Image: CNBC Squawk Box

Inflation Will Give Way to Deflation But it Will Take Some Time Says Cathie Wood

Cathie Wood thinks we’re in a recession and said she admittedly underestimated the severity of inflation. The hedge fund manager, known for her optimism and bullishness on innovative and disruptive technologies, spoke on CNBC’s Squawk Box this morning (June 28) and backed off her usual balls-to-the-walls approach to investing in tomorrow’s technology. In fact, it was shocking to see her usual style of pushing through adversity and unrelenting advice that “truth will win out,” succumb to relent.

Instead, The Founder, CEO, and CIO of ARK Invest, which has seen portfolios under management shrink this year by as much as 66%, backed off. She even outdid the current mainstream pessimism saying the U.S. is already in an economic downturn. And while she had recently pinpointed deflation as the greatest risk to economic growth, she told the CNBC host she underestimated the severity and persistence of inflationary pressures.

“We think we are in a recession,” Wood said. “We think a big problem out there is inventories… the increase of which I’ve never seen this large in my career. I’ve been around for 45 years,” were some of the comments from the Wall Street veteran who will be 67 in November. Wood blamed the hot and dogged inflation on supply problems and the geopolitical crisis. “We were wrong on one thing, and that was inflation being as sustained as it has been,” Wood said. “Supply chain … Can’t believe it’s taking more than two years and Russia’s invasion of Ukraine, of course, we couldn’t have seen that. Inflation has been a bigger problem, but it has set us up for deflation.”

Wood said consumers are feeling the rapid price increases. She pointed to the University of Michigan’s Survey of Consumers, which showed a reading of 50 in June, the lowest level ever.

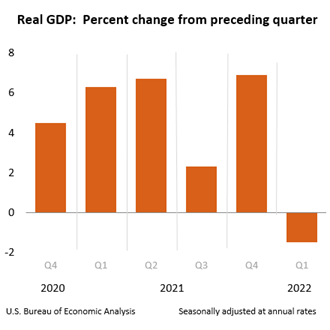

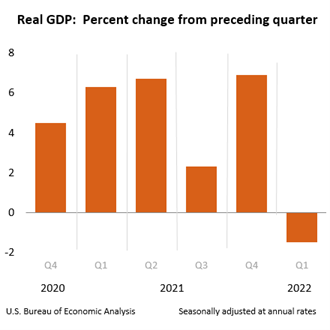

The traditional definition of a recession is two consecutive quarters of negative GDP. The U.S. experienced a negative quarter during Q1, so a second-quarter would officially define the current period as “in a recession.”

Gross Domestic Product, 2nd Quarter 2022 (Advance Estimate) will be released on July 28 at 8:30 AM. This first look at second-quarter growth will be the morning after the end of the two-day FOMC meeting and the accompanying announcement on monetary policy.

Cathie Wood, who is widely followed, especially by technology investors, remarked that her clients are mostly sticking with her, and money flow is positive into her funds. She attributes some of it to investors seeking diversification in a down market. ARKK had more than $180 million in inflows in June. “We are dedicated completely to disruptive innovation. “Innovation solves problems,” Wood said. “I think the inflows are happening because our clients have been diversifying away from broad-based benchmarks like the Nasdaq 100.”

Cathie Wood was early to put bitcoin in her funds and held high-flying names like Tesla and Zoom before they were on the radar of others. Lately, she has been accused of being out of touch. Most of her funds are well defined, leaving the discretion for the CIO to names, not broader sectors. The ARK Invest CIO may have found her hands tied by prospectuses and may continue to be challenged with this. But her economic calls are all her own, and she has backed way off what up to this point could have been seen as cheerleading economic releases and keeping her fingers crossed.

Managing Editor, Channelchek

Suggested Content

Michael Burry Uses Burgernomic’s logic to Evaluate the U.S. Dollar

|

Why Michael Burry has Better Opportunity Than Cathie Wood

|

SEC Pokes Fun at Investors, Draws Controversy

|

Will Consumers Finally Adjust Spending Down?

|

Sources

https://www.cnbc.com/2022/06/28/ark-invests-cathie-wood-says-the-us-is-already-in-a-recession.html

https://www.bea.gov/news/schedule

https://www.marketwatch.com/story/cathie-wood-warns-u-s-is-already-in-a-recession-11656424710

https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

Stay up to date. Follow us:

|

{kind=link}