Los Angeles, CA, Nov. 07, 2022 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty) Brands Inc. (Nasdaq: FAT) today announced that it has withdrawn its previously announced proposed registered public offering of shares of its Class A Common Stock as a result of market conditions.

Andy Wiederhorn, the Company’s Chief Executive Officer, said, “This transaction was opportunistic in nature. While we appreciate the significant interest in the proposed offering, we have concluded that the current terms and conditions available in the market were not sufficiently attractive for us to move forward with a transaction at this time. We will continue to monitor market conditions and evaluate whether to pursue another offering in the future.”

This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies including, but not limited to, uncertainties surrounding the severity, duration and effects of the COVID-19 pandemic, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other risks, uncertainties and contingencies. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

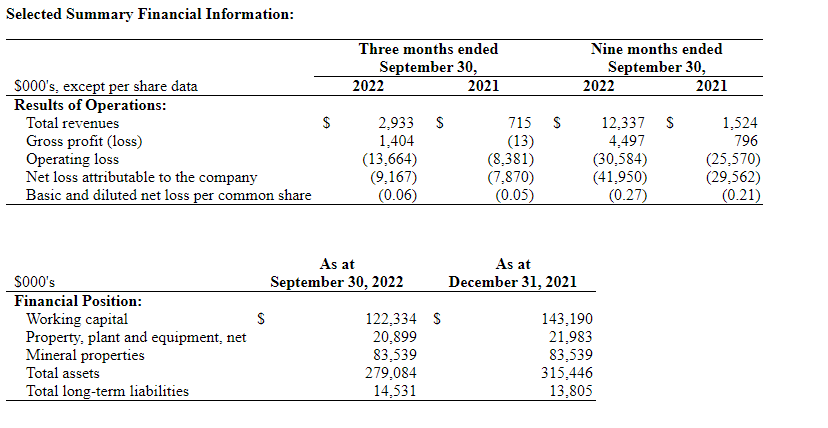

Newrange is focused on district-scale exploration for precious metals in the prolific Red Lake District of northwestern Ontario. The past-producing high-grade Argosy Gold Mine is open to depth, while the adjacent North Birch Project offers additional blue-sky potential. Focused on developing shareholder value through exploration and development of key projects, the Company is committed to building sustainable value for all stakeholders. Further information can be found on our website at www.newrangegold.com .

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Creating a new silver-focused development and production company. Newrange recently signed a definitive agreement with Great Panther Mining Limited (NYSE American, GPL) to acquire a 100% interest in the past-producing Coricancha mine in central Peru. Coricancha is a high-grade, narrow-vein, gold-silver-copper-lead-zinc underground mine in the Central Polymetallic Belt of Peru and will take the stage as the company’s flagship project. It is ninety kilometers east of Lima and includes a 600-tonne per day processing plant, dry-stack tailings storage facility and requisite surface and underground infrastructure.

Acquisition terms. Newrange has agreed to make a single cash payment of US$750,000 to Great Panther upon closing. Because the transaction is on a cash basis, it does not require shareholder approval. Newrange is considering a “one new for six old” share consolidation and subsequent name change to be effective upon closing. Closing is subject to certain conditions, including financing by Newrange, and receipt of all necessary third-party approvals, including by the TSX Venture Exchange.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Business Remains on Track. Information Services Group remains on track to post record revenue and adjusted EBITDA. According to management, demand remains strong for digital services, driving a strong profitable mix of products and services, while ISG continues to see an uptick in demand for its cost takeout services given the uncertain economic environment.

Priming the Pump for Additional Growth. ISG added 56 professionals during the quarter, an increase of 3.8%. The new hires are expected to focus on the higher growth digital and recurring revenue opportunities. During the quarter, ISG serviced 625 clients, including 65 new to ISG, both up from the prior year and quarter-over-quarter.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gray Television is a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets in the United States. Our television stations serve 113 television markets that collectively reach approximately 36 percent of US television households. This portfolio includes 80 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station. We also own video program companies Raycom Sports, Tupelo Honey, PowerNation Studios and Third Rail Studios.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 below expectations. The company reported Q3 revenue of $909 million, 4% below our estimate of $948 million. The revenue variance was due to lower than expected Political advertising. Adj. EBITDA of $336 million was 11% below our estimate of $377 million, surprisingly good given the absence of $50 million in high margin revenue.

Political below forecast. The quarterly miss was due primarily to lower-than-expected Political revenue, $144 million compared with our estimate of $194 million. Political advertising shifted toward some of the tight races in larger markets. Nonetheless, for the first nine months of the year, Political revenue was just 3.5% below the cyclical high Presidential election of 2020, on a combined historic basis.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Eagle Bulk Shipping Inc. (“Eagle”) is a US-based drybulk owner-operator focused on the Supramax/Ultramax mid-size asset class, which ranges from 50,000 and 65,000 deadweight tons in size; these vessels are equipped with onboard cranes allowing for the self-loading and unloading of cargoes, a feature which distinguishes them from the larger classes of drybulk vessels and provides for greatly enhanced flexibility and versatility- both with respect to cargo diversity and port accessibility. The Company transports a broad range of major and minor bulk cargoes around the world, including coal, grain, ore, pet coke, cement, and fertilizer. Eagle operates out of three offices, Stamford (headquarters), Singapore, and Hamburg, and performs all aspects of vessel management in-house including: commercial, operational, technical, and strategic.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Eagle reported 2002-3Q Net Revenues of $185.3 million on TCE rates of $28,099. We had recently lowered our net revenue estimate to $158.9 million based on an assumed TCE rate to $25,000. Higher-than-expected revenues reflect a high level of charter-in days (1000 versus our 600 assumption) and an impressive utilization rate of 99.7%. The company has 70% of fourth-quarter available days covered at $25,040 which compares favorably with our models.

But costs were higher. Eagle reported 2002-3Q voyage expenses of $40.8 million versus $30.3 million last year and our estimate of $25.6 million. Voyage operating expenses were $33.1 million versus $28.1 million and our $27.5 million estimate. G&A expenses were $9.7 million versus $7.9 million and our $8.4 million estimate. Higher costs reflect industry trends but bear watching going forward.

What is Inflammation? Two Immunologists Explain How the Body Responds to Everything from Stings to Vaccination and Why it Sometimes Goes Wrong

When your body fights off an infection, you develop a fever. If you have arthritis, your joints will hurt. If a bee stings your hand, your hand will swell up and become stiff. These are all manifestations of inflammation occurring in the body.

We are two immunologists who study how the immune system reacts during infections, vaccination and autoimmune diseases where the body starts attacking itself.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Prakash Nagarkatti, Professor of Pathology, Microbiology and Immunology, University of South Carolina and Mitzi Nagarkatti Professor of Pathology, Microbiology and Immunology, University of South Carolina

While inflammation is commonly associated with the pain of an injury or the many diseases it can cause, it is an important part of the normal immune response. The problems arise when this normally helpful function overreacts or overstays its welcome.

What is Inflammation?

Generally speaking, the term inflammation refers to all activities of the immune system that occur where the body is trying to fight off potential or real infections, clear toxic molecules or recover from physical injury. There are five classic physical signs of acute inflammation: heat, pain, redness, swelling and loss of function. Low-grade inflammation might not even produce noticeable symptoms, but the underlying cellular process is the same.

Take a bee sting, for example. The immune system is like a military unit with a wide range of tools in its arsenal. After sensing the toxins, bacteria and physical damage from the sting, the immune system deploys various types of immune cells to the site of the sting. These include T cells, B cells, macrophages and neutrophils, among other cells.

The B cells produce antibodies. Those antibodies can kill any bacteria in the wound and neutralize toxins from the sting. Macrophages and neutrophils engulf bacteria and destroy them. T cells don’t produce antibodies, but kill any virus-infected cell to prevent viral spread.

Additionally, these immune cells produce hundreds of types of molecules called cytokines – otherwise known as mediators – that help fight threats and repair harm to the body. But just like in a military attack, inflammation comes with collateral damage.

The mediators that help kill bacteria also kill some healthy cells. Other similar mediating molecules cause blood vessels to leak, leading to accumulation of fluid and influx of more immune cells.

This collateral damage is the reason you develop swelling, redness and pain around a bee sting or after getting a flu shot. Once the immune system clears an infection or foreign invader – whether the toxin in a bee sting or a chemical from the environment – different parts of the inflammatory response take over and help repair the damaged tissue.

After a few days, your body will neutralize the poison from the sting, eliminate any bacteria that got inside and heal any tissue that was harmed.

Asthma is caused by inflammation that leads to swelling and a narrowing of airways in the lungs, as seen in the right cutaway in this image. BruceBlaus/Wikimedia Commons, CC BY-SA

Inflammation as a Cause of Disease

Inflammation is a double-edged sword. It is critical for fighting infections and repairing damaged tissue, but when inflammation occurs for the wrong reasons or becomes chronic, the damage it causes can be harmful.

Allergies, for example, develop when the immune system mistakenly recognizes innocuous substances – like peanuts or pollen – as dangerous. The harm can be minor, like itchy skin, or dangerous if someone’s throat closes up.

Chronic inflammation damages tissues over time and can lead to many noninfectious clinical disorders, including cardiovascular diseases, neurodegenerative disorders, obesity, diabetes and some types of cancers.

The immune system can sometimes mistake one’s own organs and tissues for invaders, leading to inflammation throughout the body or in specific areas. This self-targeted inflammation is what causes the symptoms of autoimmune diseases such as lupus and arthritis.

Another cause of chronic inflammation that researchers like us are currently studying is defects in the mechanisms that curtail inflammation after the body clears an infection.

While inflammation mostly plays out at a cellular level in the body, it is far from a simple mechanism that happens in isolation. Stress, diet and nutrition, as well as genetic and environmental factors, have all been shown to regulate inflammation in some way.

There is still a lot to be learned about what leads to harmful forms of inflammation, but a healthy diet and avoiding stress can go a long way toward helping maintain the delicate balance between a strong immune response and harmful chronic inflammation.

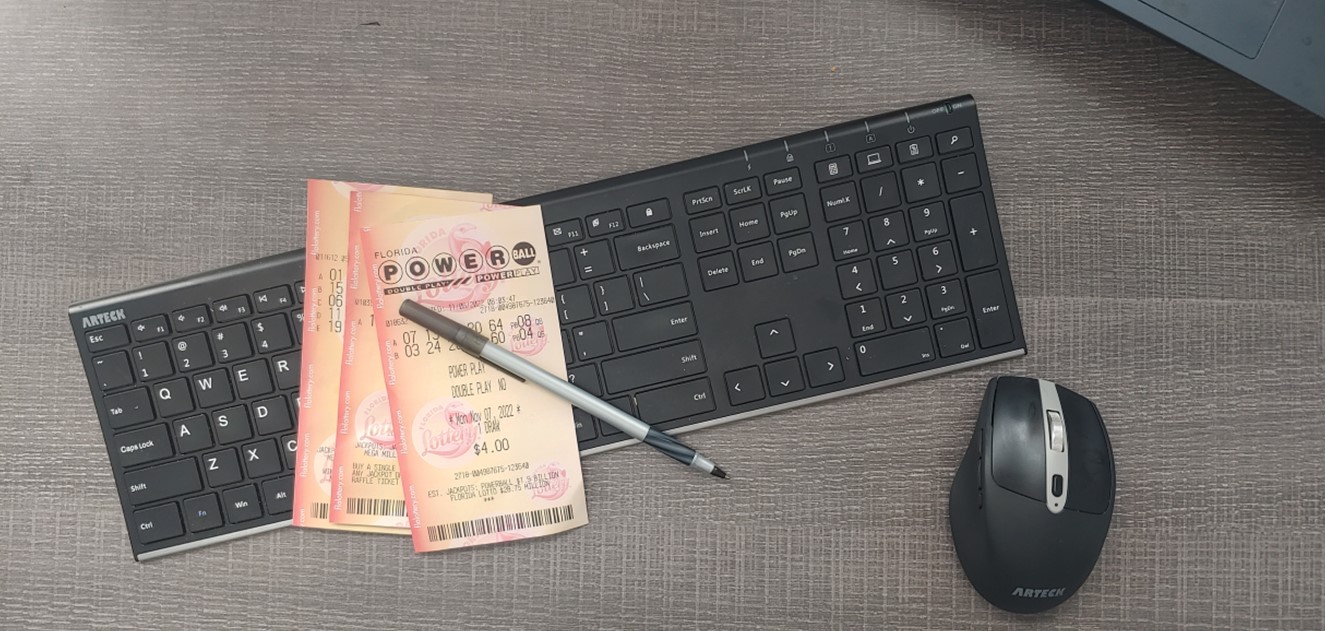

Why the Future Value of the Lottery’s Grand Prize is Significantly Higher than Last Year

There is a link between the current $1.9 billion Powerball prize money and Federal Reserve Chair Jerome Powell – and it is inflating the prize money.

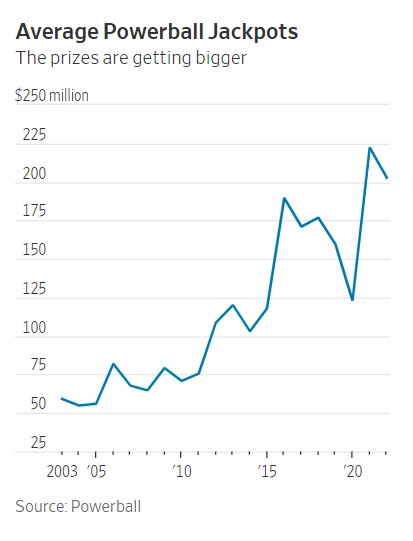

A new billionaire was not minted over the weekend, at least not because of winning the enormous Powerball jackpot prize. So the weekend prize money, plus a small fortune more, is up for grabs at 10:59 PM Monday, November 7. The headline prize money, in this case, $1.9 billion, is the future value of the cash award, which, according to Powerball.com, is $929.1 million. The larger, almost two billion amount, would not have been nearly as large last year. Its sum is much bigger because the Fed has been jacking up interest rates.

To drill down a bit more, the prize calculation uses the 30-year U.S. Treasury bond interest rate to determine the annuity paid to the winner based on the cash lump sum award. The present value of that number, even if on par with a cash award a year ago, would pay a substantially larger annuity. And it is the annuity that is the advertised prize, which draws more and more players as it grows. The more players, the higher the present value or cash prize.

A year ago (November 8, 2021), the 30-year US Treasury bond had a yield of 1.90%. This was used to calculate the headline prize amount. Today, the same term Treasury is yielding 4.27%. This yield impact is roughly reflected in the average prizes over the years.

The Numbers Boiled Down Further

Of all ticket sales, 34% of Powerball ticket sales fund the grand prize. Another 16% fund the lower-tier prizes. (The remaining 50% goes to various state programs, operating costs, and retailer commissions.) If a winner chooses the lump sum payout, they receive the 34%. If instead, the winner chooses the jackpot in annual payments over 30 years, the prize money is invested in a portfolio of bonds.

The last time a winner chose an annuity was in 2014.

Economists who have researched lotteries have learned that once jackpots near the $500 million mark, non-regular lottery players are more likely to take a chance. The $500 million or more mark is where the media begins to make “lottery fever” a news event worth reporting on. The added publicity then feeds more money into the pot.

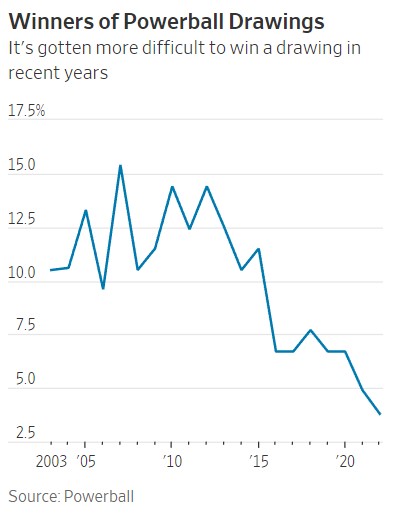

The prize pools are also growing because the games of chance have become statistically more difficult to take the top prize. In 2015, Powerball increased the cost of the ticket and altered the game to make it easier for players to win smaller prizes while reducing the odds of winning the headline prize.

Only 3.8% of drawings so far this year had had a winner, down from roughly 11% in 2014, the last full year before the change went into effect.

This is why the five times in the U.S. where $1 billion has been surpassed have all been recent. They include the biggest one, a $1.58 billion prize from Powerball in 2016, followed by a $1.53 billion Mega Millions jackpot in 2018 and this week’s $1.5 billion Powerball prize.

Lottery tickets also tend to become more popular during economic downturns and when people become more money conscious.

Even though the odds of winning Powerball are 1 in 292.2 million, players will take a shot and buy a ticket to have the fantasy. If the prize money continues to reach over $500 million on a regular basis, it may work against the program as those who don’t normally play won’t feel it is a special event.

Federal Reserve President Speeches With Elections and CPI to Shape the Week’s Trading

Yes, the stock markets are open on Veterans Day (Friday). But bond trading, which the stock market has been more keenly focused on this year, will be taking the day off along with other U.S. government services. Equity traders can get a sense of interest rate sentiment on Friday by turning to the Chicago Board of Options and viewing tickers ZF=F (5 yr. USTN), ZN=F (10 yr. USTN), ZB=F (30 yr. USTB).

All markets are open on Election Day, and the outcome, as measured by House seats and Senate seats distributed among the major political parties, has the potential to be market-moving.

It’s a quiet week for economic numbers, except for Thursday, when the CPI report is released. This has the potential of changing those calling for a 50 bp hike at the next meeting to up their expectations or those still forecasting 75bp to lower their call. Certainly, the Fed governors will be watching this and all measures of inflation up to the December 14-15 meeting. There are a number of Fed governors speaking this week; this could alter the tone; however, the next meeting is far out into the future.

Election Day.

Monday 11/7

3:00 PM ET the amount of consumer installment credit for September, including credit cards, auto loan, and student loans outstanding, indicate current consumer spending and borrowing patterns. The markets tend to ignore this number as we are already in November and this report measures September

3:40 PM ET, the Federal Reserve Bank Presidents Mester (Cleveland) and Collins (Boston), will be speaking. Both are considered fairly hawkish.

6:00 PM ET, the Federal Reserve Bank President Harkey (Philadelphia) will be speaking.

Tuesday 11/8

Election Day.

Meet the Management; Noble Capital Markets hosts Management of Entravision Communications (EVC) in West Palm Beach, FL. This is a no-cost-to-attend, in-person breakfast meeting with investors. If interested, click here.

Meet the Management, Noble Capital Markets hosts Management of Entravision Communications (EVC) in Boca Raton, FL. This is a no-cost-to-attend, in-person lunch meeting with investors. If interested, click here.

Wednesday 11/9

It can be expected that the newswires will be filled with Election Day outcomes and market-moving conjecture.

7:00 AM ET Mortgage Applications. The Mortgage Bankers Association (MBA) creates a statistic from several mortgage loan indexes. The Mortgage Applications index measures applications at mortgage lenders. It’s considered a leading indicator and is especially important for single-family home sales and housing construction. Both are considered foundational in a strong economy.

10 Year Treasury Note Auction is held in the middle of each month and settles on or around the 15th (depending on weekends). The yield is a benchmark for 30-year mortgages and has recently been noted by investment markets because it has been trading at a yield lower than shorter maturities. This inversion of the yield curve has some market players suggesting a recession is expected in the future. Any surprises at the auction will reverberate through the stock market.

10:30 AM ET, EIA Petroleum Status Report.

11:00 AM ET, Federal Reserve President Barkin (Philadelphia) speaks.

Meet the Management; Noble Capital Markets hosts Management of Entravision Communications (EVC) in Winter Park, FL. This is a no-cost-to-attend, in-person breakfast meeting with investors. If interested, click here.

Meet the Management; Noble Capital Markets hosts Management of Entravision Communications (EVC) in Orlando, FL. This is a no-cost-to-attend, in-person lunch meeting with investors. If interested, click here.

Thursday 11/10

8:30 AM ET, U.S. Consumer Price Index (CPI) is the inflation indicator most widely broadcast. With inflation being a primary focus, this will be the big number coming out this week. The number represents a basket of goods considered typical for an urban consumer and is taken as the change in the cost of that basket of goods. A percentage is derived from the change. CPI is also reported with food and energy removed as it is considered that other non-economic factors influence these prices. The September report indicated CPI rose 0.4% for the month and 8.2% YOY. Expectations are for an increase to 0.7% for October and a YOY rate of 8.0%.

8:30 AM ET U.S. Jobless Claims which represent the prior week’s employment are expected to have increased to 221,000 from 217,000. From jobless claims, investors can gain a sense of how tight or how loose the job market is. If wage inflation takes hold, interest rates will likely rise, and bond and stock prices will fall. Remember, the lower the number of unemployment claims, the stronger the job market, and vice versa.

10:30 AM ET, EIA Natural Gas Status Report.

Friday 11/11

Veterans Day, the stock market is one, the futures markets are open, and the bond market and other U.S. government-related offices are closed.

10 AM ET Consumer Sentiment, November (preliminary). This barometer, reported by the University of Michigan, questions households each month on their assessment of current conditions and expectations of future conditions. This “preliminary” release is for the month of November and is expected to have fallen to 59.6 versus 59.9 last month.

What Else

It is a light week for economic releases and Fed governor addresses, but the election outcome and CPI have the potential to whip markets around.

We’re entering the holiday shopping season when there will be a number of measures that investors focus on that will give a hint as to how strong the consumer is in the current economy.

US Sailors, Coastal Riverine Group, Restoring Command Anchor with Gold Paint, Credit: US Pacific Fleet (Flickr)

Can the Dollar Once Again Be Anchored by Gold? One Congressman Believes It Can

On October 7, 2022, US congressman Alex Mooney (a Republican from West Virginia) introduced a bill (the Gold Standard Restoration Act, H.R. 9157) that stipulates that the US dollar must be backed by physical gold owned by the US Treasury. The initiative clearly indicates that the increasingly inflationary US dollar is triggering efforts to get better money.

It should be noted that there have already been many legislative changes to make precious metals more attractive as a means of payment in recent years: in many US states, the value-added and capital gains taxes on gold and silver, but also on platinum and palladium, have been abolished. Mr. Mooney’s proposal is divided into three sections.

The first section of the bill establishes the need for a return to a gold-backed US dollar. For example, it is said that the US dollar—or more precisely, the bill refers to “Federal Reserve Notes”—that is, banknotes issued by the US Federal Reserve (Fed)—has lost its purchasing power on a massive scale in the past: Since 2000, it has dropped by 30 percent, and since 1913 by 97 percent. The bill also argues that with an inflation target of 2 percent, the Fed will not preserve the purchasing power of the US dollar but will have it halved after just thirty-five years. Moreover, the bill points out that it is in the interest of US citizens and firms to have a “stable US dollar.” The bill highlights that the inflationary US dollar has been eroding the industrial base of the US economy, enriching the owners of financial assets, while endangering workers’ jobs, wages, and savings.

The second section of the bill describes in more detail the technical process for re-anchoring the US dollar to the US official gold stock. It states that (1) the US secretary of the Treasury must define the US dollar banknotes using a fixed fine gold weight thirty days after the law goes into effect, based on the closing price of the gold on that day. The Fed must (2) ensure that the US banknotes are redeemable for physical gold at the designated rate at the Fed. (3) If the banks of the Fed system fail to comply with peoples’ exchange requests, the exchange must be made by the US Treasury, and in return, the Treasury takes the Fed’s bank assets as collateral.

The third section specifies how a “fair” gold price in US dollar can develop in an orderly manner within thirty days after the bill has taken effect. To this end, (1) the US Treasury and the Fed must publish all of their gold holdings, disclosing all purchases, sales, swaps, leases, and all other gold transactions that have taken place since the “temporary” suspension of the redeemability of the US dollar into gold on August 15, 1971, under the Bretton Woods Agreement of 1944. In addition, (2) the US Treasury and the Fed must publicly disclose all gold redemptions and transfers in the 10 years preceding the “temporary” suspension of the US dollar’s gold redemption obligation on August 15, 1971.

What to Make of This?

The bill’s core is the idea of re-anchoring the US dollar to physical gold based on a fair gold price freely determined in the market. (By the way, this is an idea put forward by the economist Ludwig von Mises (1881–1973) in the early 1950s.) In this context, the bill refers to US banknotes. However, banknotes only comprise a (fractional) part of the total US dollar money supply. But since US bank deposits can be redeemed (at least in principle) in US banknotes, not only US dollar cash (coins and notes) could be exchanged for gold, but also the money supply M1 or M2 as fixed and savings deposits could be exchanged for sight deposits, and sight deposits, in turn, could be withdrawn in cash by customers, and the banknotes could then be exchanged for gold at the Fed.

As of August 2022, the stock of US cash (“currency in circulation”) amounted to $2,276.3 billion. Assuming that the official physical gold holdings of the US Treasury amount to 261.5 million troy ounces, and the market expected US cash to be backed by the official US gold stock, a gold price of about $8,700 per troy ounce would result. This would correspond to a 418 percent increase compared to the current gold price of $1,680. If, however, the market were to expect the entire US money supply M2 to be covered by the official US gold stock, then the price of gold would move toward $83,000 per troy ounce—an increase of 4.840 percent compared to the current gold price. Needless to say, such an appreciation of gold has far-reaching consequences.

All goods prices in US dollars can be expected to rise (perhaps to the extent that the price of gold has risen). After all, the purchasing power of the owners of gold has increased significantly. Therefore, they can be expected to use their increased purchasing power to buy other goods (such as consumer goods, but also stocks, houses, etc.). If this happens, the prices of these goods in US dollar terms will be pushed up—and thus, the initial purchasing power gain that the gold dollar holders have enjoyed by being tied to the increased gold price will melt away again. Moreover, if US banks were willing to accept additional gold from the public in exchange for issuing new US dollar, reanchoring the US dollar in gold would increase the upward price effect.

A re-anchoring of the US dollar in the US official gold stock will result in a far-reaching redistribution of income and wealth. In fact, it would be fatal for the outstanding US dollar debt: US dollar goods prices would rise, caused by a rise in the US dollar gold price at which the US dollar is redeemable for physical gold, thereby eroding the US dollar’s purchasing power. In the foreign exchange markets, the US dollar would probably appreciate drastically against those currencies that are not backed by gold and against currencies which are backed by gold, not as fine compared to the fineness of the gold backing of the US dollar. The purchasing power of the US dollar abroad would increase sharply, while the US export economy would suffer. US goods would become correspondingly expensive abroad, while foreign companies gain high price competitiveness in the US market.

Once the US dollar is re-anchored in gold, today’s chronic inflation will end; monetary policy–induced boom-and-bust cycles will come to an end; the world will become more peaceful because financing a war in a gold-backed monetary system will be very expensive, and the general public will most likely not want to bear its costs. However, there is still room for improvement. A “Gold Standard Restoration Act” will deserve unconditional support if and when it paves the way toward a truly “free market for money.” A free market in money means that you and I have the freedom to choose the kind of money we believe serves our purposes best; and that people are free to offer their fellow human beings a good that they voluntarily choose to use as money.

In a truly free market, people will choose the good they want to use as money. Most importantly, in a truly free market in money, the state (as we know it today) loses its influence on money and money production altogether. In fact, the state (and the special interest groups that exploit the state) no longer determine which kind of gold (coins and bars, cast or minted) can be used as money; the state is no longer active in the minting business and cannot monopolize it anymore; there is no longer a state-controlled central bank to intervene in the credit and money markets and influence market interest rates. That said, let us hope that the Gold Standard Restoration Act proposed by Mr. Mooney will pave the way to reforming the US dollar currency system—and that it will eventually move us toward a truly free market in money.

About the Author

Dr. Thorsten Polleit is the Chief Economist of Degussa and an Honorary Professor at the University of Bayreuth. He also acts as an investment advisor.

LAKEWOOD, Colo., Nov. 4, 2022 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”) today reported its financial results for the quarter ended September 30, 2022. The Company’s quarterly report on Form 10-Q has been filed with the U.S. Securities and Exchange Commission (“SEC“) and may be viewed on the Electronic Document Gathering and Retrieval System (“EDGAR“) at www.sec.gov/edgar.shtml, on the System for Electronic Document Analysis and Retrieval (“SEDAR“) at www.sedar.com, and on the Company’s website at www.energyfuels.com. Unless noted otherwise, all dollar amounts are in U.S. dollars.

Highlights:

At September 30, 2022, the Company had a robust balance sheet with $122.3 million of working capital, including $77.1 million of cash and cash equivalents, $11.6 million of marketable securities, $27.3 million of inventory, and no short term (or long term) debt. At current commodity prices, the Company’s product inventory has a value of $44.1 million.

During the quarter ended September 30, 2022, the Company incurred a net loss of $9.3 million, which includes increases in development, permitting and land holding costs and selling, general and administration costs associated with the Company’s efforts to enhance its business processes and operational readiness for the current and future growth and activity in our uranium and rare earth element (“REE“) operations.

With recent uranium market strength and having secured three long-term uranium contracts with major U.S. utilities earlier this year, the Company has hired over 20 new employees and is beginning to perform the work needed to recommence production at one or more of our mines and ISR facilities, starting as soon as 2023. Until such time when the Company has ramped back up to commercial uranium production, we can rely on our significant uranium inventories to fulfill our new contract requirements.

In June 2022, the U.S. Department of Energy (“DOE“) issued a Request for Proposals (“RFP“) to purchase uranium (“U3O8“) for the new U.S. Uranium Reserve Program. The DOE states that they expect to purchase up to 1 million pounds of U3O8 inventory from up to four (4) qualified U.S. uranium producers with individual awards ranging from 100,000 pounds to 500,000 pounds. The uranium must be physically located at Honeywell’s Metropolis Works conversion facility (the “U.S. Converter“). Energy Fuels believes it meets all qualifications to supply the Reserve, and the Company currently holds about 610,000 pounds of U3O8 at the U.S. Converter. The Company has submitted a bid to sell U3O8 to the Reserve, taking into consideration our long-term contract commitments and current and expected market conditions. There are no guarantees the DOE will purchase uranium from the Company under this RFP. Assuming the bid review process is not extended by DOE, the Company expects the DOE to issue the awards by mid-November 2022, with deliveries expected to occur by the end of 2022 or early 2023.

During the first nine months of 2022, the Company produced approximately 205 tonnes of mixed partially separated carbonate (“RE Carbonate“), containing approximately 95 tonnes of total rare earth oxides (“TREO“). Energy Fuels’ partially separated RE Carbonate contains a higher concentration of valuable NdPr, roughly 32% – 34% NdPr, compared to our previously produced non-separated RE Concentrate which contained approximately 22% NdPr, and is the most advanced REE material being produced in the U.S. today. During Q4-2022, the Company expects to receive approximately 640 tonnes of monazite, which will be processed into partially separated RE Carbonate during Q4-2022 and Q1-2023.

In May 2022, the Company announced it had entered into agreements to acquire a 58 square mile rare earth land position in Brazil (the “Bahia Project“). The Bahia Project is a well-known heavy mineral sand (“HMS“) deposit that has the potential to feed the Company’s White Mesa Mill with REE and uranium-bearing monazite sand for decades. Due diligence on the Bahia Project was completed at the end of August, at which time the Company advised the sellers that it intended to proceed with the purchases and was ready to commence closing procedures. After completion of a number of administrative logistics required in both the U.S. and Brazil, the mineral transfers were initiated in mid-October, and closing is currently expected to occur in late 2022 or early 2023 upon approval of the Brazilian governmental authorities reviewing the pending transfers. Upon acquisition, the Company plans to conduct an extensive exploration program to better define the HMS and monazite resource, including comprehensive sonic drilling (for a total phase 1 program of 2,250 meters) and geophysical mapping, with the intent to undertake an Initial Assessment under SK-1300 (U.S.) and a Technical Report under NI 43-101 (Canada) during Q4-2023, to be completed in early Q1-2024.

The Company is currently in active discussions with several additional sources of natural monazite sands around the world to significantly increase the supply of feed for our growing REE initiative.

The Company continues to make excellent progress toward installing full REE separation capabilities at the Mill to produce both “light” and “heavy” separated REE oxides in the coming years. The Company plans to initially install a “light” REE separation circuit within the existing Mill facilities in the next 12-18 months with the expected ability to produce between 2,500 – 5,000 tonnes TREO (500 – 1,000 tonnes NdPr oxide or oxalates) per year. As this circuit would be constructed within existing Mill facilities, capital expenditures are expected to be low. The Company is also proceeding with the design, engineering and permitting of a separate crack and leach circuit and a second larger “light” and “heavy” separations circuit with capacity in the order of 10,000 – 15,000 tonnes TREO per year to provide additional REE processing capacity at the Mill in the coming years.

During the first nine months of 2022, the Company sold approximately 642,000 pounds of existing inventory of vanadium (“V2O5“) (as ferrovanadium, “FeV“), for an average weighted net price of $13.69 per pound of V2O5. Vanadium markets have dropped in recent months. Therefore, the Company has halted sales of its inventory which currently stands at approximately 987,000 pounds of V2O5. However, the Company expects to resume sales as markets may improve in the future. The Company is evaluating the potential to resume vanadium recovery at the Mill in the future as market conditions may warrant for future sale and to replace sold inventory, where its tailings pond solutions contain an estimated additional 1.0 to 3.0 million recoverable pounds of V2O5.

Mark S. Chalmers, Energy Fuels’ President and CEO, stated:

“Energy Fuels continues to strengthen our U.S. market leading position in uranium and rare earth elements, which are both critical to the clean energy transition. Energy Fuels has ‘one-of-a-kind’ competencies that are critical to uranium, rare earth elements, medical isotopes, and vanadium markets; namely our ability to process feedstocks that are naturally radioactive and recover critical materials needed for the clean energy transition. No other company in the U.S. can do the things Energy Fuels does. We are committed to advancing each of these initiatives in a disciplined manner, while working toward profitability and sustained cash flow.

“Uranium is the fuel for carbon-free nuclear energy, and nations around the world are embracing nuclear, as it provides reliable, carbon-free, baseload electricity. Governments in numerous countries, including the U.S., are supporting both existing and new nuclear to help solve national security, energy security, and carbon reduction challenges. We are saddened by the continuing atrocities being committed by Russian forces in Ukraine, and we stand by our partners in the U.S. nuclear industry and the U.S. government to shift away from Russian uranium and nuclear fuel imports as soon as practicable. As previously disclosed, Energy Fuels has signed new long-term uranium sales contracts with major U.S. nuclear utilities, with sales – and sales revenues – beginning in 2023. We are also excited to announce that we are making significant investments in a number of our existing mines and production facilities, including hiring people, with an eye toward resuming large-scale uranium production very soon. We have been the only U.S. company to continue to produce uranium over the past several years, while maintaining several of our projects on standby status, which provides an excellent foundation from which we can build our production in the coming years. We look forward to maintaining our position as the largest U.S. uranium producer and being a long-term supplier of secure and responsibly sourced U.S. uranium that is insulated from geopolitical, transport, and other supply chain issues. We are also pleased to have been able to submit a bid to sell uranium to the U.S. government under the new U.S. Uranium Reserve, a program that resulted from the Company’s 2018 Section 232 Petition, and we eagerly await the results of that bidding process.

“We also continue to make spectacular progress on rare earth elements. Indeed, we are pleased to announce that we plan to install a commercial-scale “light” rare earth separation circuit within the existing footprint of our White Mesa Mill in Utah that we expect to be operational in the next 12 – 18 months. We are already producing the most advanced rare earth product in the U.S. today, a high-purity, partially separated mixed rare earth carbonate. We expect to go one step further by producing up to 500 – 1,000 tonnes of NdPr oxide (or oxalates) per year by late-2023 or early-2024. If successful, we hope to be the ‘first to market’ in the U.S. for this high-value, advanced material. We anticipate selling our separated NdPr oxide (or oxalate) to major electric vehicle manufacturers in the U.S. and Europe, with a goal to significantly increase this capacity in coming years. This should position Energy Fuels as one of the ‘go to’ suppliers of advanced rare earth materials in the U.S. and one of the first companies that electric vehicle (EV) and other clean technology manufacturers look to for the raw materials they need. Ultimately, we plan to install the capacity to produce over 3,000 tonnes of NdPr oxide, plus 250 tonnes of dysprosium oxide and 100 tonnes of terbium oxide per year, in the next 3-4 years, subject to licensing, commissioning, financing, offtake, market conditions, and sufficient monazite feedstock.

“On the monazite feedstock front, we continue to make excellent progress. With regard to our Bahia Project in Brazil, we continue to move diligently toward closing. The mineral transfers were initiated in mid-October after a number of administrative logistics required for closing were completed in both the U.S. and Brazil. Closing is scheduled to occur as soon as the transfers have been approved by the Brazilian governmental authorities reviewing the pending transfers, which we expect by the end of 2022 or in early 2023. Upon acquisition, the Company plans to conduct an initial phase of exploration drilling on the properties, totaling 2,250 meters, in order to maintain expected production timelines. In addition, we continue discussions with a number of monazite suppliers from around the world interested in partnering with Energy Fuels, and we are confident in our ability to secure monazite supply deals that ensure a ‘win-win’ for both Energy Fuels and our partners.

“Finally, we continue to make progress on medical isotopes with major players in the space. If we can successfully recover radioactive isotopes needed for emerging cancer treatments from our existing process streams, we will have secured yet another opportunity to generate significant cash flows in the next 5 to 10 years. We also continue to track vanadium markets to determine when to resume sales of our existing inventories and when to resume production.”

Webcast at 4:00 pm ET on November 8, 2022:

Energy Fuels will be hosting a video webcast on November 8, 2022 at 4:00 pm ET (2:00 pm MT) to discuss its Q3-2022 financial results, the outlook for 2022, uranium, rare earths, vanadium, and medical isotopes. To join the webcast and access the presentation and viewer-controlled webcast slides, please click on the link below:

Webcast Link

If you would like to participate in the webcast and ask questions, please dial in to 1-888-664-6392 (toll free in the U.S. and Canada).

A link to a recorded version of the proceedings will be available on the Company’s website shortly after the webcast by calling 1-888-390-0541 (toll free in the U.S. and Canada) and by entering the code 619525#. The recording will be available until November 22, 2022.

Financial Discussion:

At September 30, 2022, the Company had $122.3 million of working capital, including $88.7 million of cash and cash equivalents and marketable securities and $27.3 million of inventory, including approximately 692,000 pounds of uranium and 987,000 pounds of high-purity vanadium, both in the form of immediately marketable product. The current spot price of U3O8, according to TradeTech, is $52.50 per pound, and the current mid-point spot price of V2O5, according to Metal Bulletin, is $7.80 per pound. Based on those spot prices, the Company’s uranium and vanadium inventories have a current market value of $36.3 million and $7.7 million, respectively, totaling $44.0 million. The Company also holds RE Carbonate inventory with a current value of $0.1 million, for total product inventory of $44.1 million at current commodity prices.

During the quarter ended September 30, 2022, the Company incurred a net loss of $9.3 million, compared to a net loss of $8.0 million for the third quarter of 2021, and a net loss of $42.0 million for the nine months ended September 30, 2022 compared to a net loss of $29.7 million during the first nine months of 2021. The increased net losses in 2022 are due primarily to a non-cash mark-to-market decrease in the value of investments accounted for at fair value of $13.7 million for the nine months ended September 30, 2022.

Operations Update and Outlook for 2022:

Overview

The Company continues to believe that uranium supply and demand fundamentals point to higher sustained uranium prices in the future. In addition, Russia’s recent invasion of Ukraine and the recent entry into the uranium market by financial entities purchasing uranium on the spot market to hold for the long-term has the potential to result in higher sustained spot and term prices and, perhaps, induce utilities to enter into more long-term contracts with non-Russian producers like Energy Fuels to ensure security of supply and more certain pricing. Having recently secured three long-term uranium contracts with major U.S. utilities, the Company is beginning to perform the work needed to recommence production at one or more of its mines and ISR facilities, starting as soon as 2023. Until such time when the Company has ramped back up to commercial uranium production, it can rely on its significant uranium inventories to fulfill its new contract requirements. To that end, the Company purchased an additional 68,552 pounds of U. S. origin U3O8 on the spot market in October 2022. The Company also continues to evaluate selling a portion of its inventories on the spot market in response to future upside price volatility, into the newly created U.S. Uranium Reserve Program, or for delivery into additional long-term supply contracts if procured. During the nine months ended September 30, 2022, the Company also sold a portion of its vanadium inventory into then strengthening markets.

The Company will also continue to seek new sources of revenue, including through its emerging REE business, as well as new sources of Alternate Feed Materials and new fee processing opportunities at the Mill that can be processed without reliance on current uranium sales prices. The Company is also seeking new sources of natural monazite sands (in addition to the pending acquisition of the Bahia Project) for its emerging REE business, is evaluating the potential to recover radioisotopes for use in the development of targeted alpha therapy medical isotopes for the treatment of cancer, and continues its support of U.S. governmental activities to assist the U.S. uranium mining industry, including the new U.S. Uranium Reserve Program and other efforts to restore domestic nuclear fuel capabilities.

Extraction and Recovery Activities Overview

During 2022, the Company plans to recover 130,000 to 140,000 pounds of uranium, which is an increase over our previous guidance of 100,000 to 120,000 pounds of uranium in 2022. This increased uranium production in 2022, combined with other factors, has resulted in a delayed start of our second REE processing campaign in 2022, which is now expected to commence in November 2022 and carry over into Q1 2023. As a result, the Company now expects to produce approximately 205 tonnes of partially separated RE Carbonate in 2022 containing approximately 95 tonnes of high-value partially separated TREO, with the remaining production from the second 2022 REE processing campaign of approximately 410 tonnes of partially separated RE Carbonate containing approximately 200 tonnes of high-value partially separated TREO being packaged in and attributable to Q1 2023. The total expected production from this second 2022 campaign plus production to date in 2022 is equivalent to approximately 831 tons of non-separated RE Carbonate containing approximately 400 tonnes of non-separated TREO, which falls within our 2022 guidance of 650-1,000 tons of non-separated RE Carbonate containing 300-650 tonnes of non-separated TREO, although a portion of that total expected production will carry over into 2023.

No vanadium production is currently planned during 2022, though the Company sold some of its existing vanadium inventory into recent strong markets and is evaluating the potential to recommence vanadium production in 2023 or later years as market conditions may warrant for future sale and to replace sold inventory.

The Company secured three new long-term sales contracts with U.S. nuclear utilities in May 2022 and is continuing to strategically pursue additional uranium sales commitments with pricing expected to have both fixed and market-related components. The Company believes that recent price increases, volatility and focus on security of supply in light of Russia’s ongoing invasion of Ukraine have increased the potential for the Company to make uranium sales and procure additional term sales contracts with utilities at pricing that sustains production and covers corporate overhead. Therefore, existing inventories may increase from 760,000 pounds of U3O8 (692,000 pounds as of September 30, 2022 plus 68,552 pounds acquired after quarter end) to 890,000 to 900,000 pounds of U3O8 at year-end 2022 or may increase to a lesser extent, or be reduced, in the event the Company sells a portion of its inventory on the spot market, to the U.S. Uranium Reserve Program, or pursuant to term contracts in 2022.

ISR Activities

The Company expects to produce insignificant quantities of U3O8 in the year ending December 31, 2022 from Nichols Ranch. Until such time when market conditions improve sufficiently, suitable term sales contracts can be procured, or the U.S. Uranium Reserve Program is expanded, the Company expects to maintain the Nichols Ranch Project on standby and defer development of further wellfields and header houses. The Company currently holds 34 fully permitted, undeveloped wellfields at Nichols Ranch, including four additional wellfields at the Nichols Ranch wellfields, 22 wellfields at the adjacent Jane Dough wellfields, and eight wellfields at the Hank Project, which is fully permitted to be constructed as a satellite facility to the Nichols Ranch Plant. The Company expects to continue to keep the Alta Mesa Project on standby until such time that market conditions improve sufficiently, suitable term sales contracts can be procured, or the U.S. Uranium Reserve Program is expanded.

Conventional Activities

Conventional Extraction and Recovery Activities

During the nine months ended September 30, 2022, the Mill did not package any material quantities of U3O8, focusing instead on developing its REE recovery business. During the nine months ended September 30, 2022, the Mill produced approximately 205 tonnes of partially separated RE Carbonate, containing approximately 95 tonnes of high value partially separated TREO. The Mill recovered small quantities of uranium during the Quarter, which were retained in circuit. During 2022, the Company expects to recover 130,000 to 140,000 pounds of uranium at the Mill as finished product. The Company expects to recover approximately 205 tonnes of partially separated RE Carbonate (equivalent to approximately 277 tonnes of non-separated RE Carbonate) containing approximately 95 tonnes of high value partially separated TREO (equivalent to approximately 128 tonnes of non-separated TREO) at the Mill during 2022. The Company expects to sell all or a portion of its mixed RE Carbonate to Neo Performance Materials (“Neo“) or other global separation facilities and/or to stockpile it for future production of separated REE oxides at the Mill or elsewhere. The Company is in advanced discussions with several sources of natural monazite sands (in addition to the Bahia Project) to secure additional supplies of monazite sands, which if successful, would be expected to allow the Company to increase RE Carbonate production.

In addition to its 760,000 pounds of finished uranium inventories currently located at North American conversion facilities and at the Mill (692,000 pounds as of September 30, 2022 plus 68,552 pounds acquired after quarter end) and the 130,000 to 140,000 pounds of U3O8 expected to be produced in 2022, the Company has approximately 170,000 pounds of U3O8 contained in stockpiled Alternate Feed Materials and other ore inventory at the Mill that can be recovered relatively quickly in the future, as general market conditions may warrant (totaling about 1,060,000 to 1,070,000 pounds of U3O8 of total uranium inventory). The Company is also seeking to acquire additional ore inventory from third party mine cleanup activities that can be recovered relatively quickly in the future.

The Company currently holds approximately 987,000 pounds of V2O5 in inventory, and there remains an estimated 1.0 to 3.0 million pounds of additional solubilized recoverable V2O5 remaining in tailings solutions awaiting future recovery, as market conditions may warrant.

Conventional Standby, Permitting and Evaluation Activities

During the nine months ended September 30, 2022, standby and environmental compliance activities continued at the fully permitted and substantially developed Pinyon Plain Project (uranium and, potentially, copper) and the fully permitted and developed La Sal Complex (uranium and vanadium). The Company increased its number of employees, and continued carrying out engineering, procurement and construction management activities, at its Pinyon Plain Project during the Quarter. The timing of the Company’s plans to extract and process mineralized materials from these projects will be based on sustained improvements in general market conditions, procurement of suitable sales contracts and/or the expansion of the U.S. Uranium Reserve Program.

The Company is selectively advancing certain permits at its other major conventional uranium projects, such as the Roca Honda Project, which is a large, high-grade conventional project in New Mexico. The Company is also continuing to maintain required permits at its conventional projects, including the Whirlwind Project, which is now in the process of recommencing mining operations, and the Sheep Mountain Project. In addition, the Company will continue to evaluate the Bullfrog Project. Expenditures for certain of these projects have been adjusted to coincide with expected dates of price recoveries based on the Company’s forecasts. All of these projects serve as important pipeline assets for the Company’s future conventional production capabilities, as market conditions may warrant.

Uranium Sales

During the three months ended September 30, 2022, the Company did not enter into any new uranium sales contracts, having just recently entered into three uranium sale and purchase agreements with major U.S. utilities in May 2022, constituting its first new long-term supply contracts since 2018. Having observed a marked uptick in interest from nuclear utilities seeking long-term uranium supply, the Company remains actively engaged in pursuing additional selective long-term uranium sales contracts. The Company submitted an offer to sell a portion of its inventories currently located at the ConverDyn conversion facility to the DOE’s newly created U.S. Uranium Reserve Program. If the offer is accepted, the Company may complete some sales of uranium during 2022.

Vanadium Sales

As a result of strengthening vanadium markets, during the nine months ended September 30, 2022, the Company sold approximately 642,000 pounds of the Company’s existing inventory of V2O5 (as FeV) at a net weighted average price of $13.69 per pound of V2O5. The Company expects to sell its remaining finished vanadium product when justified into the metallurgical industry, as well as other markets that demand a higher purity product, including the aerospace, chemical, and potentially the vanadium battery industries. The Company expects to sell to a diverse group of customers in order to maximize revenues and profits. The vanadium produced in the 2018/19 Pond Return campaign was a high-purity vanadium product of 99.6%-99.7% V2O5. The Company believes there may be opportunities to sell certain quantities of this high-purity material at a premium to reported spot prices. The Company may also retain vanadium product in inventory for future sale, depending on vanadium spot prices and general market conditions.

RE Carbonate Sales

The Company commenced its ramp-up to commercial production of a mixed RE Carbonate in March 2021 and has shipped all of its RE Carbonate produced to-date to Neo’s Silmet facility in Estonia, where it is currently being fed into their separation process. All RE Carbonate produced at the Mill in 2022 is expected to be sold to Neo for separation at Silmet. Until such time as the Company expects to permit and construct its own separation circuits at the Mill, production in future years is expected to be sold to Neo for separation at Silmet and, potentially, to other REE separation facilities outside of the U.S. To the extent not sold, the Company expects to stockpile mixed RE Carbonate at the Mill for future separation and other downstream REE processing at the Mill or elsewhere. During the quarter ended September 30, 2022, the Company sold approximately 89,000 kilograms of TREO at an average price of $25.03 per kilogram of TREO.

While the Company continues to ramp up its mixed RE Carbonate production and additional funds are spent on process enhancements, improving recoveries, product quality and other optimization, profits from this initiative are expected to be minimal until such time when monazite throughput rates are increased and optimized. However, even at the current throughput rates, the Company is recovering most of its direct costs of this growing initiative, with the other costs associated with ramping up production, process enhancements and evaluating future separation capabilities at the Mill being expensed as underutilized capacity production costs applicable to RE Carbonate and development expenditures. Throughout this process, the Company is gaining important knowledge, experience and technical information, all of which will be valuable for current and future mixed RE Carbonate production and expected future production of separated REE oxides and other advanced REE materials at the Mill. As discussed above, the Company is planning to install a “light” separation circuit within existing Mill facilities and is evaluating installing a separate crack and leach circuit and full separation circuit at the Mill to produce both “light” and “heavy” separated REE oxides in the coming years, subject to successful licensing, financing, and commissioning and continued strong market conditions.

About Energy Fuels: Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. The Company also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up to full commercial-scale production of RE Carbonate. Its corporate offices are in Lakewood, Colorado near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch ISR Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant, as well as RE Carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is currently on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also currently on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest S-K 1300 and NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Cautionary Note Regarding Forward-Looking Statements: This news release contains certain “Forward Looking Information” and “Forward Looking Statements” within the meaning of applicable United States and Canadian securities legislation, which may include, but are not limited to, statements with respect to: production and sales forecasts; costs of production; any expectation that the Company will be awarded any sales under the U.S. Uranium Reserve; scalability, and the Company’s ability and readiness to re-start, expand or deploy any of its existing projects or capacity to respond to any improvements in uranium market conditions or in response to the Uranium Reserve; any expectation as to future uranium, vanadium, RE Carbonate or REE market fundamentals or sales; any expectation as to recommencement of production at any of the Company’s uranium mines or the timing thereof; any expectation regarding any remaining dissolved vanadium in the Mill’s tailings facility solutions or the ability of the Company to recover any such vanadium at acceptable costs or at all; any expectation as to the ability of the Company to secure any new sources of Alternate Feed Materials or other processing opportunities at the Mill; any expectation as to timelines for the permitting and development of projects; any expectation as to longer term fundamentals in the market and price projections; any expectation as to the implications of the current Russian invasion of Ukraine on uranium, vanadium or other commodity markets; any expectation that the Company will maintain its position as a leading uranium company in the United States; any expectation with respect to timelines to production; any expectation that the Mill will be successful in producing RE Carbonate on a full-scale commercial basis; any expectation that Neo will be successful in separating the Mill’s RE Carbonate on a commercial basis; any expectation that Energy Fuels will be successful in developing U.S. separation, or other value-added U.S. REE production capabilities at the Mill, or otherwise, including the timing of any such initiatives and the expected production capacity or capital and operating costs associated with any such production capabilities; any expectation that the Company will restore U.S. rare earth separation capabilities in the coming years; any expectation with respect to the future demand for REEs; any expectation with respect to the quantities of monazite sands to be acquired by Energy Fuels, the quantities of RE Carbonate to be produced by the Mill or the quantities of contained TREO in the Mill’s RE Carbonate; any expectation that any additional supplies of monazite sands will result in sufficient throughput at the Mill to reduce underutilized capacity production costs and allow the Company to realize its expected margins on a continuous basis; any expectation that the Company may sell its separated NdPr oxide (or oxalate) to major electric vehicle manufacturers in the U.S. and Europe or that the Company may position itself as one of the “go to” suppliers of advanced rare earth materials in the U.S.; any expectation that the Bahia Project has the potential to feed the Mill with REE and uranium-bearing monazite sand for decades; any expectation that the Company will complete comprehensive sonic drilling and geophysical mapping at the Bahia Project or complete an Initial Assessment under SK-1300 (U.S.) and a Technical Report Technical Report under NI 43-101 (Canada) during Q4-2023 or Q1-2024, or otherwise; any expectation that the Company’s evaluation of thorium and radium recovery at the Mill will be successful; any expectation that the potential recovery of medical isotopes from any thorium or radium recovered at the Mill will be feasible; any expectation that any thorium, radium or other isotopes can be recovered at the Mill and sold on a commercial basis; any expectation as to the quantities to be delivered under existing uranium sales contracts, or that such contracts may help underpin the Company’s uranium business for many years to come; any expectation that the Company will be successful in completing any additional contracts for the sale of uranium to U.S. utilities; any expectation that any existing or potential future uranium sales contracts will be at prices and quantities that provide an appropriate rate of return or sustain production and cover corporate overhead; any expectation that the value of the Company’s investments accounted for at fair value may improve in future periods; and any expectation that the Company will generate net income in future periods. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans,” “expects,” “does not expect,” “is expected,” “is likely,” “budgets,” “scheduled,” “estimates,” “forecasts,” “intends,” “anticipates,” “does not anticipate,” or “believes,” or variations of such words and phrases, or state that certain actions, events or results “may,” “could,” “would,” “might” or “will be taken,” “occur,” “be achieved” or “have the potential to.” All statements, other than statements of historical fact, herein are considered to be forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements express or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements include risks associated with: commodity prices and price fluctuations; processing and mining difficulties, upsets and delays; permitting and licensing requirements and delays; changes to regulatory requirements; legal challenges; the availability of sources of Alternate Feed Materials and other feed sources for the Mill; competition from other producers; public opinion; government and political actions; available supplies of monazite sands; the ability of the Mill to produce RE Carbonate to meet commercial specifications on a commercial scale at acceptable costs; the ability of Neo to separate the RE Carbonate produced by the Mill to meet commercial specifications on a commercial scale at acceptable costs; market factors, including future demand for REEs; the ability of the Mill to be able to separate radium or other radioisotopes at reasonable costs or at all; market prices and demand for medical isotopes; and the other factors described under the caption “Risk Factors” in the Company’s most recently filed Annual Report on Form 10-K, which is available for review on EDGAR at www.sec.gov/edgar.shtml, on SEDAR at www.sedar.com, and on the Company’s website at www.energyfuels.com. Forward-looking statements contained herein are made as of the date of this news release, and the Company disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or if management’s estimates or opinions should change, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements. The Company assumes no obligation to update the information in this communication, except as otherwise required by law.

SOURCE Energy Fuels Inc.

For further information: Investor Inquiries: Energy Fuels Inc., Curtis Moore, VP – Marketing and Corporate Development, (303) 974-2140 or Toll free: (888) 864-2125, investorinfo@energyfuels.com, www.energyfuels.com

Acquisition creates a global powerhouse in change management

STAMFORD, Conn., November 3, 2022 ― Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced it has acquired Change 4 Growth, an award-winning company specializing in transformational change for enterprises.

Founded in 2017, Change 4 Growth offers market-leading change solutions and expertise to support large-scale business transformations involving people, process and technology. Last year it was named a top 10 change management company in the U.S. by Manage HR magazine.

“The combination of Change 4 Growth and our existing ISG Enterprise Change business creates a global powerhouse in change management at a time when demand for such services is expected to grow significantly,” said Michael P. Connors, chairman and CEO of ISG. “Enterprises are in a state of continuous transformation, as they adjust to new technologies, new competitors, and ever-changing market forces. To be successful, they need a highly adaptable, change-ready workforce.”

The combined business will go to market as ISG Enterprise Change with capabilities in organizational change management (OCM), communications, training development and delivery, leadership development, mentoring, Diversity, Equity and Inclusion (DEI) programs, executive coaching and culture change.

“Transformational change is a complex journey best undertaken with a strong and knowledgeable partner,” said Beth Thomas, CEO and founder of Change 4 Growth, who has been named partner and co-leader of ISG Enterprise Change. “Together, we will offer unrivalled expertise, methodologies and tools to help our clients build and sustain change-capable organizations. We could not be more excited to be joining ISG and expanding the reach of both firms’ industry-leading solutions.”

Among those solutions is ATLAS™, a transformational change platform developed by Change 4 Growth that provides access to OCM templates and tools for greater efficiency and gives clients real-time visibility via dashboards into the progress and health of their business transformations. ISG Enterprise Change intends to offer this new solution to its clients immediately.

Change 4 Growth and ISG Enterprise Change together have successfully conducted more than 1,000 change management engagements involving more than 5 million employees. The two businesses have served more than 300 clients in industries including retail, automotive, manufacturing, banking and financial services, insurance, utilities and healthcare.

For more information about ISG’s OCM services, visit the ISG website.

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 800 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

Reports third-quarter GAAP revenues of $69 million, reflecting negative FX impact of $4 million

Reports net income of $6 million, GAAP EPS of $0.11 and adjusted EPS of $0.14

Reports adjusted EBITDA of $11 million

Achieves record year-to-date results: GAAP revenues of $212 million, up 6% in constant currency; net income of $15 million, up 29%; adjusted EBITDA of $32 million, up 12%; GAAP EPS of $0.30, up 30%; adjusted EPS of $0.40, up 18%

Returns $7 million to shareholders in the form of share repurchases and dividends in Q3

Declares fourth-quarter dividend of $0.04 per share, payable December 19 to record holders as of December 5

Sets fourth-quarter guidance for achieving record full-year revenue and EBITDA performance: revenues between $70 million and $72 million and adjusted EBITDA between $10 million and $11 million

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced financial results for the third quarter ended September 30, 2022.

“ISG remains on track to deliver record full-year revenue and profitability after another solid operating performance in Q3,” said Michael P. Connors, chairman and CEO. “Despite macroeconomic headwinds, in the third quarter we delivered double-digit growth in recurring revenues, as well as in Europe, on an operating basis. Our product mix of higher-margin digital advisory, research and platform services drove the expansion of our adjusted EBITDA margin to 16 percent, our highest-ever quarterly margin.”

Change 4 Growth Acquisition

ISG said today it has acquired Change 4 Growth, a business specializing in transformational change for enterprises. Founded in 2017, Change 4 Growth offers market-leading change solutions and expertise to support large-scale business transformations involving people, process and technology.

“The combination of Change 4 Growth and our existing ISG Enterprise Change business creates a global powerhouse in change management at a time when demand for such services is expected to grow significantly,” said Connors.

ISG estimates demand for organizational change management (OCM) services will grow at a compound annual rate of more than 15 percent over the next five years, as companies continuously adjust to new technologies, new competitors, and ever-changing market forces.

With the acquisition, Connors noted that ISG adds a new platform solution, ATLAS™, that provides access to OCM templates and tools for greater engagement efficiency and gives clients real-time visibility via dashboards into the progress and health of their business transformations.

Third-Quarter 2022 Results

Reported revenues for the third quarter were $68.8 million, down 3 percent from $71.1 million in the prior year, and up 2 percent in constant currency. Currency translation negatively impacted reported revenues by $4.0 million versus the prior year. Reported revenues were $42.2 million in the Americas, down 2 percent versus the prior year, impacted by the completion of a large Automation engagement; $19.3 million in Europe, down 4 percent versus the prior year on a reported basis and up 13 percent in constant currency, and $7.3 million in Asia Pacific, down 10 percent versus the prior year on a reported basis and down 3 percent in constant currency.