Helping the Liver Regenerate Itself Could Give Patients with End-Stage Liver Disease a Treatment Option Besides Waiting for a Transplant

The liver is known for its ability to regenerate. It can completely regrow itself even after two-thirds of its mass has been surgically removed. But damage from medications, alcohol abuse or obesity can eventually cause the liver to fail. Currently, the only effective treatment for end-stage liver disease is transplantation.

However, there is a dearth of organs available for transplantation. Patients may have to wait from 30 days to over five years to receive a liver for transplant in the U.S. Of the over 11,600 patients on the waiting list to receive a liver transplant in 2021, only a little over 9,200 received one.

But what if, instead of liver transplantation, there were a drug that could help the liver regenerate itself?

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Satdarshan (Paul) Singh Monga, MD, FAASLD, Professor of Pathology and Medicine, University of Pittsburgh Health Sciences.

I am the founding director of the Pittsburgh Liver Research Center and run a lab studying liver regeneration and cancer. In our recently published research, my team and I found that activating a particular protein with a new medication can help accelerate regeneration and repair after severe liver injury or partial surgical removal in mice.

Key Players in Liver Regeneration

The liver performs over 500 key functions in your body, including producing proteins that carry fat through the body, converting excess glucose into glycogen for storage and breaking down toxins like ammonia, among others.

Liver cells, or hepatocytes, take on these many tasks by a divide-and-conquer strategy, also called zonation. This separates the liver into three zones with different tasks, and cells are directed to perform specialized functions by turning on specific genes active in each zone. However, exactly what controls the expression of these genes has been poorly understood.

Over the past two decades, my team and other labs have identified one group of 19 proteins called Wnts that play an important role in controlling liver function and regeneration. While researchers know that Wnt proteins help activate the repair process in damaged liver cells, which ones actually control zonation and regeneration, as well as their exact location in the liver, have been a mystery.

To identify these proteins and where they came from, my team and I used a new technology called molecular cartography to identify how strongly and where 100 liver function genes are active. We found that only two of 19 Wnt genes, Wnt2 and Wnt9b, were functionally present in the liver. We also found that Wnt2 and Wnt9b were located in the endothelial cells lining the blood vessels in zone 3 of the liver, an area that plays a role in a number of metabolic functions.

To our surprise, eliminating these two Wnt genes resulted in all liver cells expressing only genes typically limited to zone 1, significantly limiting the liver’s overall function. This finding suggests that liver cells experience an ongoing push and pull in gene activation that can modify their functions, and Wnt is the master regulator of this process.

Eliminating the two Wnt genes from endothelial cells also completely stopped liver cell division, and thus regeneration, after partial surgical removal of the liver.

Liver Regeneration After Tylenol Overdose

We then decided to test whether a new drug could help recover liver zonation and regeneration. This drug, an antibody called FL6.13, shares similar functions with Wnt proteins, including activating liver regeneration.

Over the course of two days, we gave this drug to mice that were genetically engineered to lack Wnt2 and Wnt9b in their liver endothelial cells. We found that the drug was able to nearly completely recover liver cell division and repair functions.

Lastly, we wanted to test how well this drug worked to repair the liver after Tylenol overdose. Tylenol, or acetaminophen, is an over-the-counter medication commonly used to treat fever and pain. However, an overdose of Tylenol can cause severe liver damage. Without immediate medical attention, it can lead to liver failure and death. Tylenol poisoning is one of the most common causes of severe liver injury requiring liver transplantation in the U.S. Despite this, there is currently only one medication available to treat it, and it is only able to prevent liver damage if taken shortly after overdose.

We tested our new drug on mice with liver damage from toxic doses of Tylenol. We found that one dose was able to decrease liver injury biomarkers – proteins the liver releases when injured – in the blood and reduce liver tissue death. These findings indicate that liver cell repair and tissue regeneration are occurring.

Reducing the Need for Transplantation

One way to address liver transplantation shortages is to improve treatments for liver diseases. While current medications can effectively cure hepatitis C, a viral infection that causes liver inflammation, other liver diseases haven’t seen the same progress. Because very few effective treatments are available for illnesses like nonalcoholic fatty liver disease and alcoholic liver disease, many patients worsen and end up needing a liver transplant.

My team and I believe that improving the liver’s ability to repair itself could help circumvent the need for transplantation. Further study of drugs that promote liver regeneration may help curb the burden of liver disease worldwide.

A certain EV Company may try to charge up its stock with a buyback.

Are stock buybacks good for companies, good for investors, and better than dividends? Last week, TESLA (TSLA) investors became excited about a tweet from founder Elon Musk that could suggest the company may bow to large shareholders and do a stock buyback. The implications for a company buying back shares and stockholders are many. Below you’ll find details on what the most typical considerations are and what it means from an investor’s standpoint.

What Is a Stock Buyback?

A stock buyback is when a public company uses cash in reserves or borrowed funds to buy shares of its own stock on the open market. A company may do this to consolidate ownership, preserve a higher stock price, boost financial ratios, work to reduce the cost of capital, or to return higher asset values to shareholders.

Investors find out when a public companies that has decided to do a stock buyback announces that the board of directors has passed a “repurchase authorization.” The amount authorized provides how much will be allocated or raised to buy back shares, or in some circumstances, the number of shares or percentage of shares outstanding it aims to purchase.

During the stock buyback, the company goes to the open market as any investor would and purchases shares of its stock in competition with other market participants. The added demand and later reduced shares available (float), puts upward pressure on the stock price. Stockholders then find their shares trade at a higher price than they would have. Shareholders are not obligated to sell their stock to the company, and a stock buyback doesn’t target any specific group of holders—retail and institutional all participate.

Public companies that have decided to do a stock buyback typically announce that the board of directors has passed a “repurchase authorization,” which details how much money will be allocated to buy back shares—or the number of shares or percentage of shares outstanding it aims to buy back.

Why Do a Stock Buyback?

The primary reason a company will buy back shares is to create value for its shareholders. Remember, fewer shares should cause those still being transacted in the open market to be trading at a higher price.

Boards of public companies’ primary responsibility are to look out for shareholders’ interests. At the top of this list is maximizing shareholder value. With this in mind, companies are always finding ways to generate the highest possible returns for their investors. This, at its most fundamental level, includes increasing the value of its stock and rewarding its investors. Buybacks and dividends work to maximize value for shareholders.

Declaring a dividend is the most direct method to return cash to shareholders; there are advantages to stock buybacks:

Tax efficiency – Dividend payments are taxed as income, whereas rising share values aren’t taxed at all. Any holders who sell their shares back to the company may recognize capital gains taxes, but shareholders who do not sell to reap the reward of a higher share value and no additional taxes until they decide when to cash in.

Directly boost share prices – The main goal of any share repurchase program is to deliver a higher share price. The board may feel that the company’s shares are undervalued, making it a good time to buy them. Meanwhile, investors may perceive a buyback as an expression of confidence by the management. After all, why would a company want to buy back stock it anticipates would decline in value?

More flexibility than dividends – Any company that initiates a new dividend or increases an existing dividend will need to continue making payments over the long term. That’s because they risk lower share values and unhappy investors if they reduce or eliminate the dividend going forward. Meanwhile, since share buybacks are one-offs, they are much more flexible tools for management.

Offset dilution – Growing companies may find themselves in a race to attract talent. If they issue stock options to retain employees, the options that are exercised over time increase the company’s total number of outstanding shares—and dilute existing shareholders. Buybacks are one way to offset this effect.

How is Value Impacted?

Key metrics investors and stock analysts use to value a public are impacted by a buyback. For example, cash is removed from a company’s balance sheet, and the number of shares trading is reduced.

Once a company has bought back its own shares, they are either canceled which reduces the number of shares available to trade (not just on the open market), or held by the company as treasury shares. These are not counted as outstanding shares, which has implications for many important measures of a company’s financial fundamentals.

Metrics important to investors, like earnings per share (EPS) are calculated by dividing a company’s profit by the number of outstanding shares. Mathematically, by reducing the number of outstanding shares, a higher EPS results as the quotient.

Price-to-earnings ratios (P/E ratio) are also mathematically improved as a higher price to the same earnings is desirable to shareholders. It helps investors measure a company’s relative valuation by comparing its stock price to its EPS.

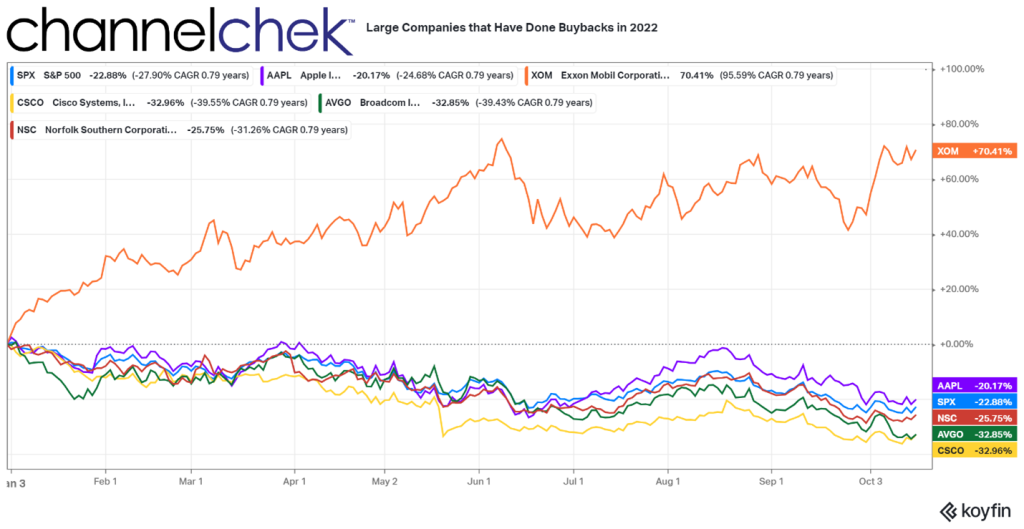

Who Else Has Done a Buyback in 2022?

If Tesla does indeed get approval from its board of directors to buy back shares, it won’t be the only large company that has in 2022. Apple (AAPL) bought back 3.5% of its shares in May ($90 billion), Exxon (XOM) bought back 2.9% of its shares in February ($10 billion), Broadcom (AVGO) bought 4.3% of its shares in May, Cisco Systems (CSCO) bought 6.4% of its shares in February (6.4%), and Norfolk Southern purchased 14.6% of its shares ($10 billion) in March.

In some cases, a buyback may not be the best way for companies to build value for shareholders:

It may not be the best use of cash. Long-range growth and building future profits come from investing in company growth, not company stock. Stockholders may prefer, depending on available opportunities for the company and other variables, that the company take a longer-term view. Stock buybacks create quick price gains but may not be the best long-term use of cash. Also, cash for a potential unforeseen challenge to the company could be comforting to some investors, depending on the situation.

When interest rates are low, companies increase their debt-financed share buybacks. In the years just prior to the pandemic, up to half of all buybacks were financed using the low-interest rates at the time. Below-average interest rates incentivized companies to borrow money to spend on share buybacks to boost stock prices. Depending on the scenario, this debt on the balance sheet may long-term weigh on shareholders.

Take Away

Profitable public companies may add value for investors through a stock buyback, also known as share buyback or share repurchase program.

If you are invested in Tesla or another company that may announce a share repurchase program, is this something to be happy about? As a rule, if a public company is profitable, has the cash to spare and its shares are relatively undervalued, then a buyback could be a positive, especially short term.

However, if the company is repurchasing shares of stock while it stymies future growth potential, it could cost long-term investors.

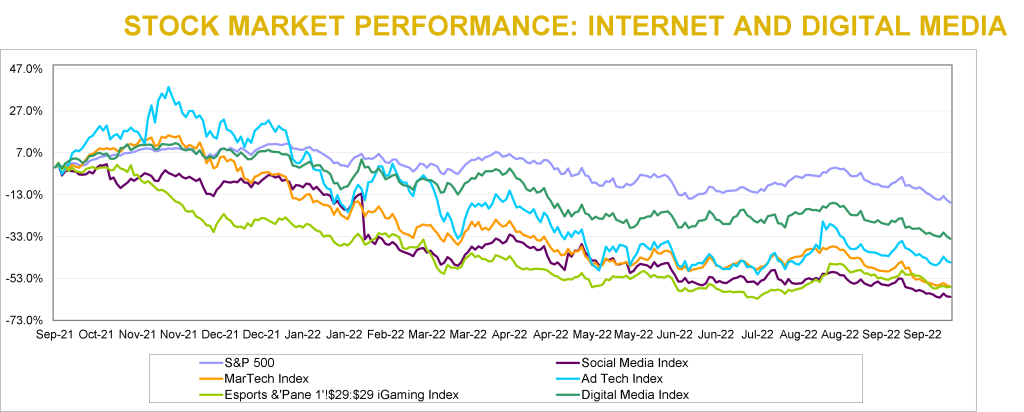

Internet and Digital Media stocks declined for the fourth consecutive quarter in a row. It wasn’t all bad, as two of Noble’s Internet and Digital Media Indices outperformed the broader market (which we define as the S&P 500). Noble’s Ad Tech (+7%) and eSports & iGaming (+7%) Indices each finished up for the quarter, and significantly outperformed the S&P 500 Index in the process, which decreased by 5% in 3Q 2022. These two sectors also materially outperformed Noble’s other Internet & Digital Media subsectors, including Noble’s Digital Media Index (-10%); Social Media Index (-15%) and MarTech Index (-16%).

Noble Indices are market cap weighted, and we attribute the relative strength of the Ad Tech Index to The Trade Desk (TTD), the Ad Tech sector’s largest market cap company, whose shares were up 42% during the quarter. Other notable performers were Digital Media Solutions (DMS; +73%) which announced a deal to be taken private, and Zeta Global (ZETA; +46%), whose 2Q results significantly exceeded guidance. Despite the relative strength of the sector, returns were not broad-based: only 9 of the 23 stocks in the Ad Tech sector were up during the quarter.

The relative strength of Noble’s eSports and iGaming sector was also driven by the largest cap stocks in the sector. Shares of Draft Kings (DKNG) increased by 30% while shares of Flutter Entertainment (ISE:FLTR), the owner of FanDuel, increased by 17%. Shares of sports betting stocks have been battered this year as investors have become skeptical of the time it might take for these companies to reach profitability amidst a backdrop of a slowing economy and consumer propensity to spend.

Year-to-date, FLTR shares are down 19% while DKNG shares are down 45%. Shares are down even more relative to their highs reached in 4Q 2020. Like the Ad Tech sector, the eSports & iGaming sector’s relative strength was not broad-based: only 4 of the 16 stocks in this sector were up during the third quarter, and all of stocks in the sector are down year-to-date.

The worst performing sector was the MarTech sector, which is also the least profitable sector, which likely explains the sector’s underperformance. Only 4 of the 24 companies we monitor in this sector generate positive EBITDA, and investors migrated away from unprofitable growth stocks towards more profitable companies or defensive sectors that might withstand a recession better. Investors would clearly like to see companies in this sector accelerate their path to profitability, and most companies in the sector are responding accordingly. To be fair, some of the companies that aren’t EBITDA positive do generate positive cash flow from operations, which is a quirk of SaaS software accounting. Of the two dozen companies in this sector, the only stock that was up during the quarter was Harte-Hanks (HHS), whose shares increased by 68%. HHS continues to generate improved operating results while lowering its debt and pension obligations.

MarTech stocks have also been victims of their own success. Earlier this year the group traded at average revenue and EBITDA multiples of 8.5x and 70.8x, respectively. Today the same group trades at average revenue and EBITDA multiples of 4.5x and 30.1x, respectively. Stocks like Shopify (SHOP), and Hubspot (HUBS) entered the year trading at 22.2x and 14.7x 2022E revenues, respectively, and now trade at 5.3x, and 7.7x, respectively. Some of this appears to be a Covid-related hangover: when Covid hit, retail companies needed to emphasize their online channels, and companies like Shopify benefited. As consumers return to stores, growth has moderated. Shopify aside, the broader message investors seem to be sending is that recurring revenues are great, but not if they are paired with EBITDA losses at a time when economy appears to be heading into a potential recession.

M&A Continues to Hold Up Well Despite Macro Headwinds

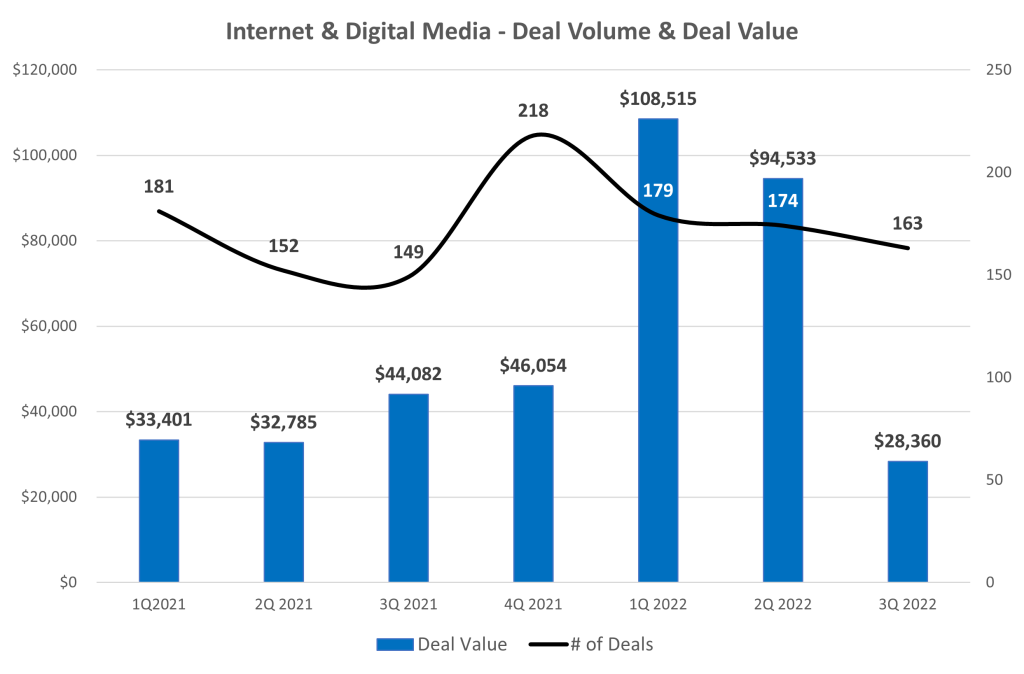

Overall, we are impressed with the resiliency of the M&A marketplace in the Internet & Digital Media sectors. Despite a background that includes public equity market volatility, Fed rate hikes, persistent inflation, contractionary monetary policy, and geopolitical conflict, the M&A marketplace has held up relatively well, all things considered. Noble tracked 163 transactions in the third quarter of 2022 in the TMT sectors we follow, a 9% increase compared to the third quarter of 2021, when we tracked 150 deals, and 6% sequential slowdown compared to 2Q 2022, when we tracked 174 transactions. Year-to-date, the number of M&A transactions is up 7% vs. the year ago period, with 516 announced transactions this year compared to 483 transactions announced through the end of last year’s third quarter.

The real difference between 2022 and 2021 is the dollar value of transactions. Total deal value in 3Q 2022 fell by 36% to $28.4 billion, down from $44.1 billion in 3Q 2021. On a sequential basis, the $28.4 billion in deal value represents a 70% decrease from 2Q 2022 levels of $94.5 billion, nearly half of which reflects Elon Musk’s $46 billion offer to acquire Twitter (TWTR).

In looking at the M&A trends in the chart on the previous page, the biggest change is not the number of deals, but primarily the number of mega-deals. There was only one transaction in 3Q 2022 that was greater than $10 billion dollars: Adobe’s $19.4 billion acquisition of Figma, a collaborative all-in-one design platform. This decline in larger deal activity suggests acquirers are becoming more cautious about making big bets in the current environment or it could also mean that arranging for financing to close on larger deals is becoming more challenging. No doubt the cost to incur debt to close on transactions today are higher than they were just a few months ago, which lowers the return on debt financed M&A transactions. Referencing the Twitter deal again, according to media reports, Apollo Global Management and Sixth Street Partners, which had agreed to provide financing for the Twitter deal when it was first announced in April, are no longer in talks with Elon Musk to provide financing.

From a deal volume perspective, the most active sectors we tracked were Marketing Tech (44 deals), Digital Content (43 deals) and Agency & Analytics (28 deals) and Information (25 deals). From a deal value perspective, the largest transaction was Adobe’s nearly $20 billion acquisition of Figma, a collaborative design software company. Other active sectors were Marketing Tech ($4.9 billion), Information ($1.1 billion, and Digital Content ($1.1B).

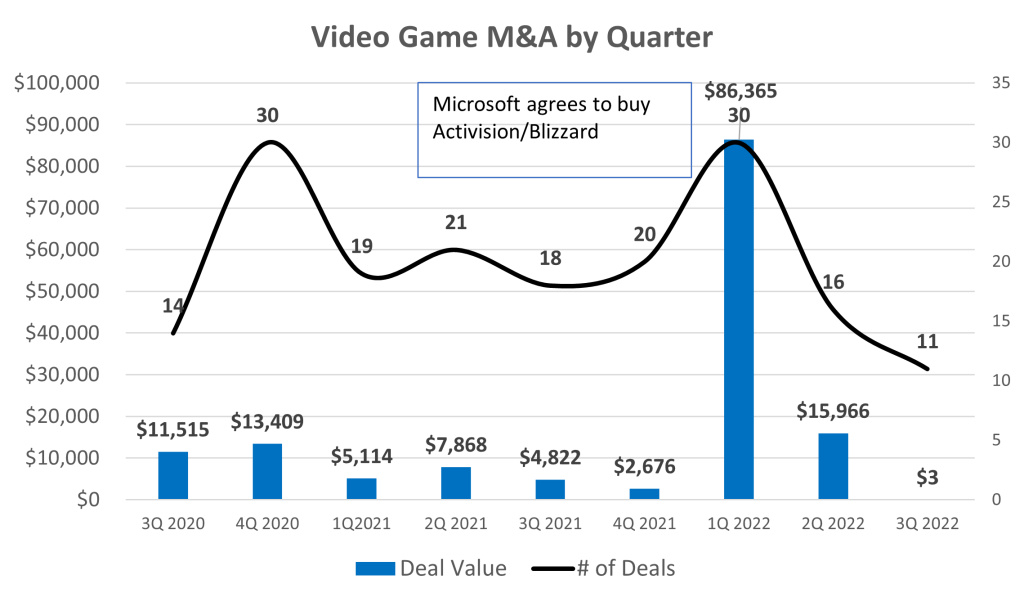

Video Game M&A Declines Precipitously

For the last several quarters we have noted how strong M&A activity was in the current quarter. Perhaps the biggest surprise of the third quarter M&A analysis was the steep drop in M&A in North America in the video gaming sector. Interest in the video gaming sector exploded at the onset of the pandemic as work form home edicts resulted in less commuting time and more time playing video games. As the pandemic has subsided and consumers return to work, the sector has faced difficult comparions, and growth has been challenged.

As shown in the chart below, over the last several quarters, the sector had averaged 21 deals per quarter and $18+ billion in deal value. In the third quarter, there were only 11 announced transactions, and only one with a transaction price announced, resulting in just $3 million of deal value. Perhaps there is some consolation in that the second largest transaction in 3Q 2022 was a gaming related transaction: Unity Software’s agreement to buy IronSource Ltd, a lead generation platform for in-game advertising, for $4.4 billion.

While we expect M&A transactions to moderate given the difficult economic backdrop and an increase in the cost of financing transactions, we expect M&A marketplace to remain resilient. In our discussions with management teams in Internet & Digital Media sectors, we are struck by how many companies believe that industry consolidation is either beneficial or necessary. Scale is widely seen as a panacea to potential slowing or declining revenue trends.

iGaming

The following is an excerpt from a recent note by Noble’s Media Equity Research Analyst Michael Kupinski

The past year has been tough on the iGaming industry. The Noble iGaming Index is down nearly 54% versus a negative 17% for the general market, as measured by the S&P 500 Index. In the latest quarter, the iGaming stocks seemed to have stabilized, up 2% versus a continued general market decline, down 5% for the general market. Interestingly, the iGaming sector was the best performing sector among the Entertainment and Esports sectors, which were up a modest 1% and down 38%, respectively.

The shares of Codere Online (CDRO) could not fight the headwinds of the industry-wide selling pressure. CDRO shares dropped 70% from its post de-SPACing in December 2021. The weakness in the shares has been in spite of the company executing on its growth strategy as planned and maintaining its fundamental pace to meet full-year guidance. In the latest quarter, the shares drifted lower (-4%) versus the industry which increased 2%.

The poor performance of the iGaming industry in many respects is due to the developmental nature of the industry. Many of the companies included in the Noble iGaming index do not generate positive cash flow, with balance sheets supporting growth investment. Certainly, there will be a shake-out of players in the industry that do not have the financial capability to invest for growth, but we believe that Codere Online is one of the survivors.

Although the company is not yet cash flow positive, its operations in Spain generated its highest quarterly cash flow since Q2 2020. Adj. EBITDA in Spain was $3.6 million, enough to offset 87% of the $4.1 million adj. EBITDA loss from the company’s operations in Mexico. Interestingly, the marketing restrictions in the country came with a silver lining of lower competition. This is because the restrictions make it harder for newer operators to establish their brands in the country. Additionally, the lower marketing costs contributed to the strong cash flow generation. Notably, management expects similar cash flow generation going forward for the Spanish operations. We view the situation in Spain favorably as the consistent cash flow profile will help fund the expansion in Latin America and have a mitigating impact on the company’s cash burn.

eSports

The Esports industry had a difficult year and a difficult quarter in terms of stock performance. The horrible stock performance does not reflect the overall industry trends. Video gaming is still on the rise. It is estimated that there are 2.7 billion gamers worldwide, expected to achieve an estimated 3.0 billion gamers in 2023, based on Newzoo’s numbers. The video game market is expected to reach $159.3 billion this year and grow to $200.0 billion in 2023. So, what about the Esports industry? Esports viewership was elevated during the Covid lockdowns, with viewership significantly higher. Viewership trends are expected to increase even from the elevated 2020 levels to over 640 million viewers in 2025.

TRADITIONAL MEDIA COMMENTARY

The following is an excerpt from a recent note by Noble’s Media Equity Research Analyst Michael Kupinski

Overview

Downward trends, but some bright spots

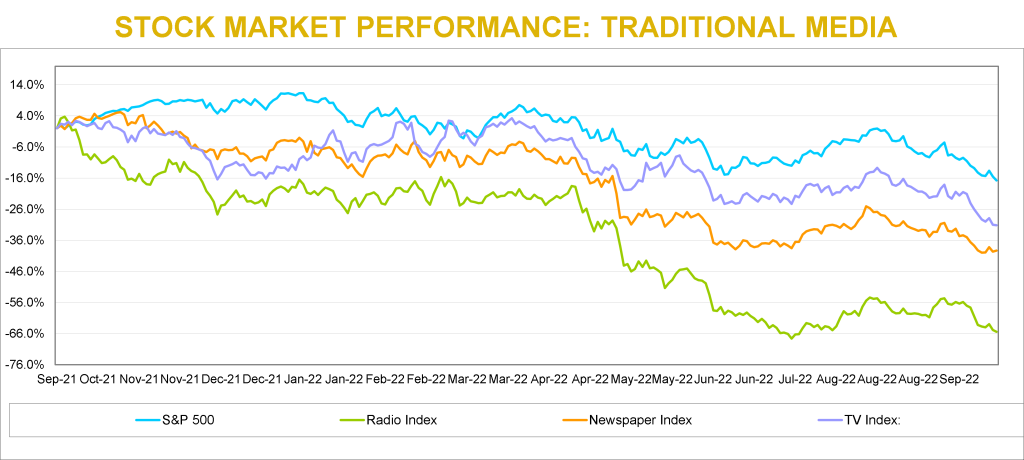

Traditional Media stocks have had tough sledding this year. All of Noble’s Traditional Media Indices have declined over the past 12 months and each have underperformed the general market. The downward spiral seemed to have moderated somewhat in the third quarter.

Notably, during the third quarter, many of the stocks had a very nice bounce before resuming a downward trend. At one point in the latest quarter, stocks were up as high as 30% from the second quarter end. It is important to note that only the Publishing stocks outperformed the general market in the latest quarter.

Broadcast Television

Will Political Carry The Quarter?

Noble’s TV Index dropped 10% in the third quarter, underperforming the broader market (-5%) As we indicated in our previous quarterly report, we believe that there would be a trading opportunity in media stocks. The latest quarter stock performance indicated that. Many of the TV stocks had a strong performance from the end of the second quarter (June 30) to highs achieved in August. Many of the TV stocks increased a strong 25% on average. It is instructive to know that E.W. Scripps had the largest advance from June 30 lows, up 31% to highs achieved August 16. When the industry is in favor, the shares of E.W. Scripps tends to outperform its industry peers. The shares of Entravision (EVC) were the next best performing within the quarter, up 30%, before trading lower and ending down 12%.

TV stocks were challenged by macro-economic pressures such as inflation, the rising cost of borrowing, and a Fed determined to curb inflation by slowing the economy. In the end, interest rate increases by the Fed curbed enthusiasm for TV stocks and the Noble TV Index ended the third quarter down.

The average television company reported 11% revenue growth in the latest quarter. Most broadcasters were very optimistic about political advertising, with some raising forecasts to be near the levels of the Presidential election, a highwater mark. We would note that Entravision had the highest revenue performance in the quarter, up 24%, as the company continues to benefit from its transition toward faster growth digital advertising, which now accounts for over 80% of its total company revenues.

EBITDA margins were healthy, with the average margin for the industry at 25.5%. It is notable to mention that Entravision’s margins appear to be significantly below that of the industry at 10%. Its digital advertising business is a rep firm business, and, as such, the company reports revenues on a net basis and not gross revenues. While a rep firm business tends to be a lower margin business, the accounting treatment for rep revenues gives the appearance of very low margins. The company is in a strong cash flow and free cash flow position.

Most companies will be reporting third quarter financial results in the first two weeks in November. We believe that the third quarter will reflect an influx of political advertising, even though the lion share of the political advertising likely will fall in the fourth quarter. Consequently, we believe that the third quarter revenue growth will be better than the second quarter, showing some acceleration. With signs of weakening national advertising, and a likely weakening local advertising environment in some larger markets, broadcasters are looking forward toward Q4 political advertising as an offset. Many broadcasters indicated that political advertising may be at record levels in 2022, even higher than the Presidential election year of 2020. Political advertising, however, is not usually evenly spent across all markets. As such, there may be winners and some disappointment.

Investors are not encouraged to buy a Television broadcaster on the basis of the upcoming fourth quarter political advertising influx. There are broader issues at play, like cord cutting, slowing retransmission revenue growth, and the prospect for a weakening economy. We believe broadcasters with minimal emphasis on national advertising, a larger focus on small to medium size markets and local advertising, are best positioned to weather an economic downturn. We also like companies that do not have high debt leverage. In addition, we like diversified companies that can benefit from cord cutting, like E.W. Scripps, or have diversified revenue streams and large fast growing digital businesses, like Entravision.

Broadcast Radio

Polishing its tarnished image

One of the epic fails of the radio industry has been Audacy (AUD), once one of the leadership companies in the industry. AUD shares are down a staggering 95% from highs in March 2021. The poor stock performance reflects the poor revenue and cash flow performance and high debt levels at the company. Recently, the company announced that it plans to sell some of its prized assets, including its podcasting business, Cadence 13, in an effort to more aggressively pare down debt.

While Audacy struggles, there are emerging leaders in the industry, many that are not focused on its radio business. The average radio revenue grew 8.9%. Companies that were at the top of the list of revenue growth had diversified revenue streams. Townsquare Media (TSQ) was the best performer, with Q2 revenue growth of 13.6%. We believe that Townsquare also benefits from significantly lower national advertising and concentration on less cyclical larger markets. Other diversified companies that performed better than the lower growth companies in the group were Salem Media and Beasley Broadcasting. Salem Media has diversified into content creation and digital media and Beasley recently accelerated its push into Digital Media. Separately, Beasley recently announced a station swap with Audacy, which will enhance its position in with its four existing stations in Las Vegas.

On the margin front, Townsquare Media also was among the leaders in the industry. Notably, Townsquare Media’s digital business carries margins similar to its radio businesses, near 30%. As such, its investments in Digital Media are not depressing its total company margins. Townsquare’s Q2 adj. EBITDA margins were 27%, well above that of the larger industry peers like iHeart (25%), Cumulus Media (19%), and Audacy (12%).

In looking forward toward the upcoming third quarter results, which will be released in coming weeks, we believe that the effects of rising inflation and weakening economy will start to show. Many of the larger broadcasters which focus on larger markets, have national network business, may disappoint. In addition, we believe that there will be spotty political advertising performances. In our view, the resulting potential weakness in the stocks may create an opportunity to more aggressively accumulate or establish positions.

Radio stocks largely mirrored the performance of the TV industry, falling 9% in the third quarter. Last quarter we pointed out that large industry players such as Audacy and iHeart had an outsized negative impact on the market cap-weighted index. This was due to the stocks being downgraded by a Wall Street firm on the basis of high leverage in a time of recession.

However, there are several broadcasters in the radio industry with improving leverage profiles. Furthermore, we believe that in a time when traditional radio companies are making a transition to more digitally based revenue sources, investors would do well to differentiate among them on that basis as well. In our view, certain companies are ahead of peers in the digital transformation and are better shielded from certain fundamental headwinds that have traditionally plagued radio broadcasters in prior recessions, such as Townsquare Media (TSQ), Salem Media (SALM), and Beasley Broadcasting (BBGI).

Publishing

Once a leader, now a laggard

It is hard to believe that Gannett was once a $90 stock and held a record for one of the longest strings of quarterly earnings gains in the S&P 500 Index. The shares are down 80% from year earlier highs to near $1.37. For some anti newspaper investors, this is a “told you so” moment. But, this view missed notable exceptions, like the New York Times, which seemed to transition more quickly toward digital revenues. There are publishers that are set apart from the weak trends at Gannett and are on a favorable trajectory toward a digital future. As such, we believe that investors should not throw the baby out with the bathwater or avoid the industry. There are gems here, which is discussed later in this report.

There were sizable differences in the financial performance of the companies in the publishing group.Q2 publishing revenue declined on average 1.5%. The notable exceptions to this performance was The New York Times, up 11.5%, News Corp, up 7.3%, and Lee Enterprises, down a modest 0.7%. The improved performance into the ranks of the leaders in the industry is quite notable. Lee’s digital subscriptions currently lead the industry. The company has exceeded all of its peers in terms of digital subscription growth in the past 11 consecutive quarters. Furthermore, over 50% of its advertising is derived from digital. Currently, roughly 30% of the company total revenues are derived from digital, still short of the 55% at The New York Times, but closing the gap.

Not only is Lee performing well on the digital revenue front, it has industry leading margins. Lee’s Q2 EBITDA margins were 12%, in line with News Corp and second only to the New York Times at 17%. We believe that margins should improve over time as the company continues to migrate toward a higher digital margin business model.

Noble’s Publishing Index, which decreased a modest 2% in the quarter, outperforming the S&P (-5%). The relatively favorable performance of the index was primarily due to its largest constituents, News Corp. and The New York Times, which rebounded from -30% and -39%, respectively in Q2, to -3% and +3%, respectively, in Q3. The average percentage change of the stocks in the industry was -16%, more in line with Traditional Media as a whole. One of the poor performing stocks in the index for the quarter was Gannett (GCI) which declined 47%. It was recently reported that the company implemented austerity measures included unpaid leave and voluntary layoffs. In the case of Lee Enterprises, the shares were down a much more modest 7%, more in line with the general market.

LEE shares trade at an average industry multiple of 5.8 times Enterprise Value to our 2023 adj. EBITDA estimate. Notably, the company is closing the gap with its Digital Media revenue contribution to that of New York Times, which is currently trading at an estimated 14.5 times EV to 2023 adj. EBITDA. We believe that the valuation gap with the New York Times should close as well. In recent Lee Enterprise news, a buyout specialist investor filed a 13D and indicated interest in taking the company private. While financial players continue to circle the wagons for Lee, we believe that investors should take note.

This newsletter was prepared and provided by Noble Capital Markets, Inc. For any questions and/or requests regarding this news letter, please contact Chris Ensley

DISCLAIMER

All statements or opinions contained herein that include the words “ we”,“ or “ are solely the responsibility of NOBLE Capital Markets, Inc and do not necessarily reflect statements or opinions expressed by any person or party affiliated with companies mentioned in this report Any opinions expressed herein are subject to change without notice All information provided herein is based on public and non public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on their own appraisal of the implications and risks of such decision This publication is intended for information purposes only and shall not constitute an offer to buy/ sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice Past performance is not indicative of future results.

Please refer to the above PDF for a complete list of disclaimers pertaining to this newsletter

Could This Week’s Economic Data Impact November’s FOMC Meeting?

There are three economic releases investors will focus on this coming week. These will provide information on housing, manufacturing, and how the economy in each Federal Reserve District is doing (Fed’s Beige Book).

Moving out a little further on the calendar, expectations for another 75 basis point rate hike at the November 1-2 FOMC meeting are widely held. The confidence in the Fed move, even though two weeks away, can be attributed to higher-than-expected inflation reports last week and the constant pounding of the drum by Fed policymakers, saying that taming inflation will remain the FOMC’s priority.

What’s on Tap for investors:

Monday 10/17

8:30 AM Empire State Manufacturing Index, will be reported. Expectations are for manufacturing to have shrank -2.5%. The Empire Manufacturing Survey gives a detailed look at how busy New York state’s manufacturing sector has been and where things are headed. Since manufacturing is a major sector of the economy, this report has a big influence on the markets. Some of the Empire State Survey sub-indexes also provide insight into commodity prices and inflation. The bond market can be sensitive to the inflation ramifications of this report. The stock market pays attention because it is the first clue on the U.S. manufacturing sector, ahead of the Philadelphia Fed’s business outlook survey.

8:45 Noble Capital Markets’ Michael Kupinski, Director of Research, provides indepth report on current state and outlook of the Digital Media segment of the Media and Entertainment sector.

Tuesday 10/18

10:00 AM Housing Market Index will be released. Expectations are for the number to be 44, down from 46 the prior month. The housing market index has consistently been lower than expectations, including September’s 46, which was an 8-year low. N.Y. Fed 5-year inflation expectations for one- and three-year-ahead inflation expectations had posted steep declines in August, from 6.2 percent and 3.2 percent in July to 5.7 percent and 2.8 percent, respectively. Investors will be watching to see if the declining expectations continue. The housing market index is a monthly composite that tracks home builder assessments of present and future sales as well as buyer traffic. The index is a weighted average of separate diffusion indexes: present sales of new homes, sales of new homes expected in the next six months, and traffic of prospective buyers of new homes.

9:45 AM Industrial Production has three components that could impact thoughts on the economic trend. Industrial Production as a whole is expected to have risen 0.1% versus down -0.2% in the prior period. Manufacturing output is expected to have risen by 0.2%, and Capacity Utilization is expected to be unchanged at 80%.

Industrial production and capacity utilization indicate not only trends in the manufacturing sector but also whether resource utilization is strained enough to forebode inflation. Also, industrial production is an important measure of current output for the economy and helps to define turning points in the business cycle (start of recession and start of recovery).

Comtech Telecommunications (CMTL) with Noble Capital Markets in NYC in-person roadshow for investors. Interested parties can find out more at this link.

Wednesday 10/19

7:00 AM Mortgage Applications. The composite index is expected to show a decline of -2.0% for the month. The purchase applications index measures applications at mortgage lenders. This is a leading indicator for single-family home sales and housing construction.

8:30 AM Housing Starts and Permits. The consensus for starts is 1.475 million (annualized), and Permits are expected to come in at 1.550 million (annualized). Housing starts to measure the initial construction of single-family and multi-family units on a monthly basis. Data on permits provide indications of future construction. A housing start is registered at the start of the construction of a new building intended primarily as a residential building.

2:00 PM, the Beige Book will be released. This report is produced roughly two weeks before the Federal Open Market Committee meeting. In it, each of the 12 Fed districts compiles anecdotal evidence on economic conditions from their districts. It is widely used in discussions at the FOMC monetary policy meetings where rate decisions are made.

EIA Petroleum Status Report. The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products, this has been a big focus for investors because of its implications for prices.

Thursday 10/20

8:30 AM Jobless Claims for the week ending 10/15. Claims are expected to be 235 thousand. Jobless claims allow a weekly look at the strength of the job market. The fewer people filing for unemployment benefits, the more they have jobs, and that sheds light for investors on the economy. Nearly every job comes with an income that gives a household spending power. Spending greases the wheels of the economy and keeps it growing.

8:30 AM Philadelphia Fed Manufacturing Index. This index has been bouncing back and forth between contraction and expansion. It’s the former that’s expected for October, where the consensus is minus 5.0.

10:00 AM Existing Home Sales. The consensus is for sales to have been 4.695 million (annualized). The previous number was 4.8 million. The pace has declined every month since January.

10:00 AM Leading Indicators. The consensus is for a decline of -0.3%. The index of leading economic indicators is a composite of 10 forward-looking components, including building permits, new factory orders, and unemployment claims. It attempts to predict general economic conditions six months out.

Engine Gaming Media (GAME) with Noble Capital Markets in St. Louis in person roadshow for investors. Interested parties can find out more at this link.

10:30 AM EIA Natural Gas Report. This is a weekly report and has gotten much more attention since the war in Ukraine and gas pipeline issues that impact much of Europe. The abundance or lack of energy impacts prices not just for the consumer, but also manufacturers. This report has the ability to move markets as a result.

4:30 PM Fed Balance Sheet. The Fed’s balance sheet is a weekly report presenting a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. This report will allow investors to see how far along the Federal Reserve has gotten on its quantitative tightening program.

Friday 10/21

1:00 PM Baker Hughes Rig Count. The expectation is for 985 in North America and 769 in the U.S. It’s all about potential supply; the count tracks weekly changes in the number of active operating oil & gas rigs. Rigs that are not active are not counted.

What Else

This week the Biden administration has plans to take new steps to lower gasoline prices. This includes potentially releasing more oil from the Strategic Petroleum Reserve and imposing limits on exports of energy products. The initiative comes a week after the Organization of the Petroleum Exporting Countries (OPEC) and its allies agreed to cut oil production by up to 2 million barrels per day.

Corporate earnings season starts to heat up with widely watched names that can set the market tone. Those to watch out for include: Monday – Bank of America, Charles Schwab, Goldman Sachs, Barclays, Johnson & Johnson, Lockheed Martin, IBM, Netflix, United Airlines, American Airlines, Procter & Gamble, and Tesla. Investors can also expect a key GDP release from China and a vital inflation reading from the U.K.

Soaring Inflation Prompts Biggest Social Security Cost-Of-Living Boost Since 1981 – 6 Questions Answered

Social Security is set to boost the benefits it provides retirees by 8.7%, the biggest cost-of-living adjustment since 1981. It comes as sky-high inflation continues to eat into incomes and savings.

The changes are set to take effect in January 2023 and were announced following the release of the September 2022 consumer price index report, which showed inflation climbing more than expected during the month, by 0.4%.

The automatic adjustment will surely come as a relief to tens of millions of retirees and those who receive supplemental security income who may be struggling to afford basic necessities as inflation has accelerated throughout 2022. But an annual adjustment wasn’t always the case – and other government benefits and programs deal with inflation differently.

John Diamond, who directs the Center for Public Finance at Rice’s Baker Institute, explains the history of the Social Security cost-of-living, or COLA, increase, what other benefits are adjusted for inflation and why the government makes these changes.

1. How fast is the cost of living rising?

The latest data, for September, shows average consumer prices are up 8.2% from a year earlier. The monthly gain of 0.4% was double what economists surveyed by Reuters had expected.

More troubling, so-called core inflation – which excludes volatile food and energy prices – gained even more in September, ticking up by 0.6%. Core inflation is a measure that’s closely watched by the Federal Reserve, as it helps show how pervasive and persistent inflation has become in the economy.

2. How are Social Security benefits adjusted for inflation?

Automatic adjustments to Social Security benefits began in 1975 after President Richard Nixon signed the 1972 Social Security amendments into law.

Before 1975, Congress had to act each year to increase benefits to offset the effects of inflation. But this was an inefficient system, as politics would often be injected into a simple economic decision. Under this system, an increase in benefits could be too small or too large, or could fail to happen at all if one party blocked the change entirely.

Not to mention that with the baby boomers – those born from 1946 to 1964 – entering the labor force it was already clear that Social Security would face long-term funding issues in the future, and so putting the program on autopilot reduced the political risk faced by politicians.

Since then, benefits have climbed automatically by the average increase in consumer prices during the third quarter of a given year from the same period 12 months earlier. This is based on a version of the consumer price index meant to estimate price changes for working people and has been rising slightly faster than the overall pace of inflation.

While helpful, these inflation adjustments are backward-looking and imperfect. For example, 2022 Social Security benefits increased by 5.9% from the previous year, even though inflation throughout this year has been significantly higher – which means the higher benefits weren’t covering the higher cost of living. Thus, the 2023 increase in benefits primarily offsets what was lost over the previous year.

A white hand holds a card reading social security

Millions of retirees and other will soon see a big jump in their Social Security benefits. AP Photo/Jenny Kane

3. Are the benefits taxable?

A growing portion of Social Security benefits are taxed in the same way as ordinary income, except at different threshold with various caps and percentages. Only 8% of benefits were subject to taxation in 1984, but that’s climbed to almost 50% in recent years. That percentage will likely continue to increase as the taxable thresholds are not adjusted for inflation.

For example, if an individual filer’s income, including benefits, is below US$25,000, none of that is taxed. But up to 50% of a person’s benefits may be taxed at incomes of $25,000 to $34,000. After that, up to 85% of their benefits may be taxed.

Such a big increase in Social Security benefits likely means some people who paid no tax will now have to pay some, while others will see larger increases in their tax liability.

4. Why does the government adjust benefits for inflation?

Rapid gains of inflation, like the kind the U.S. and many other countries are currently experiencing, can have significant impacts on the finances of households and businesses.

For example, it might mean seniors cutting back on heating or food. Government policies generally try to account for this to reduce the negative impacts that rising prices can have on those with limited or fixed resources.

In addition, reducing the impacts of price changes creates a more efficient and fair allocation of resources and reduces the arbitrary outcomes that would otherwise occur.

5. What other government programs typically get a COLA?

Other government programs and benefits also increase to account for inflation.

The U.S. Department of Agriculture estimates the cost of its Thrifty Food Plan each June and adjusts Supplemental Nutrition Assistance Program or SNAP benefits – formerly known as food stamps – in October of each year. Beginning in October 2022, food stamp benefits rose by 12.5%, which helps make up for the largest increases in food prices since the 1970s.

In addition, the federal poverty level is adjusted for changes in the consumer price index annually by the Department of Health and Human Services, an adjustment that affects a number of government-provided benefits, such as housing benefits, health insurance and others, including SNAP benefits.

6. Does the tax system also adjust for inflation?

While some aspects of the tax code adjust for inflation, others do not.

For example, income tax bracket thresholds, the size of the standard deduction, alternative minimum tax parameters and estate tax provisions all increase annually for inflation. That means come tax filing season next year, U.S. tax filers will likely see big changes in all these items.

But examples of provisions that are not adjusted for inflation include the maximum value of the child tax credit and the $10,000 cap on the deduction of state and local taxes. In addition, the threshold that determines who is liable for the net investment income tax – the additional 3.8% tax on investment and passive income for taxpayers above a certain income level – doesn’t adjust, which means each year more individuals are subject to it.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of John W. Diamond, Director of the Center for Public Finance at the Baker Institute, Rice University.

MOTORSPORT GAMES’ LATEST INSTALLMENT OF THE NASCAR GAMING FRANCHISE COMBINES ASPECTS OF RACING RIVALRIES INTO A SINGLE USER EXPERIENCE

MIAMI, Oct. 14, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world, announced today the launch of NASCAR Rivals, exclusive for Nintendo Switch consoles. The officially licensed video game of the 2022 NASCAR Cup Series season, this latest installment of the video game franchise combines the thrill of the NASCAR Cup Series with the intensity of motorsports rivalry to fans everywhere. NASCAR Rivals is available starting today across leading retailers and the Nintendo eShop for $49.99. A link to the trailer can be found here.

NASCAR Rivals brings the excitement of the NASCAR Cup Series regular season and playoffs to fans on the go with the Nintendo Switch’s easy, built-in mobility. The game’s variety of race modes provide players the ability to race and compete in different ways, emphasizing rivalry across the sport itself and among teams in the NASCAR Cup Series, drivers and the players, both locally and via multiplayer. All of the tracks, cars, drivers and teams from the 2022 NASCAR Cup Series regular season and playoffs are included. Modes available to play include ‘Race Now,’ ‘Career Mode,’ and an exciting ‘Challenges’ mode, which incorporates sequences based on real-life-on-track events to test players’ resilience and see if they have what it takes to navigate the selected scenarios.

“As we continue to build new ways to bring the NASCAR Cup Series to life, our goal with NASCAR Rivals was to highlight a pertinent component of all motorsports, the competition,” said Jay Pennell, Brand Manager, NASCAR, at Motorsport Games. “This latest offering not only lets fans challenge their own skills, but compete against their friends, other online players, and challenges within the sport itself. We’re excited for our fans to truly immerse themselves in what it means to be a NASCAR champion, while allowing them to embrace their inner rival wherever and whenever.”

The game’s numerous ‘Multiplayer’ functions offer players varying ways to challenge each other on the track. In ‘Split Screen’ mode, friends can race against each other locally using the Nintendo Switch Joy Cons. In ‘Online Multiplayer’ users will be able to compete against up to 15 other players anywhere in the world via Nintendo Switch Online. Additionally, newly-added creative elements in NASCAR Rivals give players the opportunity to create custom and unique schemes with an enhanced ‘Paint Booth,’ in addition to their driver avatars with a variety of appearances, sponsor logos and more to truly curate an experience around their own legacies in the game.

Motorsport Games developed NASCAR Rivals as an elevated experience for fans to fully embrace the intensity and thrill of NASCAR with the unlimited portability of the Nintendo Switch console. NASCAR Rivals gives gamers and fans alike the ability to pick up the NASCAR experience anywhere they desire to hone their skills and take on the competition one by one.

NASCAR Rivals is now available at all leading retailers and for download on the Nintendo eShop for $49.99.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. RFactor 2 also serves as the official sim racing platform of Formula E, while also powering Formula 1™ centers through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements: Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. These forward-looking statements include, but are not limited to, statements concerning the timing, participants and expected benefits of the NASCAR Rivals game and related products and updates. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation: difficulties, delays in or unanticipated events that may impact the timing and expected benefits of the NASCAR Rivals game and/or related products and updates, such as due to unexpected release delays. Factors other than those referred to above could also cause Motorsport Games’ results to differ materially from expected results. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date. Additionally, the business and financial materials and any other statement or disclosure on, or made available through, Motorsport Games’ website or other websites referenced or linked to this press release shall not be incorporated by reference into this press release.

Website and Social Media Disclosure: Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

CHELMSFORD, MA / ACCESSWIRE / October 14, 2022 / Harte Hanks Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for nearly 100 years, will be a featured presenter on a panel program and discussion at the upcoming Reuters Strategic Marketing Conference.

The Harte Hanks panel presentation, “Gen Z & The Rise of Digital Commerce,” will examine how leading-edge digital marketers are leveraging data and analytics to fully engage with Gen Z customers, the largest and most influential consumer segment shaping brand performance.

A featured speaker, Harte Hanks’ Chief Analytics Officer, Dan Rubin, will discuss specific methods of how smart data and analytics can drive better reach and engagement with this key audience. “We’ll offer key insights on how to facilitate an e-commerce shopping experience that moves Gen Z customers seamlessly through the purchase funnel,” Mr. Rubin noted. Mr. Rubin will also share effective strategies for creating authentic, organic content that engages Gen Z and creates a shared sense of purpose with a brand.

With over 20 years of analytics and CRM experience, Mr. Rubin was one of the founding members of the Harte Hanks Analytics team. Dan’s analytics expertise spans across many different clients and across all industries, including retail, banking, gaming, automotive, high-tech/B2B, travel/entertainment, pharmaceutical and packaged goods.

The Reuters Strategic Marketing Conference 2022, on October 21-22, will bring together leaders from the world’s most influential brands to define the future of marketing. The global platform is designed to empower marketing leaders with the tools they need to ensure their brands are engaging with modern audiences with human-first data strategies.

In addition, Harte Hanks will be an exhibitor in the Reuters Customer Service and Experience Conference and Expo at the Brooklyn Bridge Marriott on October 18-19, 2022, featuring a range of leading brands including M&T Bank, IHG Hotels & Resorts, UPS and Citizens Financial Group, among others.

About Harte Hanks:

Harte Hanks (Nasdaq: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe and Asia Pacific.

Partnership allows Awin and ShareAsale’s 21,000 retailers to leverage a market proven influencer relationship management platform in Sideqik

NEW YORK, NY / ACCESSWIRE / October 14, 2022 / Sideqik (“Sideqik”), the end-to-end influencer marketing platform that enables brands to build scalable, repeatable and predictable revenue engines, a wholly-owned subsidiary of Engine Gaming and Media, Inc. (NASDAQ:GAME)(TSXV:GAME), today announced a partnership with Awin and ShareASale, the fastest-growing affiliate marketing platforms in North America.

Sideqik’s database of over 60 million influencers across the 10 most popular social networks will allow Awin’s 21,000 retailers to better identify relevant, brand-safe influencers, streamline relationship management and grow their sales and customer base, simultaneously leveraging Sideqik’s robust, AI-powered database, providing actionable insights and real time reporting throughout the whole influencer marketing lifecycle.

“Across the industry, there is a growing demand from consumer brands to execute more profitable, better measured influencer marketing campaigns,” said Joris Cretien, Partner Growth Director at Awin. “Awin and ShareASale’s integration with Sideqik allows our brands to identify and manage influencer partnerships, deploy spend at scale and report on the return – a critical element for smaller businesses with tighter budgets – all through Sideqik’s robust tool set.”

“Sideqik, Engine’s influencer relationship management platform, is gaining adoption as part of mainstream marketing strategies for companies of all sizes,” commented Lou Schwartz, CEO, Engine Gaming & Media. “Our partnership with Awin and ShareASale unlocks a substantial number of retailers looking to leverage a market proven platform with expertise in supporting both affiliate sales and expansion of consumers through social media channels. We are excited to support the growth and scaling of these businesses.”

About Sideqik

Sideqik is an influencer marketing platform that offers brands, CPG, direct marketers, and agencies tools to discover, connect and execute marketing campaigns with content creators. Sideqik’s end-to-end solutions offer marketers advanced capabilities to discover influencers with demographic and content filtering; connect and message influencers; share marketing collateral such as campaign briefs, photos, logos, videos; measure reach, sentiment, and engagement across all major social media platforms; and evaluate earned media value and ROI across the entire campaign.

Awin is a marketing technology platform, providing an open marketplace for businesses to create any type of acquisition partnership. Together with ShareASale, the platforms’ 240,000+ partners – including traditional affiliates, global mass media houses, trusted micro-influencers and innovative fintech businesses – enable advertisers to generate more sales, expand customer reach and strengthen their brand. Retailers that migrate to the Awin Group from competitor platforms experience triple-digit affiliate program growth and a 63% uplift in revenue. In addition to leading the way with our reach, Awin and ShareASale’s award-winning technology and tools – including first-party tracking, multi-channel attribution and in-app tracking – ensure a program tracks all sales, making it optimally attractive for partners to want to promote.

Engine Gaming and Media, Inc. (NASDAQ:GAME) (TSX-V:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Company Contact: Lou Schwartz 647-725-7765

Investor Relations Contact: Shannon Devine MZ North America Main: 203-741-8811 GAME@mzgroup.us

Shareholder Conference Call and Webcast will be held on Wednesday November 16th, 2022

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (NYSE American: SMTS) (BVL or Bolsa de Valores de Lima: SMT) (“Sierra Metals” or the “Company”) will release Q3-2022 consolidated financial results on Tuesday November 15th, 2022, after Market Close. Senior Management will also host a webcast and conference call on Wednesday November 16th, 2022, at 11:00 am EST. Details of the Conference Call and Webcast are as follows:

Via Webcast:

A live audio webcast of the meeting will be available on the Company’s website:

The webcast along with presentation slides will be archived for 180 days on www.sierrametals.com.

Via phone:

For those who prefer to listen by phone, dial-in instructions are below. To ensure your participation, please call approximately five minutes prior to the scheduled start time of the call.

Canada dial-in number (Toll Free): 1 833 950 0062 Canada dial-in number (Local): 1 226 828 7575 US dial-in number (Toll Free): 1 844 200 6205 US dial-in number (Local): 1 646 904 5544 All other locations: +1 929 526 1599

Access code: 991150

Press *1 to ask a question, *2 to withdraw your question, or *0 for operator assistance

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company with Green Metal exposure including copper production and base metal production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. The Company has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com or contact:

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

InPlay received Toronto Stock Exchange approval for a Normal Course Issuer Bid. Under the NCIB, InPlay may purchase and cancel up to 10% of public float of the shares of IPO on the TSX subject to a daily limit of 25% of the average daily trading volume. At current prices, the buyback would be approximately C$20 million if maxed out. Management believes the buyback is a prudent step given the energy market volatility and its belief that, at times, its stock is undervalued. We would note that the shares of IPO (and IPOOF on the OTC exchange) have declined 40% off of June peak levels despite very positive recent operational developments (see 9/29/2022 report). NCIB approval follows 9/28/22 comments that Board of Directors had approved a share buyback program.

The company has the cash flow and balance sheet to do a share buyback. At current energy price levels, we expect the company to generate approximately C$150 million in Adjusted Fund Flow, far exceeding recently-raised capital expenditures of C$70-72 million (up from C$18 million in 2020). The company has been paying down debt and expects to reduce its net debt to EBITDA ratio to 0.1-0.2 times by the end of 2022 (implying that the current net debt level of C$52 million will be reduced to C$15-30 million). Net debt, which represented 50% of total capitalization as recently as 2020, now represents less than 10% of capitalization. We believe management has adequate cash flow to continue to grow capital expenditures, pay down debt, and still initiate a share repurchase program.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Partners with Meta in Ghana. The company announced that it has partnered with Meta (Facebook) to be its ad agency in the country of Ghana. While this is not a large country, with a potential market opportunity of $10 million, it does set the table for future relationships with Meta in other parts of the world.

Accelerated purchase of Cisneros become clear. Entravision recently accelerated the purchase of Cisneros for a total of $44 million of the remaining 49% interest that it did not own. This would free the company to expand its relationship with Meta to other parts of the globe, outside of its current Latin American market. The recent expansion in Ghana is an example of that.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Pre-clinical in meniscus repair officially begins. ChitogenX announced the second orthopedic indication for ORTHO-R is moving from feasibility studies to formal pre-clinical status, beginning November 2022. Meniscus repair is needed due to acute trauma tears and degenerative tears, but surgical failure rates are currently in the 20%-40% range, offering substantial opportunity for ChitogenX’s platform technology to improve healing outcomes.

Meniscus repair program will test 22 sheep. The sheep will be tested with sutures alone (current standard of care) vs. platelet rich plasma (PRP) alone vs. PRP delivered by ORTHO-R biopolymer. Repair surgeries are scheduled beginning mid-November and should be completed by first of December. Results are expected approximately in 12 months in fall of 2023.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Elon Musk Argues Twitter is Better off Without a Board of Directors – Is He Right?

After a wild ride, it looks like Elon Musk’s bid to buy Twitter will move ahead.

Twitter’s board of directors had sued the Tesla billionaire in July 2022 when Musk tried to terminate the US$44 billion deal. The board has yet to drop its lawsuit to force Musk to complete the buyout, while many parts have been thrown out.

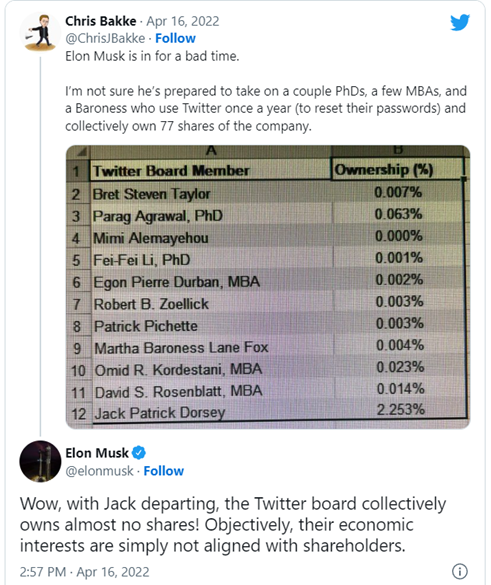

The board has in fact been at the center of this saga since the beginning, when Musk launched his hostile takeover bid while criticizing board members for owning almost no shares of the company they oversee. Twitter founder Jack Dorsey called the board the “dysfunction of the company.”

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Michael Withers, Associate Professor of Business, Texas A&M University, Steven Boivie, Professor of Management, Texas A&M University.

As experts on corporate governance, we believe this feud raised two important corporate governance questions: What purpose does a board of directors serve? And does it matter if a member owns company stock or not?

‘A Bad Board Will Kill’

“Good boards don’t create good companies, but a bad board will kill a company every time.”

Venture capitalist Fred Destin wrote that in 2018, citing what he called an “old Silicon Valley proverb.” The quote has been making the rounds on Twitter recently in light of Musk’s hostile bid. It even seemed to get a nod from Dorsey himself when he replied to a tweet containing the quote with “big facts.”

This tweet and the general conversation that has emerged have important implications for understanding boards and their role in shepherding a company.

Broadly speaking, a board’s most important roles include hiring, paying and monitoring the chief executive officer.

Academic research suggests that board members at large companies – who typically receive generous compensation packages – may be limited in their ability to perform these tasks effectively. In our work, we found that boards often find it impossible to conduct adequate monitoring and rein in wayward CEOs because there’s just so much information for modern boards to process with their limited time. And the social dynamics involved in the board also make it difficult for directors to speak up and oppose other directors.

In a separate study involving face-to-face interviews with directors, we were consistently told that directors take their board service seriously and operate with their companies’ best interests in mind. But they do so with an eye toward collaborating with the CEO and the rest of the executive team rather than serving as impartial observers, as their “independent” status suggests they should.

While our work didn’t focus on this, if the board and the CEO fundamentally disagree about the direction of company – which was often the case between Dorsey and the Twitter board – it would certainly be problematic and could lead to less than optimal decisions being made.

In other words, a board that isn’t functioning effectively can definitely destroy a company’s value. And some reporting suggests that’s what happened to Twitter, whose shares were trading at less than half their 2021 peak before Musk disclosed he had amassed a 9% ownership stake.

A Raider’s Lament