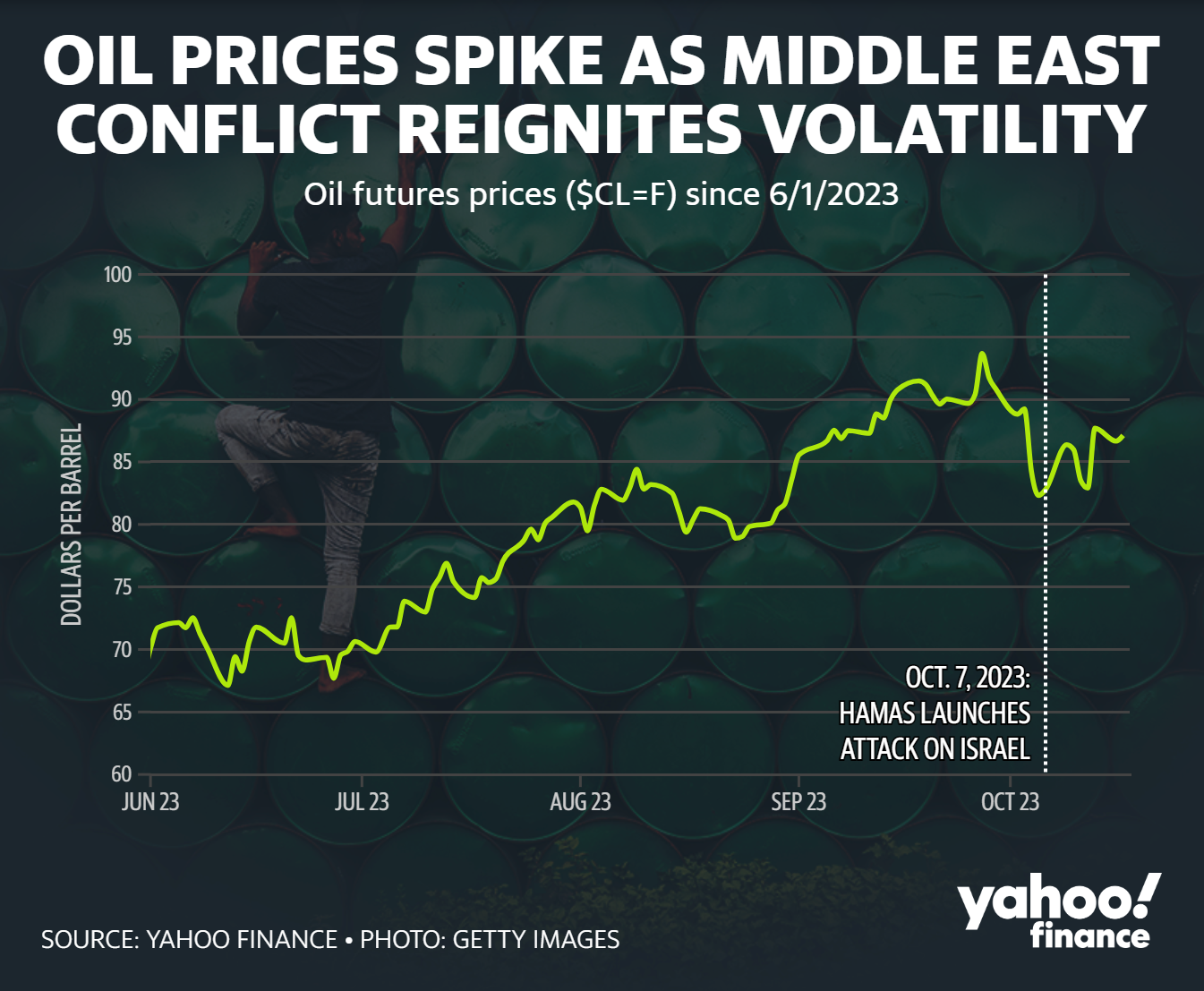

Oil prices surged over $2 per barrel on Friday as rising geopolitical tensions in the Middle East sparked fears of potential supply disruptions. Brent crude jumped 2.3% to nearly $90 per barrel, while WTI crude also gained 2.3% to exceed $85 per barrel. The abrupt price spike reflects growing worries among traders that intensifying regional conflicts could impact oil exports.

The increase came after U.S. forces conducted airstrikes on Iranian-backed militias in Syria. This retaliatory move followed attacks on American troops in the region by Iran-supported groups. The escalating tit-for-tat strikes raised concerns that oil-rich Iran could get dragged into a wider regional conflagration.

Iran’s foreign minister warned that the U.S. would “not be spared” from retaliation if Israel does not halt its ongoing offensive against Hamas forces in Gaza. Iran is a major oil producer and key Hamas backer, so any disruption to its exports would impact global supply.

The Gaza conflict has already killed dozens and shows no signs of abating despite international efforts. Israel continues to pound Hamas targets and says preparations for a ground invasion are underway. The potential for the violence to spill over into neighboring countries and inflame sectarian divisions adds another worrying dimension for oil markets.

While no direct oil infrastructure has been affected yet, the market is trading on fears of what could transpire if hostilities spread further. Key transit points like the Strait of Hormuz could be threatened if regional clashes escalate. About 17% of global oil shipments flow through this narrow passage from the Persian Gulf.

Even Saudi Arabia, the world’s top oil exporter, could see its supply chains disrupted if the chaotic conflicts metastasize. While its production facilities remain insulated so far, continued attacks between Israel and Hamas, along with the risk of Iranian retaliation on U.S. forces, are setting markets on edge.

Traders are operating with limited visibility into how much further tensions may rise or which countries could get sucked in. Major oil producers like Saudi Arabia, Iraq, and the UAE would be hard pressed to supplant any lost Iranian barrels in a tight market. The low spare capacity leaves oil supplies extremely vulnerable to regional instability.

With myriad conflicts simmering, anxious traders are bidding up prices based on a worst-case scenario of supply shocks. However, this geopolitical risk premium could evaporate quickly if the situation de-escalates. Much depends on how hardline regimes like Iran choose to counter Israeli and U.S. actions in the days ahead.

For now, investors should brace for more volatility as headlines oscillate between conflict and ceasefire. Oil markets will remain on edge, with prices whip-sawing on any indications that Middle East disputes could jeopardize supply flows. While an outright supply crunch may not emerge, the risk has clearly increased.

Traders are weighing these bullish supply disruption anxieties against bearish demand uncertainties. Resurgent Covid cases in China along with broader inflationary pressures and economic weakness continue to dampen the consumption outlook. For oil markets, layers of complexity will drive price gyrations going forward. Strap in for a bumpy ride.

Shares of Siemens Energy took a nosedive on Thursday after the German wind power firm revealed it is seeking financial guarantees from the government to shore up its balance sheet. The company’s stock plunged over 32% amid concerns over ongoing problems at its wind turbine manufacturing subsidiary Siemens Gamesa.

This latest crisis of confidence in Siemens Energy comes after a tumultuous year where the company scrapped its profit forecasts due to major setbacks at Siemens Gamesa. Persistent quality control issues and production delays have plagued Siemens Gamesa, dragging down the parent company’s financial performance. Siemens Energy shocked investors earlier this year when it warned that these issues could persist for years.

Now Siemens Energy is looking to the German government for a lifeline to provide the guarantees it needs for long-term projects and growth ambitions. With its strong order intake and project pipeline, Siemens requires sizeable guarantees to move forward. It remains unclear exactly how much financing Siemens Energy is seeking from the government and what form this support may take. The company is holding preliminary talks with German officials, banks, and other stakeholders to find a solution.

For investors, this latest turmoil calls Siemens Energy’s financial health into question. While the company left its 2023 guidance unchanged, its stock has been battered this year. Shares are down nearly 60% year-to-date due to the cascading problems at Siemens Gamesa. The turbine troubles will continue to be a dark cloud over Siemens Energy until substantial progress is made on quality control and production. Siemens Gamesa’s issues with offshore wind ramp up also remain a glaring concern.

All of this uncertainty around Siemens Energy and its finances have sent investors rushing for the exits. But for bargain hunters, the plummeting stock could also look like a tempting buying opportunity. Siemens Energy maintains a strong long-term outlook in the booming renewable energy market. Demand for wind power is surging, especially in Europe, as countries move aggressively toward carbon neutrality. Siemens Energy still boasts an enviable portfolio of technology and intellectual property in the industry.

If Siemens Energy can weather its current storms, its future prospects in offshore and onshore wind power remain bright. But the company must fix its turbine troubles and strengthen its balance sheet to fully capture the potential ahead. For conservative investors, it may be best to wait on the sidelines until more clarity emerges. But for speculators willing to stomach volatility and risk, Siemens Energy’s swooning shares could offer a high-risk, high-reward proposition.

Much depends on whether the German government views Siemens Energy as simply too big and important to fail. Germany is staking much of its economic future on renewable energy leadership. Having a national industrial champion falter so badly would be an embarrassment and setback. Siemens Energy is essentially making the case that it’s too strategically vital for Germany’s interests to be allowed to flounder.

Yet the German government also has to be wary of setting a precedent of bailing out struggling companies at taxpayer expense. Germany may be willing to extend credit guarantees to Siemens Energy, but direct financial aid seems unlikely. The coming months will be crucial in determining if Siemens Energy can right itself and deliver on its clean energy ambitions. For investors, the ride may continue to be bumpy until the company can prove it has turned a corner.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Permex completed a 1 for 4 common share consolidation. The consolidation, which was effective October 23, 2023, was initially announced on October 19, 2023. The consolidation affects Permex shares on the Canadian Securities Exchange (CSE), the Frankfurt Stock Exchange and the OTCQB. With the consolidation, the number of outstanding shares has been reduced from approximately 2 million to 400,000. The consolidation was needed to be listed on the Nasdaq Capital Market. If completed at an assumed post-consolidation price of $7.64 per share, the offerings would generate $29 million.

Permex to issue common equity and warrants. On October 20, 2023, Permex filed a prospectus to issue up to 1.9 million common units with accompanying warrants and to issue up to 1.9 million pre-funded units and warrants. The warrant associated with the common units does not have a set exercise price, which we will assume will be near the common stock offer price. The warrants for the pre-funded common shares will have an exercise price of $0.01 per share. The new shares, if approved, will trade on the Nasdaq Capital Market under the symbols OILS and OILSW.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Oct. 23, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) is pleased to announce the release of our 2022 Sustainability Report (the “Report”), highlighting our approach to environmental, social and governance (“ESG”) practices for the year ended December 31, 2022 and outlining our commitment to building a sustainable future for all of our stakeholders. A full copy of the Report, which was approved by Alvopetro’s Board of Directors, can be found on our website at https://alvopetro.com/Sustainability.

2022 ESG highlights included:

Natural gas focused production (96% of total 2022 production);

Alvopetro’s locally produced natural gas resulted in average savings of 57% for consumers relative to imported LNG;

Maintained low emission intensity with Scope 1 & 2 emissions intensity of 7.4 kg CO2e per boe;

No reported environmental spills;

Zero lost-time safety incidents;

33% of our total workforce and 38% of our senior leadership team positions are held by women;

Strengthened commitment to biodiversity and conservation with our northeastern collared sloth conservation program;

Expanded social investment programs to benefit over 600 recipients, increasing spending by 156% ; and,

With increased production and cash flows, we paid over $20 million in royalties, income taxes and sales taxes, contributing to direct and indirect benefits for the communities we operate and to Brazil as a whole.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé and Murucututu natural gas fields and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning Alvopetro’s approach to ESG practices and plans for the future. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning the success of future drilling, completion, testing, recompletion and development activities, equipment availability, the timing of regulatory licenses and approvals, the outlook for commodity markets and ability to access capital markets, the impact of global pandemics and other significant worldwide events, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR+ profile at www.sedarplus.ca. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

In a significant move that underscores the ongoing transformation within the energy sector, Chevron (NYSE: CVX) has recently announced its acquisition of Hess (NASDAQ: HES) in a monumental $53 billion all-stock deal. This mega-merger comes on the heels of Exxon Mobil’s $60 billion bid for Pioneer Natural Resources, marking the second colossal consolidation among major U.S. oil players this month.

The strategic significance of this merger revolves around the ambitions of both Chevron and Exxon to unlock the untapped potential of Guyana’s burgeoning oil industry. Guyana, once an inconspicuous player in the oil sector, has rapidly ascended the ranks to become one of Latin America’s foremost oil producers, second only to industry giants Brazil and Mexico, thanks to substantial oil discoveries in recent years.

This high-stakes deal positions Chevron in direct competition with its formidable rival, Exxon, in the race to capitalize on Guyana’s newfound prominence. Chevron’s offer, consisting of 1.025 of its shares for each share of Hess or $171 per share, represents a premium of approximately 4.9% to the stock’s most recent closing price. The total value of the transaction, encompassing debt, amounts to a staggering $60 billion.

Upon the successful completion of this transaction, John Hess, CEO of Hess Corp, is set to join Chevron’s board of directors, cementing the collaborative vision of the two energy giants. Chevron has also expressed its commitment to fortify its share repurchase program, intending to bolster it by an additional $2.5 billion, reaching the upper limit of its annual $20 billion range. This decision underscores Chevron’s confidence in future energy prices and its robust cash generation.

Notably, this merger serves as a testament to Chevron’s unwavering dedication to fossil fuels. In a climate where global energy dynamics are evolving rapidly, Chevron’s move underscores a resolute belief in the enduring strength of oil demand. Large energy producers continue to employ acquisitions as a strategy to replenish their reserves after years of underinvestment, further highlighting the industry’s drive to secure its future in a dynamically shifting landscape.

This merger between Chevron and Hess not only signals the industry’s determination to harness the full potential of Guyana’s oil reserves but also represents a pivotal moment in the evolution of the energy sector, as established players seek new avenues for growth and consolidation in a rapidly changing world. The deal is expected to close around the first half of 2024, setting the stage for a new chapter in the energy industry’s ongoing narrative.

U.S. drivers have seen welcome relief in recent weeks as gas prices steadily drift lower, even while oil continues to trade near $90 per barrel. The national average gasoline price now sits at $3.58 per gallon, down 30 cents over the last month.

What’s behind this divergence between oil and gas prices? And what does it mean for the average American’s wallet?

Seasonal Shifts Push Gas Prices Lower

The primary drivers pulling gas prices downward are seasonal factors. In the fall, refineries begin switching to cheaper winter-blend gasoline formulations. At the same time, cooler weather means lower fuel demand. Both these trends allow gas prices to detach from oil markets.

Rebecca Babin, an energy trader at CIBC Private Wealth, explained that “gas prices seasonally fall every autumn. 2022 is no exception.” Gas prices often decline 20 to 25 cents per gallon or more between September and December.

Supply Growth Eases Market Tightness

This year’s price declines also come as fuel inventories have rebounded nearly 10% from 2021 levels. Whereas last year saw tight fuel supplies amid recovering demand, expanded refinery runs have improved market balance in 2022.

“Anything that adds product to the market is going to help bring down refinery margins,” said Jeff Barron of the U.S. Energy Information Administration. These inventory and supply differences make today’s environment markedly different from a year ago.

On the crude side, OPEC+ production cuts and global disruptions have kept oil prices elevated. Prices spiked last week on Middle East escalation fears before retreating again.

According to Babin, oil markets remain well-supported in the low $80s per barrel due to the supply-demand balance. Further gains into the $90s could threaten demand, however. The key uncertainty is whether OPEC+ extends output curbs into 2023.

Gas Demand Slackens Amid High Prices

Sky-high prices have also dampened U.S. retail fuel demand, which recently slipped below 2020 levels. Brenda Shaffer, an energy specialist at Georgetown University, notes demand may decline “as Americans cut back on unnecessary car trips to save money.”

With households pinched by inflation, discretionary driving becomes a prime target for budget cuts. But lower fuel consumption then puts further downward pressure on prices.

The Consumer Impact

Falling pump prices come as welcome relief, especially heading into the busy holiday travel season. The 40-cent drop from the September peak has saved U.S. households nearly $10 billion, by some estimates.

“It’s like getting a little raise, without having to ask your boss,” says Patrick De Haan, head of petroleum analysis at GasBuddy.

Lower fuel costs help curb inflationary pressures and provide savings that can be redirected to other household needs. But prices remain elevated historically. Americans are still paying nearly $400 more per year to fill up than just two years ago.

While the gas price outlook remains murky, any further declines over the next few months would aid consumers through winter. Yet many will likely remain wary of rising fuel bills cutting into tight budgets.

The Biden administration is making a major push to develop a domestic hydrogen economy by funding 7 regional hydrogen hubs across the United States. The hubs will share up to $7 billion in federal funding aimed at spurring hydrogen production and use.

President Joe Biden and Energy Secretary Jennifer Granholm announced Friday the selection of hubs in Appalachia, California, the Gulf Coast, the Heartland, Mid-Atlantic, Midwest, and Pacific Northwest regions. The funds come from last year’s Bipartisan Infrastructure Law.

Accelerating the Hydrogen Economy

The goal is to accelerate the growth of a clean hydrogen industry in the U.S. Hydrogen is a versatile fuel seen as a critical tool for decarbonizing major sectors like heavy industry, transportation, and power generation.

When produced using low-carbon methods, hydrogen can provide emissions-free energy for hard-to-abate sectors. Expanding hydrogen is a key plank of the Biden administration’s strategy to cut greenhouse gas emissions and combat climate change.

The 16-state regional hubs model fosters clusters of hydrogen supply and demand, minimizing transportation needs. The administration expects the $7 billion federal injection to mobilize over $43 billion in private capital.

Leveraging Regional Strengths

Each hydrogen hub leverages unique geographic strengths ideal for clean hydrogen production. For example:

The Appalachia Hub will use the region’s abundant natural gas supply, applying carbon capture to lower emissions.

California and the Pacific Northwest have access to seaports critical for shipping hydrogen.

The Heartland can utilize wind resources to produce hydrogen via electrolysis.

The Midwest Hub will tap into nuclear power to make hydrogen.

In addition to production, the regional hubs focus on cultivating local hydrogen markets. Some will provide hydrogen for industrial uses while others may focus on fertilizer or fuel cell vehicle growth.

Building on Bipartisan Policy

The hydrogen hub funding originated from the bipartisan infrastructure package passed in 2021. The law included $8 billion for at least four regional hubs.

The Biden administration expanded the program to seven hubs to extend geographic impact. The policy builds on bipartisan support for advancing hydrogen in the U.S.

Last year’s Infrastructure Investment and Jobs Act also created a hydrogen production tax credit. The recently passed Inflation Reduction Act further boosted hydrogen incentives with an additional $3 per kg production credit.

The Energy Department will provide guidance on utilizing the tax credits later this year. The credits will aid long-term viability of the regional hubs.

Spurring Private Investment

The federal money is intended to galvanize substantial private capital investment in building out hydrogen infrastructure. Siting hydrogen hubs near key anchor facilities can spur economic growth.

For example, California’s hub grants will likely stimulate billions in private funding around port facilities. Financial incentives like the hydrogen tax credits create ideal conditions for private sector buy-in.

Over time, decreasing costs through scale and technology improvements could make hydrogen competitive with conventional fuels. The regional hubs represent a starting point designed to nurture both supply and demand.

Next Steps for Growth

The hydrogen hubs mark an important early phase of U.S. efforts to scale up the hydrogen economy. Biden administration officials noted work remains to develop connective infrastructure and further applications.

Ongoing policy support via research funding, incentives, and enabling regulation will help drive growth. Continued bipartisan cooperation around hydrogen could lead to additional catalytic investments.

With the right policy environment, hydrogen could become a major pillar of America’s clean energy economy. The regional hubs represent a down payment on the infrastructure needed to realize hydrogen’s vast decarbonization potential across the economy.

CALGARY, AB, Oct. 11, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) is pleased to announce that we have now completed drilling the 183-A3 well on our 100% owned Murucututu natural gas field. Based on open-hole logs, the well encountered potential net natural gas pay across two separate formations totaling 127.7 metres, with an average porosity of 10.3%.

President and CEO, Corey C. Ruttan commented:

“The results from our uphole 183-A3 Caruaçu exploration target has significantly exceeded our pre-drill expectations and has the potential to open up a large stacked multi-zone development opportunity in further support of our longer-term natural gas growth objectives.”

The 183-A3 well was drilled to a total measured depth (“MD”) of 3,540 metres. Based on open-hole logs, the well encountered potential net natural gas pay in both the Caruaçu Member of the Maracangalha Formation and the Gomo Member of the Candeias Formation, with an aggregate 127.7 metres total vertical depth (“TVD”) of potential natural gas pay, using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cutoff.

Caruaçu Exploration Target

In the Caruaçu Member, a total of 116.1 metres TVD of potential net natural gas pay was encountered between 2,542 metres and 3,062 metres, at an average 38.5% water saturation and an average porosity of 10.4%. Alvopetro currently has no reserves or resources assigned to this Target.

Candeias Formation

In the Gomo Member of the Candeias Formation, a total of 11.6 metres TVD of potential net natural gas pay was encountered between 3,085 metres and 3,270 metres, at an average water saturation of 30.6% and an average porosity of 9.1%. Our Proved reserves for this development well had estimated 12.5 meters of net natural gas pay with porosity of 11.0% and 17% water saturation.

Based on these drilling results, subject to regulatory approvals and equipment availability, we plan to complete the well and put it on production directly to the adjacent field production facility.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé and Murucututu natural gas fields and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Testing and Well Results. Data obtained from the 183-A3 well identified in this press release, including hydrocarbon shows, open-hole logging, net pay and porosities should be considered to be preliminary until testing, detailed analysis and interpretation has been completed. Hydrocarbon shows can be seen during the drilling of a well in numerous circumstances and do not necessarily indicate a commercial discovery or the presence of commercial hydrocarbons in a well. There is no representation by Alvopetro that the data relating to the 183-A3 well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Cautionary statements regarding the filing of a Notice of Discovery. We have submitted a Notice of Discovery of Hydrocarbons to the Agência Nacional do Petróleo, Gás Natural e Biocombustíveis (the “ANP”) with respect to the 183-A3 well. All operators in Brazil are required to inform the ANP, through the filing of a Notice of Discovery, of potential hydrocarbon discoveries. A Notice of Discovery is required to be filed with the ANP based on hydrocarbon indications in cuttings, mud logging or by gas detector, in combination with wire-line logging. Based on the results of open-hole logs, we have filed a Notice of Discovery relating to our 183-A3 well. These routine notifications to the ANP are not necessarily indicative of commercial hydrocarbons, potential production, recovery or reserves.

Oil and natural gas reserves. This news release includes certain information contained in the independent reserves and resources assessment and evaluation prepared by GLJ Ltd. (“GLJ”) dated February 27, 2023 with an effective date of December 31, 2022 (the “GLJ Reserves and Resource Report”). Specifically, this news release contains information concerning proved reserves in the GLJ Reserves and Resource Report applicable to the 183-A3 well. The information included herein represents only a portion of the disclosure required under NI 51-101. Full disclosure with respect to the Company’s reserves as at December 31, 2022 is included in the Company’s annual information form for the year ended December 31, 2022 which has been filed on SEDAR+ (www.sedarplus.ca) The reserves definitions used in this evaluation are the standards defined by COGEH reserve definitions and are consistent with NI 51-101 and used by GLJ. The recovery and reserve estimates of the Company’s reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual reserves may be greater than or less than the estimates provided herein

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning potential net natural gas pay in the 183-A3 well and expectations regarding future development plans for the well and the Murucututu natural gas field. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning results from completing the 183-A3 well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of global pandemics and other significant worldwide events, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR+ profile at www.sedarplus.ca. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Gas sales declined due to a temporary reduction in demand. Gas sales to Bahiagas in September averaged 6.8 MMcf/d down 35% from August sales and well below peak sales of 15.8 MMcf/d in the March quarter. Gas sales were below take or pay agreements by 1.2 MMcf/d, which will be treated as deferred revenue. Gas sales had been declining in recent months because Alvopetro’s joint venture partner in its primary field had increased its nominations for gas sales following the start-up of its plant. The decline in September is related to lower demand and comes in addition to nomination issues.

Management views the decline as temporary and is working to increase production in 100% owned fields. As we have indicated before, increased partner nominations will result in lower partner nominations in the latter years of well lives. In addition, Alvopetro is making progress drilling new wells that do not have nomination issues. Regarding the drop in demand, we would remind investors that the city of Bahia is a vibrant growing city that has limited gas supply options beyond Alvopetro. We are not concerned with a one-month decline in demand but recommend investors monitor demand issues going forward.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Oil giant Exxon Mobil is making a huge bet on shale with its just-announced $59 billion all-stock acquisition of Pioneer Natural Resources, one of the largest producers in the Permian Basin of West Texas and New Mexico. Shale oil is a type of unconventional oil found in shale rock formations that must be hydraulically fractured to extract the oil.

The deal, which is Exxon’s biggest since its merger with Mobil in 1999, will give it access to Pioneer’s large acreage position in the Permian, allowing Exxon to more than double its current production in the region to over 1 million barrels per day once the deal closes in 2024.

This massive expansion of Exxon’s shale oil production comes even as much of the industry has pulled back investments in new drilling due to investor pressure to improve returns and limit growth. While Exxon is already one of the most active drillers in the Permian, the addition of Pioneer’s operations will make it the largest shale oil producer in the basin by far.

The shale boom propelled U.S. oil production to record highs in recent years, though growth has slowed more recently. The Biden administration has also paused new leases for drilling on federal lands, creating uncertainty around future shale production. However, the industry is still projected to provide most new sources of oil supply worldwide in the coming years.

Exxon’s bet is that shale, especially the Permian where production costs are lowest, will continue to drive future growth. Pioneer outlined an ambitious plan last year to raise Permian production as high as 2 million barrels per day by 2030. Together, the companies expect to capture major cost savings by combining operations.

But analysts say the deal is not without risk for Exxon. While shale helped supercharge U.S. production, the industry has had a mixed track record of profitability. Investors have lost patience with shale companies struggling to deliver consistent returns, pushing firms like Pioneer to focus more on cost discipline and shareholder payouts rather than maximum production growth.

Outside shale, Exxon is also working to develop large, costly conventional oil projects offshore Guyana and in other regions to replenish reserves. Some analysts question whether Exxon might be spreading itself thin trying to balance massive shale drilling with high-stakes conventional projects.

More broadly for the oil industry, concerns around climate change have made the long-term outlook uncertain. With electric vehicles going mainstream and many governments setting net-zero emissions targets, peak oil demand may already be behind us according to some forecasts.

While Exxon says shale oil will be needed to meet global energy demand for decades to come, increasing pressure on the industry to reduce emissions led Pioneer to accelerate its own net zero target from 2050 to 2035 after the acquisition was announced. With shale methane emissions a major focus for policymakers, combining operations could allow for more investment in leak detection and reductions.

For now, Exxon seems confident in the value of shale, and particularly the Permian’s vast oil riches. The Pioneer deal positions it to be the dominant driller in the West Texas region as others pull back. But only time will tell whether the big bet on shale pays off or leaves Exxon overextended. The deal reflects one of the oil majors’ biggest signals of confidence yet that shale will continue driving growth well into the future.

CALGARY, AB, Oct. 5, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces September 2023 sales volumes and an operational update.

September 2023 Sales Volumes

September sales volumes averaged 1,203 boepd, including natural gas sales of 6.8 MMcfpd and associated natural gas liquids sales (“NGLs”) from condensate of 69 bopd, bringing our average sales volumes to 1,696 boepd in the third quarter of 2023.

Natural gas, NGLs and crude oil sales:

September 2023

August 2023

Q3 2023

Q2 2023

Natural gas (Mcfpd), by field:

Caburé

6,165

9,894

8,949

9,891

Murucututu

642

662

726

665

Total Company natural gas (Mcfpd)

6,807

10,556

9,675

10,556

NGLs (bopd)

69

84

81

84

Oil (bopd)

–

8

3

8

Total Company (boepd)

1,203

1,852

1,696

1,852

Our offtaker, Bahiagás reduced offtake in September due to a temporary reduction in end user consumption. As a result, natural gas nominations and production were below Bahiagás’ take or pay limits within our contract. Our contract requires that Bahiagás pay Alvopetro for the greater of actual gas delivered in the month or 80% of the Firm contracted volumes for the period. Our Firm contracted volume is currently 300,000 m3/d1 or 10.6 MMcfpd1, before adjusting for heat content of our delivered natural gas. As such, Bahiagas is required to pay Alvopetro for gas not taken up to 8.5 MMcfpd1. On a heat adjusted basis this amounted to 1.2 MMcfpd (35 MMcf) in September which is in addition to the September sales volume noted above of 6.8 MMcfpd. This volume paid but not taken by Bahiagas is to be compensated by Alvopetro in the future through natural gas deliveries in excess of 9.5 MMcfpd1. Natural gas deliveries during October have been approximately 8.7 MMcfpd to-date.

1 Volume represents contract volume based on contract referenced natural gas heating value. Note that Alvopetro’s delivered natural gas sales volumes, as reflected in the table above, are prior to any adjustments for heating value of Alvopetro natural gas. Alvopetro’s natural gas is approximately 7.5% hotter than the contract reference heating value.

Operational Update

In July, we spud our 183-A3 well on our Murucututu natural gas field. We are currently drilling at 3,383 metres and our plan is to drill the well to 3,480 metres total depth.

On our Bom Lugar field, we drilled the BL-6 well to a total depth of 3,244 metres. The well was completed in two intervals. The first Caruaçu interval from 2,591 to 2,598 metres was perforated and 28 barrels of fluid was swabbed over a 12-hour period with 17 barrels of 29 degree API oil and 39% water cut. The second Caruaçu interval from 2,486 to 2,598 metres swabbed 101 barrels of fluid over 24 hours with 89 barrels of 33 degree API oil and 12% water cut. We completed an organic acid stimulation and are equipping the well with an artificial lift system and expect to have the well on production next week.

Upcoming Investor Conference

Corey C. Ruttan, President and Chief Executive Officer, will present at the ‘Schachter Catch the Energy’ Conference on Saturday October 14, 2023, at 11:30 am (Mountain time).

Date:

October 14, 2023

Time:

11:30 am to 12:05 pm (Mountain time)

Location:

Mount Royal University (4825 Mt Royal Gate SW, Calgary, Alberta) Bella Concert Hall & Ross Glen Hall (Presentation Room 1)

The Conference is hosted by Josef Schachter, CFA and author of the Schachter Energy Report. Alvopetro’s presentation will include a moderated Q&A session. In addition, company personnel will be available throughout the day at Alvopetro’s booth to answer investor questions.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé and Murucututu natural gas fields and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Abbreviations:

bbls

=

barrels

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

BRL

=

Brazilian real

m3

=

cubic metre

m3/d

=

cubic metre per day

MMBtu

=

million British thermal units

Mcf

=

thousand cubic feet

Mcfpd

=

thousand cubic feet per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

Q2 2023

=

three months ended June 30, 2023

Q3 2023

=

three months ended September 30, 2023

BOE Disclosure. The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Testing and Well Results. Data obtained from the BL-06 well identified in this press release, including initial testing data and associated production, should be considered to be preliminary. Production during testing is useful in confirming the presence of hydrocarbons, however, such production and production rates are not determinative of the rates at which such well will continue production and decline thereafter. Test results are not necessarily indicative of long-term performance of the relevant well or fields or of ultimate recovery of hydrocarbons and there is no representation by Alvopetro that the data relating to the BL-06 well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning the expected timing of certain of Alvopetro’s testing and operational activities including the expected timing of drilling the 183-A3 well, expected timing of production commencement from the BL-06 well, exploration and development prospects of Alvopetro, and expected natural gas sales and gas deliveries under the Company’s long-term gas sales agreement. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning testing results of the BL-06 well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of global pandemics and other significant worldwide events, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR+ profile at www.sedarplus.ca. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

CALGARY, AB, Oct. 2, 2023 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.015 per common share payable on October 31, 2023, to shareholders of record at the close of business on October 16, 2023. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Oil price rose 30% in the third quarter helping propel the XLE Energy Index up 11.4%. Natural gas prices also rose after twelve months of decline. Higher oil prices reflect declining inventories due to rising demand that is not being met by rising supply.

Domestic oil demand is rising. Oil demand largely tracks the economy. And, while monetary tightening has slowed growth, demand is still growing. Recently, domestic demand has increased due to warm summer weather and increased propane exports to Europe.

Oil supply is not keeping pace. OPEC+ extended its production cuts. In previous decades, domestic producers would respond to production cuts by accelerating drilling. In recent years, producers have not increased drilling as noted by a sharp decline in domestic oil rig activity. Oil drilling rigs even declined this quarter despite the rise in oil prices. Limited drilling, combined with sharper well decline curves, has meant supply is not keeping up with demand.

Small cap producers are uniquely positioned to take advantage of higher prices. The production gains that came from horizontal drilling and fracking in the Permian Basin appear to be waning. That means well profitability has declined as producers move on to secondary and tertiary targets. This is especially an issue for larger production companies that need a large number of wells drilled to provide growth. In addition, large companies face regulatory and investor pressures regarding fossil fuel production that the smaller companies may avoid.

Energy Stocks

Energy stocks, as measured by the XLE Energy Index, rose 11.4% in the 2023 third quarter as compared to a 3.6% decline in the S&P 500 Index. The outperformance was largely due to rising oil prices. The November 2023 futures contract rose 30% during the quarter. Natural gas prices rose 4.9% during the quarter largely reflecting normal seasonal trends.

Oil Prices

The rise in oil prices corresponds to a drop in inventories. After a covid-induced spike in early 2020, domestic inventories have fallen steadily. During this period of monetary tightening, demand growth has slowed but remained positive. Supply, on the other hand, has stagnated. OPEC+ has extended cutbacks and domestic drilling activity has declined.

Figure #1

Source: EIA

The decline in drilling activity can best be seen by looking at domestic oil rig activity. Where once there were more than 1600 active wells, now there are one-third that number. What’s more, oil drilling activity has continued to decline in the third quarter even as oil prices have risen.

Figure #2

Source: Baker Hughes

Weather has also played a part as warm temperatures have meant increased use of oil for electric generations. Although oil represents a small portion of the generation load, it is an important component in the summer months when generation demand is greatest. Temperatures in the United States have been warmer than average each month this summer and 17 of the 24 months over the last four years.

Figure #3

Finally, it is worth noting that petroleum exports have been growing. Exports jumped after the Ukraine invasion as the United States rushed to ship petroleum to Europe to offset Russian supply disruptions. Note the large jump in propane exports since 2021 in the chart below. Propane, a component of the crude oil barrel, is one of the easier fuels to export until additional liquified natural gas export terminals are completed.

Figure #4

The combination of limited drilling, growing demand for electric generation and exports, and OPEC production cuts bodes well for oil prices.

Natural Gas Prices

The story for natural gas is less positive but improving. Sharp declines last winter bottomed out in April and have slowly begun to creep back upward. Natural gas production profitability is not great at prices near $3.00 per thousand cubic feet (mcf) but still profitable.

Figure #5

Source: Nymex, EIA

Outlook

We believe the outlook for energy companies remains favorable. Oil prices are high and do not show signs of falling due to OPEC cuts, reduced domestic drilling and rising demand for power generation and exports. We believe the case for smaller cap energy stocks is especially strong because they are less liquid and slower to react to rising energy prices. Smaller energy companies also face less political and investor pressure to shift away from carbon-based production.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.