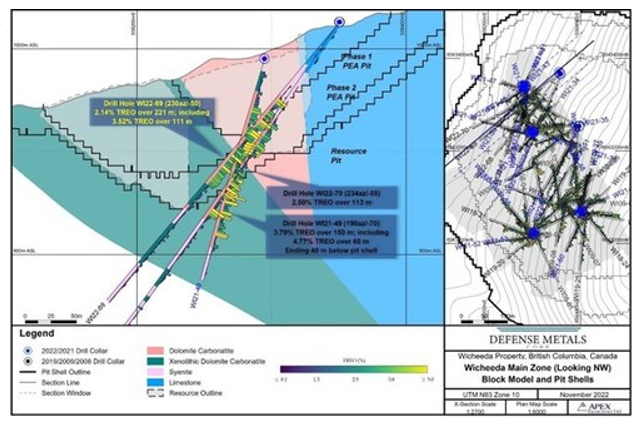

VANCOUVER, BC, Nov. 15, 2022 /PRNewswire/ – Defense Metals Corp. (“Defense Metals” or the “Company“; (TSX-V: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce additional partial Rare Earth Element (“REE“) assay results from one additional core hole, totalling 353 metres (m), collared within the northern area of Defense Metals’ 100% owned Wicheeda REE Deposit.

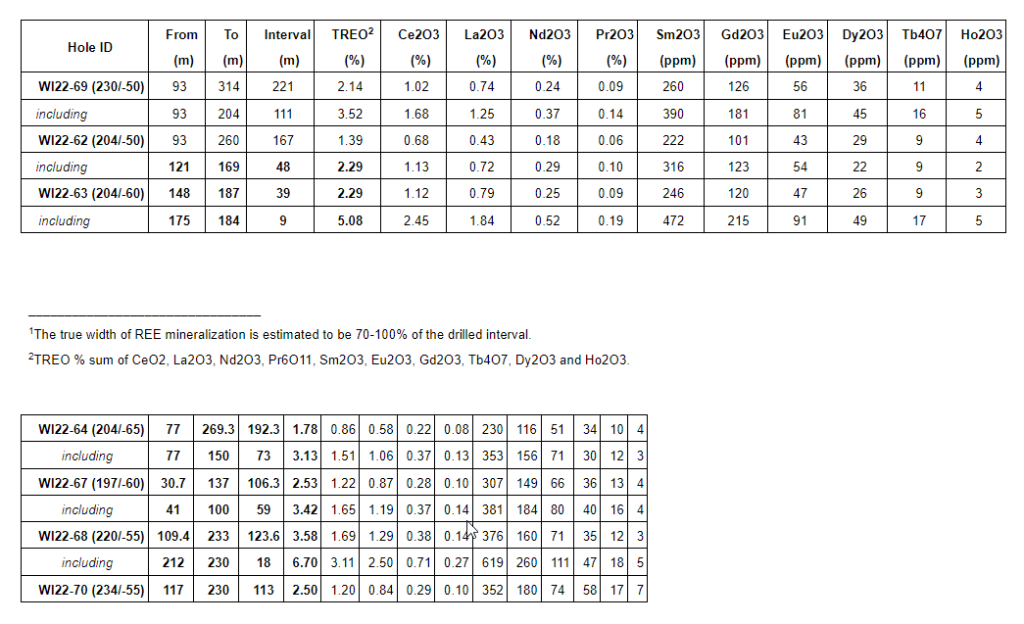

Infill drill hole WI22-69 (-50o dip / 230o azimuth) was drilled southwest within the northern area of the deposit intersected a broad zone of mineralized dolomite carbonatite averaging 2.14% total rare earth oxide (“TREO”) over 221 metres (m)1; including a higher-grade interval averaging 3.52% TREO over 111 m (Figure 1).

With over 5,500 m of drilling in 18 holes now complete as part of the 2022 Wicheeda resource delineation and pit geotechnical program, the Company has released assays for a total of 2,493 m in 7 holes. Assays for the remaining 11 holes totalling 3,017 m are expected in the coming weeks and months.

Luisa Moreno, President, and Director of Defense Metals stated: “With these additional assay results our 2022 drilling continues to yield significant intervals of the high-grade REE dolomite carbonatite (DC) lithology. Recent flotation variability testwork has shown this type of mineralization consistently delivers high grade mineral concentrates greater than 40% TREO, at recoveries in excess of 80% (see Defense Metals news release dated October 17, 2022). All the drill holes released to date have included significant REE mineralized DC intervals. As such Defense Metals is confident the 2022 drilling results will contribute positively to the planned Preliminary Feasibility Study (PFS).”

The 100% owned 4,244 hectare Wicheeda REE Property, located approximately 80 km northeast of the city of Prince George, British Columbia, is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, the CN railway, and major highways.

The Wicheeda REE Project yielded a robust 2021 preliminary economic assessment technical report (PEA) that demonstrated an after-tax net present value (NPV@8%) of $517 million, and 18% IRR3. A unique advantage of the Wicheeda REE Project is the production of a saleable high-grade flotation-concentrate. The PEA contemplates a 1.8 Mtpa (million tonnes per year) mill throughput open pit mining operation with 1.75:1 (waste:mill feed) strip ratio over a 19 year mine (project) life producing and average of 25,423 tonnes REO annually. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

Methodology and QA/QC

The analytical work reported on herein was performed by ALS Canada Ltd. (ALS) at Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (QA/QC) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (BC) Principal and Consultant of APEX Geoscience Ltd. of Edmonton, AB, a director of Defense Metals and a “Qualified Person” as defined in NI 43-101. Mr. Raffle verified the data disclosed which includes a review of the sampling, analytical and test data underlying the information and opinions contained therein.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

____________________________

3 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, drill results including anticipated timeline of such results/assays, the Company’s plan to commence the PFS, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

Conference Call Tuesday November 15, 2022 at 11:00 AM (EST)

(All $ figures reported in USD)

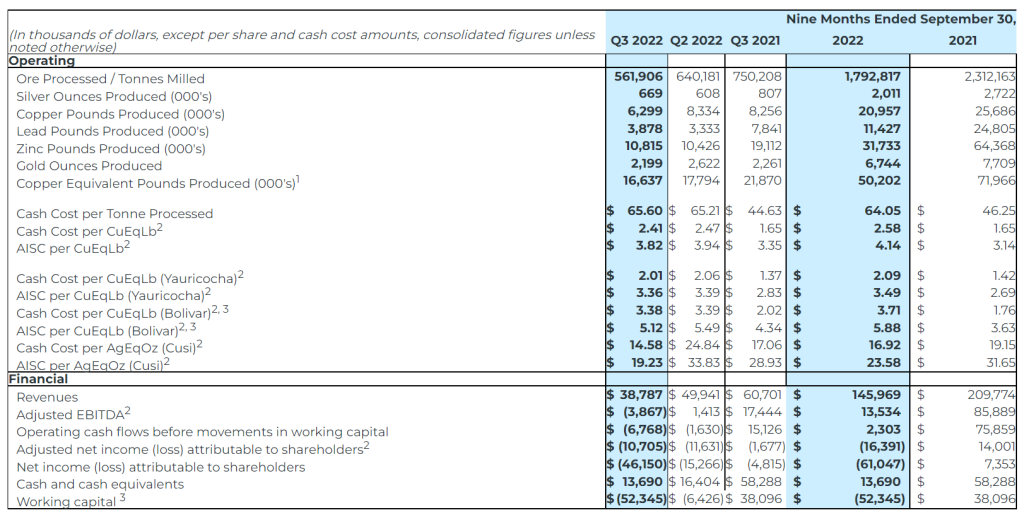

Revenue from metals payable of $38.8 million in Q3 2022, a 36% decrease from $60.7 million in Q3 2021 and a 22% decrease from the previous quarter, due to lower throughput at Yauricocha and slower ramp up at Bolivar as a result of a flooding event and operational restrictions due to limited ventilation in the Bolivar NorthWest zone.

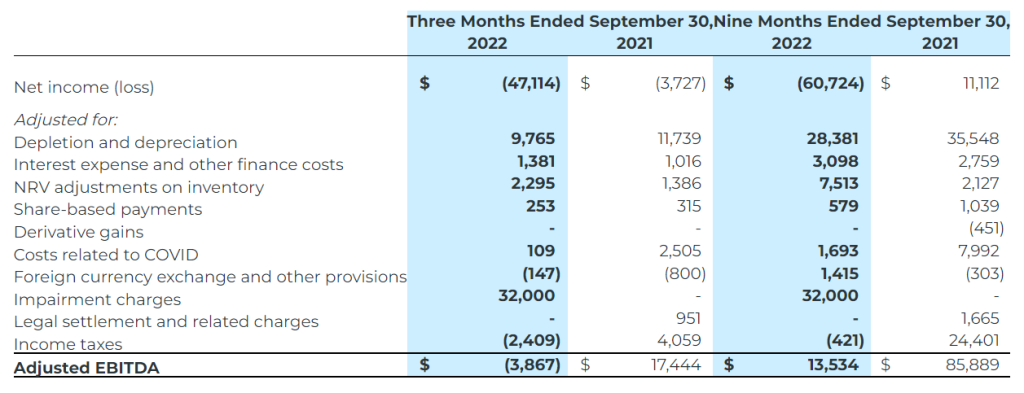

Adjusted EBITDA of $(3.9) million in Q3 2022, compared to $17.4 million in Q3 2021 and $1.4 million in Q2 2022.

Net loss attributable to shareholders for Q3 2022 of $46.2 million, or $(0.28) per share (basic and diluted), compared to a net loss of $4.8 million, or ($0.03) per share in Q3 2021, and a net loss of $15.3 million or $(0.09) per share in Q2 2022.

Net loss for Q3 2022 and 9M 2022 includes an impairment charge of $25.0 million ($nil for Q3 2021 and 9M 2021) for the Bolivar mine and $7.0 million ($nil for Q3 2021 and 9M 2021) for the Cusi mine.

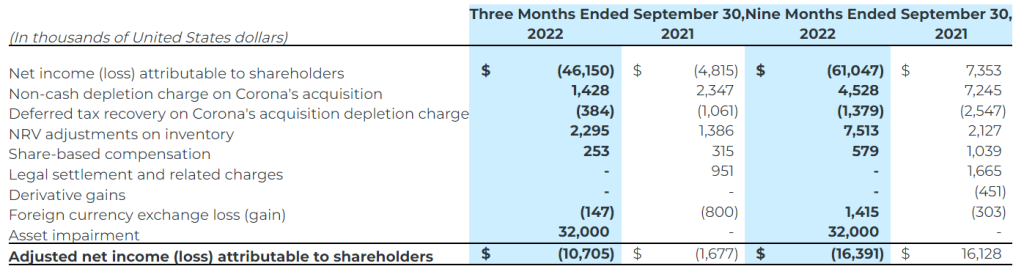

Adjusted net loss attributable to shareholders(1) of $10.7 million, or $(0.07) per share for Q3 2022, compared to adjusted net loss of $1.7 million or $(0.01) per share for Q3 2021 and an adjusted net loss of $11.6 million, or $0.07 per share for Q2 2022.

$13.7 million of cash and cash equivalents and working capital of $(52.3) million1 as at September 30, 2022.

Net Debt of $73.6 million as at September 30, 2022.

Suspension of production and financial guidance remains in effect.

1 The negative working capital is largely due to the reclassification of the long-term portion of the credit facility as current, resulting from the breach of certain debt covenants as at September 30, 2022. The Company is seeking accommodation from the lending banks in the form of waivers for this non-compliance.

A shareholder conference call will be held Tuesday, November 15, 2022, at 11:00 AM (EST). Click here to register.

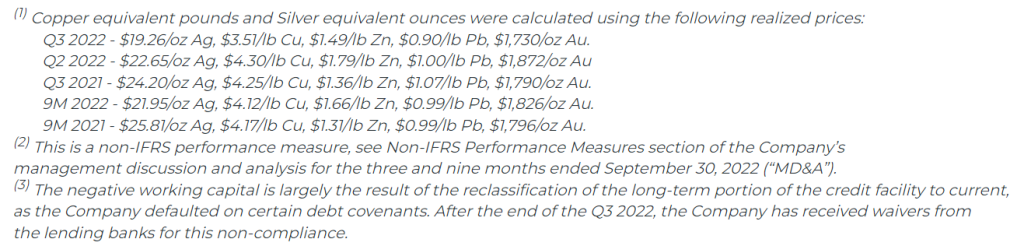

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (BVL or Bolsa de Valores de Lima: SMT) (NYSE AMERICAN: SMTS) (“Sierra Metals” or “the Company”) today reported revenue of $38.8 million, a 36% decline from Q3 2021 and a 22% decline from Q2 2022, and adjusted EBITDA of $(3.9) million, a 122% decrease from Q3 2021 and a 379% decrease from Q2 2022 on throughput of 561,906 tonnes and metal production of 16.6 million copper equivalent pounds for the three-month period ended September 30, 2022.

Luis Marchese, CEO of Sierra Metals, commented, “the unexpected events during our latest quarter have made for another challenging period at Sierra Metals.

We have all been deeply impacted by the tragic mudslide incident at Yauricocha. As our primary objective remains the safety and well-being of all employees and contractors, a rigorous safety assurance process continues at the mine. Although production is ramping up, full production can only be reached once this process is complete.

In the coming months, we will continue to incorporate ore from the high-grade Fortuna zone and work towards recovery of tonnage at the Yauricocha Mine. In addition, exploration efforts will continue, both inside the mine for near term reach and in brownfield locations in close proximity to operations, in order to generate new exploration targets.”

He continued, “at Bolivar, unexpected flooding during most of the quarter in addition to the operational restrictions due to limited ventilation at the Bolivar NorthWest zone, negatively impacted throughput and grades.

On a consolidated basis, the Company’s revenues and EBITDA decreased 36% and 122%, respectively due to a 24% decrease in copper equivalent production when compared to the same quarter last year, coupled with a reduction in all metals prices, except zinc.”

He concluded, “Recent setbacks at both the Yauricocha and Bolivar Mines have prevented us from achieving full production and our turnaround goals within the initially proposed timeline, leading to suspended 2022 operating guidance. These unexpected challenges have culminated in the liquidity issues facing the Company. The Special Committee of our Board diligently continues its strategic review process. In the meantime, we remain disciplined in our approach to day-to-day operations.”

The following table displays selected financial and operational information for the three months and nine months ended September 30, 2022 compared to the corresponding periods for 2021 and the three months ended June 30, 2022:

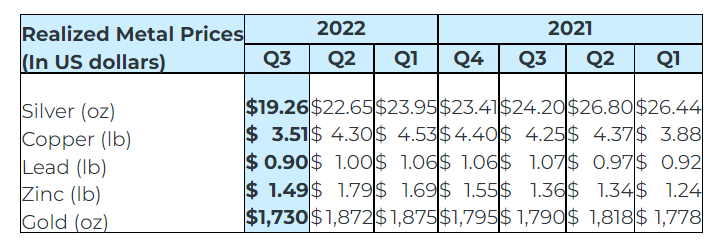

The following table shows the Company’s realized selling prices for the three months ended September 30, 2022, and each of the last six quarters:

Q3 2022 Consolidated Operating Highlights

Copper equivalent production of 16.6 million pounds; a 24% decrease from Q3 2021 and a 7% decrease from Q2 2022.

Consolidated Q3 2022 throughput of 561,906 tonnes was a 25% decrease over the Q3 2021 throughput of 750,208 tonnes. As compared to Q2 2022, consolidated throughput was 12% lower for Q3 2022.

Throughput from the Yauricocha Mine during Q3 2022 was 269,057 tonnes, a 17% decline when compared to Q3 2021 due to the suspension of mining activity and work stoppages during the quarter, which resulted in a 31% decrease in copper equivalent pounds produced. Declining grades due to restricted access to non-permitted areas of the mine also affected production. When compared to the previous quarter, throughput declined by 15%.

At the Bolivar Mine, throughput was 227,669 tonnes during Q3 2022. When compared to Q3 2021, throughput at Bolivar was 38% lower and while grades were higher for silver and gold, they were not enough to offset the lower throughput, resulting in a 16% decrease in copper equivalent pounds produced. Operational ramp up has been slower than expected due to unforeseen flooding in the Bolivar NorthWest zone during the quarter. When compared to Q2 2022, an 11% decrease in throughput, along with lower grades in copper and silver, resulted in a 10% decrease in copper equivalent pound production.

At Cusi, throughput was 65,180 tonnes during Q3 2022. When compared to Q3 2021, a 7% increase in throughput, combined with higher head grades for all metals except lead, resulted in a 22% increase in silver equivalent ounces production. Cusi suffered from an unexpected flooding event that restricted access to the lower areas of the mine during the second quarter. At the beginning of Q3, access to the lower levels of the mine was still limited. While throughput was 2% lower, it was offset by higher grades in all metals, resulting in a 32% increase in silver equivalent ounces produced.

Q3 2022 Consolidated Financial Highlights

Revenues Declined Due to Decrease in Metal Sales and a Drop in Metals Prices

Revenue from metals payable of $38.8 million in Q3 2022 or a decrease of 36% over the revenue of $60.7 million in Q3 2021 due to the decrease in metal sales and the drop in average realized prices for all metals, except zinc, as compared to Q3 2021.

Revenues for Q3 2022 were 22% lower than the revenue of $49.9 million in Q2 2022, as lower production from the Yauricocha and Bolivar Mines impacted metal sales quantities. The average realized prices for Q3 2022 decreased for copper (18%), zinc (17%), lead (10%), silver (15%) and gold (8%) as compared to the same during Q2 2022.

Cost of Operations Increased at Yauricocha and Bolivar Due to Lower Throughput

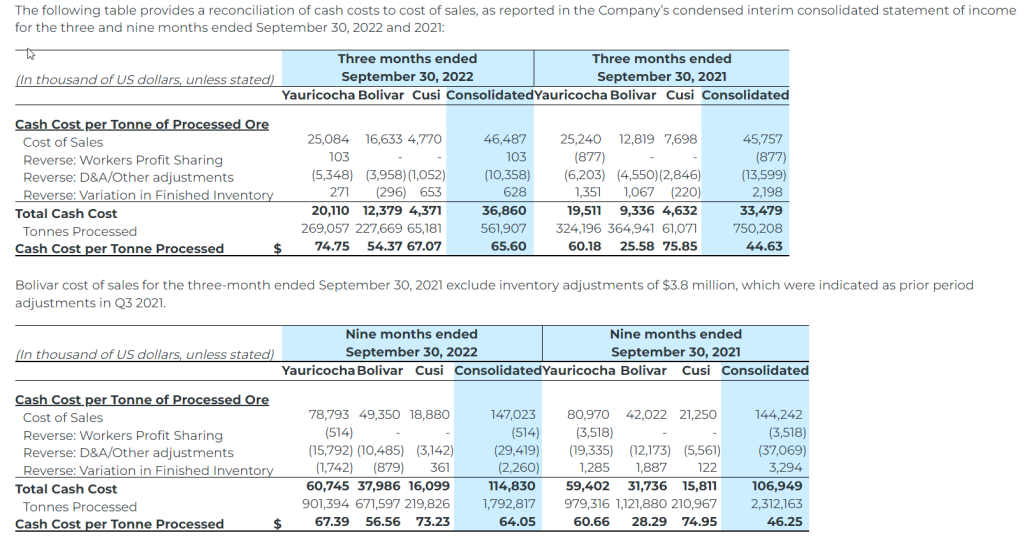

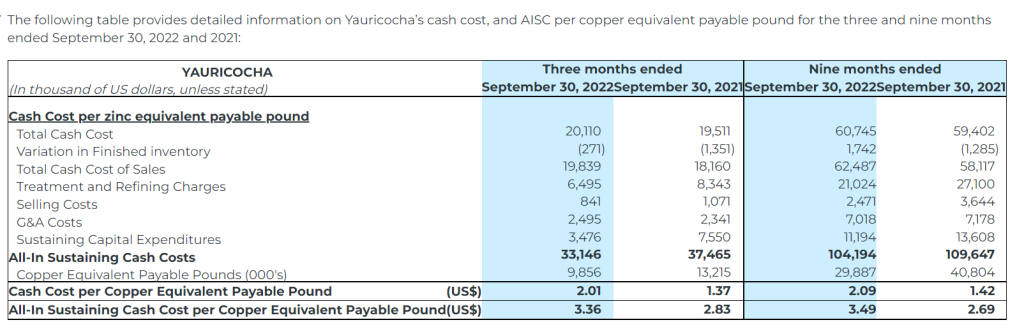

Yauricocha’s cash cost per copper equivalent payable pound was $2.01 (Q3 2021 – $1.37), and AISC (as defined herein) per copper equivalent payable pound of $3.36 (Q3 2021 – $2.83) for Q3 2022. The increase in cash costs and AISC was mainly a result of the 25% decrease in copper equivalent payable pounds as compared to Q3 2021. Despite 14% fewer copper equivalent payable pounds in Q3 2022 as compared to Q2 2022, cash cost and AISC per copper equivalent pound decreased from $2.06 and $3.39 respectively in Q2 2022, due to lower cost of sales and sustaining costs.

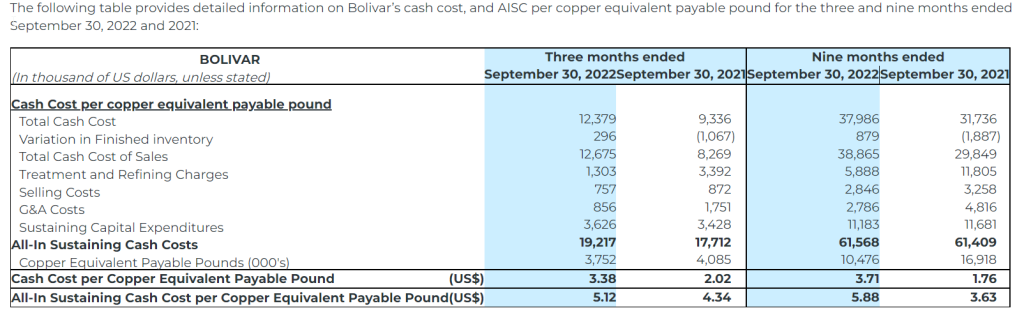

Bolivar’s cash cost per copper equivalent payable pound was $3.38 (Q3 2021 – $2.02), and AISC per copper equivalent payable pound was $5.12 (Q3 2021 – $4.34) for Q3 2022 due to higher operating costs per tonne and an 8% decrease in the copper equivalent payable pounds compared to Q3 2021. Bolivar’s Q3 2022 cash cost and AISC per copper equivalent pound decreased however from $3.39 and $5.49 respectively in Q2 2022.

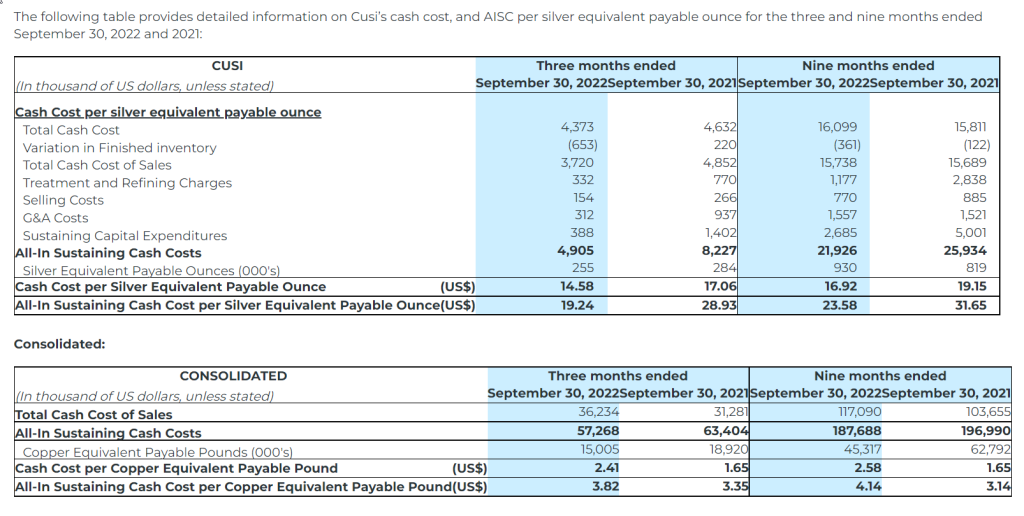

Cusi’s Q3 2022 cash cost per silver equivalent payable ounce decreased to $14.58 from $17.06 in Q3 2021 as a result of higher grades. AISC per silver equivalent payable ounce decreased to $19.23 (Q3 2021 – $28.93). Unit costs decreased during Q3 2022, despite fewer silver equivalent payable ounces, as a result of lower operating costs per tonne and lower sustaining costs during Q3 2022 as compared to Q3 2021.

EBITDA, Net Income and Cash Flow Generation Impacted by Lower Revenues and Higher Operating Costs

Adjusted EBITDA(1) decreased 122% to $(3.9) million for Q3 2022 compared to $17.4 million in Q3 2021 and a 379% decrease compared to $1.4 million in the previous quarter. The decrease in EBITDA is related to drop in revenues attributable to lower production and higher operating costs during Q3 2022.

Net loss attributable to shareholders for Q3 2022 was $46.2 million or $(0.28) per share (basic and diluted), compared to net loss of $4.8 million or $(0.03) per share (basic and diluted) in Q3 2021 and net loss of $15.3 million or $(0.09) per share (basic and diluted) in Q2 2022.

Adjusted net loss attributable to shareholders(1) of $10.7 million, or $(0.07) per share for Q3 2022, compared to adjusted net loss of $1.7 million or $(0.01) per share for Q3 2021 and adjusted net loss of $11.6 million, or $0.0 per share for Q2 2022.

Operating cash flow before movements in working capital of $(6.8) million for Q3 2022 as compared to $15.1 million of cash generated from operating activities in Q3 2021 and $(1.6) million in Q2 2022. The decrease resulted from lower revenue and higher costs during the quarter.

Cash and cash equivalents of $13.7 million and working capital of $(52.3) million as at September 30, 2022 compared to $34.9 million and $17.3 million, respectively, at the end of 2021. The negative working capital is largely the result of the reclassification of the long-term portion of the credit facility to current, as the Company defaulted on certain debt covenants as of September 30, 2022. The Company is seeking accommodation from the lending banks in the form of waivers for this non-compliance. If the Company is unable to obtain such waivers for the current and any potential future breaches of its debt covenants, it could materially and adversely affect the Company’s future operations, cash flows, earnings, results of operations, financial condition and the economic viability of its projects.

Cash and cash equivalents decreased during the nine-month period ended September 30, 2022 due to $31.2 million used in investing activities offset by $6.1 million of cash generated from operating activities and $3.8 million of cash generated from financing activities.

Financing activities included $25.0 million received from Banco de Credito del Peru (“BCP”) and Banco Santander by the Company’s subsidiary, Sociedad Minera Corona, to finance the repayment of the installments of $18.8 million on the original credit facility received from BCP.

1 This is a non-IFRS performance measure. See the Non-IFRS Performance Measures section of the MD&A.

Project Development

Mine development at Bolivar during Q3 2022 totaled 2,080 meters, which included 1,265 meters of development to prepare stopes for mine production, and 815 meters to development of ramps; and

Mine development at Cusi during Q3 2022 totaled 631 meters.

Exploration Update

Peru:

Approximately 2,532 meters of diamond drilling was completed during Q3 2022 in the Fortuna North, Katty and Violeta zones with the aim to replace and increase the depleted mineral resources. Additionally, approximately 2,000 meters of greenfield exploration drilling was completed in the Tucumachay prospect.

Mexico:

Bolivar

At Bolivar during Q3 2022, 18,318 meters were drilled in the Bolivar West, Bolivar NorthWest, the Cieneguita zones and El Gallo Superior encountering skarn intersections with mineralization. Additionally, infill drilling of 4,479 meters was completed in the Bolivar West, El Gallo Inferior and Bolivar NorthWest zones;

Cusi

During Q3 2022, the Company completed 2,196 meters of infill drilling to support the development of the Santa Rosa de Lima vein and NE Trend.

Covid-19 Update And Outlook

The COVID-19 pandemic has impacted the Company’s operations over the past two years. While there are still concerns regarding the newer variants of the virus, there is reduced pressure on the operations due to relaxed measures as the Company has achieved almost 100% vaccination rate for its employees at all locations. The additional costs related to COVID dropped to $1.7 million during the nine-month period ended September 30, 2022 as compared to $8.0 million spent during the comparative nine-month period of 2021.

Impairment Charge

Lower market capitalization due to the drop in the Company’s share price, declining metal prices, lower production and consequent decrease in profitability were considered as indicators of impairment as on September 30, 2022. The Company performed an impairment analysis for each of its cash generating units (“CGU”) using Life of Mine (“LOM”), which incorporate current operational practices, long term metal prices based on recent analyst consensus and productivity assumptions, based on recent operating experience at the mines.

The Company updated the Bolivar LOM using updated information from the mine performance, required capex, metal prices and discount rate, and concluded that an impairment of $25.0 million was required for the Bolivar CGU.

The Cusi LOM was updated for the latest metal prices and discount rate. Following this analysis, management concluded that an impairment of $7.0 million was needed for the Cusi CGU as on September 30, 2022.

The updated Yauricocha LOM did not indicate any impairment as at September 30, 2022.

Suspended Guidance

In addition to the delays in the anticipated turnaround at the Bolivar mine due to the unexpected flooding in the Bolivar NW zone during the quarter, the Company also experienced production delays at the Yauricocha mine as a result of the mudslide incident and ensuing community blockade in September. Although mining restarted in parts of Yauricocha in October, the Company is following due assurance processes to ensure safe operations in the remaining sections of the mine. In view of these delays, the Company has suspended its production and financial guidance for 2022.

Strategic Review Process

In response to liquidity challenges from an accumulation of operational losses and negative cashflows, primarily from its Mexican operations, the Company announced, on October 18, 2022, the formation of a Special Committee and the initiation of a strategic review process.

The mandate of the Special Committee, comprised of its independent directors, includes exploring, reviewing and considering options to optimize the operations of the Company and possible financing, restructuring and strategic options in the best interests of the Company. Financial and legal advisors with particular expertise in turnaround and restructuring matters have been engaged to advise on this process.

The Company has engaged CIBC Capital Markets as a financial advisor in this process.

Delisting

As previously announced, the Company will voluntarily delist its common shares from the New York Stock Exchange American (“NYSE”) and the Bolsa de Valores de Lima (“BVL”). The final day of trading on the NYSE was today, November 14, 2022 with shares to be suspended from trading before market open on November 15, 2022.

The Company is continuing to pursue its BVL delisting and suspension from trading is anticipated later during the year. An update will be provided once a final trading date of the common shares on the BVL has been confirmed.

The Company’s common shares will continue to be listed and traded in Canadian dollars on the Toronto Stock Exchange.

Conference Call and Webcast

Sierra Metals’ senior management will host a conference call on Tuesday, November 15, 2022, at 11:00 AM (EDT) to discuss the Company’s financial and operating results for the three months ended September 30, 2022.

Via Webcast:

A live audio webcast of the meeting will be available on the Company’s website:

The webcast, along with presentation slides, will be archived for 180 days on www.sierrametals.com.

Via phone:

For those who prefer to listen by phone, dial-in instructions are below. To ensure your participation, please call approximately five minutes prior to the scheduled start time of the call.

Canada dial-in number (Toll Free): 1 833 950 0062 Canada dial-in number (Local): 1 226 828 7575 US dial-in number (Toll Free): 1 844 200 6205 US dial-in number (Local): 1 646 904 5544 All other locations: +1 929 526 1599

Access code: 991150

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance

Non-IFRS Performance Measures

The non-IFRS performance measures presented do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be directly comparable to similar measures presented by other issuers.

Non-IFRS reconciliation of adjusted EBITDA

EBITDA is a non-IFRS measure that represents an indication of the Company’s continuing capacity to generate earnings from operations before taking into account management’s financing decisions and costs of consuming capital assets, which vary according to their vintage, technological currency, and management’s estimate of their useful life. EBITDA comprises revenue less operating expenses before interest expense (income), property, plant and equipment amortization and depletion, and income taxes. Adjusted EBITDA has been included in this document. Under IFRS, entities must reflect in compensation expense the cost of share-based payments. In the Company’s circumstances, share-based payments involve a significant accrual of amounts that will not be settled in cash but are settled by the issuance of shares in exchange for cash. As such, the Company has made an entity specific adjustment to EBITDA for these expenses. The Company has also made an entity-specific adjustment to the foreign currency exchange (gain)/loss. The Company considers cash flow before movements in working capital to be the IFRS performance measure that is most closely comparable to adjusted EBITDA.

The following table provides a reconciliation of adjusted EBITDA to the condensed interim consolidated financial statements for the three and nine months ended September 30, 2022 and 2021:

Non-IFRS reconciliation of adjusted net income

The Company has included the non-IFRS financial performance measure of adjusted net income, defined by management as the net income attributable to shareholders shown in the statement of earnings plus the non-cash depletion charge due to the acquisition of Corona and the corresponding deferred tax recovery and certain non-recurring or non-cash items such as share-based compensation and foreign currency exchange (gains) losses. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors may want to use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS.

The following table provides a reconciliation of adjusted net income to the condensed interim consolidated financial statements for the three and nine months ended September 30, 2022 and 2021:

Cash cost per silver equivalent payable ounce and copper equivalent payable pound

The Company uses the non-IFRS measure of cash cost per silver equivalent ounce and copper equivalent payable pound to manage and evaluate operating performance. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

All-in sustaining cost per silver equivalent payable ounce and copper equivalent payable pound

All‐In Sustaining Cost (“AISC”) is a non‐IFRS measure and was calculated based on guidance provided by the World Gold Council (“WGC”) in June 2013. WGC is not a regulatory industry organization and does not have the authority to develop accounting standards for disclosure requirements. Other mining companies may calculate AISC differently as a result of differences in underlying accounting principles and policies applied, as well as differences in definitions of sustaining versus development capital expenditures.

AISC is a more comprehensive measure than cash cost per ounce/pound for the Company’s consolidated operating performance by providing greater visibility, comparability and representation of the total costs associated with producing silver and copper from its current operations.

The Company defines sustaining capital expenditures as, “costs incurred to sustain and maintain existing assets at current productive capacity and constant planned levels of productive output without resulting in an increase in the life of assets, future earnings, or improvements in recovery or grade. Sustaining capital includes costs required to improve/enhance assets to minimum standards for reliability, environmental or safety requirements. Sustaining capital expenditures excludes all expenditures at the Company’s new projects and certain expenditures at current operations which are deemed expansionary in nature.”

Consolidated AISC includes total production cash costs incurred at the Company’s mining operations, including treatment and refining charges and selling costs, which forms the basis of the Company’s total cash costs. Additionally, the Company includes sustaining capital expenditures and corporate general and administrative expenses. AISC by mine does not include certain corporate and non‐cash items such as general and administrative expense and share-based payments. The Company believes that this measure represents the total sustainable costs of producing silver and copper from current operations and provides the Company and other stakeholders of the Company with additional information of the Company’s operational performance and ability to generate cash flows. As the measure seeks to reflect the full cost of silver and copper production from current operations, new project capital and expansionary capital at current operations are not included. Certain other cash expenditures, including tax payments, dividends and financing costs are also not included.

Additional non-IFRS measures

The Company uses other financial measures, the presentation of which is not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. This includes:

Operating cash flows before movements in working capital – excludes the movement from period-to-period in working capital items including trade and other receivables, prepaid expenses, deposits, inventories, trade and other payables and the effects of foreign exchange rates on these items.

This term does not have a standardized meaning prescribed by IFRS, and therefore the Company’s definition is unlikely to be comparable to similar measures presented by other companies. The Company’s management believes that their presentation provides useful information to investors because cash flows generated from operations before changes in working capital excludes the movement in working capital items. This, in management’s view, provides useful information of the Company’s cash flows from operations and is considered to be meaningful in evaluating the Company’s past financial performance or its future prospects. The most comparable IFRS measure is cash flows from operating activities.

Qualified Persons

Américo Zuzunaga, FAusIMM (Mining Engineer) Vice President, Technical is a Qualified Person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company with Green Metal exposure including increasing copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. Sierra Metals has recently had several new key discoveries and still has many more exciting brownfield exploration opportunities at all three Mines in Peru and Mexico that are within close proximity to the existing mines. Additionally, the Company also has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com.

This press release contains forward-looking information within the meaning of Canadian and United States securities legislation, including with respect to timing of the conference call, exploration and production plans and the delisting of the Company’s common shares. Forward-looking information relates to future events or the anticipated performance of Sierra and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra to be materially different from any anticipated performance expressed or implied by such forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 16, 2022 for its fiscal year ended December 31, 2021 and other risks identified in the Company’s filings with Canadian securities regulators and the United States Securities and Exchange Commission, which filings are available at www.sedar.com and www.sec.gov, respectively.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations, and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

Schwazze (OTCQX:SHWZ, NEO:SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Results. Revenue was $43.2 million, up 36% y-o-y from $31.8 million. Adjusted EBITDA was $15.9 million, or 36.7% of revenue in the quarter, up from $8.8 million, or 26.7%, a year ago. Schwazze reported operating income of $11.1 million and net income of $25,124, or breakeven EPS, versus $3.8 million, $968,756 and $0.02 last year.

Quarterly Drivers. The most influential factor driving revenue increases in the third quarter 2022 was the inclusion of four consummated acquisitions in Colorado and revenue from R. Greenleaf. Revenue from wholesale sales decreased, due in large part to continued pricing pressure in the Colorado wholesale market as a result of supply saturation in flower and bulk distillate products.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

We currently own a modern fleet of five tankers engaged in seaborne transportation of refined petroleum products and other bulk liquids. We are focused on growing our fleet of medium range product tankers, which provide operational flexibility and enhanced earnings potential due to their “eco” features and modifications. We are positioned to opportunistically expand and maximize our fleet due to competitive cost structure, strong customer relationships and an experienced management team whose interests are aligned with those of its shareholders. For more information, visit: http://www.pyxistankers.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Pyxis Tankers reported another quarter of impressive results due to higher tanker shipping rates. Pyxis reported net revenues of $17.0 million for the 2022-2Q, up from $7.0 million for the same period last year and in line with expectations. Higher revenues reflect a TCE rate of 29,062 versus 7,326. Higher revenues more than offset increased vessel operating costs, which were $5.0 million versus $3.6 million. The result was a boost to adjusted EBITDA to $8.0 million versus $(1.3) million. Net income available to common was $5.1 million ($0.42 per diluted share) versus a loss of $3.7 million ($0.39 per diluted share).

The near-term outlook remains favorable. The displacement of traditional shipping routes caused by the conflict in Ukraine has led to longer voyages at higher prices. This will most likely continue and may even accelerate as European countries replace Russian natural gas with oil and diesel. In addition, the Chinese government has now authorized the export of refined oil, which may lead to additional demand for tankers. Pyxis has committed three of its five vessels to short-term charters at rates above 30,000 while leaving the remaining two vessels to receive spot prices. Traditional, tanker shipping prices are strong in the winter heating season.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Financial Results Reported With Full Data. PDS Biotech reported a 3Q22 loss of $7.4 million or $(0.26) per share, with cash on September 30 of $71.6 million. PDS Management reviewed two presentations at last week’s Society for Immunotherapy of Cancer (SITC) meeting, providing additional information to the data published in the abstracts. These data continue to show improved efficacy for PDS0101 over current treatments.

Data From Two Studies Was Presented At SITC. As discussed in our Research Note on November 8, the response rate and patient survival for the Phase 2 IMMUNOCERV trial in cervical cancer exceeded the standard of care. Data presented from the Phase 2 Triple Therapy trial showed anti-tumor action by PDS0101, with increases in immune response markers against the tumors and decreases in markers of immune suppression.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company has proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation. Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in two Phase 1 dose-escalation and expansion studies. These trials are currently underway in the United States and China. Onconova’s product candidate rigosertib is being studied in an investigator-sponsored study program, including in a dose-escalation and expansion Phase 1/2a investigator-sponsored study with oral rigosertib in combination with nivolumab for patients with KRAS+ non-small cell lung cancer.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Showed Continued Progress In Ongoing Trials. Onconova announced a loss of $5.4 million or $(0.26) per quarter for 3Q22, ending the quarter with $42.6 million in cash. In addition to updates on its current clinical trials, the company announced its intentions to start a new Phase 1/2a trial testing narazaciclib in low-grade endometrioid endometrial cancer (LGEEC). This new trial is expected to begin in 1Q23 with first data announced in 4Q23.

New Trial Planned In Endometrial Cancer. The Phase 1/2a trial will test the combination of narazaciclib with letrozole (Femara, an aromatase inhibitor from Novartis) in recurrent low-grade endometrioid endometrial cancer (LGEEC). The trial will start with safety cohorts testing the combination, with a 200 mg dose of narazaciclib with the standard 2.5 mg dose of letrozole. This is the narazaciclib dose that is in its fifth cohort in the Phase 1 trial for solid tumors.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Proposed Equity Offering. Monday morning, FAT Brands announced an ATM sales agreement to raise a maximum $21.4 million through the sale of Class A common stock and/or the 8.25% Series B Cumulative Preferred. At Friday’s close, a full raise in common would add just under three million shares to the public float.

A Switch. The proposed ATM is a switch from the Class A equity offering floated by the Company just 10 days ago. That offering was tabled after the shares sold off some 17% over the weekend. Under the ATM, FAT can decline to sell shares if the shares cannot be sold at or above a price designated by the Company, which we believe is above $7.00 per share.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results rise on higher shipping rates and additional ships. Euroseas reported net revenues of $46 million for the quarter ended September 30, 2022 versus $23 million for the same period last year. Higher revenues reflect an increase in the TCE rate to $30,893 from $19,482 and the deployment of 18 vessels versus 14 last year. Results were a few million below our forecast as was adjusted net income of $20.9 million. The company continues to buck industry trends by holding the line on vessel costs per shipping day.

Euroseas is well protected from the recent sharp decline in shipping rates. Euroseas has locked in 99% of its shipping days for the rest of the year, 78% of 2023 shipping days, and 54% of 2024 shipping days. In fact it has even chartered three new builds to be delivered in 2023. Management indicated it is unlikely to lock in rates any time in the near future for the four ships to be delivered in 2024. While realized TCE rates will undoubtedly slip below $30,000 in upcoming quarters, the company will not face the sharp declines most other shippers will face.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Energy Fuel reached a definitive agreement to sell the Alta Mesa mill to enCore Energy for $120 million. Energy Fuels will receive $60 million in cash upon closing and $60 million in convertible debt bearing an 8% annual interest rate. The mill is one of 11 licensed uranium processing plants and has an operating capacity of 1.5 million pounds per year. UUUU acquired Alta Mesa in 2016 for $13.6 million.

Energy Fuel, which operates Alta Mesa on a standby basis, did not have plans to activate the plant in the near future. Energy Fuel retains three other processing mills including the White Mesa mill which is licensed to produce 8 million pounds of uranium per year. We believe the White Mesa mill is large enough to meet all of UUUU’s uranium production needs in addition to producing vanadium and rare earth elements.The Alta Mesa plant costs approximately $2 million annually to maintain.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Beasley Broadcast Group, Inc. owns and operates 61 stations (47 FM and 14 AM) in 15 large- and mid-size markets in the United States. Approximately 20 million consumers listen to the Company’s radio stations weekly over-the-air, online and on smartphones and tablets, and millions regularly engage with the Company’s brands and personalities through digital platforms such as Facebook, Twitter, text messaging, digital and web applications and email. The Overwatch League’s Houston Outlaws esports team is a wholly owned subsidiary. The Company also owns BeasleyXP, a national esports content hub, and AXLR-R8, a Rocket League Championship Series team, in its esports portfolio. For more information, please visit www.bbgi.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Favorable Q3 results. The company reported revenue of $63.8 million, slightly beating our estimate of $63.0 million and at the higher end of its previous guidance range. The revenues benefited from strong digital revenues, up 23%, offset by declines in national advertising. Adj. EBITDA of $7.2 million was slightly lower than our estimate of $7.8 million.

Digital traction. Digital revenue grew by 23.2% year-over-year and accounted for 16% of total revenue in Q3, an increase from 13% earlier in the year. Notably, Digital accounts for more than National advertising at 15% of total revenues. Additionally, digital margins grew from 14.4% in Q2 to 19.6% in Q3. Management reiterated its goal of digital revenue to account for 20% of total revenue in Q4.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Scion Asset Management and Michael Burry Report Third Quarter Holdings

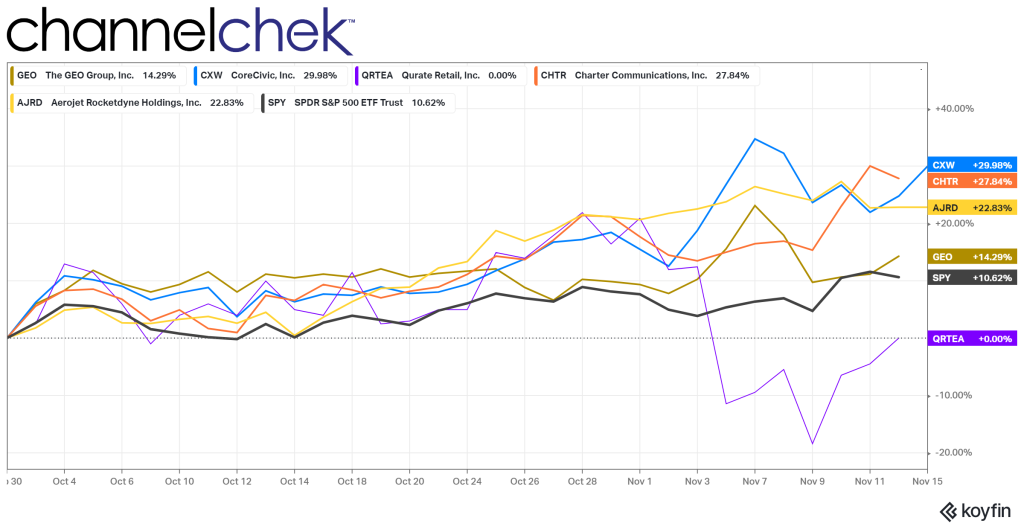

Four times a year, the quarter-end holdings of famous hedge fund manager Michael Burry become public through his firm’s required 13-F filing with the SEC. It’s newsworthy because people are interested in this iconic investor’s thinking. The list of 13-F securities is rarely more than a dozen positions and is just a one-day snapshot, but it can help one to understand his preferences and expectations.

The latest 13-F filing became public on Monday (November 14). It shows that he is not negative on all stocks, as he has built on his one position from the last reporting period, and added a few others. He clearly does not limit himself to only meg-cap companies. In fact two of his positions are small-cap stocks, one is a midcap, and one large cap.

Scion Asset Management’s Positions

His largest position is Geo Group (GEO) and represents 37.65% of the five. The shares represent 0.409% of GEO’s outstanding stock or 501,360 shares. The average price was listed as $6.42 per share.

The quarter-end market value of Scion’s GEO position was $3,309,000 consisting of 501,360 shares. This represents 0.4092% of the company. According to Scion’s Form ADV, filed on April 18, 2022, Scion had assets under management of $291,659,289. The GEO position is not likely a significant portion of his entire portfolio, but it represents more than a third of the firm’s 13F reportable securities.

Michael Burry first reported owning GEO Group during the fourth quarter of 2020. It’s a unique company, which may be positioned to take advantage of changes in the U.S. and internationally.

The GEO Group, based out of Boca Raton, FL, specializes in owning’ leasing, and managing secure confinement facilities, processing centers, and reentry facilities in the United States and globally. In addition to owning and operating secure and community facilities, GEO provides compliance technologies, monitoring services, and supervision and treatment programs for community-based parolees, probationers, and pretrial defendants.

For the year ended December 31, 2021, The GEO Group generated approximately 66% of its revenues from the U.S. Secure Services business, 24% from its GEO Care segment, and 10% of revenue from its International Services segment.

Gomes confirmed his earlier price target of $15.00 and reported solid operating results during the third quarter.

Scion’s third largest position is mentioned second because it also provides for correctional facilities and ancillary service, it is CoreCivic Inc. (CXW). CoreCivic is a private detention facility with three segments, CoreCivic Safety, CoreCivic Community, and CoreCivic Properties. It provides a broad range of solutions to governments with corrections and detention management, a growing network of residential reentry centers to help address America’s recidivism crisis, and government real estate solutions.

In his November 4 research report on CXW Joe Gomes pointed to the excess capacity of CXW, indicating that much of that could soon be utilized as covid restrictions loosen. Corecivic has ample excess capacity from which to add to their bottom line under improving conditions.

Burry’s second largest 13-F holding is Qurante Retail Group, Inc. (QRTEA). The company is involved in video online commerce and owns the well-known HSN (Home Shopping Network) and QVC shopping network. Its segments market and sell a wide variety of consumer products in the United States, primarily using its televised shopping programs and via the Internet through their websites and mobile applications; QVC International segment markets and sells a wide variety of consumer products in several foreign countries, primarily using its televised shopping programs and via the Internet through its international websites and mobile applications; and Zulily markets and sells a wide variety of consumer products in the United States and several foreign countries. Its geographical segments include the United States, Japan, Germany, and Other countries.

Aerojet Rocketdyne Holdings, Inc. (AJRD) is a midcap company that is Scion’s fourth largest holding. It designs, develops, manufactures, and sells aerospace and defense products and systems in the United States. It operates in two segments, Aerospace and Defense and Real Estate. The Aerospace and Defense segment offers aerospace and defense products and systems for the United States government, including the Department of Defense, the National Aeronautics and Space Administration, and aerospace and defense prime contractors. This segment provides liquid and solid rocket propulsion systems, air-breathing hypersonic engines, and electric power and propulsion systems for space, defense, civil, and commercial applications, and armament systems. The Real Estate segment engages in the re-zoning, entitlement, sale, and leasing of the company’s excess real estate assets. It owns 11,277 acres of land adjacent to the United States Highway 50 between Rancho Cordova and Folsom, California, east of Sacramento. The company was formerly known as GenCorp Inc. and changed its name to Aerojet Rocketdyne Holdings, Inc. in April 2015. Aerojet Rocketdyne Holdings, Inc. was incorporated in 1915 and is headquartered in El Segundo, California.

Burry’s smallest holding is the largest company. As the only large-cap stock of the five, Charter Communications, Inc. (CHTR) operates as a broadband connectivity and cable operator serving residential and commercial customers in the US. The company offers subscription-based video services, video on demand, high-def TV, DVR, and pay-per-view. It also has Web-based service management and sells local advertising across various platforms for networks, such as TBS, CNN, and ESPN to local sports and news channels.

Take Away

Michael Burry’s 13F filing for the third quarter showed two of his top three holdings are privately held correctional facilities that had relied on government contracts. The lifting of covid restrictions may help bolster future profits. Along with Aerojet, his fourth-largest position, GEO and Corecivic own real estate. Could this be part of Burry’s attraction?

The TV shopping channels owned by Qurante seem obscure, but the defense company Aerojet Rocketdyne should come as no surprise in a world that is moving more militarily and Space Force is gearing up.

If you have not already signed up to receive email from Channelchek with up-to-the-minute research reports on companies like GEO Group and Corecivic, along with insightful articles, sign-up here.

After 50 Years in the Dark, There May Be a Light at the End of the Tunnel for Psychedelics

Last week, voters in Colorado chose to decriminalize psychedelic use for residents over the age of 21, becoming the second state in the nation to move towards acceptance of this burgeoning therapeutic treatment. The ballot measure also set the stage for state-regulated “healing centers” where medical professionals can administer psychedelic treatment as part of a therapeutic regimen. Psychedelics remain a Schedule 1 drug on the Federal level, but the FDA has recently given them a “breakthrough therapy” designation. So, what is next for these so-called magic mushrooms?

What the Vote Means

Decriminalization. This portion of the bill allows residents aged 21 and over to grow, posses, and share psychedelic substances (magic mushrooms) without committing a crime. Sale of the substances is still not allowed.

Supervised Use. The bill also allows state-regulated centers to administer psilocybin and psilocin treatments. These active compounds in psychedelics are being studied as a potential mental health breakthrough, used in-tandem with mental health therapy sessions, capable of treating various conditions, including depression, PTDS, anxiety, eating disorders, and substance abuse disorders.

“In recent years, the Food and Drug Administration (FDA) has granted psychedelic compounds Breakthrough Therapy status, which has opened the door to new research studies and the potential development of new medications. Recently, research and approval of new drugs has progressed past phase 2 trials for the use of psilocybin – the naturally occurring psychedelic prodrug compound produced by numerous fungi species – as treatment for depressive disorder. In another example, a drug proposed for the treatment of certain PTSD diagnoses is heading towards a second phase 3 trial, with full FDA approval possible as early as 2022.”

While full approval in 2022 didn’t happen, psychedelics continue to make headway in the FDA approval process. In July of this year, Filament Health (FLHLF) announced the beginning of dosing in the first FDA-approved clinical trial studying the effects of naturally derived psychedelic drug candidates. This study, designed to compare both the physiological and the psychological effects of psilocin, is expected to conclude towards the end of 2024.

While psychedelics and the FDA have a checkered past, the tide appears to be turning. A growing mental health crisis, along with years of research on the potential positive effects of psychedelic treatments, appear to be nudging the FDA closer to approval. Just last year, Johns Hopkins Medicine was awarded a National Institute of Health grant to stud psychedelic treatment for tobacco addiction. This federal research grant was the first of its kind approved in the past 50 years.

What’s Next

Schedule 1. Under the Controlled Substances Act, psychedelics remain in most restrictive Category 1, which creates numerous hurdles for approval as treatment. FDA approval would help. If current and future clinical trials lead the FDA to approve the drug for various treatments, the DEA would be prompted to reevaluate the drug’s schedule. Ballot initiatives like those in Oregon and Colorado also help on the local level.

Treatment. After more than 50 years, the study of psychedelics as part of a mental health treatment regimen is finally allowed. There’s a lot of lost time to make up for. Clinical trials will be needed for various conditions to determine appropriate dosing and combination therapies. Still deep in an opioid crisis, it’s fair to expect the FDA and DEA to proceed with caution, even with promising early results.

Parallels. While completely different, it’s easy to draw certain parallels with the medical and recreational legalization of marijuana in the US. Over two decades, we’ve seen various states vote to legalize medical-only use, with others voting in favor of complete decriminalization along with legal recreational use, while a few states remain steadfast in keeping it a crime. Will we see similar results with psychedelics? It’s possible that, with the growing number of nearly untreatable conditions that psychedelics could improve, we see widespread medical acceptance in the coming years. Recreational use will almost certainly take longer with the current Schedule 1 status.

Acceptance and Capital. Acceptance is half the battle. The other is capital. The companies involved in bringing psychedelics to market will need investors backing them to move forward. Between clinical trials, therapeutic training, production, and marketing, these companies will need a great deal of funding to make it to market. But the potential is clear. Efficacy in early studies far surpasses any currently available treatment method for various mental health conditions, creating a market expected to grow to a value of over $3 billion by 2026.

Global Restaurant Franchising Company HiresExperienced C-Suite Growth Leader to Drive Expansion Efforts

LOS ANGELES, Nov. 14, 2022 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., announces the hiring of its first Chief Growth Officer, Jeremy Theisen. Theisen joins FAT Brands with over 20 years of experience in significantly increasing the revenue stream for high-growth start-ups in the restaurant sector and will be focused on spearheading the growth of the development pipeline across the FAT Brands portfolio. This includes bringing new franchisees into the system and driving multi-unit expansion with existing franchisees.

Prior to joining FAT Brands, Theisen served as Chief Revenue Officer of PathSpot, a hygiene management system geared towards the foodservice industry, where he not only grew the company’s contracted revenue by 15 times in 24 months, but also, was key in their overseas expansion in Europe and Australia. Theisen also served as Chief Sales Officer of Punchh, the restaurant industry leader in loyalty and engagement programs, where he saw the company through its launch to generating $50 million in revenue prior to being acquired by Par Technology Corporation several years later. Other experiences include Google and Truaxis, a loyalty rewards and personalized statement solutions company owned by MasterCard.

“Over the last several years, FAT Brands continues to reach new heights from a growth perspective,” said FAT Brands CEO Andy Wiederhorn. “While our acquisition strategy has been a key mechanism for growth, we have also been heavily invested in building out our deep, organic pipeline. This year has already been record-breaking from an opening standpoint, and we are just getting started. Jeremy is a great addition to our team to drive this growth forward exponentially in the years to come. His experience of quickly scaling companies from start-ups to industry leaders aligns with our fast-paced growth mentality.”

“I am excited for the new journey ahead at FAT Brands,” said Jeremy Theisen. “I have had the pleasure of working with the company while at my other ventures and have been amazed at the growth they have achieved. What was once Fatburger has now transformed into a 17-concept portfolio with a strong worldwide presence. I look forward to adding to the already strong growth trajectory of the company and forging new relationships with new and existing franchisees.”

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide.