Petrodollar Dusk, Petroyuan Dawn: What Investors Need To Know

While most investors were trying to gauge the Federal Reserve’s next moves in light of recent bank failures last week, something interesting happened in Moscow.

During a three-day state visit, Chinese President Xi Jinping held friendly talks with Russian President Vladimir Putin in a show of unity, as both countries increasingly seek to position themselves as leaders of what they call a “multipolar world order,” one that challenges U.S.-centric alliances and agreements.

Among those agreements is the petrodollar, which has been in place for over 50 years.

In case you’re wondering, “petrodollars” are not a real currency. They’re simply dollars being used to trade oil. Early in the 1970s, the U.S. government provided economic aid to Saudi Arabia, its chief oil-producing rival, in exchange for assurances that Riyadh would price its crude exports exclusively in the U.S. dollar. In 1975, other members of the Organization of Petroleum Exporting Countries (OPEC) followed suit, and the petrodollar was born.

This had the immediate effect of strengthening the U.S. dollar. Since countries around the world had to have dollars on hand in order to buy oil (and other key commodities such as gold, also priced in dollars), the greenback became the world’s reserve currency, a status formerly enjoyed by the British pound, French franc and Dutch guilder.

All things must come to an end, however. We may be witnessing the end of the petrodollar as more and more countries, including China and Russia, are agreeing to make settlements in currencies other than the U.S. dollar. This could have wide-ranging implications on not just a macro scale but also investment portfolios.

This article was republished with permission from Frank Talk, a CEO Blog by Frank Holmes of U.S. Global Investors (GROW). Find more of Frank’s articles here – Originally published March 27, 2023

Dawn For The Petroyuan?

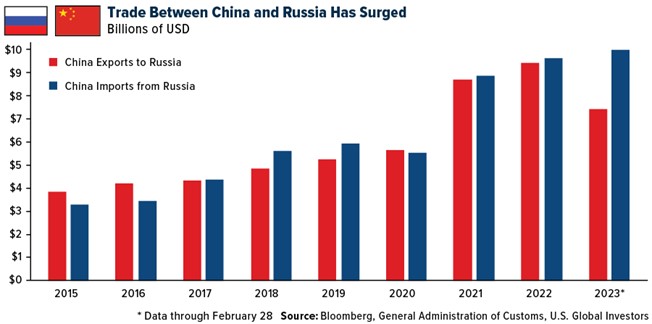

Putin couldn’t have been more explicit. During Xi’s state visit, he named the Chinese yuan as his favored currency to conduct trade in. Ever since Western sanctions were levied on the Eastern European country for its invasion of Ukraine early last year, Russia has increasingly depended on its southern neighbor to buy the oil other countries won’t touch.

In just the first two months of 2023, China’s imports from Russia totaled $9.3 billion, exceeding full-year 2022 imports in dollar terms. In February alone, China imported over 2 million barrels of Russian crude, a new record high.

Except that now, the yuan is presumably being used to make these settlements.

As Zoltar Pozsar, New York-based economist and investment research director at Credit Suisse, put it recently: “That’s dusk for the petrodollar… and dawn for the petroyuan.”

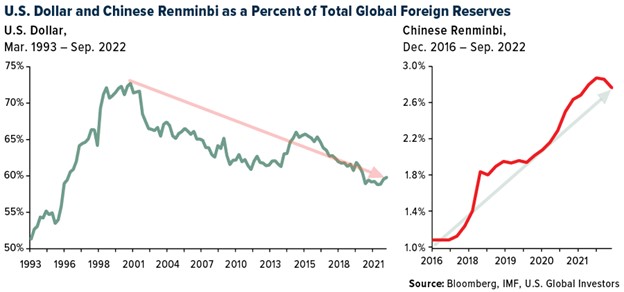

U.S. Dollar Still The World’s Reserve Currency, But Its Dominance Is Slipping

Before you dismiss Pozsar’s comment as an exaggeration, consider that other major OPEC nations and BRICS members (Brazil, Russia, India, China and South Africa) are either accepting yuan already or strongly considering it. Russia, Iran and Venezuela account for about 40% of the world’s proven oilfields, and the three sell their oil in exchange for yuan. Turkey, Argentina, Indonesia and heavyweight oil producer Saudi Arabia have all applied for admittance into BRICS, while Egypt became a new member this week.

What this suggests is that the yuan’s role as a reserve currency will continue to strengthen, signifying a broader shift in the global power balance and potentially giving China a bigger hand with which to shape economic policies that affect us all.

To be clear, the U.S. dollar remains the world’s top reserve currency for now, though its share of global central banks’ official holdings has slipped in the past 20 years, from 72% in 2001 to just under 60% today. By contrast, the yuan’s share of official holdings has more than doubled since 2016. The Chinese currency accounted for about 2.8% of reserves as of September 2022.

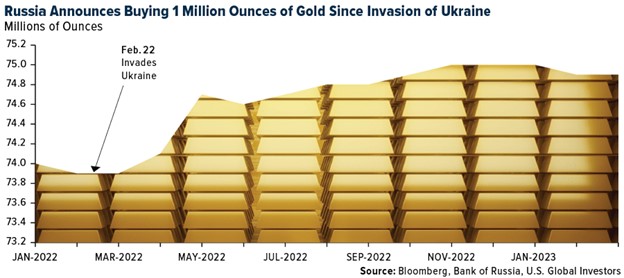

Russia Diversifying Away From The Dollar By Loading Up On Gold

It’s not all about the yuan, of course. Gold has also increased as a foreign reserve, especially among emerging economies that seek to diversify away from the dollar.

Last week, Russia announced that its bullion holdings jumped by approximately 1 million ounces over the past 12 months as its central bank loaded up on gold in the face of Western sanctions. The bank reported having nearly 75 million ounces at the end of February 2023, up from about 74 million a year earlier.

Long-Term Implications For Investors

The implications of the dollar potentially losing its status as the global reserve are numerous. Obviously, there may be currency risks, and a decrease in demand for U.S. Treasury bonds could result in rising interest rates. I would expect to see massive swings in commodity prices, especially oil prices, which could be an opportunity if you can stomach the volatility.

Gold would look exceptionally attractive, I think. A significant decrease in the relative value of the dollar would be supportive of the gold price, and I would be surprised not to see new highs. It’s for reasons like these that I always recommend a 10% weighting in gold, with 5% in physical bullion and the other 5% in high-quality gold mining equities. Be sure to rebalance at least on an annual basis.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The building wave of M&A deals in at least two of the mining sectors, is difficult to ignore. This week, lithium miner Albemarle (ALB) disclosed it had submitted a proposal to acquire Liontown Resources (LTR.Australia). Last month Newmont Mining’s proposed acquisition of Newcrest Mining, highlighted the rising interest in M&A in the gold sector. To date, both proposals have been shunned, but as companies look to increase production, inflation increases producers capital outlays, plus long permitting processes, a case could be made that growth by acquisition, friendly or not, is becoming more appealing in the sector.

Typically growing demand to buy smaller companies in a sector puts upward pressure on valuations.

The gold and lithium sectors have mostly lead over the past six months in terms of deal-making. For gold, the largest driver is these miners remain undervalued by historical levels. The trend for lithium producers in the years ahead, as battery production ramps up to meet surging demand for electric storage and green technology, is expected to continue to accelerate.

The Price of lithium, key to batteries found in most EVs, over the years has risen. This created a situation where car manufacturers themselves have realized that the best way to ensure a key ingredient to their product is to own all or part of a large enough producer. Lithium producers are looking for ways to increase yield and own more production facilities. These factors could unfold into a situation where the stock prices of companies producing either of these two metals, and even other mined minerals with growing demand, could outperform other sectors.

Five Reasons to Explore Small Mining Companies

While the real heat is on producers of minerals used to make batteries and gold miners, the below supply/demand concepts may apply to an increased need for other miners to involve themselves in M&A as well.

New List of Acquirers – The big car companies, energy companies, and other additional industrial consumers are in need of reliable supply.

Cheaper to Buy than Find – M&A is a solution to the increased costs of growing organically. It also helps circumvent what could be permitting delays and supply chain problems that prevent headway.

Scale – Gold companies normally try to extract synergies when seeking to size up, while lithium producers seek pure scale.

Big Picture Economics – The economic environment favors miners if inflation remains elevated; the companies’ production is more likely to sell for more. The cost of money, on an opportunity cost basis, especially net of inflation (real interest) favors mining.

Finding Value – Informed stock selection is key to discover and invest in companies best positioned to benefit from swelling M&A in the sector.

The fifth on this list is less of a reason to explore mining companies and more a common sense reminder. Last week the Channelchek Take Away Series brought to viewers a live in-depth presentation of 12 mining companies that were just coming off the huge PDAC mining conference in Canada. These presentations are being replayed and may be just the place to begin to hear from company executives, and a highly respected senior natural resources analyst. Audience questions and answers follow.

The information on these on-demand replay videos is current, and as you’ll see by clicking here, the list of video presentations includes a diversified mix of producers and explorers.

CALGARY, AB, March 21, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) is pleased to announce a 17% increase in our quarterly dividend, to US$0.14 per common share, our financial results for the year ended December 31, 2022, filing of our annual information form, an automatic share repurchase plan, and an operational update.

All references herein to $ refer to United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

President & CEO, Corey C. Ruttan commented:

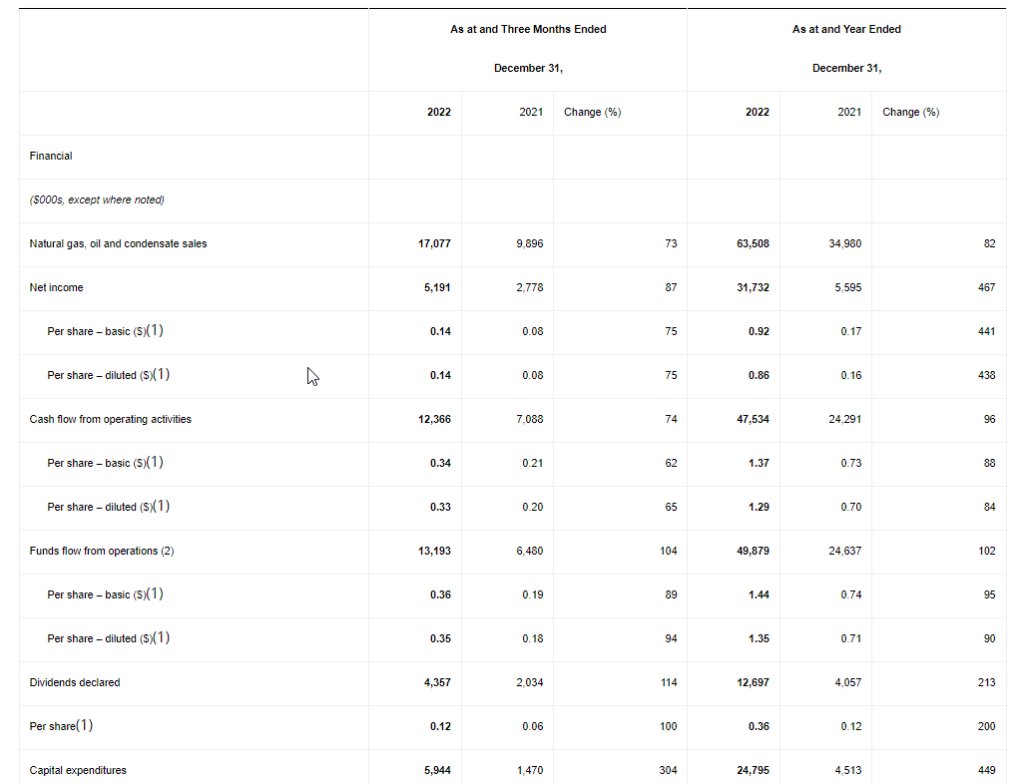

“We are very pleased with our 2022 results, from revenues of $63.5 million we generated $49.9 million of funds flow from operations and net income of $31.7 million, increases of 82%, 102% and 467% respectively, year over year. This represents industry leading operating netback margins underpinning our disciplined capital allocation model that balances organic growth and stakeholder returns. Since commencing production from our Caburé project in 2020, we have repaid all outstanding debt and today’s announcement represents the third increase in our quarterly dividend since Q1 2022. With this, we will have already returned $22 million ($0.62/share) to shareholders in the form of dividends. We are also firmly focused on our next phase of growth and are looking forward to an exciting 2023 capital program.”

Quarterly Dividend Increased 17% to $0.14 per Share

Alvopetro is pleased to announce that our Board of Directors has approved a 17% increase in our quarterly dividend, to $0.14 per common share, payable in cash on April 14, 2023, to shareholders of record on March 31, 2023. This dividend is designated as an “eligible dividend” for Canadian income tax purposes.

Dividend payments to non-residents of Canada will be subject to withholding taxes at the Canadian statutory rate of 25%. Shareholders may be entitled to a reduced withholding tax rate under a tax treaty between their country of residence and Canada. For further information, see Alvopetro’s website at https://alvopetro.com/Dividends-Non-resident-Shareholders.

Operational Update

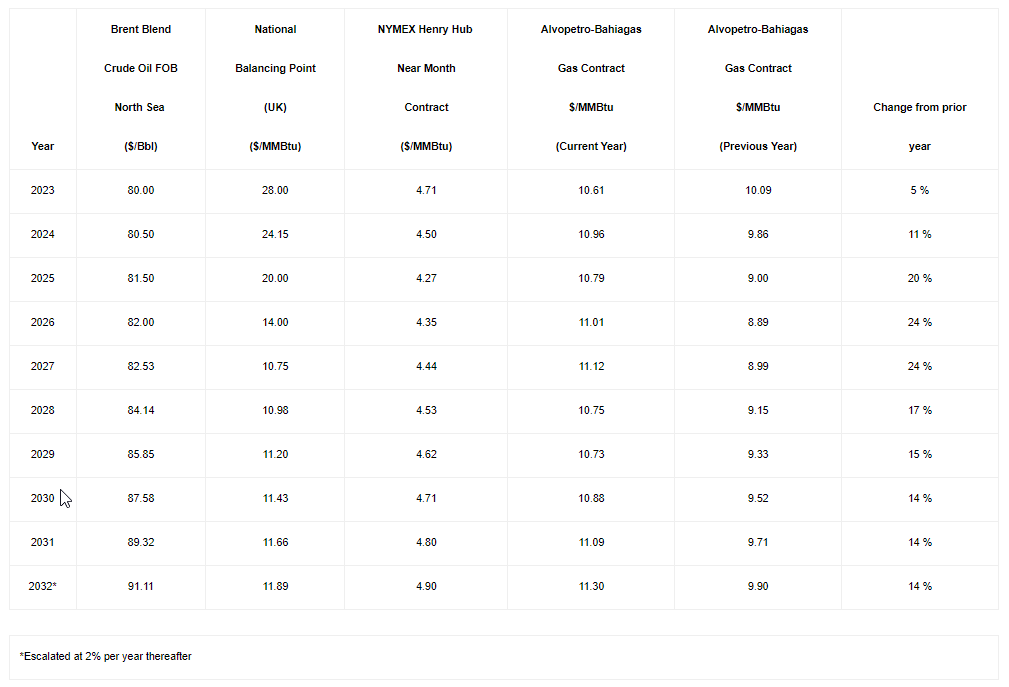

Our average daily sales have continued at strong rates in 2023, averaging 2,754 boepd in January and a new daily record of 2,866 boepd in February. Effective February 1, 2023, our natural gas price increased to BRL2.00/m3 and is effective for all natural gas sales from February 1 to July 31, 2023. Including recently approved and enhanced sales tax credits, our realized gas price, net of sales taxes, for the month of February was approximately $12.23/Mcf (based on our average heat content to date and the average February 2023 BRL/USD foreign exchange rate of 5.17).

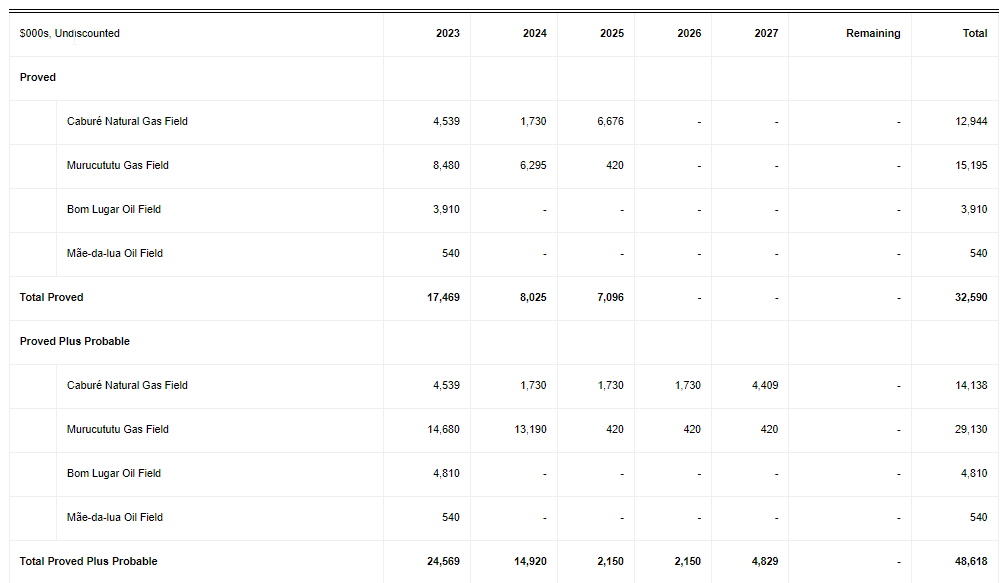

On February 6, 2023, we announced our 2023 capital program, focused on lower risk development opportunities on our Murucututu natural gas project and our Bom Lugar oil field. We have commenced stimulation operations at our 197(1) well on Murucututu. The 197(1) well location has already been tied in to our 183(1) facility and we expect to commence production from the well in the second quarter. Following this stimulation, we plan to drill two follow-up wells at Murucututu, with one well having additional uphole exploration potential. We have budgeted total capital expenditures of $16 million for our Murucututu project in 2023.

On our Bom Lugar field, we plan to drill up to two development wells in 2023, targeting the Caruaçu Formation with additional potential in the deeper Gomo and Agua Grande Formations, the first of which is planned for the second quarter. Total capital expenditures of up to $11 million are budgeted at Bom Lugar.

Additional capital spending budgeted for 2023 includes $3 million on our Caburé field for the expansion of unit facilities and drilling two additional wells, $0.5 million at our Mãe-da-lua field for stimulation of the existing well and $0.4 million in capital expenditures at our 182-C2 and 183-B2 wells.

Automatic Share Repurchase Plan

In January 2023, we received approval from the TSX Venture Exchange (“TSXV”) for a normal course issuer bid (the “NCIB”) as more particularly described in our news release dated January 3, 2023. The terms of the NCIB permit Alvopetro to repurchase up to 2,876,414 common shares from January 6, 2023 to the earlier of January 5, 2024 or when the NCIB is completed or terminated by Alvopetro. No repurchases have been made under the NCIB to date.

Alvopetro intends to enter into an automatic share purchase plan (“ASPP”) with our designated broker, subject to the approval of the TSXV. The ASPP is intended to allow for the purchase of common shares under the NCIB at times when the Corporation may not ordinarily be permitted to purchase common shares due to regulatory restrictions and customary self-imposed blackout periods.

The ASPP is to be implemented upon TSXV approval and would allow the designated broker to purchase common shares pursuant to the proposed ASPP until the expiry of the NCIB on January 5, 2024. Such purchases will be determined by the broker at its sole discretion based on the purchasing parameters set out by the Corporation in accordance with the rules of the TSXV, applicable securities laws and the terms of the ASPP. The ASPP will terminate on the earlier of the date on which: (i) the NCIB expires; (ii) the maximum number of common shares have been purchased under the ASPP; and (iii) the Corporation terminates the ASPP in accordance with its terms.

Outside of the ASPP and outside of pre-determined blackout periods, common shares may continue to be purchased under the NCIB based on management’s discretion, in compliance with the rules of the TSXV and applicable securities laws. All purchases made under the ASPP will be included in the number of common shares available for purchase under the NCIB.

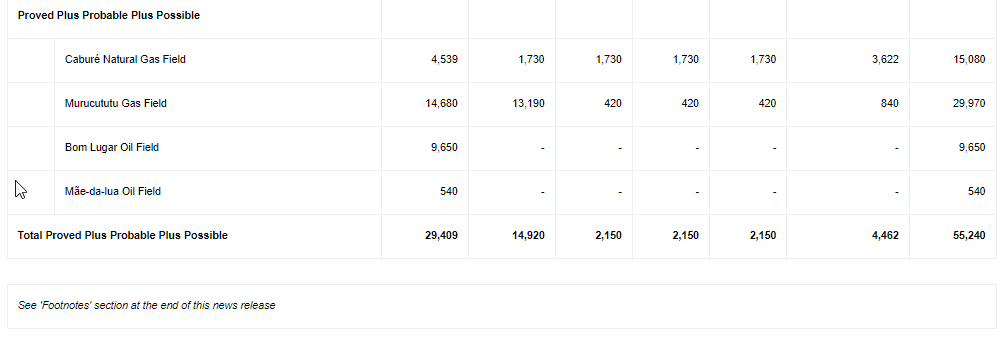

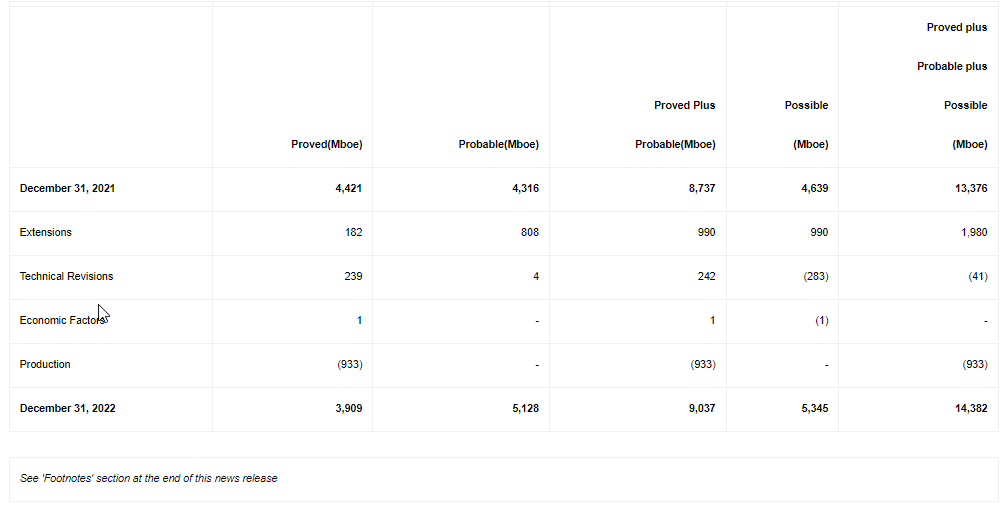

December 31, 2022 Reserves and Net Asset Value

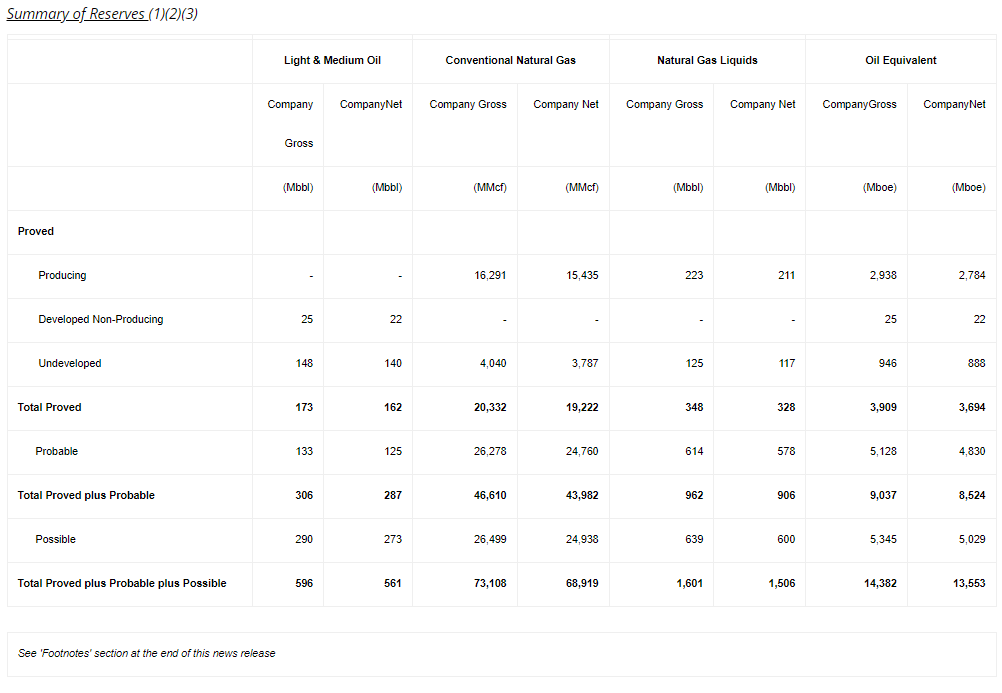

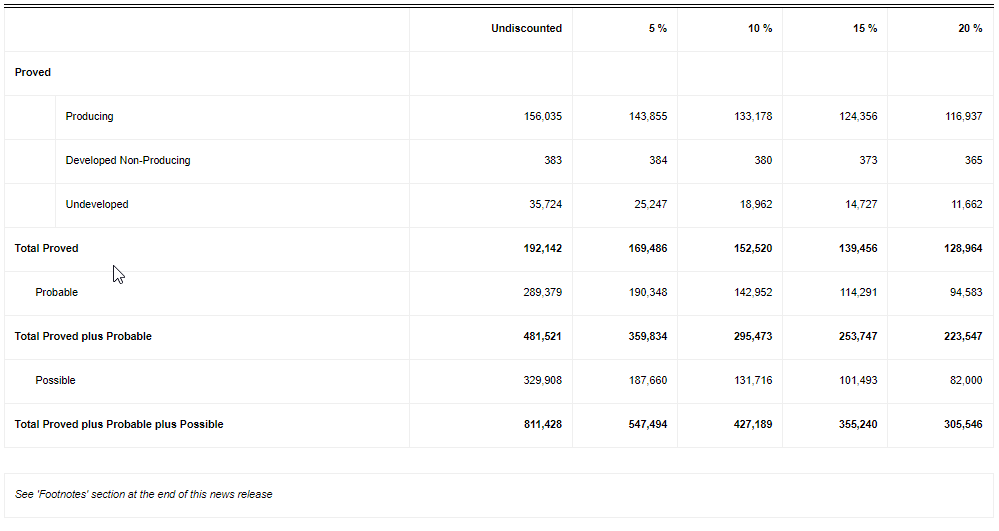

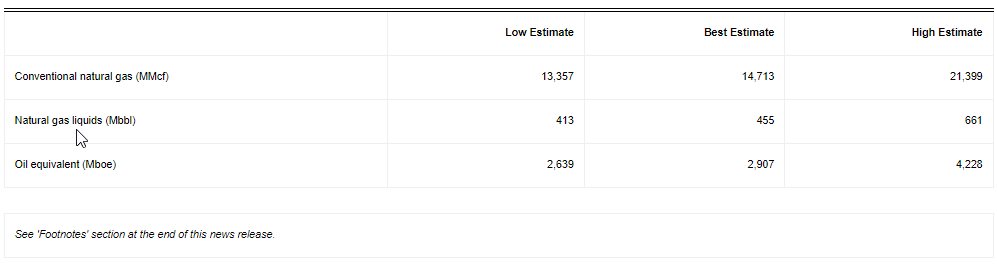

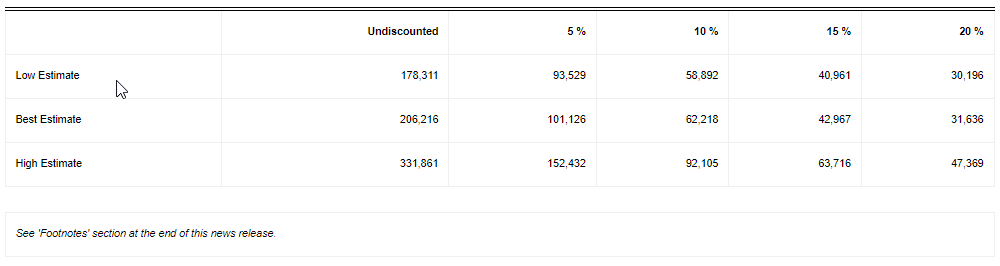

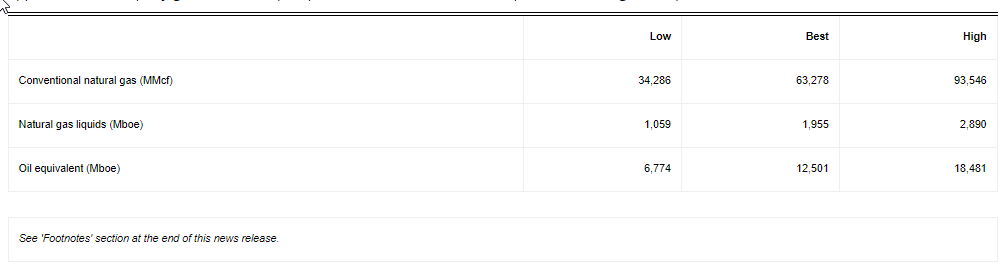

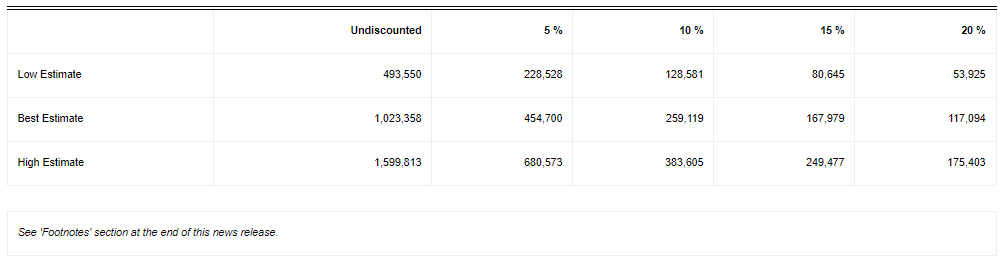

On February 28, 2023, Alvopetro announced its December 31, 2022 reserves based upon the independent reserve assessment and evaluation prepared by GLJ Ltd. (“GLJ”) dated February 27, 2023 with an effective date of December 31, 2022 (the “GLJ Reserves and Resources Report”).

Key highlights from the GLJ Reserves and Resources Report1:

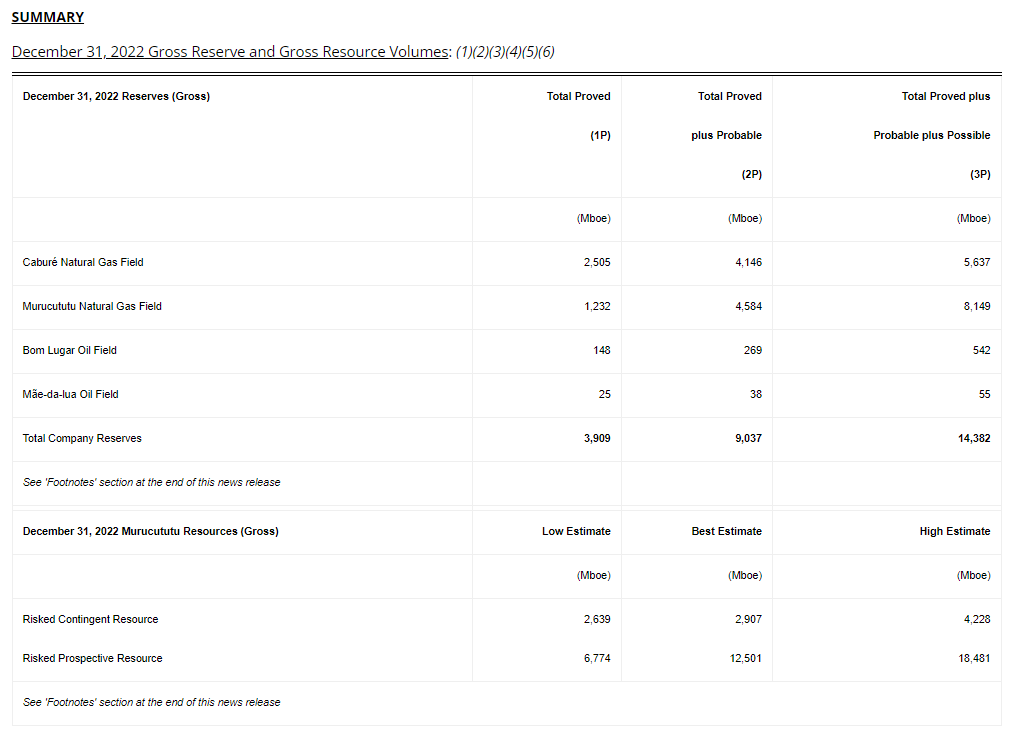

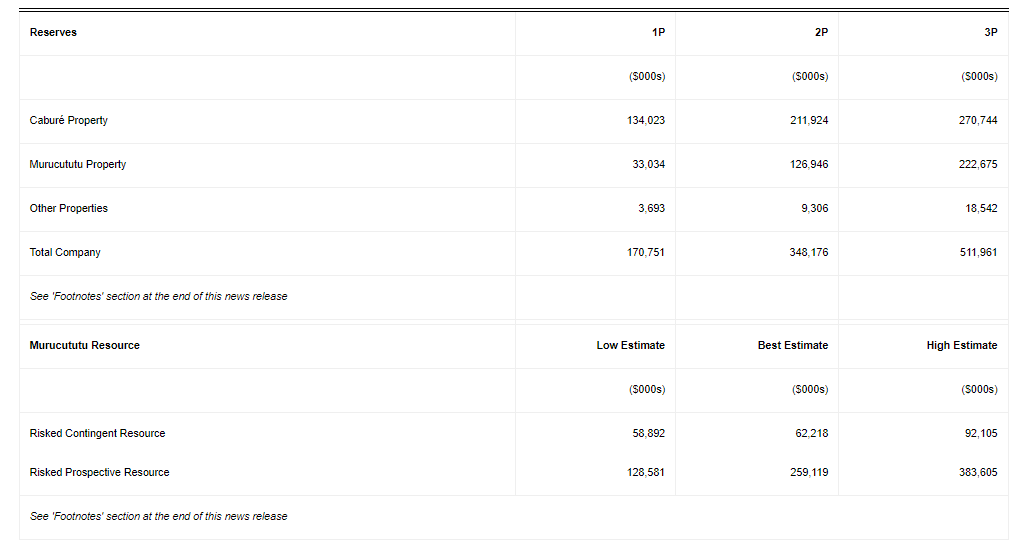

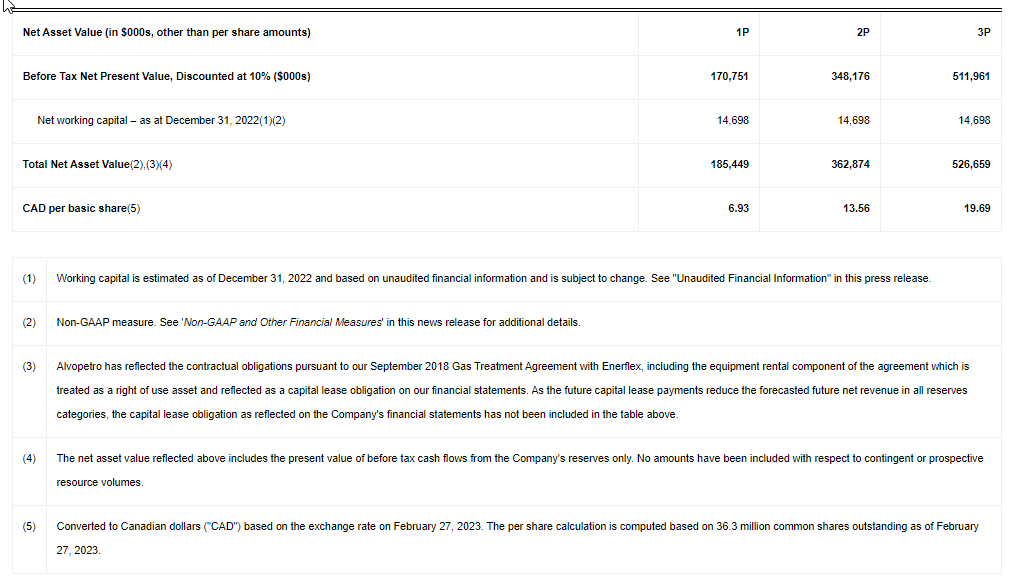

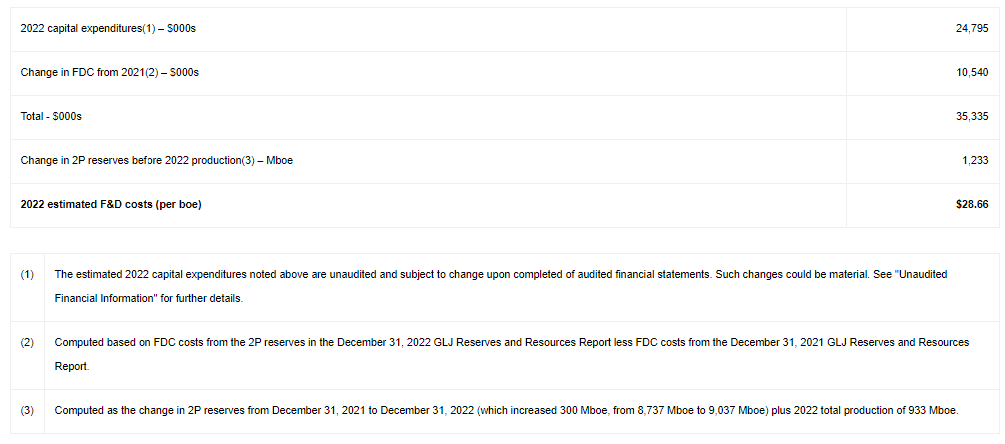

2P net present value before tax discounted at 10% (“NPV10”) increased 17% to $348.2 million.

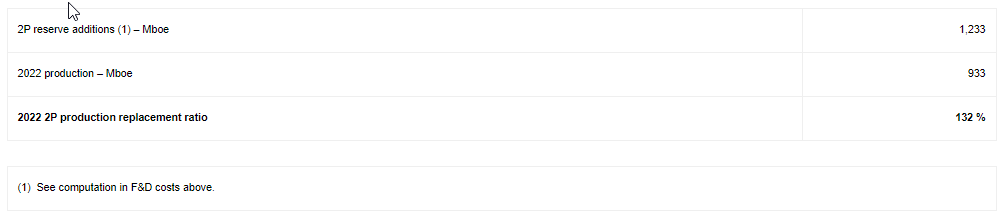

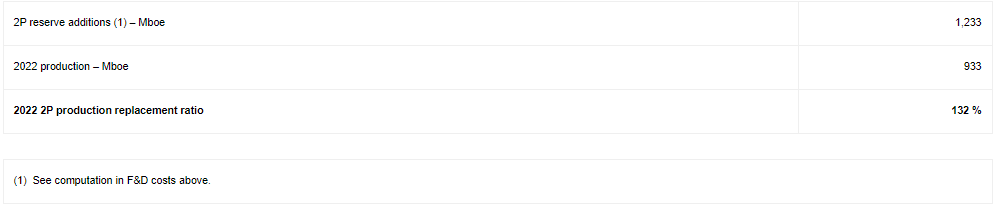

Proved reserves (“1P”) decreased 12% to 3.9 MMboe and 2P reserves increased 3% to 9.0 MMboe after 0.9 MMboe of production in 2022.

2P production replacement ratio of 132%.

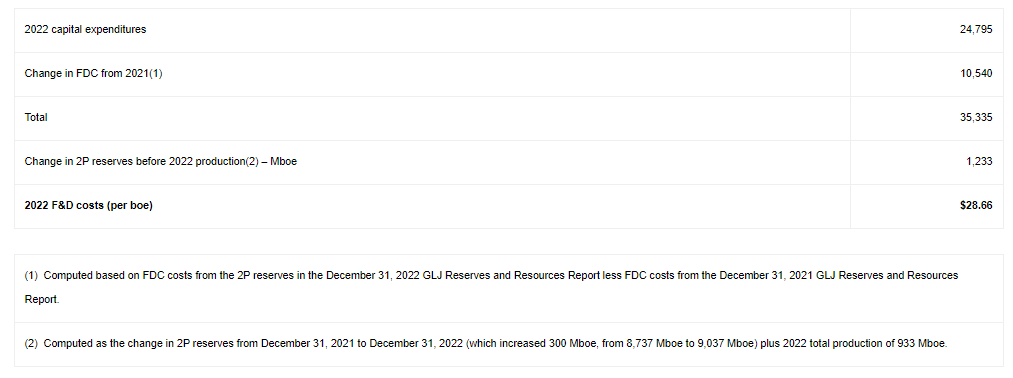

2P F&D costs of $28.66/boe.

2P recycle ratio of 2.1 times.

2P Net Asset Value of CAD$13.70/share ($9.99/share) before any potential from contingent or prospective resources.

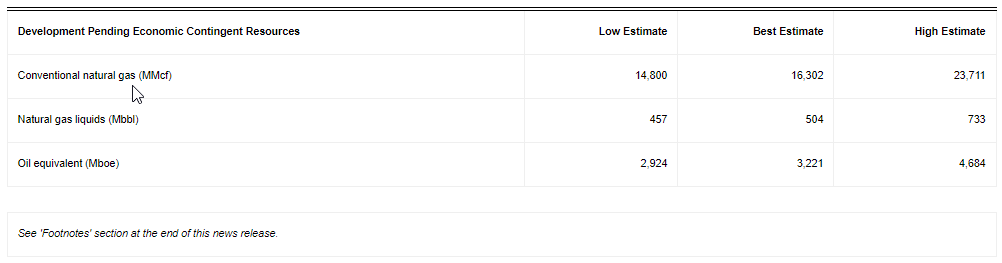

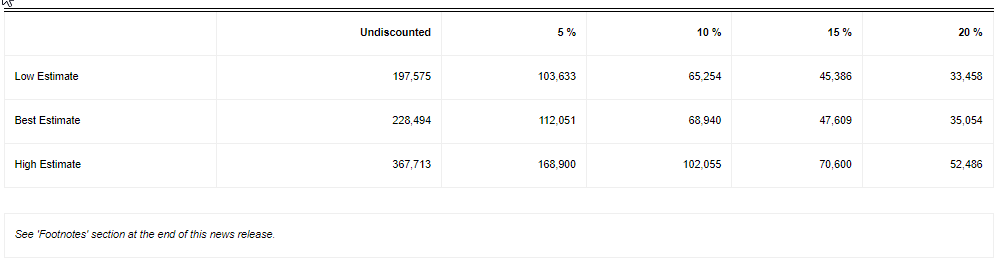

Risked best estimate contingent resource of 2.9 MMboe (NPV10 $62.2 million) and risked best estimate prospective resource of 12.5 MMboe (NPV10 $259.1 million).

1 Refer to the section entitled “Oil and Natural Gas Advisories” for additional disclosures regarding oil and natural gas reserves, contingent resources and prospective resources. In addition refer to “Oil and – Natural Gas Advisories – Other Metrics” and “Non-GAAP and Other Financial Measures” for additional disclosures and assumptions used in calculating production replacement ratio, F&D costs, recycle ratio, net asset value and net asset value per share.

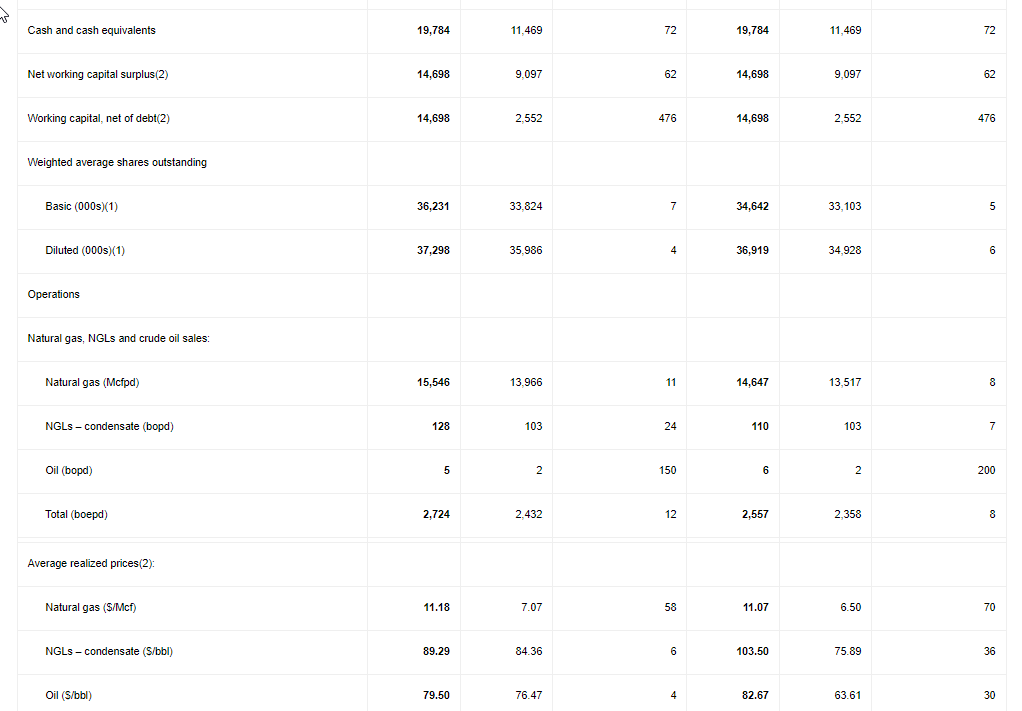

Financial and Operating Highlights – Fourth Quarter of 2022

Our average daily sales increased to a new quarterly record of 2,724 boepd (+3% from Q3 2022 and +12% from Q4 2021).

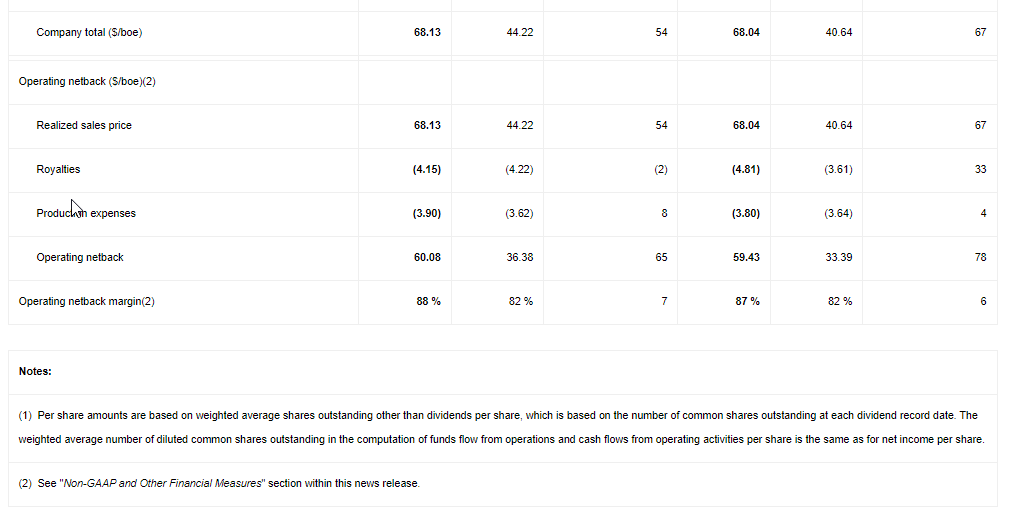

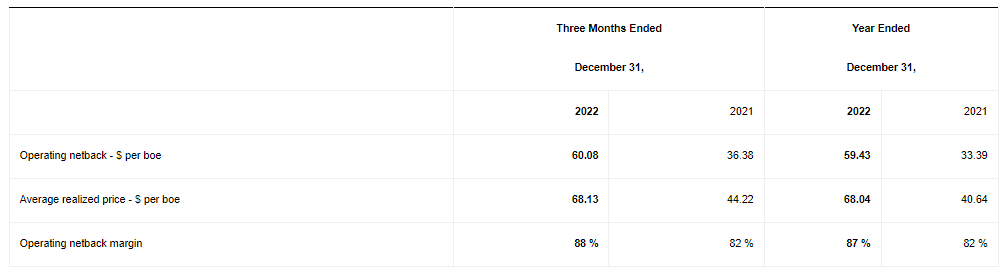

With natural gas sales in Q4 2022 continuing at the ceiling price in our contract, our average realized natural gas price was $11.18/Mcf (+58% from Q4 2021) and our average realized price per boe was $68.13 (+54% from Q4 2021). Higher realized prices and record daily sales volumes resulted in a 73% increase in our natural gas, condensate and oil revenue compared to Q4 2021.

Our operating netback was $60.08 per boe in Q4 2022, an improvement of $23.70 per boe from Q4 2021 (+65%) and $0.25 per boe from Q3 2022.

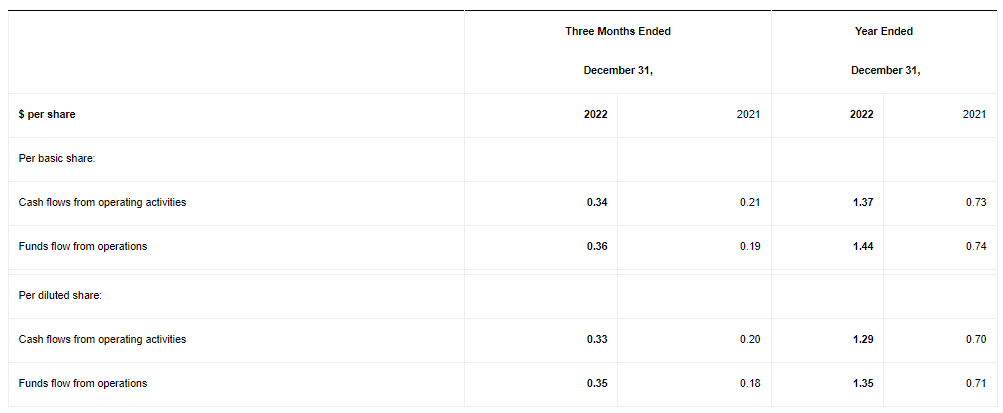

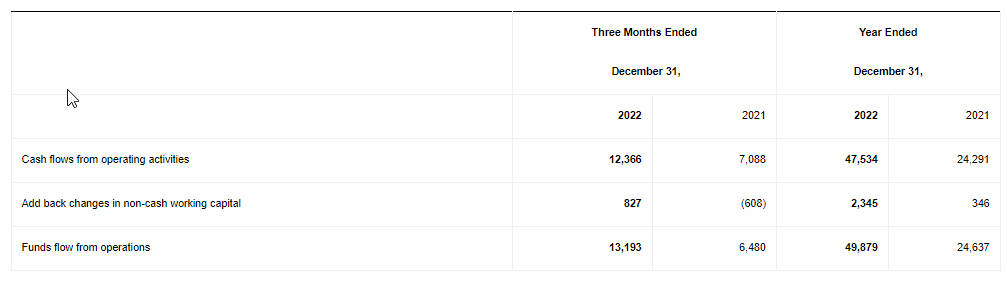

We generated funds flows from operations of $13.2 million ($0.36 per basic share and $0.35 per diluted share), an increase of $6.7 million compared to Q4 2021 and a decrease of $0.2 million compared to Q3 2022.

We reported net income of $5.2 million in Q4 2022, an increase of $2.4 million (+87%) compared to Q4 2021. Net income was impacted by impairment expense of $6.3 million recognized on exploration assets.

Capital expenditures totaled $5.9 million, including drilling and testing costs for our 182-C2 well, testing of the Unit-C well and facilities expenditures at the Caburé unit, testing costs for our 183-B1 well, development costs on our Murucututu project and long-lead purchases.

Our Q4 2022 dividend increased 50% to $0.12 per share. The Q4 2022 dividend was paid on January 13, 2023 to shareholders of record on December 30, 2022.

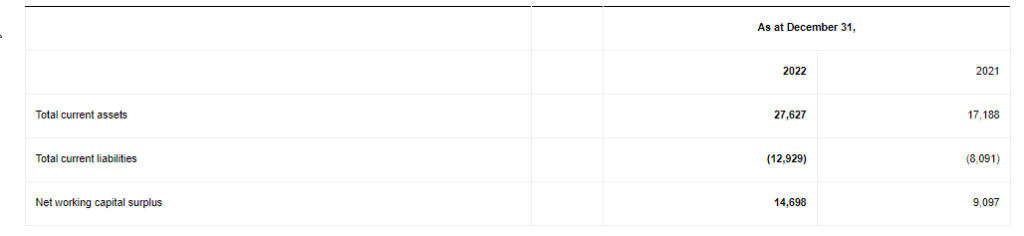

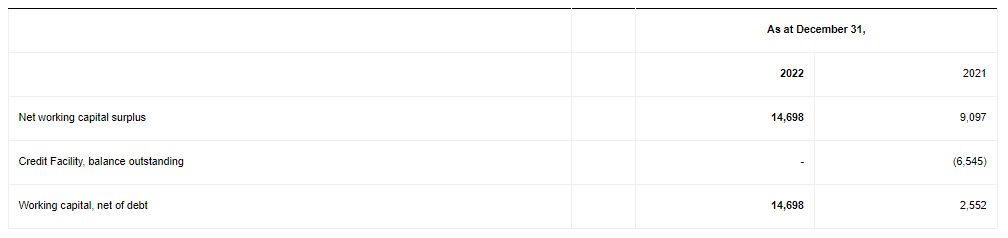

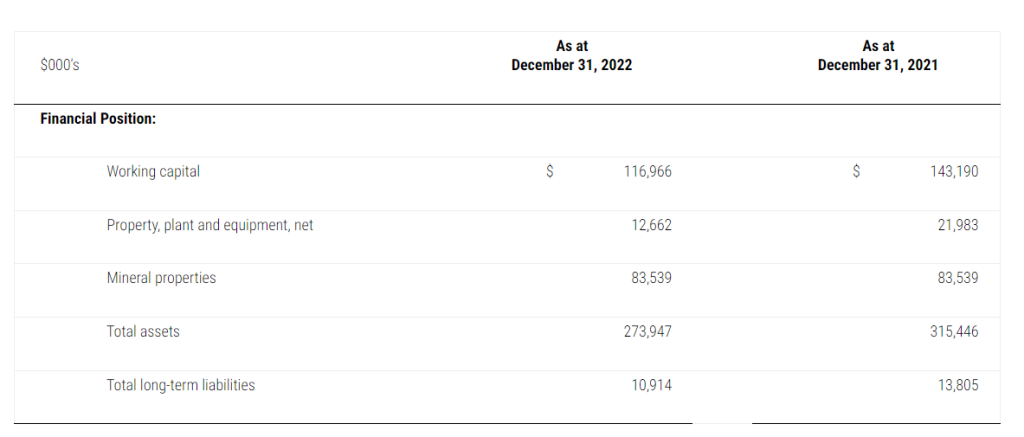

Our cash and working capital increased to $14.7 million, an improvement of $2.5 million compared to September 30, 2022 and an increase of $12.1 million compared to December 31, 2021 working capital net of debt of $2.6 million.

Financial and Operating Highlights – Year Ended December 31, 2022

Our annual sales averaged 2,557 boepd (95% natural gas, 4% NGLs from condensate and marginal crude oil production), an increase of 8% compared to 2021.

We reported net income of $31.7 million, compared to $5.6 million in 2021 (+467%).

We generated funds flow from operations of $49.9 million ($1.44 per basic share on $1.35 per diluted share) compared to $24.6 million in 2021 ($0.74 per basic share and $0.71 per diluted share).

Capital expenditures totaled $24.8 million in 2022.

In the third quarter of 2022, all outstanding warrants were exercised. Alvopetro received cash proceeds of $2.4 million and issued a total of 2,081,616 common shares on the exercise.

The credit facility was fully repaid in September 2022 and has been cancelled.

Dividends totaled $0.36 per share in 2022 compared to $0.12 per share in 2021 (+200%).

The following table provides a summary of Alvopetro’s financial and operating results for periods noted. The consolidated financial statements with the Management’s Discussion and Analysis (“MD&A”) are available on our website at www.alvopetro.com and will be available on the System for Electronic Document Analysis and Retrieval (SEDAR) website at www.sedar.com.

2022 Results Webcast

Alvopetro will host a live webcast to discuss 2022 financial results at 9:00 am Mountain time on Wednesday March 22, 2023. Details for joining the event are as follows:

The webcast will include a question and answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to socialmedia@alvopetro.com.

Annual Information Form

Alvopetro has filed its annual information form (“AIF”) with the Canadian securities regulators on SEDAR. The AIF includes the disclosure and reports relating to oil and gas reserves data and other oil and gas information required pursuant to National Instrument 51-101 of the Canadian Securities Administrators. The AIF may be accessed electronically at www.sedar.com.

Corporate Presentation

Alvopetro’s updated corporate presentation is available on our website at:

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Oil and Natural Gas Advisories

Oil and Natural Gas Reserves

The disclosure in this news release summarizes certain information contained in the GLJ Reserves and Resources Report but represents only a portion of the disclosure required under National Instrument 51-101 (“NI 51-101”). For additional details, see our news release dated February 28, 2023. Full disclosure with respect to the Company’s reserves as at December 31, 2022 is contained in the Company’s annual information form for the year ended December 31, 2022 which has been filed on SEDAR (www.sedar.com). All net present values in this press release are based on estimates of future operating and capital costs and GLJ’s forecast prices as of December 31, 2022. The reserves definitions used in this evaluation are the standards defined by the Canadian Oil and Gas Evaluation Handbook (COGEH) reserve definitions, are consistent with NI 51-101 and are used by GLJ. The net present values of future net revenue attributable to the Alvopetro’s reserves estimated by GLJ do not represent the fair market value of those reserves. Other assumptions and qualifications relating to costs, prices for future production and other matters are summarized herein. The recovery and reserve estimates of the Company’s reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual reserves may be greater than or less than the estimates provided herein. Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

Contingent Resources

This news release discloses estimates of Alvopetro’s contingent resources and the net present value associated with net revenues associated with the production of such contingent resources as included in the GLJ Reserves and Resources Report. There is no certainty that it will be commercially viable to produce any portion of such contingent resources and the estimated future net revenues do not necessarily represent the fair market value of such contingent resources. Estimates of contingent resources involve additional risks over estimates of reserves. For additional details with respect to Alvopetro’s contingent resources evaluated as at December 31, 2022, see our news release dated February 28, 2023 and additional details contained in the Company’s annual information form for the year ended December 31, 2022 which has been filed on SEDAR (www.sedar.com).

Prospective Resources

This news release discloses estimates of Alvopetro’s prospective resources included in the GLJ Reserves and Resources Report. There is no certainty that any portion of the prospective resources will be discovered and even if discovered, there is no certainty that it will be commercially viable to produce any portion. Estimates of prospective resources involve additional risks over estimates of reserves. The accuracy of any resources estimate is a function of the quality and quantity of available data and of engineering interpretation and judgment. While resources presented herein are considered reasonable, the estimates should be accepted with the understanding that reservoir performance subsequent to the date of the estimate may justify revision, either upward or downward. For additional details with respect to Alvopetro’s prospective resources evaluated as at December 31, 2022, see our news release dated February 28, 2023 and additional details contained in the Company’s annual information form for the year ended December 31, 2022 which has been filed on SEDAR (www.sedar.com).

Other Metrics

This press release contains metrics commonly used in the oil and natural gas industry, which have been prepared by management, including “F&D costs”, “net asset value”, “net asset value per share”, “production replacement ratio” and “recycle ratio”. These terms do not have a standardized meaning and may not be comparable to similar measures presented by other companies, and therefore should not be used to make such comparisons.

“F&D costs” are reflected on a per barrel of oil equivalent and are calculated as the sum of capital expenditures in the current year plus the change in FDC for the period, divided by the change in reserves in the period, before current year production. The 2022 F&D costs are computed as follows:

“Net asset value” is based on the before tax net present value of the Company’s reserves as at December 31, 2022, discounted at 10% plus the Company’s net working capital balance as of December 31, 2022. Net working capital is a capital management measure. See “Non-GAAP and Other Financial Measures” below for further details.

“Net asset value per share” is based on the computation of net asset value divided by basic shares outstanding of 36,311,579 adjusted to Canadian dollars based on the foreign exchange rate on March 21, 2023.

“Production replacement ratio” is calculated as total reserve additions divided by current year production. Alvopetro’s 2P production replacement ratio in 2022 is calculated as:

“Recycle ratio” is calculated by dividing the 2022 operating netback by F&D costs per boe for the year. The Company’s 2022 recycle ratio is calculated as follows:

Management uses these oil and gas metrics for its own performance measurements and to provide shareholders with measures to compare our operations over time. Readers are cautioned that the information provided by these metrics, or that can be derived from the metrics presented in this press release, should not be relied upon for investment or other purposes.

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this report should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s MD&A which may be accessed through the SEDAR website at www.sedar.com.

Non-GAAP Financial Measures

Operating netback

Operating netback is calculated as natural gas, oil and condensate revenues less royalties and production expenses. This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations.

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback divided by total sales volumes (barrels of oil equivalent). This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe).

Operating netback margin

Operating netback margin is calculated as operating netback per boe divided by the realized sales price per boe. Operating netback margin is a measure of the profitability per boe relative to natural gas, oil and condensate sales revenues per boe and is calculated as follows:

Funds Flow from Operations Per Share

Funds flow from operations per share is a non-GAAP ratio that includes all cash generated from operating activities and is calculated before changes in non-cash working capital, divided by the weighted the weighted average shares outstanding for the respective period. For the periods reported in this news release the cash flows from operating activities per share and funds flow from operations per share is as follows:

Capital Management Measures

Funds Flow from Operations

Funds flow from operations is a non-GAAP capital management measure that includes all cash generated from operating activities and is calculated before changes in non-cash working capital. The most comparable GAAP measure to funds flow from operations is cash flows from operating activities. Management considers funds flow from operations important as it helps evaluate financial performance and demonstrates the Company’s ability to generate sufficient cash to fund future growth opportunities. Funds flow from operations should not be considered an alternative to, or more meaningful than, cash flows from operating activities however management finds that the impact of working capital items on the cash flows reduces the comparability of the metric from period to period. A reconciliation of funds flow from operations to cash flows from operating activities is as follows:

Net Working Capital

Net working capital is computed as current assets less current liabilities. Net working capital is a measure of liquidity, is used to evaluate financial resources, and is calculated as follows:

Working Capital Net of Debt

Working capital net of debt is computed as net working capital surplus decreased by the carrying amount of the Credit Facility. Working capital net of debt is used by management to assess the Company’s overall financial position.

Supplementary Financial Measures

“Average realized natural gas price – $/Mcf” is comprised of natural gas sales as determined in accordance with IFRS, divided by the Company’s natural gas sales volumes.

“Average realized NGL – condensate price – $/bbl” is comprised of condensate sales as determined in accordance with IFRS, divided by the Company’s NGL sales volumes from condensate.

“Average realized oil price – $/bbl” is comprised of oil sales as determined in accordance with IFRS, divided by the Company’s oil sales volumes.

“Average realized price – $/boe” is comprised of natural gas, condensate and oil sales as determined in accordance with IFRS, divided by the Company’s total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Production expenses per boe” is comprised of production expenses, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

BOE Disclosure

The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6 Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Forward-Looking Statements and Cautionary Language

This news release contains forward-looking information within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward–looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking statements concerning plans relating to the Company’s operational activities, proposed exploration development activities and the timing for such activities, exploration and development prospects of Alvopetro, capital spending levels, future capital and operating costs, timing and taxation of dividends and plans for dividends in the future, plans for share repurchases under the NCIB and the duration of the NCIB, future production and sales volumes, the expected natural gas price, gas sales and gas deliveries under Alvopetro’s long-term gas sales agreement, the expected timing of production commencement from the 197(1) well, the proposed automatic share purchase plan, and projected financial results. Forward-looking statements are necessarily based upon assumptions and judgments with respect to the future including, but not limited to, expectations and assumptions concerning the timing of regulatory licenses and approvals, equipment availability, the success of future drilling, completion, testing, recompletion and development activities and the timing of such activities, the performance of producing wells and reservoirs, well development and operating performance, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, the outlook for commodity markets and ability to access capital markets, foreign exchange rates, general economic and business conditions, forecasted demand for oil and natural gas, the impact of the COVID-19 pandemic, weather and access to drilling locations, the availability and cost of labour and services, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. In addition, the declaration, timing, amount and payment of future dividends remain at the discretion of the Board of Directors. Although we believe that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because we can give no assurance that they will prove to be correct. Since forward looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actual results could differ materially from those currently anticipated due to a number of factors and risks. These include, but are not limited to, risks associated with the oil and gas industry in general (e.g., operational risks in development, exploration and production; delays or changes in plans with respect to exploration or development projects or capital expenditures; the uncertainty of reserve estimates; the uncertainty of estimates and projections relating to production, costs and expenses, reliance on industry partners, availability of equipment and personnel, uncertainty surrounding timing for drilling and completion activities resulting from weather and other factors, changes in applicable regulatory regimes and health, safety and environmental risks), commodity price and foreign exchange rate fluctuations, market uncertainty associated with financial institution instability, and general economic conditions. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Three Reasons the Willow Arctic Oil Drilling Project Was Approved

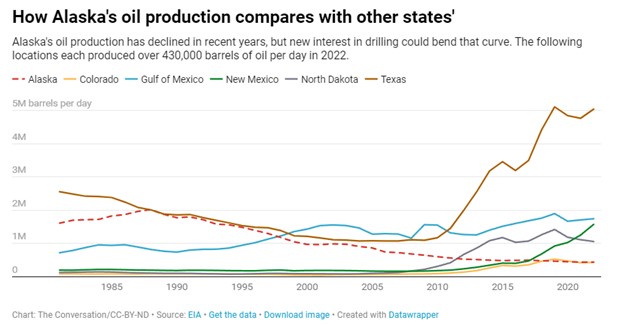

For more than six decades, Alaska’s North Slope has been a focus of intense controversy over oil development and wilderness protection, with no end in sight. Willow field, a 600-million-barrel, US$8 billion oil project recently approved by the Biden administration – to the outrage of environmental and climate activists – is the latest chapter in that long saga.

To understand why President Joe Biden allowed the project, despite vowing “no more drilling on federal lands, period” during his campaign for president, some historical background is necessary, along with a closer look at the ways domestic and international fears are complicating any decision for or against future oil development on the North Slope.

More Than Just Willow

The Willow project lies within a vast, 23 million-acre area known as the National Petroleum Reserve-Alaska, or NPR-A. This was one of four such reserves set aside in the early 1900s to guarantee a supply of oil for the U.S. military. Though no production existed at the time in NPR-A, geologic information and surface seeps of oil suggested large resources across the North Slope.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Scott L. Montgomery, Lecturer, Jackson School of International Studies, University of Washington.

Proof came with the 1968 discovery of the supergiant Prudhoe Bay field, which began producing oil in 1977. Exploratory programs in the NPR-A, however, found only small oil accumulations worthy of local uses.

Then, in the 2000s, new geologic understanding and advanced exploration technology led companies to lease portions of the reserve, and they soon made large fossil fuel discoveries. Because NPR-A is federal land, government approval is required for any development. To date, most have been approved. Willow is the latest.

Caribou in the National Petroleum Reserve-Alaska are important for Native groups. However, Native communities have also been split over support for drilling, which can bring income. Bob Wick/Bureau of Land Management

Caribou in the National Petroleum Reserve-Alaska are important for Native groups. However, Native communities have also been split over support for drilling, which can bring income. Bob Wick/Bureau of Land Management

Opposition to North Slope drilling from conservationists, environmental organizations and some Native communities, mainly in support of wilderness preservation, has been fierce since the opening of Prudhoe Bay and the construction of the Trans-Alaska Pipeline in the 1970s. In the wake of 1970s oil crises, opponents failed to stop development.

During the next four decades, controversy shifted east to the Arctic National Wildlife Refuge. Republican presidents and congressional leaders repeatedly attempted to open the refuge to drilling but were consistently stifled – until 2017. That year, the Trump administration opened it to leasing. Ironically, no companies were interested. Oil prices had fallen, risk was high and the reputational cost was large.

To the west of the refuge, however, a series of new discoveries in NPR-A and adjacent state lands were drawing attention as a major new oil play with multibillion-barrel potential. Oil prices had risen, and though they fell again in 2020, they have been mostly above $70 per barrel – high enough to encourage significant new development.

ConocoPhillips’ Willow project is in the northeast corner of the National Petroleum Reserve-Alaska. USGS, Department of Interior

Opposition, with Little Success

Opposition to the new Willow project has been driven by concerns about the effects of drilling on wildlife and of increasing fossil fuel use on the climate. Willow’s oil is estimated to be capable of releasing 287 million metric tons of carbon dioxide if refined into fuels and consumed.

In particular, opponents have focused on a planned pipeline that will extend the existing infrastructure further westward, deeper into NPR-A, and likely encourage further exploratory drilling.

So far, that resistance has had little success.

Twenty miles to the south of Willow is the Peregrine discovery area, estimated to hold around 1.6 billion barrels of oil. Its development was approved by the Biden administration in late 2022. To the east lies the Pikka-Horseshoe discovery area, with around 2 billion barrels. It’s also likely to gain approval. Still other NPR-A drilling has occurred to the southwest (Harpoon prospect), northeast (Cassin), and southeast (Stirrup).

One reason the Biden administration approved the Willow project involves legality: ConocoPhillips holds the leases and has a legal right to drill. Canceling its leases would bring a court case that, if lost, would set a precedent, cost the government millions of dollars in fees and do nothing to stop oil drilling.

Instead, the government made a deal with ConocoPhillips that shrank the total surface area to be developed at Willow by 60%, including removing a sensitive wildlife area known as Teshekpuk Lake. The Biden administration also announced that it was putting 13 million acres of the NPR-A and all federal waters of the Arctic Ocean off limits to new leases.

That has done little to stem anger over approval of the project, however. Two groups have already sued over the approval.

Taking Future Risks into Account

To further understand Biden’s approval of the Willow project, one has to look into the future, too.

Discoveries in the northeastern NPR-A suggest this will become a major new oil production area for the U.S. While actual oil production is not expected there for several years, its timing will coincide with a forecast plateau or decline in total U.S. production later this decade, because of what one shale company CEO described as the end of shale oil’s aggressive growth.

Historically, declines in domestic supply have brought higher fuel prices and imports. High gasoline and diesel prices, with their inflationary impacts, can weaken the political party in power. While current prices and inflation haven’t damaged Biden and the Democrats too much, nothing guarantees this will remain the case.

Geopolitical Concerns, Particularly Europe

The Biden administration also faces geopolitical pressure right now due to Russia’s war on Ukraine.

U.S. companies ramped up exports of oil and natural gas over the past year to become a lifeline for Europe as the European Union uses sanctions and bans on Russian fossil fuel imports to try to weaken the Kremlin’s ability to finance its war on Ukraine. U.S. imports have been able to replace a major portion of Russian supply that Europe once counted on.

Europe’s energy crisis has also led to the return of energy security as a top concern of national leaders worldwide. Without a doubt, the crisis has clarified that oil and gas are still critical to the global economy. The Biden administration is taking the position that reducing the supply by a significant amount – necessary as it is to avoid damaging climate change – cannot be done by prohibition alone. Halting new drilling worldwide would drive fuel prices sky high, weakening economies and the ability to deal with the climate problem.

Energy transitions depend on changes in demand, not just supply. As an energy scholar, I believe advancing the affordability of electric vehicles and the infrastructure they need would do much more for reducing oil use than drilling bans. Though it may seem counterintuitive, by aiding European economic stability, U.S. exports of fossil fuels may also help the EU plan to accelerate noncarbon energy use in the years ahead.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results demonstrate strong growth, generally meeting expectations. Annual production volumes came in at the lower end of guidance but 58% above last year. Higher production levels in the area may be beginning to show signs of affecting takeaway capacity (see third party curtailment and widening basis discount differentials). Weak summer natural gas prices bounced back nicely in the fourth quarter.

Drilling is accelerating and creating higher producing wells. The company drilled 17.5 net wells in 2022 surpassing our 15 well estimate. Management reports that initial production rates for recent wells were “significantly above internal expectations”. InPlay has been shifting towards longer horizontal laterals and spending more on infrastructure. Production increases seem to justify the higher costs. Management believes the steps it is taking will offset recent curtailments and reiterated 2023 production guidance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURE™ and VPURE+™ products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Sales and realized prices were down. Production volumes (preannounced) fell 31% q-t-q due to maintenance and rain. Realized vanadium prices fell 12% with Largo prices falling below benchmark prices due to a drop in ferrovanadium prices and timing factors associated with contract deliveries.

Costs were up. Operating costs continued to rise in the fourth quarter. The change in cost per unit produced was especially noteworthy as production levels dropped. Management has put a priority on controlling operating costs and expects costs in future quarters to decline. Non-operating cost remain high, although they have eased since the third quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

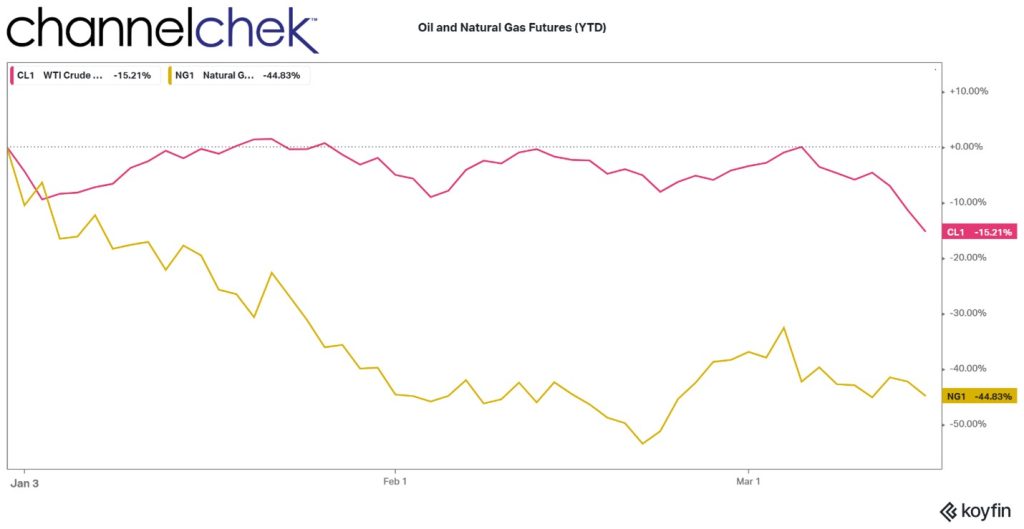

Which Way is Oil Going, and What it Could Mean for Investors in Related Sectors

Whether the sudden and severe decline in oil prices is an opportunity to invest in sectors that will benefit from cheaper fuel, a sign of further problems in the economy, or transitory, remains to be seen. It may depend on two overriding factors – and there are strong arguments supporting each. Below we look at the different scenarios and the sectors that are impacted.

Background

Energy futures and oil-related stocks like Chevron (CVX) and Exxon (XOM) gapped down at the open two days this week as concern about the overall health of the financial sector as two banks were closed and a major rating agency downgraded the banking sector Since Friday. U.S. oil futures remained below $70 per barrel midweek, as prices of WTI have now dipped 13% to levels not seen since December 2021.

These downward price moves are a reaction to thinking that demand will wane in a slowing U.S. economy. Also that it may take longer for the Chinese economy to rise to expected levels. Although far less impactful, approval of the Willow oil drilling project by the White House demonstrates a reversal of the ‘no more drilling’ policy by this administration.

A report by the International Energy Agency (IEA) this morning suggests the price decline may be temporary. The IEA anticipates that the oil markets will switch from a supply overhang in the first half of 2023 to a deficit later in the year. This is expected as OPEC continues its plan to cut production, and that the increased air traffic, along with an economic rebound in China will push global oil demand to a record high, according to the IEA.

Image: President Joe Biden meets with staff in the Oval Office, Monday, January 23, 2023, to discuss the Willow oil project. (Official White House Photo by Cameron Smith)

Oil remains one of the most crucial commodities to the modern world. Its price has a significant impact on various industries and investment sectors. Below are the sectors that stand to benefit if the recent decline in prices remains intact or declines further:

Transportation Industry is a significant beneficiary of lower oil prices. The reason of course is because fuel costs are a significant expense for airlines, trucking, and shipping companies. When the cost of fuel follows the decline, the transportation industry enjoys a reduction in operating costs. This can result in wider margins on tickets sold for air travel, lower shipping costs for businesses including retailers, and lower prices for cruise lines.

The Chemical Industry is another sector that benefits from declining oil prices. Many chemicals are derived from crude oil, and a decrease in oil prices means a decrease in the cost of raw materials. This, in turn, can lead to lower prices for chemical products such as fertilizers, plastics, and other materials.

The Consumer Goods Industry is also a significant beneficiary of declining oil prices. This is because many consumer goods are made from oil-based materials such as plastics, rubber, and synthetic fabrics. When oil prices decline, the cost of these materials decreases, resulting in lower production costs and, ultimately, lower prices for consumers.

The Renewable Energy Industry is not directly related to oil prices, a decline in oil prices can benefit this sector indirectly. Renewable energy sources such as wind and solar power are becoming increasingly competitive with traditional fossil fuels, and a decrease in the price of oil can make it more challenging for the fossil fuel industry to compete. This can result in increased investment in renewable energy and a shift toward cleaner, more sustainable sources of energy.

Emerging Markets, particularly those that are oil-importing countries, can benefit significantly from declining oil prices. These countries rely heavily on imported oil, and a decrease in oil prices can result in significant cost savings for these countries. This can lead to increased economic growth, as businesses have more money to invest in other areas and consumers have more disposable income to spend.

Take Away

Oil has dropped considerably this year. This is in part because economic activity is expected to become lower, and problems in the banking sector. This may not last through the year as indicated by the IEA. Others believe this is the start of further declines. Should oil prices not track higher, stock market investors could look at the transportation, chemical, and consumer goods industries, as well as the renewable energy sector and emerging markets. As with any economic change, it is essential to carefully analyze the potential effects on different industries and sectors to make informed investment decisions.

All dollar amounts expressed are in thousands of U.S. dollars unless otherwise indicated.

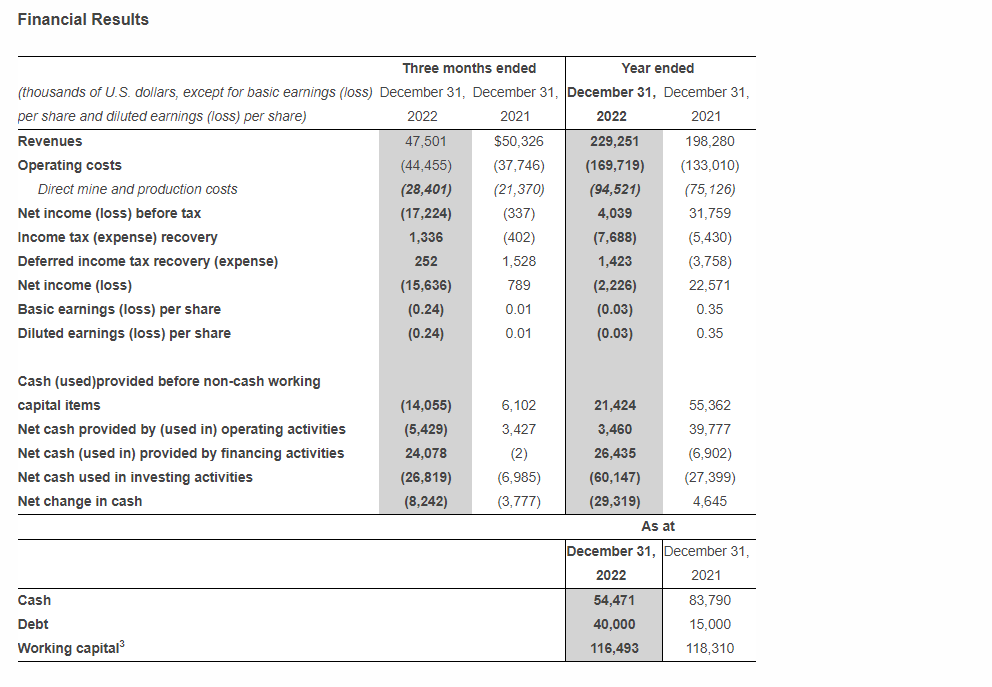

Q4 & Full Year 2022 Highlights

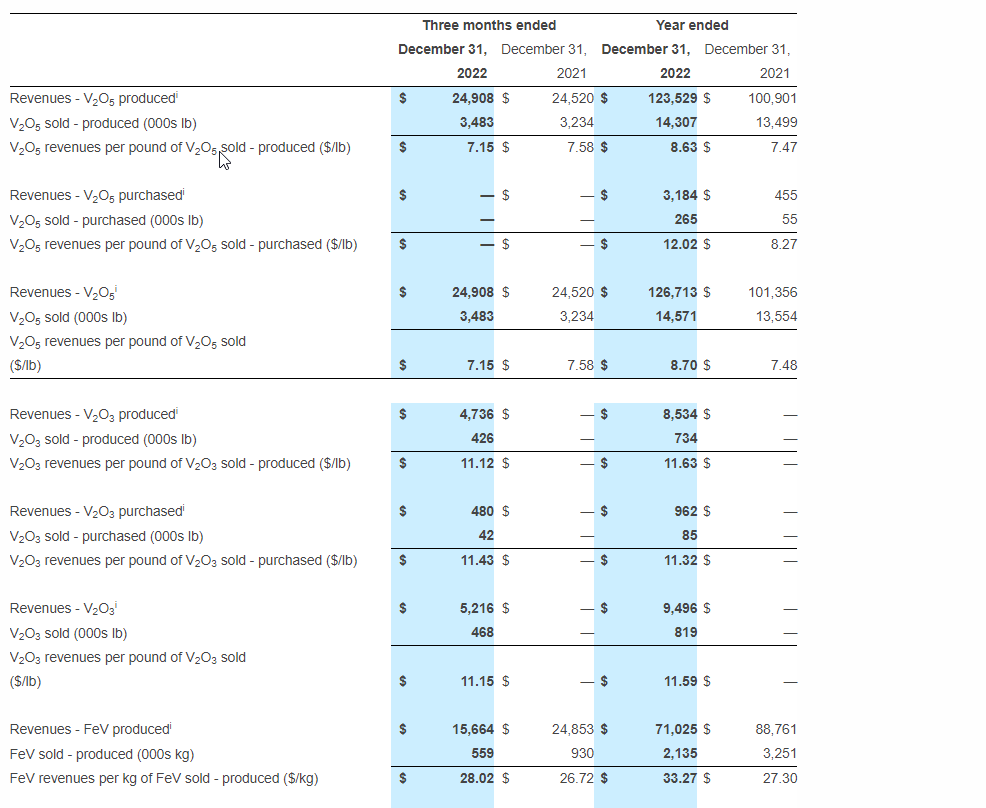

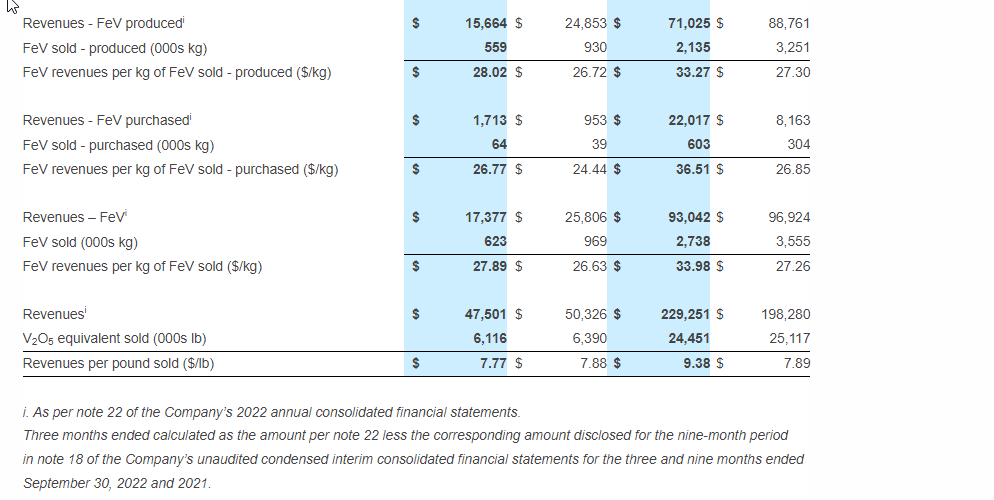

Revenues of $47.5 million in Q4 2022, 6% below Q4 2021; Revenues per pound sold1 of $7.77 in Q4 2022, largely in line with $7.88 recognized in Q4 2021

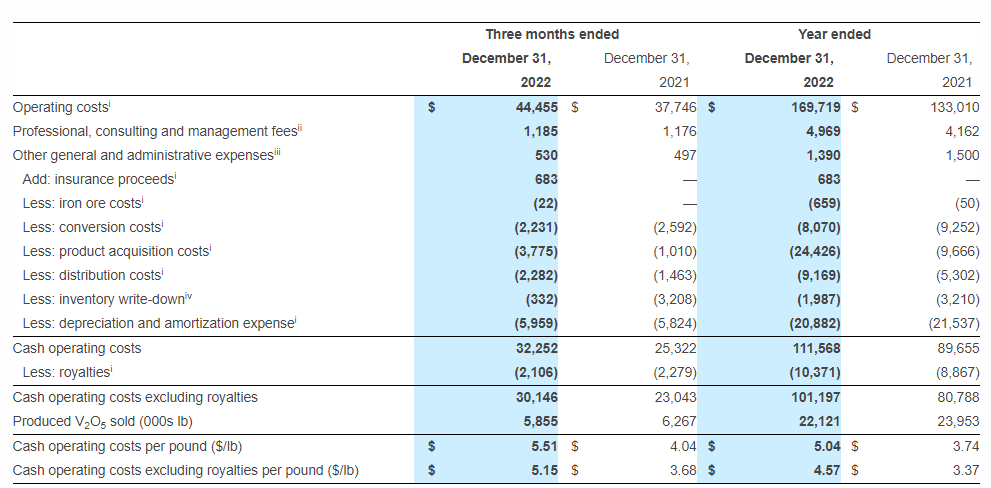

Operating costs of $44.5 million in Q4 2022 vs. $37.7 million in Q4 2021, and cash operating costs excluding royalties per pound1 of V2O5 equivalent sold of $5.15 in Q4 2022 vs. $3.68 in Q4 2021

Net loss of $15.6 million in Q4 2022 vs. net income of $1.0 million in Q4 2021; Basic loss per share of $0.24 in Q4 2022 vs. basic earnings per share of $0.01 in Q4 2021

In Q4 2022, the Company’s net loss included approximately $6.3 million of non-recurring expenditures

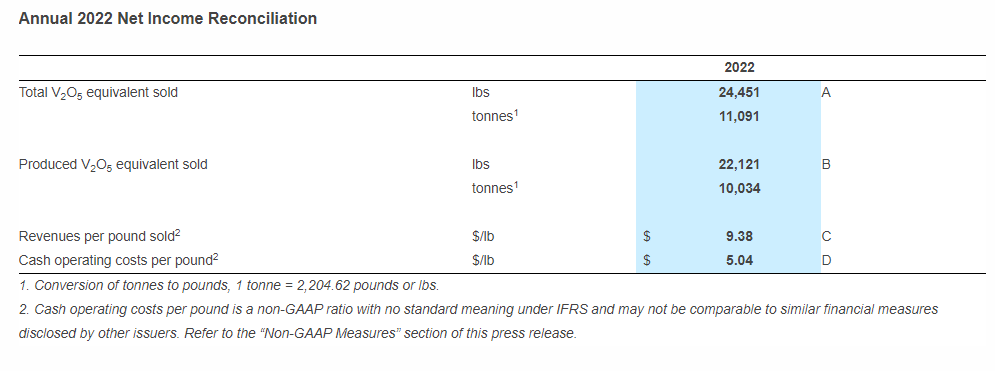

Revenues of $229.3 million in 2022, a 16% increase over 2021; Revenues per pound sold1 of $9.38 in 2022, a 19% increase over 2021

Operating costs of $169.7 million in 2022 vs. $133.0 million in 2021, and cash operating costs excluding royalties per pound1 of V2O5 equivalent sold of $4.57 in 2022 vs. $3.37 in 2021; 2% above upper range of revised 2022 guidance for cash operating costs excluding royalties per pound1

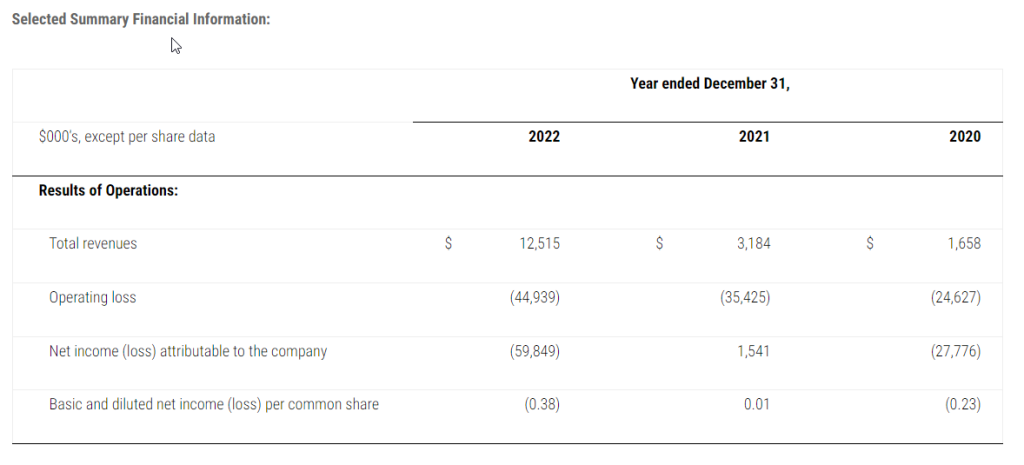

Net loss of $2.2 million in 2022 vs. net income of $22.6 million in 2021; Basic loss per share of $0.03 in 2022 vs. basic earnings per share of $0.35 in 2021

In 2022, the Company’s net loss included approximately $15.0 million of non-recurring expenditures

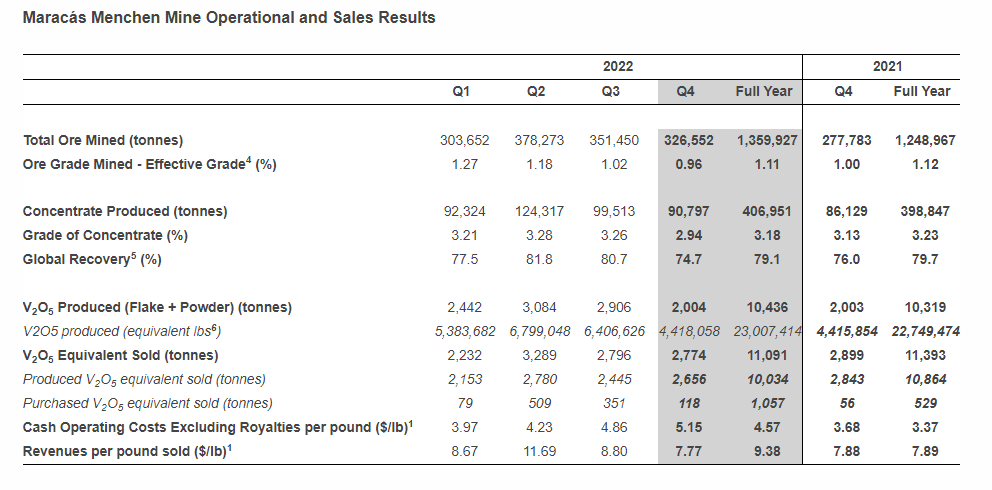

V2O5 production of 2,004 tonnes in Q4 2022 vs. 2,003 tonnes in Q4 2021; Annual V2O5 production of 10,436 tonnes in 2022 vs. 10,319 tonnes in 2021 and 6% below lower range of revised production guidance

Quarterly sales of 2,772 tonnes of V2O5 equivalent (inclusive of 118 tonnes of purchased material) in Q4 2022 vs. 2,899 tonnes in Q4 2021; Annual V2O5 equivalent sales of 11,091 (inclusive of 1,057 tonnes of purchased material) tonnes in 2022 vs. 11,393 tonnes in 2021 and within revised sales guidance of 11,000 – 12,000 tonnes

Vanadium Price Update2

The average benchmark price per pound of V2O5 in Europe was $8.25 in Q4 2022, being largely in line with the average of $8.23 seen in Q3 2022 and $8.30 in Q4 2021; The average benchmark price as of March 3, 2023 was $10.78, a 44% increase from the lows of 2022

The average benchmark price per kg of ferrovanadium (“FeV”) in Europe was $33.35 in Q4 2022, a 3% decrease from the average of $32.29 seen in Q4 2021; The average FeV benchmark price as of March 3, 2023 was $40.88, a 30% increase from the lows of 2022

TORONTO–(BUSINESS WIRE)– Largo Inc. (“Largo” or the “Company“) (TSX: LGO) (NASDAQ: LGO) today released financial and operating results for the three and twelve months ended December 31, 2022. The Company reported annual vanadium pentoxide (“V2O5”) equivalent sales of 11,091 tonnes at a cash operating cost excluding royalties per pound1 sold of $4.58. Revenues in 2022 increased 16% over 2021 to $229.3 million mainly due to a strengthening of vanadium prices in the year.

Daniel Tellechea, Interim CEO and Director of Largo, stated: “For Largo, 2022 was a challenging year, which led to an underperformance on both production and cost metrics, particularly in Q4 2023 with the mining disruption caused by record rainfall at our mine, cost inflation of key raw materials and sizeable non-recurring expenditures. Although we continue to navigate an inflationary environment, we anticipate delivering and capitalizing on a 10% increase in production for 2023 over 2022, particularly with the recent strengthening of vanadium prices.” He continued: “This recent increase is due in part to increased demand from the energy storage sector, especially in China, where new vanadium redox flow battery (“VRFB”) deployments totaling around 2 GWh or approximately 10% of global vanadium output are planned for the next 12-24 months.Importantly, the VRFB sector accounted for the second largest source of vanadium demand outside of the steel sector in Q3 2022, according to Vanitec, a global vanadium organization. Other key markets including steel, aerospace, and chemical have also shown considerable demand growth in recent months.”

He continued: “As for growth plans this year, Largo’s ilmenite project remains on track and is expected to generate a new source of revenue for the Company. We anticipate providing guidance on ilmenite production for 2023 once commissioning of the plant has been completed. We continue to make progress on the installation of our first VRFB in Spain and our negotiations toward the formation of a joint venture with Ansaldo Green Tech (“Ansaldo”) for the deployment of VRFBs in the Europe, Middle East and Africa power generation markets. Lastly, safety and sustainability remain key priorities for Largo and we are pleased to be recently ranked in the top quartile of our peer group as measured by certain ESG rating agencies for 2022.”

Q4 & Full Year 2022 Financial Results Overview

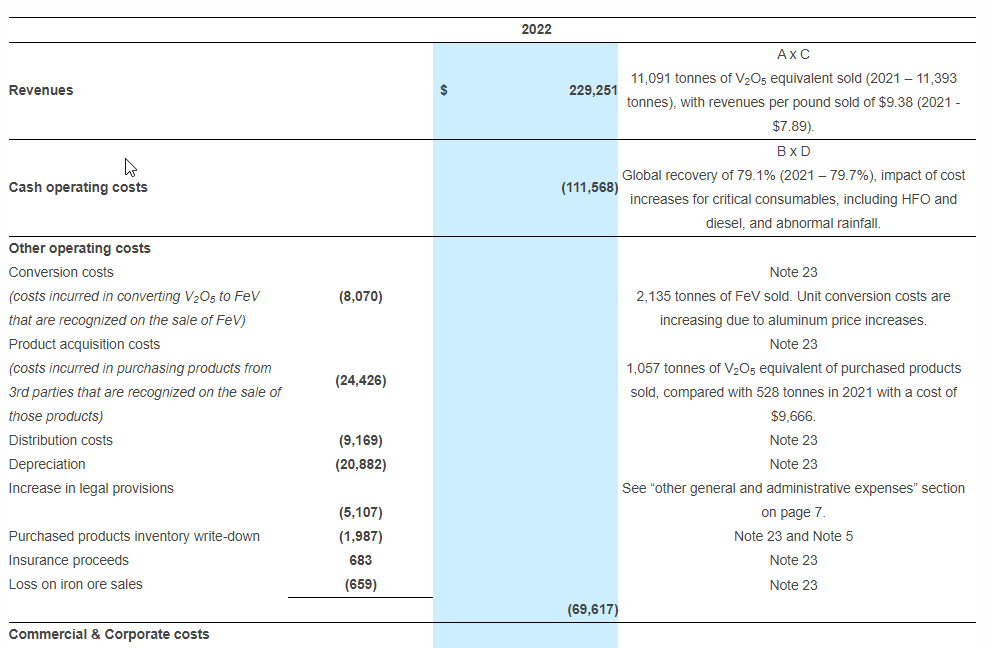

During 2022, the Company recognized revenues of $229.3 million from sales of 11,091 tonnes of V2O5 equivalent (2021 – 11,393 tonnes). This represents a 16% increase in revenues over 2021 ($198.3 million) mainly due to higher vanadium prices in the year, particularly with revenues recognized in Q2 2022. During Q4 2022, the Company recognized revenues of $47.5 million (Q4 2021 – $50.3 million) from sales of 2,772 tonnes of V2O5 equivalent (Q4 2021 – 2,899 tonnes).

Operating costs of $169.7 million in 2022 (2021 – $133.0 million) include direct mine and production costs of $94.5 million (2021 – $75.1 million), conversion costs of $8.1 million (2021 – $9.3 million), product acquisition costs of $24.4 million (2021 –$9.7 million), royalties of $10.4 million (2021 – $8.9 million), distribution costs of $9.2 million (2021 – $5.3 million), inventory write-down of $2.3 million (2021 – $3.2 million), depreciation and amortization of $20.9 million (2021 – $21.5 million) and iron ore costs of $1.0 million (2021 – $0.05 million), partially offset by insurance proceeds of $1.0 million (2021 – $nil).

Operating costs of $44.5 million in Q4 2022 (Q4 2021 – $37.7) include direct mine and production costs of $28.4 million (Q4 2021 – $21.4 million), conversion costs of $2.2 million (Q4 2021 – $2.6 million), product acquisition costs of $3.8 million (Q4 2021 – $1.0 million), royalties of $2.1 million (Q4 2021 – $2.3 million), distribution costs of $2.3 million (Q4 2021 – $1.5 million), inventory write-down of $0.4 million (Q4 2021 – $3.2 million), depreciation and amortization of $6.0 million (Q4 2021 – $5.8 million) and iron ore costs of $0.02 million (Q4 2021 – $nil), partially offset by insurance proceeds of $1.0 million (Q4 2021 – $nil).

The increases in direct mine and production costs are attributable to a decrease in the global recovery5, cost increases in critical consumables, including heavy fuel oil (“HFO”) and ammonium sulfate, as well as increased consumption of these critical consumables and sodium carbonate. Costs were further impacted by the Company’s mining contractor transition in Q3 2022 and corrective maintenance in the plant throughout the year. Higher costs of production in the current and previous periods in the year related to shutdowns caused by abnormally high rainfall during Q4 2022, while corrective maintenance continued to impact operating costs as a result of the time between production and sales.

Cash operating costs excluding royalties per pound1 of V2O5 equivalent soldwere $4.57 in 2022, compared with $3.37 in 2021. Cash operating costs excluding royalties per pound1 sold were $5.15 in Q4 2022, compared with $3.68 in Q4 2021. The increase seen in Q4 2022 and 2022 compared with Q4 2021 and 2021 is largely due to the impacts noted previously, in addition to produced V2O5 equivalent sold having decreased in 2022 as compared with 2021, with 10,034 tonnes sold versus 10,864 tonnes.

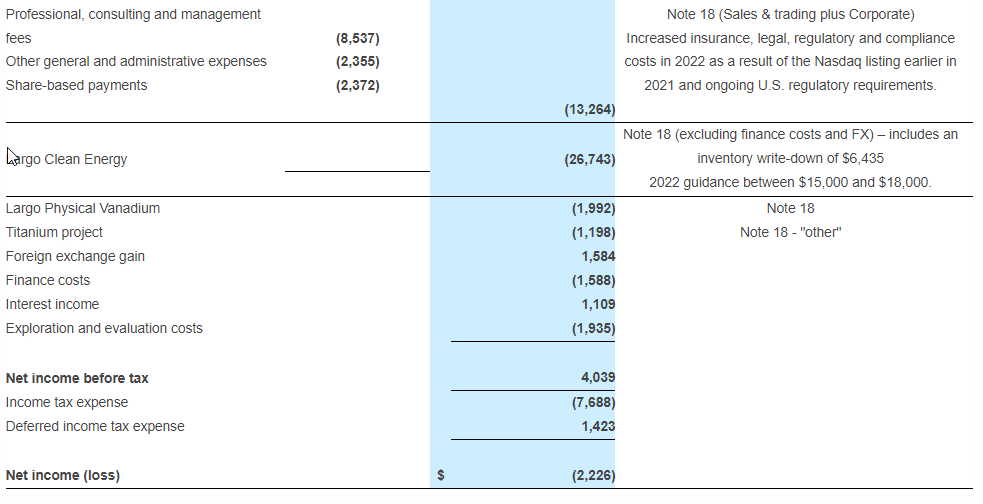

Professional, consulting and management fees were $25.3 million in 2022, compared with $17.9 million in 2021. Professional, consulting and management fees were $5.7 million in Q4 2022, compared with $5.6 million in Q4 2021. For 2022, the increase is primarily attributable to costs incurred earlier in the year in connection with LCE, which was not fully operational earlier in 2021 and transaction and listing related costs incurred by Largo Physical Vanadium Corp. (“LPV”) in connection with the completion of its qualifying transaction.

Other general and administrative expenses were $14.3 million in 2022, compared with $6.4 million in 2021. Other general and administrative expenses were $3.5 million in Q4 2022, compared with $2.3 million in Q4 2021. For 2022, the increase is primarily due to an increase in provisions as well as costs incurred in Q4 2022 in connection with LPV, and in Largo Clean Energy Corp. (“LCE”) which has scaled up activities throughout 2022. The increase in provisions relates to a supply agreement for the Maracás Menchen Mine which was filed with Brazilian courts in October 2014. The ruling requires the Company to pay amounts due, plus interest and legal fees.

Technology start-up costs were $12.7 million in 2022 (2021 – $3.8 million) and $8.2 million in Q4 2022 (Q4 2021 – 3.1 million). This includes a full write-down of battery components inventory at LCE of $6.4 million (Q4 2022 and 2022) (Q4 2021 and 2021 – $nil) to their expected net realizable value. Technology start-up costs relate to LCE’s activities related to ramping up its operations for the deployment of the VCHARGE VRFB system and the titanium project in Brazil.

Finance costs in Q4 2022 increased from Q4 2021 by 118% (or $0.4 million), which is attributable to increased debt, as well as the initial financing fees on the Company’s new debt facilities.

For 2022, cash provided by financing activities increased from cash used in financing activities in 2021 by $33.3 million. The movement is primarily attributable to the receipt of debt of $55.0 million and cash received from the sale of non-controlling interest of $7.3 million (2021 – $nil), partially offset by the repayment of debt of $30.0 million (2021 – $24.8 million) and share repurchases of $6.0 million. Cash provided by financing activities in Q4 2022 increased from cash used in financing activities in Q4 2021 by $24.1 million. This movement was primarily due to the receipt of new debt of $40.0 million, partially offset by a repayment of debt of $15.0 million.

Cash used in investing activities in Q4 2022 of $26.8 million is an increase of $19.8 million from the $7.0 million seen in Q4 2021. This movement was primarily driven by the purchase of vanadium assets and continued work on the ilmenite project. For 2022, the increase from 2021 was $32.7 million. Expenditures in 2022 primarily relate to the ilmenite project, mining equipment, costs relating to a software implementation and cash outflows for purchased product vanadium assets.

Additional Company Updates

Q4 and Full Year 2022 Operational Results: Production of 2,004 tonnes of V2O5 in Q4 2022 was in line with the 2,003 tonnes of V2O5 produced in Q4 2021, primarily due to reduced massive ore inventory arising from the transition in mining contractors in Q3 2022 and due to unusually heavy rainfall in December 2022. In Q4 2022, the Company produced 839 V2O5 equivalent tonnes of high purity products, including 650 tonnes of high purity V2O5 and 189 tonnes of high purity vanadium trioxide (“V2O3”). This represented 42% of the total quarterly production. In 2022, the Company produced 1,801 V2O5 equivalent tonnes of high purity products, including 1,368 tonnes of high purity V2O5 and 433 tonnes of high purity V2O3. In Q4 2022, 326,552 tonnes of ore were mined with an effective grade4 of 0.96% of V2O5. The ore mined in Q4 2022 was 18% higher than in Q4 2021. The Company produced 90,797 tonnes of concentrate with an effective grade4 of 2.94%. The global recovery5 achieved in Q4 2022 was 74.7%, a decrease of 1.7% from the 76.0% achieved in Q4 2021 and 7.4% lower than the 80.7% achieved in Q3 2022. The global recovery5 in October 2022 was 75.0%, with 67.8% achieved in November 2022 and 80.8% achieved in December 2022.

Continued Focus on ESG in 2022: The Company continued to improve its overall Environmental, Social and Governance (“ESG”) performance and public disclosures in 2022. This is reflected in additional improved ratings and scores, most notably its S&P Global Corporate Sustainability Assessment (“CSA”) rating having improved approximately 38%, placing the Company in the top quartile of its mining peer group for 2022. This improvement was largely driven by updates to Largo’s governance of ESG, including new policies, ESG oversight at the Board level and climate-related disclosures, as well as improved responses related to the Company’s on-going environmental compliance in Brazil. The Company expects to issue its 2022 sustainability report in late Q2 2023.

Largo Clean Energy Recent Developments: During Q4 2022, LCE continued to make significant progress on the delivery of the Enel Green Power España (“EGPE”) contract, which remains a priority focus. Substantially all the hardware is either in transit to or is in Spain awaiting installation. The Company shipped the remaining six of 12 electrolyte storage containers in early 2023 and the Field Service team has been on site in Q1 2023 and work is ongoing to install and interconnect the AC and DC power systems. Provisional acceptance, which requires the completion of as-build drawings, manuals, final punch-list items, and operational testing by EGPE, is expected to be completed by the end of May 2023. Additionally, LCE and Ansaldo continue to focus on the formation of a joint venture for the manufacturing and commercial deployment of VRFBs in the European, African and Middle East power generation markets. The Company’s previously announced memorandum of understanding (“MOU”) has been extended to March 31, 2023, to allow for the negotiation and entering into a joint venture and other ancillary agreements. Ansaldo and LCE continue to develop a business path for the joint venture to service the European markets with Long Duration Energy Storage (“LDES”).

Ilmenite Concentration Plant Progress: The Company progressed with the construction of its ilmenite concentration plant at its Maracás Menchen Mine in Q4 2022. The Company received all required flotation structures and is finalizing the building of its desliming, flotation, filtration, warehouse and pipe rack structures ands expects commissioning of the plant to be completed in Q2 2023.

January and February 2023 Production and Sales: Subsequent to Q4 2022, the Company produced 354 tonnes of V2O5 in January and 843 tonnes in February. The Company also sold 1,080 tonnes of V2O5 equivalent (including 68 tonnes of purchased material) in January 2023 and 750 tonnes (including 11 tonnes of purchased material) in February. Production in January and February was largely impacted by low ore availability in due to the heavy rains at the mine site and planned maintenance of the kiln for its refractory refurbishment, with sales in February being impacted by a delay in sales recognition. The Company expects to remain within its quarterly production and sales guidance for Q1 2023.

Largo Physical Vanadium Update: LPV’s net assets are now over 90% held in physical vanadium products and near-term delivery commitments (approximately 2.9 million lbs of V2O5 equivalent). The launch of LPV in September 2022 coincided with lower vanadium prices, which allowed LPV to purchase vanadium units at favorable market prices. LPV’s net asset value (“NAV”) is now C$2.56 per share or 28% above the closing share price of C$2.00 per share on March 8, 2023. LPV believes its NAV to share price discount offers current and new LPV investors an attractive investment case and closing this disconnect is now LPV’s key focus. LPV management are working on a broad marketing and communication campaign to raise awareness of its investment proposal.

Director Resignation: Following the Company’s previously announced leadership change on February 16, 2023, Mr. Paulo Misk has resigned from his position as a Director of the Company effective March 7, 2023.

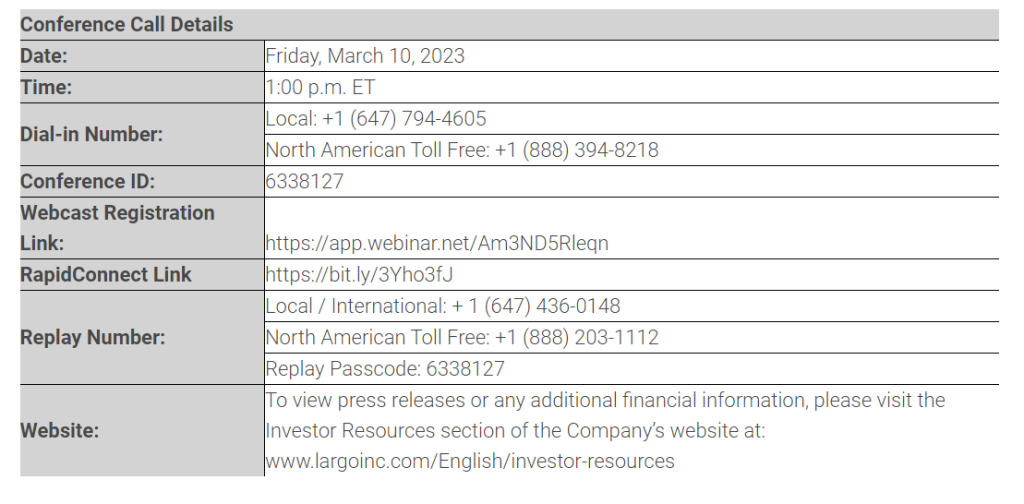

Annual 2022 Webcast and Conference Call Information

The Company will host a webcast and conference call on Friday, March 10, 2023, at 1:00 p.m. ET, to discuss its fourth quarter and annual 2022 results and progress.

Details of the webcast and conference call are listed below:

To join the conference call without operator assistance, you may register and enter your phone number at https://bit.ly/3Yho3fJ to receive an instant automated call back.

You can also dial direct to be entered to the call by an Operator via dial-in details below.

A playback recording will be available on the Company’s website for a period of 60-days following the conference call.

The information provided within this release should be read in conjunction with Largo’s annual consolidated financial statements for the years ended December 31, 2022 and 2021 and its management’s discussion and analysis for the year ended December 31, 2022 which are available on our website at www.largoinc.com or on the Company’s respective profiles at www.sedar.com and www.sec.gov.

About Largo

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURETM and VPURE+TM products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company will be implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Largo’s common shares trade on the Nasdaq Stock Market and on the Toronto Stock Exchange under the symbol “LGO”. For more information, please visit www.largoinc.com.

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable Canadian and United States securities legislation. Forward‐looking information in this press release includes, but is not limited to, statements with respect to the timing and amount of estimated future production and sales; the future price of commodities; costs of future activities and operations, including, without limitation, the effect of inflation and exchange rates; the effect of unforeseen equipment maintenance or repairs on production; timing and cost related to the build-out of the ilmenite plant; the ability to produce vanadium trioxide according to customer specifications; the extent of capital and operating expenditures; the impact of global delays and related price increases on the Company’s global supply chain and future sales of vanadium products. Forward‐looking information in this press release also includes, but is not limited to, statements with respect to our ability to build, finance and successfully operate a VRFB business, the projected timing and cost of the completion of the EGPE project; our ability to protect and develop our technology, our ability to maintain our IP, the competitiveness of our product in an evolving market, our ability to market, sell and deliver our VCHARGE batteries on specification and at a competitive price, our ability to successfully deploy our VCHARGE batteries in foreign jurisdictions; our ability to negotiate and enter into a joint venture with Ansaldo Green Tech on terms satisfactory to the Company and the success of such joint venture; the receipt of necessary governmental permits and approvals on a timely basis, our ability to secure the required resources to build and deploy our VCHARGE batteries, and the adoption of VRFB technology generally in the market.

The following are some of the assumptions upon which forward-looking information is based: that general business and economic conditions will not change in a material adverse manner; demand for, and stable or improving price of V2O5 and other vanadium commodities; receipt of regulatory and governmental approvals, permits and renewals in a timely manner; that the Company will not experience any material accident, labour dispute or failure of plant or equipment or other material disruption in the Company’s operations at the Maracás Menchen Mine or relating to Largo Clean Energy, specially in respect of the installation and commissioning of the EGPE project; the availability of financing for operations and development; the ability to mitigate the impact of continuing heavy rainfall; the Company’s ability to procure equipment and operating supplies in sufficient quantities and on a timely basis; that the estimates of the resources and reserves at the Maracás Menchen Mine are within reasonable bounds of accuracy (including with respect to size, grade and recovery and the operational and price assumptions on which such estimates are based); the competitiveness of the Company’s VRFB technology; the ability to obtain funding through government grants and awards for the Green Energy sector, the accuracy of cost estimates and assumptions on future variations of VCHARGE battery system design, that the Company’s current plans for ilmenite and VRFBs can be achieved; the Company’s “two-pillar” business strategy will be successful; the Company’s sales and trading arrangements will not be affected by the evolving sanctions against Russia; and the Company’s ability to attract and retain skilled personnel and directors; the ability of management to execute strategic goals.