Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Consolidation. Last week, Titan announced a decision to consolidate production within its North American manufacturing footprint, which will result in the closure of its manufacturing facility in Jackson, Tennessee, by the end of October 2026. The Company expects production currently performed in Jackson to be transitioned to other existing Titan facilities over the coming months. We view this action as part of the Company’s ongoing efforts to optimize its manufacturing footprint and improve capacity utilization, given the uncertain operating environment.

Details. The Jackson closure is part of the ongoing synergies the Company expected to deliver from the Carlstar acquisition. The one-time costs for the plant closure and manufacturing relocation are estimated to be in the $7 million range, likely to hit in relatively equal amounts over the next three quarters. Estimated annual savings are in the $5 million range, with the full amount likely to begin in 2027.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

WEST CHICAGO, Ill., March 18, 2026 /PRNewswire/ — Titan International, Inc. (NYSE: TWI) (“Titan” or the “Company”), a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products, today announced a decision to consolidate production within its North American manufacturing footprint, which will result in the closure of its manufacturing facility in Jackson, Tennessee by the end of October 2026.

The Company expects production currently performed in Jackson to be transitioned to other existing Titan facilities over the coming months. This action is part of Titan’s ongoing efforts to optimize its manufacturing footprint and improve capacity utilization.

“The decision to consolidate production and close the Jackson facility is difficult knowing the impact it has on our team members and their families,” said Paul Reitz, President and CEO of Titan International. “Titan continues to take deliberate actions to improve its operating efficiency while maintaining the flexibility and scale required to serve our customers.”

The closure of the Jackson, TN facility will impact approximately 140 people and Titan is committed to supporting affected employees through this transition. The Company will work closely with local leadership and provide assistance to impacted team members, including severance, benefits continuation and job placement support. The Company will continue to operate a robust network of manufacturing facilities across North America to support its customers across outdoor power equipment, powersports, agriculture, construction, earthmoving, and other off‑highway end markets.

About Titan: Titan International, Inc. (NYSE: TWI) is a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products. Headquartered in West Chicago, Illinois, the company globally produces a broad range of products to meet the specifications of original equipment manufacturers (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets. For more information, visit www.titan-intl.com.

ACCO Brands Corporation is one of the world’s largest designers, marketers and manufacturers of branded academic, consumer and business products. Our widely recognized brands include AT-A-GLANCE®, Esselte®, Five Star®, GBC®, Kensington®, Leitz®, Mead®, PowerA®, Quartet®, Rapid®, Rexel®, Swingline®, Tilibra®, and many others. Our products are sold in more than 100 countries around the world. More information about ACCO Brands, the Home of Great Brands Built by Great People, can be found at www.accobrands.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Despite continued demand challenges globally and tariff-related disruptions in the U.S., ACCO maintained or grew its market position in most categories, demonstrating the resilience and strength of the brand portfolio. ACCO delivered sales and adjusted EPS in-line with management’s outlook.

4Q25 Results. Net sales were $428.8 million, down 4.3% y-o-y, reflecting soft global demand for certain products, partially offset by growth in gaming accessories. We were at $435 million. Comp sales were down 7.8%. Adjusted EBITDA totaled $68.6 million, or a 16% margin, compared to $73.6 million and 16.4%, respectively, in 4Q24. ACCO reported adjusted EPS of $0.38, flat with the $0.39 reported in 4Q24. We were at $0.38.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Fourth quarter sales of $155 million, EPS of ($0.19), Adjusted EBITDA of $2.3 million

CVG named Zoox Robotaxi low voltage wire harness strategic supplier

Provides outlook and guidance for full year 2026

NEW ALBANY, Ohio, March 10, 2026 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its fourth quarter and full year ended December 31, 2025.

Fourth Quarter 2025 Highlights(Compared with prior-year period, where comparisons are noted)

Revenue of $154.8 million, down 5.2% due primarily to softer North American demand.

Operating loss of $1.8 million, and adjusted operating loss of $0.9 million, improved compared to operating loss of $5.3 million and adjusted operating loss of $4.3 million. The decrease in operating loss was driven primarily by improved gross margin performance and lower SG&A expenses.

Net loss from continuing operations of $6.4 million, or $(0.19) per diluted share, compared to net loss of $35.0 million, or $(1.04) per diluted share. Net loss in the prior-year period included a non-cash tax valuation allowance of $28.8 million. Adjusted net loss from continuing operations of $6.0 million, or $(0.18) per diluted share, compared to adjusted net loss of $5.1 million, or $(0.15) per diluted share.

Adjusted EBITDA of $2.3 million, up 155.6%, with an adjusted EBITDA margin of 1.5%, up from 0.6%.

Free cash flow of $8.8 million, up $7.9 million, due to better working capital management.

Full Year 2025 Highlights(Compared with prior-year period, where comparisons are noted)

Revenue of $649.0 million, down 10.3%, driven by softer North American Class 8 production volumes.

Operating loss of $0.7 million, improved by $0.1 million, and adjusted operating income of $4.8 million, down $1.7 million. The change in adjusted operating income was due to lower sales volumes, partially offset by lower SG&A expenses.

Free cash flow of $34.0 million, up $21.5 million, due to better working capital management and reduced capital expenditures. Total debt decreased $29.1 million compared to year-ended 2024.

The Global Electrical Systems segment returned to growth driven by the contribution of new business ramps, with margin expansion supported by the continued shift of production capacity to new, lower-cost facilities in Morocco and Mexico.

James Ray, President and Chief Executive Officer, said, “We are encouraged by the resilience and consistency seen in our fourth quarter results. The actions we took to drive operational efficiencies and right-size our footprint continued to pay off, highlighted by the year-over-year gross margin improvement of 190 basis points seen last quarter. Our focus on our cost structure also drove a full year decline of $4.8 million in SG&A expenses in 2025. We expect to see continued operating leverage into 2026 as we ramp new business wins and our end markets stabilize and start to recover.”

Mr. Ray continued, “After returning to growth in the third quarter, we saw further acceleration in our Global Electrical Systems segment revenue and margins as we continue to ramp new wins in that business, most significantly the Zoox autonomous vehicle platform. We expect continued growth in 2026 in this segment. In our Global Seating segment, we saw operating margin expansion, even in a softer demand environment, driven by operational efficiencies and cost reductions. Our Trim Systems and Components segment faced continued weakness in the North American Class 8 truck market, but we have taken proactive steps that we believe will lead to improved profitability in this segment. I’m encouraged by the momentum we are building in our businesses, as a result of our operational efficiencies and in advance of end market recovery.”

Andy Cheung, Chief Financial Officer, added, “CVG delivered results consistent with our adjusted full-year guidance. We continue to see margin benefits from the strategic actions we’ve taken. Furthermore, our focus on working capital and capital expenditure reductions supported strong free cash flow, both in the fourth quarter and for the full year. Looking to 2026, we expect to see revenue and EBITDA growth for the company, prioritizing free cash flow for debt paydown.”

Consolidated Results from Continuing Operations

Fourth Quarter 2025 Results

Fourth quarter 2025 revenues were $154.8 million compared to $163.3 million in the prior year period, a decline of 5.2%. The decrease in revenues was due to lower sales as a result of a softening in North American customer demand in the Global Seating and Trim Systems & Components segments.

Operating loss for the fourth quarter 2025 was $1.8 million compared to operating loss of $5.3 million in the prior year period. Excluding special costs, the fourth quarter of 2025 adjusted operating loss was $0.9 million, compared to adjusted operating loss of $4.3 million in 2024. The improvement in adjusted operating loss was driven primarily by improved gross margin performance and lower SG&A expenses.

Interest expense was $4.2 million and $2.2 million for the fourth quarter ended December 31, 2025 and 2024, respectively, due to higher interest rates.

Net loss from continuing operations was $6.4 million, or $(0.19) per diluted share, for the fourth quarter 2025 compared to net loss of $35.0 million, or $(1.04) per diluted share, in the prior year period.

On December 31, 2025, the Company had $16.8 million of outstanding borrowings on its U.S. revolving credit facility and $1.4 million on its China credit facility, $33.3 million of cash and $101.8 million availability from the credit facilities (subject to customary borrowing base and other conditions), resulting in total liquidity of $135.1 million.

Fourth Quarter 2025 Segment Results (Compared with prior-year period, where comparisons are noted)

Global Seating Segment

Revenues were $70.7 million compared to $74.8 million for the prior year period, a decrease of 5.6% primarily due to lower sales volume as a result of decreased customer demand.

Operating income was $1.1 million compared to $0.7 million in the prior year period, an increase of $0.4 million, primarily due to lower SG&A expenses. The fourth quarter of 2025 adjusted operating income was $1.8 million compared to $0.6 million in the prior year period, an increase of 175.9%.

Global Electrical Systems Segment

Revenues were $49.7 million compared to $44.0 million in the prior year period, an increase of 12.7%, primarily as a result of ramping new business wins.

Operating income was $0.8 million compared to operating loss of $3.0 million, an increase of $3.8 million, primarily attributable to higher sales and operating efficiencies. The fourth quarter of 2025 adjusted operating income was $0.9 million compared to adjusted operating loss of $3.0 million in the prior year period, an increase of $3.9 million.

Trim Systems and Components Segment

Revenues were $34.4 million compared to $44.4 million in the prior year period, a decrease of 22.5%, primarily due to lower sales volumes.

Operating loss was $1.5 million compared to $0.1 million in the prior year period, a decrease of $1.4 million. The decrease in operating income was primarily attributable to lower demand. The fourth quarter of 2025 adjusted operating loss was $1.4 million compared to income of $0.9 million in the prior year period.

Outlook

CVG is providing the following outlook for the full year 2026:

This outlook reflects, among others, current industry forecasts for North American Class 8 truck builds. According to ACT Research’s February report, 2026 North American Class 8 truck production levels are expected to be approximately 260,000 units. The 2025 actual Class 8 truck builds according to the ACT Research was 251,247 units.

The outlook for the Construction end market reflects low-single digit growth in 2026.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Wednesday, March 11, 2026, at 8:30 a.m. ET. Management intends to reference the Q4 2025 Earnings Call Presentation posted on our website during the conference call. To participate, dial (800) 549-8228 using conference code 45919. International participants dial (289) 819-1520 using conference code 45919.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at www.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 45919 and international callers can dial (289) 819-1325 using access code 45919.

Company Contact

Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Commercial Vehicle Group, Inc. and its subsidiaries, is a global provider of systems, assemblies and components to global commercial vehicle markets and electric vehicle markets. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. For this purpose, any statements contained herein that are not statements of historical fact, including without limitation, certain statements herein regarding industry outlook, the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment, including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions or divestitures, production of new products, plans for capital expenditures and our results of operations or financial position and liquidity, may be deemed to be forward-looking statements. Without limiting the foregoing, the words “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions, as they relate to us, are intended to identify forward-looking statements. The important factors discussed in “Item 1A – Risk Factors” in the Company’s Annual Report on Form 10-K, among others, could cause actual results to differ materially from those indicated by forward-looking statements made herein and presented elsewhere by management from time to time. Such forward-looking statements represent management’s current expectations and are inherently uncertain. Investors are warned that actual results may differ from management’s expectations. Additionally, various economic and competitive factors could cause actual results to differ materially from those discussed in such forward-looking statements, including, but not limited to, factors which are outside our control.

Any forward-looking statement that we make in this press release speaks only as of the date of such statement, and we undertake no obligation to update any forward-looking statement or to publicly announce the results of any revision to any of those statements to reflect future events or developments. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should only be viewed as historical data.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Titan ended 2025 with another positive quarter as fourth quarter revenue, gross margin, and adjusted EBITDA exceeded fourth quarter 2024 results. These results are ahead of management’s revenue guidance and also better than adjusted EBITDA expectations. The EMC segment was the standout performer, with revenue growth of 21% and gross margin expansion of 3.4 percentage points.

4Q25 Results. Revenue grew 7.0% to $410.4 million. Ex foreign exchange, the Ag segment was flat, EMC up nicely, and Consumer down modestly. Adjusted EBITDA came in at $11 million, up 18% y-o-y. Due to non-cash valuation allowances, Titan recorded a GAAP net loss of $56 million in the quarter, compared to net income of $1.3 million in 4Q24. Adjusted net loss was $17.4 million, or $0.27/sh, compared to net income of $5.8 million, or $0.09/sh, in 4Q24.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

WEST CHICAGO, Ill., Feb. 26, 2026 /PRNewswire/ — Titan International, Inc. (NYSE: TWI) (“Titan” or the “Company”), a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products, today reported financial results for the fourth quarter and year ended December 31, 2025. The full earnings release including a reconciliation of GAAP to Non-GAAP figures can be found in the investor relations section of the Company’s website at https://ir.titan-intl.com/news-and-events/news-releases/default.aspx.

Q4 2025 Key Figures

Revenues grew 7% to $410 million

Gross margin improved to 10.9%

Adjusted EBITDA increased 18% to $11 million

Paul Reitz, President and Chief Executive Officer, commented, “We wrapped-up 2025 with another positive quarter as our Q4 2025 results exceeded Q4 2024 in terms of revenue, gross margin and Adjusted EBITDA. Our EMC segment was a standout performer, with revenue growth of 21% and gross margin expansion of 3.4 percentage points. Importantly, we anticipate continued growth in this segment in 2026. Our Ag segment recorded a top-line increase of 2.6% in the fourth quarter, roughly flat excluding FX. Going into 2026 in Ag we expect demand for smaller equipment to outpace high-horsepower units as farmers continue to contend with elevated input costs and weaker commodity prices. In our Consumer segment, fourth quarter sales were up slightly within our Specialty division, while down modestly overall. Focusing on 2026, OEMs and their dealer networks look to have generally reached the end of their finished goods destocking and we expect to see some benefit from that as a result. A resumption in demand would therefore flow through to demand for tires, wheels and other components. It also bears repeating that our Consumer segment enjoys a high proportion of aftermarket sales and therefore is less susceptible to the OEM cycles.”

Mr. Reitz concluded, “Over the past couple years visibility across our end markets has been constrained — and that added complexity creates an advantage for Titan with our One Stop Shop strategy. Our diversified supply chain offers global manufacturing, strategic sourcing and JVs and this gives us flexibility to adapt quickly to the frequent changes we continue to see in trade policy and ultimately allows us to serve our customers better than anyone else. By keeping our customers at the forefront of everything we do, we continue to cement our market leadership position. We remain well positioned for an Ag market rebound and as always, we will continue to prioritize our customers and in doing so, we expect 2026 will be a good year for Titan.”

First Quarter and Fiscal Year 2026 Outlook

Tony Eheli, Chief Financial Officer, stated, “We ended the year with a strong balance sheet and maintained a disciplined expense profile that drove improvements in margin and profitability, while allowing us to continue to invest in our product, people, and processes. We expect to start 2026 with a seasonal uptick in activity with Q1 sales between $490 million and $510 million and Adjusted EBITDA between $28 million and $33 million. For the full year we are expecting revenue in the $1.85 to $1.95 billion range with Adjusted EBITDA between $105 million and $115 million.”

About Titan

Titan International, Inc. (NYSE: TWI) is a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products. Headquartered in West Chicago, Illinois, the Company globally produces a broad range of products to meet the specifications of original equipment manufacturers (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets. For more information, visit www.titan-intl.com.

Safe Harbor Statement

This press release contains forward-looking statements. These forward-looking statements are covered by the safe harbor for “forward-looking statements” provided by the Private Securities Litigation Reform Act of 1995. The words “believe,” “expect,” “anticipate,” “plan,” “would,” “could,” “potential,” “may,” “will,” and other similar expressions are intended to identify forward-looking statements, which are generally not historical in nature. These forward-looking statements are based on our current expectations and beliefs concerning future developments and their potential effect on us. Although we believe the assumptions upon which these forward-looking statements are based are reasonable, these assumptions are subject to significant risks and uncertainties, and are subject to change based on various factors, some of which are beyond Titan International, Inc.’s control. As a result, any of these assumptions could prove to be inaccurate and the forward-looking statements based on these assumptions could be incorrect. The matters discussed in these forward-looking statements are subject to risks, uncertainties, and other factors that could cause actual results and trends to differ materially from those made, projected, or implied in or by the forward-looking statements depending on a variety of uncertainties or other factors including, but not limited to, the effect of geopolitical instability; the effect of a recession on the Company and its customers and suppliers; changes in the Company’s end-user markets into which the Company sells its products as a result of domestic and world economic or regulatory influences or otherwise; changes in the marketplace, including new products and pricing changes by the Company’s competitors; the Company’s ability to maintain satisfactory labor relations; unfavorable outcomes of legal proceedings; the Company’s ability to comply with current or future regulations applicable to the Company’s business and the industry in which it competes or any actions taken or orders issued by regulatory authorities; availability and price of raw materials; levels of operating efficiencies; the effects of the Company’s indebtedness and its compliance with the terms thereof; changes in the interest rate environment and their effects on the Company’s outstanding indebtedness; unfavorable product liability and warranty claims; actions of domestic and foreign governments, including the imposition of additional tariffs; geopolitical and economic uncertainties relating to the countries in which the Company operates or does business; risks associated with acquisitions, including difficulty in integrating operations and personnel, disruption of ongoing business, and increased expenses; results of investments; the realization of projected synergies; the effects of potential processes to explore various strategic transactions, including potential dispositions; fluctuations in currency translations; risks associated with environmental laws and regulations; risks relating to our manufacturing facilities, including that any of our material facilities may become inoperable; risks relating to financial reporting, internal controls, tax accounting, and information systems; and the other risks and factors detailed in the Company’s periodic reports filed with the Securities and Exchange Commission, including the disclosures under “Risk Factors” in those reports. These forward-looking statements are made only as of the date hereof. The Company cautions that any forward-looking statements included in this press release are subject to a number of risks and uncertainties, and the Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, changed circumstances or future events, or for any other reason, except as required by law.

NEW ALBANY, Ohio, Feb. 24, 2026 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI) will hold its quarterly conference call on Wednesday, March 11, 2026, at 8:30 a.m. ET, to discuss fourth quarter and full year 2025 financial results. CVG will issue a press release and presentation prior to the conference call.

Toll-free participants dial (800) 549-8228 using conference code 51917. International participants dial (289) 819-1520 using conference code 51917. This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com where it will be archived for one year.

A telephonic replay of the conference call will be available until March 25, 2026. To access the replay, toll-free callers can dial (+1) 888 660 6264 using access code 51917 #, and toll callers in North America and other locations can dial (+1) 289 819 1325.

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Nathan Skown Alpha IR Group CVGI@alpha-ir.com

CHARLOTTE, N.C., Feb. 19, 2026 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, announced today that it will release its fourth quarter and full year 2025 financial results for the period ended December 31st, 2025, after the close of the market on Wednesday, March 4th, 2026. The Company will hold a related conference call on Thursday, March 5th, 2026, at 9:00 a.m. E.T. Participants on the call are asked to register five to ten minutes prior to the scheduled start time by dialing 1-877-255-4315 and from outside the U.S. at 1-412-317-6579.

The conference call will be webcast simultaneously and in its entirety through the NN, Inc. Investor Relations website. Shareholders, media representatives and others may participate in the webcast by registering through the Investor Relations section on the company’s website at https://investors.nninc.com/.

For those who are unavailable to listen to the live call, a replay will be available shortly after the call on NN’s website through March 12th, 2027.

About NN, Inc. NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and Asia. For more information about the company and its products, please visit www.nninc.com.

Investor Relations: Joe Caminiti or Abe Plimpton NNBR@alpha-ir.com 312-445-2870

Alan Smith, Vice President and General Manager of Graham Manufacturing to retire in April 2026 and will serve in an advisory role moving forward

William Zmyndak is expected to assume the role of Vice President and General Manager of Graham Manufacturing upon Mr. Smith’s retirement

Additionally, the Company announces the appointments of Keith Oufnac as Chief Information Officer and Rachel Jaakkola as Chief Human Resources Officer

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer vacuum, and advanced mixing technologies for the Defense, Energy & Process and Space industries, today announced the appointment of William Zmyndak, Deputy General Manager of Graham Manufacturing.

As part of a proactive succession plan, Alan Smith, currently Vice President and General Manager of Graham Manufacturing, will transition to a consulting and advisory role beginning in April 2026. In this capacity, Mr. Smith will continue to support the business and leadership team through a transition period upon his retirement. Effective April 2026, Mr. Zmyndak will assume the role of Vice President and General Manager of Graham Manufacturing upon Alan’s retirement.

Mr. Zmyndak brings more than three decades of manufacturing and operational leadership experience, including senior leadership and P&L responsibility across complex, multi-site aerospace and industrial businesses. Prior to joining Graham, he served as Vice President and General Manager at ITT Control Technologies, where he led operations across multiple U.S. and international locations and drove margin expansion, operational excellence, and growth initiatives. Earlier in his career, Mr. Zmyndak held senior leadership roles at Kaman Aerosystems, Chromalloy, Barnes Aerospace, and Pratt & Whitney. He holds a Master of Business Administration from Purdue University and a Bachelor of Science in Manufacturing Engineering from Boston University.

In addition to this leadership transition, the Company announced two key leadership appointments that further strengthen its executive team.

Keith Oufnac has been appointed Chief Information Officer. Mr. Oufnac has more than 20 years of experience leading digital transformation, IT strategy, and cybersecurity initiatives across defense, aerospace, and highly regulated industries. Most recently, he served as Vice President of Information Technology at Bollinger Shipyards, where he led enterprise-wide infrastructure modernization, cybersecurity enhancements, and large-scale systems integration efforts, including support for significant acquisition activity.

Rachel Jaakkola has been appointed Chief Human Resources Officer. Ms. Jaakkola is a seasoned human resources executive with over a decade of experience building and scaling people organizations within aerospace, defense, and energy companies. She has a proven track record in talent strategy, leadership development, employee engagement, and M&A integration. Prior to joining Graham, Ms. Jaakkola served in senior HR leadership roles at Barber-Nichols, where she established and led the human resources function through periods of significant growth and organizational transformation.

Matthew J. Malone, President and Chief Executive Officer of Graham Corporation, said, “Alan has been instrumental in strengthening Graham Manufacturing for over 30 years of his career, and we are grateful for his continued support during the transition. Will brings extensive operational and P&L leadership experience across complex manufacturing environments, along with a strong commitment to people and execution. I am confident he is the right leader to build on our momentum and continue driving operational excellence and growth. The additions of Keith and Rachel further strengthen our leadership team as we invest in the systems, people and capabilities needed to support our long-term strategy.”

About Graham Corporation

Graham is a global leader in the design and manufacture of mission-critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise, proprietary technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “expects,” “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, expected future management personnel changes and the timing of such changes, expected expansion and growth opportunities, and its growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

CHICAGO, Feb. 12, 2026 /PRNewswire/ — Titan International, Inc. announces that Kim Marvin has stepped down from its Board of Directors.

Mr. Marvin stepped down from the Board of Directors of Titan International, Inc. after approximately 24 months of service due to time constraints and other professional commitments. The company currently has no intention of replacing this board seat.

Paul Reitz, President and CEO of Titan International stated “I want to thank Kim for his contributions over the past two years. Kim provided valuable operational continuity following the Carlstar acquisition and Titan benefited from his combination of engineering expertise, financial and transactional experience. We want to wish Kim all the best in his future endeavors.”

About Titan: Titan International, Inc. (NYSE: TWI) is a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products. Headquartered in West Chicago, Illinois, the company globally produces a broad range of products to meet the specifications of original equipment manufacturers (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets. For more information, visit www.titan-intl.com.

Leadership Changes. In early December, Titan announced CFO David Martin transitioned into a new role as Chief Transformation Officer, while Tony Eheli, former Chief Accounting Officer, was named CFO. In the new CTO role, Mr. Martin will oversee the critical alignment of information technology, including the acceleration of AI adoption, along with human capital and risk management functions and initiatives.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

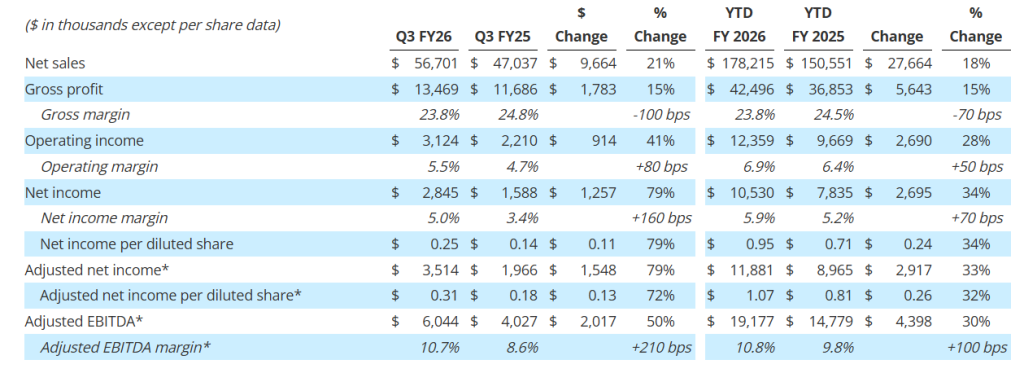

Gross profit increased 15% to $13.5 million; Gross profit margin was 23.8%

Net income per diluted share increased 79% to $0.25; adjusted net income per diluted share1 increased 72% to $0.31

Adjusted EBITDA1 increased 50% to $6.0 million; Adjusted EBITDA margin1 was 10.7%

Orders2 were $71.7 million; Book-to-Bill ratio2 of 1.3x and record backlog2 of $515.6 million

Strong balance sheet with no debt, $22.3 million in cash, and access to $43.0 million under its revolving credit facility at quarter end to support growth initiatives

Updating and increasing full year fiscal 2026 guidance; Remain on track to reach strategic goal of 8% to 10% annual organic revenue growth and low to mid-teen Adjusted EBITDA margins1 by fiscal 2027

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Energy & Process, and Space industries, today reported financial results for its third quarter for the fiscal year ending March 31, 2026 (“fiscal 2026”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “Our third quarter results reflect continued strong, disciplined execution across the organization as we progress through the back half of fiscal 2026. Revenue growth and profitability were driven by solid performance across our end markets and supported by a record backlog, which provides meaningful visibility into future demand. Activity in our Defense market remains robust, while the Energy & Process and Space markets continue to perform in line with our expectations.”

Mr. Malone continued, “As we move through the remainder of the fiscal year, we remain focused on disciplined execution, operational efficiency, and advancing strategic initiatives that strengthen our competitive position. We continue to invest in automation, advanced testing, and new technical capabilities that enhance productivity and support margin expansion. In addition, the recent acquisition of FlackTek in January 2026 meaningfully expands our technology portfolio and further positions Graham to deliver differentiated, mission-critical solutions to our core end markets.”

1Adjusted net income per diluted share, Adjusted EBITDA, and Adjusted EBITDA margin are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures. 2Orders, backlog, and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

Third Quarter Fiscal 2026 Performance Review

(All comparisons are with the same prior-year period unless noted otherwise.)

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), adjusted net income, adjusted net income per diluted share, adjusted EBITDA, and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information provided at the end of this press release for important disclosures regarding Graham’s use of these non-GAAP measures.

Quarterly net sales of $56.7 million increased 21%, or $9.7 million over the prior year reflecting our diversified revenue base. Sales to the Defense market contributed $8.3 million to growth primarily due to the timing of project milestones, new programs, and growth in existing programs. Sales to the Energy & Process market increased $2.1 million or 13% over the prior year driven by Aftermarket sales, as well as continued momentum in our New Energy markets and in particular small modular reactors (“SMRs”). Aftermarket sales to the Energy & Process and Defense markets totaled $10.8 million for the quarter, 11% above the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $1.8 million, or 15%, to $13.5 million compared to the prior-year period of $11.7 million. As a percentage of sales, gross profit margin decreased 100 basis points to 23.8%, compared to the third quarter of fiscal 2025. This decrease in gross profit margin reflects the mix of sales during the third quarter of fiscal 2026, and a higher level of material receipts which carry lower profit margins. Additionally, the third quarter and the first nine months of fiscal 2025 gross profit benefited $0.3 million and $1.5 million, respectively, from a grant received in the prior year from the BlueForge Alliance to reimburse the Company for the cost of its defense welder training programs in Batavia, which did not repeat in fiscal year 2026. For the first nine months of fiscal 2026, we estimate the impact of tariffs on our consolidated financial statements to be approximately $1.0 million compared to the prior year and was immaterial for the third quarter of fiscal 2026. For the full fiscal 2026, we now expect the potential impact of tariffs to be between an incremental $1.0 to $1.5 million compared to the prior year.

Selling, general and administrative expense (“SG&A”), including intangible amortization, totaled $10.6 million, an increase of $0.9 million compared with the prior year due to the investments being made in operations, employees, and technology, higher acquisition and integration costs due to the Xdot and FlackTek acquisitions, as well as higher performance-based compensation due to Graham’s increased profitability, which was partially offset by a reversal of bad debt reserves. As a percentage of sales, SG&A, including amortization of 18.6%, decreased 200 basis points compared to the prior year period, reflecting the higher level of sales during the quarter, as well as our continued financial discipline.

Cash Management and Balance Sheet

Cash provided by operating activities totaled $4.8 million for the quarter ended December 31, 2025. As of December 31, 2025, cash and cash equivalents were $22.3 million.

Capital expenditures, net for the third quarter fiscal 2026 were $2.2 million, focused on capacity expansion, increasing capabilities, and productivity improvements.

The Company had no debt outstanding as of December 31, 2025, with $43.0 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio

See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the third quarter of fiscal 2026 were $71.7 million. This increase was primarily in the Defense and Space markets, which continue to exhibit strong tail-winds. Energy & Process orders were consistent with prior year levels, as strong demand in New Energy offset weaker Aftermarket orders. Total Aftermarket orders for the third quarter of fiscal 2026 decreased $5.2 million to $8.0 million from the record levels of the prior year.

Note that our orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was a record $515.6 million, a 34% increase over the prior-year period, driven by strong bookings including contributions from Xdot of $0.5 million, primarily in the Defense and Space markets. For the quarter, the Company achieved a book-to bill ratio of 1.3x. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 25% to 30% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 85% of our backlog as of December 31, 2025, was to the Defense industry, which provides stability and visibility to our business.

FlackTek Acquisition

On January 23, 2026, subsequent to the end of the third quarter, Graham acquired FlackTek Manufacturing, LLC and FlackTek Sales, LLC (collectively, “FlackTek”). The acquisition establishes advanced mixing and materials processing as a third core technology platform for Graham, complementing its existing vacuum, heat transfer, and turbomachinery capabilities and further aligning with the Company’s Defense, Energy & Process, and Space end markets.

Under the terms of the transaction, Graham acquired 100% of the equity of FlackTek for a purchase price of $35.0 million, comprised of 85% cash and 15% using 75,818 shares of Graham’s common stock, along with the potential to earn an additional $25 million in future performance-based cash earnouts over four years beginning in fiscal year 2027, based upon achieving progressively increasing adjusted EBITDA performance targets. The base purchase price represents approximately 12x FlackTek’s projected adjusted EBITDA for 2026. The transaction was funded through a combination of cash on-hand and borrowings under the Company’s revolving credit facility.

In connection with the acquisition, Graham amended its revolving credit agreement with Wells Fargo Bank, National Association, increasing the borrowing limit from $50 million to $80 million. Following the closing of the transaction, the Company’s pro forma leverage ratio is approximately 1.2x.

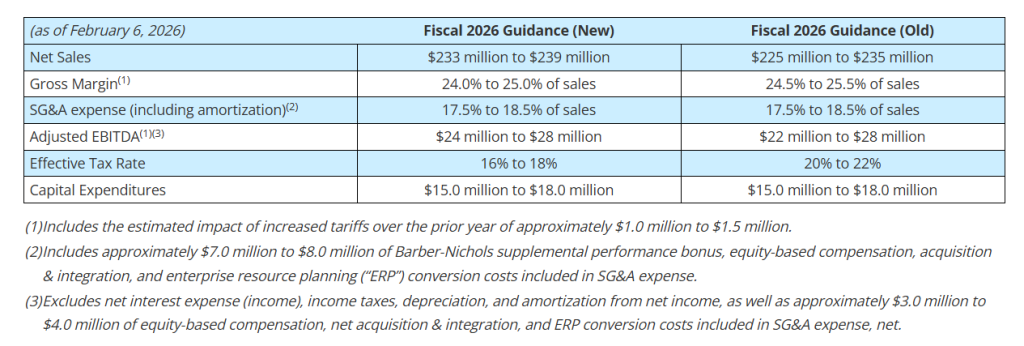

Fiscal 2026 Outlook

Based upon the results for the first nine months of fiscal 2026, our expectations for the remainder of the fiscal year, and inclusive of the acquisition of FlackTek and Xdot, Graham is updating its full year fiscal 2026 guidance as follows:

Graham’s Chief Financial Officer, Christopher J. Thome, said, “We are pleased with our performance through the first nine months of fiscal 2026 and continue to see strong demand across most of the markets we serve. Reflecting this momentum, including the contribution from the FlackTek acquisition, we are increasing our full-year fiscal 2026 guidance.

Mr. Thome continued, “After the acquisition of FlackTek, our balance sheet remains strong with low leverage, a modest amount of debt of $20 million, and increased capacity under our line of credit. We believe this increased capacity, along with our strong operating cash flow, provides us ample liquidity to continue to execute our capital allocation strategy and future growth.”

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on February 6, 2026, at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201)-689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, February 13, 2026. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13757532 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise, proprietary technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

The artificial intelligence boom has reshaped the global technology landscape, turning companies like Nvidia into market behemoths and pushing cloud giants such as Microsoft and Google to new earnings highs. But while GPUs and AI software platforms dominate headlines, another corner of the semiconductor market is quietly delivering some of the most explosive gains: memory and storage stocks.

As AI data centers multiply around the world, demand for high-performance memory and storage chips has surged to unprecedented levels. These facilities, packed with thousands of servers, rely not only on powerful GPUs from Nvidia and Advanced Micro Devices, but also on vast amounts of DRAM, NAND, and other storage technologies to process and move massive datasets. The result has been a supply crunch years in the making—and eye-popping stock gains for companies positioned to benefit.

Some memory-related stocks have delivered returns that rival even the hottest AI chip names. Sandisk, which began trading in early 2025 following its spin-off from Western Digital, has seen its share price climb more than 1,800%. Micron Technology is up over 360% in the past year, while Western Digital shares have surged nearly 500%. International players are seeing similar momentum, with South Korea’s SK Hynix up roughly 375% and Japan’s Kioxia soaring more than 1,000%.

This surge is the culmination of a “perfect storm” in the memory industry. During the COVID era, demand for PCs, smartphones, and enterprise hardware spiked, leading to heavy investment in memory production. When that demand cooled, the industry entered a deep downturn, with sharp revenue declines in 2023. Micron, for example, saw revenue collapse nearly 50% that year, while Western Digital endured steep sales declines.

Then AI arrived at scale.

As hyperscalers raced to build out AI infrastructure, demand for memory rebounded violently. Western Digital’s revenue jumped 51% in 2025, while Micron posted back-to-back growth years of 62% and 49% in 2024 and 2025, respectively. Micron has leaned so aggressively into the AI opportunity that it has begun winding down its consumer-facing Crucial brand to focus more heavily on enterprise and data center customers, where margins are higher and demand is more consistent.

Industry analysts say the shortage did not fully materialize until late 2025 because manufacturers were initially able to draw down excess inventory left over from the post-COVID slowdown. Once that buffer disappeared, supply simply could not keep pace with accelerating AI-driven demand from companies like Nvidia, Broadcom, and AMD.

With supply tight, memory producers have gained significant pricing power. That scarcity has become the primary catalyst behind soaring profits—and investor enthusiasm. However, the sector’s history serves as a reminder that memory is one of the most cyclical segments of the semiconductor industry. As new manufacturing capacity comes online and supply chains normalize, pricing pressure could eventually ease.

Even so, analysts caution that relief may not come quickly. AI demand continues to grow at a rapid pace, and building new fabrication capacity takes years. Until supply meaningfully catches up, memory and storage companies may continue to enjoy elevated pricing, strong margins, and outsized stock performance—making them an increasingly important, if often overlooked, pillar of the AI trade in today’s stock market.