In one of the largest utility deals of the year, Black Hills Corp. (NYSE: BKH) and NorthWestern Energy Group, Inc. (Nasdaq: NWE) announced a definitive agreement to merge in an all-stock, tax-free transaction that gives the combined company an enterprise value of roughly $15.4 billion. The boards of both companies approved the deal unanimously, setting the stage for the creation of a new regulated electric and natural gas utility with operations across eight states.

Together, the companies will serve about 2.1 million customers, including more than 700,000 electric customers and 1.4 million natural gas customers. Their combined footprint will stretch across Arkansas, Colorado, Iowa, Kansas, Montana, Nebraska, South Dakota, and Wyoming, supported by nearly 97,000 miles of transmission and distribution lines and close to 3 gigawatts of generation capacity from a mix of thermal, hydro, and wind resources. The companies expect the deal to nearly double their combined rate base to $11.4 billion, providing the scale needed to meet rising energy demand and expand infrastructure for new industries such as data centers.

Management emphasized that the merger would create long-term value for both shareholders and customers. The new utility is projected to deliver annual earnings-per-share growth in the range of 5 to 7 percent, a pace that exceeds what either company had targeted on a standalone basis. Executives also pointed to stronger access to capital, a more balanced regulatory profile, and improved financial flexibility as key benefits of the transaction. Shareholders of Black Hills will own about 56 percent of the merged company, while NorthWestern shareholders will hold the remaining 44 percent.

The combined company will be headquartered in Rapid City, South Dakota, but leadership responsibilities will be shared. NorthWestern’s chief executive Brian Bird will serve as CEO, while Black Hills’ senior vice president and chief utility officer Marne Jones will become chief operating officer. Crystal Lail, currently CFO of NorthWestern, will take the same role in the new company, and Kimberly Nooney, CFO of Black Hills, will become chief integration officer. The board of directors will include six members from Black Hills and five from NorthWestern.

Both companies said they remain committed to safety, reliability, and sustainability, and they plan to continue investing heavily in grid modernization and renewable energy. With more than $7 billion in planned investments between 2025 and 2029, the new entity expects to play a central role in supporting the energy transition while keeping costs manageable for customers.

The merger, which is subject to shareholder approval, regulatory review in several states, and clearance from the Federal Energy Regulatory Commission, is expected to close within 12 to 15 months. If approved, it would establish a premier mid-cap regulated utility with diversified operations, predictable cash flows, and the capacity to pursue growth opportunities across an expanding energy landscape.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Reverse Split. Effective February 24, Comstock Inc. implemented a reverse split of its common stock at a ratio of 1-for-10, resulting in ~23.8 million shares outstanding. Comstock’s authorized number of shares of common stock remains 245.0 million. LODE shares began trading on a split-adjusted basis on February 25 and gained 5.6% to close at $3.05 per share.

Updating estimates. While we have made no changes to our 2024 estimates, we estimate first quarter 2025 weighted average shares outstanding of 154.5 million due to the timing of the reverse split. We have reduced our share count for the last three quarters of 2025 and project weighted average shares in 2025 to be 56.2 million. While our full year loss forecast of $22.0 million is unchanged, our earnings per loss estimate increased to $(0.39) from $(0.09).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Supply contracts secured. Comstock Metals has secured enough end-of-life solar panel supplier commitments to begin commissioning its first demonstration photovoltaic (PV) recycling facility upon receipt of required permits. Comstock Metals is negotiating agreements with major customers for industry-scale supply agreements. Comstock’s technology and renewable solutions provide a better alternative to land fill disposition of these materials. Comstock’s solution ensures safe deconstruction, decontamination, separation, and productive reuse of metals contained in end-of-life photovoltaic materials.

Demonstration PV recycling system. Comstock Metals is readying a demonstration facility that commercializes technologies for efficiently crushing, conditioning, extracting, and recycling metal and mineral concentrates from photovoltaics and other electronic devices. Comstock Metals previously received a storage permit and expects to receive the remaining air quality and solid waste permits shortly and expects to begin receiving, commissioning, and then processing the end-of-life panels in early 2024. Because Comstock Metals will likely receive a tipping fee for handling the end-of-life solar panels, Comstock Metals could begin generating cash flow with revenue recognized once the waste is processed and recycled.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The ongoing fighting between Israel and Hamas risks causing substantial disruptions to the global oil market, threatening to send crude prices to unprecedented levels according to a new warning from the World Bank.

In a worst-case scenario where the conflict escalates and key oil producing nations impose embargos, oil prices could surge as high as $157 per barrel. That would far surpass the previous record of $147 set in 2008 and have dramatic ripple effects across industries.

The World Bank laid out various scenarios in its latest commodity outlook report. In a “large disruption” comparable to the 1973 Arab oil embargo, global supplies could drop by 6 to 8 million barrels per day. This massive shortage of oil on the international market would cause prices to jump by 56-75%, catapulting prices up to the $140 to $157 range.

The crisis in 1973 quadrupled oil prices after Arab producers like Saudi Arabia and Iraq imposed an export ban on nations supporting Israel in the Yom Kippur War. While neither Israel nor Hamas are major oil exporters themselves, provoking producers in the surrounding region poses a major risk.

Surging crude prices would directly impact consumers at the gas pump. Each $10 rise in the cost of a barrel of crude translates to about a 25 cent increase in gas prices according to analysts. That means if oil hit $150, gas could surge above $4 per gallon nationally, far exceeding the recent highs earlier this year. Areas like California would likely see prices cross $5 or even $6 per gallon.

High fuel costs not only hurt commuters but drive up expenses for the transportation industry. Airlines would be forced to raise ticket prices to cover the inflated expense of jet fuel. Trucking and freight companies would also pass on the costs through higher shipping rates, feeding inflation throughout the economy.

Plastics and chemical manufacturers dependent on petrochemical feedstocks would see margins squeezed as oil prices stay elevated. Other goods with significant transportation expenses embedded in their supply chains would also see prices increased.

The pain would not be limited to oil-reliant sectors. As consumers are forced to spend more on transportation and energy needs, discretionary income gets reduced. This results in lower spending at retailers, restaurants and entertainment venues. Tourism also declines as pricier gas dissuades vacations and trips.

In essence, persistently high oil prices threaten to stall the economy by depressing spending, raising inflation and input costs across many industries all at once. While the US is now a net exporter of crude and refined fuels, it remains exposed to global price movements shaped by international events.

The World Bank warned that an escalation of the Israel-Hamas tensions could create a dual supply shock when combined with reduced oil and gas exports from Russia. Global markets are still reeling from the loss of Russian energy supplies due to Western sanctions and bans.

Prior to Russia’s invasion of Ukraine, investment bank Goldman Sachs had predicted oil could reach $100 per barrel this year. The fighting has already caused prices to spike above $120 at points, showing how geopolitical instability in one region can roil prices worldwide.

The grim scenarios described by the World Bank underscore the interconnectedness binding energy markets across the globe. An event thousands of miles away increasing instability in the Middle East could end up costing American consumers, businesses, and the economy dearly.

While the baseline forecast calls for prices to moderate over the next year, an expansion of the Israel-Hamas conflict could upend those predictions. Investors, businesses, and policymakers must watch the situation closely to prepare for the economic impacts of further turmoil.

All parties involved must also be cognizant of how violence that disrupts oil production and trade risks global fallout. Diplomatic solutions take on new urgency to prevent a worst-case scenario that would inflict widespread hardship as oil races past $150 per barrel into uncharted territory.

In a bold move to combat surging fuel prices and rampant inflation, President Biden is unleashing a flood of black gold onto the markets. The White House is planning to tap a massive 180 million barrels of crude oil from the nation’s Strategic Petroleum Reserve (SPR) – the biggest withdrawal in the reserve’s history.

The news sent oil prices tumbling 5% in early trading as speculators reacted to the supply boost. But will the SPR floodgates really succeed in taming the oil price beast that has economists worried about recession?

The sheer size of the release, equivalent to two full days of global oil consumption, grabbed headlines. Set to be gradually emptied over several months, Biden’s SPR unleashing is meant to act like a shot of bear tranquilizer for the raging oil market.

Ever since Russia’s invasion of Ukraine, reduced supply from the world’s No. 2 exporter combined with surging demand has driven prices to their highest levels since 2008. Brent crude already flirted with a mind-boggling $140 per barrel in March. Even after the SPR news-driven dip, benchmark oil remains stubbornly high at around $105.

For Biden, doling out the emergency crude is a midterm elections Hail Mary pass. Painfully high gas prices have contributed to the president’s dismal approval ratings. Tapping the SPR to lower fuel costs may be his best bet to avoid Democrats enduring a disastrous drubbing by the Republicans in November.

Beyond politics, uncorking America’s oil reserves also sends an important message to the market. It signals the Administration’s determination to fight an inflation rate that keeps printing four-decade highs. Few things impact inflation expectations like changes in oil prices. A meaningful drop could help tamp down the runaway price increases eroding consumer confidence.

But will the effort succeed or will it flounder like past attempts? With global crude inventories at historic lows, many analysts see the SPR release as a mere band-aid solution. It provides some short-term relief but doesn’t fix the supply and demand imbalance.

Goldman Sachs estimates the 180 million barrel slug will help rebalance markets this year. But it warned the move doesn’t resolve the structural deficit caused by excluding Russian exports.

Previous SPR releases also failed to produce lasting effects. Oil prices quickly rebounded after 60 million barrels were tapped in November 2021 and another 30 million in March 2022.

This time, the White House is also counting on allies for help. The International Energy Agency meets soon to potentially coordinate a collective release from its members’ reserves.

But Biden’s SPR gambit already seems at odds with other moves meant to restrict oil supply and fight climate change. Canceling the Keystone XL pipeline permit and banning new federal drilling auctions counterproductively worsened the supply crunch. A of couple million extra daily barrels from those sources would have eased pressure on prices.

The Administration now finds itself trying to fix with one hand problems partly created by the other. That internal tension undermines the large SPR release’s credibility.

Traders also scoffed when OPEC refused to boost production more than a token amount after the U.S. lobbied for extra output. With the cartel and allies like Russia benefitting handsomely from $100+ oil, they have little incentive to pump much more.

Meanwhile, risks of a demand-killing recession loom if the Fed’s inflation fight requires jumbo interest rate hikes. And Covid lockdowns in China already hurt oil demand in the world’s largest importer.

So while Biden’s SPR flow should offer some near-term relief at the pump, it may not move the needle much for long. Markets fear what happens if 180 million barrels merely postpones the supply day of reckoning rather than preventing it.

With inventories low, spare capacity shrinking, geopolitical unrest continuing, and ESG considerations constraining investment, oil looks poised to remain highly volatile. While the SPR release was historic in size, it likely won’t fully tranquilize the energy markets.

Oil markets and energy stocks often get painted with a broad brush. But within the sector, offshore drilling stocks offer upside that many investors are overlooking. Despite cries of peak oil demand, fundamentals for rig owners point to gains ahead.

The oil services sector has rocketed over 50% higher in the last year, soundly beating the S&P 500. Yet offshore drilling stocks remain unloved. This creates an opportunity for investors willing to take a contrarian bet.

The bull case lies in constrained supply and rapidly rising prices. ESG considerations have limited capital investment in new oil production. But robust demand has returned as pandemic impacts recede. This supply/demand imbalance has sent oil above $80 per barrel.

Day rates for offshore rigs are soaring as utilization rates stick near 90%. However, shipyards are focused on liquefied natural gas, not building fresh drilling ships. That means supply can’t catch up to growing demand in a hurry.

This grants pricing power to rig owners. Valaris, Noble, and Weatherford have emerged from bankruptcy with pristine balance sheets. Meanwhile Transocean boasts the most high-specification rigs, positioning it to profit from climbing day rates.

Yet valuations look disconnected from fundamentals. Offshore drillers trade at up to an 80% discount to replacement value, signaling the market doubts their potential. But conditions point to further gains.

Why Energy Could Shine for Investors

Beyond compelling fundamentals, two key reasons make energy stocks stand out right now:

Inflation hedge – Energy equities have historically held up well during inflationary periods. With prices still running hot, oil stocks may offer protection if high inflation persists.

Contrarian bet – Energy is the most hated sector this year, with heavy net outflows from funds. That sets up a chance to buy low while others are selling.

To be clear, the long-term peak oil argument holds merits. The global energy transition will likely constrain fossil fuel demand over time. But that shift will take decades to play out.

In the meantime, diminished investment and stiff demand creates room for shares like offshore drillers to run higher. For investors willing to make a contrarian bet, the neglected energy space offers rare value.

ESG Sours Sentiment But Oil Remains Key

What about the ESG push away from fossil fuels? Shift is clearly underway. But hydrocarbons still supply 80% of global energy needs. Realistically, oil and gas will remain vital to powering the world for years to come.

Market sentiment has soured on all things oil. But investors should remember that supply/demand, not narrative, ultimately drives commodity prices. Offshore drillers look primed to benefit from that dynamic.

While oil markets face uncertainty beyond the next decade, conditions now point to upside in left-behind niches like offshore drilling stocks. For investors who see value where others only see headwinds, forgotten energy corners may hold diamonds in the rough.

Blackrock’s Support for ESG May Have Been Unsustainable

Blackrock, a firm with a reputation for strongly supporting ESG resolutions, having voted yes on 47% of them in 2020, voted down 93% in the past year. The company provided the reasons for shunning 371 proposals out of 399 in its annual Stewardship Report released on August 23rd. With $9.4 trillion under management, investors pay attention to the investment manager. This gives it the power, whether it likes it or not, to create trends as others follow its lead. Should the company’s adjusted position on ESG be taken as something others want to mimic? The reasons given leave that in question.

BlackRock is the world’s largest asset manager. As such, the funds it manages own significant amounts of shares of a broad array of public companies. The Blackrock funds vote on important matters related to the underlying companies if a corporate resolution requires a shareholder vote. Think of the ETF or mutual fund as a trust, and the fund manager, Blackrock, gets to vote on behalf of the assets in the trust. Whereas if an investor owns individual shares of a company, they get to decide and vote themselves, either at a board meeting or more likely, through a proxy statement. Certainly, the amount of control over the decisions of corporations worldwide given to an asset manager of this size is immense.

Each year, the company files a report on its voting during the proxy season. It broke records by voting down 91% of all shareholder proposals and against 93% of those focused on environmental and social issues during the 2023 proxy year. The 7% of ESG proposals that BlackRock supported this year is down sharply from 2022, when BlackRock’s investment stewardship team supported 24% of such proposals, and from 2021, when it supported 47%.

BlackRock’s Investment Stewardship team, makes the voting decisions on both management and shareholder proposals on behalf of BlackRock’s clients. It said the large number of “NO” votes this year is partly related to a huge influx of shareholder proposals. These were described as “poor quality” by the BIS team, either because they were “lacking economic merit,” were “overly prescriptive” and “sought to micromanage a company’s strategy,” or were simply redundant, asking a company to do something it had already done, the Stewardship Report said.

BlackRock’s support for management proposals (not shareholder proposals), which accounted for more than 99% of the roughly 172,000 proposals voted on by BIS, remained high at 88%.

BlackRock’s trend of voting against shareholder proposals is largely in line with other fund managers. The median shareholder support for environmental and social proposals in the U.S. fell sharply from 25% in 2022 to just 15% in the 2023 proxy year.

The firm has backed away from ESG as a term if not a concept. The most recent CEO newsletter did not include the acronym at all, and during a June interview, CEO Larry Fink said he does not use the term, he gave this reason, “I’m not blaming one side or the other, but it has been totally weaponized,” Mr. Fink said. “In my last CEO letter, the phrase ESG was not uttered once, because it’s been unfortunately politicized and weaponized.” He now has a reluctance to have his firm associated with the term ESG after a wave of backlash from both sides of the political spectrum.

In December 2022, Florida’s chief financial officer announced that the state would pull $2 billion worth of assets managed by BlackRock, the largest such divestment by a state opposed to the asset manager’s environmental, social and corporate governance (ESG) policies. BlackRock also lost some of its business of oil rich Texas from its government pension funds because of its ESG policies. Louisiana and Missouri, have also taken steps to divest from BlackRock.

Although not specifically stated in the report, Blackrock fund managers still support the idea that good corporate citizenship could in turn, benefit shareholders. But they will no longer be out front as though ESG factors are the most important criteria. Earlier this month S&P Global Ratings decided it would not provide ESG ratings separate from its credit ratings. Instead, S&P will factor in all of the obligors’ business practices as it relates to risk of non-payment, and assign only a credit rating.

The term has become polarizing as differing political philosophies tend to stand together in support of ESG issues being taken into investment consideration, and other political leanings stand opposed to the not fully developed concept. This has hurt Blackrock.

Republican politicians have been probing Blackrock’s business dealings and asking conservative-leaning state pension funds to divest from the company, which they say has unfairly excluded the traditional energy sector.

On the other hand, environmental activists have lambasted Mr. Fink and his company for not doing enough to stop climate change, protesting in front of BlackRock’s headquarters and heckling senior executives at public speaking engagements. In June Blackrock began providing high-level security to protect Mr. Fink and others in management.

Take Away

When you put your money into most mutual funds, you give away the power that comes with voting on important matters to the underlying shares held by the trust of which you are a part owner. As mutual funds and ETFs have grown, more of the power to guide companies has been handed to the elite running asset management companies.

The growth in popularity in “sustainability” investing caused a rush from investors to these funds, which then needed to place assets in the limited number of companies in the segment. This caused a rise in the share prices of the companies and a rise in the popularity of the funds. Many investors were indifferent to ESG, but not indifferent to making money, they also jumped in. Companies quickly caught on and adjusted their logos to include leaves and the color green, altering some business practices.

While the leadership that Blackrock provides may signal the eventual demise of the term ESG, there has always been, and will always be an interest in putting your money where your heart is. The concept will live, but with Blackrock’s lead, the acronym may transform to something that is less political and less likely to cause protests outside of his home.

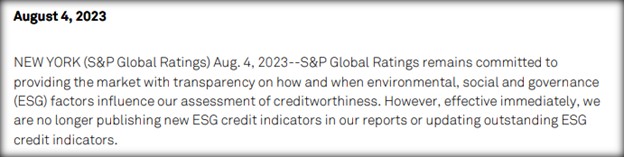

Why S&P Global Ratings Dropped Its Alphanumeric ESG Ratings

As evidence that new concepts need to go through a cycle and find their place, S&P Global Ratings has stopped including environmental, social, and governance (ESG) ratings on its reports. S&P Global Ratings is the credit ratings division of Standard & Poor’s. The division specializes in providing company-sponsored research, analysis, credit ratings, and data to assist investors in evaluating the creditworthiness and risk associated with financial instruments and entities.

In an official press release titled, S&P Global Ratings Update On ESG Credit Indicators released this month. The prominent and perhaps best-known Nationally Recognized Statistical Ratings Organization (NRSRO) revealed its decision to discontinue the publication of new ESG credit indicators, and will not be updating those ESG scores previously determined.

Source: S&P Global Ratings, Dated August 4, 2023

S&P defines ESG credit indicators as “those ESG factors that can materially influence the creditworthiness of a rated entity or issue.” The rating agency said in the release that it had initially begun publishing alphanumeric ESG credit indicators for publicly rated entities in some sectors and asset classes in 2021. “These indicators were intended to illustrate and summarize the relevance of ESG credit factors on our rating analysis through the use of an alphanumerical scale,” the agency added, “They supplemented the narrative paragraphs in our credit rating reports where we describe the impact of ESG credit factors on creditworthiness.”

It has been just two years, and S&P has changed its reporting, if not its methodology. The release explained that after further review the “dedicated analytical narrative paragraphs in our credit rating reports are most effective at providing detail and transparency on ESG credit factors material to our rating analysis, and these will remain integral to our reports.” So there is no separate breakout rating, but to the extent that an ESG related factor could impact creditworthiness, S&P will include the discussion in its write-ups, and it will be reflected when appropriate in an institutions’ security ranking.

S&P Global was clear that the immediately implemented policy does not affect its ESG principles criteria or its research and commentary on ESG-related topics, including the influence that ESG factors may have on a companies ability to pay interest and return principal.

Fitch Ratings, chief credit officer, Richard Hunter told Pension and Investments that: “Fitch believes that there are profound limits to what text disclosures can do for investors monitoring an entire portfolio of hundreds of serviced issuers and bonds. This is the second time in less than amonth that the two NRSROs demonstrated very different methodologies. After Fitch Ratings downgraded U.S. backed Treasuries and other obligations, S&P said they would not unless the U.S. was going to miss a payment.

To round out the big three institutional rating agencies, Moody’s said in a statement that it “incorporates all risks, including those related to ESG, into its credit ratings when they are material, and also publishes ESG scores on a 1 to 5 scale.”

Take Away

The definitions, overall landscape, and actions taken to support sustainability are evolving. S&P Global Ratings’ decision to not separately rank obligors is a strategic recalibration in its presentation of ESG factors that may impact an entities ability to pay. It believes the credit factors don’t warrant a separate carve-out within their reports – and that clarity and assessing creditworthiness is best discussed and not boiled down to an alphanumeric rating for use by investors.

Investors Especially Hate Companies that Say They’re Good Then Behave Badly – Unless the Money is Good

The Big Idea

Stock investors punish companies caught doing something unethical a lot more when these businesses also have a record of portraying themselves as virtuous. This hypocrisy penalty is the main finding of a study we recently published in the Journal of Management.

Companies often espouse their supposed virtue – known as “virtue signaling” – usually with the aim of getting benefits, such as higher sales, positive investor sentiment or better employees. We wanted to know what happens when such companies then do something wrong.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Brian L. Connelly, Professor of Management and Entrepreneurship, Auburn University, Lori Trudell, Assistant Professor of Entrepreneurship, Clemson University.

So we examined corporate communications and media coverage for every company in the Standard & Poor’s 500 to develop a comprehensive database of both virtue signaling and misconduct.

To gauge virtue signaling, we conducted linguistic analysis of each company’s letters to shareholders. This is a form of computer-aided text analysis that identifies and categorizes language to draw inferences. For example, we looked for words and patterns to identify conscientiousness, empathy and integrity and considered how language patterns developed over time. Each company received a score that reflected how much of their corporate communication was devoted to virtue rhetoric.

We then examined over half a million news articles to identify unethical behavior, such as egregious events like a CEO’s being fired for sexual misconduct, but also less severe transgressions, like not treating employees fairly.

Finally, our study considered how shareholders respond. Specifically, we looked at price swings the day after the media initially reported the misbehavior.

We found that share prices fell 1.5% overnight in response to unethical behavior when companies had engaged in lots of virtue signaling, compared with 0.4% for those that did less virtue signaling or none at all. For an average company, that difference amounts to over half a billion dollars in lost value.

Keep in mind, too, that these ethical violations are not uncommon events. About a quarter of companies in our sample engaged in this kind of behavior in any given year. Stated simply, bad things happen, and when they do the stock market will clobber those who do not seem to be walking their talk.

Well, with one critical exception related to a company’s expected future performance. If investors anticipate that a company will perform well in the future, there is no hypocrisy penalty – the consequences of misconduct are the same for those that use virtue signaling and those that do not.

Apparently, shareholders are very concerned about executives who say one thing and do another – unless the company is expected to make lots of money, in which case there is little or no penalty for unethical behavior.

Why it Matters

Many companies, and the CEOs who run them, publicly say they care a lot about their people, the environment and the communities around them, among other virtuous signals.

For example, ice cream maker Ben & Jerry’s proudly declares that it seeks to “advance human rights and dignity, support social and economic justice for historically marginalized communities, and protect and restore the Earth’s natural systems.” At the other end of the political spectrum, restaurant chain Chick-fil-A proclaims that it is “about more than just selling chicken”; its corporate purpose: “To glorify God by being a faithful steward of all that is entrusted to us.”

Whether from the right or the left, this virtue signaling establishes, and implicitly promises adherence to, a set of ethical standards. What happens, though, when behavior does not align with virtuous talk?

Academics have two decidedly different views about how to answer this question. Some contend that virtue signaling buffers companies from the negative ramifications of misconduct. Another perspective suggests that there’s a more severe adverse reaction whenever anyone deviates from expectations. Think, for example, of the special vehemence reserved for the priest who pilfers from the church coffers.

Our study confirms that the latter – a hypocrisy penalty – is more likely what is happening.

What’s Next

We are now exploring different types of shareholders and how they respond to organizational behavior – and misbehavior. For example, social activist funds could be especially put off when companies in which they invest behave badly, whereas the most powerful institutional investors are less likely to be concerned about a mismatch between a company’s words and deeds.

Berkshire Hathaway Finds ESG Concerns Are a Plus for Oil and Gas Investments

Warren Buffett’s Berkshire Hathaway is capitalizing on the current commodity price dip to expand its oil and gas sector stake. This year, Berkshire committed $3.3 billion to increase its ownership in a liquefied natural gas export terminal in Maryland. Additionally, it raised its stake in Occidental Petroleum Corp. by 15% and acquired more shares in five Japanese commodity traders. The company is also lobbying for increased financial support for natural gas power plants.

Warren Buffett, the Oracle of Omaha, demonstrated how he earned the “oracle” title during the most uncertain days of the pandemic, by investing heavily in oil and gas. The sector has had impressive returns as it posted record earnings in 2022. The 92-year-old Buffett is not booking the massive gains by selling; instead Buffett is selectively adding to positions.

Are Buffett’s investment moves classic bargain-hunting, with the energy sector possibly undervalued tied to environmental, social, and governance concerns, as well as an anticipation of declining demand for fossil fuels in the future? Based on standard metrics, the energy sector is undervalued. According to data from Bloomberg, energy now trades at the lowest price-to-earnings valuation among all sectors in the S&P 500 Index, at the same time it generates the most cash flow per share. And, as a help to the industry, Berkshire’s energy division is actively lobbying for a bill that would allocate at least $10 billion to natural gas-fired power plants in Texas to support the state’s grid.

His approach in the sector is obviously deliberate and narrowly targeted. Despite Buffett’s interest in energy, his fossil fuel investments aren’t without nuances. For example, Berkshire remains the third-largest shareholder in Chevron Corp., even after it reduced its stake by about 21% in the first quarter. Each investment in companies like Occidental and Cove Point LNG has unique aspects that position them as valuable assets in the global energy landscape, regardless of the path that any U.S. or global energy transition takes.

Buffett believes that shale, a substantial part of U.S. oil production, is different and even preferred over conventional sources of oil in the Middle East and Russia. One difference is taking shale from the ground and into production can be done more quickly and have a shorter production lifespan. This provides flexibility for operators to adapt to changes in oil demand and prices. At Berkshire’s annual meeting in May, Buffett emphasized making rational decisions about energy production and criticized both extremes in the climate debate.

One of Buffett’s nuanced and targeted energy investments is Cove Point LNG. It not only exports liquefied gas but also has the rare capability to import gas, making it more versatile than other facilities along the Gulf Coast. With rising global LNG demand driven by Europe’s shift away from Russian gas and Asia’s use of gas for power generation, Cove Point’s long-term contracts with buyers, including Tokyo Gas Co. and Sumitomo Corp., make it appealing. Berkshire is Sumitomo’s second-largest shareholder after the Japanese government’s pension fund.

Outside of its stock holdings, Berkshire Hathaway Energy, under the leadership of Buffett’s expected successor Greg Abel, has been performing well. Earnings for the division hit a record high of $3.9 billion in 2022, nearly doubling over five years.

Take Away

The world’s appetite for energy, whether from fossil fuels or renewables, seems insatiable; even amid a global penchant to reduce fossil fuel use, oil demand is expected to continue rising throughout the decade. While environmental concerns have caused some investors to shy away from the energy sector, Buffett’s investments demonstrate his belief that ESG considerations are keeping oil and gas stocks attractively priced. Market participants prioritizing ESG, therefore, presents an opportunity for Berkshire to profit further from its strategic investments in the oil and gas sector.

What is Hydrogen, and Can it Really Become a Climate Change Solution?

As the United States and other countries react to achieve a goal of zero-carbon electricity generation by 2035, energy providers are swiftly ramping up renewable resources such as solar and wind. But because these technologies churn out electrons only when the sun shines and the wind blows, a backup from more reliable energy sources would prevent blackouts and brownouts. Currently, plants burning fossil fuels, primarily natural gas, fill in the gaps. Can we stop using fossil fuels now? – Paul Hoffman, Managing Editor, Channelchek

Hydrogen, or H₂, is getting a lot of attention lately as governments in the U.S., Canada and Europe push to cut their greenhouse gas emissions.

But what exactly is H₂, and is it really a clean power source?

I specialize in researching and developing H₂ production techniques. Here are some key facts about this versatile chemical that could play a much larger role in our lives in the future.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Hannes van der Watt, Research Assistant Professor, University of North Dakota.

So, What is Hydrogen?

Hydrogen is the most abundant element in the universe, but because it’s so reactive, it isn’t found on its own in nature. Instead, it is typically bound to other atoms and molecules in water, natural gas, coal and even biological matter like plants and human bodies.

Hydrogen can be isolated, however. And on its own, the H₂ molecule packs a heavy punch as a highly effective energy carrier.

It is already used in industry to manufacture ammonia, methanol and steel and in refining crude oil. As a fuel, it can store energy and reduce emissions from vehicles, including buses and cargo ships.

Hydrogen can also be used to generate electricity with lower greenhouse gas emissions than coal or natural gas power plants. That potential is getting more attention as the U.S. government proposes new rules that would require existing power plants to cut their carbon dioxide emissions.

Because it can be stored, H₂ could help overcome intermittency issues associated with renewable power sources like wind and solar. It can also be blended with natural gas in existing power plants to reduce the plant’s emissions.

Using hydrogen in power plants can reduce carbon dioxide emissions when either blended or alone in specialized turbines, or in fuel cells, which consume H₂ and oxygen, or O₂, to produce electricity, heat and water. But it’s typically not entirely CO₂-free. That’s in part because isolating H₂ from water or natural gas takes a lot of energy.

How is Hydrogen Produced?

There are a few common ways to produce H₂:

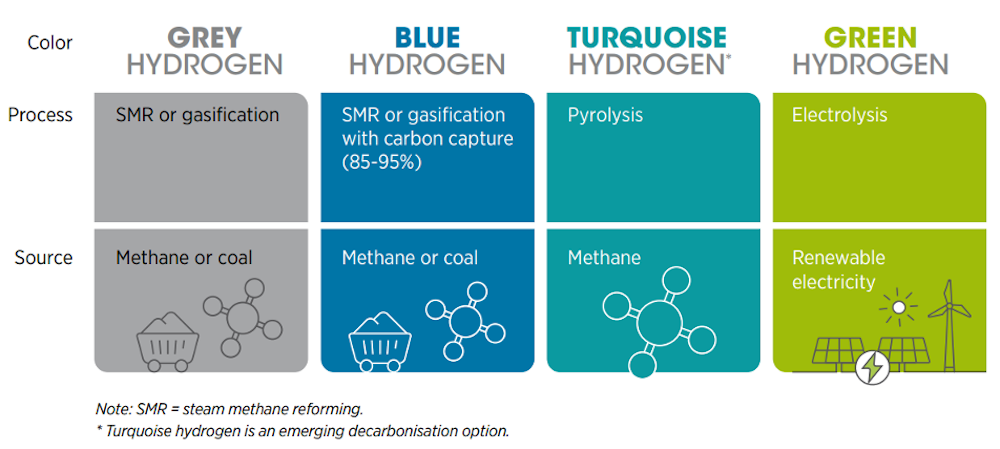

Electrolysis can isolate hydrogen by splitting water – H₂O – into H₂ and O₂ using an electric current.

Methane reforming uses steam to split methane, or CH₄, into H₂ and CO₂. Oxygen and steam or CO₂ can also be used for this splitting process.

Gasification transforms hydrocarbon-based materials – including biomass, coal or even municipal waste – into synthesis gas, an H₂-rich gas that can be used as a fuel either on its own or as a precursor for producing chemicals and liquid fuels.

Each has benefits and drawbacks.

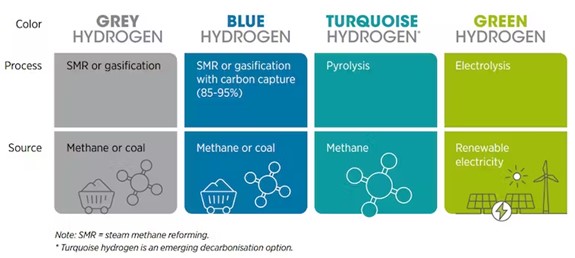

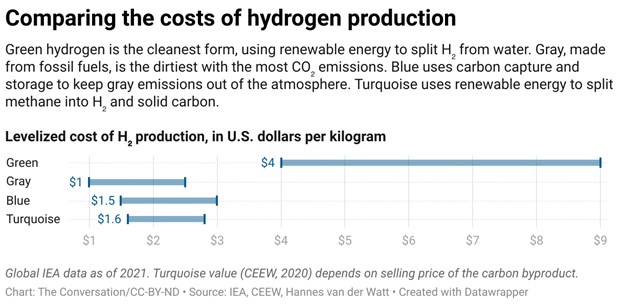

Green, Blue, Gray – What Do the Colors Mean?

Hydrogen is often described by colors to indicate how clean, or CO₂-free, it is. The cleanest is green hydrogen.

Green H₂ is produced using electrolysis powered by renewable energy sources, such as wind, solar or hydropower. While green hydrogen is completely CO₂-free, it is costly, at around US$4-$9 per kilogram ($2-$4 per pound) because of the high energy required to split water.

The largest share of hydrogen today is made from natural gas, meaning methane, which is a potent greenhouse gas. IRENA (2020), Green Hydrogen: A guide to policymaking

Other less energy-intensive techniques can produce H₂ at a lower cost, but they still emit greenhouse gases.

Gray H₂ is the most common type of hydrogen. It is made from natural gas through methane reforming. This process releases carbon dioxide into the atmosphere and costs around $1-$2.50 per kilogram (50 cents-$1 per pound).

If gray hydrogen’s CO₂ emissions are captured and locked away so they aren’t released into the atmosphere, it can become blue hydrogen. The costs are higher, at around $1.50-$3 per kilogram (70 cents-$1.50 per pound) to produce, and greenhouse gas emissions can still escape when the natural gas is produced and transported.

Another alternative is turquoise hydrogen, produced using both renewable and nonrenewable resources. Renewable resources provide clean energy to convert methane – CH₄ – into H₂ and solid carbon, rather than that carbon dioxide that must be captured and stored. This type of pyrolysis technology is still new, and is estimated to cost between $1.60 and $2.80 per kilogram (70 cents-$1.30 per pound).

Can We Switch Off the Lights on Fossil Fuels Now?

Over 95% of the H₂ produced in the U.S. today is gray hydrogen made with natural gas, which still emits greenhouse gases.

Whether H₂ can ramp up as a natural gas alternative for the power industry and other uses, such as for transportation, heating and industrial processes, will depend on the availability of low-cost renewable energy for electrolysis to generate green H₂.

It will also depend on the development and expansion of pipelines and other infrastructure to efficiently store, transport and dispense H₂.

Without the infrastructure, H₂ use won’t grow quickly. It’s a modern-day version of “Which came first, the chicken or the egg?” Continued use of fossil fuels for H₂ production could spur investment in H₂ infrastructure, but using fossil fuels releases greenhouse gases.

What Does the Future Hold for Hydrogen?

Although green and blue hydrogen projects are emerging, they are small so far.

Policies like Europe’s greenhouse gas emissions limits and the 2022 U.S. Inflation Reduction Act, which offers tax credits up to $3 per kilogram ($1.36 per pound) of H₂, could help make cleaner hydrogen more competitive.

Hydrogen demand is projected to increase up to two to four times its current level by 2050. For that to be green H₂ would require significant amounts of renewable energy at the same time that new solar, wind and other renewable energy power plants are being built to provide electricity directly to the power sector.

While green hydrogen is a promising trend, it is not the only solution to meeting the world’s energy needs and carbon-free energy goals. A combination of renewable energy sources and clean H₂, including blue, green or turquoise, will likely be necessary to meet the world’s energy needs in a sustainable way.

How Decision-Making and Market Impact is Shifting for Retail Investors

Retail investors’ preferences change over time. This impacts sector strength and the overall direction of markets. Even the methods of interacting with exchanges change as newer products like trading apps, artificial intelligence, and exchange-traded products (ETP) become available.

The influence retail has is growing, and anecdotally shifting preferences happen more quickly. Within this category, there are self-directed investors with different knowledge bases and at different stages of their lives. As people move through different stages, their concerns, outlooks, and risk tolerances adjust. Nasdaq just published its second annual survey of retail investors to measure how their interests are changing and what impact that may have. The survey of 2,000 investors from Gen Z to Baby Boomers uncovered some surprising trends in decision-making, fears, comfort zones, and asset class preferences.

Generational Groupings

There were a number of commonalities exposed by the Nasdaq survey between the different generations. They all listed their greatest concerns to be inflation and recession, but while the youngest (Gen Z, born 1997 – 2012) found housing and real estate a deep concern, the oldest group (Baby Boomers, born 1946 – 1964) are more concerned about tax rate changes. The generations in the middle (Gen X born 1965 –1980) and (Millennials born 1981 – 1996) show a greater concern over interest rate changes.

The survey question sought to understand how much time investors in each generation spent researching buy and sell investment decisions. Of Gen Z, on average 48% spent less than an hour, while 3% of these younger adults evaluated the transaction for at least a month. The next age category, Millennials, spent a bit more time on diligence. Only 28% would buy or sell with less than an hour of thought put into the transaction. Of this group, 4% took a month or longer to decide. This trend toward more time researching research continued as the survey reveals the Gen X greater propensity to spend more time evaluating before a purchase. Only 15% would press the buy or sell button with less than an hour spent understanding the investment – 7% of Gen X investors say they take a month or longer.

A big difference between the youngest and the oldest, is that among the Gen Z investors, although almost half said they spend fewer than 60 minutes researching, 0% said they did not research at all. Of the Baby Boomers surveyed, 24% indicated they spend no time researching before they buy or sell. It’s unclear if this is because the older group is less tech savvy, hires a professional to do the research, or believes they have the knowledge to move without digging deeper.

Overlap in Generational Preferences

Data Sources: Nasdaq

Other Trends

Despite their top concerns listed as recession and inflation, 71% of Gen Z and 50% of Millennials say they are investing more aggressively. This is in stark difference to the 9% of Boomers and 20% of Gen X describing their strategies as more aggressive than the previous year.

The influence of Twitter, Facebook and even TikTok keeps expanding. 73% of Gen Z use TikTok as a source for investment information. This is an 18% increase from the prior year. Baby boomer TikTok investment use rose by 16% to its current 25%.

The investment themes from year-to-year show ESG and crypto interest sinking, while robotics and other autonomous technology is where the focus has increased most. Younger investors are more active in their investments than before, and more frequently conducting their own research ahead of transacting. Investors of all ages are more likely to consider alternative options than they had before, these could include options, cryptocurrencies, exchange traded products, etc.

Competition among brokerage platforms is as fierce as it is in any innovative, tech heavy industry. The availability of advanced technology and commission-free trading have made investing more accessible, especially for the younger investors.

Take Away

The second annual survey conducted by Nasdaq indicates that the retail investor growth and power we’ve experienced in recent years was not a fad, it is growing and becoming more sophisticated. They are more influential and should be understood as they are here to stay. This is expected to continue to disrupt and influence markets dramatically.

As retail trends take a higher position of importance in defining the day-to-day challenges of investing and mapping the markets’ future, these self-directed investors are finding more services to accommodate them. One source is the Channelchek platform where retail and institutional investors, of all ages can review research reports, absorb video discussions with management of interesting opportunities, expand understanding through daily articles, and, if relevant, attend a roadshow to meet a particular company’s management.

Could Small Oil Companies Perform Especially Well With OPEC’s Reduced Output

Earlier this week, OPEC+ announced the cartel’s plans for production cuts. Saudi Arabia and other oil-producing members of OPEC+ defied expectations by announcing they would implement production cuts of around 1.1 million barrels a day. Prices of WTI and Brent crude quickly moved higher in the futures market – energy stocks followed. The increased cost of petroleum directly impacts the price of fuel and plastics and indirectly impacts goods that involve transportation – which is mostly all goods.

The decision by OPEC+ is highly likely to put upward pressure on CPI and PPI inflation measures as early as April. The CPI report for April will be released on May 10, and PPI on May 11. Id there good news for investors in the OPEC decision? What stocks might investors look at as potentially benefiting, assuming the OPEC countries adhere to the new production levels?

Background

U.S. markets were not open when the Organization of Petroleum Exporting Countries announced the large cut of over one million barrels per day. When regular trading resumed in the U.S. on Monday, oil prices jumped up 6.3%, and crude oil prices breached $80. Energy stocks, as measured by the Energy Sector SPDR (XLE) rose 4.5%. The price of crude based on futures contracts and the XLE have remained near these levels.

With change comes opportunity. Investors and traders are now trying to determine if this is the start of a new upward trend for the energy sector and, if so, what specific moves may benefit investors most.

One consideration they may have is that, although OPEC is cutting production, the members aren’t the only producers. Historically, domestic production was increased in N. America when prices climbed. This has been less so in recent years as the number of U.S. rigs operating hasn’t increased as might have been expected.

Will this dramatic price spike now prompt action from domestic producers? In his Energy Industry Report published on April 4, titled Why Domestic Producers Cannot Offset OPEC Production Cuts, Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, says that oil is produced in the U.S. at around $30-$40 per barrel. Heim says in his report, “If producers had the ability to ramp up drilling, we would have thought they would have done so even at $60/bbl. prices.”

Possible Beneficiaries

According to the Noble Analyst, large producers have been constrained from growing their oil operations which stems from political and even shareholder pressures to move away from carbon-based energy products. However, Heim says in his report, “Smaller producers face less pressure. Companies with ample acreage and drilling prospects are best positioned to take advantage of a prolonged oil price upcycle.”

In a conversation with the analyst, he shared that when oil prices spiked during the second half of the pandemic and later had added upward movement with the start of the Russia/Ukraine war, many small oil companies took in enough additional revenue to strengthen their finances. Some even began paying dividends for the first time, while others increased their regular dividend to shareholders.

These smaller oil producers not in the political spotlight that may reap additional benefits from OPEC’s cut could include Hemisphere Energy (HMENF). This company increased production by 55% in 2022. According to a research report by Noble Capital Markets initiating coverage on Hemisphere (dated April 3, 2023), “proven reserve findings and development costs are less than C$12/barrel, providing an extremely attractive return on investment for drilling.” It continued, “Hemisphere’s finding and development costs are among the lowest of western Canadian producers and reflect its favorable drilling locations and the company’s experience drilling in the area.” The increase in price per barrel could enhance cash flow for this North American producer, allowing it to expand production.

Permex Petroleum (OILCD, OIL.CN) is a junior oil and gas company that already had a significant upside potential before the jump in per-barrel prices. This boost in cash from higher oil prices and a possible uplisting to the NYSE, could work to benefit shareholders.

InPlay Oil (IPOOF) increased annual production last year by 58%. InPlay is an example of a smaller producer that has been able to increase drilling when prices rise. It has used increased cash flow to lower debt levels by 59% and pay shareholders with its first dividend payment.

Indonesia Energy Corporation Ltd. (INDO) is an oil and gas exploration and production company operating in Indonesia. The company plans on drilling 18 wells in the Kruh Block (four have been completed). Covid19 steps in the region where Indo Energy operates have pushed back drilling that was expected in 2023-2024 one year.

Take Away

With change comes opportunity. Higher oil prices will impact all of us that must still occasionally stop our internal combustion engine vehicles at gas stations. But the oil price increase may lead to a melting up of some stocks.

There are arguments that can be made that smaller, more nimble producers, not burdened by the political spotlight and perhaps enjoying a better financial position from the last run-up in oil, are worth looking into. A Channelchek search returned over 200 companies that may fall into this category. This search result is available here.

{kind=link}