Vancouver, British Columbia–(Newsfile Corp. – July 11, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that the TSX Venture Exchange (the “TSXV”) has accepted the Company’s Notice of Intention to renew of its Normal Course Issuer Bid (the “NCIB”) to purchase for cancellation, from time to time, as Hemisphere considers advisable, up to 8,255,766 common shares (“Common Shares”) of the Company, representing approximately 10% of the current public float of the Common Shares.

Purchases of Common Shares will be made on the open market through the facilities of the TSXV. For any Common Shares purchased, Hemisphere will pay the prevailing market price of the Common Shares. The actual number of Common Shares that may be purchased for cancellation and the timing of any such purchases will be determined by the Company and dependent on market conditions.

The Company is commencing the NCIB because it believes that, from time to time, the market price of its Common Shares may not properly reflect the underlying, intrinsic value of the Company, and that, at such times, the purchase of Common Shares for cancellation will increase the proportionate interest of, and be advantageous to, all remaining shareholders.

The NCIB will commence on July 14, 2024 and will terminate on July 13, 2025 or at such earlier time as the NCIB is completed or terminated at the option of Hemisphere. The Company has retained Canaccord Genuity Corp. as its broker to conduct the NCIB on its behalf.

Under the Company’s previous notice of intention to conduct a normal course issuer bid, the Company sought and received approval of the TSXV to purchase 8,670,636 Common Shares for the period from July 14, 2023 to July 13, 2024. During that period, the Company purchased 4,074,400 Common Shares on the open market at a weighted-average price of $1.425 per Common Share.

About Hemisphere Energy Corporation

Hemisphere is a dividend paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Note Regarding Forward-Looking Statements and Other Advisories

This document contains forward-looking information. This information relates to future events and the Company’s future performance. All information and statements contained herein that are not clearly historical in nature constitute forward-looking information, and the words “may”, “will”, “should”, “could”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “propose”, “predict”, “potential”, “continue”, “aim”, or the negative of these terms or other comparable terminology are generally intended to identify forward-looking information. Such information represents the Company’s internal projections, estimates, expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. This information involves known or unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking information. Hemisphere believes that the expectations reflected in this forward-looking information are reasonable; however, undue reliance should not be placed on this forward-looking information, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. This press release contains forward-looking information concerning, among other things, the anticipated advantages of the NCIB to Hemisphere’s shareholders and the Company’s business strategy, the price to be paid by Hemisphere for purchases of Common Shares under the NCIB and Hemisphere’s plans for maximizing value per share growth with the sustainable development of its high netback high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. The reader is cautioned that such information, although considered reasonable by the Company, may prove to be incorrect. A number of risks and other factors could cause actual results to differ materially from those expressed in the forward-looking information contained in this document including, but not limited to, the risk that the anticipated benefits of the NCIB may not be achieved and the risk that the Company may not be able to successfully execute its business strategy or growth plans. Readers are cautioned that the foregoing list of factors is not exhaustive. Although the forward-looking statements contained in this document are based upon assumptions which management of Hemisphere believes to be reasonable, Hemisphere cannot assure investors that actual results will be consistent with these forward-looking statements. With respect to forward-looking statements contained in this document, Hemisphere has made assumptions regarding, among other things, the ability of Hemisphere to fund purchases of Common Shares under the NCIB and its business strategy. These forward-looking statements are made as of the date of this document and Hemisphere disclaims any intent or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or results or otherwise, other than as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

In a surprising turn of events, oil prices have climbed for the second consecutive session, with Brent crude settling above $85 per barrel. This uptick comes as hopes for U.S. interest rate cuts were fueled by an unexpected slowdown in inflation. The market’s reaction to these economic indicators highlights the intricate connections between macroeconomic factors and commodity prices.

The latest data from the U.S. Bureau of Labor Statistics revealed a decline in consumer prices for June. This unexpected drop has boosted expectations that the Federal Reserve might cut interest rates sooner than anticipated. Following the release of the inflation data, traders saw an 89% chance of a rate cut in September, up from 73% the day before. Slowing inflation and potential rate cuts are expected to spur more economic activity. Analysts from Growmark Energy have noted that such measures could bolster economic growth, subsequently increasing demand for oil.

Federal Reserve Chair Jerome Powell acknowledged the recent improvements in price pressures but stressed to lawmakers that more data is needed to justify interest rate cuts. His cautious approach underscores the Fed’s commitment to data-driven policy decisions. The possibility of rate cuts also impacted the U.S. dollar index, causing it to drop. A weaker dollar generally supports oil prices by making dollar-denominated commodities cheaper for buyers using other currencies. Gary Cunningham, director of market research at Tradition Energy, emphasized this point, noting that a softer dollar could enhance oil demand.

The rise in oil prices also reflects broader market dynamics. On Wednesday, U.S. data showed a draw in crude stocks and strong demand for gasoline and jet fuel, ending a three-day losing streak for oil prices. Additionally, front-month U.S. crude futures recorded their steepest premium to the next-month contract since April. This market structure, known as backwardation, indicates supply tightness. When market participants are willing to pay a premium for earlier delivery dates, it often signals that current supply isn’t meeting demand.

While current market conditions suggest strong demand, future demand forecasts from major industry players show significant divergence. The International Energy Agency (IEA) recently predicted global oil demand growth to slow to under a million barrels per day (bpd) this year and next, mainly due to reduced consumption in China. In contrast, the Organization of the Petroleum Exporting Countries (OPEC) maintained a more optimistic outlook, forecasting world oil demand growth at 2.25 million bpd this year and 1.85 million bpd next year. This discrepancy between the IEA and OPEC forecasts is partly due to differing views on the pace of the global transition to cleaner fuels.

Alex Hodes, an analyst at StoneX, noted that the divergence in demand forecasts is unusually wide, attributing it to varying opinions on how quickly the world will shift to cleaner energy sources. This uncertainty adds another layer of complexity to market predictions and planning.

The interplay between inflation data, interest rate expectations, and oil demand forecasts creates a nuanced picture for the future of oil prices. If the Federal Reserve proceeds with rate cuts, increased economic activity could boost oil demand. However, the ongoing transition to clean energy and geopolitical factors will continue to play crucial roles. For now, market participants and analysts will closely monitor economic indicators and policy decisions. The recent rise in oil prices highlights the market’s sensitivity to macroeconomic trends and the importance of timely and accurate data in shaping market expectations.

These recent movements in oil prices underscore the complex interdependencies between economic data, policy decisions, and market dynamics. As inflation shows signs of cooling and hopes for rate cuts grow, the oil market is poised for potentially significant shifts. Understanding these trends is crucial for stakeholders across the industry as they navigate the evolving landscape of global energy markets.

In a bold move that underscores its commitment to the energy transition, Honeywell International Inc. (NYSE: HON) announced on Wednesday its agreement to acquire Air Products’ (NYSE: APD) liquefied natural gas (LNG) process technology and equipment business for $1.81 billion in cash. This acquisition, Honeywell’s fourth in 2024, signals the industrial giant’s aggressive push into the burgeoning LNG market and its determination to position itself as a key player in the global energy landscape.

The deal comes at a time when LNG demand is surging, particularly in power generation and data center applications. According to the Energy Information Administration, U.S. LNG exports are projected to reach 12.2 billion cubic feet per day in 2024 and 14.3 billion cubic feet per day in 2025, up from a record 11.9 billion cubic feet per day in 2023. This growth trajectory presents a significant opportunity for Honeywell to capitalize on the increasing global appetite for cleaner energy sources.

By acquiring Air Products’ LNG unit, Honeywell gains access to cutting-edge technologies such as heat exchangers and cryogenic equipment, which complement its existing LNG pretreatment business. The addition of Air Products’ coil-wound heat exchangers, known for their efficient liquefaction capabilities and minimal space requirements, will enhance Honeywell’s competitive edge in both onshore and offshore LNG applications.

From an investor’s perspective, this acquisition aligns perfectly with Honeywell’s strategic focus on three “mega trends” identified by CEO Vimal Kapur: automation, the future of aviation, and energy transition. The LNG business acquisition squarely addresses the energy transition pillar, potentially opening up new revenue streams and market opportunities for the company.

Financially, the deal is expected to be accretive to Honeywell’s adjusted earnings per share in the first full year of ownership. Analyst Sheila Kahyaoglu from Jefferies estimates that the transaction could boost adjusted earnings by approximately 1% in 2025. Moreover, Honeywell anticipates growth opportunities in aftermarket services and digitalization through its Forge platform, which could further enhance the deal’s long-term value proposition.

The acquisition also demonstrates Honeywell’s commitment to growth through strategic M&A activity. With this latest deal, the company is on track to deploy around $15 billion in acquisitions in 2024 alone, a clear indication of its aggressive growth strategy and confidence in its ability to integrate and leverage new technologies and market positions.

For investors, Honeywell’s move into the LNG space offers exposure to a critical segment of the energy transition. As countries worldwide seek to reduce their carbon footprint while ensuring energy security, LNG is increasingly seen as a crucial “bridge fuel” in the shift from coal to renewables. Honeywell’s enhanced capabilities in LNG technology position it to benefit from this global trend.

However, investors should also consider the potential risks. The LNG market can be volatile, subject to geopolitical tensions and fluctuations in global energy demand. Additionally, the success of the acquisition will depend on Honeywell’s ability to effectively integrate Air Products’ LNG business and leverage its technologies across its existing customer base.

Honeywell’s $1.81 billion acquisition of Air Products’ LNG business represents a strategic bet on the future of energy. This move positions the company as a more comprehensive player in the LNG value chain, potentially opening up new revenue streams and market opportunities. For investors seeking exposure to the energy transition trend through a diversified industrial giant, this deal enhances Honeywell’s appeal. The company’s ability to integrate this acquisition effectively and leverage its new technologies across its existing customer base will be crucial to realizing the full value of this investment. As Honeywell continues to align itself with key technological and market trends, investors should closely monitor how this strategic move contributes to the company’s long-term growth trajectory and its role in shaping the evolving global energy landscape.

As Tesla continues to dominate headlines with its electric vehicles and ambitious plans for autonomous driving, a less-discussed segment of the company is quietly becoming a potential game-changer. Tesla’s energy business, particularly its energy storage division, is showing signs of becoming a major contributor to the company’s bottom line and future growth prospects.

In a recent production and delivery report, Tesla revealed that it had deployed a record-breaking 9.4 GWh (gigawatt hours) of battery energy storage in the second quarter of 2024. This figure represents more than double the amount deployed in the first quarter, signaling explosive growth in this sector.

Tesla’s energy storage solutions range from residential Powerwall units to utility-scale Megapack installations. A single Powerwall can store enough energy to power a small home for a day, while a Megapack installation boasts the capacity to provide electricity to 3,600 homes for an hour. This scalability allows Tesla to cater to a wide range of customers, from individual homeowners to large utility companies and municipalities.

The financial performance of Tesla’s energy business is equally impressive. In the first quarter of 2024, the segment generated $1.6 billion in revenue and $403 million in gross profit. What’s particularly noteworthy is the gross margin of 24.6%, significantly higher than Tesla’s overall gross margin of 17.4% for the same period. This robust profitability comes at a crucial time for Tesla, as its automotive business faces margin pressure due to recent price cuts aimed at stimulating demand.

Wall Street is taking notice of this shift. Adam Jonas, an analyst at Morgan Stanley, dubbed the Q2 energy deployment figures a “show stealer” and valued Tesla Energy at $36 per Tesla share, or approximately $130 billion. This valuation suggests that the energy business could be a substantial component of Tesla’s market capitalization in the future.

The growth potential for Tesla’s energy storage business is closely tied to broader technological and infrastructure trends. The increasing adoption of artificial intelligence and the subsequent need for more data centers are expected to drive a “multigenerational increase in energy demand,” according to Jonas. This surge in electricity needs, coupled with the ongoing transition to renewable energy sources, positions Tesla’s energy storage solutions as a critical component of future power grids.

Moreover, the Inflation Reduction Act in the United States is likely to accelerate investments in grid infrastructure, potentially creating more opportunities for Tesla’s energy products. As utilities and businesses look to modernize and stabilize the power grid, Tesla’s Megapack installations could play a crucial role in load balancing and ensuring reliable power supply.

While much of the investor focus has been on Tesla’s automotive innovations, including the anticipated launch of a lower-priced electric vehicle and the reveal of its robotaxi concept, the energy business could provide a significant upside surprise in upcoming earnings reports. This diversification of revenue streams may also help to stabilize Tesla’s financial performance, reducing its reliance on the cyclical automotive market.

It’s worth noting that Tesla’s energy business isn’t limited to storage solutions. The company also produces solar roof tiles and conventional solar panels, although these products have received less attention in recent years. As the energy storage business continues to grow, it may create synergies with Tesla’s solar products, offering customers comprehensive energy solutions.

As we approach Tesla’s Q2 earnings report in July 2024, investors and analysts will be keenly watching the performance of the energy storage segment. If the strong deployment figures translate into substantial revenue and profit growth, it could mark a turning point in how the market perceives Tesla – not just as an automaker, but as a diversified energy and technology company.

In conclusion, Tesla’s energy storage business is emerging as a powerful growth driver for the company. With its impressive profit margins, scalable solutions, and alignment with global energy trends, this segment could play a crucial role in Tesla’s future success and valuation. As the world continues its transition to sustainable energy, Tesla appears well-positioned to capitalize on the growing demand for advanced energy storage solutions.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Looking ahead. While first quarter production was 5% lower than the prior year period, we expect a stronger second quarter due to wells that went into production in late March and early April and stronger crude oil prices. InPlay plans to drill and bring new production online in the third quarter of 2024 that is focused on high oil-weighted properties. The oil-weighted production from new wells is expected to benefit from higher realized oil prices forecasted for the balance of the year.

Updating estimates. We have increased our 2024 and 2025 EPS estimates to $0.18 and $0.26, respectively, from $0.16 and $0.23. Our estimates reflect modestly higher production in the second and third quarters of 2024 and higher crude oil prices. We forecast adjusted funds flow of $91.0 million in 2024 and $99.4 million in 2025. Depending on the company’s production profile, we think our estimates may prove conservative.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Special dividend. Excluding special dividends, Hemisphere Energy pays a base dividend of C$0.025 per share per quarter, or C$0.10 per share on an annual basis. Hemisphere Energy recently declared a special dividend of C$0.03 per common share. The special dividend will be paid on July 26 to shareholders of record on July 12. In May, the company’s board of directors approved a quarterly cash dividend of C$0.025 per share that will be paid on June 28 to shareholders of record on June 20.

Return of capital to shareholders. To date in 2024, Hemisphere has committed to returning C$10.7 million to shareholders, including shares repurchased and canceled under the company’s normal course bid, quarterly dividend payments in February and June, and the special dividend payment in July. Returns of capital are funded entirely with free cash flow supported by ultra-low decline rates, low operating expenses, low capital-intensive assets, long life reserves and minimal decommissioning liabilities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – June 4, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that its board of directors has approved the declaration of a special dividend to shareholders.

Given the strong financial position and performance outlook of the Company, Hemisphere is pleased to announce that its board of directors has approved the declaration of a special dividend of C$0.03 per common share. The special dividend is part of Hemisphere’s comprehensive shareholder return model, and will be paid on July 26, 2024 to shareholders of record on July 12, 2024. This special dividend is designated as an eligible dividend for Canadian income tax purposes. It is in addition to the Company’s quarterly base dividend of C$0.025 per common share announced on May 29, 2024, and is in accordance with the Company’s dividend policy.

Hemisphere has committed to shareholder returns of $10.7 million thus far in 2024, including shares repurchased and cancelled under the Company’s normal course issuer bid, two quarterly dividend payments in February and June, and the special dividend payment in July. This return of capital is funded entirely by the Company’s free cash flow and is made possible by its high-margin enhanced oil recovery (“EOR”) assets, ultra-low production decline, and healthy balance sheet.

Subsequent to Hemisphere’s last news release, the Company has now brought online all three producers in its new Marsden, Saskatchewan development play. The purpose of primary production at these wells prior to polymer flood start-up is to gather fluid samples, pressure data, and other relevant reservoir data that will assist in EOR project planning. Construction of Hemisphere’s multi-well battery is currently underway, with anticipated polymer skid delivery and EOR project start-up in the third quarter.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood EOR methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a quarterly dividend will be paid in June 2024; that a special dividend will be paid to shareholders on July 26, 2024 to shareholders of record on July 12, 2024; and the timing of Hemisphere’s anticipated polymer skid delivery and EOR project start-up in the third quarter.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the timing for payment of the special dividend; no delays in the anticipated timing for delivery of the polymer skid and EOR project; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in project timelines and workstreams; changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer, and vacuum technologies for the defense, space, energy, and process industries, today announced that it has received approximately $17 million of orders for two expansion projects in the energy and petrochemical markets.

Daniel J. Thoren, President and CEO, commented, “We are excited to work with our North American customer as they aim to create the world’s first net-zero carbon emissions integrated ethylene cracker and derivatives site. Graham’s surface condensers with custom venting package allow the turbine drives to operate at peak efficiency and are considered state of the art in our industry. Additionally, we received a notable order to support an expansion project in the Middle East, which we attribute to our strong relationship and our customer’s preference for our high-performance steam jet ejectors.”

The North American order includes three surface condenser systems for critical service in both a main process unit and utility unit. This project aims to advance the eco-friendliness of natural gas refining, with the collective goal to minimize carbon emissions throughout the production process. The order was received in April 2024 and approximately 50% of the revenue is expected to be recognized in fiscal 2025 with the remainder expected in fiscal 2026.

For the Middle East expansion project, the Company was awarded a contract to supply a new vacuum system for a crude to chemical vacuum distillation tower. This project aims to bolster the production of Group II and Group III Base Oils. This order was received in March 2024, with revenue expected to be recognized in fiscal 2025.

About Graham Corporation

GHM is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy and process industries. The Graham Manufacturing and Barber-Nichols’ global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems.

Graham Corporation routinely posts news and other important information on its website, www.grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “aims,” “expects,” “anticipates,” “potential,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, winning potential future or multi-year orders, potential revenues and timing of such revenues, capacity, demand growth, and delivering timely or otherwise on schedule are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission, including under the heading entitled “Risk Factors,” its quarterly reports on Form 10-Q, and other filings it makes with the Securities and Exchange Commission. Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Hemisphere Energy reported production results, pricing, and costs in line with expectations. The company remains on track to meet or beat management guidance. With production and oil prices rising, we expect cash flow and earnings to improve in upcoming quarters.

The company is actively drilling, including in a new area. Hemisphere drilled five wells during the quarter which should lead to production growth. Current production has already reached peak levels. The recently acquired property Marsden play represents a step out of current production and could be an important area for future growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – May 29, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the first quarter ended March 31, 2024, declares a quarterly dividend payment to shareholders, renews credit facility, and provides operations update.

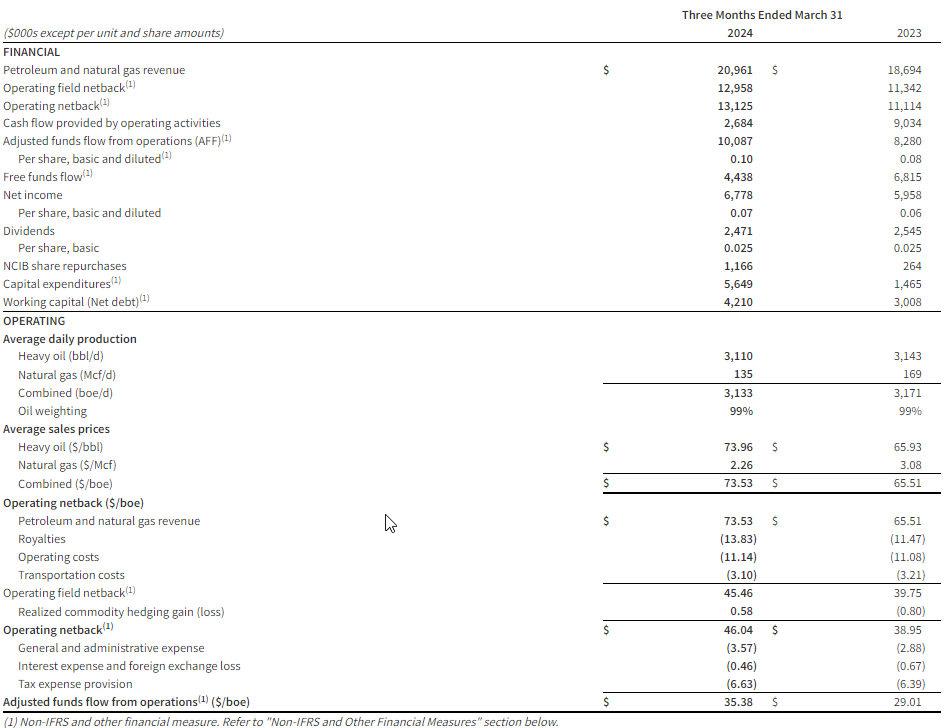

Q1 2024 Highlights

Produced a quarterly average of 3,133 boe/d (99% heavy oil), including significant downtime in January and early February due to extreme cold weather.

Attained quarterly revenue of $21.0 million.

Maintained low operating and transportation costs of $14.24/boe despite reduced quarterly production.

Delivered an operating netback1 of $13.1 million, or $46.04/boe.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $10.1 million, or $35.38/boe.

Achieved free funds flow1 of $4.4 million, or $0.04 per share.

Executed a $5.6 million capital expenditure1 program, including drilling five horizontal wells (three producers, two injectors) in the Company’s new Marsden, Saskatchewan oil play.

Received Enhanced Oil Recovery (“EOR”) project approval from the Ministry of Energy and Resources for a pilot polymer flood in Marsden.

Distributed $2.5 million, or $0.025 per share, in dividends to shareholders during the quarter.

Purchased and cancelled 869,100 shares for $1.2 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Exited the first quarter with positive working capital1 of $4.2 million, compared to $3.0 million at the end of March 2023.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditure, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited consolidated interim financial statements and related notes, and the Management’s Discussion and Analysis for the three months ended March 31, 2024 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Financial and Operating Summary

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on June 28, 2024 to shareholders of record as of the close of business on June 20, 2024. The dividend is designated as an eligible dividend for income tax purposes.

Credit Facility

The Company has completed its annual bank review and renewed its $35.0 million two-year extendible credit facility, with the next annual review date set for May 31, 2025.

Operations Update

Hemisphere’s Atlee Buffalo polymer injection projects both continue to perform well, contributing to slight overall corporate production growth. Current production is approximately 3,500 boe/d (99% heavy oil, field estimates between April 1 – May 25, 2024), 3% higher than the fourth quarter of 2023 despite no new wells having been brought online since last September.

In the first quarter of 2024, the Company received EOR project approval from the Ministry of Energy and Resources for a polymer flood pilot in its recently acquired Marsden acreage in Saskatchewan. Subsequently, Hemisphere executed a $5.6 million capital expenditure program, which included drilling five Marsden wells (three producers and two injectors). The Company has recently brought one well on primary production to a single well battery in order to gather initial test data required for EOR project planning. Hemisphere expects to commission a new polymer injection skid and oil treating battery for its Marsden project during the third quarter.

Preparation is also underway for the remainder of Hemisphere’s 2024 capital expenditure program, which includes up to nine new wells in the Atlee Buffalo area being drilled and brought on production to existing facilities later this summer.

Annual General and Special Meeting of Shareholders

Hemisphere’s Annual General and Special Meeting of Shareholders will be held at 10:00 am (Pacific Daylight Time) on May 30, 2024 in the Walker Room of the Terminal City Club located at 837 West Hastings Street, Vancouver, British Columbia.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that the Company expects to commission a new polymer injection skid and oil treating battery for its Saskatchewan production during the third quarter; the timing and execution of Hemisphere’s 2024 capital expenditure program, which includes up to nine new wells in the Atlee Buffalo area being drilled and brought on production to existing facilities later this summer; and that a dividend will be paid June 28, 2024 to shareholders of record as of the close of business on June 20, 2024.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the length of time that oil and gas operations will be impaired by the outbreak of Covid-19; the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, free funds flow, capital expenditures, operating field netback, operating netback, and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered more meaningful than IFRS measures in evaluating the Company’s performance.

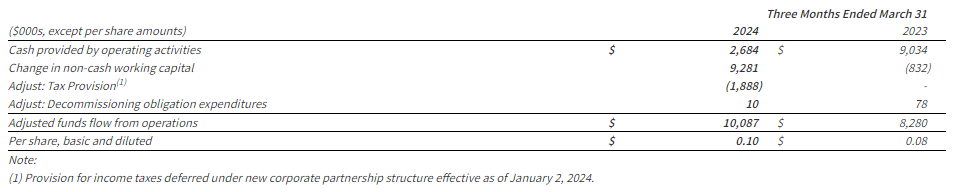

a)Adjusted funds flow from operations (“AFF”) (Non-IFRS Financial Measure and Ratio if calculated on a per share or boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

A reconciliation of AFF to cash provided by operating activities is presented as follows:

b)Free funds flow (“FFF”) (Non-IFRS Financial Measure): Calculated by taking adjusted funds flow and subtracting capital expenditures, excluding acquisitions and dispositions. Management believes that free funds flow provides a useful measure to determine Hemisphere’s ability to improve returns and to manage the long-term value of the business.

c)Capital Expenditures (Non-IFRS Financial Measure): Management uses the term “capital expenditures” as a measure of capital investment in exploration and production assets, and such spending is compared to the Company’s annual budgeted capital expenditures. The most directly comparable IFRS measure for capital expenditures is cash flow used in investing activities. A summary of the reconciliation of cash flow used in investing activities to capital expenditures is set forth below:

d)Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): A benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses, and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e)Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): calculated as the operating field netback plus the Company’s realized gain (loss) on derivative financial instruments on an absolute and per barrel of oil equivalent basis.

f)Working Capital/Net debt (Non-IFRS Financial Measure): Closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working capital/Net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding derivative financial instruments, decommissioning obligations, lease liabilities, and tax provisions, and including any bank debt. There is no IFRS measure that is reasonably comparable to working capital/net debt.

The following table outlines the Company calculation of working capital/net debt:

g)Supplementary Financial Measures and Non-IFRS Ratios

“Adjusted Funds Flow from operations per basic share” is comprised of funds from operations divided by basic weighted average common shares. “Adjusted Funds Flow from operations per diluted share” is comprised of funds from operations divided by diluted weighted average common shares. “Annual Free Funds Flow” is comprised of free funds flow from the current three-month period multiplied by four. “Operating expense per boe” is comprised of operating expense, as determined in accordance with IFRS, divided by the Company’s total production. “Realized heavy oil price” is comprised of heavy crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. “Realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. “Realized combined price” is comprised of total commodity sales from production, as determined in accordance with IFRS, divided by the Company’s total production. “Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the Company’s total production. “Transportation costs per boe” is comprised of transportation expense, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2023 and the interim period ended March 31, 2024, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

Any references in this news release to initial production rates (including as a result of recent water or polymer flood activities) are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

Barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

IFRS

International Financial Reporting Standards

boe/d

barrel of oil equivalent per day

$/boe

dollar per barrel of oil equivalent

US$

United States Dollar

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

The United States government has fired a major salvo in the escalating electric vehicle (EV) battleground with China, slapping heavy tariffs on Chinese EV imports as well as key battery materials and components. While the move aims to protect American jobs and manufacturers, it carries significant implications for automakers, suppliers, and investor portfolios on both sides of the Pacific.

At the center of the new trade barriers is a 100% tariff on Chinese-made EVs entering the U.S. market. The administration has also imposed 25% duties on lithium-ion batteries, battery parts, and critical minerals like graphite, permanent magnets, and cobalt used in EV production.

For American automakers like Tesla, General Motors, and Ford, the tariffs could provide a substantial competitive advantage on home soil. By erecting steep import costs on Chinese EVs, it makes their domestically produced electric models immediately more price competitive versus foreign rivals. This pricing edge could help ramp up EV sales for Detroit’s Big Three as they work to gain traction in this burgeoning market.

The tariffs represent a major headache for Chinese automakers like BYD that have ambitions to crack the lucrative U.S. EV market. BYD and peers like Nio have been counting on American sales to drive their global expansion efforts. The 100% tariff makes their EVs essentially uncompetitive on price compared to domestic alternatives.

However, the calculus could change if Chinese EV makers ramp up battery production and vehicle assembly closer to U.S. shores. BYD has already established a manufacturing footprint in Mexico. If more production is localized in North America, Chinese brands may be able to circumvent the duties while realizing lower logistics costs.

The impacts extend beyond just automakers. Battery material suppliers and lithium producers could face production cuts and lower pricing if Chinese EV demand softens due to fewer exports heading stateside. Major lithium producers like Albemarle and SQM saw shares dip as the tariff news increased global oversupply fears.

But if U.S. electric vehicle adoption accelerates in response to the import barriers, it could create new demand for lithium and other battery materials from domestic sources, analysts note. North American miners and processors may emerge as beneficiaries as automakers look to localize their supply chains.

Of course, trade disputes cut both ways. There are risks that China could retaliate against major U.S. exports or American companies operating in the country. That creates potential headwinds for a wide range of U.S. multinationals like Apple, Boeing, and Starbucks that rely on Chinese production and consumption. Any tit-for-tat actions could ripple across the global economy.

The levies also raise costs across EV supply chains at a vulnerable time. With inflation already depressing consumer demand, pricier batteries and components could curb the pace of electrification both in the U.S. and globally if passed along to car buyers. Conversely, domestic automakers have leeway to absorb higher input expenses to gain market share from Chinese imports.

With EV competition heating up between the world’s two largest economies, investors will need to scrupulously analyze potential winners and losers from the unfolding trade battle across the electric auto ecosystem. In the near-term, the tariffs appear to boost American legacy automakers while putting China’s crop of upstart EV makers on the defensive. Global battery and mineral suppliers face an uncertain shake-up.

Over the longer haul, costs, capital outlays, production geography, and consumer demand dynamics will ultimately determine the fallout’s enduring market impacts. The new levies represent a double-edged sword potentially accelerating the EV transition in the U.S. while fracturing previously integrated cross-border supply lines.

Prudent investors should weigh both the risks and opportunities across the entire EV value chain. While headline-grabbing, tariffs alone won’t determine winners and losers in the seismic shift to electric mobility taking shape globally. Proactively adjusting portfolios to the changing landscape will be crucial for optimizing exposures.

Want small cap opportunities delivered straight to your inbox? Channelchek’s free newsletter will give you exclusive access to our expert research, news, and insights to help you make informed investment decisions.

In a transformative transaction for the U.S. shale industry, Crescent Energy Company has agreed to acquire rival Eagle Ford producer SilverBow Resources in an all-stock deal valued at $2.1 billion. The combination solidifies Crescent’s position as a leading player in the prolific Eagle Ford basin of South Texas, creating the second largest operator in the region.

The deal significantly bolsters Crescent’s scale and low-cost inventory. SilverBow shareholders can elect to receive 3.125 Crescent shares for each SilverBow share owned, or opt for $38 per share in cash up to a $400 million cap. Post-closing, expected in Q3 2024, existing Crescent investors will own between 69-79% of the combined entity.

The merged company boasts imposing production of around 250,000 boe/d from a complementary portfolio of high-quality, long-life assets spanning the Eagle Ford and Uinta basins. This large-scale, high-margin asset base underpins robust free cash flow generation backed by a deep inventory of high-return drilling locations to drive compelling growth.

For Crescent, the deal achieves increased scale and premiumization of its portfolio through SilverBow’s attractive Eagle Ford position assembled over 30 years in the region. The combination enhances corporate returns through $65-$100 million of expected annual synergies from combined operating efficiencies and cost of capital benefits.

Crescent characterizes the transaction as highly accretive on all key per share metrics. It aligns with the company’s proven strategy of pursuing disciplined acquisitions at attractive valuations to augment its free cash flow, production, and inventory depth. Maintaining a fortress investment-grade balance sheet post-merger affords financial flexibility to further consolidate the fragmented shale landscape.

The deal represents a compelling value proposition for SilverBow shareholders. They gain exposure to Crescent’s larger-scale diversified assets while participating in the upside from performance improvements, synergy realization, and further consolidation. Alternatively, investors can opt for immediate cash consideration at a premium.

Crescent’s leadership expressed high confidence in the strategic merits of the transaction. Chairman John Goff labeled it “a compelling transaction…creating a premier growth platform”, while CEO David Rockecharlie highlighted SilverBow’s “complementary and high-quality” Eagle Ford position enhancing Crescent’s “unique value proposition.”

The merger exemplifies the accelerating consolidation across the U.S. shale patch as producers pursue scale, streamlining, and consistent shareholder returns. Crescent emerges exceptionally well-positioned to lead this rationalization as a serial acquirer given its sector-leading free cash flow generation, returns philosophy, and strong balance sheet.

Want small cap opportunities delivered straight to your inbox? Channelchek’s free newsletter will give you exclusive access to our expert research, news, and insights to help you make informed investment decisions.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production results were below expectations as extremely cold weather affected wells. InPlay was actively drilling in the first quarter. Several wells were completed at the end of the quarter and should help out next quarter’s production. The resumption of drilling in a prolific region this fall should lead to higher production in 2025.

Pricing remains an issue as the discount to WTI oil prices remains large, but the discount shows signs of improving. The discount between realized prices and WTI oil prices (as expressed in Canadian dollars) remains wide. New oil and gas pipelines in western Canada should lower the discount. Oil and gas futures already indicate as much.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.