SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision Communications Corporation (NYSE: EVC), a leading global advertising solutions, media and technology company, today announced financial results for the three- and twelve-month periods ended December 31, 2022.

Fourth Quarter and Full Year 2022 Highlights

Record fourth quarter and annual revenue

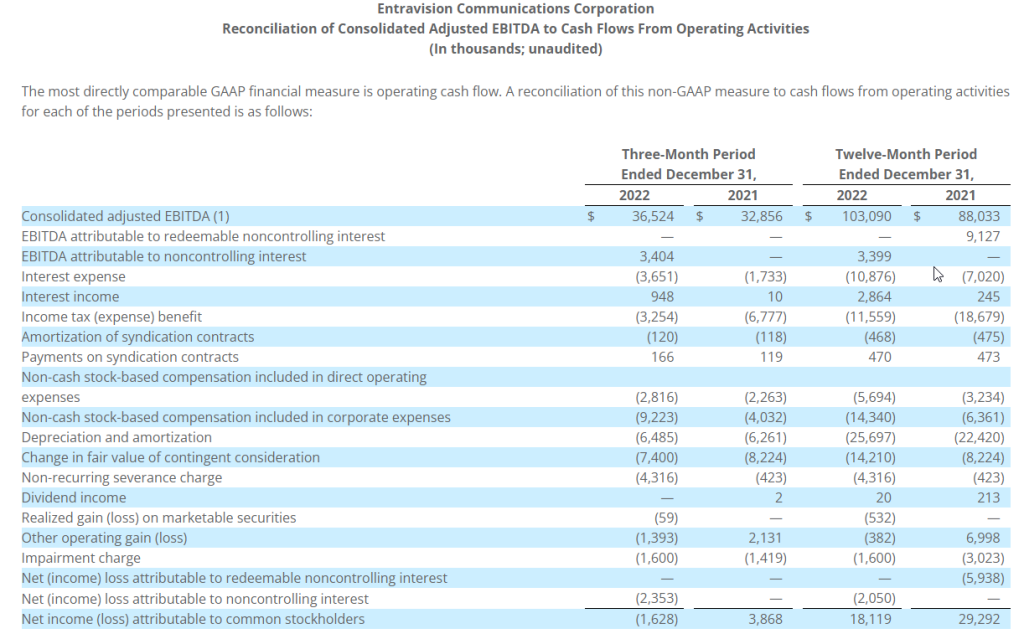

Record fourth quarter and annual consolidated adjusted EBITDA

Record political advertising revenue compared to prior election cycles, including presidential

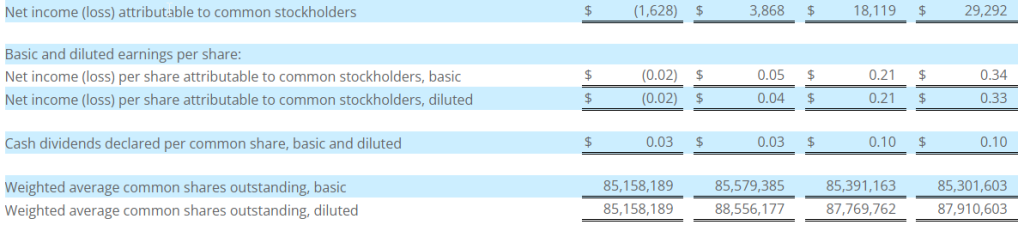

Net loss attributable to common stockholders of $1.6 million in the fourth quarter compared to net income attributable to common stockholders of $3.9 million in the prior-year quarter

Net income attributable to common stockholders for the full year down 38% compared to the prior-year

Consolidated adjusted EBITDA up 11% and 17% compared to the prior-year quarter and full year, respectively

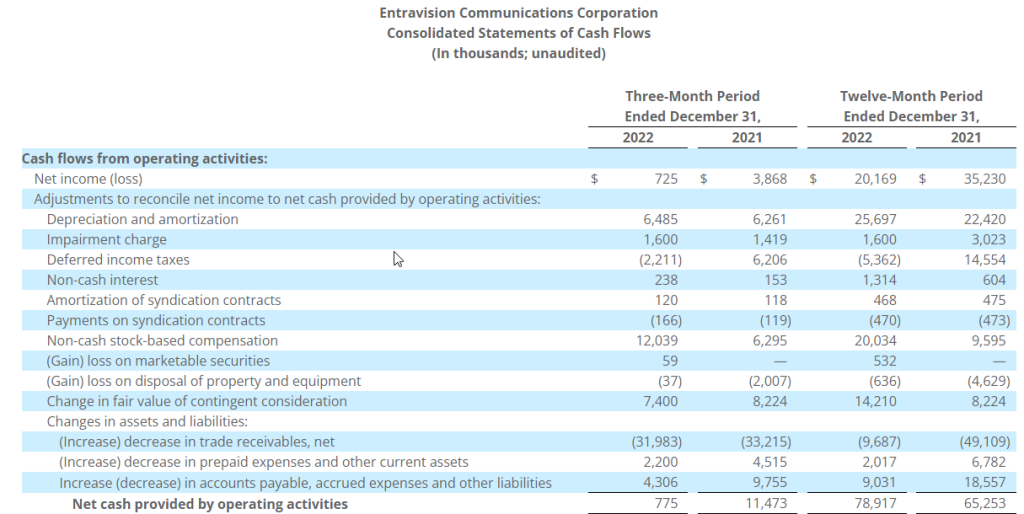

Operating cash flow down 93% and up 21% compared to the prior-year quarter and full year, respectively

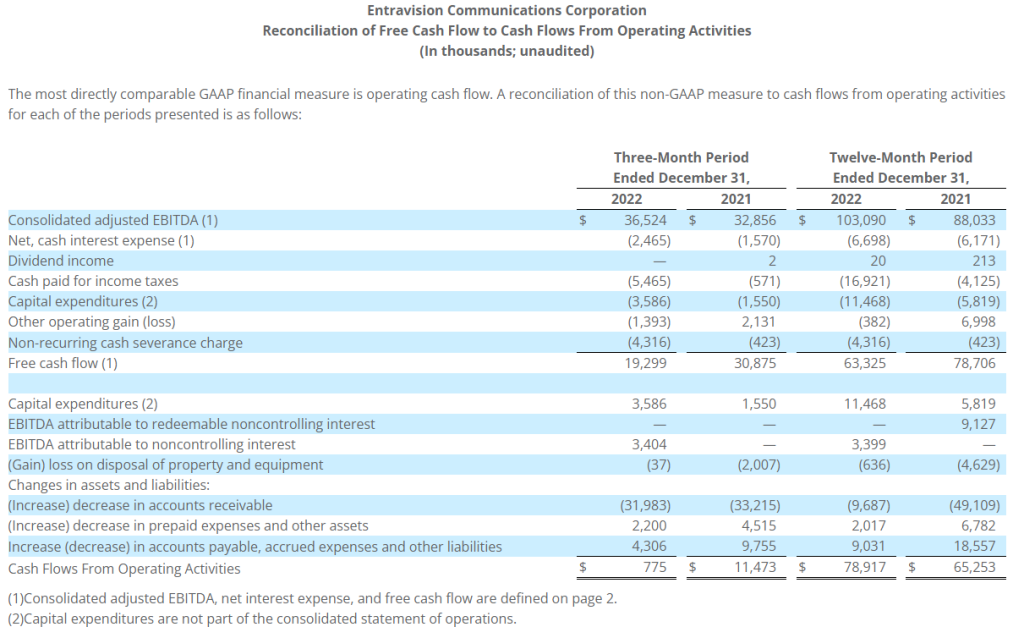

Free cash flow down 37% and 20% compared to the prior-year quarter and full year, respectively

Quarterly cash dividend increase to $0.05 per share

“We are pleased with our 2022 performance, which marks a record year for Entravision for revenue and consolidated adjusted EBITDA,” said Entravision Interim Chief Executive Officer and Chief Financial Officer, Chris Young. “Our results demonstrate the resiliency and strength of our business through challenging macro conditions, and the successful execution of our strategic plan to create a leading global advertising solutions, media and technology company. We have enhanced our digital segment organically, as well as through strategic partnerships, geographic expansion and accretive acquisitions to bolster our suite of digital services in the large and growing advertising industry. Our complementary non-digital businesses, while a smaller percentage of our revenue portfolio, continue to be an important contributor to our growth. We will continue to leverage our tools, reach, technology and world-class team to meet our clients’ evolving needs and deliver enhanced shareholder value.”

Paul Zevnik, Interim Chair and co-founder said, “The Entravision team mourns the sudden and tragic loss of our late CEO, founder and dear friend, Walter Ulloa. Walter passed unexpectedly on the last day of the most successful year in the company’s history. Since we founded Entravision in 1996, we have developed a clear vision to build a leading global advertising solutions, media and technology company serving diverse demographics with diverse media. Through Walter’s leadership and with the support of a strong leadership team and dedicated entrepreneurs across each of Entravision’s business platforms, we have achieved tremendous growth and transformed the Company’s geographical breadth and media portfolio. Most importantly, we created a company that is a great place to work with a focus on engagement, trust, open communications, community service and involvement, and long-lasting relationships with our key partners. I miss our friend dearly, and the Board is committed to working with management to advance Walter’s vision and execute on our roadmap to deliver enhanced value for our stakeholders and partners.”

Quarterly Cash Dividend

As previously announced, the Company’s Board of Directors approved a quarterly cash dividend to shareholders of $0.05 per share on the Company’s Class A and Class U common stock, in an aggregate amount of approximately $4.4 million. This is double the Company’s previous quarterly dividend of $0.025 in 2022 and returns the dividend to its pre-pandemic level. The quarterly dividend will be payable on March 31, 2023 to shareholders of record as of the close of business on March 16, 2023, and the common stock will trade ex-dividend on March 15, 2023. The Company currently anticipates that future cash dividends will be paid on a quarterly basis; however, any decision to pay future cash dividends will be subject to approval by the Board.

Non-GAAP Financial Measures

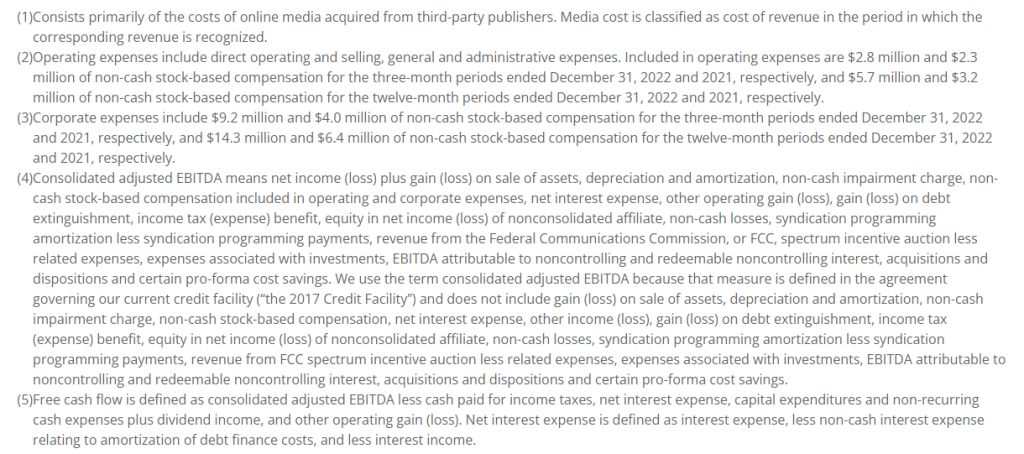

This press release contains certain non-GAAP financial measures as defined by SEC Regulation G. The GAAP financial measure most directly comparable to each of these non-GAAP financial measures, and a table reconciling each of these non-GAAP financial measures to its most directly comparable GAAP financial measure is included beginning on page 10.

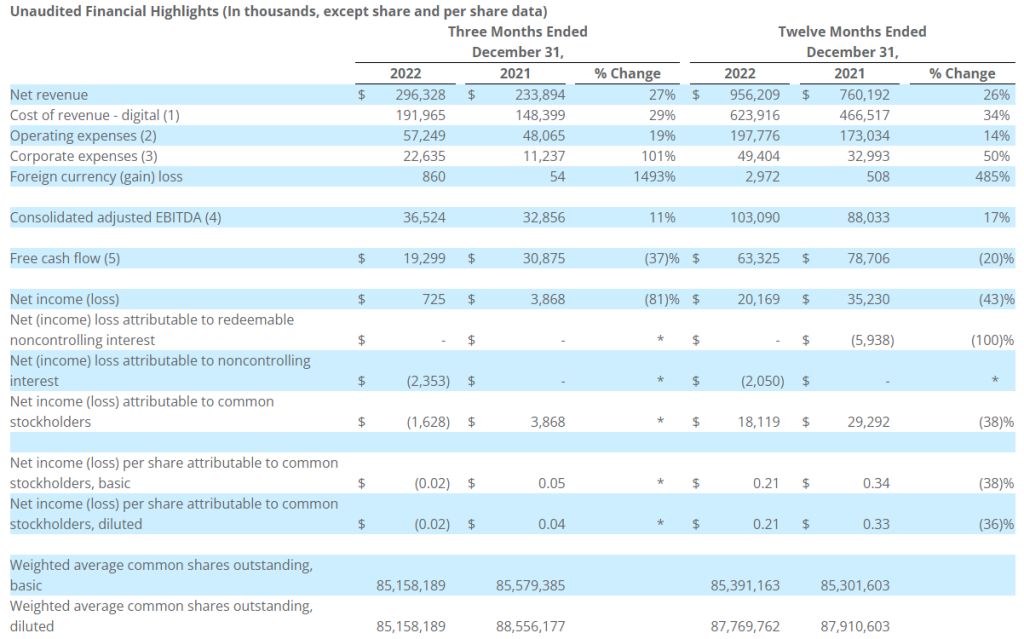

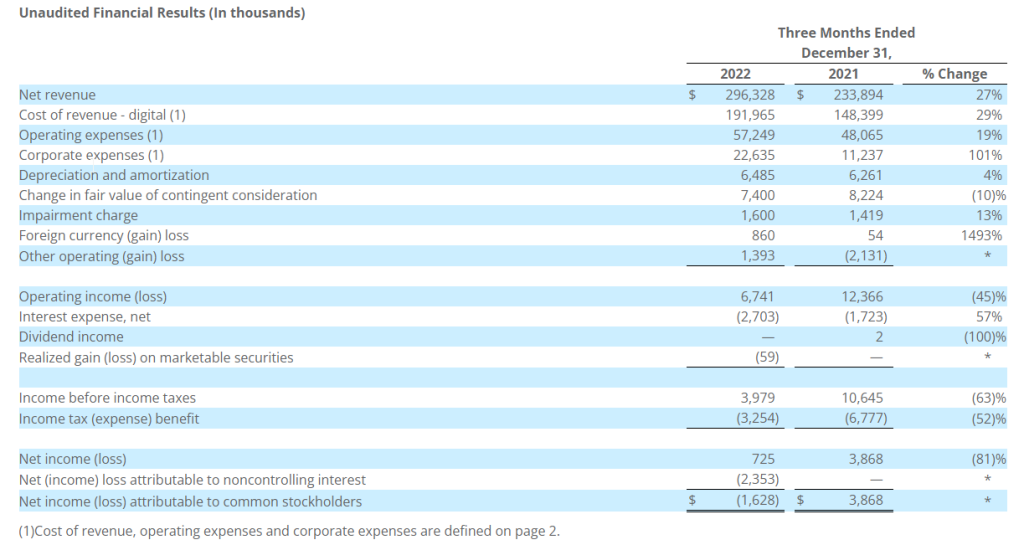

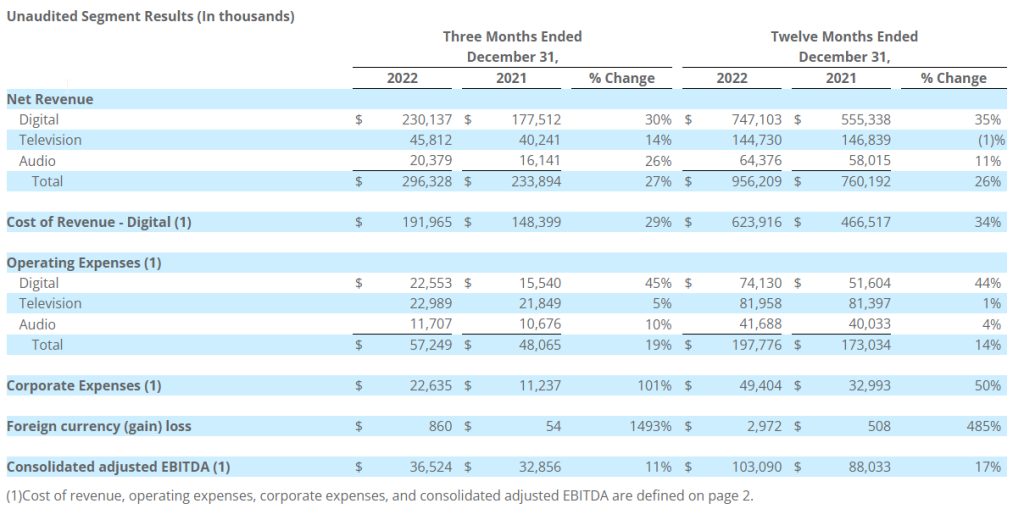

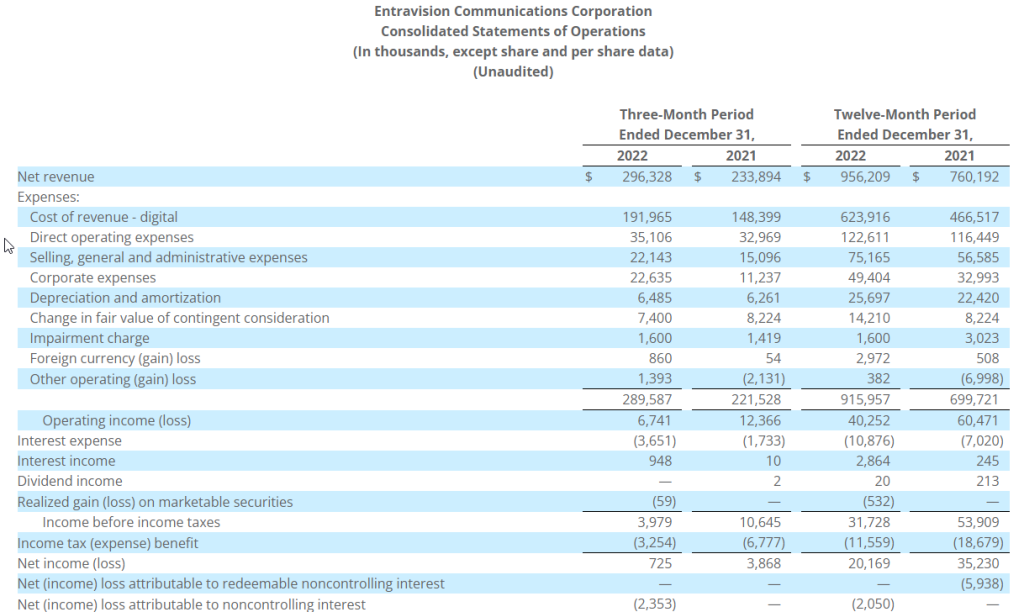

Net revenue in the fourth quarter of 2022 totaled $296.3 million, up 27% from $233.9 million in the prior-year period. Of the overall increase, approximately $52.6 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business. In addition, the increase in net revenue in our digital segment was due to our investments in variable interest entities in 2022, which did not contribute to our results of operations in the comparable prior-year period. In addition, of the overall increase, approximately $5.6 million was attributable to our television segment, primarily due to an increase in political advertising revenue, partially offset by decreases in local and national advertising revenue. These decreases were mainly attributed to the expiration of our Univision and UniMás network affiliation agreements in Orlando, Tampa and Washington, D.C. on December 31, 2021. Additionally, of the overall increase, approximately $4.2 million was attributable to our audio segment, primarily due to increases in political advertising revenue and national advertising revenue, partially offset by a decrease in local advertising revenue.

Cost of revenue in the fourth quarter of 2022 totaled $192.0 million, up 29% from $148.4 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to our investments in variable interest entities in 2022, which did not contribute to our results of operations in the comparable prior-year period.

Operating expenses in the fourth quarter of 2022 totaled $57.2 million, up 19% from $48.1 million in the prior-year period. Of the overall increase, approximately $7.0 million was attributable to our digital segment and was primarily due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense and non-cash stock-based compensation, and an increase due to our investments in variable interest entities in 2022, which did not contribute to our results of operations in the comparable prior-year period. In addition, of the overall increase in operating expenses, approximately $1.1 million was attributable to our television segment primarily due to an increase in rent expense, an increase in bad debt expense and an increase in non-cash stock-based compensation, partially offset by a decrease in expenses associated with the decrease in local and national advertising revenue. Additionally, of the overall increase in operating expenses, approximately $1.0 million was attributable to our audio segment primarily due to an increase in expenses associated with the increase in national advertising revenue and an increase in rent expense.

Corporate expenses in the fourth quarter of 2022 totaled $22.6 million, up 101% from $11.2 million in the prior-year period. The increase was primarily due to $8.1 million of severance related expense incurred upon the passing of our late Chief Executive Officer, and due to increases in non-cash stock-based compensation and an increase in salaries.

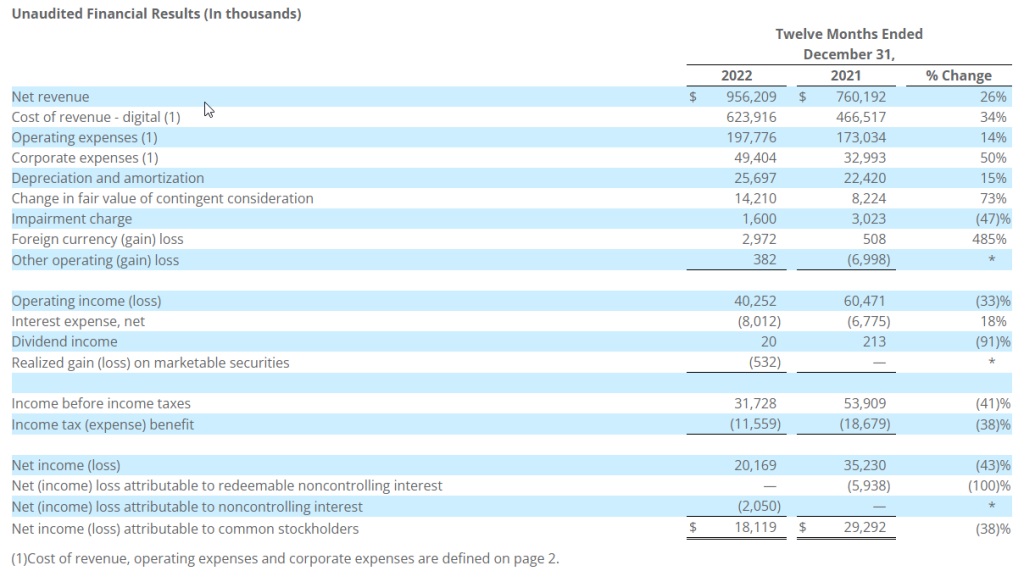

Net revenue for the year ended December 31, 2022 totaled $956.2 million, up 26% from $760.2 million in the prior-year period. Of the overall increase, approximately $191.8 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business. In addition, the increase in net revenue in our digital segment was due to our investments in variable interest entities in 2022 and our acquisitions in 2021, which did not contribute to our results of operations for the full prior-year period. In addition, of the overall increase, approximately $6.4 million was attributable to our audio segment primarily due to increases in political advertising revenue and local advertising revenue, partially offset by a decrease in national advertising revenue. The overall increase was partially offset by a decrease of approximately $2.1 million attributable to our television segment, primarily due to decreases in local and national advertising revenue, a decrease in spectrum usage rights revenue, and a decrease in retransmission consent revenue. These decreases were mainly attributed to the expiration of our Univision and UniMás network affiliation agreements in Orlando, Tampa and Washington, D.C. on December 31, 2021. The decrease in our television segment revenue was partially offset by an increase in political advertising revenue.

Cost of revenue for the year ended December 31, 2022 totaled $623.9 million, up 34% from $466.5 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to our investments in variable interest entities in 2022 and our acquisitions in 2021, which did not contribute to our results of operations for the full prior-year period.

Operating expenses for the year ended December 31, 2022 totaled $197.8 million, up 14% from $173.0 million in the prior-year period. Of the overall increase, approximately $22.5 million was attributable to our digital segment and was primarily due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense and non-cash stock-based compensation, and an increase due to our investments in variable interest entities in 2022 and our acquisitions in 2021, which did not contribute to our results of operations for the full prior-year period. In addition, of the overall increase in operating expenses, approximately $0.6 million was attributable to our television segment primarily due to an increase in rent expense, an increase in bad debt expense and an increase in non-cash stock-based compensation, partially offset by a decrease in expenses associated with the decrease in local and national advertising revenue. Additionally, of the overall increase in operating expenses, approximately $1.7 million was attributable to our audio segment primarily due to an increase in expenses associated with the increase in local advertising revenue and an increase in rent expense.

Corporate expenses for the year ended December 31, 2022 totaled $49.4 million, up 50% from $33.0 million in the prior-year period. The increase was primarily due to $8.1 million of severance related expense incurred upon the passing of our late Chief Executive Officer, and due to increases in non-cash stock-based compensation and an increase in salaries.

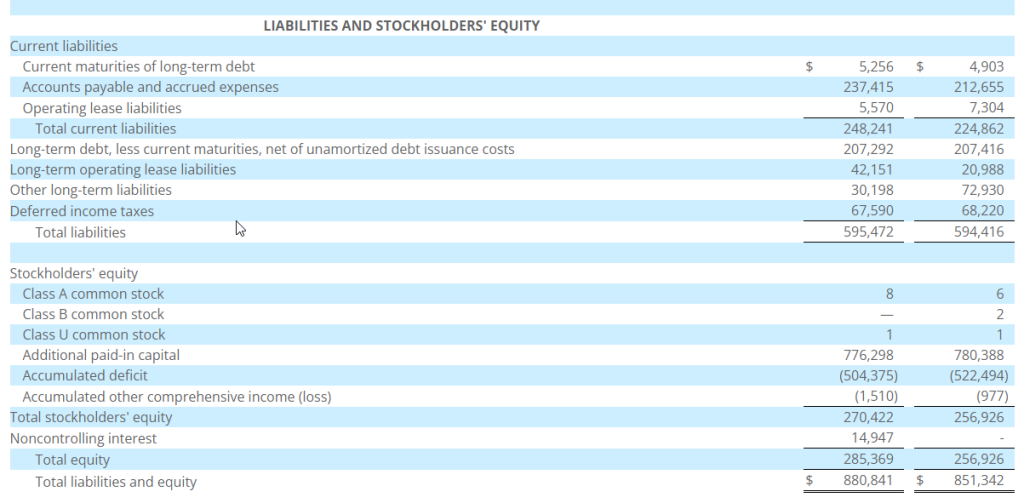

Balance Sheet and Related Metrics

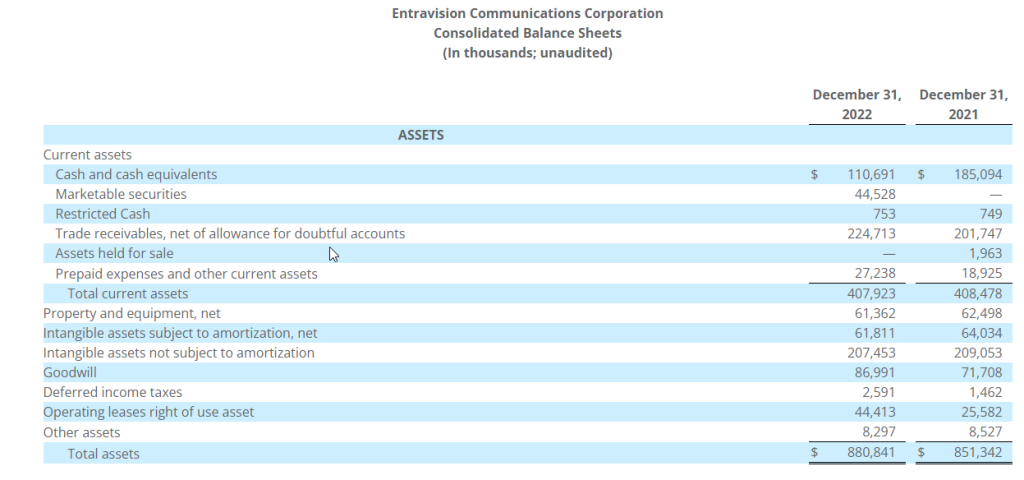

Cash and marketable securities as of December 31, 2022 totaled approximately $155.2 million. Total debt under the Company’s credit agreement was $209.3 million. Net of $75 million of cash and marketable securities, total leverage as defined in the Company’s credit agreement was 1.3 times as of December 31, 2022. Net of total cash and marketable securities, total leverage was 0.5 times.

Notice of Conference Call

Entravision Communications Corporation will hold a conference call to discuss its fourth quarter and full year 2022 results on Thursday, March 9, 2023 at 5:00 p.m. Eastern Time. To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (Int’l) ten minutes prior to the start time and reference Conference ID number 10176187. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

About Entravision Communications Corporation

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, is comprised of four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 45 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Forward-Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements, which are included in accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, may involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance in future periods to be materially different from any future results or performance suggested by the forward-looking statements in this press release. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that actual results will not differ materially from these expectations, and the Company disclaims any duty to update any forward-looking statements made by the Company. From time to time, these risks, uncertainties and other factors are discussed in the Company’s filings with the Securities and Exchange Commission.

Christopher T. Young Interim Chief Executive Officer, and Chief Financial Officer and Treasurer Entravision Communications Corporation 310-447-3870

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q4 results. The company reported Q4 revenue of $120.3 million, an increase of 8.8% from the prior year period, beating our estimate of $118.1 million by 1.8%. Adj. EBITDA of $28.4 million grew by 11% from the same period last year and beat our estimate of $28 million by 1.4%. Digital advertising grew $5.2 million to $36.8 million, up 16.3% from the prior year period.

Soft start to the year. Management guided Q1 revenue to be flat to modestly higher from the year earlier in the range of $100 million to $102 million. Adj. EBITDA to be down yoy in the range of $17.5 million to $18.5 million. National advertising is pacing down 30% in Q1, a decline of $3 million from prior year quarter, with sports accounting for 66%. Its Interactive business has softened and is pacing flat revenues in Q1, while digital advertising is pacing up 12% to 14%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Results. ISG reported record fourth quarter revenue of $74.2 million, up from $69.6 million in the year ago period. FX negatively impacted revenue by $3.2 million. We had estimated $71 million. Fourth quarter net income was $4.3 million, GAAP EPS was $0.09, and adjusted EPS was $0.13. Adjusted EBITDA was $11.1 million, a 9% increase year-over-year. We forecasted net income of $4.45 million, EPS of $0.09, adjusted EPS of $0.13, and adjusted EBITDA of $10.6 million.

Segment Results. Reported revenues were $43.6 million in the Americas, up 12%; $23.9 million in Europe, up 1% on a reported basis and up 12% in constant currency; and $6.7 million in Asia Pacific, down 4% on a reported basis and up 5% in constant currency, all versus the prior year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q4 results. The company reported quarterly revenue of $296.3 million, up 27% from the prior year period, surpassing our estimate of $265.4 million by 11.7%. Adj. EBITDA of $36.5 million increased 11% year over year and beat our estimate of $34.8 million by 5.1%. The quarter was driven by strong digital revenue growth of $52.6 million, up 30% year-over-year.

Capital allocation. The company announced a 100% increase in its quarterly cash dividend, from $0.025 per share to $0.05 per share. Given its favorable cash position of $ $110.7 million and robust free cash flow generation of $63.3 million in 2022, we expect the company to seek additional accretive acquisitions and comfortably pay the dividend. Notably, management highlighted a favorable pipeline of potential targets.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Key executive appointment. Comstock appointed Dr. Fortunato Villamagna as President of Comstock Metals Corporation which owns LINICO Corporation, Comstock’s lithium-ion battery metals recycling business. Dr. Villamagna earned a PhD in Chemistry from McGill University, along with MSc and BSc degrees in Chemistry from Concordia University. His experience in new technology development, commercialization, product introduction, market development, and team building are expected to benefit the growth of Comstock’s battery recycling business.

Reassessing property needs. LINICO agreed to sell its battery recycling facility in the Tahoe-Reno Industrial Center in Nevada for gross proceeds of $27 million ex the legacy processing equipment to American Battery Technology Company (OTCQX, ABML). LINICO had leased the facility with an option to purchase for $15.25 million, of which $3.25 million was paid. Comstock expects to receive net proceeds of approximately $12.5 million. While the sale could extend LINICO’s development time line, the transaction turns a $12 million cash obligation into a $12.5 million net cash inflow.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Stock are Less Likely to Spring Ahead for Daylight Savings Time

Alan Greenspan once made a brief comment saying that there is a correlation between sales of mens underwear and difficult markets ahead. Apparently, the Great Maestro, could support his data with an elasticity of demand chart. The data showed that sales in underpants were extremely consistent, except just before a recession. Another stock market correlation (with likely causation), is daylight savings time and stock prices. This has been the subject of another time-consuming study of numbers by a couple of Yale College professors.

With all stock market traders eager to develop an edge in the market, over time there has been a growing interest in the impact of external factors on the stock market. A study titled “Losing Sleep at the Market: The Daylight-Savings Anomaly,” conducted by Matthew J. Kotchen and Laura E. Grant from Yale University. It explored the impact of DST on stocks. The study found that DST may have a negative impact on the market during the first week after the time change.

Kotchen and Grant’s study focused on the impact of DST on the New York Stock Exchange (NYSE) from 1964 to 2012. They found that during the first week after the springtime change to DST, stock prices tended to dip. This effect was most pronounced on the Monday following the time change, with an average decrease of 0.31% in stock prices. This effect was observed even after controlling for other factors that may have affected the stock market.

One possible explanation for this phenomenon is that the disruption to people’s sleep patterns may affect their productivity and decision-making abilities. This could lead to a decrease in trading activity and a temporary decline in stock prices. Another explanation is that the time change may lead to a decrease in trading volume due to confusion or technical glitches.

It’s worth noting that the effect of DST on the stock market, while statistically significant, is not very large and normally short-lived. The study found that the negative impact on stock prices disappeared after the first week, and there was no significant impact during the fall transition out of DST.

While Kotchen and Grant’s study sheds light on the impact of DST on the stock market, it’s important to keep in mind that many other factors have a much greater impact on stock prices. Economic indicators, political events, and company earnings reports are just a few examples of factors that can affect the stock market. Investors should not view this as significant enough to trade off of.

Take Away

“Losing Sleep at the Market: The Daylight-Savings Anomaly” suggests that DST may have a small, temporary negative impact on the stock market during the first week after the time change. However, the overall impact of DST on the stock market is likely to be small compared to other factors that affect stock prices.

The SVB Loss Demonstrates A Risk Investors Should Pay Attention To

Individual investors and even some institutional money managers are reminded of a helpful truth from the Silicon Valley Bank (SVB) balance sheet problem. The reminder of the investment risk stands in conflict with what many top firms have been recommending to investors. So it should be revisited because, unlike banks, individuals and wealth managers tend to have a wider variety of places to look for return.

Bank balance sheet management is tricky. I say this with some credibility. In August of 2008, I accepted a role as the Treasurer of a mid-sized bank just two weeks before Freddie Mac and Fannie Mae were placed into conservatorship, and three weeks before Lehman filed for bankruptcy. I was responsible for quickly finding solutions for a big potential balance sheet problem. It was a problem similar to SVB’s. Depositors at the bank were taking money out at a faster pace than bank investments, including loans cashflows, could cover. Money that had not been committed to loans were invested in low-risk investment-grade fixed-income securities. It was nerve-racking, at one point, I calculated if any two of the largest ten customers withdrew all of their funds, the bank would not have the ability to cover the withdrawal. The pain that SVB is faced with is not dissimilar.

SVB is a bank that serves many fledgling companies during a period when capital and investment in start-ups have weakened from the days of easier money just a couple of years ago. Banks make money by borrowing short from customers (demand deposits, checking, and CDs) and then lend long, presumably at a higher rate. Here they make the spread that a typical upward-sloping yield curve provides. The main risk is in maturity. What happens if your longer-term loans were made at Fed Funds plus 2.50% two years ago when average deposit costs were 0.20%, since today Fed Funds are 4.50%? Your loans are paying the bank less than the bank’s cost to fund them with short deposits. This is a risk that all banks manage – balance sheet risk.

As deposits ran off at SVB because of business conditions in Silicon Valley, the bank turned to its investment portfolio to fund withdrawals. Securities in a US bank portfolio, when purchased, are designated at the custodian, by the Treasurer, either “Trading” which in this department of the bank is rare, “Available for Sale,” which provides the treasury department the ability to sell if need be, but also requires the assets to be priced at market (this impacts the banks valuation), or “Hold to Maturity” where the fixed income securities appear on the balance sheet at cost.

If the securities are designated at purchase “Hold to Maturity” and the bank finds itself needing to sell any “Hold to Maturity” security, all securities marked “Hold to Maturity” become what regulators call tainted. The entire portfolio also becomes designated “Available for Sale.” This decision could dramatically reduce the bank’s book value in cases when interest rates have risen and bond values have dropped.

In the case of SVB, its securities portfolio, designed to earn more than deposits, was marked “Available for Sale.” When they sold, the market values were in such a lower position, from just a year earlier, that they recognized a dramatic loss. A $1.8 billion dollar loss which prompted its shares to lose more than half their market price.

Self-Directed Investors and Money Managers Should Note

The SVB explanation above, wernt a long way to remind that bonds, including US Treasury Notes have prices that rise and fall. They are different than equities, but price risk is real, and the $1.8 billion loss SVB recognized is front page proof. But since the beginning of the year many top-tier investment firms have recommended investors increase these fixed income investments and capture the new higher yields. Some even suggested ETFs in mortgaged-backed securities (MBS) or emerging markets (EM).

Goldman Asset Management is just one of the respected firms that have loudly suggested fixed income investments (CNBC, February 7, 2023)

Bond prices fall as rates rise. The Chair of the Federal Reserve, the same person that had orchestrated near zero rates, has clearly stated that the Fed will continue orchestrating higher rates. So while the stock market has been unattractive over the past 14 months, so have bonds. The difference, of course, is that bond math is absolute. As rates rise, the present value of any fixed-income security is calculated by the future value of future cash flow – this more or less determines the bonds price movement. For example, if an investor buys a bond that yields 3%, and later rates go to 6% for the same maturity, the present value is about halved. This is a plausible scenario currently, with inflation near 6%.

Stock indexes have taken a beating over the past 14 months, just like bonds. The difference is rising rates sink all bonds. It doesn’t sink all stocks.

So while the S&P 500 is down 17% since January 1, 2022, and the Russell 2000 small-cap index is down 20%, one doesn’t even have to get out of the A’s to find AT&T (T) is up 4.15% in the same period, and Canadian Company Alvopetro (ALVOF) is up 43.6%). You won’t find this type of disparity in performance or direction on the fixed-income side. US Treasuries were down 10.5% for the period.

So from one perspective, stock selection may provide potential upside, whereas rising rates could mathematically sink all bond portfolio holdings.

Take Away

Silicon Valley Bank is in a unique situation as its customer base is not very diversified. The challenges they face may be similar to other banks, but this does not appear indicative of the whole sector based on recent stress tests. Banks are restricted in what they can invest in, with rates having risen, and promised to rise more, fixed-income holdings are at a loss in many portfolios, SVB’s need to raise cash caused them to recognize what was already a market loss.

Investors, however, can take a lesson from the loss the bank took. While I have seen articles this year suggesting capitalizing on higher interest rates, the ten-year US Treasury Note is well below its historical average (40-yr. avg.+5.17% vs 3.73% today). And rates are not even returning a real rate of return relative to current and expected inflation. This would indicate a period of likely market losses on bond holdings put on today.

A Stock, or portfolio of stocks, of course, may also present losses, but the odds that any particular stock, or even an index, would seem less certain than bonds.

VIRGINIA CITY, NEVADA, MARCH 9, 2023 – Comstock Inc. (NYSE: LODE) (“Comstock” or the “Company”) today announced that it will host a conference call on Thursday, March 16, 2023, at 1:15 p.m. Pacific Daylight Time (4:15 p.m. Eastern Daylight Time) to report its 2022 year end results and business update. The webcast will include a moderated question and answer session after the Company’s prepared remarks. Please click the link below to register in advance and please join the event at least 10 minutes prior to the scheduled start time.

Once registered, you will receive a confirmation email containing information about joining the Webcast.

March 16, 2023, 1:15 PM Pacific Daylight Time / 4:15 PM Eastern Daylight Time (US and Canada)

Topic: Comstock’s Year End 2022 Results and Business Update

Please click here to register in advance for this webcast.

About Comstock

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon and through the deployment of more advanced mineral and material discovery technologies. To learn more, please visit www.comstock.inc.

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future industry market conditions; future explorations or acquisitions; future changes in our exploration activities; future prices and sales of, and demand for, our products; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; and future working capital, costs, revenues, business opportunities, debt levels, cash flows, margins, taxes, earnings and growth. These statements are based on assumptions and assessments made by our management considering their experience and their perception of historical and current trends, current conditions, possible future developments, and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; ability to achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology, quantum computing and advanced materials development, and development of cellulosic technology in bio-fuels and related carbon-based material production; ability to successfully identify, finance, complete and integrate acquisitions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether because of new information, future events, or otherwise.

Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Contact information:

Comstock Inc. P.O. Box 1118 Virginia City, NV 89440 www.comstock.inc

Corrado De Gasperis Executive Chairman & CEO Tel (775) 847-4755 degasperis@comstockinc.com

Zach Spencer Director of External Relations Tel (775) 847-5272 Ext.151 questions@comstockinc.com

Preparing multiple uranium mines for production, completing profitable sales & developing rare earth refining capacity to power up to 1 million EVs per year by late-2023 or early-2024, while strengthening the balance sheet and avoiding debt.

LAKEWOOD, Colo., March 8, 2023 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”) today reported its financial results for the year ended December 31, 2022. The Company’s Annual Report on Form 10-K has been filed with the U.S. Securities and Exchange Commission (“SEC“) and may be viewed on the Electronic Document Gathering and Retrieval System (“EDGAR“) at www.sec.gov/edgar.shtml, on the System for Electronic Document Analysis and Retrieval (“SEDAR“) at www.sedar.com, and on the Company’s website at www.energyfuels.com. Unless noted otherwise, all dollar amounts are in U.S. dollars.

Financial Highlights:

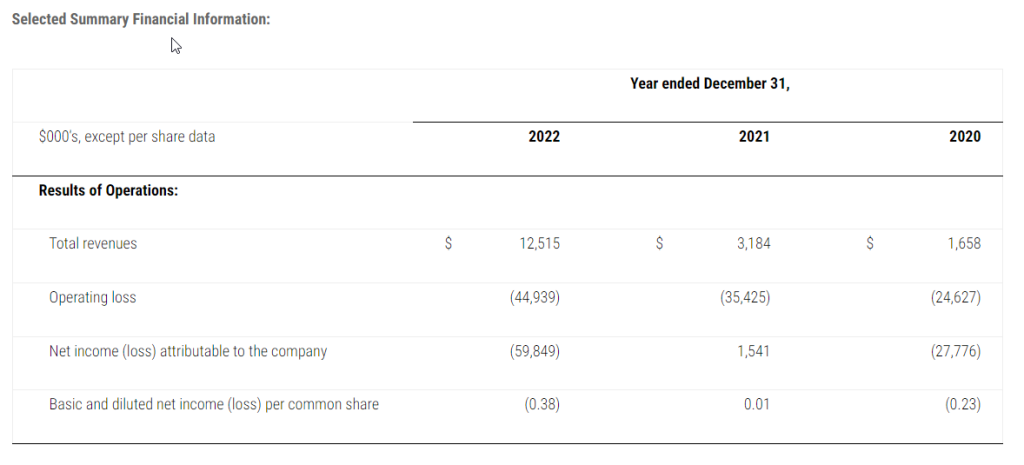

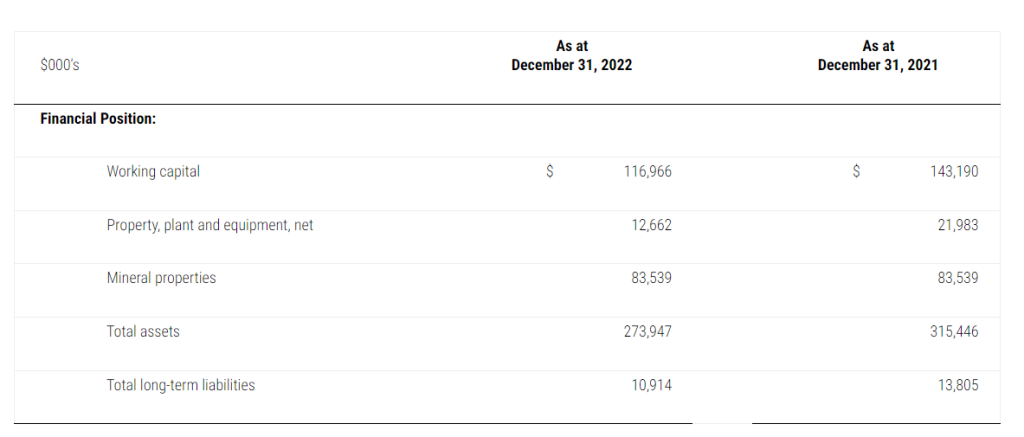

At December 31, 2022, the Company had a robust balance sheet with $116.97 million of working capital, including $62.80 million of cash and cash equivalents, $12.19 million of marketable securities, $38.16 million of inventory, and no debt. At current commodity prices, the Company’s product inventory has a value of $62.48 million;

During the year ended December 31, 2022, the Company incurred a net loss of $59.85 million or $0.38 per share, due in large part to: i) a non-cash mark-to-market loss on investments accounted for at fair value of $16.90 million; ii) increased expenses associated with preparing four(4) of our uranium mines for production; iii) development expenses associated with developing commercial rare earth element (“REE“) separation capabilities in addition to our existing mixed REE carbonate (“RE Carbonate“) commercial production capabilities; (iv) expenses associated with advancing our medical isotope initiatives;(v) increased selling, general and administrative expenses arising from costs associated with acquiring the South Bahia monazite sand project in Brazil (the “Bahia Project“) and costs associated with the sale of the Company’s Alta Mesa in situ recovery (“ISR“) project in Texas; and (vi) increased other selling, general and administrative expenses associated with significant additions to personnel, enhanced business processes, and other general and administrative expenses required to support all these increased levels of activity.

The Company held 1,027,000 pounds of finished uranium (“U3O8“) inventory at year end, along with approximately 985,000 pounds of finished vanadium (“V2O5“) inventory. At March 8, 2023, following sale and purchase transactions discussed below, the Company held 847,000 pounds of U3O8 and approximately 945,000 pounds of V2O5 inventory.

Uranium Highlights:

During 2022, the Company produced 162,000 pounds of U3O8 at its White Mesa Mill in Utah (the “Mill“) and remains the largest producer of uranium in the U.S.

During 2022, the Company was awarded four (4) new uranium supply contracts, with deliveries beginning in 2023, of which three (3) are long-term contracts with U.S. nuclear utilities and one (1) is with the U.S. government to supply the newly established strategic U.S. Uranium Reserve (“U.S. Uranium Reserve“).

In January 2023, the Company completed the sale of 300,000 pounds of U.S.-origin U3O8 to the U.S. Uranium Reserve realizing total gross proceeds of $18.47 million, or $61.57 per pound of U3O8, resulting in an expected margin of approximately $35.85 per pound of uranium.

During Q4-2022 and Q1-2023, the Company purchased a total of 301,052 pounds. of U.S.-origin U3O8 on the spot market for a weighted-average price of $50.08 per pound.

During 2022, the Company made significant progress in preparing four (4) of its conventional uranium and uranium/vanadium mines to be ready to resume uranium ore production, including significant workforce expansion and performing needed rehabilitation of surface and underground infrastructure.

On February 15, 2023, the Company announced it had completed its previously announced sale of its Alta Mesa ISR Project to enCore Energy Corp. (“enCore“) for total consideration of $120 million, comprised of $60 million in cash and $60 million in a secured convertible note bearing interest at a rate of eight percent (8%) per annum, convertible into common shares of enCore at a price of $2.9103 per share. This sale of a lower priority project provides Energy Fuels with significant additional cash and working capital, enabling the Company to ramp-up its US industry-leading uranium and REE production, while avoiding dilution to shareholders.

Rare Earth Element Highlights:

During 2022, the Company produced approximately 205 metric tons (“MT“) of high-purity, partially separated RE Carbonate from monazite, containing approximately 95 MT of total rare earth oxides (“TREO“), which is the most advanced REE material being produced commercially in the U.S. today. In Q4-2022, the Company received approximately 600 MT of monazite, which is expected to be processed into 375 to 485 MT of RE Carbonate, containing 175 to 225 MT or TREO, during 2023.

In early 2023, the Company began modifying and enhancing its existing solvent extraction (“SX“) circuits at the Mill to be able to produce separated REE oxides (“Phase 1“). “Phase 1” is expected to be completed and fully commissioned by late 2023 or early 2024 and have the capacity to produce roughly 800 to 1,000 MT of recoverable separated neodymium-praseodymium (“NdPr“) oxide per year, subject to securing sufficient monazite feed, or enough to provide the permanent magnets to power up to 1 million electric vehicles (“EVs“) per year, which is expected to position the Company as one of the world’s leading producers of NdPr outside of China. “Phase 1” capital costs are expected to total approximately $25 million. The Company is also proceeding with engineering on further enhancements to expand NdPr production capability (“Phase 2“) by 2026 and to produce separated dysprosium (“Dy“), terbium (“Tb“) and potentially other REE materials in the future (“Phase 3“) from monazite and potentially other REE process streams by 2027.

On February 13, 2023, the Company announced it had completed its previously announced acquisition of a large heavy mineral project in Brazil (the “Bahia Project“), which has the potential to supply the Company’s growing REE business with significant quantities of REE-bearing natural monazite sand for decades. The Bahia Project also contains significant quantities of high-value titanium (ilmenite and rutile) and zirconium (zircon) minerals.

The Company is currently in active discussions with several additional suppliers of natural monazite around the world to significantly increase the supply of feed for our growing REE initiative.

Vanadium Highlights:

During 2022, the Company sold approximately 642,000 pounds of existing V2O5 inventory (as ferrovanadium, “FeV“), for an average weighted net price of $13.67 per pound of V2O5.

Medical Isotope Highlights:

The Company continued advancing its program to evaluate the potential to recover radioisotopes from its process streams for use in emerging targeted alpha therapy (“TAT“) cancer therapeutics.

Mark S. Chalmers, Energy Fuels’ President and CEO, stated:

“2022 was an extraordinary year for Energy Fuels as we expanded our US industry-leading uranium business and established a new, sustainable US rare earth supply chain that is already commercially producing the most advanced rare earth material in the US today. We believe we have clearly emerged as one of the leading U.S. critical mineral companies, producing many of the raw materials needed for the clean energy transition.

“In 2022, positive uranium market fundamentals were magnified by concerns over security of supply, potentially creating new market dynamics for nuclear fuel. Nations around the world are embracing nuclear, as it provides clean, carbon-free electricity on a 24/7 basis, making it indispensable in the fight against climate change. Existing uranium mines globally are depleting, and underinvestment in new mines globally over the past several years could cause supply shortfalls in the coming years. These market fundamentals alone are the best I’ve seen in decades. Then, just over a year ago, Russia invaded Ukraine. Regrettably, the world has allowed Russian state-owned entities to exert disproportionate influence over global uranium and nuclear fuel supply chains over the past several years. Our company has been a leader warning about the inherent risks of such dependence since at least 2017. Most governments and utilities are taking concrete action to stop funding Russia’s war effort in Ukraine through uranium and nuclear fuel purchases. Energy Fuels continues to stand ready to supply and increase the availability of secure, US-produced uranium.

“We have been very active in the uranium space over the past year. In 2022, we began readying several of our conventional uranium and uranium/vanadium mines for production. We have hired about 30 people, and we are making the investments required to put one or more of these facilities into production as soon as later this year. We were also the only U.S. company to produce material quantities of uranium in 2022, having produced 162,000 pounds during Q4-2022, far more than any other company in the U.S. We are proud to have had the opportunity to sell 300,000 pounds of U.S.-produced uranium to the newly established strategic U.S. Uranium Reserve, which is a small but important step in re-establishing the U.S. nuclear fuel capabilities that will allow us to reduce our reliance on Russian uranium imports. We also have another 260,000 pounds of uranium deliveries to a U.S. utility later this year. Our strong uranium inventory position, which currently sits at 847,000 pounds along with another approximately 351,000 pounds contained in ore on the pad at the Mill, together with planned production, will allow us to meet contract deliveries over the life of those contracts, while also providing the flexibility to sell into the spot market and sign new long-term contracts under favorable market conditions.

“2022 was also an incredible year for our rare earth business. No other company is making progress like Energy Fuels in the rare earth space. We continued to produce and optimize our production of partially separated mixed RE Carbonate, though we produced less than expected due to a delay in deliveries that pushed late-2022 production into early-2023. We announced that we are beginning development of a rare earth separation circuit at the Mill that is expected to be commissioned in late-2023 or early-2024. Once operational, this circuit will have the capacity to produce up to 1,000 MT of refined NdPr oxide per year, or enough for up to one million EVs per year. We are also securing the monazite required to feed our rare earth infrastructure, including our recent acquisition of the Bahia Project — a large rare earth, titanium and zirconium project in Brazil — with additional third-party purchases of monazite from Chemours and others expected to be in the pipeline. Today, Energy Fuels’ mixed RE Carbonate is already the most advanced rare earth material commercially produced in the U.S. If we continue to be successful, no other U.S. company will be producing commercial quantities of refined NdPr products ready for offtake as quickly as Energy Fuels.

“We opportunistically sold some of our vanadium inventory in 2022, and we are looking to potentially sell more with V2O5 prices gaining strength recently. Further, our medical isotope initiative is continuing to progress well, and we hope to have more announcements on this very soon.

“Finally, we continue to manage our cash, assets, and working capital to achieve all these heightened initiatives. We take pride in maintaining a strong balance sheet and maintaining the flexibility to do big things. At the end of 2022, we had about $117 million of working capital, with inventories considerably worth more if you apply today’s market prices for uranium and vanadium. In January 2023, we completed the sale of 300,000 pounds of U3O8 to the U.S. Department of Energy for $18.5M. In February 2023, we closed on the sale of our Alta Mesa property in Texas, adding another $120 million to our treasury. Of this, $60 million is in cash and $60 million is in a convertible note bearing interest at eight percent per annum, or about $4.8 million per year.

“We accomplished a great deal over the past year, but this is just the beginning. We have market, geopolitical, and societal tailwinds behind all the commodities we produce, and we fully intend to continue building our critical mineral processes and capabilities. We look forward to providing more updates on future milestones as we achieve them in the weeks and months to come.”

Webcast at 11:00 am ET on March 10, 2023:

Energy Fuels will be hosting a video webcast on March 10, 2023 at 11:00 1m ET (9:00 am MT) to discuss its FY-2022 financial results, the outlook for 2023, and its uranium, rare earths, vanadium, and medical isotopes initiatives. To join the webcast and access the presentation and viewer-controlled webcast slides, please click on the link below:

By clicking this link and registering your name and phone number, the system will call you and place you directly into the call without talking to an operator. If you wish to call in on your own, please dial in to 1-888-664-6392 (toll free in the U.S. and Canada).

A link to a recorded version of the proceedings will be available on the Company’s website shortly after the webcast by calling 1-888-390-0541 (toll free in the U.S. and Canada) and by entering the code 145847#. The recording will be available until March 24, 2023.

Financial Discussion:

At December 31, 2022, the Company had $116.97 million of working capital, including $74.27 million of cash and cash equivalents and marketable securities and $38.16 million of inventory, including approximately 1,027,000 pounds of uranium and 985,000 pounds of high-purity vanadium, both in the form of finished, immediately marketable product. The current spot price of U3O8, according to TradeTech, is $50.50 per pound, and the current mid-point spot price of V2O5, according to Fastmarkets, is $10.78 per pound. Based on those spot prices, the Company’s uranium and vanadium inventories have a current market value of $51.86 million and $10.62 million, respectively, totaling $62.48 million

For the year ended December 31, 2022, we recognized a net loss of $59.85 million or $0.38 per share compared to net income of $1.54 million or $0.01 per share for the year ended December 31, 2021. The change between periods was primarily due to (i) a gain of $35.73 million recognized on the sale of a portfolio of the Company’s non-core conventional uranium projects to Consolidated Uranium Inc. (“CUR“) in 2021 primarily in exchange for shares in CUR; (ii) a non-cash mark-to-market loss on investments accounted for at fair value of $16.90 million in 2022 due primarily to a decrease in the market price of our CUR shares over 2022 (iii) increased expenses in 2022 associated with preparing four (4) of our uranium mines for production or operational readiness amounting to $2.4 million; (iv) development expenses in 2022 associated with developing commercial REE separation capabilities in addition to our existing mixed RE Carbonate commercial production capabilities; (v) expenses in 2022 associated with advancing our medical isotope initiatives; (vi) increased transaction expenses in 2022 arising from costs associated with acquiring the Bahia Project and costs associated with the sale of the Company’s Alta Mesa project in Texas; and (vii) increased other selling, general and administrative expenses in 2022 of $10.2 million associated with significant additions to executive and management/supervisory personnel (including non-cash share-based compensation of $2.5 million), enhanced business processes, and other general and administrative expenses required to support all these increased levels of activity, partially offset by increased revenues in 2022.

Sale to the U.S. Uranium Reserve:

On December 16, 2022, the Company announced it had been awarded a contract to sell 300,000 pounds of U3O8 for $18.5 million ($61.57 per pound of U3O8) to the U.S. government for the establishment of the U.S. Uranium Reserve, resulting in an expected margin of approximately $35.85 per pound of uranium. The Uranium Reserve is intended to be a backup source of supply for domestic nuclear power plants in the event of a significant market disruption. The Company completed the transfer and received the proceeds in January 2023.

Update on Rare Earth Initiatives and the Bahia Project:

Earlier this year, the Company began “Phase 1” REE separation, which includes modifications and enhancements to the existing SX circuits at the Mill. “Phase 1” is expected to have the capacity to process approximately 8,000 to 10,000 MT of monazite per year, producing roughly 4,000 to 5,000 MT TREO, containing roughly 800 to 1,000 MT of recoverable separated NdPr oxide per year. Because Energy Fuels is utilizing existing infrastructure at the Mill, “Phase 1” capital is expected to total only about $25 million. “Phase 1” is expected to be operational later this year or early 2024, subject to receipt of sufficient monazite supply and successful development and commissioning. If these milestones are achieved, Energy Fuels believes it will be the ‘first to market’ among U.S. companies with commercial quantities of separated NdPr available to EV, renewable energy, and other companies for offtake. Later, the Company expects to complete further enhancements to the Mill to expand NdPr production capability (“Phase 2“) by 2026 and to produce separated Dy, Tb and potentially other REE materials in the future (“Phase 3“) from monazite and potentially other REE-bearing process streams by 2027.

On February 13, 2023, the Company announced it had completed the previously announced acquisition of the Bahia Project located between the towns of Prado and Caravelas in the State of Bahia, Brazil totaling 15,089.71 hectares (approximately 37,300 acres or 58.3 square miles). The Bahia Project is a well-known heavy mineral sand (“HMS“) deposit that has the potential to supply 3,000 – 10,000 MT of natural monazite per year for decades to the Mill for processing into high-purity RE Carbonate, separated REE oxides and other REE products and materials. The Bahia Project is also expected to produce large quantities of high-quality titanium (ilmenite and rutile) and zirconium (zircon) minerals that are also in high demand. REE production is highly complementary to Energy Fuels’ existing US-leading uranium business, as monazite and other major REE-bearing minerals naturally contain uranium that will be recovered and other impurities that will be removed at the Mill before further processing into advanced high-purity REE materials. 3,000 – 10,000 MT of monazite contains roughly 1,500 – 5,000 MT of TREO, including 300 – 1,000 MT of NdPr and significant commercial quantities of Dy and Tb.

Prior to the closing on the Bahia Project, the Company commenced a sonic drilling program to further define and quantify the HMS resource, particularly at depth. The limited sonic drilling completed by Energy Fuels over the past few months appears to be confirming that the mineral-bearing sands continue at depth. The Company finished phase 1 of sonic drilling at the Bahia Project on February 14, 2023 totaling 2,266 meters. The Company plans to announce phase 1 drilling results this year and start phase 2 drilling in Q3-2023. Once data from both drill programs are available, the Company plans to engage industry leaders to calculate an initial mineral resource estimate for use in an S-K 1300 (U.S.) compliant Initial Assessment and an NI 43-101 (Canada) compliant Technical Report.

Prior owners of the Bahia Project performed extensive exploration work on the property, including the drilling of over 3,300 hand augur drill holes and a gamma survey of the region. Data from the drilling was used to publish highly detailed exploration and “reserve” reports prepared between 2016 and 2022 that were submitted to the National Mineral Agency of Brazil (“ANM“) in order to move the areas forward toward mining. Based on these seventeen historical reports dated between October 20, 2016 and April 29, 2022, the Bahia Project is estimated to contain 204 million MT of HMS, containing 7.18 million MT of heavy minerals at an average grade of 3.52%, including monazite concentrations in the HMS concentrate between 0.66% and 13.1%. It should be noted that these numbers are historical in nature and a Qualified Person under S-K 1300 or NI-43-101 has not done sufficient work to classify the estimates as a current estimate of Mineral Resources, Mineral Reserves, or exploration results. The Company is not treating these estimates as a current estimate of Mineral Resources, Mineral Reserves or exploration results. Further drilling and data collection might not prove out these numbers.

Sale of Alta Mesa Property to enCore Energy:

On February 15, 2023, the Company announced it had completed the sale (the “Closing“) of three (3) wholly owned subsidiaries that together hold the Alta Mesa ISR Project (“Alta Mesa“) to enCore Energy Corp. (“enCore“) for total consideration of $120 million (the “Transaction“). The consideration is comprised of:

$60 million cash at or prior to Closing; and

$60 million in a secured convertible note (the “Note“), payable two (2) years from the Closing, bearing annual interest of eight percent (8%). The Note will be convertible at Energy Fuels’ election into enCore common shares at a conversion price of $2.9103 per share, being a 20% premium to the 10-day volume-weighted average price of enCore shares ending the day before the Closing. enCore was recently listed on the NYSE American and also trades on the TSX Venture Exchange.

The Note is guaranteed by enCore and is fully secured by Alta Mesa. Unless a block trade or similar distribution is executed by Energy Fuels to sell enCore shares received upon conversion of the Note, Energy Fuels will be limited to converting the Note into a maximum of $10 million principal amount per thirty (30) day period.

In addition, enCore replaced the existing reclamation bonds for the Alta Mesa project shortly after the Closing, which will result in Energy Fuels receiving an additional $3.6 million cash as a return of collateral from those bonds. The Transaction is also expected to reduce the Company’s holding costs related to Alta Mesa by approximately $2 million per year.

The Transaction provides Energy Fuels with significant additional cash and working capital, enabling the Company to ramp-up its US industry-leading uranium and REE production, while avoiding dilution to shareholders. In addition, the Note provides Energy Fuels with significant exposure to uranium market upside through potential conversion into enCore common shares.

Operations Update and Outlook for 2023:

Overview

The Company continues to believe that uranium supply and demand fundamentals point to higher sustained uranium prices in the future. The Company believes that nuclear energy, fueled by uranium, is experiencing a global resurgence with an increased focus by governments, policymakers, and citizens on decarbonization, electrification, and security of energy supply. In addition, Russia’s invasion of Ukraine and the entry into the uranium market by financial entities purchasing uranium on the spot market to hold for the long-term has the potential to result in higher sustained spot and term prices and, perhaps, induce utilities to enter into more long-term contracts with non-Russian producers like Energy Fuels to foster security of supply, avoid transportation issues, and ensure more certain pricing.

In 2022, we entered into three long-term uranium contracts with major U.S. utilities for which the Company is beginning to perform the necessary work to recommence production at one or more of its mines, starting as soon as 2023. Until such time when the Company has ramped back up to commercial uranium production, it can rely on its significant uranium inventories to fulfill its new contract requirements, including its recent purchases of U.S. origin uranium on the spot market.

The Company is seeking additional sources of natural monazite to supply feedstock to its emerging REE projects. The Company is also evaluating the potential to recover radioisotopes for use in the development of TAT medical isotopes for the treatment of cancer and continues its support of U.S. governmental activities to assist the U.S. uranium mining industry, including expanding the new U.S. Uranium Reserve Program, supporting efforts to restore domestic nuclear fuel capabilities, and advocating for the responsible sourcing of uranium and nuclear fuel.

We continually evaluate the optimal mix of production, inventory and purchases in order to retain the flexibility to deliver long-term value.

Mill Activities

During the year ended December 31, 2022, the Company recovered and packaged approximately 162,000 pounds of its final uranium product, U3O8, at the Mill, which was added to the Company’s finished product inventory. The Mill recovered an additional small quantity of uranium, which was retained in-circuit and was not packaged in 2022. During 2022, the Mill also focused on its mixed RE Carbonate production and produced approximately 205 MT of high-purity, partially separated mixed RE Carbonate during 2022, while working to secure additional monazite ore feedstock to increase production. The Mill did not recover any vanadium in 2022.

During 2023, the Company does not plan to recover uranium at the Mill, other than from its monazite processing which will likely remain in circuit and not be packaged in 2023. During early 2023, the Company expects to process approximately 600 MT of monazite delivered late in 2022 from Chemours and recover approximately 175 to 225 MT of TREO at the Mill in the form of approximately 375 to 485 MT of RE Carbonate. The Company expects to receive an additional 400 – 700 MT of monazite from Chemours later in 2023, which the Company expects to process for the recovery of uranium and production of separated NdPr and a heavy REE (Sm+) Re Carbonate upon commissioning of the Mill’s Phase 1 REE Separation circuit in late 2023 or early 2024. The Company is also in active discussion with several parties globally to acquire additional quantities of natural monazite, which if secured and delivered to the Mill, could result in significant additional quantities of uranium and separated NdPr and heavy REE (Sm+) Re Carbonate production in 2024 and beyond.

No vanadium production is currently planned during 2023, though the Company continually monitors its inventory and vanadium markets to guide future potential vanadium production.

Conventional Mine Activities

During the year ended December 31, 2022, the Company performed rehabilitation and development work on its La Sal, Beaver, Whirlwind and Pinyon Plain projects for future potential production, including engineering, procurement, construction management, increased development activities, significant workforce expansion and needed rehabilitation of surface and underground infrastructure, while its other conventional mining properties remain on standby. The Company expects to continue its rehabilitation and development work, as it prepares these mines for future production. Although, the timing of the Company’s plans to extract and process mineralized materials from these projects will be based on current contract requirements, inventory levels, sustained improvements in general market conditions, procurement of suitable sales contracts and/or the expansion of the U.S. Uranium Reserve Program, the Company is making the investments required to put one or more of these facilities into production as soon as later in 2023.

The Company is selectively advancing certain permits at its other major conventional uranium projects, such as the Roca Honda, Sheep Mountain, and Bullfrog Projects. All these projects serve as important pipeline assets for the Company’s future conventional production capabilities, as market conditions may warrant.

ISR Mine Activities

The Company expects to produce insignificant quantities of U3O8 in the year ending December 31, 2023 from Nichols Ranch. Until such time when (i) market conditions improve sufficiently, (ii) suitable term sales contracts can be procured, and/or (iii) the U.S. Uranium Reserve Program is expanded, the Company expects to maintain the Nichols Ranch Project on standby and defer development of further wellfields and header houses. The Company currently holds 34 fully permitted, undeveloped wellfields at Nichols Ranch, including four additional wellfields at the Nichols Ranch wellfields, 22 wellfields at the adjacent Jane Dough wellfields, and eight wellfields at the Hank Project, which is fully permitted to be constructed as a satellite facility to the Nichols Ranch Plant.

Inventory

As of December 31, 2022, the Company had approximately 1,027,000 pounds of finished uranium inventories located at North American conversion facilities. Additionally, the Company had approximately 351,000 pounds of additional U3O8 contained in stockpiled Alternate Feed Materials and other ore inventory at the Mill that can be recovered relatively quickly in the future, as general market conditions may warrant. During Q1-2023, the Company completed the purchase 120,000 additional pounds of uranium and the sale of 300,000 pounds of uranium to the U.S. Uranium Reserve, resulting in the Company holding approximately 847,000 pounds of U3O8 in inventory as of March 8, 2023. The Company expects to deliver 260,000 pounds of U3O8 under its existing uranium term contracts in 2023, resulting in expected uranium inventories to total approximately 587,000 pounds of U3O8 at year-end 2023, subject to currently unplanned uranium spot sales and purchases.

The Company currently has approximately 945,000 pounds of V2O5 in inventory, and there remains an estimated 1.0 to 3.0 million pounds of additional solubilized recoverable V2O5 remaining in tailings solutions awaiting future recovery, as market conditions may warrant.

Sales Update and Outlook for 2023

Uranium Sales

While the Company did not sell uranium during the year ended December 31, 2022, the Company entered into four (4) uranium sale and purchase agreements in 2022, three (3) with major U.S. nuclear utilities and one (1) with the U.S. Uranium Reserve. Under these contracts, the Company expects to sell 560,000 pounds of U3O8 during 2023 with an expected weighted-average sales price of $58 – $60 per pound, subject to then-prevailing market prices at the time of delivery.

The three (3) utility contracts require deliveries of uranium between 2023 and 2030, with base quantities totaling 3.0 million pounds of uranium over the period, and up to 4.1 million pounds of uranium if all remaining options are exercised. Having observed a marked uptick in interest from nuclear utilities seeking long-term uranium supply, the Company remains actively engaged in pursuing additional selective long-term uranium sales contracts. During 2023, the Company expects to sell 260,000 pounds of its U3O8 inventory into these contracts at an expected sales price of approximately $54 – $58 per pound, subject to inflation and spot prices in effect at the time of delivery. In addition, in January 2023, the Company completed the sale of 300,000 pounds of its inventories located at ConverDyn to the U.S. Uranium Reserve, receiving total proceeds of $18.47 million ($61.57 per pound).

To provide the Company with additional flexibility to fulfill its contract obligations and gain direct exposure to potential future uranium price increases, the Company has recently purchased a total of 301,052 lbs. of U.S. origin uranium on the spot market for a weighted-average gross price of approximately $50.08 per pound.

Vanadium Sales

As a result of strengthening vanadium markets, during the year ended December 31, 2022, the Company sold approximately 642,000 pounds of the Company’s existing inventory of V2O5 (as FeV) at a net weighted average price of $13.67 per pound of V2O5. The Company expects to sell its remaining finished vanadium product when justified into the metallurgical industry, as well as other markets that demand a higher purity product, including the aerospace, chemical, and potentially the vanadium battery industries. The Company expects to sell to a diverse group of customers in order to maximize revenues and profits. The vanadium produced in the 2018/19 Pond Return campaign was a high-purity vanadium product of 99.6%-99.7% V2O5. The Company believes there may be opportunities to sell certain quantities of this high-purity material at a premium to reported spot prices.

The Company intends to continue to selectively sell itsV2O5 inventory on the spot market as markets warrant but will otherwise continue to maintain its vanadium in inventory.

Rare Earth Sales

The Company commenced its commercial production of a mixed RE Carbonate in March 2021 and has shipped all its RE Carbonate produced to-date to Neo Performance Material’s (“Neo’s“) REE separation plant, Silmet, located in Estonia where it is currently being fed into their separation process. All RE Carbonate produced at the Mill in 2022 was sold to Neo for separation at Silmet. Until such time as the Company commissions its own separation circuits at the Mill, which is expected to be in late 2023 or early 2024, all or a portion of RE Carbonate production is expected to be sold to Neo for separation at Silmet and/or, potentially, to other REE separation facilities outside of the U.S. To the extent not sold, the Company expects to stockpile mixed RE Carbonate at the Mill for future separation and other downstream REE processing at the Mill or elsewhere. During the year ended December 31, 2022, the Company sold approximately 89,000 kilograms of RE Carbonate at an average price of $23.88 per kilogram of RE Carbonate.

While the Company continues to make progress on its mixed RE Carbonate production and additional funds are spent on process enhancements, improving recoveries, product quality and other optimization, profits from this initiative are expected to be minimal until such time when monazite throughput rates are increased and optimized. However, even at the current throughput rates, the Company is recovering most of its direct costs of this growing initiative, with the other costs associated with ramping up production and process enhancements at the Mill being expensed as underutilized capacity production costs applicable to RE Carbonate and development expenditures. Throughout this process, the Company is gaining important knowledge, experience and technical information, all of which are valuable for current and future mixed RE Carbonate production and planned future production of separated REE oxides and other advanced REE materials at the Mill or elsewhere.

ABOUT ENERGY FUELS