Research News and Market Data on COCP

NOVEMBER 13, 2023

- Enrollment underway in Phase 1 trial with novel protease inhibitor CDI-988, the first potential dual coronavirus-norovirus oral antiviral

- Dosing expected to begin later this year in Phase 2a human challenge trial with oral CC-42344 for the treatment of pandemic and seasonal influenza A

- Phase 1 trial with inhaled CC-42344 expected to begin in the first half of 2024

BOTHELL, Wash., Nov. 13, 2023 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) (Cocrystal or the Company) reports financial results for the three and nine months ended September 30, 2023, and provides updates on its antiviral pipeline, upcoming milestones and business activities.

“We are making excellent progress in the clinical development of potent antivirals that address some of the world’s leading viral diseases,” said Sam Lee, Ph.D., President and co-CEO of Cocrystal. “With our novel oral PB2 inhibitor CC-42344 for the treatment of pandemic and seasonal influenza A, we expect to dose the first subjects in a Phase 2a human challenge study before year-end. We also are on track to begin a Phase 1 healthy volunteer trial in the first half of 2024 with inhaled CC-42344 as a potential therapeutic and prophylactic treatment for influenza A.

“Enrollment is underway in a Phase 1 trial with our first-in-class pan-coronavirus and pan-norovirus protease inhibitor CDI-988,” added Dr. Lee. “This oral potent antiviral candidate could reduce severity and death from pandemic outbreaks of highly contagious viral infections. CDI-988 has shown activity against multiple coronavirus and norovirus strains, including the genogroup II, genotype 4 (GII.4) norovirus strain, which is responsible for major norovirus outbreaks. With no approved treatments or vaccines, norovirus represents a significant unmet medical need.”

“With three clinical-stage antiviral programs in high-value unmet medical indications, the coming year promises to be active and potentially transformational for Cocrystal,” said James Martin, CFO and co-CEO. “I’m pleased to report that under our cost-efficient business model, we believe our current cash position is sufficient to fund planned operations beyond the next 12 months.”

Antiviral Product Pipeline Overview

We are developing therapeutics that inhibit the viral replication function of RNA viruses that cause acute and chronic diseases. Our drug-discovery process focuses on the highly conserved regions of the viral enzymes and inhibitor-enzyme interactions at the atomic level. By designing and selecting antiviral drug candidates that interrupt the viral replication process and have specific binding characteristics, we seek to develop drugs that are effective against the virus and mutants of the virus, and also have reduced off-target interactions that may cause undesirable side effects. Our drug discovery process differs from traditional, empirical medicinal chemistry approaches that often require iterative high-throughput compound screening and lengthy hit-to-lead processes.

Influenza Programs

Influenza is a severe respiratory illness caused by the influenza A or B virus that results in disease outbreaks mainly during the winter months. Influenza is a major global health threat that may become more challenging to treat in the future due to the emergence of highly pathogenic avian influenza viruses and resistance to approved influenza antivirals.

Each year there are approximately 1 billion cases of seasonal influenza worldwide, 3-5 million severe illnesses and up to 650,000 deaths, according to the World Health Organization. On average about 8% of the U.S. population contracts influenza each season. In addition to the health risk, influenza is responsible for approximately $10.4 billion in direct costs for hospitalizations and outpatient visits for adults in the U.S. annually.

- Pandemic and Seasonal Influenza A

- Our novel oral PB2 inhibitor CC-42344 has shown excellent in vitro antiviral activity against influenza A strains including pandemic and seasonal strains, as well as strains that are resistant to Tamiflu® and Xofluza®.

- In March 2022 we initiated enrollment in a randomized, double-controlled, dose-escalating Phase 1 trial to evaluate the safety, tolerability and pharmacokinetics (PK) of orally administered CC-42344 in healthy adults.

- In July 2022 we reported PK results from the single-ascending dose portion of the trial that support once-daily dosing.

- In December 2022 we reported favorable safety and tolerability results from the CC-42344 Phase 1 trial.

- In October 2023 we announced authorization from the United Kingdom Medicines and Healthcare Products Regulatory Agency to conduct a Phase 2a human challenge trial and we expect to begin treating influenza-infected subjects in this trial during the fourth quarter of 2023.

- Preclinical development is underway with inhaled CC-42344 as a potential therapeutic treatment and prophylaxis for influenza A. We expect to begin a Phase 1 clinical trial with inhaled CC-42344 in Australia in the first half of 2024.

- Pandemic and Seasonal Influenza A/B Program

- In January 2019 we entered into an Exclusive License and Research Collaboration Agreement with Merck Sharp & Dohme Corp. (Merck) to discover and develop certain proprietary influenza antiviral agents that are effective against influenza A and B strains. This agreement includes milestone payments of up to $156 million plus royalties on sales of products discovered under the agreement.

- In January 2021 we announced completion of all research obligations under the agreement, making Merck solely responsible for further preclinical and clinical development of these compounds.

- In early 2023 Merck notified us of its intent to continue development of the compounds discovered under this agreement and of their filing on behalf of both companies of multiple U.S. and international patent applications associated with these compounds. Merck continues to be responsible for managing the patents.

COVID-19 and Other Coronavirus Programs

By targeting viral replication enzymes and protease, we believe it is possible to develop effective treatments for all diseases caused by coronaviruses including COVID-19, Severe Acute Respiratory Syndrome (SARS) and Middle East Respiratory Syndrome (MERS). Our main SARS-CoV-2 protease inhibitors showed potent in vitro pan-viral activity against common human coronaviruses, rhinoviruses and respiratory enteroviruses that cause the common cold, as well as against noroviruses that can cause symptoms of acute gastroenteritis. Driven by the anticipated emergence of new COVID-19 variants, the global COVID-19 therapeutics market is estimated to exceed $16 billion by the end of 2031.

- Oral Protease Inhibitor CDI-988

- In October 2022 we announced the selection of CDI-988 as our lead candidate for development as a potential oral treatment for SARS-CoV-2. Designed and developed using our proprietary structure-based drug discovery platform technology, CDI-988 targets a highly conserved region in the active site of SARS-CoV-2 3CL (main) protease required for viral RNA replication.

- CDI-988 exhibited superior in vitro potency against SARS-CoV-2 with activity maintained against variants of concern, and demonstrated a safety profile and PK properties that support once-daily dosing.

- In May 2023 we announced approval of our application to the Australian regulatory agency for a planned randomized, double-blind, placebo-controlled Phase 1 trial to evaluate the safety, tolerability and PK of oral CDI-988 in healthy volunteers.

- In September 2023 we dosed the first subject in the CDI-988 Phase 1 trial.

- Intranasal/Pulmonary Protease Inhibitor CDI-45205

- CDI-45205 is our novel SARS-CoV-2 3CL (main) protease inhibitor and was among the broad-spectrum viral protease inhibitors we obtained from Kansas State University Research Foundation (KSURF) under an exclusive license agreement announced in April 2020. We believe the protease inhibitors obtained from KSURF have the ability to convert the inactive SARS-CoV-2 polymerase replication enzymes into an active form.

- CDI-45205 and several analogs showed potent in vitro activity against the main SARS-CoV-2 variants, surpassing the activity observed with the original Wuhan strain of the virus.

- CDI-45205 delivered via intraperitoneal injection demonstrated good bioavailability in mouse and rat PK studies, and no cytotoxicity against a variety of human cell lines. CDI-45205 also demonstrated a strong synergistic effect with the FDA-approved COVID-19 medicine remdesivir.

- In January 2022 we received guidance from the FDA regarding further preclinical and clinical development of CDI-45205.

Norovirus Program

Norovirus is a highly contagious infection and is the most common cause of acute gastroenteritis, accounting for nearly one in five cases. According to the Centers for Disease Control and Prevention (CDC), an estimated 685 million cases and an estimated 200,000 deaths are attributed to norovirus each year worldwide, with an estimated societal cost of $60 billion.

- In August 2023 we announced our selection of the novel broad-spectrum 3CL protease inhibitor CDI-988 as our lead potential oral treatment for norovirus. CDI-988 is being evaluated in a first-in-human trial in healthy volunteers in Australia. The CDI-988 trial is expected to serve as a Phase 1 trial for both our norovirus and our coronavirus programs.

- In September 2023 we dosed the first subject in our dual norovirus-coronavirus oral CDI-988 Phase 1 trial.

Third Quarter Financial Results

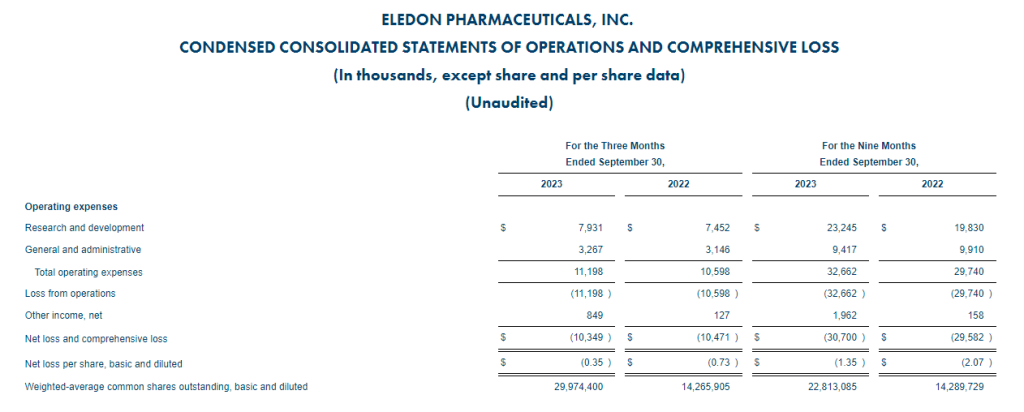

Research and development (R&D) expenses for the third quarter of 2023 were $4.2 million, compared with $3.9 million for the third quarter of 2022. The increase was primarily due to the influenza CC-42344 product candidate moving into a Phase 2a clinical trial and the ongoing Phase 1 clinical trial of CDI-988 for norovirus-coronavirus. General and administrative (G&A) expenses for the third quarters of 2023 and 2022 were relatively stable at $1.8 million.

During the third quarter of 2023, the Company received a $1.6 million refund from the registry of the court reflecting the recovery of funds following a successful appeal in the Company’s litigation with an insurer, which created a positive impact by reducing operating expenses by that amount.

Total other income, net for the third quarter of 2023 was $0.3 million, which was primarily related to interest earned on cash in bank accounts. This compared with minimal other expense, net for the third quarter of 2022.

The net loss for the third quarter of 2023 was $4.2 million, or $0.41 per share, compared with the net loss for the third quarter of 2022 of $5.7 million, or $0.70 per share.

Nine Month Financial Results

R&D expenses for the nine months ended September 30, 2023 were $10.9 million, compared with $9.1 million for the nine months ended September 30, 2022, with the increase primarily due to clinical advancement of our Influenza A and norovirus-coronavirus programs. G&A expenses for the first nine months of 2023 were $4.6 million, compared with $4.5 million for the first nine months of 2022.

During the first nine months of 2023, the Company received a $1.6 million refund from the registry of the court, as noted above. The Company obtained a summary judgment during the second quarter of 2022 and accounted for a potential $1.6 million adverse award by expensing the same amount during the first nine months of 2022.

During the first nine months of 2022, the Company recorded a $19.1 million non-cash goodwill impairment. There was no comparable impairment charge during the first nine months of 2023.

Total other income, net for the first nine months of 2023 was $0.4 million, compared with minimal other expense, net for the first nine months of 2022.

The net loss for the nine months ended September 30, 2023 was $13.5 million, or $1.43 per share. The net loss for the nine months ended September 30, 2022 was $34.3 million, or $4.23 per share, and reflected the litigation expense and non-cash impairment charge described above.

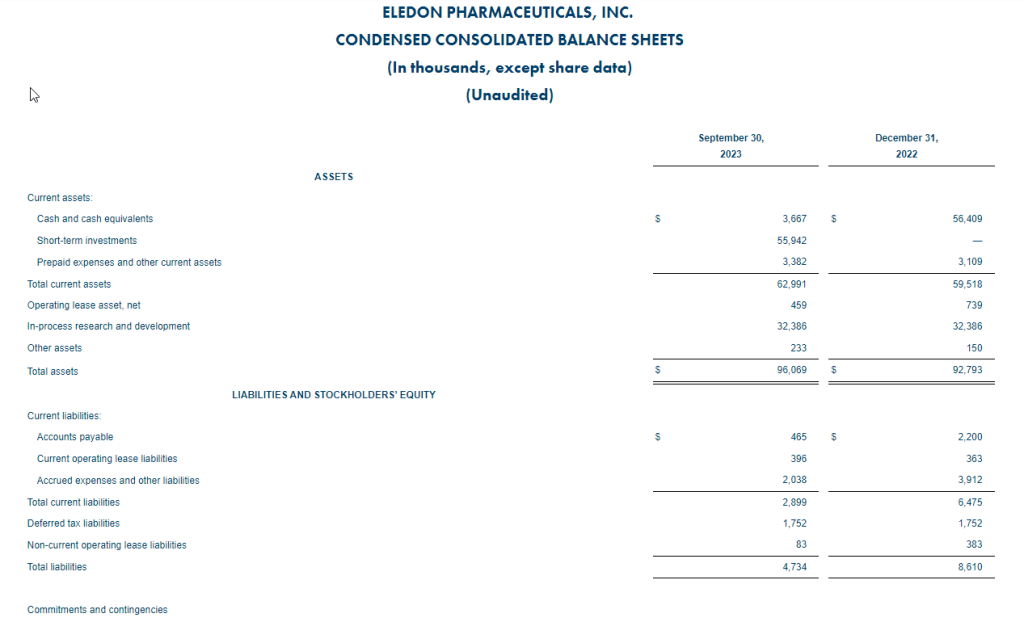

Cocrystal reported unrestricted cash as of September 30, 2023 of $29.7 million, compared with $37.1 million as of December 31, 2022. Net cash used in operating activities for the first nine months of 2023 was $11.3 million, compared to $16.5 million for the first nine months of 2022. The Company had working capital of $30.3 million and 10.2 million common shares outstanding as of September 30, 2023.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), noroviruses and hepatitis C viruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Cautionary Note Regarding Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our plans for the future development of preclinical and clinical drug candidates, our expectations regarding future characteristics of the product candidates we develop, the expected time of achieving certain value-driving milestones in our programs, including, preparation, commencement and advancement of clinical studies for certain product candidates in 2023 and beyond, the viability and efficacy of potential treatments for diseases our product candidates are designed to treat, expectations for the markets for certain therapeutics, our ability to execute our clinical and regulatory goals and deploy regulatory guidance towards future studies, the expected sufficiency of our cash balance to advance our programs and fund our planned operations, and our liquidity. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from interest rate increases in response to inflation, uncertainty in the financial markets, the possibility of a recession and geopolitical conflict in Ukraine and Israel on our Company, our collaboration partners, and on the U.S., UK, Australia and global economies, including manufacturing and research delays arising from raw materials and labor shortages, supply chain disruptions and other business interruptions on our ability to proceed with studies as well as similar problems with our vendors and our current and any future clinical research organization (CROs) and contract manufacturing organizations (CMOs), the ability of our CROs to recruit volunteers for, and to proceed with, clinical studies, our reliance on Merck for further development in the influenza A/B program under the license and collaboration agreement, our and our collaboration partners’ technology and software performing as expected, financial difficulties experienced by certain partners, the results of any current and future preclinical and clinical trials, general risks arising from clinical trials, receipt of regulatory approvals, regulatory changes, development of effective treatments and/or vaccines by competitors, including as part of the programs financed by the U.S. government, potential mutations in a virus we are targeting that may result in variants that are resistant to a product candidate we develop, and the outcome of the ongoing litigation with the insurance company. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2022. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Investor Contact:

LHA Investor Relations

Jody Cain

310-691-7100

jcain@lhai.com

Media Contact:

JQA Partners

Jules Abraham

917-885-7378

Jabraham@jqapartners.com

Financial Tables to follow

COCRYSTAL PHARMA, INC.

CONSOLIDATED BALANCE SHEETS

(in thousands)

| September 30, 2023 | December 31, 2022 | |||||||

| (unaudited) | ||||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash | $ | 29,738 | $ | 37,144 | ||||

| Restricted cash | 75 | 75 | ||||||

| Tax credit receivable | 550 | 716 | ||||||

| Prepaid expenses and other current assets | 1,842 | 2,243 | ||||||

| Total current assets | 32,205 | 40,178 | ||||||

| Property and equipment, net | 252 | 342 | ||||||

| Deposits | 46 | 46 | ||||||

| Operating lease right-of-use assets, net (including $57 and $99 respectively, to related party) | 111 | 274 | ||||||

| Total assets | $ | 32,614 | $ | 40,840 | ||||

| Liabilities and stockholders’ equity | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued expenses | $ | 1,806 | $ | 976 | ||||

| Current maturities of finance lease liabilities | – | 7 | ||||||

| Current maturities of operating lease liabilities (including $57 and $59 respectively, to related party) | 118 | 233 | ||||||

| Total current liabilities | 1,924 | 1,216 | ||||||

| Long-term liabilities: | ||||||||

| Operating lease liabilities (including $0 and $42 respectively, to related party) | – | 57 | ||||||

| Total liabilities | 1,924 | 1,273 | ||||||

| Commitments and contingencies | ||||||||

| Stockholders’ equity: | ||||||||

| Common stock, $0.001 par value 150,000 shares authorized as of September 30, 2023, and December 31, 2022; 10,174 and 8,143 shares issued and outstanding as of September 30, 2023 and December 31, 2022 | 10 | 8 | ||||||

| Additional paid-in capital | 342,130 | 337,489 | ||||||

| Accumulated deficit | (311,450 | ) | (297,930 | ) | ||||

| Total stockholders’ equity | 30,690 | 39,567 | ||||||

| Total liabilities and stockholders’ equity | $ | 32,614 | $ | 40,840 | ||||

COCRYSTAL PHARMA, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

(in thousands, except per share data)

| Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| Operating expenses: | ||||||||||||||||

| Research and development | 4,194 | 3,872 | 10,902 | 9,105 | ||||||||||||

| General and administrative | 1,849 | 1,822 | 4,591 | 4,530 | ||||||||||||

| Legal settlement | (1,600 | ) | – | (1,600 | ) | 1,600 | ||||||||||

| Impairments | – | – | – | 19,092 | ||||||||||||

| Total operating expenses | 4,443 | 5,694 | 13,893 | 34,327 | ||||||||||||

| Loss from operations | (4,443 | ) | (5,694 | ) | (13,893 | ) | (34,327 | ) | ||||||||

| Other income (expense): | ||||||||||||||||

| Interest income (expense), net | 320 | (1 | ) | 460 | (2 | ) | ||||||||||

| Foreign exchange loss | (42 | ) | (5 | ) | (87 | ) | (19 | ) | ||||||||

| Change in fair value of derivative liabilities | – | – | – | 12 | ||||||||||||

| Total other income (expense), net | 278 | (6 | ) | 373 | (9 | ) | ||||||||||

| Net loss | $ | (4,165 | ) | $ | (5,700 | ) | (13,520 | ) | (34,336 | ) | ||||||

| Net loss per common share, basic and diluted | $ | (0.41 | ) | $ | (0.70 | ) | (1.43 | ) | (4.23 | ) | ||||||

| Weighted average number of common shares, | 10,153 | 8,143 | 9,461 | 8,143 | ||||||||||||

| basic and diluted | ||||||||||||||||

# # #

Source: Cocrystal Pharma, Inc.

Released November 13, 2023