Research News and Market Data on CVGI

AUGUST, 01, 2023

Strong quarterly revenues of $262 million, up 4.5% year-over-year

EPS of $0.30, adjusted EBITDA of $20.8 million or 7.9% of revenue

Continued strategy execution and operational excellence driving improved results

NEW ALBANY, Ohio, Aug. 01, 2023 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its second quarter ended June 30, 2023.

Second Quarter 2023 Highlights (Compared with prior year, where comparisons are noted)

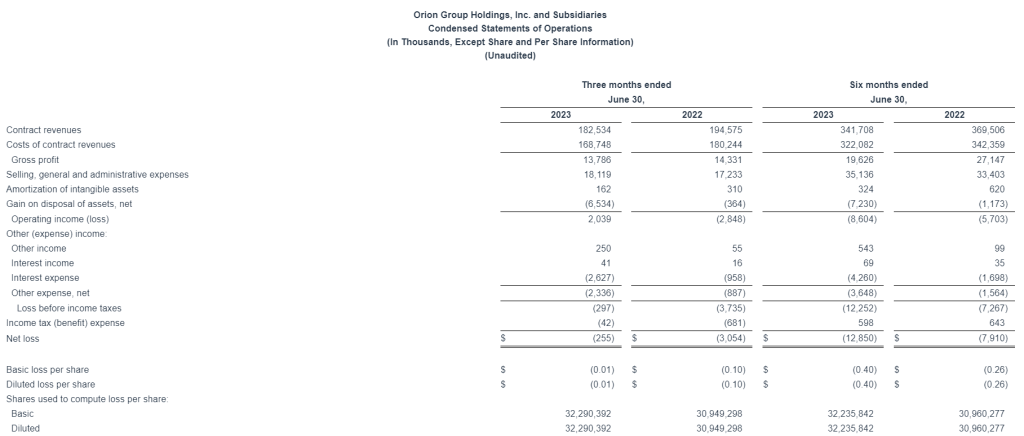

- Revenues of $262.2 million, up 4.5% primarily driven by strong price realization.

- Operating income of $15.9 million, up 156.0%; adjusted operating income of $16.7 million, up 106.2%. Improved operating income was driven primarily by improved pricing and cost management.

- Net income of $10.1 million, or $0.30 per diluted share. Adjusted net income of $10.7 million, or $0.32 per diluted share.

- Adjusted EBITDA of $20.8 million, up 67.7% with an adjusted EBITDA margin of 7.9%, tracking further towards the Company’s long-term profitability target.

- Net new business wins year-to-date are $124 million. The majority of the new business awards continue to be in the Electrical Systems segment.

- Our cost reduction program continues to deliver cost savings through process improvements, footprint changes and organizational streamlining.

Robert C. Griffin, Chairman of the Board and Interim President and Chief Executive Officer, said, “CVG delivered solid second quarter results and we continued to execute well on our long-term strategy. The team’s efforts to drive the Company’s strategic plan are delivering improved financial results, highlighted by strong improvements in revenue, operating income, adjusted EBITDA and free cash flow during the quarter. Additionally, I am pleased to report that our Electrical Systems plant expansions are on track and the Aldama, Mexico plant is open and ramping up production. We remain on track to deliver record revenues in 2023 and continue to expect our full year Adjusted EBITDA margins to show significant expansion versus last year, based on the current vehicle production outlook for the second half of the year. We also believe we continue to be on track to deliver our 2027 targets of $1.5 billion in revenue and 9% EBITDA margin.”

Mr. Griffin concluded, “I would like to thank our team of employees who helped us improve CVG this quarter and continue to execute our strategy of growing and diversifying our revenue, optimizing our cost structure through process automation and cost reduction, and increasing our margins to become a bigger, more profitable company.”

Andy Cheung, Chief Financial Officer, added, “The continued execution of our strategy is delivering improved financial results for CVG. Our focus on winning new business, improved price realization and cost reduction has allowed us to continue to improve our margins and profit. Additionally, we remain heavily focused on optimizing working capital, increasing cash flows, and paying down our debt.”

Consolidated Results

Second Quarter 2023 Results

- Second quarter 2023 revenues were $262.2 million, compared to $250.8 million in the prior year period, an increase of 4.5%. The increase in revenues was primarily driven by increased pricing and volume from new Electrical Systems business, partially offset by lower volumes in the Industrial Automation segment. Foreign currency translation also favorably impacted second quarter 2023 revenues by $0.7 million, or 0.3%.

- Operating income in the second quarter 2023 was $15.9 million compared to $6.2 million in the prior year period. The increase in operating income was attributable to higher margins, partially offset by higher SG&A. The second quarter 2023 adjusted operating income was $16.7 million, excluding special charges.

- Interest associated with debt and other expenses was $2.8 million and $2.1 million for the second quarter 2023 and 2022, respectively.

- Net income was $10.1 million, or $0.30 per diluted share, for the second quarter 2023 compared to net income of $2.5 million, or $0.08 per diluted share, in the prior year period.

At June 30, 2023, the Company had $9.0 million of outstanding borrowings on its U.S. revolving credit facility and $4.1 million outstanding on its China credit facility, $42.4 million of cash and $148.1 million of availability from the credit facilities, resulting in total liquidity of $190.5 million.

Second Quarter 2023 Segment Results

Vehicle Solutions Segment

- Revenues were $152.7 million compared to $142.8 million for the prior year period, an increase of 7.0%, primarily resulting from increased pricing.

- Operating income was $14.1 million, compared to $1.5 million in the prior year period, an increase of 836.7%, primarily attributable to price increases with customers and cost reduction initiatives. Adjusted operating income was $14.5 million.

Electrical Systems Segment

- Revenues were $63.6 million compared to $47.3 million in the prior year period, an increase of 34.4%, primarily resulting from increased sales volume and pricing.

- Operating income was $7.7 million compared to $5.9 million in the prior year period, an increase of 28.9%. The increase in operating income was primarily attributable to increased sales volume and pricing.

Aftermarket & Accessories Segment

- Revenues were $36.8 million compared to $32.2 million in the prior year period, an increase 14.5%, primarily resulting from increased pricing.

- Operating income was $5.5 million compared to $1.1 million in the prior year period, an increase of 388.2%. The increase in operating income was primarily attributable to increased pricing and cost reduction.

Industrial Automation Segment

- Revenues were $9.0 million compared to $28.5 million in the prior year period, a decrease of 68.4%, primarily due to decreased customer demand which is expected to continue in the third quarter.

- Operating loss was $2.1 million compared to operating income of $1.3 million in the prior year period. The decrease in operating income was primarily attributable to volume reduction and an inventory charge of $1.6 million. Adjusted operating loss was $1.7 million.

2023 Demand Outlook

According to ACT Research, 2023 North American Class 8 truck production levels are expected to be at 339,000 units and Class 5-7 production levels are expected to be at 258,000 units. Estimates from FTR for 2023 are 325,000 units, slightly lower than ACT Research for Class 8 truck builds. The 2022 actual Class 8 truck builds according to the ACT Research was 315,128 units.

The global commercial and automotive vehicle wire harness market is growing at approximately 4.5%. The global electric truck market expected to grow approximately 15% CAGR.

According to Interact Analysis, the Global Off-Highway vehicle market is expected to increase approximately 4% to 6.2 million units in 2023 from 5.9 million units in 2022. Beyond 2023, the Off-Highway vehicle market is expected to grow in the 4-5% range. We expect our legacy business growth rates to be in line with this outlook.

Industry forecasts are expecting at least 4% growth in 2023 for North American aftermarket truck parts. Compounded annual growth of at least 4% is forecasted for 2023-2027.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Wednesday, August 2, 2023, at 10:00 a.m. ET. Management intends to reference the Q2 2023 Earnings Call Presentation during the conference call. To participate, dial (888) 259-6580 using conference code 34051647. International participants dial (416) 764-8624 using conference code 34051647.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (877) 674-7070 using access code 051647 and international callers can dial (416) 764-8692 using access code 051647.

Company Contact

Andy Cheung

Chief Financial Officer

CVG

IR@cvgrp.com

Investor Relations Contact

Ross Collins or Stephen Poe

Alpha IR Group

CVGI@alpha-ir.com

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction equipment business, the Company’s prospects in the wire harness, warehouse automation and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

Use of Non-GAAP Measures

This earnings release contains financial measures that are not calculated in accordance with U.S. generally accepted accounting principles (“GAAP”). In general, the non-GAAP measures exclude items that (i) management believes reflect the Company’s multi-year corporate activities; or (ii) relate to activities or actions that may have occurred over multiple or in prior periods without predictable trends. Management uses these non-GAAP financial measures internally to evaluate the Company’s performance, engage in financial and operational planning and to determine incentive compensation.

Management provides these non-GAAP financial measures to investors as supplemental metrics to assist readers in assessing the effects of items and events on the Company’s financial and operating results and in comparing the Company’s performance to that of its competitors and to comparable reporting periods. The non-GAAP financial measures used by the Company may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies.

The non-GAAP financial measures disclosed by the Company should not be considered a substitute for, or superior to, financial measures calculated in accordance with GAAP. The financial results calculated in accordance with GAAP and reconciliations to those financial statements set forth above should be carefully evaluated.

Source: Commercial Vehicle Group, Inc.