CERRITOS, Calif., Nov. 13, 2025 (GLOBE NEWSWIRE) — The Oncology Institute, Inc. (NASDAQ: TOI) (“TOI” or the “Company”), one of the largest value-based community oncology groups in the United States, today reported financial results for its three months ended September 30, 2025 and updated its full year 2025 guidance.

Recent Operational Highlights

Fee-for-service revenue growth of 13% over Q3 2024, driven by continued organic growth performance in Florida and Oregon.

Retail Pharmacy and Dispensary set fill records, contributing $75.9 million in revenue and $12.8 million in gross profit in Q3.

Signed several new in-network MSO providers in the Florida market and opened our new TOI pharmacy location in Florida.

Welcomed Kristin England as our new Chief Administrative Officer overseeing our Enterprise Central Business Operations, Technology Strategy and AI Enablement.

Third Quarter 2025 Financial Highlights

All comparisons are to the quarter ended September 30, 2024 unless otherwise noted

Consolidated revenue of $136.6 million increased 36.7% from $99.9 million

Gross profit of $18.9 million, increased 31.7%

Net loss of $16.5 million compared to net loss of $16.1 million

Basic and diluted (loss) earnings per share of $(0.14) compared to $(0.18)

Adjusted EBITDA of $(3.5) million compared to $(8.2) million

Cash and cash equivalents of $27.7 million as of September 30, 2025

Outlook for Fiscal Year 2025

TOI uses Adjusted EBITDA and Free Cash flow, each a non-GAAP metric, as an additional tool to assess its operational and financial performance. See “Financial Information: Non-GAAP Financial Measures” below. In reliance on the unreasonable efforts exception provided under Regulation S-K, TOI is not reasonably able to provide a quantitative reconciliation for forward-looking information of Adjusted EBITDA and Free Cash Flow to net (loss) income and net cash provided by operations, respectively, the most directly comparable GAAP financial measures, without unreasonable efforts due to uncertainties regarding taxes, capital expenditures, operating activities, share-based compensation, goodwill impairment charges, change in fair value of liabilities, unrealized (gains) losses on investments, practice acquisition-related costs, consulting and legal fees, transaction costs and other non-cash items. The variability of these items could have an unpredictable, and potentially significant, impact on TOI’s future GAAP financial results. The Company, given the revenue and profitability growth in the first three quarters, is updating its full year revenue and Adjusted EBITDA guidance as follows:

2025 Guidance – Previous

2025 Guidance – Updated

Revenue

$460 to $480 million

$495 to $505 million

Gross Profit

$73 to $82 million

$73 to $82 million

Adjusted EBITDA

$(8) to $(17) million

$(11) to $(13) million

Free Cash Flow

$(12) to $(21) million

$(12) to $(21) million

Additionally, the Company expects Adjusted EBITDA of approximately $0 to $2 million in the fourth quarter of 2025. TOI’s achievement of the anticipated results is subject to risks and uncertainties, including those disclosed in its filings with the U.S. Securities and Exchange Commission. The outlook does not take into account the impact of any unanticipated developments in the business or changes in the operating environment, nor does it take into account the impact of TOI’s acquisitions, dispositions or financings. TOI’s outlook assumes a largely stable global market, which would likely be negatively impacted if recent tariff rate increases and exchange rate changes persist and adversely affect world trade.

Management Commentary

Daniel Virnich, CEO of TOI, commented, “We had a solid third quarter across all lines of our business. Our Pharmacy business continues to set records, and our new delegated lives in Florida are ramping nicely with strong MLR performance. During the quarter, we made meaningful progress in leveraging AI to drive efficiencies in our operations and improve the patient experience. These were just some of the factors that allowed us to increase our full-year guidance and reaffirm our positive outlook for Q4 adjusted EBITDA. As a leader in oncology value-based care, it is important for us to not only raise the quality of care but also lower that cost of care. We believe we are well-positioned to achieve this goal, while simultaneously driving durable and sustainable growth.”

Webcast and Conference Call

TOI will host a conference call on Thursday, November 13, 2025 at 5:00 p.m. (Eastern Time) to discuss third quarter results and management’s outlook for future financial and operational performance.

The conference call can be accessed live over the phone by dialing 1-877-407-0789, or for international callers, 1-201-689-8562. A replay will be available two hours after the call and can be accessed by dialing 1-844-512-2921, or for international callers, 1-412-317-6671. The passcode for the live call and the replay is 13756737. The replay will be available until Thursday, November 20, 2025.

Interested investors and other parties may also listen to a simultaneous webcast of the conference call by logging onto the Investor Relations section of TOI’s website at https://investors.theoncologyinstitute.com.

About The Oncology Institute, Inc.

Founded in 2007, The Oncology Institute, Inc. (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better. For more information visit www.theoncologyinstitute.com.

Forward-Looking Statements

This press release includes certain statements that are not historical facts but are forward-looking statements for purposes of the safe harbor provisions under the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements generally are accompanied by words such as “preliminary,” “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “predict,” “potential,” “guidance,” “approximately,” “seem,” “seek,” “future,” “outlook,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding projections, anticipated financial results, estimates and forecasts of revenue and other financial and performance metrics and projections of market opportunity and expectations. These statements are based on various assumptions and on the current expectations of TOI and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by anyone as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of TOI. These forward-looking statements are subject to a number of risks and uncertainties, including the accuracy of the assumptions underlying the 2025 full fiscal year outlook and the Q4 2025 outlook with respect to Adjusted EBITDA discussed herein, the outcome of judicial and administrative proceedings to which TOI may become a party or investigations to which TOI may become or is subject that could interrupt or limit TOI’s operations, result in adverse judgments, settlements or fines and create negative publicity; changes in TOI’s patient or payors’ preferences, prospects and the competitive conditions prevailing in the healthcare sector; failure to continue to meet stock exchange listing standards; the impact of a cybersecurity incident affecting a software provider on TOI’s business; those factors discussed in the documents of TOI filed, or to be filed, with the SEC, including the Item 1A. “Risk Factors” section of TOI’s Annual Report on Form 10-K for the year ended December 31, 2024 filed with the SEC on March 26, 2025 and any subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K. If the risks materialize or assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that TOI currently is evaluating or does not presently know or that TOI currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect TOI’s plans or forecasts of future events and views as of the date of this press release. TOI anticipates that subsequent events and developments will cause TOI’s assessments to change. TOI does not undertake any obligation to update any of these forward-looking statements. These forward-looking statements should not be relied upon as representing TOI’s assessments as of any date subsequent to the date of this press release. Accordingly, undue reliance should not be placed upon the forward-looking statements.

Partnership deployed touchless prior authorization system in eight weeks, achieving 95% reduction in authorization workload

CERRITOS, Calif. and NEW YORK, Nov. 13, 2025 (GLOBE NEWSWIRE) — Ascertain, a healthcare technology company pioneering agentic AI to automate administrative workflows, and The Oncology Institute, Inc. (NASDAQ: TOI), a leading value-based oncology care provider, today announced a co-development partnership to create “near-touchless” administrative workflows that reduce manual interactions between providers and payers.

The collaboration centers on Ascertain’s Unified Payer Portal (UPP) — an AI-powered automation module that streamlines payer-related tasks required ahead of outpatient oncology visits. The system enables near-touchless workflows by automating manual data entry, documentation submission, and payer portal navigation, significantly reducing the administrative effort required to prepare for each patient encounter.

The joint team achieved rapid implementation, going from a signed statement of work to a live early-stage deployment in just eight weeks. That pace demonstrates both the adaptability of Ascertain’s technology and the strength of the operational partnership between the two organizations.

Since going live in September 2025, the automation has reduced TOI’s office visit authorization submission time at pilot sites by over 80 percent, freeing hundreds of staff hours each week. As TOI scales this solution across all authorization types, the initiative is expected to generate significant efficiencies that could yield up to an estimated $2 million in operating expense savings in 2026. The system now processes prior authorizations across TOI’s 100+ clinics and affiliate locations, allowing staff to focus more time on direct patient care.

Mark Michalski, MD, CEO of Ascertain, said:

“The Oncology Institute has been a national leader in bringing value-based cancer care to scale, and we are proud to co-develop automation tools that help sustain that mission. This first deployment of our Unified Payer Portal represents just the beginning. Together, we’re proving that administrative work between providers and payers can become truly touchless — faster, more accurate, and far less burdensome for clinical teams.”

Daniel Virnich, CEO of The Oncology Institute, said:

“Our partnership with Ascertain reflects TOI’s ongoing focus on operational excellence and efficiency. We’ve seen how thoughtfully applied automation can simplify complex tasks and allow our staff to focus more of their time on supporting patients. This first implementation went live in only eight weeks, and we look forward to continuing to build on that progress with Ascertain’s team.”

About Ascertain

Ascertain is a healthcare technology company using agentic AI to automate complex, forms-heavy administrative workflows in healthcare. The company’s platform replaces manual tasks — such as payer communications, documentation assembly, and eligibility verification — with touchless, intelligent automation. Ascertain was founded in partnership with Northwell Health and Aegis Ventures and is backed by Deerfield Management. For more information, visitwww.ascertain.com.

About The Oncology Institute

Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better. For more information, visit www.theoncologyinstitute.com.

TOI is an oncology practice management company that provides administrative services to oncology clinics. These clinics provide cancer care to a population of approximately 1.9 million patients. Services include cancer care, pharmacy and dispensary services, clinical trials, and services associated with oncology care. The company employs nearly 120 clinicians and over 700 teammates at over 70 clinic locations.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q25 Was A Strong Quarter. The Oncology Institute reported a loss of $16.5 million or $(0.14) per share, with revenues from Patient Services and Dispensary both ahead of our estimates. Adjusted EBITDA turned positive for the first time at the end of the quarter. Management raised guidance for Full-Year Revenues, and confirmed the ranges for Adjusted EBITDA, and Free Cash Flow. On September 30, the company had $27.7 million in cash.

Total Revenues Beat Our Estimates. Total Revenue of $136.6 million easily beat our estimate of $122.5 million. This was an increase from $119.8 million in 2Q25 (up 14%) and $99.9 million (up 37%) in 4Q24. Adjusted EBITDA of $(3.5) million was also better than the $(3.8) million we had estimated. COGS included a new reserve of $8.1 million for bad debts, lowering gross margin from 19.8% to 13.9% compared with the 15.2% we estimated.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 results below expectations. GoHealth reported Q3 revenue of $34.2 million versus our estimate of $100.0 million and an adj. EBITDA loss of $47.1 million, compared with our projected loss of $11.6 million. The variance reflected an intentional pullback in Medicare Advantage policy volume as management prioritized persistency and unit economics over near-term growth.

Health plans facing headwinds. Carriers are contending with lower reimbursement under the new CMS V28 risk model and heightened difficulty maintaining high STAR ratings. These dynamics have shifted industry priorities toward member retention, stability, and margin integrity rather than volume growth, reducing pre-funded marketing and broker commissions across the sector.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Day One Biopharmaceuticals announced a definitive agreement to acquire Mersana Therapeutics (Nasdaq: MRSN), marking a strategic move to strengthen its position in oncology drug development. The deal, valued at up to $285 million, combines Day One’s commercial expertise with Mersana’s innovative antibody-drug conjugate (ADC) technology, expanding the company’s pipeline in targeted cancer therapies.

Under the terms of the agreement, Day One will acquire Mersana through a tender offer followed by a merger, offering $25 per share in cash upfront and up to $30.25 per share in additional contingent value rights (CVRs). The CVRs are tied to the achievement of specific clinical, regulatory, and commercial milestones, particularly related to Emi-Le (emiltatug ledadotin), Mersana’s B7-H4-directed ADC candidate. The total equity value at closing is estimated at $129 million, with the full deal potentially reaching $285 million if all milestones are met.

The acquisition highlights Day One’s intent to broaden its oncology focus beyond its current lead programs. Known for its commitment to developing therapies for pediatric and underserved cancer populations, Day One plans to leverage Mersana’s ADC platforms—Dolasynthen and Immunosynthen—to accelerate the development of next-generation cancer treatments.

For Mersana, the deal represents both validation and a strategic exit amid a challenging biotech funding environment. The company has been recognized for its innovative ADC technology, which delivers cytotoxic and immune-modulating agents directly to cancer cells, minimizing harm to healthy tissue. Its lead candidate, Emi-Le, is currently being explored for the treatment of triple-negative breast cancer and adenoid cystic carcinoma, both areas with high unmet clinical needs.

Upon completion of the acquisition, Mersana will become a wholly owned subsidiary of Day One, and its common stock will be delisted from public exchanges. The transaction is expected to close by the end of January 2026, subject to customary regulatory approvals and the tender of a majority of Mersana’s outstanding shares.

The merger agreement was unanimously approved by Mersana’s board of directors, which has recommended that shareholders tender their shares once the offer is formally launched. Key shareholders, including affiliates of Bain Capital Life Sciences, representing approximately 8.5% of outstanding shares, have already agreed to support the transaction.

Financially, TD Cowen is serving as Mersana’s advisor, while WilmerHale is acting as legal counsel. Fenwick & West LLP is representing Day One in the deal.

This acquisition aligns with broader industry trends in oncology, where partnerships and mergers are accelerating innovation in targeted therapies. ADCs have become one of the most promising drug classes in oncology, combining precision targeting with potent efficacy. The addition of Mersana’s technology could give Day One a competitive edge in developing more effective, tumor-specific treatments.

With closing anticipated early next year, the merger positions Day One Biopharmaceuticals as a growing force in precision oncology, combining innovative science with a mission-driven focus on expanding treatment options for patients of all ages battling cancer.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 Results. The company reported Q3 revenue of $59.9 million and adj. EBITDA of $9.5 million, both of which surpassed our estimates of $54.0 million and $2.6 million, respectively. Additionally, the strong results surpassed the high end of company issued guidance, of $51.0 million to $58.0 million in revenue and $2.0 million to $6.0 million in adj. EBITDA. Furthermore, the company hit an important milestone, recording net income for the first time since 2021.

Improved operating structure. Over the past several years, the company has significantly lowered its break-even point from $900 million in 2022 to $180 million in 2025, largely through SG&A optimization and the elimination of Multi Layer sales costs. The new model offers enhanced operating leverage, enabling profitability at lower revenue levels and providing a favorable outlook ahead of several new product releases.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Cadrenal Made A Significant Acquisition In 3Q25. Cadrenal reported a loss of $2.7 million or $(1.31) per share, less than the loss of $3.1 million we estimated. The company also provided an update on clinical progress for tecarfarin and the products acquired through the recent acquisition of eXithera Therapeutics. At the end of the quarter on September 30, the company had cash on hand of $3.9 million.

Tecarfarin Is Making Clinical Progress. During the quarter, the company continued to support the Phase 2 trial in LVAD (left ventricular assist devices) as part of its collaboration with Abbott. Separately, it also continued its consultations with Clinical Investigators to design a Phase 2 trial in dialysis patients previously treated with warfarin. The manufacture of tecarfarin supplies for clinical trials that comply with the FDA’s Good Manufacturing Practices (cGMP) was also completed.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Quarter Sales Were Driven By Etuary. Gyre reported Net Income of $5.9 million or $0.04 per basic share. Revenue of $30.6 million showed year-over-year growth of 20.0%. This was driven by strength in Etuary with sales of $27.7 million. Sales of Etorel and Contiva sales were of $1.5 million and $1.2 million respectively. At the end of 3Q25 on September 30, the company had $80.3 in cash, equivalents, and securities.

The Company Made Progress In Several Important Clinical Programs. During 3Q, Gyre continued working to submit its NDA for Hydronidone approval in China. The Phase 3 trial testing Etuary in pneumonoconiosis completed enrollment, while a Phase 2/3 trial for pulmonary complications in oncology (radiation induced lung injury/pneumonitis) is planned to begin in 4Q25. The IND for a Phase 2 trial in MASH in the US is now expected to be filed in early 2026, within the timeframe we had expected.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase 2 BESTOW Trial Data Reported. On Thursday evening, November 6, the results of the Phase 2 BESTOW trial in kidney transplant patients were presented. The trial did not meet its primary endpoint of tegoprubart superiority to the control arm but showed improvements in several important endpoints. We believe tegoprubart performed well and that the sharp decline in stock price is unwarranted.

Design Of The Phase 2 BESTOW Trial. The trial enrolled 126 patients into and randomized them into two arms. The first received tegoprubart and the second received tacrolimus, the standard of care, as a control arm. The primary endpoint was a difference in eGFR, a measure of kidney filtration and function. Additional endpoints reported were for the iBOX composite and measures of adverse events.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Mixed Fiscal Q1 results. SelectQuote reported Q1 revenue of $328.8 million, above our estimate of $310.0 million. Adj. EBITDA loss of $32.1 million was slightly wider than expected due to temporary pharmacy reimbursement headwinds. Overall, results showed resilient topline growth despite short-term margin pressure, reflecting solid execution across Healthcare Services and Senior segments in a seasonally lighter quarter.

Healthcare Services headwind. Lower reimbursement rates from one pharmacy benefit manager impacted both revenue and margins in Healthcare Services in the quarter. The reimbursement adjustment, tied to the PBM’s calendar-year 2025 pricing update, will continue through fiscal Q2, when management expects segment adj. EBITDA to reach breakeven before normalizing in the second half.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Ocugen Reports 3Q25 With Milestones For FY2026. Ocugen reported a 3Q25 loss of $20.1 million or $(0.07) per share and gave updates on its clinical programs. Importantly, all three clinical trials are meeting or beating our expectations for progress toward the BLA filings. We continue to expect “3 filings in 3 years”, with the first approval in mid-2027.

OCU400 Expected To Start Rolling BLA Filing In 1H26. OCU400 received RMAT designation from the FDA, allowing portions of the BLA to be submitted as they are completed rather than waiting to submit the entire BLA at once. The non-clinical portions are planned for submission in early 2026, with clinical trial data submitted in 4Q26. This should start the FDA review earlier and allow for approval in mid-2027.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

First Quarter of Fiscal Year 2026 – Consolidated Earnings Highlights

Revenue of $328.8 million

Net loss of $30.5 million

Adjusted EBITDA* of $(32.1) million

First Quarter Fiscal Year 2026 – Segment Highlights

Senior

Revenue of $59.0 million

Adjusted EBITDA of $(21.0) million

Approved Medicare Advantage policies of 62,510

Healthcare Services

Revenue of $221.4 million

Adjusted EBITDA of $7.2 million

106,914 SelectRx members

Life

Revenue of $46.6 million

Adjusted EBITDA of $5.6 million

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT) reported consolidated revenue for the first quarter of fiscal year 2026 of $328.8 million compared to consolidated revenue for the first quarter of fiscal year 2025 of $292.3 million. Consolidated net loss for the first quarter of fiscal year 2026 was $30.5 million compared to consolidated net loss for the first quarter of fiscal year 2025 of $44.5 million. Finally, consolidated Adjusted EBITDA* for the first quarter of fiscal year 2026 was $(32.1) million compared to consolidated Adjusted EBITDA* for the first quarter of fiscal year 2025 of $(1.7) million.

Tim Danker, SelectQuote Chief Executive Officer, remarked “The strength of our integrated healthcare model was exhibited again in our fiscal first quarter. Early work to prepare for new eligibility parameters in this year’s Medicare Advantage special election period was evident in our Senior business. We successfully reallocated resources and agents for the expected decline in volume and, as a result, performed well in the quarter and more importantly positioned our Senior business for another strong season. We firmly maintain our view that SelectQuote’s Medicare Advantage business has durable competitive advantage and flexibility to drive strong results in a range of environments. While the past three years have presented different challenges and opportunities, SelectQuote has excelled and validated our visibility and confidence in the generation of return and cash flow in our Senior distribution business.”

Mr. Danker added, “Our Healthcare Services business also continues to perform well, serving over 100,000 SelectRx members with convenient drug delivery that drives improved health outcomes. Our value-added prescription drug delivery and patient adherence pharmacy offers real, differentiated value to both the patient and the insurance payor. When our data and service approach provides better care, patients win, and do so at more efficient cost to the overall healthcare system. We continue to see SelectQuote as a healthcare services ecosystem that can create system-wide value in a range of use cases. In this quarter, SelectQuote generated a revenue to customer acquisition cost (CAC) ratio of 6.4x, which is an all-time high and nearly 40% higher than it was a year ago. While profitability is our ultimate north star, we view this metric as a strong indicator on how we are helping our customers with more and more, each and every year.”

Mr. Danker concluded, “At this time, we are not changing our fiscal 2026 financial outlook of $1.65 to $1.75 billion in revenue and $120 to $150 million in Adjusted EBITDA*. In Healthcare Services, a temporary reimbursement rate headwind in our SelectRx business impacted this quarter and we expect will drive adjusted EBITDA around breakeven for the segment in the fiscal second quarter. SelectQuote and our PBM partners are committed to the significant value provided to patients of SelectRx, and we expect Healthcare Services to exit fiscal 2026 at an Adjusted EBITDA run rate in the $40 to $50 million range.”

* See “Non-GAAP Financial Measures” below.

Segment Results

We currently have three reportable segments: 1) Senior, 2) Healthcare Services and 3) Life. The performance measures of the segments include total revenue and adjusted EBITDA. Costs of commissions and other services revenue, cost of goods sold-pharmacy revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses that are directly attributable to a segment are reported within the applicable segment. Indirect costs of revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses are allocated to each segment based on varying metrics such as headcount. Adjusted EBITDA is our segment profit measure to evaluate the operating performance of our business. We define Adjusted EBITDA as net income (loss) before income tax expense (benefit) plus interest expense, depreciation and amortization, changes in fair value of warrant liabilities, and certain add-backs for non-cash or non-recurring expenses, including restructuring and share-based compensation expenses. Adjusted EBITDA margin is calculated as adjusted EBITDA divided by revenue.

Senior

Financial Results

The following table provides the financial results for the Senior segment for the periods presented:

Operating Metrics

Submitted Policies

Submitted policies are counted when an individual completes an application with our licensed agent and provides authorization to the agent to submit the application to the insurance carrier partner. The applicant may have additional actions to take before the application will be reviewed by the insurance carrier.

The following table shows the number of submitted policies for the periods presented:

Approved Policies

Approved policies represents the number of submitted policies that were approved by our insurance carrier partners for the identified product during the indicated period. Not all approved policies will go in force.

The following table shows the number of approved policies for the periods presented:

Lifetime Value of Commissions per Approved Policy

Lifetime value of commissions per approved policy represents commissions estimated to be collected over the estimated life of an approved policy based on multiple factors, including but not limited to, contracted commission rates, carrier mix and expected policy persistency with applied constraints. The lifetime value of commissions per approved policy is equal to the sum of the commission revenue due upon the initial sale of a policy, and when applicable, an estimate of future renewal commissions.

The following table shows the lifetime value of commissions per approved policy for the periods presented:

Healthcare Services

Financial Results

The following table provides the financial results for the Healthcare Services segment for the periods presented:

Operating Metrics

Members

The total number of SelectRx members represents the amount of active customers to which an order has been shipped and the prescriptions per day represents the total average prescriptions shipped per business day. These two metrics are the primary drivers of revenue for Healthcare Services.

The following table shows the total number of SelectRx members as of the periods presented:

The total number of SelectRx members increased by 24% as of September 30, 2025, compared to September 30, 2024, due to our strategy to grow SelectRx membership.

The following table shows the average prescriptions shipped per day for the periods presented:

Combined Senior and Healthcare Services – Consumer Per Unit Economics

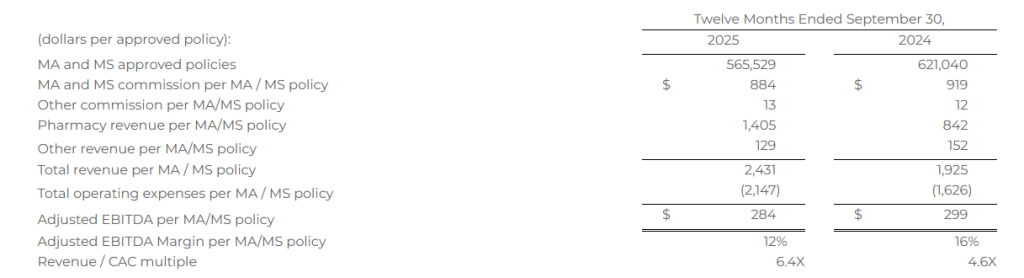

Combined Senior and Healthcare Services consumer per unit economics represents total MA and MS commissions; other product commissions; other revenues, including revenues from Healthcare Services; and operating expenses associated with Senior and Healthcare Services, each shown per number of approved MA and MS policies over a given time period. Management assesses the business on a per-unit basis to help ensure that the revenue opportunity associated with a successful policy sale is attractive relative to the marketing acquisition cost. Because not all acquired leads result in a successful policy sale, all per-policy metrics are based on approved policies, which is the measure that triggers revenue recognition.

The MA and MS commission per MA/MS policy represents the LTV for policies sold in the period. Other commission per MA/MS policy represents the LTV for other products sold in the period, including DVH prescription drug plan, and other products, which management views as additional commission revenue on our agents’ core function of MA/MS policy sales. Pharmacy revenue per MA/MS policy represents revenue from SelectRx, and other revenue per MA/MS policy represents revenue from Population Health, production bonuses, marketing development funds, lead generation revenue, and adjustments from the Company’s reassessment of its cohorts’ transaction prices. Total operating expenses per MA/MS policy represents all of the operating expenses within Senior and Healthcare Services. The revenue to customer acquisition cost (“CAC”) multiple represents total revenue as a multiple of total marketing acquisition cost, which represents the direct costs of acquiring leads. These costs are included in marketing and advertising expense within the total operating expenses per MA/MS policy.

The following table shows combined Senior and Healthcare Services consumer per unit economics for the periods presented. Based on the seasonality of Senior and the fluctuations between quarters, we believe that the most relevant view of per unit economics is on a rolling 12-month basis. All per MA/MS policy metrics below are based on the sum of approved MA/MS policies, as both products have similar commission profiles.

Total revenue per MA/MS policy increased 26% for the twelve months ended September 30, 2025, compared to the twelve months ended September 30, 2024, primarily due to the increase in pharmacy revenue. Total operating expenses per MA/MS policy increased 32% for the twelve months ended September 30, 2025, compared to the twelve months ended September 30, 2024, driven by an increase in cost of goods sold-pharmacy revenue for Healthcare Services due to the growth of the business.

Life

Financial Results

The following table provides the financial results for the Life segment for the periods presented:

Operating Metrics

Life premium represents the total premium value for all policies that were approved by the relevant insurance carrier partner and for which the policy document was sent to the policyholder and payment information was received by the relevant insurance carrier partner during the indicated period. Because our commissions are earned based on a percentage of total premium, total premium volume for a given period is the key driver of revenue for our Life segment.

The following table shows term and final expense premiums for the periods presented:

Earnings Conference Call

SelectQuote, Inc. will host a conference call with the investment community on November 6, 2025 beginning at 8:30 a.m. ET. To register for this conference call, please use this link: https://registrations.events/direct/Q4I4247512. After registering, a confirmation will be sent via email, including dial-in details and unique conference call codes for entry. Registration is open through the live call, but to ensure you are connected for the full call we suggest registering at least 10 minutes before the start of the call. The event will also be webcasted live via our investor relations website https://ir.selectquote.com/investor-home/default.aspx.

Non-GAAP Financial Measures

This release includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. To supplement our financial statements presented in accordance with GAAP and to provide investors with additional information regarding our GAAP financial results, we have presented in this release Adjusted EBITDA, which, when presented on a consolidated basis, is a non-GAAP financial measure. This non-GAAP financial measure is not based on any standardized methodology prescribed by GAAP and is not necessarily comparable to any similarly titled measure presented by other companies. We define Adjusted EBITDA as net income (loss) plus interest expense, income taxes, depreciation and amortization, changes in fair value of warrant liabilities, and certain add-backs for non-cash or non-recurring expenses, including restructuring and share-based compensation expenses. The most directly comparable GAAP measure is net income (loss). We monitor and have presented in this release Adjusted EBITDA because it is a key measure used by our management and Board of Directors to understand and evaluate our operating performance, establish budgets, and develop operational goals for managing our business. In particular, we believe that excluding the impact of these expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core operating performance.

A reconciliation of the differences between Adjusted EBITDA and its most directly comparable GAAP measure, net income (loss), is presented below on page 14. The Company is unable to provide a quantitative reconciliation of forward-looking Adjusted EBITDA to its most directly comparable GAAP measure without unreasonable effort because it is not possible to predict certain information included in the calculation of such GAAP measure, including the fair value of outstanding warrants to purchase shares of the Company’s common stock. The unavailable information could have a significant impact on the Company’s GAAP financial results.

Forward Looking Statements

This release contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following: our reliance on a limited number of insurance carrier partners and any potential termination of those relationships or failure to develop new relationships; existing and future laws and regulations affecting the health insurance market; changes in health insurance products offered by our insurance carrier partners and the health insurance market generally; insurance carriers offering products and services directly to consumers; changes to commissions paid by insurance carriers and underwriting practices; competition with brokers, exclusively online brokers and carriers who opt to sell policies directly to consumers; competition from government-run health insurance exchanges; developments in the U.S. health insurance system; our dependence on revenue from carriers in our senior segment and downturns in the senior health as well as life, automotive and home insurance industries; our ability to develop new offerings and penetrate new vertical markets; risks from third-party products; failure to enroll individuals during the Medicare annual enrollment period; our ability to attract, integrate and retain qualified personnel; our dependence on lead providers and ability to compete for leads; failure to obtain and/or convert sales leads to actual sales of insurance policies; access to data from consumers and insurance carriers; accuracy of information provided from and to consumers during the insurance shopping process; cost-effective advertisement through internet search engines; ability to contact consumers and market products by telephone; global economic conditions, including inflation and tariffs; disruption to operations as a result of future acquisitions; significant estimates and assumptions in the preparation of our financial statements; impairment of goodwill; existing or potential litigation and other legal proceedings or inquiries, including the Department of Justice action alleging violations of the federal False Claims Act; our existing and future indebtedness; our ability to maintain compliance with our debt covenants; access to additional capital; failure to protect our intellectual property and our brand; fluctuations in our financial results caused by seasonality; accuracy and timeliness of commissions reports from insurance carriers; timing of insurance carriers’ approval and payment practices; factors that impact our estimate of the constrained lifetime value of commissions per policyholder; changes in accounting rules, tax legislation and other legislation; disruptions or failures of our technological infrastructure and platform; failure to maintain relationships with third-party service providers; cybersecurity breaches or other attacks involving our systems or those of our insurance carrier partners or third-party service providers; our ability to protect consumer information and other data; failure to market and sell Medicare plans effectively or in compliance with laws; and other factors related to our pharmacy business, including manufacturing or supply chain disruptions, access to and demand for prescription drugs, contractual reimbursement rates, and regulatory changes or other industry developments that may affect our pharmacy operations. For a further discussion of these and other risk factors that could impact our future results and performance, see the section entitled “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended June 30, 2025 and subsequent periodic reports filed by us with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) pioneered the model of providing unbiased comparisons from multiple, highly-rated insurance companies, allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads. Today, the Company operates an ecosystem offering high touchpoints for consumers across insurance, pharmacy, and virtual care.

With an ecosystem offering engagement points for consumers across insurance, Medicare, pharmacy, and value-based care, the company now has three core business lines: SelectQuote Senior, SelectQuote Healthcare Services, and SelectQuote Life. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a Patient-Centered Pharmacy Home™ (PCPH) accredited pharmacy, SelectPatient Management, a provider of chronic care management services, and Healthcare Select which proactively connects consumers with a wide breadth of healthcare services supporting their needs.

Eli Lilly & Co. and Novo Nordisk A/S have reached a sweeping agreement with the Trump administration to cut the prices of their blockbuster obesity drugs in exchange for tariff relief and expanded Medicare access — a move poised to reshape both the weight-loss market and broader healthcare policy in the U.S.

Under the deal, the two pharmaceutical giants will lower prices on their popular medications, Zepbound and Wegovy, bringing the monthly cost for eligible Medicare and Medicaid patients with obesity and related conditions down to roughly $245, with co-pays for Medicare users capped near $50. Both companies will also offer discounted direct-purchase programs: Eli Lilly will sell Zepbound’s lowest dose for about $299 a month via its LillyDirect platform, while Novo Nordisk’s Wegovy will be available at $499 through NovoCare. That’s less than half their current U.S. list prices, which exceed $1,000 per month.

In return, the companies receive a three-year exemption from new import tariffs on pharmaceutical products and fast-track regulatory reviews for upcoming weight-loss pills, which could reach the market next year at introductory prices near $149 per month. Both Lilly and Novo have pledged to manufacture these new products in the U.S., aligning with the administration’s push to onshore critical drug production.

The timing of the announcement, coming just days after midterm election losses for the Republican Party, underscores the political weight behind lowering healthcare costs. The White House framed the move as part of a broader effort to ease cost-of-living pressures, a theme that has dominated recent public sentiment.

For the pharmaceutical industry, the agreement signals a new era of negotiation — one in which pricing concessions may secure favorable trade treatment and regulatory acceleration. Rival firms including Pfizer, AstraZeneca, and Germany’s Merck KGaA have reportedly pursued similar arrangements to avoid heavier restrictions or penalties.

The deal also reflects growing momentum toward allowing Medicare coverage for anti-obesity drugs — something long prohibited under federal law. Beginning next year, patients with qualifying health conditions such as prediabetes or heart failure will gain access to these treatments under government plans, marking a significant policy shift that could expand the addressable market for weight-loss medications to millions of new patients.

From an investment standpoint, the move could reverberate across healthcare and biotech stocks. Large-cap players like Lilly and Novo may face slimmer margins on price-controlled drugs but stand to gain from much higher volume and broader insurance access. Small-cap biotech firms developing next-generation metabolic or appetite-control treatments could benefit from renewed investor attention and potential partnership opportunities as major pharmaceutical companies look to diversify pipelines and defend market share.

While the announcement temporarily weighed on Lilly’s shares and lifted Novo’s, analysts expect the broader obesity-drug market to continue expanding rapidly — particularly if upcoming oral treatments deliver similar efficacy at lower costs. For investors, the balance between pricing pressure and explosive demand could define one of the most lucrative — and politically charged — healthcare themes heading into 2026.