2023 Financial Results

Cash Position: Cash totaled approximately $6.1 million as of September 30, 2023, compared to $10.9 million in cash as of December 31, 2022.

Research and Development (R&D) Expenses: R&D expenses were approximately $2.6 million for the quarter ended September 30, 2023, compared to approximately $2.3 million for quarter ended September 30, 2022. The increase was primarily related to an increase in scientific research expenses.

General and Administrative (G&A) Expenses: G&A expenses were approximately $2.4 million for the quarter ended September 30, 2023, compared to approximately $1.7 million for the quarter ended September 30, 2022. The increase for the quarter was primarily related to an increase in professional fees related to the write-off of deferred offering costs and an increase in investor relations costs.

Other Income, Net: Other income was approximately $0.08 million for the quarter ended September 30, 2023, compared to other income, net of $0.19 million for the quarter ended September 30, 2022, primarily related to a change in the fair value of warrant liability.

Net Loss: Net loss was approximately $4.9 million, or $0.36 per share, for the quarter ended September 30, 2023, as compared to net loss of approximately $4.9 million, or $0.48 per share, for the quarter ended September 30, 2022. Weighted average shares outstanding were 13,675,802 in the third quarter of 2023, compared to 10,165,622 in the third quarter of 2022.

For additional information on the Company’s financial results for the quarter ended September 30, 2023, please refer to the Form 10-Q filed with the SEC.

About THIO

THIO (6-thio-dG or 6-thio-2’-deoxyguanosine) is a first-in-class investigational telomere-targeting agent currently in clinical development to evaluate its activity in Non-Small Cell Lung Cancer (NSCLC). Telomeres, along with the enzyme telomerase, play a fundamental role in the survival of cancer cells and their resistance to current therapies. The modified nucleotide 6-thio-2’-deoxyguanosine (THIO) induces telomerase-dependent telomeric DNA modification, DNA damage responses, and selective cancer cell death. THIO-damaged telomeric fragments accumulate in cytosolic micronuclei and activates both innate (cGAS/STING) and adaptive (T-cell) immune responses. The sequential treatment with THIO followed by PD-(L)1 inhibitors resulted in profound and persistent tumor regression in advanced, in vivo cancer models by induction of cancer type–specific immune memory. THIO is presently developed as a second or later line of treatment for NSCLC for patients that have progressed beyond the standard-of-care regimen of existing checkpoint inhibitors.

About THIO-101, Phase 2 Clinical Trial

THIO-101 is a multicenter, open-label, dose finding Phase 2 clinical trial. It is the first trial designed to evaluate THIO’s anti-tumor activity when followed by PD-(L)1 inhibition. The trial is testing the hypothesis that low doses of THIO administered prior to an anti-PD-1 agent will enhance and prolong immune response in patients with advanced NSCLC who previously did not respond or developed resistance and progressed after first-line treatment regimen containing another checkpoint inhibitor. The trial design has two primary objectives: (1) to evaluate the safety and tolerability of THIO administered as an anticancer compound and a priming immune activator (2) to assess the clinical efficacy of THIO using Overall Response Rate (ORR) as the primary clinical endpoint. For more information on this Phase II trial, please visit ClinicalTrials.gov using the identifier NCT05208944.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. These forward-looking statements are only predictions and may differ materially from actual results due to a variety of factors including: (i) lower than anticipated rate of patient enrollment, (ii) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (iii) our ability to advance product candidates into, and successfully complete, clinical studies, (iv) the timing or likelihood of regulatory filings and approvals, (v) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (vi) the rate and degree of market acceptance of our product candidates, (vii) the size and growth potential of the markets for our product candidates and our ability to serve those markets, (viii) our ability to obtain and maintain intellectual property protection for our product candidates and (ix) other risks and uncertainties detailed from time to time in our filings with the Securities and Exchange Commission, including without limitation our periodic reports on Form 10-K and 10-Q, each as amended and supplemented from time to time. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.