Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Brand Strength. To illustrate the strength of MariMed’s brands, during the quarter in Illinois, the Company experienced a 23% sequential sales increase despite sales being down statewide 1.5%, according to Hoodie. In Massachusetts, MariMed sales increased 5% sequentially, compared to a 2% decline in the state, again according to Hoodie.

Wholesale. In terms of Wholesale, MariMed has achieved 75% penetration across all of its markets, excluding Missouri, leaving significant white space for future growth. The next step is to increase the breadth of relationship with customers, garnering additional shelf space for MariMed product.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Kelly reported 3Q25 results below expectations, even after scrubbing away a number of one-time events. Lower demand from the federal government and a few large customers negatively impacted results. Nonetheless, Kelly continued to capture growth in certain markets.

3Q25 Results. 3Q25 revenue fell 9.9% to $935 million from $1.04 billion last year. Consensus was $973 million, and we were at $975 million. Adjusted EBITDA was $16.5 million, or a 1.9% margin, compared to $26.2 million, or a 2,5% margin, in 3Q24. Consensus was $33 million, and we were at $33.5 million. Adjusted EPS was $0.18 vs $0.21 last year. Consensus was $0.42, we were at $0.45.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. While the restaurant industry continues to face headwinds, FAT Brands did see some positives from the operating side. Most encouraging is the momentum in same-store sales performance. The Company narrowed the SSS decline to just 3.5%, down from 4.2% in the second quarter, representing the strongest quarterly performance so far this year.

3Q25 Financials. Quarterly revenue totaled $140 million, a 2.3% decrease from $143.4 million in last year’s quarter. The decline was driven primarily by the closure of 11 underperforming Smokey Bones locations as planned. Adjusted EBITDA was $13.1 million, compared to $14.1 million a year ago. The Company reported a GAAP net loss of $58.2 million versus a net loss of $44.8 million a year ago. Adjusted net loss was $45.4 million, or $2.67/sh, compared to adjusted net loss of $38.0 million, or $2.34/sh, in 3Q24.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The E.W. Scripps Company (NASDAQ: SSP) is a diversified media company focused on creating a better-informed world. As one of the nation’s largest local TV broadcasters, Scripps serves communities with quality, objective local journalism and operates a portfolio of 61 stations in 41 markets. The Scripps Networks reach nearly every American through the national news outlets Court TV and Newsy and popular entertainment brands ION, Bounce, Defy TV, Grit, ION Mystery, Laff and TrueReal. Scripps is the nation’s largest holder of broadcast spectrum. Scripps runs an award-winning investigative reporting newsroom in Washington, D.C., and is the longtime steward of the Scripps National Spelling Bee. Founded in 1878, Scripps has held for decades to the motto, “Give light and the people will find their own way.”

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 Core outperforms peers. Core advertising increased 2%, outperforming its peers, which on average declined 2% in the quarter. In addition, the company overachieved adj. EBITDA on better than expected expense savings on employee costs across both operating segments.

Q4 core outlook outperforms peers as well. Management guided core advertising to increase 10% in Q4, significantly better than its peers, with most guiding flat to down as much as 5%. The biggest disappointment is in its Scripps Networks division, with Q4 revenues guided down low double-digits, impacted by the absence of Political and Medicare enrollment advertising due to the government shutdown.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. With four new contracts during the quarter, CoreCivic made substantial progress in contracting to use a significant portion of its idle facility capacity in the quarter. The four new contracts effective in the third quarter are expected to generate approximately $320 million of annual revenue once the facilities achieve stabilized occupancy. Notably, CoreCivic’s detention populations and revenues have been unaffected by the government shutdown.

3Q25 Results. Revenue of $580.4 million rose 18.1% y-o-y, driven by increased populations. We were at $550 million. CoreCivic recorded adjusted EBITDA of $88.8 million, up 6.6% y-o-y, but slightly below our $91.8 million estimate. Adjusted EPS was $0.24, up 26.3% y-o-y and in-line with our $0.27 estimate. Normalized FFO was $0.48, up 11.6% y-o-y and in-line with our $0.48 estimate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Data. Bit Digital reported its monthly Ethereum (“ETH”) treasury and staking metrics for the month of October 2025. As of October 31, 2025, the Company held approximately 153,547 ETH, versus 121,187 ETH at the end of September. Included in the ETH holdings were approximately 15,139 ETH and ETH-equivalents held in an externally managed fund, and approximately 5,132 ETH presented on an as-converted basis from LsETH using the Coinbase conversion rate as of 10/31/25. The Company’s total staked ETH was approximately 132,480 as of October 31st.

Yield and Value. Staking operations generated approximately 249 ETH in rewards during October, representing an annualized yield of approximately 2.93%. Based on a closing ETH price of $3,845.79, as of October 31, 2025, the market value of the Company’s ETH holdings was approximately $590.5 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Rumble Inc. announced plans to acquire Northern Data AG, a European leader in artificial intelligence and high-performance computing infrastructure, marking a transformative moment for the company’s growing cloud division. The agreement represents a bold step in Rumble’s “Freedom-First” vision—an initiative centered on building technology that prioritizes privacy, independence, and resilience over centralized control.

Under the terms of the deal, Rumble will launch a voluntary public exchange offer to Northern Data shareholders, granting them newly issued Rumble shares in return. Once completed, the transaction will give Rumble access to one of Europe’s largest GPU fleets—approximately 22,000 Nvidia units, including the latest H100 and H200 chips—and a globally distributed network of data centers. This infusion of infrastructure will allow Rumble to expand its cloud services dramatically while strengthening its foothold in the global AI ecosystem.

The acquisition also accelerates Rumble’s international growth strategy, extending its reach beyond North America into major European markets such as Germany, Sweden, Norway, Portugal, the Netherlands, and the United Kingdom. Northern Data’s energy-efficient data centers and liquid-cooled GPU technology will provide Rumble with a strong foundation to compete in high-performance computing and AI training at scale.

A major backer of the deal is Tether, which made a $775 million strategic investment in Rumble earlier this year. Tether’s continued involvement underscores the growing alignment between decentralized finance and digital infrastructure, and the company is expected to serve as a key customer following the transaction’s completion. Together, Rumble, Northern Data, and Tether aim to form a vertically integrated AI ecosystem designed to challenge the dominance of established technology giants.

In addition to its infrastructure assets, Northern Data brings expertise in managing complex compute operations and optimizing power efficiency—critical advantages as demand for GPU-based AI processing surges worldwide. The company’s Maysville, Georgia facility alone is expected to deliver up to 180 megawatts of capacity once complete, contributing significantly to Rumble’s total data center output.

Beyond scaling capacity, Rumble expects the acquisition to fuel innovation across its video, creator, and advertising businesses. Access to advanced AI hardware will accelerate the company’s efforts to integrate machine learning into content delivery, recommendation systems, and advertising solutions. The move also supports Rumble’s broader ambition to develop complementary services such as AI chatbots, cloud productivity tools, and financial applications under the Rumble Wallet brand.

The exchange offer is expected to close in the second quarter of 2026, pending regulatory approvals. Northern Data shareholders will own roughly 30% of the combined company after the transaction, reflecting the strategic significance of the merger. Once finalized, Northern Data plans to delist its shares, with no separate offer required since it is not traded on a regulated market.

For Rumble, the acquisition represents far more than an infrastructure upgrade—it signals an intent to redefine how technology infrastructure is built and governed. By merging AI computing power, distributed data networks, and financial independence, the company aims to create a sustainable foundation for a new era of digital freedom.

Bitcoin prices are facing their sharpest correction in months, with the cryptocurrency falling nearly 20% from its record high above $126,000 in early October. After briefly slipping below the key $100,000 threshold, Bitcoin is now trading near its lowest level in six months, leaving investors wondering whether the current downturn signals a temporary pullback or the start of a longer bear phase.

Analysts point to a combination of factors driving the decline, including profit-taking by early adopters and large-scale liquidations of leveraged positions. Data from Compass Point shows that long-term holders have sold more than 1 million Bitcoin since late June, marking one of the most significant waves of distribution in recent history. The selloff has weakened key support levels around $117,000 and $112,000, triggering stop-loss cascades and forcing many leveraged traders to unwind positions.

Market strategists caution that sentiment remains fragile. Markus Thielen of 10X Research noted that Bitcoin has failed to reclaim previous support zones, suggesting that the market may still have room to correct further before finding stability. According to Thielen, the next few weeks could be pivotal as investors reassess risk amid tightening liquidity and shifting macroeconomic dynamics. His firm warns that a drop below $93,000 could open the door to deeper losses, potentially testing the $70,000 level if liquidation pressures intensify.

The broader macro backdrop has also turned less favorable. The U.S. dollar has staged a rebound in recent weeks, exerting downward pressure on risk assets, including cryptocurrencies. Historically, Bitcoin tends to struggle when the dollar strengthens, as it reduces international purchasing power and dampens speculative demand. Additionally, the ongoing U.S. government shutdown has tightened liquidity conditions across financial markets, further weighing on investor sentiment.

Still, not all analysts are pessimistic. Some see this correction as a healthy reset in a long-term uptrend that remains intact. JPMorgan recently suggested that much of the forced deleveraging that triggered October’s decline has already played out. The bank’s analysts argue that rising volatility in gold has made Bitcoin relatively more attractive to investors seeking alternative stores of value. Their projections suggest Bitcoin could rebound to as high as $170,000 over the next 6 to 12 months, especially if market confidence stabilizes and macro conditions improve.

Potential catalysts could come from the policy side. A possible Federal Reserve rate cut in December and speculation about a more dovish leadership change when Chair Jerome Powell’s term expires in May could inject new optimism into markets. Similarly, the eventual resolution of the government shutdown may bring renewed liquidity into the system, which some believe could spill over into digital assets.

For now, the crypto market remains caught between optimism about long-term adoption and the short-term realities of profit-taking and tightening liquidity. While Bitcoin’s resilience near the $100,000 mark shows that investor interest remains strong, the coming weeks will likely determine whether this pullback marks a buying opportunity or the start of a more prolonged consolidation phase.

Consumer confidence in the United States has dropped to its lowest level in three years as the ongoing government shutdown weighs heavily on Americans’ views of the economy and their own financial situations. The University of Michigan’s preliminary consumer sentiment index for November fell to 50.3, marking a six percent decline from October and nearly a 30 percent decrease compared to the same month last year.

The latest reading reflects widespread unease among households. Many are increasingly worried about the effects of the prolonged government shutdown, which has now stretched past a month and become the longest in U.S. history. The shutdown has disrupted access to key government data on inflation, employment, and growth, leaving businesses and consumers uncertain about the true state of the economy.

Without fresh official data, Americans are relying on private reports that paint a concerning picture. Job cuts have surged, and labor market conditions appear to be softening. A report from Challenger, Gray & Christmas indicated that October saw the highest number of announced layoffs in more than two decades. Job openings have slowed, and many unemployed workers are finding it harder to secure new positions. Together, these trends suggest that confidence in the labor market is fading.

The decline in sentiment is not evenly spread across the population. Wealthier households, particularly those with large stock portfolios, remain more optimistic thanks to record highs in the equity markets. This contrast highlights the widening gap between those benefiting from strong financial markets and those struggling with everyday costs. The result is a divided economic landscape where prosperity is unevenly distributed, reinforcing the perception of a two-speed economy.

For most Americans, persistent inflation, higher interest rates, and the uncertainty caused by the shutdown are combining to erode financial stability. Even though inflation has eased from last year’s highs, the prices of essential goods and services remain well above pre-pandemic levels. Meanwhile, delays in government services such as Social Security payments and student loan processing are adding frustration and stress to households already under pressure.

The timing of this drop in confidence is particularly concerning as the country heads into the holiday shopping season. Consumer spending drives much of the U.S. economy, and a downturn in sentiment could translate into weaker retail sales. Businesses that rely on end-of-year spending may face slower demand if consumers choose to save rather than spend amid the growing uncertainty.

Economists warn that if the shutdown continues and confidence remains weak, growth could slow in the early months of 2026. The longer the political stalemate drags on, the greater the risk of long-term damage to household finances and business activity.

Overall, the latest sentiment data suggests that Americans are growing increasingly uneasy about both their personal finances and the broader economy. Until the government resolves the shutdown and restores a sense of stability, confidence is likely to remain depressed and the economic recovery may continue to lose momentum.

FLORHAM PARK, N.J., Nov. 07, 2025 — Conduent Incorporated (Nasdaq: CNDT), a global technology driven business process solutions and services company, today announced its third quarter 2025 financial results.

Cliff Skelton, Conduent President and Chief Executive Officer, stated, “Q3 represents not only a quarter where we met guidance on Adjusted Revenue and Adjusted EBITDA Margin, but also the continuation of our drive toward year-over-year revenue growth. New business signings were consistent year over year and our Public Sector businesses had a particularly strong quarter, despite the cyclical nature of government funding and the Federal government shutdown. As mentioned in Q2 earnings, we continue to be pleased with ongoing Transportation opportunities and momentum. Additionally, as a result of our operational efficiency efforts, Adjusted EBITDA and Adjusted EBITDA Margin improved both year over year and sequentially, in line with guidance. We also deployed AI enhancements with Conduent’s proprietary technology and platforms across document processing, customer experience, and fraud prevention—delivering greater efficiency for clients and further streamlining our internal operations.”

Skelton continued, “Regarding our portfolio rationalization efforts, 87% of our $1B capital allocation target has been achieved to date, and we remain on track to exceed that goal. We continue to be focused on cash generation, sales, and expanding our pipeline opportunities especially within our current client base, while maintaining more than ample liquidity through cash reserves and a recently renewed credit facility. As always, we remain confident in our team and our strategy as we continue to deliver the best value possible to our shareholders and to our clients and their end users.”

Key Financial Q3 2025 Results

($ in millions, except margin and per share data)

Q3 2025

Q3 2024

Current Quarter Y/Y B/(W)

Revenue

$767

$807

(5.0)%

Adjusted Revenue(1)

$767

$781

(1.8)%

GAAP Net Income (Loss)

$(46)

$123

n/m

Adjusted EBITDA(1)

$40

$32

25.0%

Adjusted EBITDA Margin(1)

5.2%

4.1%

110 bps

GAAP Income (Loss) Before Income Tax

$(38)

$159

n/m

GAAP Diluted EPS

$(0.30)

$0.72

n/m

Adjusted Diluted EPS(1)

$(0.09)

$(0.14)

35.7%

Cash Flow from Operating Activities

$(39)

$(13)

(200.0)%

Adjusted Free Cash Flow(1)

$(54)

$(6)

(800.0)%

Performance Commentary At the end of the quarter, Conduent maintained a cash balance of $264 million along with $198 million unused capacity under its recently renewed credit facility. During the quarter, Conduent repurchased approximately 4.7 million shares of common stock.

Pre-tax income (loss) for the third quarter of 2025 was $(38) million versus $159 million in the prior year period. This decrease is primarily caused by the divestiture-driven gain on the transfer of the Casualty Claims Solutions business.

Q3 2025 Adjusted EBITDA of $40 million and Adjusted EBITDA margin of 5.2% both increased versus the prior year period and were in line with guidance showing continued momentum toward our target margin.

Additional Q3 2025 Performance Highlights Conduent achieved several milestones related to its technology-led solutions, contract awards, financial foundation, and client support capabilities, including:

Announced the integration of generative AI (GenAI) and other advanced AI technologies into the Company’s government solutions to improve the disbursement of critical government benefits, enhance the citizen experience, and combat fraud in government benefit programs.

Successfully completed the refinancing of the Company’s revolving credit facility, extending the maturity, and paying off the Term Loan A.

Awarded a contract by the Richmond Metropolitan Transportation Authority to implement a Pay-by-Plate toll collection system supporting the transition to all-electronic tolling designed to streamline traffic for a faster, safer, and more enjoyable driving experience.

Announced an expansion of the Company’s Philippines operations with a new facility in Lipa-Malvar to support customer experience management solutions (CXM) for a leading U.S. healthcare company.

Expanded its FastCap® Finance Analytics solution by integrating GenAI-powered contract and spend analytics capability that enables expedited contract intake, verification of contract compliance, and identification of procurement savings and tariff-related financial exposures more efficiently and more accurately.

Implemented Conduent’s Maven® Disease Surveillance & Outbreak Management System for the State of Delaware, helping to monitor, report, and better understand public health threats and infectious disease outbreaks.

FY 2025 Outlook(2)

FY 2024 Actuals

FY 2025 Outlook(2)

Adj. Revenue(1)

$3,176M

$3,050 – $3,100

Adj. EBITDA(1) / Adj. EBITDA Margin(1)

$124M / 3.9%

5.0% – 5.5%

(1) Refer to Appendix for definition and complete non-GAAP reconciliations of Adjusted Revenue, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Diluted EPS and Adjusted Free Cash Flow. (2) Refer to Appendix for additional information regarding non-GAAP outlook.

Conference Call Management will present the results during a conference call and webcast on November 7, 2025 at 9:00 a.m. ET.

The call will be available by live audio webcast along with the news release and online presentation slides at https://investor.conduent.com/

The conference call will also be available by calling 877-407-4019 toll-free. If requested, the conference ID for this call is 13755924.

The international dial-in is 1-201-689-8337. The international conference ID is also 13755924.

A recording of the conference call will be available by calling 1-877-660-6853 three hours after the conference call concludes. The replay ID is 13755924.

The telephone recording will be available until Nov 21, 2025.

About Conduent Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 53,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling approximately 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing over 13 million tolling transactions every day. Learn more at www.conduent.com.

Non-GAAP Financial Measures We have reported our financial results in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In addition, we have discussed our financial results using non-GAAP measures. We believe these non-GAAP measures allow investors to better understand the trends in our business and to better understand and compare our results. Accordingly, we believe it is necessary to adjust several reported amounts, determined in accordance with U.S. GAAP, to exclude the effects of certain items as well as their related tax effects. Management believes that these non-GAAP financial measures provide an additional means of analyzing the results of the current period against the corresponding prior period. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, our reported results prepared in accordance with U.S. GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a substitute for comparable U.S. GAAP measures and should be read only in conjunction with our Consolidated Financial Statements prepared in accordance with U.S. GAAP. Our management regularly uses our non-GAAP financial measures internally to understand, manage and evaluate our business and make operating decisions. Providing such non-GAAP financial measures to investors allows for a further level of transparency as to how management reviews and evaluates our business results and trends. These non-GAAP measures are among the primary factors management uses in planning for and forecasting future periods. Compensation of our executives is based in part on the performance of our business based on certain of these non-GAAP measures. Refer to the “Non-GAAP Financial Measures” section attached to this release for a discussion of these non-GAAP measures and their reconciliation to the reported U.S. GAAP measures.

Forward-Looking Statements

This press release, any exhibits or attachments to this release, and other public statements we make may contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. The words “anticipate,” “believe,” “estimate,” “expect,” “expectations,” “in front of us,” “plan,” “intend,” “will,” “aim,” “should,” “could,” “forecast,” “target,” “may,” “continue to,” “looking to continue,” “endeavor,” “if,” “growing,” “projected,” “potential,” “likely,” “see,” “ahead,” “further,” “going forward,” “on the horizon,” “as we progress,” “going to,” “path from here forward,” “think,” “path to deliver,” “from here,” “on track,” “remain” and similar expressions (including the negative and plural forms of such words and phrases), as they relate to us, are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. All statements other than statements of historical fact included in this press release or any attachment to this press release are forward-looking statements, including, but not limited to, statements regarding our financial results, condition and outlook; changes in our operating results; general market and economic conditions; and our projected financial performance, including all statements made under the section captioned “FY 2025 Outlook” within this release. These statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions, many of which are outside of our control, that could cause actual results to differ materially from those expected or implied by such forward-looking statements contained in this press release, any exhibits to this press release and other public statements we make.

Important factors and uncertainties that could cause our actual results to differ materially from those in our forward-looking statements include, but are not limited to: government appropriations and termination rights contained in our government contracts, the competitiveness of the markets in which we operate and our ability to renew commercial and government contracts, including contracts awarded through competitive bidding processes; our ability to recover capital and other investments in connection with our contracts; our reliance on third-party providers; risk and impact of geopolitical events and increasing geopolitical tensions (such as the war in the Ukraine and conflict in the Middle East), macroeconomic conditions, natural disasters and other factors in a particular country or region on our workforce, customers and vendors; our ability to deliver on our contractual obligations properly and on time; changes in interest in outsourced business process services; claims of infringement of third-party intellectual property rights; our ability to estimate the scope of work or the costs of performance in our contracts; the loss of key senior management and our ability to attract and retain necessary technical personnel and qualified subcontractors; our failure to develop new service offerings and protect our intellectual property rights; our ability to modernize our information technology infrastructure and consolidate data centers; expectations relating to environmental, social and governance considerations; utilization of our stock repurchase program; risks related to our use of artificial intelligence; the failure to comply with laws relating to individually identifiable information and personal health information; the failure to comply with laws relating to processing certain financial transactions, including payment card transactions and debit or credit card transactions; breaches of our information systems or security systems or any service interruptions; risks related to hacking or other cybersecurity threats to our data systems, information systems and network infrastructure and other service interruptions, including relating to the previously disclosed cyber event that took place in January 2025, including Conduent’s investigation of such incident and mitigation and remediation efforts, the nature and extent of such incident, the potential disruption to our business or operations, the potential impact on Conduent’s reputation, and Conduent’s assessments of the likely financial and operational impacts of such incident; our ability to comply with data security standards; developments in various contingent liabilities that are not reflected on our balance sheet, including those arising as a result of being involved in a variety of claims, lawsuits, investigations and proceedings; risks related to recently completed divestitures including (i) the transfer of the Company’s BenefitWallet’s health savings account, medical savings account and flexible spending account portfolio, (ii) the sale of the Company’s Curbside Management and Public Safety Solutions businesses and (iii) the sale of the Company’s Casualty Claims Solutions business, including but not limited to the Company’s ability to realize the benefits anticipated from such transactions, unexpected costs, liabilities or delays in connection with such transactions, and the significant transaction costs associated with such transactions; risk and impact of potential goodwill and other asset impairments; our significant indebtedness and the terms of such indebtedness; our failure to obtain or maintain a satisfactory credit rating and financial performance; our ability to obtain adequate pricing for our services and to improve our cost structure; our ability to collect our receivables, including those for unbilled services; a decline in revenues from, or a loss of, or a reduction in business from or failure of significant clients; fluctuations in our non-recurring revenue; increases in the cost of voice and data services or significant interruptions in such services; our ability to receive dividends or other payments from our subsidiaries; and other factors that are set forth in the “Risk Factors” section, the “Legal Proceedings” section, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section and other sections in our 2024 Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with or furnished to the Securities and Exchange Commission. Any forward-looking statements made by us in this release speak only as of the date on which they are made. We are under no obligation to, and expressly disclaim any obligation to, update or alter our forward-looking statements, whether because of new information, subsequent events or otherwise, except as required by law.

NEW YORK, November 7, 2025 /PRNewswire/ — Bit Digital, Inc. (Nasdaq: BTBT) (“Bit Digital” or the “Company”) today announced its monthly Ethereum (“ETH”) treasury and staking metrics for the month of October 2025:

Key Highlights for October 2025

As of October 31, 2025, the Company held approximately 153,546.9[1] ETH.

Based on a closing ETH price of $3,845.79, as of October 31, 2025, the market value of the Company’s ETH holdings was approximately $590.5 million.

During the month of October 2025, the Company acquired 31,057.3 ETH.

The Company’s total average ETH acquisition price for all holdings was $3,045.14 as of October 31, 2025.

The Company staked an additional 32,544 ETH during the month. The Company’s total staked ETH was ~132,480, or ~86.3% of its total holdings, as of October 31, 2025.

Staking operations generated approximately 249 ETH in rewards during the period, representing an annualized yield of approximately 2.93%.

Bit Digital shares outstanding were 322,140,256 as of October 31, 2025.

The Company maintains ownership of approximately 27.0 million WhiteFiber (WYFI) shares with a market value of approximately $917.7 million as of October 31, 2025.

About Bit Digital Bit Digital is a publicly traded digital asset platform focused on Ethereum-native treasury and staking strategies. The Company began accumulating and staking ETH in 2022 and now operates one of the largest institutional Ethereum staking infrastructures globally. Bit Digital’s platform includes advanced validator operations, institutional-grade custody, active protocol governance, and yield optimization. Through strategic partnerships across the Ethereum ecosystem, Bit Digital aims to deliver exposure to secure, scalable, and compliant access to onchain yield. For additional information, please contact ir@bit-digital.com or follow us on LinkedIn or X.

Investor Notice Investing in our securities involves a high degree of risk. Before making an investment decision, you should carefully consider the risks, uncertainties and forward-looking statements described under “Risk Factors” in Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2024 (Annual Report) and any subsequently filed quarterly reports on Form 10-Q and any Current Reports on Form 8-K. If any material risk was to occur, our business, financial condition or results of operations would likely suffer. In that event, the value of our securities could decline and you could lose part or all of your investment. The risks and uncertainties we describe are not the only ones facing us. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations. In addition, our past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results in the future. See “Safe Harbor Statement” below.

Safe Harbor Statement This press release may contain certain “forward-looking statements” relating to the business of Bit Digital, Inc., and its subsidiary companies. All statements, other than statements of historical fact included herein are “forward-looking statements.” These forward-looking statements are often identified by the use of forward-looking terminology such as “believes,” “expects,” or similar expressions, involving known and unknown risks and uncertainties. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. Investors should not place undue reliance on these forward-looking statements, which speak only as of the date of this press release. The Company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in the Company’s periodic reports that are filed with the Securities and Exchange Commission and available on its website at http://www.sec.gov. All forward-looking statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by these factors. Other than as required under the securities laws, the Company does not assume a duty to update these forward-looking statements.

[1] Includes approximately 15,139.6 ETH and ETH-equivalents held in an externally managed fund, and approximately 5,131.6 ETH presented on as-converted basis from LsETH using the Coinbase conversion rate as of 10/31/25.

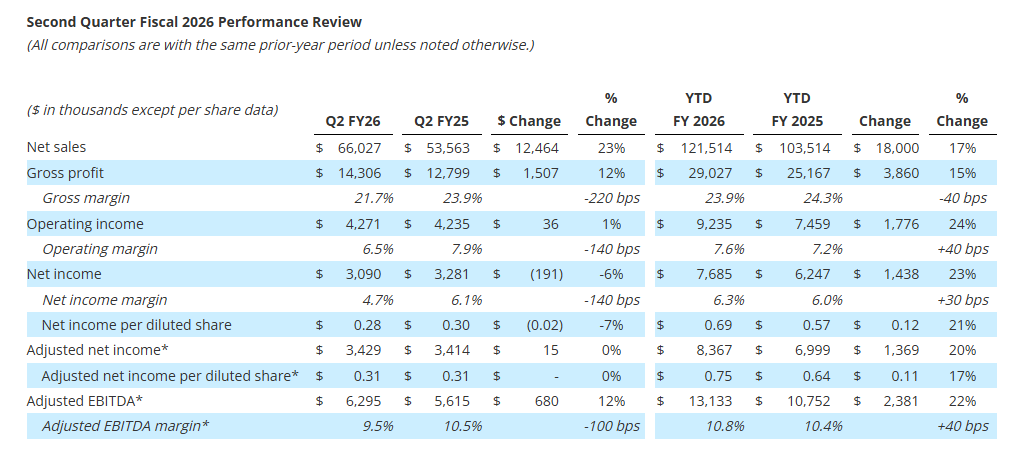

Gross profit increased 12% to $14.3 million; Gross profit margin was 21.7%

Net income per diluted share was $0.28; adjusted net income per diluted share1 was $0.31

Adjusted EBITDA1 increased 12% to $6.3 million; Adjusted EBITDA margin1 was 9.5%

Orders2 were $83.2 million; Book-to-Bill ratio2 of 1.3x and record backlog2 of $500.1 million

Strong balance sheet with no debt, $20.6 million in cash, and access to $44.7 million under its revolving credit facility at quarter end to support growth initiatives

Reiterating full year fiscal 2026 revenue and adjusted EBITDA guidance; Remain on track to reach strategic goal of 8% to 10% annual organic revenue growth and low to mid-teen Adjusted EBITDA margins1 by fiscal 2027

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, today reported financial results for its second quarter for the fiscal year ending March 31, 2026 (“fiscal 2026”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “I am pleased with our performance through the first half of the fiscal year. Our team continues to execute well across all business lines, driving broad-based growth supported by a record $500.1 million backlog. Demand across our end markets remains healthy as our Defense and Space markets continue to experience robust activity, and the Energy & Process market remains resilient. These trends are underscored by approximately $14.8 million of new Space orders secured and a $25.5 million follow-on order for the MK48 Torpedo program during the quarter, reinforcing our position as a trusted partner on critical platforms.”

Mr. Malone continued, “As we look to the second half of the year, we remain focused on advancing high-return initiatives that strengthen Graham’s competitive position and drive sustainable value creation. Across our operations, we are investing in automation, advanced testing, and new technical capabilities designed to enhance productivity, efficiency, and profitability. These include automated welding systems, advanced radiographic testing technologies, our NextGenTM steam ejector Nozzle, and our new cryogenic testing facility in Florida. Each of these projects is expected to deliver returns above 20%, improve margins, and create meaningful opportunities for growth in both defense and commercial markets.”

1Adjusted net income per diluted share, Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures. 2Orders, backlog and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), adjusted net income, adjusted net income per diluted share, adjusted EBITDA and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information provided at the end of this press release for important disclosures regarding Graham’s use of these non-GAAP measures.

Quarterly net sales of $66.0 million increased 23%, or $12.5 million. Sales in the Defense market contributed $9.9 million to growth primarily due to the timing of project milestones (primarily material receipts), new programs and growth in existing programs. Sales for the Energy & Process market increased $2.0 million or 11% driven by increased sales in China and timing of larger capital projects, partially offset by decreased sales in India due to project timing. Aftermarket sales in the Energy & Process and Defense markets of $9.8 million remained strong and were slightly higher than the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $1.5 million, or 12%, to $14.3 million compared to the prior-year period of $12.8 million. As a percentage of sales, gross profit margin decreased 220 basis points to 21.7%, compared to the second quarter of fiscal 2025. This decrease in gross profit margin reflects the mix of sales during the second quarter of fiscal 2026, and particularly, an extraordinarily high level of material receipts which carry a lower profit margin. Additionally, the second quarter and the first six months of fiscal 2025 gross profit benefited $0.4 million and $0.9 million, respectively, from a grant received in the prior year from the BlueForge Alliance to reimburse the Company for the cost of its defense welder training programs in Batavia which did not repeat in fiscal year 2026. For the first six months of fiscal 2026, we estimate the impact of tariffs on our consolidated financial statements to be approximately $1.0 million compared to the prior year.

Selling, general and administrative expense (“SG&A”), including intangible amortization, totaled $10.2 million, an increase of $1.1 million compared with the prior year due to the investments being made in operations, employees, and technology, as well as higher performance-based compensation due to Graham’s increased profitability. As a percentage of sales, SG&A, including amortization of 15.5%, decreased 160 basis points compared to the prior year period, reflecting the higher level of sales during the quarter as well as our continued financial discipline.

Cash Management and Balance Sheet

Cash provided by operating activities totaled $13.6 million for the quarter-ending September 30, 2025. As of September 30, 2025, cash and cash equivalents were $20.6 million, compared with $32.3 million as of September 30, 2024.

Capital expenditures for the second quarter fiscal 2025 were $4.1 million, focused on capacity expansion, increasing capabilities, and productivity improvements.

The Company had no debt outstanding as of September 30, 2025, with $44.7 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio

See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the second quarter of fiscal 2026 were $83.2 million. The increase in orders was across all our principle markets and included a $25.5 million follow-on order to provide mission-critical hardware for the MK48 Mod 7 Heavyweight Torpedo, as well as orders from leading Space/Aerospace customers. After-market orders for the Energy & Process and Defense markets for the second quarter of fiscal 2026 decreased $3.2 million to $9.6 million from the record levels of the prior year, but still remain strong.

Note that our orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was a record $500.1 million, a 23% increase over the prior-year period. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 25% to 30% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 85% of our backlog as of September 30, 2025, was to the Defense industry, which we believe provides stability and visibility to our business.

Fiscal 2026 Outlook

Based upon the results for the first half of fiscal 2026, as well as our expectations for the remainder of the fiscal year, Graham is reiterating its full year fiscal 2026 guidance for all metrics.

The Company has reduced the high end of its previously announced fiscal 2026 tariff impact by $1.0 million. Graham now expects tariffs to have an estimated impact of approximately $2.0 million to $4.0 million on its consolidated financial results. The Xdot Bearing Technologies (“Xdot”) Acquisition announced in October 2025 does not materially impact this guidance.

Graham’s Chief Financial Officer, Christopher J. Thome, said, “Given the continued strength in demand, we are reaffirming our full-year guidance. As a reminder, our third quarter typically represents our seasonally lowest revenue period, reflecting normal holiday impacts on production schedules.”

Mr. Thome continued, “Additionally, we are narrowing our full-year estimated tariff impact range to $2.0 million to $4.0 million, down from the prior $2.0 million to $5.0 million. With a record backlog and solid order momentum, we remain confident in our full-year outlook and our ability to deliver consistent performance throughout the fiscal year.”

Expectations for sales and profitability assume that the Company will operate its production facilities at planned capacity, maintain access to its global supply chain and subcontractors, avoid significant global disruptions, and not be materially affected by unforeseen events.

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on November 7, 2025 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201)-689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, November 14, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13756267 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “estimate,” “expects,” “future,” “outlook,” “believes,” “could,” “guidance,” “may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the Defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures

Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, equity-based compensation, ERP implementation costs, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

Forward-Looking Non-GAAP Measures

Adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators

In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent definitive agreements with customers to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Total backlog can include both funded and unfunded orders under government contracts. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission-critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space markets, today announced growing momentum in its commercial space business, supported by a series of recent orders from leading Space/Aerospace customers in aggregate value of approximately $22 million.

During its fiscal second and third quarters, Graham’s wholly owned subsidiary, Barber-Nichols LLC (“BN”), booked multiple new orders for advanced turbomachinery and precision-engineered components from six industry leading players in the commercial space launch market. These orders, which are expected to convert into revenue over the next 12 to 24 months, underscores the Company’s expanding role as being a critical supplier for next-generation space systems.

To support this continued demand, Graham is investing in production capacity and capabilities at its Colorado-based Barber-Nichols facility, including the addition of new CNC machining centers, a liquid nitrogen test stand, and supporting infrastructure to increase throughput and meet accelerating customer schedules. These investments are in addition to the previously announced cryogenic test facility the company is constructing near its P3 Technologies subsidiary in Jupiter, Florida expected to be opened later this year.

“We are seeing strong and sustained momentum from both new and existing customers in the space sector,” said Mike Dixon, General Manager of Barber-Nichols. “These orders reflect Barber-Nichols long commitment to the space industry and key development programs that support the commercial launch sector that are now beginning to transition to higher rate production. Our team’s expertise in high-speed rotating equipment and precision manufacturing continues to position us as a trusted supplier for complex, high-performance systems. With additional machining capacity and test capabilities coming online, we are well positioned to deliver on these programs and continue supporting our customers’ missions.”

Graham’s growing presence in the space market complements its established leadership across defense and energy end markets and reinforces the Company’s strategy to diversify its portfolio across high-growth, technology-driven applications.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “expected,” “positions,” “will,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, completion and profitability of future projects and the business, its ability to deliver to plan, potential revenues and timing of such revenues, capacity, demand growth, and delivering timely or otherwise on schedule are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.