Research News and Market Data on DRCT

November 09, 2023 4:01pm EST

Third Quarter 2023 Revenue Up 129% Year-Over-Year to $59.5 Million

Company Raises Full-Year 2023 Revenue Guidance to $170 Million – $190 Million

HOUSTON, Nov. 9, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced financial results for the third quarter ended September 30, 2023.

Mark D. Walker, Chairman and Chief Executive Officer, commented, “In recent quarters, we have made significant investments in our technology stack, advertising platform and operational structure. We initially expected to see the impact of these investments in 2024, however, we are pleased to report that these benefits have arrived much earlier in 2023. Our strong technology partnerships and our overarching business strategy have enabled us to meet a growing number of customers’ demands and further the capabilities of our sell-side technology platform. On both the sell-side and the buy-side, increased spend from our buying partners has resulted in an associated increase in our impression count and organic growth profile with a direct positive impact on net income and adjusted EBITDA(1).”

Keith Smith, President, added, “The growth seen in this quarter, as well as the past year, has been fueled by a combination of our strategic investments and partnerships, our differentiated approach to advertising solutions, as well as a set of market dynamics which have been highly beneficial to our position in the industry. We have capitalized on the shift in ad spend towards digital media on both the sell- and buy-side and will continue to grow our presence in the space through our recent partnerships and advancements of our technology stack. We remain committed to executing on the same growth and investment initiatives that led us to the strong third quarter results we are reporting today.”

Third Quarter 2023 Business Highlights

- For the third quarter ended September 30, 2023, Direct Digital Holdings processed over 400 billion monthly impressions through its sell-side advertising segment, an increase of 220% over the same period of 2022.

- In addition, the Company’s sell-side advertising platforms received over 34 billion monthly bid responses in the third quarter of 2023, an increase of over 210% over the same period in 2022. Sell-side revenue per advertiser for the third quarter of 2023 increased 241% compared to the same period of 2022.

- The Company’s buy-side advertising segment served approximately 228 customers in the third quarter of 2023 and buy-side revenue per customer increased 14% compared to the same period of 2022.

Third Quarter 2023 Financial Highlights:

- Revenue was $59.5 million in the third quarter of 2023, an increase of $33.5 million, or 129% over the $26.0 million in the same period of 2022.

- Sell-side advertising segment revenue grew to $51.6 million and contributed $32.8 million of the increase, or 174% growth over the $18.9 million of sell-side revenue in the same period of 2022.

- Buy-side advertising segment revenue grew to $7.9 million and contributed $0.7 million of the increase, or 10% growth over the $7.1 million of buy-side revenue in the same period of 2022.

- Consolidated operating income in the third quarter of 2023 was $4.5 million compared to consolidated operating income of $1.8 million in the same period of 2022, an increase of 144% year-over-year.

- Net income was $3.4 million in the third quarter of 2023, compared to net income of $0.8 million in the same period of 2022, an increase of 313% year-over-year.

- Adjusted EBITDA(1) was $5.4 million in the third quarter of 2023, compared to $2.4 million in the same period of 2022, an increase of 123% year-over-year.

Financial Outlook

Assuming the U.S. economy does not experience any major economic conditions that deteriorate or otherwise significantly reduce advertiser demand, we are increasing our previously issued estimate as disclosed in our second quarter 2023 update:

- For fiscal year 2023, we expect revenue to be in the range of $170 million to $190 million, or 101% year-over-year growth at the mid-point.

“We are thrilled to announce the raising of our fiscal year 2023 revenue guidance to $180 million at the midpoint, a 101% increase over full-year 2022 results. This increase reflects our belief in our ability to execute on our various growth strategies, demonstrates the strength of our operating leverage and highlights the favorable market trends that we expect to continue for the remainder of this year,” commented Diana Diaz, Chief Financial Officer.

Conference Call and Webcast Details

Direct Digital will host a conference call on Thursday, November 9, 2023 at 5:00 p.m. Eastern Time to discuss the Company’s third quarter 2023 financial results. The live webcast and replay can be accessed at https://ir.directdigitalholdings.com/. Please access the website at least fifteen minutes prior to the call to register, download and install any necessary audio software. For those who cannot access the webcast, a replay will be available at https://ir.directdigitalholdings.com/ for a period of twelve months.

Footnotes

(1) “Adjusted EBITDA” is a non-GAAP financial measure. The section titled “Non-GAAP Financial Measures” below describes our usage of non-GAAP financial measures and provides reconciliations between historical GAAP and non-GAAP information contained in this press release.

Forward Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to the Company. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; our limited operating history, which could result in our past results not being indicative of future operating performance; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, on receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the Securities and Exchange Commission that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this press release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The Company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage on average over 125,000 clients monthly, generating over 300 billion impressions per month across display, CTV, in-app and other media channels.

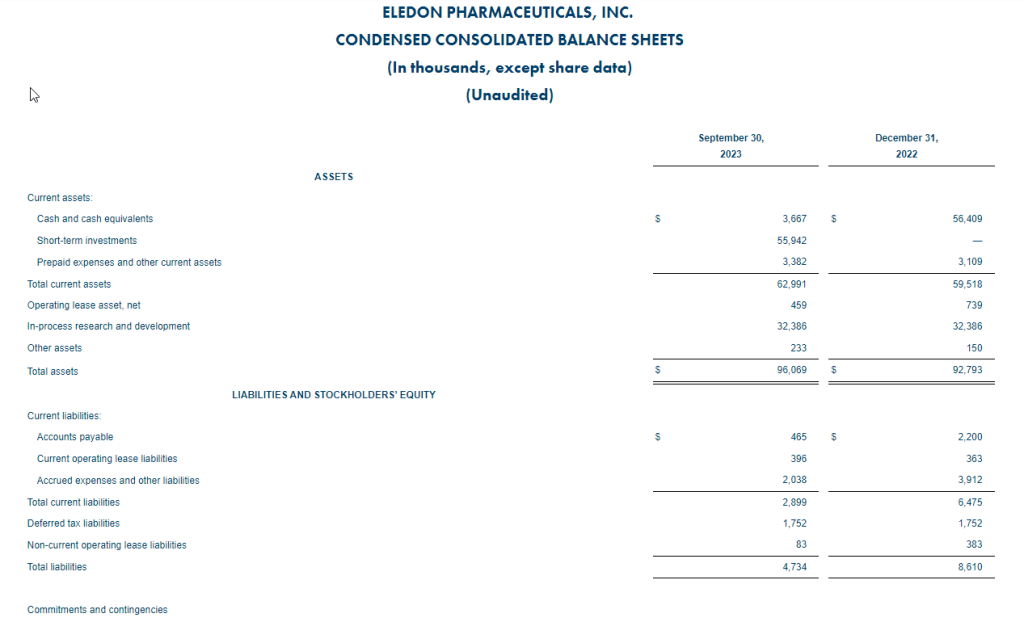

| CONSOLIDATED BALANCE SHEETS (unaudited) | |||||||

| September 30, 2023 | December 31, 2022 | ||||||

| ASSETS | |||||||

| CURRENT ASSETS | |||||||

| Cash and cash equivalents | $ | 5,481,949 | $ | 4,047,453 | |||

| Accounts receivable, net | 54,637,634 | 26,354,114 | |||||

| Prepaid expenses and other current assets | 1,426,925 | 883,322 | |||||

| Total current assets | 61,546,508 | 31,284,889 | |||||

| Property, equipment and software, net of accumulated depreciation and amortization of $219,386 and $34,218, respectively | 625,028 | 673,218 | |||||

| Goodwill | 6,519,636 | 6,519,636 | |||||

| Intangible assets, net | 12,172,396 | 13,637,759 | |||||

| Deferred tax asset, net | 5,082,424 | 5,164,776 | |||||

| Operating lease right-of-use assets | 674,846 | 798,774 | |||||

| Other long-term assets | 127,492 | 46,987 | |||||

| Total assets | $ | 86,748,330 | $ | 58,126,039 | |||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

| CURRENT LIABILITIES | |||||||

| Accounts payable | $ | 45,021,034 | $ | 17,695,404 | |||

| Accrued liabilities | 4,071,128 | 4,777,764 | |||||

| Liability related to tax receivable agreement, current portion | 41,141 | 182,571 | |||||

| Notes payable, current portion | 1,146,250 | 655,000 | |||||

| Deferred revenues | 1,044,069 | 546,710 | |||||

| Operating lease liabilities, current portion | 49,977 | 91,989 | |||||

| Income taxes payable | 113,355 | 174,438 | |||||

| Related party payables | 1,428,093 | 1,448,333 | |||||

| Total current liabilities | 52,915,047 | 25,572,209 | |||||

| Notes payable, net of short-term portion and deferred financing cost of $1,722,716 and $2,115,161, respectively | 22,323,534 | 22,913,589 | |||||

| Economic Injury Disaster Loan | 150,000 | 150,000 | |||||

| Liability related to tax receivable agreement, net of current portion | 4,245,234 | 4,149,619 | |||||

| Operating lease liabilities, net of current portion | 717,632 | 745,340 | |||||

| Total liabilities | 80,351,447 | 53,530,757 | |||||

| COMMITMENTS AND CONTINGENCIES (Note 9) | |||||||

| STOCKHOLDERS’ EQUITY | |||||||

| Class A common stock, $0.001 par value per share, 160,000,000 shares authorized, 2,991,792 and 2,900,000 shares issued and outstanding, respectively | 2,992 | 2,900 | |||||

| Class B common stock, $0.001 par value per share, 20,000,000 shares authorized, 11,278,000 shares issued and outstanding | 11,278 | 11,278 | |||||

| Additional paid-in capital | 8,782,092 | 8,224,365 | |||||

| Accumulated deficit | (2,399,479) | (3,643,261) | |||||

| Total stockholders’ equity | 6,396,883 | 4,595,282 | |||||

| Total liabilities and stockholders’ equity | $ | 86,748,330 | $ | 58,126,039 | |||

| CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) | |||||||||||||

| For the Three Months Ended | For the Nine Months Ended | ||||||||||||

| September 30, | September 30, | ||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||

| Revenues | |||||||||||||

| Buy-side advertising | $ | 7,850,058 | $ | 7,130,736 | $ | 27,092,816 | $ | 22,283,044 | |||||

| Sell-side advertising | 51,622,066 | 18,854,639 | 89,006,018 | 36,333,976 | |||||||||

| Total revenues | 59,472,124 | 25,985,375 | 116,098,834 | 58,617,020 | |||||||||

| Cost of revenues | |||||||||||||

| Buy-side advertising | 3,113,491 | 2,471,170 | 10,650,541 | 7,694,987 | |||||||||

| Sell-side advertising | 44,605,815 | 16,053,461 | 77,189,787 | 30,344,670 | |||||||||

| Total cost of revenues | 47,719,306 | 18,524,631 | 87,840,328 | 38,039,657 | |||||||||

| Gross profit | 11,752,818 | 7,460,744 | 28,258,506 | 20,577,363 | |||||||||

| Operating expenses | |||||||||||||

| Compensation, taxes and benefits | 4,747,081 | 3,845,918 | 12,934,406 | 9,895,646 | |||||||||

| General and administrative | 2,512,330 | 1,770,002 | 8,717,584 | 5,187,875 | |||||||||

| Total operating expenses | 7,259,411 | 5,615,920 | 21,651,990 | 15,083,521 | |||||||||

| Income from operations | 4,493,407 | 1,844,824 | 6,606,516 | 5,493,842 | |||||||||

| Other income (expense) | |||||||||||||

| Other income | 83,331 | — | 175,472 | 47,982 | |||||||||

| Forgiveness of Paycheck Protection Program loan | — | — | — | 287,143 | |||||||||

| Loss on redemption of non-participating preferred units | — | — | — | (590,689) | |||||||||

| Contingent loss on early termination of line of credit | — | — | (299,770) | — | |||||||||

| Interest expense | (1,059,890) | (905,605) | (3,104,684) | (2,269,643) | |||||||||

| Total other expense | (976,559) | (905,605) | (3,228,982) | (2,525,207) | |||||||||

| Income before taxes | 3,516,848 | 939,219 | 3,377,534 | 2,968,635 | |||||||||

| Tax expense | 165,994 | 128,436 | 165,658 | 215,112 | |||||||||

| Net income | $ | 3,350,854 | $ | 810,783 | $ | 3,211,876 | $ | 2,753,523 | |||||

| Net income per common share: | |||||||||||||

| Basic | $ | 0.23 | $ | 0.06 | $ | 0.23 | $ | 0.23 | |||||

| Diluted | $ | 0.23 | $ | 0.06 | $ | 0.22 | $ | 0.23 | |||||

| Weighted-average number of shares of common stock outstanding: | |||||||||||||

| Basic | 14,268,168 | 14,178,000 | 14,216,211 | 11,846,601 | |||||||||

| Diluted | 14,827,165 | 14,545,241 | 14,817,770 | 11,996,969 | |||||||||

| CONSOLIDATED STATEMENTS OF CASH FLOWS (unaudited) | ||||||

| For the Nine Months Ended September 30, | ||||||

| 2023 | 2022 | |||||

| Cash Flows Provided By Operating Activities: | ||||||

| Net income | $ | 3,211,876 | $ | 2,753,523 | ||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||

| Amortization of deferred financing costs | 434,847 | 463,008 | ||||

| Amortization of intangible assets | 1,465,363 | 1,465,364 | ||||

| Amortization of right-of-use assets | 123,928 | 94,974 | ||||

| Amortization of capitalized software | 159,057 | — | ||||

| Depreciation of property and equipment | 26,112 | — | ||||

| Stock-based compensation | 545,504 | 85,437 | ||||

| Forgiveness of Paycheck Protection Program loan | — | (287,143) | ||||

| Deferred income taxes | 82,352 | (40,591) | ||||

| Payment on tax receivable agreement | (45,815) | — | ||||

| Loss on redemption of non-participating preferred units | — | 590,689 | ||||

| Contingent loss on early termination of line of credit | 299,770 | — | ||||

| Bad debt expense | 97,740 | 2,717 | ||||

| Changes in operating assets and liabilities: | ||||||

| Accounts receivable | (28,381,260) | (13,520,067) | ||||

| Prepaid expenses and other assets | (524,098) | 482,190 | ||||

| Accounts payable | 27,325,629 | 10,008,327 | ||||

| Accrued liabilities | (513,138) | 1,555,037 | ||||

| Income taxes payable | (61,083) | 94,440 | ||||

| Deferred revenues | 497,359 | (201,907) | ||||

| Operating lease liability | (69,720) | (75,396) | ||||

| Related party payable | — | (70,801) | ||||

| Net cash provided by operating activities | 4,674,423 | 3,399,801 | ||||

| Cash Flows Used In Investing Activities: | ||||||

| Cash paid for capitalized software and property and equipment | (136,978) | — | ||||

| Net cash used in investing activities | (136,978) | — | ||||

| Cash Flows Used In Financing Activities: | ||||||

| Proceeds from note payable | — | 4,260,000 | ||||

| Payments on term loan | (491,250) | (412,500) | ||||

| Payments of litigation settlement | (193,500) | — | ||||

| Payments on lines of credit | — | (400,000) | ||||

| Payment of deferred financing costs | (442,181) | (525,295) | ||||

| Proceeds from Issuance of Class A common stock, net of transaction costs | — | 11,167,043 | ||||

| Redemption of common units | — | (7,200,000) | ||||

| Redemption of non-participating preferred units | — | (7,046,251) | ||||

| Proceeds from options exercised | 215 | — | ||||

| Proceeds from warrants exercised | 12,100 | — | ||||

| Distributions to members | (1,988,333) | (916,433) | ||||

| Net cash used in financing activities | (3,102,949) | (1,073,436) | ||||

| Net increase in cash and cash equivalents | 1,434,496 | 2,326,365 | ||||

| Cash and cash equivalents, beginning of the period | 4,047,453 | 4,684,431 | ||||

| Cash and cash equivalents, end of the period | $ | 5,481,949 | $ | 7,010,796 | ||

| Supplemental Disclosure of Cash Flow Information: | ||||||

| Cash paid for taxes | $ | 348,862 | $ | 133,401 | ||

| Cash paid for interest | $ | 2,667,283 | $ | 1,744,365 | ||

| Non-cash Financing Activities: | ||||||

| Transaction costs related to issuances of Class A shares included in accrued liabilities | $ | — | $ | 1,000,000 | ||

| Outside basis difference in partnership | $ | — | $ | 3,234,000 | ||

| Tax receivable agreement payable to Direct Digital Management, LLC | $ | — | $ | 278,900 | ||

| Tax benefit on tax receivable agreement | $ | — | $ | 485,100 | ||

| Issuance related to vesting of restricted stock units, net of tax withholdings | $ | 90 | $ | — | ||

NON-GAAP FINANCIAL MEASURES

In addition to our results determined in accordance with U.S. generally accepted accounting principles (“GAAP”), including, in particular operating income, net cash provided by operating activities, and net income, we believe that earnings before interest, taxes, depreciation and amortization (“EBITDA”), as adjusted for stock compensation expense, loss on early termination of line of credit, and loss on early extinguishment of debt, and loss on early redemption of non-participating preferred units (“Adjusted EBITDA”), a non-GAAP financial measure, is useful in evaluating our operating performance. The most directly comparable GAAP measure to Adjusted EBITDA is net income (loss).

In addition to operating income and net income, we use Adjusted EBITDA as a measure of operational efficiency. We believe that this non-GAAP financial measure is useful to investors for period-to-period comparisons of our business and in understanding and evaluating our operating results for the following reasons:

- Adjusted EBITDA is widely used by investors and securities analysts to measure a company’s operating performance without regard to items such as depreciation and amortization, interest expense, provision for income taxes, and certain one-time items such as acquisition transaction costs and gains from settlements or loan forgiveness that can vary substantially from company to company depending upon their financing, capital structures and the method by which assets were acquired;

- Our management uses Adjusted EBITDA in conjunction with GAAP financial measures for planning purposes, including the preparation of our annual operating budget, as a measure of operating performance and the effectiveness of our business strategies and in communications with our board of directors concerning our financial performance; and

- Adjusted EBITDA provides consistency and comparability with our past financial performance, facilitates period-to-period comparisons of operations, and also facilitates comparisons with other peer companies, many of which use similar non-GAAP financial measures to supplement their GAAP results.

Our use of this non-GAAP financial measure has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results as reported under GAAP. The following table presents a reconciliation of Adjusted EBITDA to net income (loss) for each of the periods presented:

| NON-GAAP FINANCIAL METRICS (unaudited) | |||||||||||||

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | ||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||

| Net income | $ | 3,350,854 | $ | 810,783 | $ | 3,211,876 | $ | 2,753,523 | |||||

| Add back (deduct): | |||||||||||||

| Interest expense | 1,059,890 | 905,605 | 3,104,684 | 2,269,643 | |||||||||

| Amortization of intangible assets | 488,455 | 488,455 | 1,465,364 | 1,465,364 | |||||||||

| Stock-based compensation | 241,491 | 70,030 | 545,504 | 85,438 | |||||||||

| Depreciation and amortization of capitalized software, property and equipment | 63,689 | — | 185,169 | — | |||||||||

| Contingent loss on early termination of line of credit | — | — | 299,770 | — | |||||||||

| Tax expense | 165,994 | 128,436 | 165,658 | 215,112 | |||||||||

| Forgiveness of PPP loan | — | — | — | (287,163) | |||||||||

| Loss on early redemption of non-participating preferred units | — | — | — | 590,689 | |||||||||

| Adjusted EBITDA | $ | 5,370,373 | $ | 2,403,309 | $ | 8,978,025 | $ | 7,092,606 | |||||

Contacts:

Investors:

Brett Milotte, ICR

Brett.Milotte@icrinc.com

View original content to download multimedia:https://www.prnewswire.com/news-releases/direct-digital-holdings-reports-third-quarter-2023-financial-results-301983927.html

SOURCE Direct Digital Holdings

Released November 9, 2023